Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

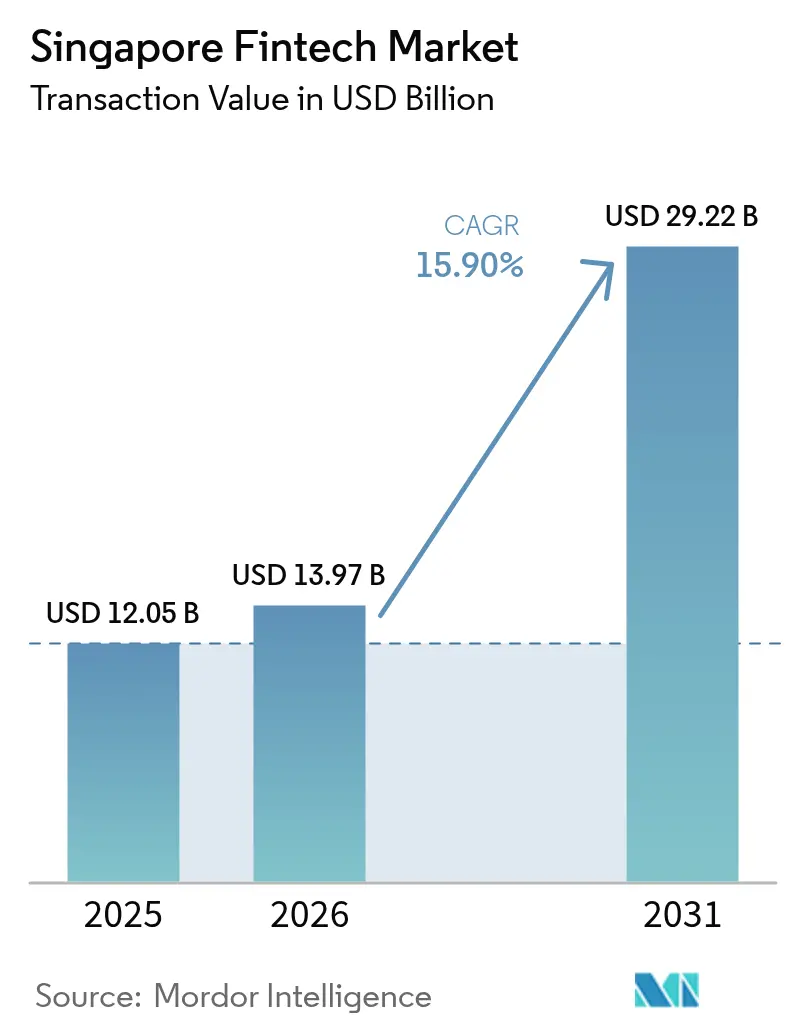

| Base Year Market Size (2025) | USD 12.05 Billion |

| Market Size (2026) | USD 13.97 Billion |

| Market Size (2031) | USD 29.22 Billion |

| Growth Rate (2026 - 2031) | 15.90% CAGR |

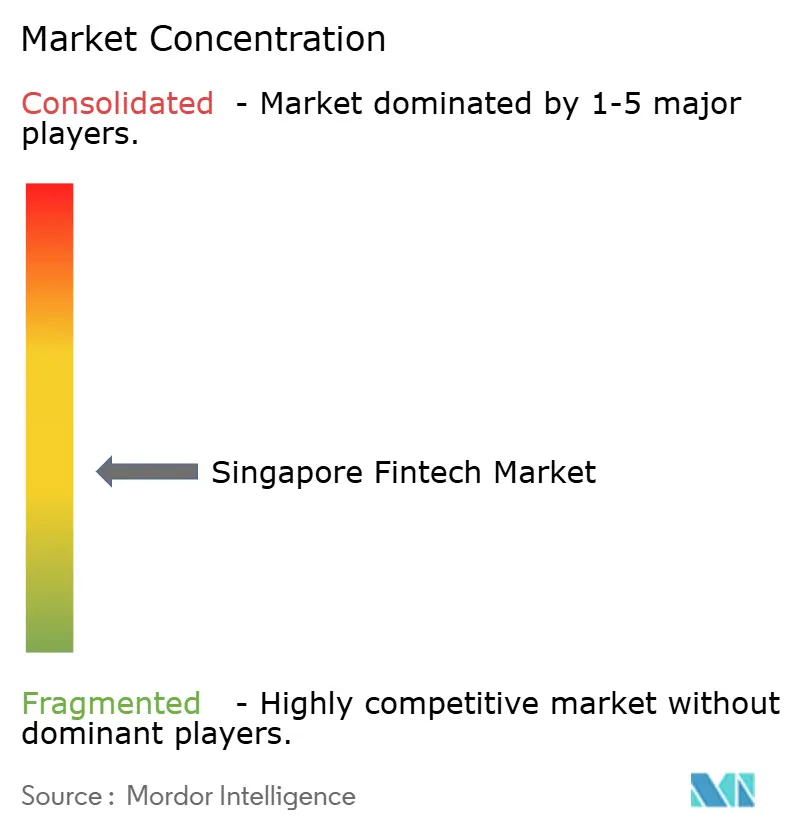

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Fintech Market Analysis by Mordor Intelligence

Singapore fintech market size in 2026 is estimated at USD 13.97 billion, growing from 2025 value of USD 12.05 billion with 2031 projections showing USD 29.22 billion, growing at 15.9% CAGR over 2026-2031. Strong policy support, deep digital infrastructure, and sustained inflows of private capital keep the Singapore fintech market on a steep expansion path, even as competitive intensity and regulatory scrutiny increase. Market momentum reflects the Monetary Authority of Singapore’s (MAS) SGD 100 million (USD 77 million) FSTI 3.0 program, which co-funds quantum-safe cybersecurity and AI-driven risk models, giving early adopters a durable technology lead[1]Monetary Authority of Singapore, “Overview of Regulatory Sandbox,” MAS.GOV.SG. . Additional uplift comes from Project Nexus—the five-country instant-payment corridor that is scheduled to go live by 2026—which will compress settlement cycles and open new revenue pools for cross-border trade service providers. The Singapore fintech market also benefits from PayNow’s growing regional linkages, accelerating demand for multi-currency wallets among SMEs engaged in cross-border e-commerce. At the same time, tightened consumer-protection rules for crypto and buy-now-pay-later (BNPL) products temper near-term revenue growth, prompting business-model pivots toward embedded finance and B2B2C distribution.

Key Report Takeaways

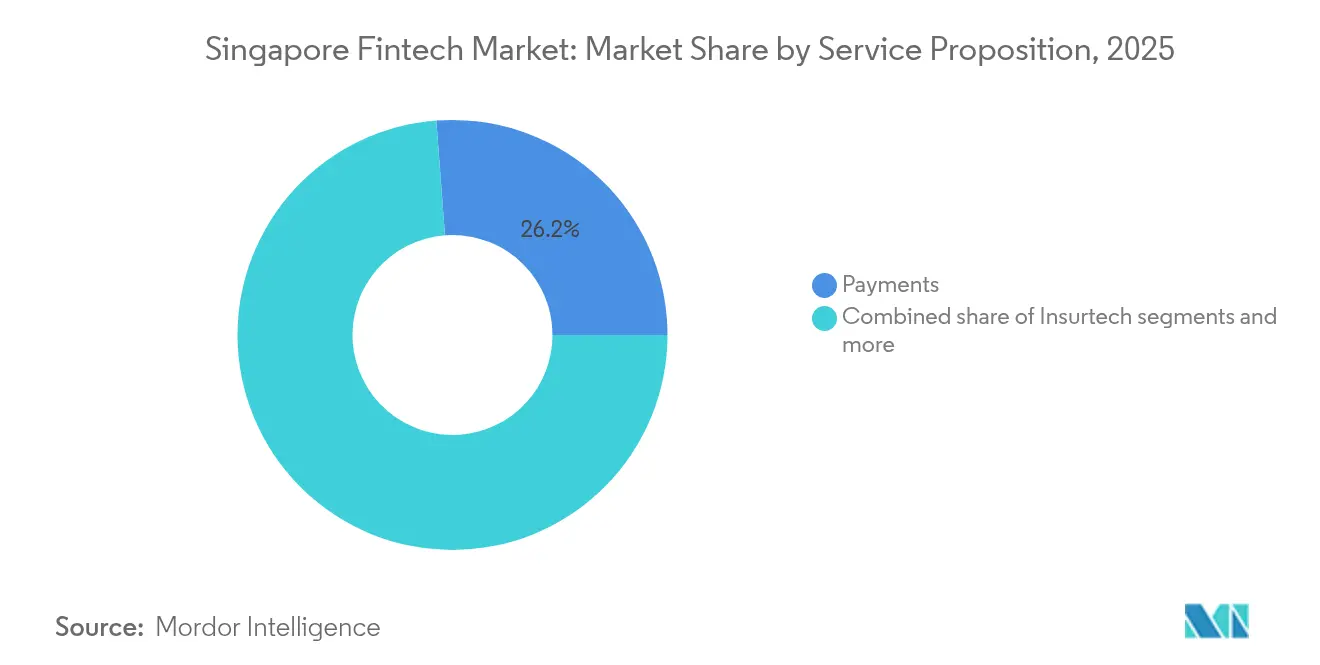

- By service proposition, payments accounted for 26.20% of the Singapore fintech market share in 2025, while the Singapore fintech market size for digital payments is projected to grow fastest at a CAGR of 16.95% between 2026 and 2031.

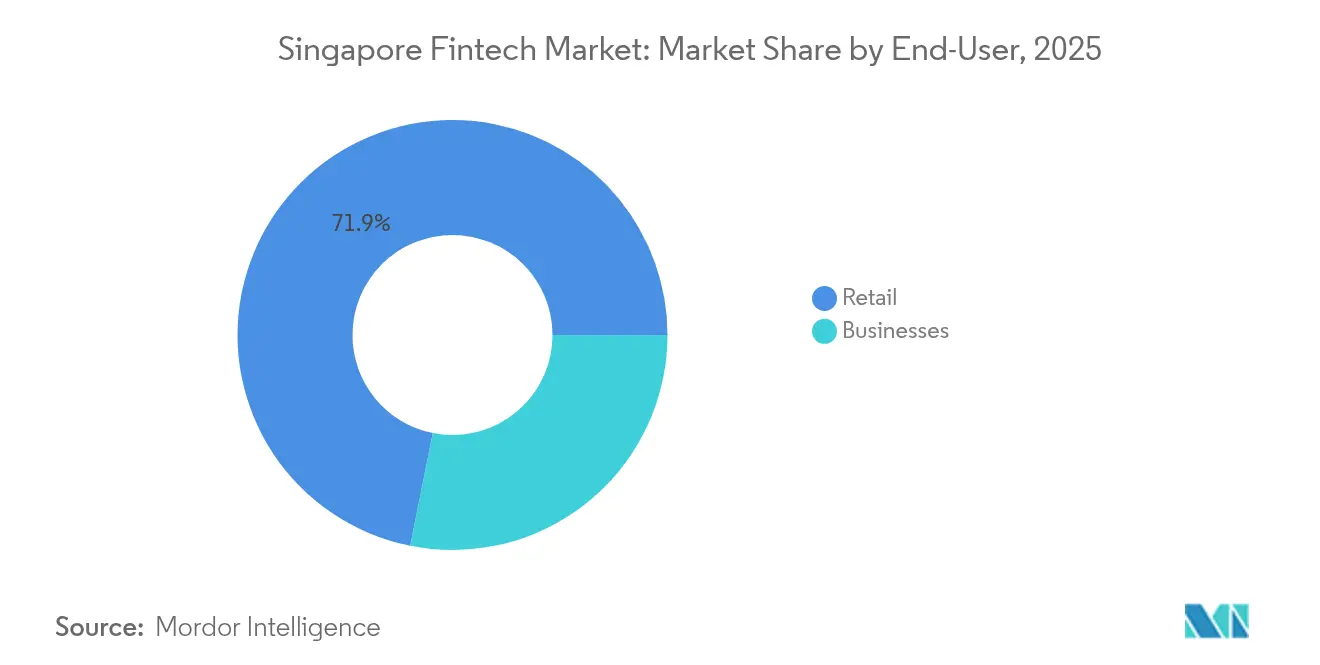

- By end-user, retail captured 71.85% of the Singapore fintech market share in 2025, with the Singapore fintech market size for business users expected to post the highest growth rate at 8.55% CAGR through 2031.

- By user interface, mobile apps held 69.10% of the Singapore fintech market share in 2025, while the Singapore fintech market size for POS/IoT devices is forecast to expand at a 13.38% CAGR during 2026–2031.

- By geography, the Central Region led with 34.10% of the Singapore fintech market share in 2025, while the Singapore fintech market size in the North-East Region is anticipated to grow at the fastest CAGR of 5.55% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid real-time payment rail adoption | +4.2% | Global, APAC focus | Medium term (2-4 years) |

| MAS grants spurring AI & quantum fintech | +2.8% | Singapore with APAC spillover | Long term (≥ 4 years) |

| Cross-border e-commerce & wallets | +1.9% | APAC, Southeast Asia concentration | Short term (≤ 2 years) |

| Digital-only banking licences | +1.1% | Singapore national | Medium term (2-4 years) |

| ESG-driven green-finance mandates | +0.9% | Global with Singapore leadership | Long term (≥ 4 years) |

| SME credit gap & alt-lending platforms | +0.8% | Singapore national, APAC expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Real-Time Payment Rails Transform Settlement Economics

Project Nexus will connect payment rails in Singapore, Malaysia, Thailand, the Philippines, and India by 2026, eliminating the need for nostro accounts and cutting settlement from T+2 to real-time [2]Monetary Authority of Singapore, “Project Nexus,” MAS.GOV.SG.. The shift frees up an estimated USD 120 billion in trapped liquidity and reduces cross-border transaction fees, generating immediate cost savings for merchants and SMEs. Early integrating fintech firms will gain share in B2B trade finance, where real-time settlement unlocks working-capital products tied to shipment milestones. PayNow’s bilateral links with PromptPay and DuitNow processed more than 2.5 million transactions in 2024, demonstrating proven customer appetite for instant regional payments. As rails converge, traditional banks must overhaul legacy APIs or risk ceding high-margin corridors to nimble challengers. The new infrastructure also supports micropayments and micro-insurance, widening addressable use cases across Southeast Asia.

Quantum-Ready Innovation Funding Accelerates Competitive Differentiation

Through FSTI 3.0, MAS co-funds up to 50% of projects deploying quantum-resistant encryption and AI-powered risk analytics[3]Monetary Authority of Singapore, “FSTI 3.0 Factsheet,” MAS.GOV.SG. . The subsidy lowers capex barriers for mid-tier fintechs, enabling them to harden cybersecurity stacks ahead of regulatory mandates. Collaboration inside the Cyber and Technology Resilience Experts (CTREX) panel ensures knowledge transfer from Microsoft, Amazon, and Google Cloud, aligning domestic standards with global best practices. Early movers already test quantum-safe payment protocols that withstand Shor-algorithm attacks, positioning them for compliance once post-quantum cryptography becomes compulsory. Banks adopting quantum-secure key exchange safeguard high-value treasury flows, giving Singapore a first-mover lead in safe-harbor financial hosting. Over the long term, quantum-enhanced optimization may also streamline credit-risk modelling and portfolio rebalancing, boosting sector productivity.

Cross-Border E-Commerce Growth Drives Multi-Currency Innovation

The ASEAN digital economy is projected to top USD 1 trillion by 2030, with cross-border transactions the fastest-expanding slice of that value pool. As sellers in Vietnam, Indonesia, and the Philippines list on Singapore-based platforms, demand for multi-currency wallets surges. Fintechs enable merchants to hold, pay, and hedge in local currencies, cutting FX spreads by up to 400 basis points versus traditional banks. Instant settlement improves supplier liquidity, while API-based invoicing accelerates order-to-cash cycles. MAS expanded the Payment Services Act to cover spot FX conversions, assuring consumer protection and guarding against hidden fees. The regulatory clarity supports further wallet innovation, including dynamic FX pricing and automated hedge triggers based on real-time inventory data.

Digital Banking Licenses Create Niche Market Opportunities

Singapore’s digital-bank regime requires licensees to serve underserved consumers and SMEs, opening profitable niches that incumbents long overlooked. GXS Bank targets gig-economy incomes with daily-interest savings accounts, while Trust Bank leverages NTUC’s membership base to cross-sell groceries and financial services. ANEXT Bank taps Ant Group’s underwriting engine to automate SME credit scores, compressing loan-origination cycles from weeks to hours. License caps on leverage and deposit exposure ensure system stability, yet still compel traditional banks such as DBS and OCBC to double down on digital reinvention. Open-banking APIs foster third-party integrations, letting merchants embed lending and insurance at checkout. Over time, digital-bank customer data will refine alternative credit models, further shrinking the SGD 20 billion (USD 14.70 billion) SME financing gap.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High customer-acquisition costs | –2.1% | Singapore national, APAC spillover | Short term (≤ 2 years) |

| Tightened crypto & BNPL consumer protection | –1.4% | Singapore national | Medium term (2-4 years) |

| AI / cybersecurity talent shortages | –1.2% | Singapore national, regional rivalry | Long term (≥ 4 years) |

| Legacy core-bank integration barriers | –0.9% | Singapore national, APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Customer Acquisition Costs Strain Fintech Profitability Models

Nearly universal smartphone ownership produces a saturated addressable base, making marginal customer wins increasingly expensive. Incentive budgets for e-wallet sign-ups ballooned by 40–60% in 2024, pushing payback periods for small fintechs beyond 30 months. App fatigue further erodes return on marketing spend because consumers prefer multifunction super-apps such as Grab, which bundle ride-hailing, food delivery, and payments. The trend forces standalone providers to pivot toward embedded-finance partnerships, integrating services into merchant or platform ecosystems to share acquisition costs. B2B2C distribution also improves unit economics; SME software vendors, for example, can embed invoicing-linked credit lines, spreading marketing costs across multiple revenue streams. Elevated acquisition costs therefore act as a filtering mechanism, rewarding fintechs with strong ecosystems or differentiated IP, while pushing under-capitalized startups to consolidate or exit.

Regulatory Tightening Constrains High-Growth Fintech Segments

MAS clamped down on high-risk marketing tactics after 2024’s enforcement action that suspended Qoo10’s payment services over delayed merchant settlements. New rules cap BNPL late-payment fees and ban crypto cash-backs, trimming revenue margins for companies that relied on aggressive promotions. Updated AML/CFT guidelines demand enhanced transaction monitoring, raising compliance costs, especially for small-cap virtual-asset providers. Mandatory risk-disclosure statements lengthen onboarding flows, putting friction into user acquisition funnels. Stricter custodial requirements also sideline lightly regulated offshore exchanges, funneling volume toward licensed entities but narrowing product scope. While the measures strengthen systemic safety, they compress growth rates of previously breakneck segments, forcing a shift toward sustainable revenue models grounded in fee-based or subscription services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Payments Infrastructure Drives Market Leadership

In 2025, digital payments accounted for 26.20% of the Singapore fintech market size, reflecting their central role in day-to-day commerce. The segment is on track to expand at a 16.95% CAGR through 2031, propelled by SGQR+ interoperability, merchant SoftPOS adoption, and PayNow’s regional links. Card-rail bypass via account-to-account transfers reduces interchange fees, encouraging merchants to prioritize QR and instant payments. Meanwhile, alternative credit scoring in digital lending continues to unlock quick-turnaround microloans for gig workers, albeit at a slower growth than payments. Insurtech firms embed bite-sized coverage within ride-hailing and delivery apps, widening reach without requiring stand-alone policy purchases. Wealth-tech platforms such as StashAway scale on low-cost ETF portfolios, challenging private banks for mass-affluent assets. MAS’s regulatory sandbox supports experiments that bundle payments, lending, and insurance, fostering holistic financial offerings. By 2030, integrated platforms are expected to direct more than 40% of domestic retail transaction value, cementing payments as the linchpin of broader fintech ecosystems.

Competition intensifies as digital-wallet providers extend credit lines and insurance add-ons, blurring traditional segment boundaries. Super-apps leverage first-party consumption data to refine underwriting, while incumbents open APIs to retain relevance within merchant checkout flows. The Singapore fintech market, therefore, continues to reward providers that control the point of sale and can layer higher-margin, add-on services onto high-frequency payment use cases. Regulatory support for tokenized deposits and network tokenization further improves security and interchange economics. As real-time rails mature, payments revenue will increasingly derive from value-added data analytics, loyalty, and payment services rather than per-transaction fees.

By End-User: Business Segment Acceleration Signals B2B Opportunity

Retail customers remain the majority, holding 71.85% of the Singapore fintech market share in 2025, but growth has plateaued in basic deposits and payments. Businesses, especially SMEs, now represent the fastest-growing user group, projected at an 8.55% CAGR to 2031. The SGD 20 billion (USD 15.60 billion) funding gap leaves many SMEs underserved by traditional banks that struggle with collateral-light balance sheets. Alt-lenders deploy cash-flow-based scoring, granting approvals in under 48 hours, a service level unattainable for legacy lenders burdened by manual processes. B2B cross-border payments profit from Project Nexus’s real-time corridors, slashing supplier settlement costs and improving cash conversion cycles.

SMEs also adopt treasury APIs that reconcile invoices in real time, aiding cash-flow forecasting. Invoice-financing fintechs further monetize transaction data, pricing risk dynamically rather than relying on static collateral. For retail users, saturation in wallets and current accounts shifts innovation toward wealth and insurance; robo-advisors now bundle term-life policies alongside ETF portfolios to widen wallet share. Forward-looking analytics recommend savings goals and automated round-ups, deepening engagement. Conversely, evolving privacy norms and MAS’s data-governance guidelines restrict unchecked data monetization, prompting platforms to emphasize consent-driven personalization.

By User Interface: POS/IoT Devices Emerge Through Merchant Innovation

Mobile applications controlled 69.10% of the Singapore fintech market size in 2025, sustained by near-universal smartphone usage and mature app ecosystems. However, POS/IoT devices are the breakout channel, forecast to climb at a 13.38% CAGR to 2031 as merchants embrace SoftPOS and sensor-based payments. Solutions from NETS, FOMO Pay, and 2C2P turn Android phones into contactless terminals, eliminating hardware costs for small retailers. IoT integration enables invisible payments at parking gates, vending machines, and smart buildings, elevating user convenience.

Web portals still serve complex, high-value B2B transactions that demand audit trails and bulk upload features. Yet browsers increasingly operate as control centers for API configuration, with the transaction front-end shifting to in-context touchpoints such as ERP systems or chatbots. MAS’s Technology Risk Management guidelines stress end-to-end encryption and secure element usage in SoftPOS deployments, safeguarding consumer data. As the line between interface and embedded layer blurs, customer experience hinges on latency, uptime, and context relevance rather than visual design. Providers optimizing for sub-200-millisecond transaction processing will capture share among merchants whose revenue depends on checkout speed.

Geography Analysis

The Central Region held 34.10% of the Singapore fintech market share in 2025, anchored by the downtown core that hosts MAS, global banks, and dense fiber connectivity. Ultra-low latency links attract high-frequency traders and data-rich fintechs that co-locate servers within proximity to hosting sites. Shared regulatory offices streamline licensing conversations, cutting time-to-market for new product launches. East Region’s airport-centric economy funnels steady demand for multi-currency wallets and duty-free payments, while its logistics hubs drive adoption of supply-chain finance solutions.

North-East Region enjoys the fastest CAGR at 5.55%, catalysed by Punggol’s digital district, where test beds for 5G, IoT, and edge data centers lower barriers for deep-tech startups. Residential demographics skew younger and more tech-savvy, producing early adopters for pilot deployments of wallet-linked wearables and biometric login. West and North Regions grow steadily as industrial estates modernize payment workflows and implement ESG-aligned carbon-credit exchanges. Across all regions, government-backed 5G densification supports pervasive connectivity, enabling fintech operators to deliver consistent user experiences city-wide.

Competitive Landscape

The Singapore fintech market shows a moderate level of concentration, with the leading five players holding a significant portion of the market, while still leaving ample room for niche and specialist providers to emerge. Grab Financial Group has capitalized on its super-app model, successfully converting its ride-hailing and food delivery user base into digital wallet customers. Meanwhile, DBS Bank has maintained a strong position by expanding its digital wealth management services and seamlessly integrating real-time payment solutions into its corporate banking offerings. These dynamics highlight the strength of ecosystem-driven strategies and the growing importance of integrated financial services. The market remains competitive, offering opportunities for both established players and innovative entrants. OCBC, UOB, and FOMO Pay round out the top tier, each focusing on distinct niches such as SME lending or merchant acquiring.

Competitive pressure centers on technology differentiation and compliance execution. Firms that operationalize MAS’s data-governance guidelines and quantum-safe encryption gain institutional trust, a key advantage when courting enterprise clients. Quantum-ready security also attracts foreign asset managers seeking a safe jurisdiction for regional hubs. Startups without deep compliance budgets partner with licensed entities under Banking-as-a-Service frameworks, trading margin for speed-to-market.

M&A activity accelerates as customer-acquisition costs soar; 2025 has already seen mid-tier robo-advisor MoneyOwl exit, while Syfe turned profitable by cross-selling insurance and pension products. Investors now prioritize path-to-profitability metrics, steering capital toward embedded-finance plays that monetize existing traffic rather than burning cash on standalone apps. Across the board, firms capable of leveraging real-time payments, AI-driven underwriting, and ESG-linked instruments are best positioned to compound growth within the Singapore fintech market.

Singapore Fintech Industry Leaders

Grab Financial Group (GrabPay, GrabFin)

DBS Bank (DBS PayLah!, digibank)

Wise

Funding Societies

Singlife with Aviva

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MAS established the Cyber and Technology Resilience Experts (CTREX) panel, replacing the previous Cyber Security Advisory Panel with an expanded mandate covering quantum security and digital financial scams, which includes global technology leaders from Microsoft, Amazon, and Google Cloud, providing strategic guidance on emerging technology risks and resilience measures for Singapore's financial sector.

- April 2025: The Monetary Authority of Singapore published comprehensive data governance guidelines for financial institutions, establishing new standards for AI model risk management and quantum-ready security implementations. The guidelines mandate enhanced cybersecurity controls and incident reporting procedures, with maximum penalties reaching SGD 1 million (USD 780,000) for data breaches.

- December 2024: Singapore outpaced Hong Kong in digital asset licensing, granting 13 crypto licenses in 2024 compared to Hong Kong's 7 fully licensed platforms. Major recipients included OKX, Upbit, Anchorage, BitGo, and GSR, positioning Singapore as the preferred regional digital asset hub through more permissive custody and token listing policies.

- October 2024: MAS published a Virtual Assets Risk Assessment identifying primary money laundering and terrorism financing threats in Singapore's digital asset ecosystem. The assessment provides guidance for financial institutions on enhanced AML/CFT controls and risk mitigation measures for virtual asset-related activities.

Singapore Fintech Market Report Scope

Singapore fintech is one of the largest fintech industries as businesses and people increasingly prefer digitized means of driving financial products for their investments, evaluation, and payments through a huge variety of fintech platforms for various types of financial products. A complete background analysis of the Singapore Fintech Market, which includes an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, is covered in the report.

The Singapore Fintech Market Is Segmented By Service Proposition (Money Transfer And Payment, Savings And Investment, Digital Lending And Lending Investment, Online Insurance And Insurance Marketplaces, And Other Service Offerings), And By End-User (Banking, E-Commerce, Income Tax Returns, Insurance, And Securities). The Market Size And Forecast For The Singapore Fintech Market In Terms Of Transaction Volume And/Or Revenue (USD) For All The Above Segments.

By Service Proposition

| Digital Payments |

| Digital Lending & Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Geography

| Central Region |

| East Region |

| North Region |

| North-East Region |

| West Region |

| By Service Proposition | Digital Payments |

| Digital Lending & Financing | |

| Digital Investments | |

| Insurtech | |

| Neobanking | |

| By End-User | Retail |

| Businesses | |

| By User Interface | Mobile Applications |

| Web / Browser | |

| POS / IoT Devices | |

| By Geography | Central Region |

| East Region | |

| North Region | |

| North-East Region | |

| West Region |

Key Questions Answered in the Report

What is the 2026 value of the Singapore fintech market?

The Singapore fintech market size was USD 13.97 billion in 2026.

How fast will digital payments grow in Singapore?

Digital payments are projected to record a 16.95% CAGR between 2026 and 2031, the highest among service categories.

Which user group is expanding the quickest?

Business users, led by SMEs, are expected to grow at an 8.55% CAGR through 2031 as alternative lending and real-time payments gain traction.

Why is the North-East Region a high-growth area?

Punggol’s digital district, lower rents, and smart-infrastructure pilots support a 5.55% CAGR, the fastest regional pace to 2031.

What role does MAS play in sector growth?

MAS drives innovation with FSTI 3.0 grants, post-quantum security standards, and instant-payment corridors that lower settlement costs.

Page last updated on: