Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.60 Billion |

| Market Size (2026) | USD 4.10 Billion |

| Market Size (2031) | USD 8 Billion |

| Growth Rate (2026 - 2031) | 14.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Neobanking Market Analysis by Mordor Intelligence

The Europe Neobanking Market size is projected to be USD 3.60 billion in 2025, USD 4.10 billion in 2026, and reach USD 8 billion by 2031, growing at a CAGR of 14.20% from 2026 to 2031.

The funding and adoption cycle in 2026 shows steady expansion as younger cohorts shift toward mobile-first banking experiences that compress onboarding time, improve fee transparency, and provide API-aligned connectivity across daily-use apps. Incumbent banks continue to renew legacy cores, yet cloud-native challengers iterate faster on product, embed financial services within partner platforms, and convert secondary accounts to primary usage through feature depth. Product roadmaps now center on turning habitual app interactions into multi-product relationships with savings, credit, and protection add-ons that support stable revenue. The balance between growth and control has tightened as fraud risks and regulatory requirements increase, shaping the economics and operating discipline across the Europe neobanking market.

Key Report Takeaways

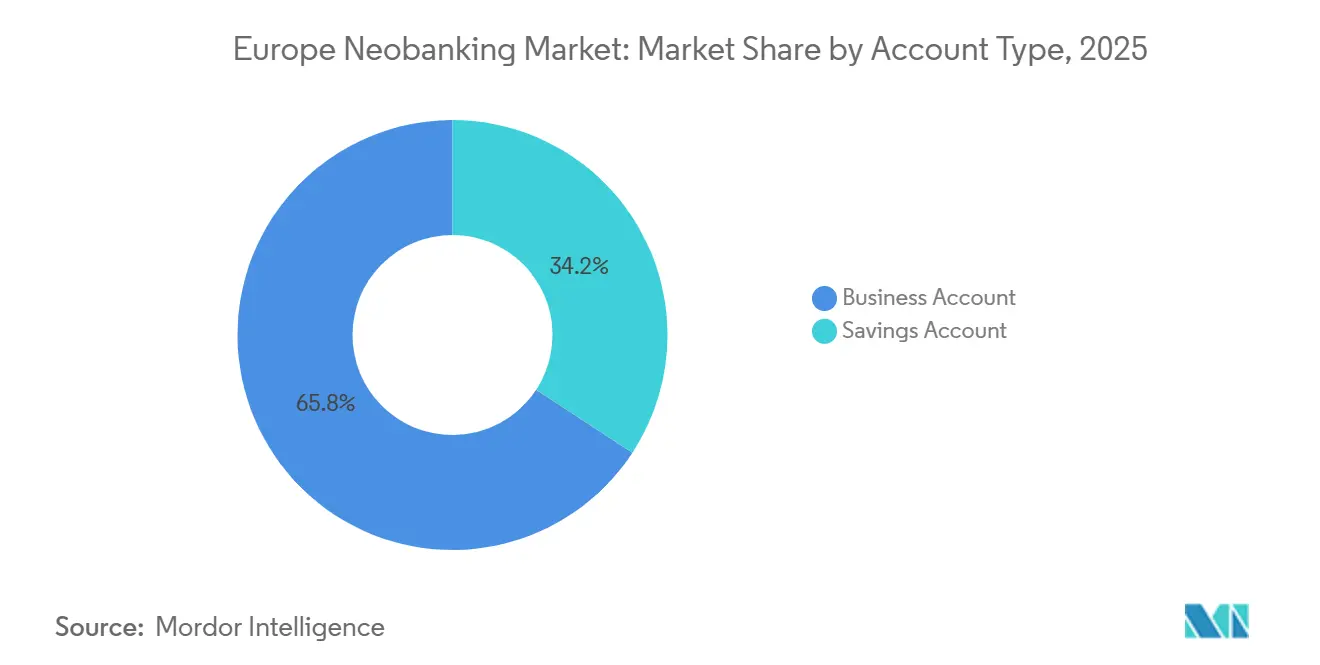

- By account type, business accounts led with 65.78% of the Europe neobanking market share in 2025, while savings accounts are projected to expand at a 41.33% CAGR through 2031.

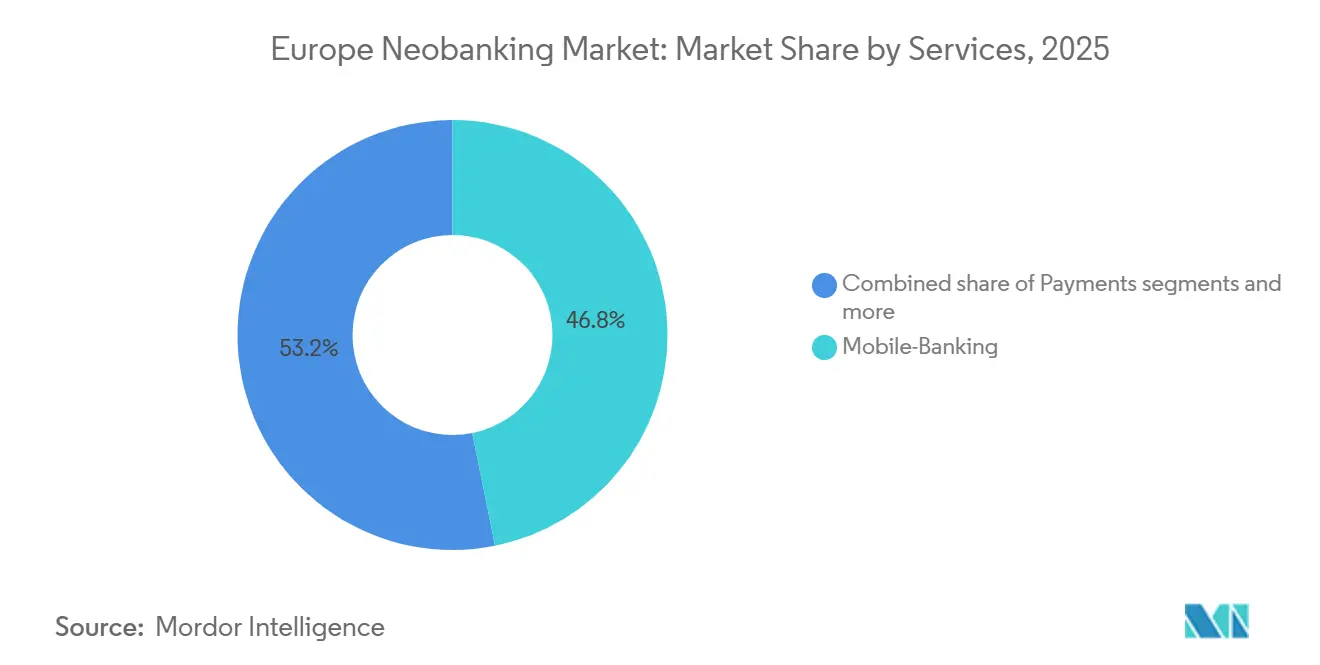

- By services, mobile banking held 46.84% of the Europe neobanking market share in 2025, while loans are forecast to grow at a 43.13% CAGR through 2031.

- By application, enterprise accounted for 68.18% of the Europe neobanking market share in 2025, while personal use is projected to grow at a 38.44% CAGR through 2031.

- By geography, the United Kingdom commanded 27.97% of the Europe neobanking market share in 2025, while Spain is forecast to expand at a 34.43% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Neobanking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile-banking app adoption | + 2.8% | EU-wide, strongest in the United Kingdom, the Nordics, and Spain | Medium term (2-4 years) |

| PSD2 and open-banking mandates | + 3.1% | EU-wide and the United Kingdom | Long term (≥ 4 years) |

| Millennial and Gen-Z digital-first demand | + 2.4% | EU-wide, concentrated in large cities | Long term (≥ 4 years) |

| SEPA Instant and national A2A schemes | + 2.6% | EU-wide, the highest uptake is in the Netherlands, Germany, and France | Medium term (2-4 years) |

| Rising-rate interest income monetization | + 1.8% | Euro area core | Short term (≤ 2 years) |

| Embedded finance and BaaS pipelines | + 1.5% | United Kingdom, Germany, France, Benelux, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Millennial & Gen-Z Digital-First Demand

ECB surveys conducted in 2024 indicated that adults aged 18 to 34 displayed meaningfully higher intent to use a digital euro relative to the general population, underscoring stronger digital adoption and comfort with app-only financial tools among younger cohorts. The same survey work linked higher educational attainment and higher income brackets with greater willingness to use central bank digital money, suggesting that early adopters skew toward demographics that also show elevated interest in digital banking utility features. In parallel, company-level traction supports the demographic shift, as CaixaBank reported that imagin contributed significantly to new customer acquisition in Spain in 2025 and that the sub-brand captured a visible share of payroll account openings among younger users [1]CaixaBank, “CaixaBank Gains 390,000 Customers in Spain During 2025,” CaixaBank, caixabank.com. These dynamics support targeted feature sets such as spending categorization, instant peer payments, and controls that prioritize transparency over branch-based advisory. The cohort effect continues to anchor forward growth, reinforcing the breadth of use cases in the Europe neobanking market.

SEPA Instant & National A2A Schemes Boost Cost Advantage

Instant payment adoption across Europe improves settlement speed and reduces unit costs for account-to-account transfers, which strengthens the economics of mobile-first offerings that connect directly to domestic and pan-European clearing systems. Real-time availability and transparent status updates are now core customer expectations for recurring payments, cross-border transfers, and reconciliation, shaping the design of product experiences across the region. Neobanks operate modern cores that can route A2A transactions with low latency and minimal marginal costs, which support consumer zero-fee propositions and enterprise treasury tools. As account-to-account usage increases at checkout and in subscription billing, the reliance on traditional card-scheme economics becomes less central to the revenue mix. These rails serve as a structural advantage for challengers when combined with consistent risk controls and service quality across the Europe neobanking market.

Rising-Rate Interest Income Monetization

Retail deposits are the primary funding base for many digital-only institutions in Europe, with national guaranteed schemes providing coverage that underpins customer confidence in 2026 [2]European Parliament, “Neobanks in Europe: Briefing,” European Parliament, europarl.europa.eu. The rate cycle that peaked in 2023 allowed banks that offer variable-rate and term deposits to expand net interest margins, and while the 2024 easing path compressed deposit betas, portfolio mix, and pricing discipline supported resilient margins. The operational priority in 2026 is to stabilize deposit depth and direct inflows toward higher-yielding assets with acceptable duration and risk. As conditions normalize, challengers are using interest-bearing products as the on-ramp and then encouraging customers to adopt subscription tiers and wealth or insurance features that raise switching costs beyond rate alone. That sequencing approach is central to sustainable unit economics in the Europe neobanking market.

Embedded-Finance/BaaS Revenue Pipelines

Banking-as-a-Service enables retailers, software vendors, and platforms to embed accounts, cards, cross-border payments, and lending under their own brands while relying on licensed providers for compliance and infrastructure. Wise reported that platform partnerships now represent a measurable share of total cross-border volume, and it continues to embed multi-currency infrastructure into partner ecosystems, which underlines the pull for modular financial services across Europe [3]Wise plc, “H1 FY26 Results,” Wise plc, wise.com. The commercial model blends per-transaction fees, platform subscriptions tied to API load, and revenue shares on credit or foreign exchange spreads, which diversifies income beyond core consumer deposits and transfers. Capital requirements and risk-weight rules still shape the extent of on-balance-sheet activity, especially where BaaS partners introduce credit exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU interchange-fee caps squeeze margins | - 1.6% | EU-wide, more acute in card-reliant markets | Long term (≥ 4 years) |

| Heightened AML and KYC compliance burden | - 1.3% | EU-wide, intensifying with a new regime | Medium term (2-4 years) |

| Fraud and false-positive spikes erode trust | - 0.9% | EU-wide, with heightened exposure in select corridors | Short term (≤ 2 years) |

| Secondary-account status limits deposit depth | - 1.2% | Euro area core, where product breadth is limited | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened AML/KYC Compliance Burden

European financial institutions continue to invest heavily in financial crime controls, with industry data showing material budgets allocated to KYC processes, documentation collection, and periodic reviews in 2025, which can slow onboarding and increase fixed costs for digital challengers. Technology modernization creates additional load, with reported project costs for AML reporting solutions ranging near USD 1.2 million using existing infrastructure or USD 1.0 million for in-house AI approaches in 2025, figures that shape investment priorities for growth-stage banks. Europe’s updated AML and CFT regime sets clearer supervisory expectations and immovable implementation dates through 2027, which require reinforced staffing, continuous monitoring, and documentation capabilities. As these requirements expand, neobanks must preserve instant onboarding while meeting stricter verification and monitoring standards that stretch operating models. This pressure elevates the need for automation and well-governed data pipelines in the Europe neobanking market.

Secondary-Account Status Limits Deposit Depth

ECB consumer research shows that in 2024, many users would allocate a small proportion of a new windfall to central bank digital money and that they would benchmark holdings primarily against monthly spending needs, which mirrors behavioral patterns in app-based accounts. The same surveys indicate a preference to pre-fund wallets with limited balances, while topping up from main current accounts only when needed, which constrains deposit depth for mobile-only providers. Europe Parliament analysis cautions that deposit bases concentrated in digital channels could be more flight-prone during stress, since customer relationships are less personal and more price sensitive in a multi-banking context. That risk reinforces the strategic need for product breadth in mortgages, pensions, and investments, ideally delivered in-app through licenses or partnerships. The banks that move users from secondary utility to primary relationship will sustain deeper balances and longer lifecycles in the European neobanking market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Account Type: Business Accounts Anchor Share, Savings Surge

Business accounts led the segment with 65.78% share in 2025, setting the tone for cash management, expense control, and multi-currency needs across SMEs that rely on seamless integrations with accounting and invoicing tools. Business users exhibit lower churn due to embedded workflows like card issuance, controls, and reconciliation that are costly to switch, and this underpins stable deposits and cross-sell potential. United Kingdom-focused research highlighted measurable GDP contributions from challenger lending in 2024, and one bank reported a USD 6.8 billion (GBP 5.8 billion) impact, which reflects the broader role of digital channels in SME finance within the Europe neobanking market. As firms standardize mobile-first banking for payables, receivables, and employee spend, the Europe neobanking industry uses tiered subscription models to bundle treasury services with analytics and dedicated support. Continued investments in security, data portability, and compliance tooling keep business accounts central to the Europe neobanking market.

Savings accounts are forecast to expand at 41.33% CAGR from 2026 to 2031, reflecting rate sensitivity and app-driven transparency that attract deposit inflows to instant-access and term products. Bank disclosures in 2025 highlighted accelerated deposit growth for digital-native providers as customers searched for yield and easy-to-manage products, and one United Kingdom institution reported USD 6.2 billion (GBP 5.3 billion) of savings balances at year end, reinforcing the appeal of mobile-first savings features. As price discovery improves through open finance tools, consumers respond faster to rate changes, which strengthens the role of agile pricing engines in retention. Product ramp strategies position interest-bearing accounts as the entry point and then layer budgeting tools, vaults, and investment options to broaden engagement. This sequence supports loan-led monetization while maintaining the trust needed to secure deeper deposits within the Europe neobanking market.

By Services: Mobile Banking Leads, Loans Accelerate Revenue Diversification

Mobile banking captured 46.84% of service-segment share in 2025 and remains the primary interface through which customers access payments, transfers, savings, and credit. Broader European usage data showed that the share of online and mobile usage for routine banking increased meaningfully into 2024, pointing to sustained engagement with digital channels through 2026. As instant notifications and near real-time clearing become normalized, customers expect balances, insights, and dispute workflows to operate inside the app with minimal friction. Payments and transfers retain utility value, while cross-border functionality differentiates based on transparency and delivered rates. With platform stickiness rising, mobile remains the anchor feature in the Europe neobanking industry and continues to drive acquisition and retention in the Europe neobanking market.

Loan services are projected to grow at a 43.13% CAGR through 2031, reflecting a pivot to balance-sheet intermediation that complements fee-based revenue. An SME-focused provider disclosed that its Partner Credit Services approached USD 2.7 billion (GBP 2 billion) in cumulative lending across multiple Europe markets by late 2025, illustrating how embedded finance can convert transaction data into working-capital solutions for small businesses. Cross-border payments infrastructure also supports credit origination for freelancers and exporters, and Wise reported strong growth in customers and cross-border volume, reinforcing the benefit of scale in delivering low-cost flows. The integration of affordability insights from open data, faster underwriting, and flexible repayment tools is now a standard expectation. Strong governance, transparent pricing, and data security will remain the foundation for loan-led growth inside the Europe neobanking market.

By Application: Enterprise Dominates, Personal Grows Faster

Enterprise applications accounted for 68.18% of usage in 2025, anchored by finance leaders who require multi-currency accounts, granular controls, and real-time reconciliation that integrates with ERP and expense platforms. Spend-management platforms illustrate the value of programmable cards, policy-based approvals, and automated receipt capture for mid-market companies that want centralized visibility and decentralized control. As enterprises standardize on mobile tools for treasury and payables, the Europe neobanking market benefits from contract-driven retention and embedded workflows that raise switching costs. The Europe neobanking industry has placed emphasis on data portability and audit-ready records, which improve customer confidence in compliance and reporting. Enterprise demand will continue to reinforce platform breadth and service quality in the Europe neobanking market.

Personal applications are projected to grow at a 38.44% CAGR through 2031, supported by younger cohorts who now expect mobile onboarding, instant payments, budgeting tools, and alerts packaged in a single app. Digital sub-brands within universal banks show the potential to onboard new-to-bank users at scale, as one Europe bank’s app-only offering surpassed 800,000 users by late 2024 in Italy and targeted 1 million by 2026, which helps the parent cross-sell mortgages and investments over time [4]BBVA, “BBVA Italy Expands Its Investment and Lending Offering to Reach One Million Customers by 2026,” BBVA, bbva.com. In Spain, CaixaBank reported that its imagin brand contributed significantly to net customer additions in 2025 and gained a visible share of payroll accounts among younger users, an outcome that signals brand-led trust in digital services. As household formation and earning power rise, customers look for home financing, investments, and family features in the same digital environment. This is the inflection where secondary accounts can transition to primary relationships in the Europe neobanking market.

Geography Analysis

The United Kingdom accounted for 27.97% of the Europe neobanking market size in 2025, supported by a policy environment that fosters secure data sharing and payment initiation under strong supervisory oversight. Challenger-led SME finance has been material to the broader economy, and one lender estimated a USD 7.8 billion (5.8 billion) GDP impact in 2024, which reflects how digital channels support smaller firms with targeted credit and working-capital tools. The United Kingdom’s financial technology ecosystem remains export-oriented and capitalized to pursue multi-country growth through 2026. Scale players are diversifying into business accounts, investing, and travel services, which broadens engagement and revenue stability across cycles. With stronger customer familiarity and a dense partner network, the United Kingdom remains an anchor geography in the Europe neobanking market.

Spain is forecast to lead growth with a 34.43% CAGR from 2026 to 2031, underpinned by a strong pipeline of mobile-first offerings from established banking groups and standalone challengers. CaixaBank reported that imagin contributed significantly to net new customer growth in 2025, while also gaining a visible share of payroll account openings among younger cohorts, which demonstrates efficient customer acquisition at scale. Platform breadth, lifestyle integrations, and commission-free features are helping digital brands capture primary account roles for younger users. With payments modernization and digital skills improving, providers can expand from transactional utility to multi-product relationships. These elements set the stage for durable expansion inside the Europe neobanking market.

Germany continues to host one of Europe’s largest financial technology ecosystems with a full spectrum of payment, banking, and infrastructure specialists, supported by a national trade and investment agenda that tracks the sector’s expansion. Regulatory consistency and operational resilience remain priorities for both incumbents and challengers in 2026, with a focus on risk controls that scale in pace with customer growth. The Nordics, Benelux, France, and Italy continue to diversify demand, each with national nuances in instant payments and open data adoption. Company disclosures signal momentum across cross-border transfers, savings products, and SME finance. With around 60 digital-only banks active in the euro area as of end-2024 and a measurable share of banking assets in digital channels, providers have a platform to scale multi-product engagement through 2031 in the Europe neobanking market.

Competitive Landscape

The competitive field shows moderate fragmentation in 2026, and the Europe neobanking market supports specialist models that can scale without aggressive price competition across identical products. Revolut completed a share sale in November 2025 at a USD 75 billion valuation, citing strong 2024 revenue and profit growth as it adds trading, travel, and insurance features alongside payments and business accounts, which demonstrates the monetization potential of a multi-product model. Product breadth and geographic reach continue to drive unit economics as cohorts adopt more services over time. The largest providers are demonstrating that diversification and operating leverage can support expansion across cycles. These dynamics set the tone for capital allocation and product sequencing in the Europe neobanking market.

Cross-border infrastructure remains a differentiator for scalable players, and Wise reported strong gains in customers, balances, and volumes during Q3 FY26, while also advancing regulated permissions in new geographies, which expands the network of partners that embed its multi-currency capabilities. N26 continued its governance evolution with a leadership transition announced in December 2025 and previously completed a legal transformation into a European Company in January 2025, moves that align the organization with long-term, multi-country expansion. These steps emphasize institutionalization, which is essential for scaling resilient operations in the Europe neobanking market.

Specialists continue to broaden product and geographic scope. Tide reported material progress in 2025 on funding and lending volumes while expanding to new EU markets for SME services, reinforcing embedded-credit strategies within digital accounts. Lunar raised USD 54.1 million (EUR 46 million) in January 2026 to support Nordic expansion and profitability efforts, which underlines continued investor conviction in focused regional strategies. Neobanks are also expanding family features and youth offerings to anchor lifelong relationships, as seen in new product launches in early 2026. Together, these moves highlight the steady broadening of addressable use cases in the Europe neobanking market.

Europe Neobanking Industry Leaders

Revolut

Starling Bank

Monzo Bank Ltd

N26 GmbH

Wise plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lunar secured USD 54.1 million (EUR 46.0 million) to accelerate Nordic expansion, scale business banking operations, and enhance its lending offerings, reinforcing its position as a leading challenger bank in the region.

- January 2026: N26 launched “N26 for under 18s,” its first family offering with a debit card for children aged 7 to 17, targeting millennial parents seeking digital financial literacy tools and parental spending controls within a unified household account ecosystem. The feature set includes spend limits and visibility for guardians. The release extends relationship coverage across household members.

- December 2025: Wise received conditional approval from the South African Reserve Bank to operate as a Category 2 Authorized Dealer with Limited Authority, marking Wise’s first regulatory approval in Africa and extending its cross-border payment network into Sub-Saharan markets. The firm noted that the approval would allow expanded services in the future, subject to final conditions. The move shows continued geographic diversification of regulated permissions.

- November 2025: N26 expanded its product portfolio by launching personal loans for customers in Spain, diversifying revenue beyond interchange and subscription fees through balance-sheet lending funded by deposit inflows and underwritten via open-banking transaction-data analytics. The launch advances the shift to interest-based income streams. It also addresses the demand for flexible personal credit within the app.

Europe Neobanking Market Report Scope

Neo-banking refers to digital-only financial service providers operating exclusively online without physical branches. These fintech entities, also known as challenger banks, offer services such as account management, payments, and lending through mobile applications, delivering a cost-effective, efficient, and seamless alternative to traditional banking.

The Europe neobanking market report is segmented by account type (business account, savings account), services (mobile-banking, payments, money-transfers, savings account, loans, others), application (personal, enterprise, other application), and geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The market forecasts are provided in terms of value (USD).

By Account Type

| Business Account |

| Savings Account |

By Services

| Mobile-Banking |

| Payments |

| Money-Transfers |

| Savings Account |

| Loans |

| Others |

By Application

| Personal |

| Enterprise |

| Other Application |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Account Type | Business Account |

| Savings Account | |

| By Services | Mobile-Banking |

| Payments | |

| Money-Transfers | |

| Savings Account | |

| Loans | |

| Others | |

| By Application | Personal |

| Enterprise | |

| Other Application | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe neobanking market growth outlook to 2031?

The Europe neobanking market is projected to grow from USD 4.1 billion in 2026 to USD 8.0 billion by 2031 at a 14.2% CAGR, supported by mobile-first adoption and broader open-finance data access.

Which customer application is expanding the fastest in Europe?

Personal-use applications are advancing the fastest with a projected 38.44% CAGR through 2031, helped by mobile onboarding, instant payments, and the shift of younger cohorts to primary app-based banking.

Which service lines are leading, and which are scaling the most quickly?

Mobile banking leads with 46.84% segment share in 2025, while loans are projected to post the highest growth at a 43.13% CAGR through 2031 as providers diversify into balance-sheet products.

What are the key restraints on profitability for European neobanks?

Interchange-fee caps reduce card-led revenue, while AML and KYC obligations, fraud losses and false positives, and secondary-account behavior raise costs and limit deposit depth across 2026.

Which geographies are most important for expansion?

The United Kingdom leads by share with 27.97% in 2025, while Spain is expected to lead by growth with a 34.43% CAGR during 2026 to 2031, reflecting strong digital-brand momentum and open-data progress.

How are leading players strengthening their positions?

Scale providers are adding products and licenses and pursuing partnerships, as seen in Revolut's 2025 share sale, Wises regulatory advances and network growth, N26s governance updates, and Lunar and Tides capital and lending expansions.

Page last updated on: