Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

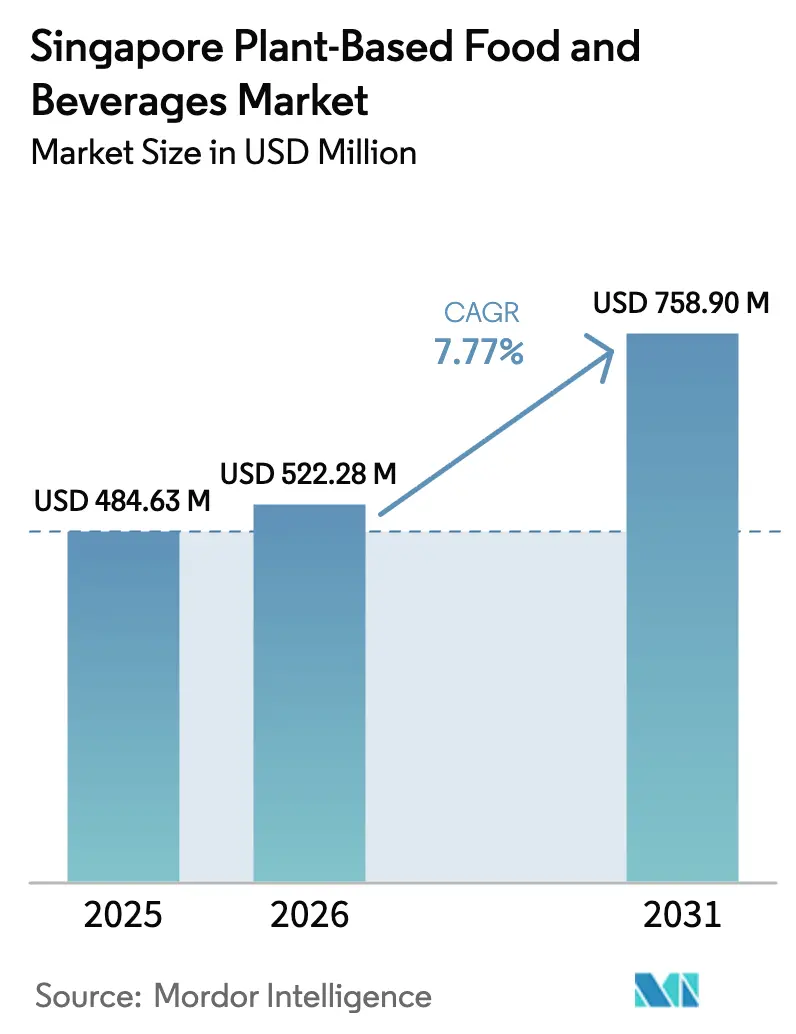

| Base Year Market Size (2025) | USD 484.63 Million |

| Market Size (2026) | USD 522.28 Million |

| Market Size (2031) | USD 758.9 Million |

| Growth Rate (2026 - 2031) | 7.77% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Plant-Based Food And Beverages Market Analysis by Mordor Intelligence

The Singapore plant-based foods market size is expected to grow from USD 484.63 million in 2025 to USD 522.28 million in 2026 and is forecast to reach USD 758.9 million by 2031 at 7.77% CAGR over 2026-2031. Strong institutional and consumer momentum fuel the current market size of alternative proteins. Singapore's "30 by 30" food security initiative, which aims to produce 30% of the country's nutritional needs locally by 2030, ongoing government research and development grants, and a regulatory framework hastening novel food approvals bolster this robust demand. Breakthroughs in precision fermentation, including advancements in microbial engineering and scalable production methods, a growing flexitarian trend among affluent consumers seeking sustainable and health-conscious options, and an expanded presence on supermarket shelves, enhance market penetration. Meanwhile, online retail platforms boost product accessibility and discovery by offering a wider range of alternative protein products and facilitating consumer education. Both multinational and local innovators focus on refining taste and reducing costs through technological advancements and economies of scale, and consistent capital inflows underscore Singapore's emerging status as Asia's precision-fermentation nucleus, attracting global attention and investment.

Key Report Takeaways

- By product category, dairy-alternative beverages led with a 41.42% revenue share in 2025, while meat substitutes are forecast to register an 10.82% CAGR to 2031.

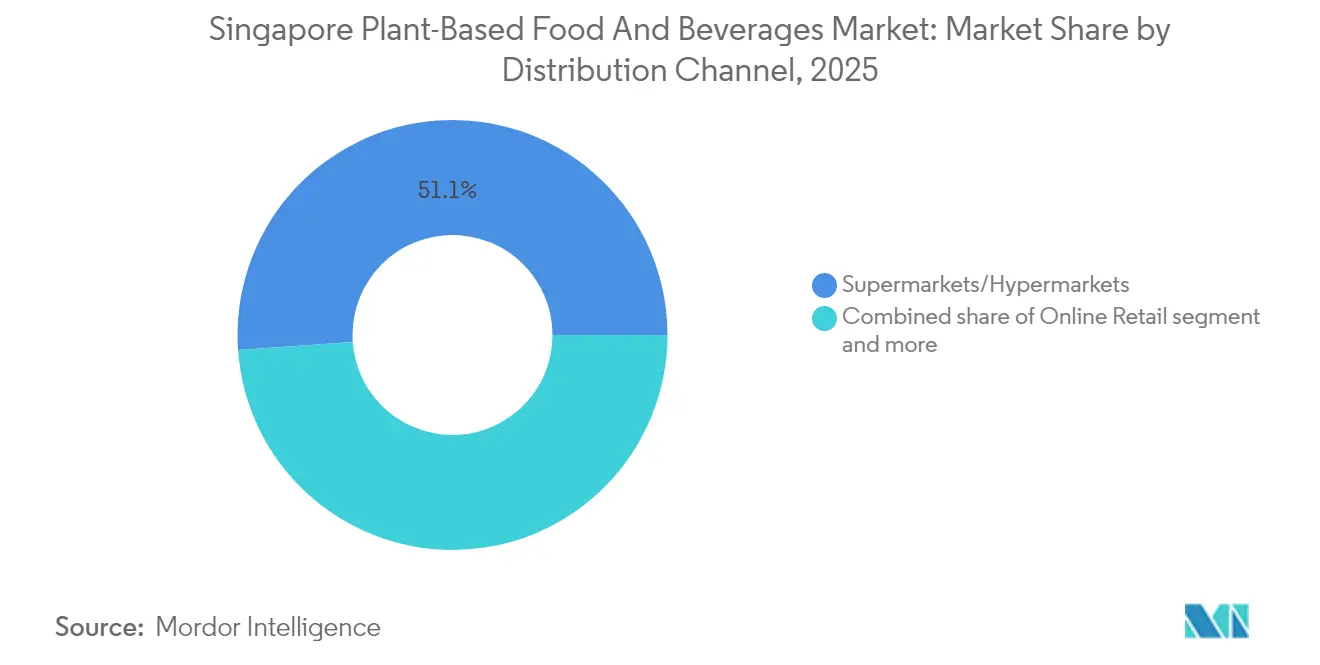

- By distribution channel, supermarkets and hypermarkets held 51.12% of the 2025 Singapore plant-based foods market share, whereas online retail is projected to expand at a 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Plant-Based Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising flexitarian and health-conscious consumer base | +1.8% | Singapore, with spillover to regional markets | Medium term (2-4 years) |

| Government "30 by 30" food-security push for alt-proteins | +2.1% | National, with early gains in precision fermentation hubs | Long term (≥ 4 years) |

| Supermarket and quick-commerce shelf expansion | +1.2% | Singapore urban centers, expanding to suburban areas | Short term (≤ 2 years) |

| Precision-fermentation research and development incentives attracting alt-dairy start-ups | +1.5% | Singapore innovation districts, Biopolis ecosystem | Long term (≥ 4 years) |

| Zero-waste valorisation of okara and spent grains into new SKUs | +0.9% | Singapore manufacturing zones, regional expansion potential | Medium term (2-4 years) |

| Canada–Singapore Asia-Pacific Market Entry Program unlocking import pipeline | +0.7% | Singapore import channels, ASEAN market access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising flexitarian and health-conscious consumer base

In Singapore, a demographic shift towards flexitarian diets is propelling the adoption of plant-based foods, moving beyond the confines of traditional vegetarianism. Surveys conducted among the city's diverse Asian populace reveal a pronounced preference for plant-based proteins, sidelining cultivated meat alternatives. With retail food sales surpassing USD 11 billion in 2023, Singapore's affluent consumers are primed for premium plant-based products, especially those touting health and sustainability benefits. Given that 90% of the Asian population is lactose-intolerant, there's a burgeoning demand for dairy alternatives, driven by heightened health consciousness. Studies on consumer acceptance highlight the pivotal role of halal considerations for Muslim Singaporeans in their reception of alternative proteins, underscoring the influence of family and social media figures on their consumption choices. Furthermore, Singapore's rising status as a vegan gastronomy hotspot is evident, with online chatter celebrating plant-based twists on local favorites like Singapore Noodles, marking a blend of health-driven choices and culinary creativity.

Government "30 by 30" food-security push for alt-proteins

Singapore's "30 by 30" initiative, backed by the Agri-food Cluster Transformation (ACT) Fund, is steering the nation towards enhanced food security via alternative protein development. The ACT Fund, which offers co-funding to local farms for capability upgrades and technological advancements, is set to continue its support until December 31, 2025[1]Source: Singapore Food Agency, "Agri-food Cluster Transformation (ACT) Fund", sfa.gov.sg. The government's USD 165 million Singapore Food Story 2.0 program focuses on alternative protein research and development, notably funding precision fermentation research, highlighted by the USD 14.8 million PreFerS project at the University of Illinois Urbana-Champaign. Regulatory frameworks are expediting novel food approvals, with the SFA's Novel Food Safety Expert Working Group trimming evaluation timelines to 9-12 months while upholding safety standards. The initiative also champions import diversification. The Farm-to-Table Recognition Programme incentivizes the HoReCa sector to embrace local and alternative protein sources[2]Source: Singapore Food Agency, "Farm-to-Table Recognition Programme (FTTRP)", .sfa.gov.sg. Singapore's move as the first nation to greenlight cultivated meat sets a regulatory benchmark and draws global investments. Esco Aster plans to inaugurate an 80,000 sq ft cultivated meat facility in Changi by 2025, aiming for an annual output of 400-500 tonnes.

Supermarket and quick-commerce shelf expansion

Major retailers are committing to plant-based expansion, dedicating shelf space and developing private labels. FairPrice Group rolls out over 100 new products each year, pricing its plant-based options 10-15% lower than international counterparts. Singapore's largest FairPrice Xtra hypermarket, now open in VivoCity, spans 90,000 sq ft with over 35,000 products, including 350 local brands. It features an in-house hydroponic farm aimed at educating consumers on sustainable food production. Quick-commerce is rising, highlighted by RedMart's debut physical storefront at Raffles Place MRT station. This outlet showcases smart vending machines, operable via the Lazada app, offering curated daily essentials, including plant-based items. DFI Retail Group's strategic moves in 2024 boosted profitability for its Giant and Cold Storage operations. By focusing on house brands and enhancing omnichannel shopping, the group made it easier for consumers to discover plant-based products. Private label penetration is nearing the global benchmark of 30%. FairPrice's house-brand range generated nearly USD 1 billion in 2024, underscoring a significant commitment to affordable plant-based alternatives.

Precision-fermentation research and development incentives attracting alt-dairy start-ups

Singapore's precision fermentation ecosystem, bolstered by targeted research and development incentives and top-tier infrastructure, is drawing considerable investment. Nurasa's launch of Asia's first Food Tech Innovation Centre (FTIC) in Biopolis, equipped with cutting-edge laboratories for precision fermentation and food processing, exemplifies this growth. TurtleTree, having secured FDA GRAS status for its precision-fermented lactoferrin LF+, underscores the commercial potential of Singapore's precision fermentation scene. The company, buoyed by USD 80 million in Series A funding, anticipates notable cost reductions by 2029. Automated research and development facilities, such as Tate & Lyle's ALFIE laboratory, are amplifying Singapore's prowess in ingredient development. Leveraging robotics, ALFIE accelerates product development tenfold and enhances predictive modeling for healthier food choices. The Novel Food Regulatory Framework, backed by the SFA's science-driven approach, streamlines market entry for innovative ingredients. This burgeoning sector is fostering international collaborations, highlighted by Temasek Holdings and Japan's Norinchukin Bank spearheading a USD 173 million fund aimed at agritech and food tech startups throughout the Asia Pacific.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus animal products | -1.4% | Singapore retail channels, price-sensitive consumer segments | Short term (≤ 2 years) |

| Taste/texture fidelity gaps | -0.8% | Singapore food service sector, consumer acceptance barriers | Medium term (2-4 years) |

| Saturation risk in small domestic consumer base | -0.6% | Singapore domestic market, limited population expansion potential | Long term (≥ 4 years) |

| Labelling and regulatory fragmentation for novel vs plant-based foods | -0.4% | Singapore regulatory compliance, cross-border trade implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium pricing versus animal products

Despite improvements in economies of scale, plant-based categories still face cost disadvantages. For instance, TurtleTree's precision fermentation ingredient, lactoferrin, is priced at a premium compared to conventional counterparts. However, TurtleTree anticipates scaling production and reducing costs by 2029. Local producers in Singapore face pricing challenges due to high operational costs, notably in energy and labor. Several high-tech farms, despite hefty investments in advanced production technologies, struggle to break even. Retail dynamics reveal consumer price sensitivity. FairPrice's tactic of pricing house-brand plant-based products 10-15% below international brands underscores demand for affordable options. This premium pricing challenge is pronounced in the food service sector, where restaurants need cost-competitive ingredients to protect profit margins. Yet, certain consumer segments are open to paying premiums for health and sustainability perks. With Singapore's high disposable income levels, market segmentation strategies balance premium positioning with accessible pricing tiers.

Taste/texture fidelity gaps

Despite technological strides, sensory experience limitations hinder mainstream adoption. Companies like ImpacFat are crafting cultivated fish fats to elevate the flavor profile of lab-grown meats. In Singapore, startups are tackling texture challenges. Jiro-Meat, for instance, is pioneering okara-based meat alternatives, harnessing fermented soybean waste to boost nutrition and mouthfeel. Research institutions are also playing a pivotal role. Nanyang Technological University has devised a method to extract over 80% protein from brewers' spent grain, yielding high-quality protein ingredients for plant-based foods. Specialized research and development facilities like Tate & Lyle's ALFIE laboratory in Singapore focus on mouthfeel solutions, employing robotics and predictive modeling to fast-track ingredient development. Studies on consumer acceptance reveal significant variation in taste preferences among Singapore's diverse ethnic groups, underscoring the need for localized flavor development that integrates familiar Asian taste profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Substitutes Drive Innovation

In 2025, dairy-alternative beverages claimed a dominant 41.42% share of Singapore's plant-based foods market revenue. This surge in demand is driven by high levels of lactose intolerance and a trend towards premiumization. Highlighting the potential of Asian flavor innovation, local brand OATSIDE stands out as a testament to scalability. The segment is making strides with precision-fermented functional proteins, and is set to debut its first ready-to-drink coffee infused with animal-free lactoferrin by mid-2025. This innovation is expected to cater to health-conscious consumers seeking functional benefits in their beverages. Concurrently, the introduction of instant oat-milk mixes is broadening consumption opportunities by offering convenient and versatile options for consumers. Consequently, the dairy-alternative segment solidifies its role as a key volume driver, supported by its ability to meet diverse consumer preferences and dietary needs.

Meat substitutes are on track to achieve the fastest growth in Singapore's plant-based foods market, with a projected CAGR of 10.82%. Formats derived from okara, now approaching commercialization, promise both sustainability and a rich protein profile, addressing the growing demand for environmentally friendly and nutritious food options. The recent regulatory nod for 16 insect species expands the ingredient palette, enabling manufacturers to explore innovative formulations and diversify product offerings. Meanwhile, ventures in cultivated seafood are swiftly moving towards pilot-scale production, signaling a significant step forward in alternative protein development. Moreover, the use of localized spice blends and texturizers in crafting satay and rendang analogs underscores significant strides in achieving culinary authenticity, ensuring these products resonate with local tastes and cultural preferences.

By Distribution Channel: Online Retail Transforms Access

In 2025, physical supermarkets, spearheaded by FairPrice, clinched 51.12% of sales, buoyed by store renovations and an expansion of private labels. With in-aisle signage and health-star labeling, shopper navigation becomes a breeze, helping consumers make informed choices quickly. Moreover, in-store hydroponic farms bolster the sustainability narrative by showcasing innovative farming practices that reduce environmental impact. Traditional chains are also leveraging dark-store fulfillment, enabling two-hour deliveries and blurring the lines with e-commerce, thereby enhancing convenience for time-sensitive shoppers.

Online retail is set to expand at an annual rate of 13.92%, driven by widespread smartphone adoption and the rise of quick-commerce pilots. RedMart's introduction of MRT vending caters to office workers, providing seamless top-up solutions and addressing the need for on-the-go convenience. Meanwhile, direct-to-consumer platforms harness first-party data, facilitating swift product iterations that align with evolving consumer preferences. Subscription bundles, featuring barista oat milk and protein-rich snacks, are on the rise, underscoring the channel's significance in education and fostering loyalty by offering tailored solutions to niche consumer demands.

Geography Analysis

Singapore's 728 sq km geography enables efficient nationwide distribution. While urban core districts lead in supermarket traffic, suburban areas are rapidly gaining ground, driven by the rise of quick-commerce. Affluent locales like Bukit Timah and Downtown Core, recognized for their high per-capita spending on specialty foods, stand out as the city's consumption hotspots. These areas not only attract premium grocery retailers but also serve as testing grounds for new specialty food products. With passenger numbers at Changi Airport rebounding in 2024, transit eateries are revamping their menus, capitalizing on the surge of tourists. This influx has also encouraged the introduction of diverse international cuisines and innovative dining concepts to cater to the varied preferences of travelers.

Singapore's strategic location, enhanced by free-trade agreements and bilingual labeling, positions it as a premier launchpad for exports to Malaysia, Indonesia, and Thailand. Numerous multinationals have established their Asia-Pacific headquarters in Singapore, taking advantage of the city's efficient re-export procedures at Jurong Port for broader regional rollouts. The country's robust infrastructure and business-friendly policies further solidify its role as a key hub for regional trade and distribution.

Even with its strategic benefits, Singapore is heavily import-dependent, sourcing over 90% of its raw ingredients from overseas. To mitigate this reliance, the government employs strategic stockpiling and diversified sourcing, recently clinching deals for pulses and canola from Canada. These agreements are part of a broader effort to ensure food security and reduce vulnerability to supply chain disruptions. The city's logistics capabilities shine through its cold-chain resilience, a fact underscored during the 2024 disruptions in the Red Sea. This resilience has been critical in maintaining the quality and safety of perishable goods, reinforcing Singapore's reputation as a reliable logistics hub.

Competitive Landscape

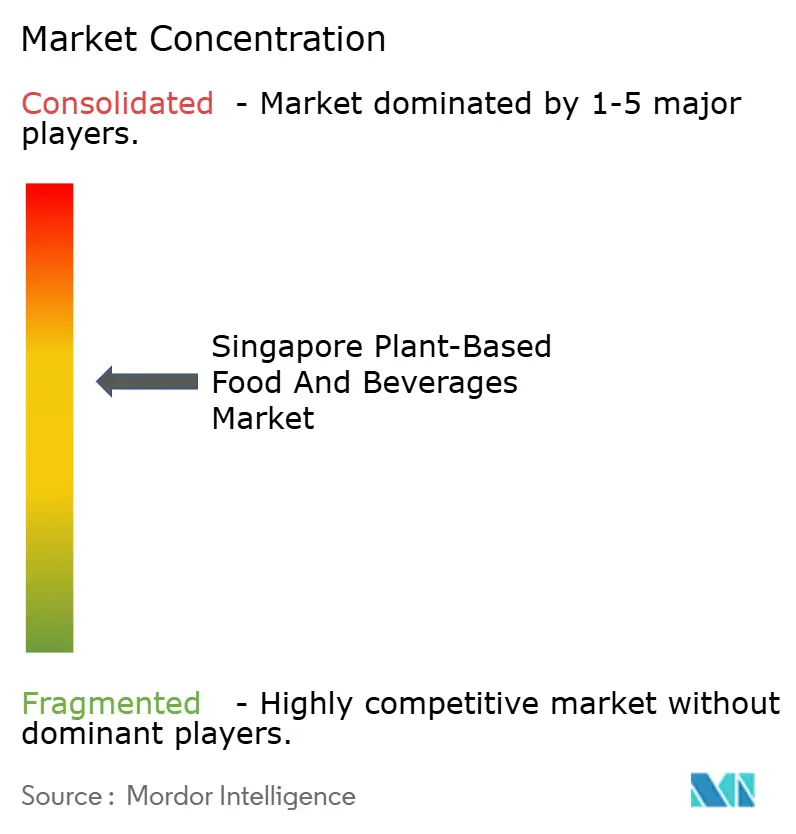

The plant-based food and beverages market in Singapore is moderately concentrated. TurtleTree's pioneering move in precision-fermented bioactives underscores the commercial potential of IP-centric models, showcasing how intellectual property can drive innovation and profitability. FairPrice, wielding its retailer clout, secures advantageous slotting fees, ensuring prime shelf space for its products, and simultaneously cultivates its proprietary SKUs to strengthen its market position. OATSIDE's swift ascent in 18 markets highlights Singapore's ability to combine innovation with consumer-driven flavor leadership, further solidifying its reputation as a hub for food technology.

Strategic alliances set players apart: Danone tailors its Alpro line extensions to resonate with Southeast Asian palates, leveraging regional insights to enhance product appeal and market penetration. Meanwhile, Esco Aster collaborates with local universities to refine crustacean cell lines, aiming to advance the development of sustainable seafood alternatives. The merger of Shiok Meats and Umami Bioworks, pooling their research and development efforts to amplify cultivated seafood production, signals a surge in merger and acquisition activity, reflecting the industry's focus on scaling innovation through consolidation.

Investment flows freely; Temasek-backed funds range from USD 5 million seed investments to USD 50 million growth capital, providing critical financial support for emerging and scaling companies. Companies championing zero-waste methods are drawing significant interest from ESG-focused family offices, emphasizing the growing importance of sustainability in investment decisions. Facilities like FTIC, with their subsidized fermentation suites, are accelerating commercialization by reducing barriers to entry for start-ups and fostering innovation. In essence, the trifecta of technological innovation, regulatory acumen, and localized flavor expertise defines the competitive landscape, shaping the future of the market.

Singapore Plant-Based Food And Beverages Industry Leaders

-

Impossible Foods

-

Beyond Meat Inc.

-

Vitasoy International

-

Danone SA

-

OATSIDE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ajinomoto unveiled its new Solein-based, dairy-free coffee in Singapore. Dubbed Atlr.72 GRe:en Drop Coffee, this innovative product is a dairy-free iced latte, harmoniously blending traditional coffee with a 'beanless' variant crafted from rice and chickpeas.

- April 2024: Singapore's Yeo Hiap Seng introduced Yeo’s Immuno Soy Milk. This fortified drink, enriched with vitamin B6 and zinc, aims to enhance immunity. Endorsed as a 'Healthier Choice' in both Singapore and Malaysia, this lactose-free, protein-packed beverage is available in original and chocolate flavors. Its smoother taste marks a significant milestone, being the brand's most substantial soy milk innovation in seven decades.

- April 2024: Vow has introduced "Quailia" (Forged Parfait), its inaugural cultivated-meat product made from Japanese quail. This move positions Vow as the third global player, following Upside Foods and GOOD Meat, to commercialize cultured meat, and interestingly, it's not the conventional chicken nuggets.

- August 2023: Agrocorp International (Agrocorp) has launched HerbY-Cheese, Singapore’s first plant-based, nut-free cheese range, sold under its consumer brand, HerbYvore.

Singapore Plant-Based Food And Beverages Market Report Scope

Plant-based food and beverage refer to dairy alternatives and meat substitutes manufactured with plant-based ingredients sourced from legumes, nuts, leaves, and seeds, among others. The Singapore plant-based food and beverages market is segmented by product type and distribution channel. By product type, the market is segmented into meat substitutes, dairy alternative beverages, non-dairy ice cream, non-dairy cheese, non-dairy yogurt, non-dairy spreads, and other plant-based products that include non-dairy chocolates, milk powders, etc. By meat substitutes, the market is further segmented into textured vegetable protein, tofu, tempeh, and other meat substitutes. By dairy alternative beverages, the market is further segmented into soy milk, almond milk, and other dairy alternative beverages. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

By Product Type

| Meat Substitutes | Textured Vegetable Protein (TVP) |

| Tofu | |

| Tempeh | |

| Seitan | |

| Plant-based Seafood | |

| Plant-based Eggs | |

| Other Meat Substitutes | |

| Dairy-Alternative Beverages | Soy Milk |

| Almond Milk | |

| Oat Milk | |

| Other Plant Milks | |

| Non-dairy Cheese | |

| Non-dairy Yogurt | |

| Non-dairy Ice-cream | |

| Non-dairy Spreads | |

| Other Plant-based Products |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Online Retail |

| Food-service (HoReCa) |

| Other Channels |

| By Product Type | Meat Substitutes | Textured Vegetable Protein (TVP) |

| Tofu | ||

| Tempeh | ||

| Seitan | ||

| Plant-based Seafood | ||

| Plant-based Eggs | ||

| Other Meat Substitutes | ||

| Dairy-Alternative Beverages | Soy Milk | |

| Almond Milk | ||

| Oat Milk | ||

| Other Plant Milks | ||

| Non-dairy Cheese | ||

| Non-dairy Yogurt | ||

| Non-dairy Ice-cream | ||

| Non-dairy Spreads | ||

| Other Plant-based Products | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Food-service (HoReCa) | ||

| Other Channels | ||

Key Questions Answered in the Report

How large is the Singapore plant-based foods market in 2026?

The market stands at USD 522.28 million in 2026 and is forecast to reach USD 758.9 million by 2031.

What is the expected CAGR for Singapore’s plant-based category?

TheSingapore plant-based foods market is projected to grow at an 7.77% CAGR between 2026 and 2031.

Which product segment leads sales today?

Dairy-alternative beverages hold the largest share at 41.42% of 2025 revenue.

How does government policy affect growth?

The “30 by 30” initiative finances R&D and accelerates novel-food approvals, adding about 2.1 percentage points to the forecast CAGR.

Page last updated on: