Singapore Last-Mile Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

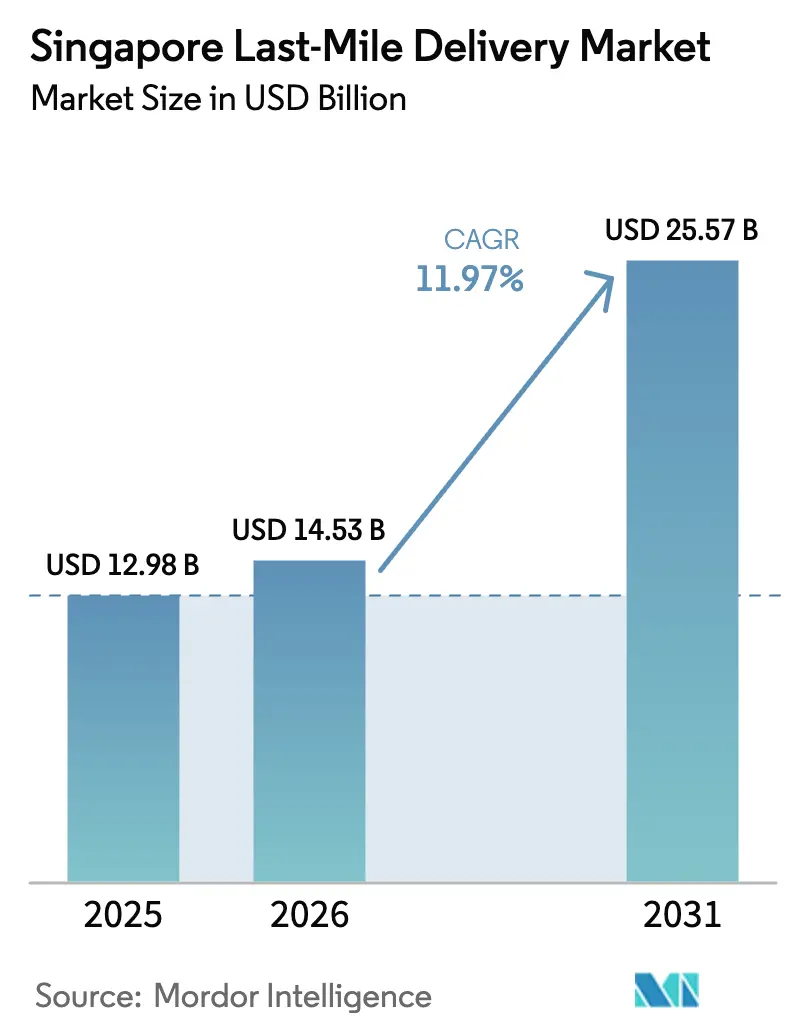

| Base Year Market Size (2025) | USD 12.98 Billion |

| Market Size (2026) | USD 14.53 Billion |

| Market Size (2031) | USD 25.57 Billion |

| Growth Rate (2026 - 2031) | 11.97% CAGR |

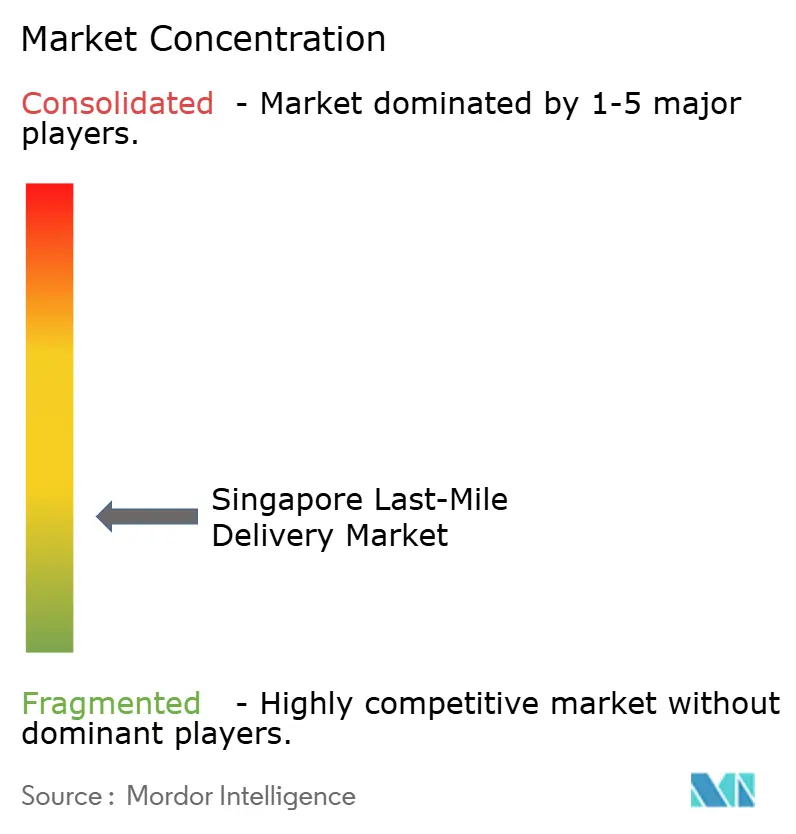

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Last-Mile Delivery Market Analysis by Mordor Intelligence

The Singapore Last-Mile Delivery market size is expected to grow from USD 12.98 billion in 2025 to USD 14.53 billion in 2026 and is forecast to reach USD 25.57 billion by 2031 at 11.97% CAGR over 2026-2031.

Strong e-commerce adoption, dense urban geography, and policy-led infrastructure investments give Singapore an outsized role in regional fulfillment. Standard delivery maintains volume leadership, but rising same-day expectations, healthcare logistics demand, and cross-border micro-shipments reinforce premium service uptake. The federated locker network, Grade-A urban warehousing, and Tuas–Changi dual-hub configuration underpin high asset utilization, while looming fleet-electrification rules reshape capital planning for operators. Intensifying automation offsets labor scarcity, and platform-owned logistics arms blur B2B, B2C, and C2C boundaries within the Singapore last-mile delivery market.

Key Report Takeaways

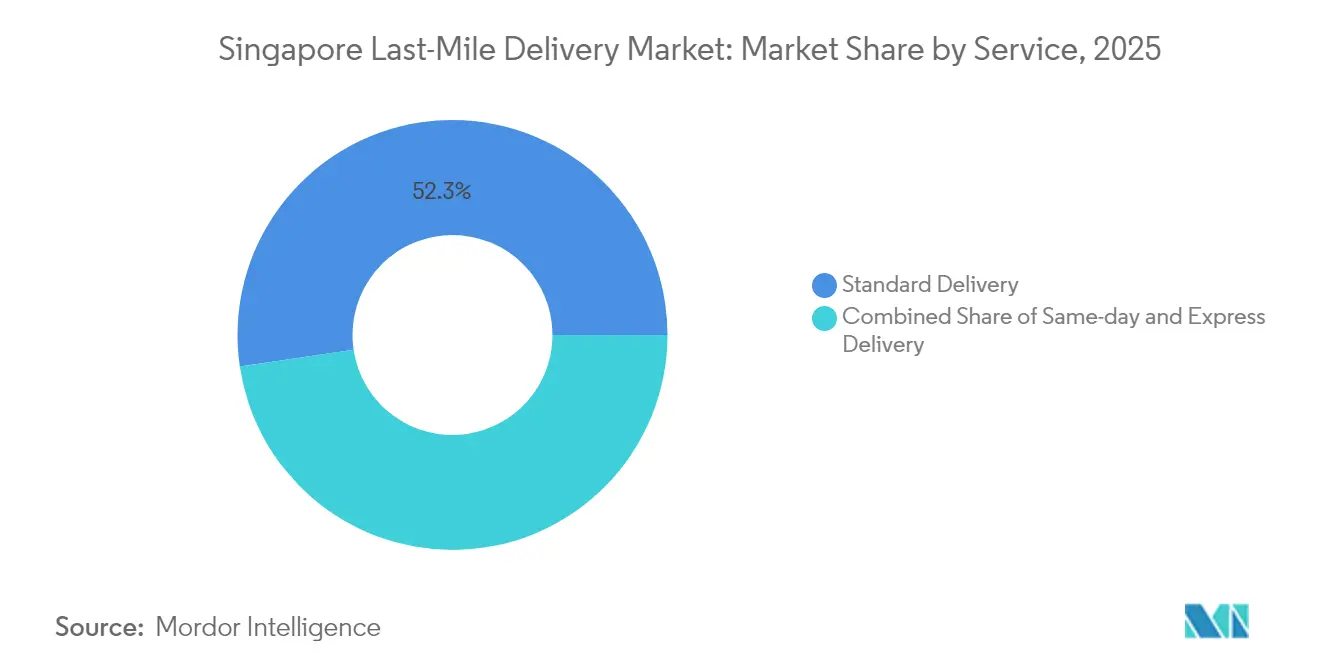

- By service, standard delivery held 52.34% of the Singapore last-mile delivery market share in 2025; express delivery is projected to post a 7.1% CAGR through 2031.

- By business model, B2B commanded a 50.42% share of the Singapore last-mile delivery market size in 2025, while C2C is forecast to advance at an 8.3% CAGR to 2031.

- By end-user, e-commerce retail accounted for 28.65% of the Singapore last-mile delivery market size in 2025; healthcare & medical supplies are rising at a 9.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Last-Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration surge | +2.8% | Nationwide | Medium term (2-4 years) |

| Rising same-day / express demand | +2.1% | Island-wide | Short term (≤ 2 years) |

| Government-backed nationwide locker network | +1.4% | Nationwide | Long term (≥ 4 years) |

| Cross-border micro-shipments via social commerce | +1.9% | Singapore–Malaysia–Thailand corridor | Medium term (2-4 years) |

| Cold-chain B2B restocking opportunities | +1.2% | Core Singapore, Johor, Batam | Long term (≥ 4 years) |

| Availability of Grade-A urban logistics real estate | +0.8% | Western & Eastern clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration Surge Drives Structural Market Expansion

Close to 55% of online purchases in Singapore arrive from overseas merchants, straining last-mile capacity during shopping festivals. Social-commerce discovery channels—TikTok, Instagram, Facebook—now funnel 59% of all cross-border purchases, making micro-shipments the new normal. Shopee’s International Platform multiplied seller orders eightfold during pilots, proving that free cross-border shipping incentives permanently elevate parcel flows. Sustained volume growth pushes carriers to invest in multi-modal customs clearance nodes and advanced small-parcel sortation capable of regional reach beyond the city-state.

Rising Same-Day and Express Demand Reshapes Service Expectations

Same-day options have become baseline as 52% of shoppers now expect sub-24-hour fulfillment across more categories. Express services grow at 7.4% CAGR, fueled by premium electronics, B2B restocking, and temperature-sensitive pharma orders. Aging demographics and telemedicine lift healthcare & medical supplies deliveries by 9.6% CAGR. Automated storage and retrieval systems capable of –35 °C to ambient handling protect cold-chain integrity and cut labor exposure. Integrated cold-chain plus express capacity therefore commands premium yields within the Singapore last-mile delivery market.

Government-Backed Nationwide Locker Network Creates Infrastructure Foundation

The Pick Network’s 1,000 parcel lockers sit within a five-minute walk of most HDB households and plug into MRT stations and community clubs, slashing failed deliveries that historically consumed up to 40% of driver time. IMDA’s federated design lets multiple operators share infrastructure, lowering capex while raising network density. Panasonic’s 500 smart lockers anchor phase one, complete with biometric authentication and real-time monitoring[1]Panasonic Connect, “Panasonic Completes 500 Parcel Lockers Island-Wide in Singapore for Pick Network,” ap.connect.panasonic.com. Urban Redevelopment Authority pilots extend the model with consolidated hubs in multi-storey carparks and autonomous robot tests, signaling long-term state commitment to last-mile optimisation.

Cross-Border Micro-Shipments Via Social Commerce Accelerate Regional Integration

TikTok Shop’s 135 million Southeast-Asian users generate impulse buys that rely on Singapore’s fast-clearance customs to hit three-day delivery targets. The city-state’s SGD 400 (USD 294) de minimis threshold keeps most parcels duty-free, cutting border dwell time to under 10 minutes[2]Janio Asia, “Singapore Markets,” janio.asia. Multi-currency corporate cards like YouBiz offer zero FX fees and 1% cashback, easing seller adoption of cross-border campaigns. These platform-centric flows pressure carriers to master specialized customs declarations and real-time duty reconciliation, capabilities that traditional freight forwarders still lack.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban curb-space & traffic congestion | -1.6% | CBD, dense residential zones | Short term (≤ 2 years) |

| Tight labour market & rising manpower costs | -2.3% | Nationwide | Short term (≤ 2 years) |

| Phasing-out of shipping subsidies by e-commerce platforms | -1.8% | National / regional | Medium term (2-4 years) |

| High COE & EV-charging costs for fleet electrification | -1.4% | Commercial vehicle operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Labour Market and Rising Manpower Costs Accelerate Automation Adoption

Eighty-nine percent of logistics employers report recruitment difficulties as sector revenue outpaces workforce growth. Autonomous mobile robots, AI route optimizers, and digital dispatch engines such as A*STAR SIMTech’s Last-Mile Logistics Management allow carriers to scale parcel volumes without proportional headcount. Automation ROI shortens further when paired with mounting wage pressure and a 1.2% annual labor-supply increase against an 8.7% revenue rise.

Urban Curb-Space and Traffic Congestion Constrain Operational Efficiency

Limited loading bays and heightened enforcement in the CBD squeeze delivery windows. LTA’s new rules reducing personal-mobility-aid speed from 10 km/h to 6 km/h temper rider efficiency but improve pedestrian safety[3]Land Transport Authority, “New Rules on Personal Mobility Aids,” lta.gov.sg. The ERP 2.0 virtual-gantry roadmap may introduce distance-based charging, nudging operators toward night deliveries and locker use to bypass peak congestion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Express Delivery Gains Momentum Despite Standard Dominance

Standard delivery retained 52.34% of the Singapore last-mile delivery market share in 2025, reflecting entrenched cost-sensitive habits and optimized 1-to-3-day networks. Express services, however, post a 7.1% CAGR (2026-2031) as merchants weaponize speed for differentiation. Same-day courier apps deliver island-wide in 45 minutes, and GrabExpress leverages super-app driver pools for blended food-and-parcel dispatch. Cold-chain add-ons, secure handling, and white-glove furniture installation broaden express addressable revenue while cushioning margins against commoditized standard rates.

Asset-light micro-fulfilment nodes sited within retail estates compress lead times further. Yet escalating curb-space constraints trigger alternate modes: locker drop-offs, autonomous robots, or scheduled pick-ups. Compliance with GDP pharma standards and HACCP rules raises operational barriers, favoring incumbents with certified quality systems. The Singapore last-mile delivery market size for express services, therefore, rises faster than overall volume growth, signaling ongoing premiumization.

By Business Model: B2B Resilience Meets C2C Innovation

B2B deliveries captured 50.42% of the Singapore last-mile delivery market size in 2025, underpinned by free-trade-zone warehousing and predictable replenishment cycles. Duty-deferred inventory at Changi Air FTZ and Jurong Port lets wholesalers restock ASEAN stores within 48 hours, ensuring low stock-out risk for multinational retailers.

C2C shipments grow at 8.3% CAGR (2026-2031) as peer marketplaces like Carousell integrate on-demand couriers for bulky items. Individual sellers use time-slot booking and digital waybills, turning ad-hoc moves into trackable logistics events. B2C flows, while mature, now blur with C2C as social-commerce micro-brands ship directly from home inventories. This hybridization forces carriers to offer granular APIs and multi-wallet settlement so that one network seamlessly handles invoices, personal parcels, and platform orders within the Singapore last-mile delivery market.

By End-User Industry: Healthcare Acceleration Transforms Traditional Retail Dominance

E-commerce retail controlled 28.65% of the Singapore last-mile delivery market size in 2025, fueled by fashion, beauty, and consumer electronics. Marketplace campaigns and buy-now-pay-later adoption sustain this base.

Healthcare & medical supplies log a 9.2% CAGR (2026-2031), requiring GDP-compliant cold vans, tamper-evident packaging, and minute-level temperature telemetry. Telehealth prescriptions now demand two-hour home delivery, pushing carriers to deploy insulated totes inside express fleets. Furniture and large appliances still hinge on white-glove assembly and flexible scheduling; automation initiatives such as route-sequenced loading reduce dwell time at destination, raising daily drop counts. As vertical specialization deepens, multi-segment operators bundle sector-specific SLAs to maximize fleet utilization across the Singapore last-mile delivery market.

Geography Analysis

Singapore’s compact 728 km² footprint means every address sits within a 50 km radius, underpinning island-wide same-day capability. The western Tuas-Jurong cluster handles 39.01 million TEUs yearly, feeding maritime-origin parcels into micro-fulfilment nodes near HDB estates. Eastern Changi logistics parks manage express air freight, aligning with healthcare and high-tech cargo that demands rapid clearance.

Cross-border corridors via Woodlands Causeway enable daily shuttles to Johor with 3-hour transit times, while ferry links to Batam serve electronics producers sourcing Singapore components. The forthcoming Johor–Singapore Special Economic Zone promises duty-free shuttle runs, expanding the regional relevance of the Singapore last-mile delivery market beyond its borders.

Competitive Landscape

Singapore’s last-mile delivery industry shows moderate fragmentation: platform-owned carriers, tech-enabled couriers, the national post, and specialized cold-chain players battle for share. Ninja Van scales proprietary routing and region-wide hubs to anchor merchant loyalty. Grab exploits its super-app to blend people, food, and parcel mobility, keeping driver utilization high.

Shopee’s SPX Express now fulfills over half of marketplace orders regionally, locking customers into the ecosystem delivery. Singapore Post pivots from mail to e-commerce logistics, investing in AI load-balancing and 4PL orchestration. Sustainability leadership appears through EV-only start-ups such as EVFY, which offers zero-emission fleets and telematics-based carbon dashboards to enterprise shippers.

Automation is an arms race: carriers pilot robot sorters, computer-vision parcel measurement, and AI dispatch to offset 2.3% wage-inflation drag. Healthcare, cold-chain, and cross-border micro-shipments remain white-space areas where smaller specialists carve defensible niches.

Singapore Last-Mile Delivery Industry Leaders

Ninja Van

Singapore Post

J&T Express

GrabExpress

DHL Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: UPS Healthcare launched an 11,500 m² facility at 36 Tuas Road, doubling its regional healthcare footprint.

- April 2025: DHL Supply Chain opened an EUR 10 million (USD 10.4 million) GDP-compliant pharma hub at Jurong Pier, adding 8,200 m² of cold-chain capacity.

- November 2024: DSV rolled out Singapore’s first electric truck fleet using Volvo FL and FM Electric models.

- July 2024: Grab acquired Chope to deepen online-to-offline dining integration after relaunching HungryGoWhere.

Singapore Last-Mile Delivery Market Report Scope

"Last mile delivery" refers to the concluding phase of the logistics process, specifically the journey a product undertakes from a warehouse to the customer's doorstep. This final leg is paramount in the delivery process, demanding meticulous management to ensure swift shipping. The report offers an in-depth analysis of Singapore's Last-Mile Delivery Market. It encompasses an evaluation of the economy, insights into sector contributions, an overview of the market, projections for key segments, trends in emerging segments, and an exploration of market dynamics and geographic patterns.

The Singapore Last-Mile Delivery Market report is segmented by service (B2B (Business-to-Business), B2C (Business-to-Consumer), C2C (Customer-to-Customer)), by delivery mode (regular delivery, same-day delivery, express delivery). The report offers the market size and forecasts in values (USD) for all the above segments.

| Standard Delivery |

| Same-day |

| Express Delivery |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

| E-commerce Retail |

| Fashion & Lifestyle |

| Beauty, Wellness & Personal Care |

| Home & Furniture |

| Consumer Electronics & Appliances |

| Healthcare & Medical Supplies |

| Others |

| By Service | Standard Delivery |

| Same-day | |

| Express Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End-user Industry | E-commerce Retail |

| Fashion & Lifestyle | |

| Beauty, Wellness & Personal Care | |

| Home & Furniture | |

| Consumer Electronics & Appliances | |

| Healthcare & Medical Supplies | |

| Others |

Key Questions Answered in the Report

How large is the Singapore last-mile delivery market in 2026?

It is valued at USD 14.53 billion in 2026 with a 11.97% CAGR outlook to 2031.

Which service segment is expanding fastest?

Express delivery posts the quickest pace at 7.1% CAGR on rising same-day expectations.

Why is healthcare logistics gaining prominence?

Strict temperature control needs and telehealth adoption push healthcare & medical supplies deliveries at 9.2% CAGR.

How do parcel lockers improve efficiency?

The 1,000-unit Pick Network cuts failed deliveries, trimming driver dwell time and curb congestion.

What role do cross-border micro-shipments play?

Social-commerce platforms funnel high-frequency, low-value parcels, boosting small-parcel volumes and customs-clearance demand.

How concentrated is competition?

The top five operators capture roughly 60–65% share, giving the market a moderate concentration score of 6.

Page last updated on: