Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.95 Billion |

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 2.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Motor Insurance Market Analysis by Mordor Intelligence

The Singapore Motor Insurance Market size in terms of premium value is expected to grow from USD 0.95 billion in 2025 to USD 0.97 billion in 2026 and is forecast to reach USD 1.07 billion by 2031 at 2.07% CAGR over 2026-2031.

Despite a plateau in vehicle population, Singapore's motor insurance market is on the rise. Insurers are harnessing digital tools, telematics, and specialized coverage for electric vehicles (EVs) to boost average premiums. Key factors shaping product design and pricing strategies include mandatory third-party liability requirements, the swift adoption of electric vehicles, and backing from the Monetary Authority of Singapore (MAS) for Insurtech pilots. Additionally, a surge in commercial fleets, especially in ride-hailing and last-mile delivery, is amplifying premium volumes. Digital innovations, like Singpass-enabled e-KYC and online aggregators, are not only slashing distribution costs but also heightening price competition. In this dynamic landscape, established insurers are fortifying their market positions by rolling out enhanced coverage add-ons, facilitating instant claims settlements, and forging partnerships to tackle the rising repair costs linked to advanced driver-assistance systems.

Key Report Takeaways

- By policy type, comprehensive cover led with 71.85% of Singapore motor insurance market share in 2025; usage-based/pay-as-you-drive products are set to grow at a 12.12% CAGR through 2031.

- By vehicle type, private passenger cars held 80.78% of the Singapore motor insurance market size in 2025, while motorcycles and scooters are projected to advance at 13.02% CAGR between 2026-2031.

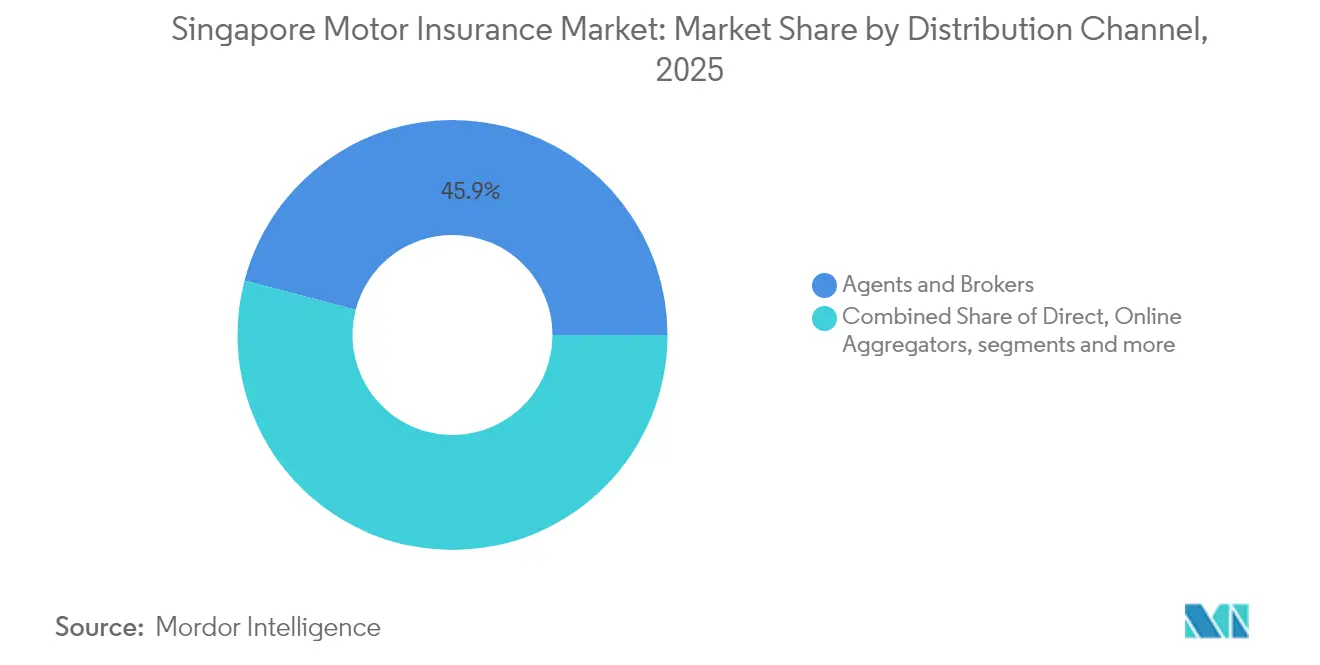

- By distribution channel, agents and brokers commanded 45.92% revenue share in 2025; online price aggregators are forecast to post the fastest 15.08% CAGR to 2031.

- By end-user, personal lines accounted for 77.63% of the Singapore motor insurance market size in 2025; commercial lines are expanding at 8.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory third-party insurance compliance | +0.5% | Singapore nationwide | Short term (≤ 2 years) |

| EV adoption and specialised covers | +0.4% | Nationwide urban focus | Medium term (2-4 years) |

| Telematics and usage-based models | +0.6% | Singapore nationwide | Medium term (2-4 years) |

| Ride-hailing and delivery fleet growth | +0.4% | Urban centers | Short term (≤ 2 years) |

| Digital aggregators in direct-to-consumer | +0.3% | Singapore nationwide | Short term (≤ 2 years) |

| Singpass-enabled e-KYC | +0.3% | Singapore nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Third-Party Motor Insurance Compliance Under Singapore Law

In Singapore, the Motor Vehicles (Third-Party Risks and Compensation) Act mandates motor insurance, significantly shaping the nation's motor insurance landscape. Legally, every motor vehicle must possess third-party liability coverage. Those who flout this rule face fines or imprisonment, leading to almost universal policy adoption and a consistent premium volume. The Motor Insurers’ Bureau bolsters market integrity by compensating victims in incidents with uninsured drivers. Regulatory moves, like mandating accident reports to insurers, aim to curb fraud and speed up claims. The General Insurance Association notes that stringent enforcement has kept motor insurance penetration near 100%[1]General Insurance Association of Singapore, “Motor Insurance Consumer Guide,” gia.org.sg. This high penetration grants insurers a predictable market, enabling them to pivot from merely acquiring customers to innovating in product development and refining risk analytics.

EV Adoption Driving Specialized Policies and Coverage Extensions

In Singapore, the surge in electric vehicle (EV) adoption is spurring the evolution of specialized motor insurance policies. While EVs constituted a mere 3.3% of the national car parc in 2024, they dominated new vehicle registrations at 32.5%. This spike is largely attributed to government incentives reaching up to SGD 40,000[2]Liberty Insurance, “Coverage and Premiums in Singapore EV Insurance,” libertyinsurance.com.sg. Insurers are now crafting products that cater to unique EV risks, including battery degradation, potential damage to charging equipment, and cyber threats. Reflecting the elevated repair costs and the scarcity of spare parts, these tailored policies come with a 15–20% premium over traditional motor insurance. A standout in this arena is Income Insurance’s eDrivo plan, boasting features like 24/7 mobile charging support and optional battery replacement coverage[3]Income Insurance, “eDrivo Car Insurance,” income.com.sg. With EV prices on a downward trend and the public charging infrastructure broadening, the premium pool for EV insurance is poised for double-digit growth, underscoring its significance as a strategic growth avenue for insurers.

Telematics & Usage-Based Insurance Backed by MAS Sandboxes

In Singapore, the motor insurance market is increasingly being shaped by telematics and usage-based insurance (UBI), with backing from the Monetary Authority of Singapore’s (MAS) regulatory sandbox framework. This initiative permits insurers to experiment with innovative models, such as pay-per-kilometre and behaviour-based pricing, while benefiting from reduced capital requirements. A notable instance is Carro’s “Covered” plan, underwritten by NTUC Income. This plan utilizes onboard diagnostics and AI-driven scoring to dynamically adjust premiums based on driving behaviour. As a result, safe drivers are reaping discounts of up to 30%. This shift indicates a move in underwriting practices, prioritizing behaviour-based metrics over traditional demographic factors. Industry experts project that by 2030, usage-based insurance could represent 15% of all motor policies, enhancing insurers' loss ratios and deepening customer engagement.

Ride-Hailing and Last-Mile Delivery Fleet Expansion Raising Policy Demand

The rise of ride-hailing services and Singapore's last-mile delivery fleets is fueling a surge in demand for motor insurance policies tailored to commercial needs. Companies like Grab and foodpanda are turning to hybrid insurance solutions that cater to both personal and commercial usage. Consequently, commercial motor premiums are witnessing a robust CAGR of 9.20%. Fleet operators are now on the lookout for features such as adjustable deductibles, roadside assistance, and tools to monitor driver performance. Insurers are harnessing the power of telematics, tracking metrics like vehicle mileage, passenger loads, and route data. This not only paves the way for usage-based pricing but also helps in curbing fraud. With Singapore's dense urban landscape, these fleets are integral to the nation's transportation framework, driving consistent growth in the motor insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price wars on aggregators | -0.4% | Singapore nationwide | Medium term (2-4 years) |

| Vehicle-population plateau | -0.3% | Singapore nationwide | Long term (≥ 4 years) |

| MAS risk-based capital rules | -0.2% | Singapore nationwide | Medium term (2-4 years) |

| Claims inflation from ADAS and EV parts | -0.3% | Singapore nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Wars and Discounting on Aggregators Compress Underwriting Margins

Digital insurers are rapidly capturing market share with ultra-low prices, sparking a race-to-the-bottom that tightens margins across the board. In response, some carriers are turning to strategies like offering higher excesses or unbundled add-ons. However, these approaches come with the risk of creating coverage gaps, potentially eroding customer trust. Ongoing discounting pressures the solvency buffers of smaller players, underscoring the critical need for robust capital strength in line with risk-based regulations. The low prices and margins hinders the growth of Singapore motor insurance market.

Vehicle Population Plateau Limits New Policy Volume

In Singapore, the motor insurance market grapples with a structural constraint on new policy volumes, primarily due to the Certificate of Entitlement (COE) system. This system curbs the growth of the vehicle population to nearly zero, a measure aimed at controlling road congestion. Consequently, insurers pivot their strategies towards customer retention, upselling enhanced coverage, and implementing premium increases to bolster revenue, sidelining the expansion of policy numbers. While shifts in COE prices can sway consumer decisions, prompting those with heftier premiums to lean towards more comprehensive coverage, the enduring cap on vehicle numbers remains a significant hurdle for top-line growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Policy Type: Usage-Based Models Disrupt Traditional Coverage

Comprehensive cover dominated with a 71.85% share in 2025 because high car values and dense traffic elevate perceived loss severity. The Singapore motor insurance market size tied to comprehensive policies is projected to edge up at 1.79% CAGR, underpinned by COE-driven vehicle valuations. Third-party fire-and-theft plus third-party only policies serve older or budget vehicles but face cannibalization when drivers shift to flexible usage-based plans.

Adoption of telematics is reshaping premium mechanics. Usage-based contracts grow 12.12% annually as drivers embrace mileage-linked savings, and MAS sandboxes shorten launch cycles. The Singapore motor insurance market share of usage-based policies would materially dilute fixed-premium dominance, forcing incumbents to refine risk-scoring algorithms and telematics partnerships.

By Vehicle Type: EV Transition Reshapes Risk Profiles

Private cars contributed 80.78% of written premiums in 2025, yielding a stable but low-growth segment because registration caps persist. The Singapore motor insurance market size for private cars is forecast to inch forward at only 1.59% CAGR through 2031. Conversely, motorcycles and scooters record 13.02% CAGR, supported by affordability and delivery-fleet demand, albeit from a lower base.

Electric vehicles inject complexity into underwriting because batteries, power electronics, and aluminium bodywork push repair bills higher. EV policies carry premiums 15-20% costlier than combustion models; however, incentives and charging-network rollout fuel rapid parc growth. By 2030, EVs may comprise a tenth of registered cars, magnifying their impact on loss ratios and giving data-rich insurers an underwriting edge.

By Distribution Channel: Digital Platforms Challenge Traditional Intermediaries

Agents and brokers retained 45.92% of policies in 2025, yet their share is slowly eroding as mobile-first purchasing gains traction. The Singapore motor insurance market size distributed via agents is expected to remain flat, while aggregator-led sales accelerate 15.08% CAGR, widening the direct channel’s revenue base.

Aggregators improve transparency but commoditise offerings. To stay relevant, intermediaries integrate digital advisory, bundle multi-line covers, and highlight claims service track records. Insurers blend omnichannel models: online for acquisition, brokers for high-value renewals and complex fleets, and banking partners for cross-selling moments.

By End-User: Commercial Segment Outpaces Personal Lines Growth

Personal lines commanded 77.63% of premiums in 2025, yet they grow slowly because individual vehicle numbers are capped. Commercial fleet premiums climb 8.98% annually as ride-hailing, logistics, and car-sharing operators scale. Loss-cost volatility is higher in commercial portfolios, pushing insurers to embed telematics, driver training, and dynamic deductibles.

As corporate sustainability targets rise, companies adopt electric vans and two-wheelers, which alter claims patterns and downtime costs. Insurers that master EV parts sourcing and rapid repair networks are likely to win share in the expanding commercial niche.

Geography Analysis

Singapore’s compact geography nullifies regional rating but sharpens focus on driver behavior, vehicle tech, and urban-density factors. Extensive CCTV coverage and smart-traffic systems supply high-quality claims evidence, aiding fraud detection and dispute resolution. Tropical rainfall triggers flash-flood events that insurers price into comprehensive covers, especially for low-lying car parks.

The government's ambition to become a “car-lite” nation shapes long-term demand. Investments in rail and bus capacity aim to cut private-vehicle reliance, yet gig-economy fleets and short-term rentals rise in parallel, diversifying premium sources. MAS supervision mandates strong solvency, prompting ongoing capital optimization, while digital-identity infrastructure underpins frictionless e-KYC, supporting cost-efficient scaling of direct channels.

EV adoption is geographically concentrated around public housing estates with communal chargers and affluent districts with landed property charging points. As the charger map densifies, insurers expect EV claim frequencies to converge with combustion norms, though severity may stay elevated due to battery pricing. Singapore’s strict import rules and scheduled de-registration at 10-year intervals ensure vehicle age remains young, keeping average repair costs high.

Competitive Landscape

Market concentration is moderate. NTUC Income Insurance Co-operative Ltd, Great Eastern General Insurance Ltd, MSIG Insurance (Singapore) Pte. Ltd., AXA Insurance Pte Ltd, and Tokio Marine Insurance Singapore Ltd are the major players in the market, backed by a broad agent network and cooperative ethos. Foreign entrants such as Budget Direct and FWD grow rapidly through low-cost online models, offering premiums 30-40% below traditional tariffs to attract price-sensitive drivers.

Technology is the main battleground. Incumbents deploy AI-driven claims portals that reduce settlement cycles from weeks to days, while challengers market instant policy issuance and pay-per-kilometer billing. Partnerships with EV manufacturers and ride-hailing firms generate exclusive affinity pools. Some carriers file patents in blockchain-enabled parametric covers to automate total-loss payouts.

Capital rules favor scale. MAS risk-based frameworks elevate capital charges for high-growth but thin-margin books, spurring consolidation of interest. Although Allianz’s 2024 bid for Income Insurance lapsed, analysts anticipate further M&A as smaller firms seek balance sheet strength and digital capabilities. Competitive differentiation is trending toward customer experience rather than pure price, especially in a market where repair inflation demands prudent underwriting.

Singapore Motor Insurance Industry Leaders

MSIG INSURANCE (SINGAPORE) PTE. LTD.

TOKIO MARINE LIFE INSURANCE SINGAPORE LTD.

THE GREAT EASTERN LIFE ASSURANCE COMPANY LIMITED

NTUC Income Insurance Co-operative Ltd

AXA Insurance Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gallagher Re said property-and-casualty insurtechs raised USD 1.13 billion in Q1 2025, with AI-focused firms capturing 61.2% of deals.

- January 2025: Liberty Insurance Pte Ltd. disclosed EVs accounted for 3.3% of the car parc in 2024, with EV registrations at 32.5% of additions.

- December 2024: Allianz Insurance Singapore withdrew its proposal to acquire Income Insurance, a move that keeps Singapore’s competitive landscape unchanged by preserving Income’s status as a leading local motor insurer

- September 2024: Income Insurance launched eDrivo Car Insurance, bundling mobile charging and battery replacement options for EV owners.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define Singapore's motor insurance market as the annual written premiums generated by licensed insurers for policies that protect privately and commercially registered motor vehicles, cars, motorcycles, light vans, and taxis, against third-party liability and own-damage risks. Values are stated in constant 2024 U.S. dollars and align with Monetary Authority of Singapore reporting conventions.

Scope exclusion: Policies sold to offshore captives, warranty extensions, and stand-alone personal-accident riders are excluded from our sizing.

Segmentation Overview

- By Policy Type

- Comprehensive Cover

- Third-Party, Fire & Theft

- Third-Party Only

- Usage-Based / Pay-As-You-Drive Policies

- By Vehicle Type

- Private Passenger Cars

- Motorcycles & Scooters

- Commercial & Light Goods Vehicles

- By Distribution Channel

- Agents & Brokers

- Direct (Insurer Website / Branch)

- Online Price Aggregators

- Bancassurance

- Automotive Dealerships

- By End-User

- Personal Lines

- Commercial Lines

Detailed Research Methodology and Data Validation

Primary Research

We spoke with underwriting managers, claims adjusters, and fleet operators across Greater Singapore and Johor commuting corridors. These discussions helped us validate loss-ratio assumptions, average premium per vehicle, and early adoption rates for usage-based products.

Desk Research

Our analysts began with open data from the General Insurance Association, Monetary Authority of Singapore annual statistics, Land Transport Authority vehicle-parc figures, and Ministry of Transport accident reports, which anchor premium volumes, claim trends, and vehicle counts. Trade journals, parliamentary speeches on Certificate of Entitlement quotas, and peer-reviewed papers on EV repair costs provided context on price inflation and risk severity. Paid databases, D&B Hoovers for insurer financials, Dow Jones Factiva for premium filings, and Questel for telematics-related patents, supplied company-level insights that public sources could not. The sources listed illustrate, not exhaust, the wider pool we, at Mordor Intelligence, routinely consult.

Market-Sizing & Forecasting

A top-down reconstruction starts with 2024 gross written premiums, adjusted for forecast changes in vehicle-parc size, average premium, and claim severity. Results are corroborated through selective bottom-up checks, sampled insurer roll-ups and channel audits, which let us fine-tune outlier segments. Key variables in our model include COE quota renewals, EV penetration, average claim cost, accident frequency, and GDP-linked disposable income.

For forecasting, we employ a multivariate regression blended with ARIMA to project premiums through 2030; coefficients are reviewed with interviewees before finalization. Data gaps in smaller sub-segments are linearly interpolated against broader indicators such as vehicle sales and repair-cost indices.

Data Validation & Update Cycle

Before sign-off, two senior reviewers test model outputs against historical GIA ratios and MAS solvency metrics. Any variance above three percentage points triggers re-work. Reports refresh every twelve months, with interim updates issued when regulatory or macro shocks materially shift assumptions.

Why Mordor's Singapore Motor Insurance Baseline Commands Reliability

Published estimates seldom match because firms pick divergent scopes, price bases, and exchange-rate paths. We acknowledge these variations upfront so clients instantly see where numbers diverge and why our disciplined filters matter.

Key gap drivers include whether ancillary fees are counted, the breadth of non-life lines folded into 'motor,' and the exchange rate year chosen. Our study limits the scope to on-shore written premiums, excludes peripheral covers, and converts at the rolling MAS average, choices that keep our 2025 baseline tight and repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.95 B (2025) | Mordor Intelligence | - |

| USD 1.20 B (2024) | Regional Consultancy A | Includes personal-accident add-ons and roadside-assistance fees |

| USD 6.12 B (2024) | Trade Journal B | Bundles all vehicle-related non-life lines and uses fixed 2023 FX rate |

Together, the comparison shows that once peripheral revenue streams and broad P&C lines are stripped away, our figure offers the most transparent, decision-ready baseline for insurers, reinsurers, and regulators alike.

Key Questions Answered in the Report

What is the current value of the Singapore motor insurance market?

The market is worth USD 0.97 billion in 2026 and is projected to reach USD 1.07 billion by 2031.

Why are premiums for electric vehicles higher in Singapore?

EV premiums sit 15-20% above conventional cars because battery packs and specialized components push repair costs higher, and actuarial data remain limited.

How does the Certificate of Entitlement (COE) system affect motor insurance growth?

COE quotas cap vehicle numbers, so insurers rely on policy upgrades and commercial fleets rather than new-vehicle growth to expand premium income.

What role do telematics play in pricing motor insurance?

Telematics devices capture mileage and driving behavior, allowing pay-as-you-drive premiums that reward safe habits with discounts up to 30%.

Page last updated on: