Singapore Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

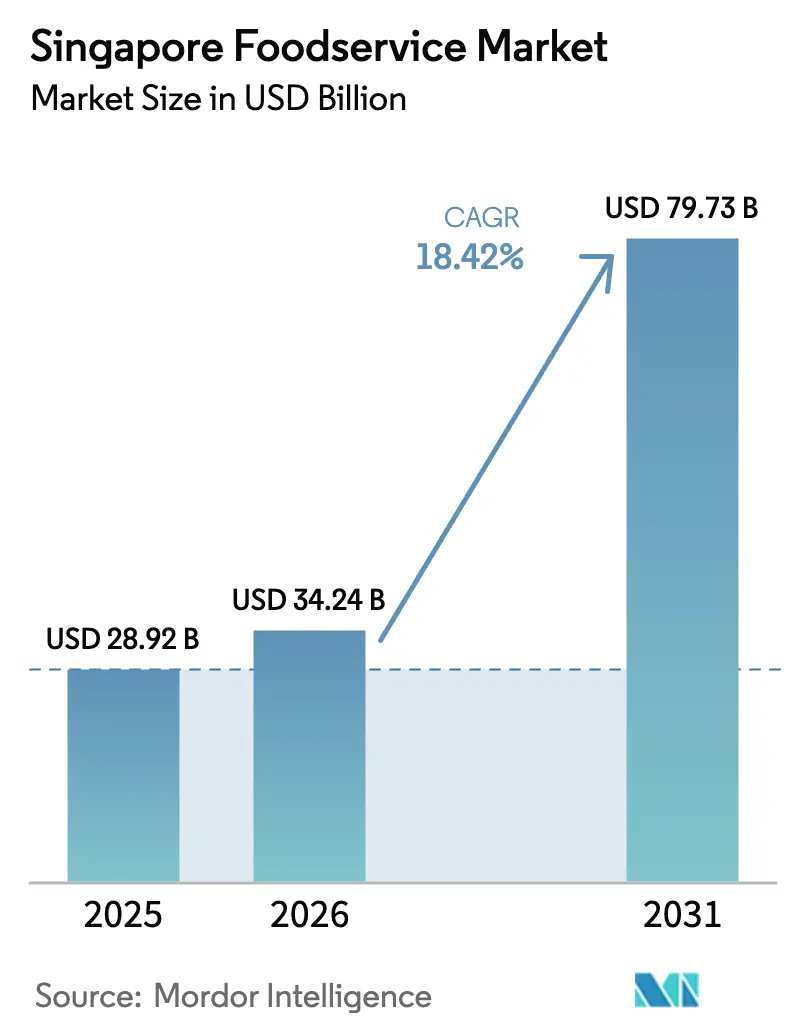

| Base Year Market Size (2025) | USD 28.92 Billion |

| Market Size (2026) | USD 34.24 Billion |

| Market Size (2031) | USD 79.73 Billion |

| Growth Rate (2026 - 2031) | 18.42% CAGR |

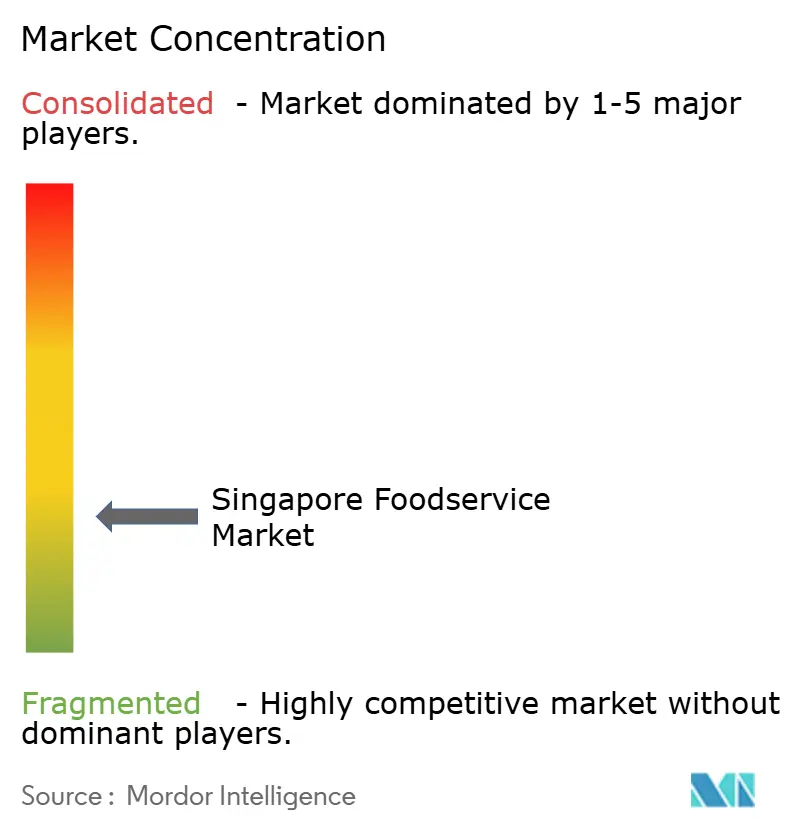

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Foodservice Market Analysis by Mordor Intelligence

The Singapore foodservice market size is expected to grow from USD 28.92 billion in 2025 to USD 34.24 billion in 2026 and is forecast to reach USD 79.73 billion by 2031 at 18.42% CAGR over 2026-2031. This growth is driven by factors such as the recovery of the tourism industry, a tech-savvy population, and strong government initiatives promoting digital payment systems. Businesses that adopt innovations like contactless ordering, loyalty programs, and creative menu offerings are likely to increase their average revenue per customer while reducing labor costs. By service type, food delivery services are growing faster than traditional dine-in options, reflecting changing consumer preferences. In terms of foodservice type, cloud kitchens are emerging as strong competitors to quick-service restaurants (QSRs), offering convenience and efficiency. When considering outlets, independent restaurants are showing resilience despite the expansion of chain establishments. Foodservice locations in lodging venues, such as hotels, are benefiting from the resurgence in tourism. The competitive landscape in Singapore's foodservice market remains intense. However, the market's low concentration provides opportunities for both multinational companies and local independent operators to grow profitably by offering unique and differentiated services.

Key Report Takeaways

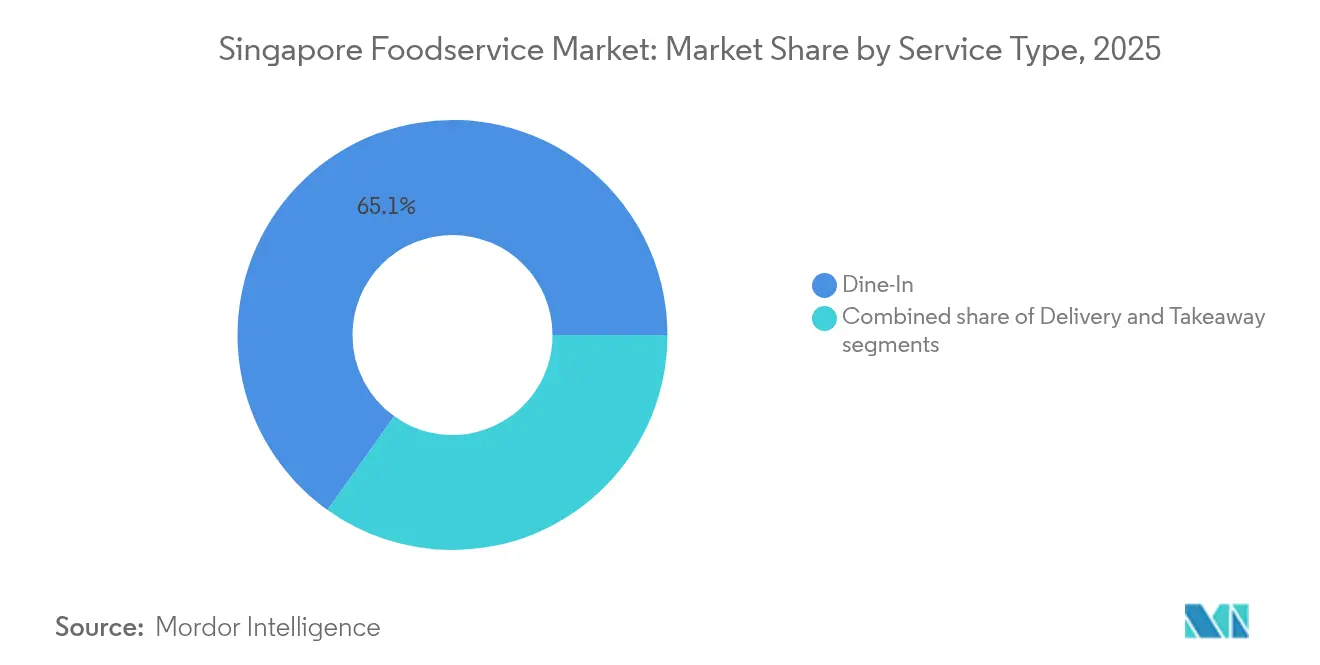

- By service type, dine-in held 65.12% of Singapore's foodservice market share in 2025, while delivery is forecast to post a 20.10% CAGR to 2031.

- By foodservice type, quick service restaurants secured 66.88% revenue share in 2025, whereas cloud kitchens are on track for a 20.05% CAGR through 2031.

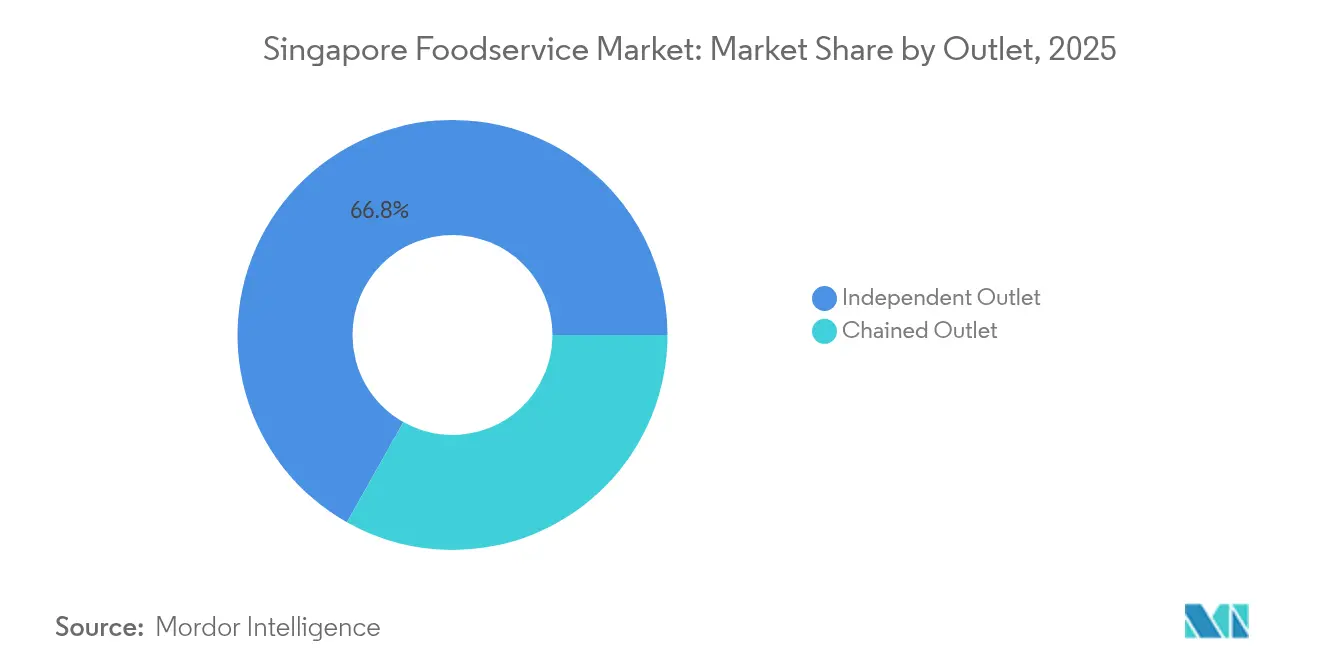

- By outlet, independent outlets commanded a 66.83% share of the Singapore foodservice market size in 2025, and chained outlets are expanding at an 18.62% CAGR toward 2031.

- By location, standalone venues led with 76.55% share in 2025, while lodging-based dining is projected to grow at a 20.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Foodservice Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for specialty beverages and a robust coffee culture | +3.2% | Singapore-wide, concentrated in Central Business District and lifestyle districts | Medium term (2-4 years) |

| Increasing preference for social and post-work gatherings | +2.8% | Singapore-wide, particularly in mixed-use developments | Short term (≤ 2 years) |

| Rising use of digital payments and contactless transaction methods | +4.1% | Singapore-wide with government Singapore Quick Response Code+ support | Short term (≤ 2 years) |

| Demand for unique dining experiences and social engagement | +2.5% | Singapore-wide, emphasis on tourist precincts | Medium term (2-4 years) |

| Shifting consumer preferences and expanding menu offerings | +1.9% | Singapore-wide across all segments | Long term (≥ 4 years) |

| Expansion of the tourism and hospitality sector | +3.8% | Singapore-wide with concentration in Orchard, Marina Bay, Sentosa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for specialty beverages and robust coffee culture

Singapore’s coffee culture is evolving from its traditional kopitiam heritage to a dynamic specialty beverage market, driven by growing consumer interest in premium and unique experiences. Since 2024, international brands like Luckin Coffee, Tim Hortons, and Kopi Kenangan have expanded their presence in the city, offering digital-first store formats that focus on speed, customization, and high-quality products. Government programs such as Hawkers Go Digital have played a key role in modernizing local coffee operators by promoting mobile ordering and digital payment systems. This has made specialty coffee more accessible to a broader audience. According to the Ministry of Trade and Industry, Singapore’s food and beverage services volume index increased by 4.2% in 2023, highlighting strong consumer spending and a thriving cafe culture that continues to support growth in the foodservice market[1]Source: Ministry of Trade and Industry, "Food and Beverage Services", mti.gov.sg.

Increasing preference for social and post-work gatherings

As employment rates rise and urban routines return to normal, Singaporeans are increasingly favoring social and after-work dining experiences. With the easing of pandemic restrictions, restaurants and venues offering flexible seating arrangements and group-friendly spaces have seen higher customer turnover, highlighting a focus on social interactions. Younger consumers, particularly millennials and professionals, are showing a growing preference for low-alcohol and non-alcoholic beverages that align with their health-conscious lifestyles while allowing them to enjoy extended gatherings. According to the International Monetary Fund, Singapore’s employment rate reached 97.9%, supporting strong incomes and frequent dining out after work to release stress and enjoy[2]Source: International Monetary Fund, "Unemployment Rate", imf.org. Supermarket chains are adapting to this trend by incorporating in-store bars and casual dining areas, creating a blend of grocery shopping and socializing opportunities.

Expansion of the tourism and hospitality sector

Singapore’s tourism recovery is driving significant growth in the foodservice market, as increasing numbers of visitors boost demand for dining options both at tourist sites and nearby areas. According to the Department of Statistics Singapore, international visitor arrivals reached 1,609,312 in January 2025, showcasing a strong recovery in travel-related spending[3]Source: Department of Statistics Singapore, "Tourism", singstat.gov.sg. Popular tourist hubs like Marina Bay, Orchard Road, and Sentosa are seeing higher foot traffic, benefiting restaurants, cafes, and bars in these areas. Events such as the Formula 1 Singapore Grand Prix and international concerts are creating seasonal spikes in demand, encouraging foodservice operators to expand capacity and hire more staff. New attractions like Minion Land at Universal Studios Singapore and recently opened hotels are providing more dining opportunities for tourists and locals alike, further supporting the market’s growth.

Rising use of digital payments and contactless transaction methods

Singapore’s foodservice market is evolving rapidly with the increasing adoption of digital payments and contactless transaction methods, making it easier for businesses to offer convenience without significant investments. The nationwide Singapore Quick Response Code+ initiative, which combines over 80 payment schemes into a single QR code, has expanded to more than 35,000 locations as of 2024. This has encouraged the widespread use of QR-based ordering systems. Innovative formats, such as Freshpod’s autonomous food kiosk at Ascent in Singapore Science Park, showcase how automation is transforming customer experiences by providing efficient service. Major players like McDonald’s Singapore are utilizing app-based loyalty programs, such as the “Collect Quest” campaign, to engage customers and encourage repeat visits, further driving growth in the market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Challenges in adhering to regulations and navigating licensing complexities | -2.1% | Singapore-wide, particularly affecting new entrants | Short term (≤ 2 years) |

| Workforce shortages and elevated employee turnover | -3.4% | Singapore-wide across all segments | Medium term (2-4 years) |

| Brand cannibalisation in multi-brand groups | -1.8% | Singapore-wide, concentrated in shopping centers | Long term (≥ 4 years) |

| Increasing raw material costs and disruptions in the supply chain | -2.7% | Singapore-wide with import dependency | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing raw material costs and disruptions in the supply chain

Rising input costs and ongoing supply chain challenges continue to be significant obstacles for Singapore’s foodservice market. While food inflation stopped at 2.5% in December 2024, as reported by the Monetary Authority of Singapore, the country’s dependence on imported ingredients leaves it vulnerable to global price fluctuations[4]Source: Monetary Authority of Singapore, "MAS Monetary Policy Statement - October 2024", mas.gov.sg. Factors such as geopolitical tensions and extreme weather conditions have disrupted the supply of key commodities like wheat, palm oil, and seafood, leading to higher costs for procurement and transportation. These challenges have directly impacted consumers, with hawker meal prices experiencing their sharpest rise since 2008. This demonstrates the limited ability of operators to absorb costs without passing them on to customers. To address these issues, suppliers like Olam Group have introduced traceable and EUDR-compliant sourcing solutions, which aim to enhance supply chain resilience and transparency.

Challenges in adhering to regulations and navigating licensing complexities

Singapore’s foodservice operators face significant challenges in complying with complex regulatory and licensing requirements. Businesses must secure multiple approvals from agencies such as the Singapore Food Agency (SFA), National Environment Agency (NEA), Singapore Civil Defense Force (SCDF), and Urban Redevelopment Authority (URA). These approvals cover areas like hygiene standards, fire safety, outlet layout, and zoning regulations. The process can be time-consuming and costly, especially for smaller or independent operators, as it often delays the opening of new outlets or the renewal of licenses. The recent increase in new food and beverage establishments has led to stricter inspections and higher compliance standards. As a result, these challenges create operational hurdles, limit flexibility, and increase costs for foodservice operators in Singapore.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Delivery Outpaces Traditional Dine-In

Dine-in remains the leading segment in Singapore’s foodservice market, holding 65.12% of the total market share in 2025. This dominance highlights consumers’ preference for dining experiences that offer a combination of good food, ambiance, and social interaction elements that digital platforms cannot fully replicate. Restaurants, cafes, and casual dining outlets, particularly in popular areas like Orchard Road and Marina Bay, continue to attract customers. To enhance the dine-in experience, operators are introducing features such as themed interiors, live cooking stations, and chef-curated menus, which help create memorable experiences and encourage repeat visits.

On the other hand, delivery is rapidly becoming the fastest-growing service channel, with its revenue projected to grow at a 20.10% CAGR from 2026 to 2031. The increasing demand for convenience and flexible meal options is driving this growth, supported by platforms like GrabFood and Foodpanda. Many restaurants are adopting cloud kitchens and partnering with delivery aggregators to reduce costs and improve efficiency. The integration of digital tools such as online menus, cashless payments, and loyalty programs is enhancing the delivery experience for customers. This shift positions delivery as a key driver of growth in Singapore’s evolving foodservice market.

By Foodservice Type: Cloud Kitchens Challenge QSR Leadership

Quick Service Restaurants (QSRs) are a key part of Singapore’s foodservice market, holding a significant 66.88% share in 2025. These restaurants succeed by offering standardized menus, efficient operations, and widespread locations, ensuring consistent quality and convenience for customers. They are especially popular among busy urban consumers who prefer quick and affordable meals. To stay competitive, QSRs regularly introduce new menu items, including limited-time offers and healthier options, to meet changing consumer preferences. Strong brand recognition and loyalty programs help these restaurants maintain their dominance in both dine-in and delivery services.

Cloud kitchens are becoming one of the fastest-growing segments in Singapore’s foodservice market, with revenue expected to grow at a 20.05% CAGR from 2026 to 2031. These kitchens operate without traditional storefronts, using shared spaces and asset-light models to focus entirely on delivery. This approach allows businesses to expand their reach while keeping costs low. By partnering with online food delivery platforms and using digital tools for menu optimization and marketing, cloud kitchens are improving efficiency and profitability. As more consumers turn to app-based meal options for convenience, cloud kitchens are set to play a major role in shaping the future of Singapore’s foodservice industry.

By Outlet: Independent Resilience Amid Chain Expansion

Independent outlets remain a key part of Singapore’s foodservice market, holding 66.83% of the market share in 2025. These outlets thrive due to their strong ties to local communities, offering unique and diverse menu options that cater to specific tastes. Their ability to quickly adapt to changing consumer demands and provide personalized service helps them stand out from larger chains. Many independent operators focus on delivering authentic dining experiences, which fosters customer loyalty and ensures their continued relevance in a competitive market. Despite challenges, their flexibility and creativity allow them to maintain a significant presence.

On the other hand, chain operators are expected to grow rapidly, with revenue projected to increase at an 18.62% CAGR through 2031. The entry of international brands is driving this growth by bringing in fresh investments, operational expertise, and advanced technologies. Chains are leveraging standardized processes and economies of scale to expand their reach and improve efficiency. The use of app-based loyalty programs and targeted marketing strategies is helping them attract and retain customers. As Singapore’s foodservice market becomes more digital and convenience-focused, chain operators are well-positioned to capture a larger share of the market.

By Location: Lodging Venues Ride Tourism Upswing

Standalone foodservice venues remained the largest segment in Singapore’s market, holding 76.55% of the market share in 2025. These venues thrive due to their strategic locations in mixed-use areas, which attract both local residents and office workers looking for convenient dining options. Their ability to draw strong walk-in traffic, adapt layouts to customer needs, and customize menus to suit local preferences has helped them maintain a competitive edge. Standalone outlets often offer unique dining experiences, which appeal to a wide range of customers and contribute to their sustained dominance in the market.

On the other hand, foodservice outlets located in lodging establishments, such as hotels and resorts, are expected to grow rapidly in the coming years. Revenue from these venues is projected to increase at a 20.13% CAGR between 2026 and 2031, driven by the recovery of the tourism sector and the development of integrated resorts. These establishments are increasingly incorporating diverse dining options, including restaurants, bars, and cafes, to cater to both in-house guests and external visitors. The combination of hospitality, entertainment, and dining experiences makes lodging-based foodservice venues a significant growth driver in Singapore’s evolving foodservice market.

Geography Analysis

Singapore’s small size means foodservice operators must focus on specific districts rather than broad regional strategies. Key areas like the Central Business District, Marina Bay, and Orchard Road are major hubs for corporate offices, luxury hotels, and tourists, making them hotspots for high-value transactions. These locations benefit from premium dining options offered by hotels and integrated developments. For example, Marina Bay hotels generate significant food and beverage revenue, and the upcoming Marina South precinct is set to introduce mixed-use spaces with dining options tailored to health-conscious consumers.

Residential neighborhoods, known as heartland estates, play a crucial role in Singapore’s foodservice market. These areas combine traditional coffee shops, hawker centers, and modern quick-service restaurants to serve local communities. Government programs like Hawkers Go Digital have helped small, family-run stalls adopt cashless payment systems, making transactions faster and more convenient. Areas like Sentosa and the Changi region benefit from spending by resort guests, airport staff, and travelers. New transit-oriented developments along MRT lines are also creating opportunities for retail and dining outlets near commuter hubs.

Tourists from different countries significantly influence Singapore’s foodservice offerings, driving demand for diverse menu options. For instance, Chinese tourists often prefer seafood and hotpot dishes, while Indonesian visitors look for halal options, and Indian travelers boost demand for vegetarian and spice-rich cuisines. This diversity encourages operators to innovate with fusion dishes while adhering to strict food safety regulations that ensure consistent quality. Looking ahead, integrated developments combining residential, commercial, and recreational spaces are expected to attract steady foot traffic, supporting a variety of dining experiences across the city-state.

Competitive Landscape

The Singapore foodservice market is highly fragmented, with no single player holding more than 5% of the market share. This creates a competitive landscape where global brands like McDonald’s, Starbucks, and KFC compete alongside regional chains such as Jollibee and Luckin Coffee, as well as numerous independent operators. Digital capabilities increasingly drive the competition, as businesses use real-time data to adjust pricing, optimize menus, and personalize marketing strategies. While multinational companies leverage large-scale loyalty programs, smaller operators rely on third-party platforms to expand their reach and attract customers.

Cloud kitchens are transforming the traditional foodservice model by offering flexible, low-cost setups that can quickly adapt to changing demand. Many international brands are drawn to Singapore due to its political stability, strong intellectual property laws, and tech-savvy population. In response, local operators are launching sub-brands to cater to emerging trends, such as plant-based dining, while avoiding competition within their own portfolio. Supply chain resilience has become a key focus, as businesses with diverse supplier networks are better positioned to manage costs and avoid disruptions, especially after the challenges faced during the pandemic.

Sustainability is becoming a critical factor in the Singapore foodservice market, driven by both regulatory pressures and consumer preferences. For example, BreadTalk has taken steps to reduce packaging waste and minimize food waste, reflecting a broader shift toward environmentally friendly practices. Large chains are now publishing plans to lower their carbon footprint, while smaller operators are adopting low-waste cooking methods and reusable service ware. These efforts not only enhance brand reputation but are also becoming essential for securing prime locations in premium mixed-use developments, further influencing competition in the market.

Singapore Foodservice Industry Leaders

-

BreadTalk Group Ltd

-

Grab Holdings Inc.

-

Hanbaobao Pte Ltd (McDonald’s)

-

QSR Brands (M) Holdings Sdn Bhd (KFC)

-

Starbucks Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Chick-fil-A opened its first restaurants in Singapore as part of a USD 175 million global expansion strategy. This move highlighted the brand's efforts to strengthen its international presence and tap into the growing demand for quick-service dining in the region.

- July 2025: Blue Bottle Coffee inaugurated a new cafe at Paragon, its second outlet in Singapore and the first in the Orchard Road area. This expansion reflected the brand's commitment to enhancing its presence in key urban locations and catering to a diverse customer base.

- April 2025: Luckin Coffee, a prominent Chinese coffee chain, announced its collaboration with the global fintech leader Stripe. This partnership aimed to facilitate Luckin Coffee's international expansion, beginning with its entry into Singapore.

- April 2023: Taster Food Pte Ltd launched its new Kit Kat Chocolate Lava buns, available across all its outlets in Singapore. This product introduction aimed to attract dessert enthusiasts and expand its customer base by offering innovative and indulgent options.

Singapore Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Dine-In |

| Takeaway |

| Delivery |

| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other Full Service Restaurants Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other Quick Service Restaurants Cuisines |

| Chained Outlet |

| Independent Outlet |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| By Service Type | Dine-In | ||

| Takeaway | |||

| Delivery | |||

| By Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other Full Service Restaurants Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other Quick Service Restaurants Cuisines | |||

| By Outlet | Chained Outlet | ||

| Independent Outlet | |||

| By Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms