Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

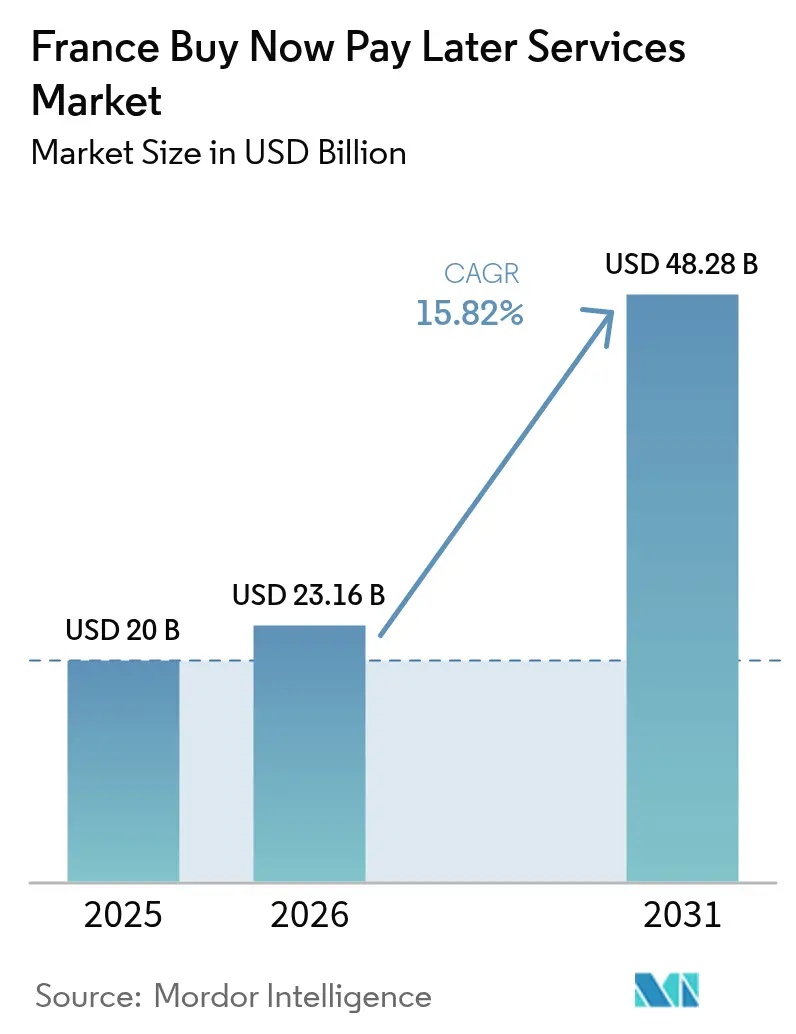

| Base Year Market Size (2025) | USD 20 Billion |

| Market Size (2026) | USD 23.16 Billion |

| Market Size (2031) | USD 48.28 Billion |

| Growth Rate (2026 - 2031) | 15.82% CAGR |

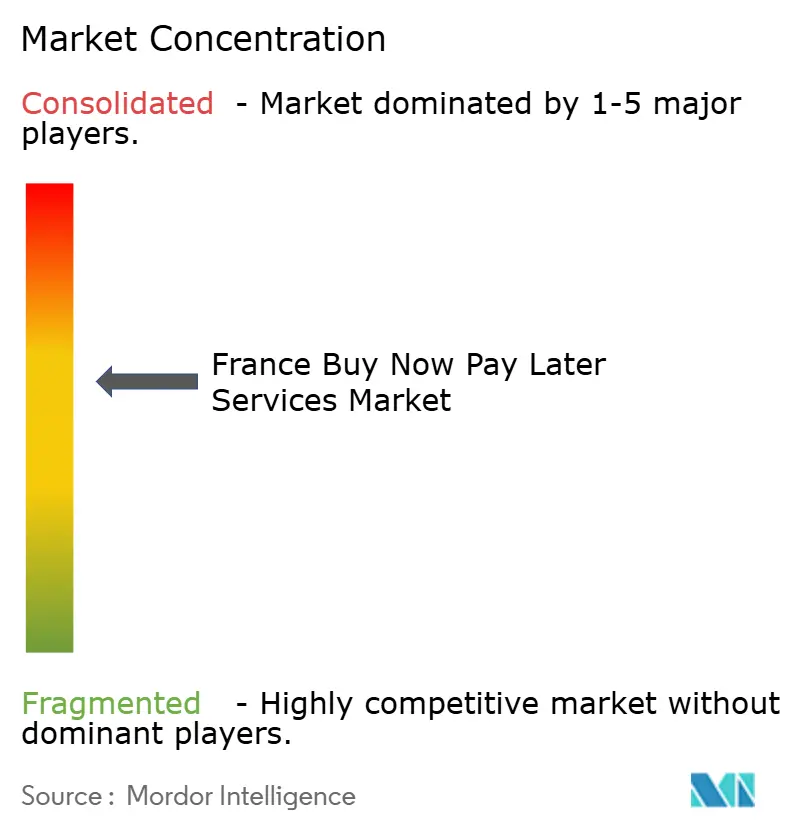

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Buy Now Pay Later Services Market Analysis by Mordor Intelligence

The France BNPL services market size was valued at USD 20 billion in 2025 and estimated to grow from USD 23.16 billion in 2026 to reach USD 48.28 billion by 2031, at a CAGR of 15.82% during the forecast period (2026-2031). Expansion rests on five pillars: merchants looking for cheaper acceptance after interchange-fee caps, consumers managing tight household budgets, instant-payment rails lowering funding costs, large marketplaces embedding BNPL APIs, and banks scaling low-cost balance-sheet lending. Competition remains intense as fintechs refine risk analytics while incumbent banks cross-sell to cardholders. Regulation increases complexity; CCD2 compliance forces fuller credit checks that raise costs, yet should improve long-run trust in providers. Technology upgrades—Carte Bancaire tokenisation, biometric authentication, and mobile in-app roll-outs—are lowering fraud and boosting checkout conversion. Neo-banks reach digital natives, whereas cost-of-living pressures extend BNPL into semi-essential categories, keeping demand resilient across economic cycles.

Key Report Takeaways

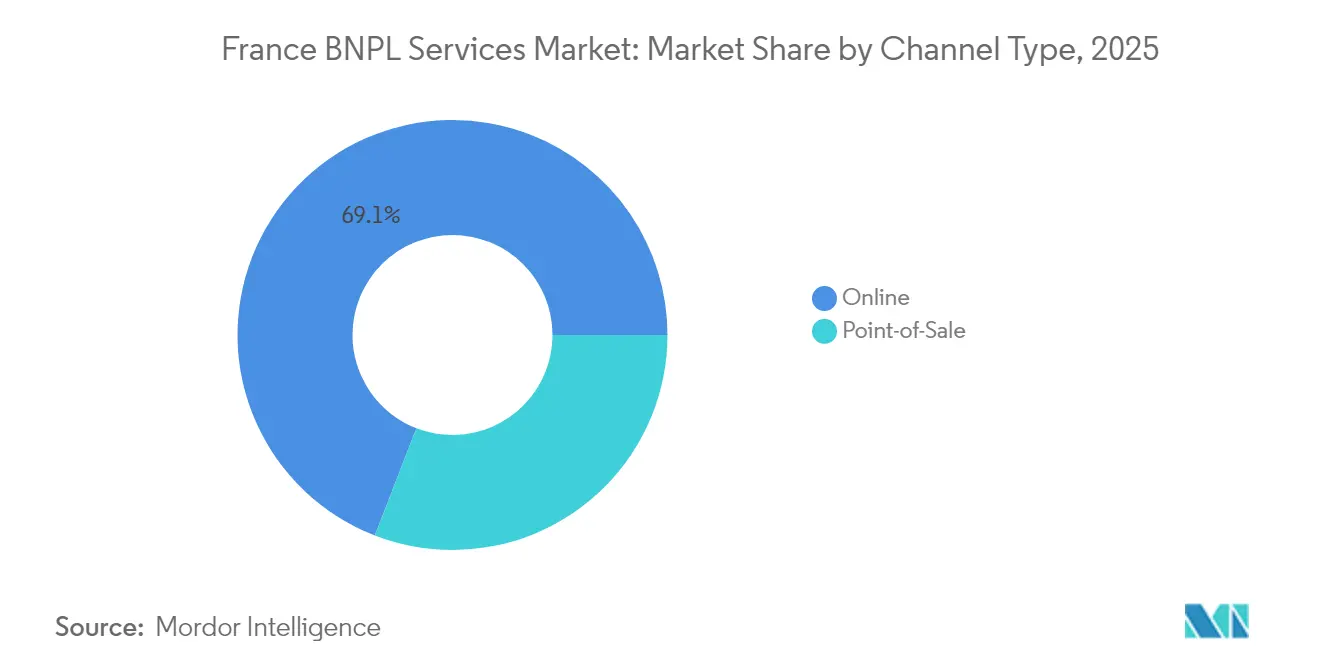

- By channel, online checkout commanded 69.12% of the France BNPL services market share in 2025, while in-store solutions are projected to expand at an 17.6% CAGR through 2031.

- By end-use industry, fashion & apparel led with 32.10% of the France BNPL services market share in 2025; travel & leisure is forecasted to grow at a 18.55% CAGR to 2031.

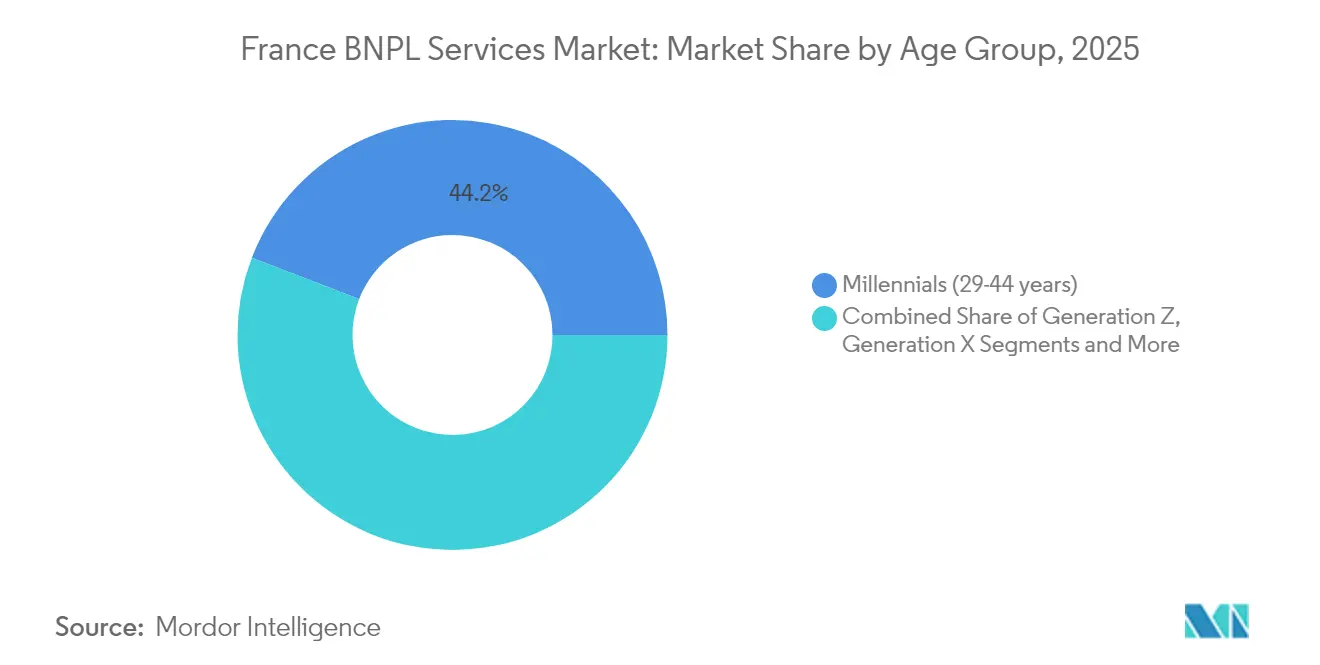

- By age group, millennials captured 44.15% of the France BNPL services market size in 2025; generation Z posts the fastest 18.92% CAGR.

- By provider type, fintech specialists held 59.45% share of the France BNPL services market size in 2025; they are set to post the highest 17.25% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Buy Now Pay Later Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-of-living squeeze boosting demand for short-term interest-free credit | +4.0% | National, stronger in urban zones | Short term (≤ 2 years) |

| BNPL API integration by major French marketplaces (Cdiscount, La Redoute) | +3.3% | France, concentrated in large e-commerce hubs | Short term (≤ 2 years) |

| Neo-bank in-app BNPL roll-outs (Lydia, Nickel) | +3.4% | National, tech-savvy demographics | Medium term (2-4 years) |

| Tightening of interchange-fee caps prompting merchant BNPL adoption | +2.7% | France with spillover across EU | Medium term (2-4 years) |

| Expansion of Carte Bancaire e-commerce tokenisation | +2.2% | France, primarily urban centres | Short term (≤ 2 years) |

| ECB/BoF instant-payment rails (TIPS) improving provider liquidity | +2.5% | France plus Eurozone | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-of-living squeeze boosting demand

Elevated inflation keeps French household budgets under pressure in 2025, turning zero-interest instalments from a novelty into a necessity. BNP Paribas recorded 43% European usage in 2024, a 22% jump on 2023, while Capgemini showed 70% adoption among French shoppers. Floa found BNPL utilisation for groceries and utilities rising 34%. Repeat usage lengthens customer lifecycles and raises lifetime value, even as average ticket sizes dip. Merchants in food, pharmacy, and utilities now present BNPL alongside cards, cementing mainstream status. Banque de France data indicate delinquencies remain manageable thanks to tighter, data-rich underwriting.

BNPL API integration by major French marketplaces

Cdiscount and La Redoute standardised BNPL APIs in 2024, streamlining onboarding for 15,000 merchants. Mollie credits this rollout with lifting BNPL availability to 42% of French online shoppers, up from 28% in 2022. Integration times fell 60%, unlocking broader verticals such as hardware and cosmetics. Worldline reports tokenised BNPL baskets running 20-25% above card equivalents. Providers also harvest richer data, improving risk scoring and enabling tailored repayment plans.

Neo-bank in-app BNPL roll-outs widening reach

Lydia and Nickel embed instalments within everyday banking apps, offering 8 million users a single-click path to credit. Lydia says 38% of its customers activated BNPL within six months, trimming acquisition cost by 62%. Proprietary current-account data halves fraud triggers and cuts default rates 40% versus market averages. Neo-banks also cater to lightly banked regions with limited card penetration, broadening inclusion and adding a sustained 3.4% lift to France's BNPL services market growth through 2029.

Tightening interchange-fee caps prompting merchant adoption

EU-wide caps hold credit-card fees at 0.3% and debit fees at 0.2%, narrowing acquirer margins. BNPL charges around 4%, yet merchants still benefit because conversion rises 30% and average basket values climb 45%, according to BNP Paribas. Mid-tier retailers that once balked at card costs now view BNPL as a growth lever, especially in electronics and home furnishings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transposition of EU CCD2 raising compliance costs | -2.0% | France and EU | Medium term (2-4 years) |

| High default rates in sub-prime segments | -2.3% | National, economically challenged regions | Short term (≤ 2 years) |

| CNIL data-privacy enforcement limiting risk-scoring data | -1.6% | France, heavier for cross-border providers | Medium term (2-4 years) |

| ACPR scrutiny on capital adequacy for non-bank players | -1.3% | France, particularly fintechs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU CCD2 transposition is increasing compliance costs

CCD2, due in French law by November 2025, brings stricter credit checks and disclosure mandates. Hogan Lovells highlights the removal of minimum loan thresholds and repayment windows capped at 50 days. Oliver Wyman forecasts 15-20% cost inflation for smaller providers. Compliance burdens could force consolidation, diminishing provider diversity yet improving transparency.

High default rates in sub-prime segments

Aggregate BNPL delinquencies stay near 2.1%, but Rothschild & Co. and the EBA flag rising stress in lower-income regions[1]European Banking Authority, “Risk Assessment Report 2024,” eba.europa.eu. OECD modelling shows stricter underwriting could exclude 18-22% of applicants[2]OECD, “Consumer Finance Risk Monitor 2024,” oecd.org. Providers have tightened scorecards, adding up-front deposits and shorter tenors, trimming the addressable pool, and subtracting a part from the France BNPL services market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Online dominance challenged by in-store growth

Online transactions comprised 69.12% of the France BNPL services market in 2025, supported by frictionless widgets and biometric login. Checkout.com places BNPL at 5.1% of global e-commerce value, with France above the continental average. One-click tokenisation cuts checkout abandonment, while cross-border localisation broadens merchant reach. The France BNPL services market size for online payments is projected to expand at 15.18% CAGR through 2031 as 5G penetration deepens and social-commerce links proliferate.

Point-of-sale BNPL, although nascent, logs an 17.6% CAGR. Worldline says 42% of physical retailers now offer instalments, up from 18% in 2022. Upgraded terminal firmware and QR code options enable paperless enrolment, and Edgar Dunn & Company reports ticket uplifts of 20% in DIY outlets. By 2031, in-store transactions could account for 39.20% of France BNPL services market share if NFC-enabled phones become universal.

By End-Use Industry: Fashion leads while travel accelerates

Fashion & apparel commanded 32.10% of the France BNPL services market size in 2025, buoyed by high return rates and “try now pay later” propositions. McKinsey highlights the growing adoption of Buy Now Pay Later (BNPL) options among French fashion chains, with 68% of these chains now offering at least one BNPL solution. This payment method has gained traction due to its higher transaction value, which is significantly above traditional card purchases. Furthermore, the implementation of automated refund-against-installment processes has streamlined operations and reduced costs. The BNPL segment is expected to experience robust growth, supported by its increasing popularity among mid-range brands.

Travel & leisure is the fastest-growing category with a 18.55% CAGR. Floa observes an 85% jump in BNPL bookings in 2024, with average transaction values near EUR 850 (USD 929 million). Flexible plans encourage consumers to lock in itinerary spend earlier, boosting occupancy for hotels and tour operators. Ancillary revenues, such as seat upgrades, enlarge provider fee pools, lifting France's BNPL services market share for the vertical.

Healthcare & wellness and home improvement tuck in with 16.52% and 15.05% CAGRs. Dental chains, optical boutiques, and vet clinics pitch six-month plans to spread essential outlays, while hardware stores pair BNPL promotions with energy-efficiency home upgrades.

By Age Group: Millennials dominate, Gen Z surges

Millennials held 44.15% of France's BNPL services market share in 2025, supported by established incomes and bigger ticket sizes. BNP Paribas lists an average BNPL basket of EUR 285 (USD 312 million) for this cohort. Family-formation pressures spur demand for furniture and daycare subscriptions spread over multiple instalments. Providers favour the cohort’s repayment reliability, keeping approval rates high.

Generation Z posts a 18.92% CAGR on digital-native behaviours. Capgemini finds 46% of French Gen Z buyers check out directly from social feeds. Embedded BNPL widgets in influencer storefronts mesh with their impulse-buy mindset, though ticket values average EUR 125 (USD 137 million). As Gen Z’s income climbs, their share of the France BNPL services market size will expand in tandem. Generation X and baby boomers adopt BNPL mainly for healthcare and home upgrades, demonstrating widening multigenerational appeal.

By Provider: Fintech leadership amid banking push

Fintechs retained 59.45% of France BNPL services market share in 2025. Alma’s partnership with Mollie enrolled 19,000 merchants and 6.8 million shoppers, lifting sales 20%. Klarna localised its French app, adding chatbots that cut service handle time by 35%. Product agility—split-payment scheduling and carbon-footprint tracking—differentiates fintechs, undergirding a 17.25% CAGR through 2031.

Banks control a 33.12% share, leveraging cheap deposits and broad client bases. BNP Paribas’s Floa unit saw 32% production growth in Q1 2025. Crédit Agricole’s joint venture with Worldline unites acquiring rails and branch distribution, broadening physical-merchant reach. Greater regulatory capital strength provides buffers against CCD2 compliance shocks, suggesting bank shares could rise steadily within the France BNPL services market.

Retailer-run instalment programs and niche credit providers occupy a 7.43% share but face rising compliance costs. M&A is accelerating: Crédit Agricole bought Pledg to internalise its merchant pipeline. Younited Credit’s SPAC listing opens liquidity for tech upgrades.

Geography Analysis

Paris and Île-de-France deliver 37.62% of BNPL transaction volume, reflecting e-commerce dominance and 100% fibre coverage. Dense delivery networks and high smartphone usage drive adoption, with click-and-collect BNPL services cutting last-mile costs.

Provence-Alpes-Côte d’Azur and Occitanie record 27.4% and 25.2% growth respectively, fuelled by tourism spending packaged with instalment offers. BNPL options for holiday rentals, ferry tickets, and festival passes broaden seasonal demand windows, boosting local SME revenue.

The north-east lags but offers untapped potential. Providers partner with chambers of commerce to onboard artisanal merchants, while mobile risk models accommodate irregular agricultural incomes. Cross-border activity matters: J.P. Morgan shows 50% of French shoppers purchase from China, the UK, and Germany, often via BNPL wallets. The Paypers stresses local-method acceptance in overseas carts, reinforcing the need for multilingual, multicurrency BNPL plugs.

Competitive Landscape

Leading providers dominate a significant portion of France's BNPL services market volume, indicating moderate concentration. Alma rolls out dynamic spending limits tied to real-time income feeds, cutting defaults by 18%. Klarna pilots carbon-tracking to attract eco-minded consumers. BNP Paribas leverages 13,000 branches to introduce Floa POS plans in rural stores, deepening reach. Worldline and Crédit Agricole’s joint venture, slated for 2025, merges acquiring tech with bank distribution.

Consolidation speeds up as CCD2 raises thresholds: Crédit Agricole Consumer Finance bought Pledg, and Younited Credit went public to fund AI risk modelling. Emerging white-space niches include B2B BNPL and biometric wallet integration post-Digital Markets Act, now that Apple must open NFC to third parties.

France Buy Now Pay Later Services Industry Leaders

Alma

Klarna

Paypal

Oney Bank

Floa Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Worldline and Crédit Agricole formed a joint venture to create a merchant-services heavyweight slated for launch in 2025.

- January 2025: Mollie integrated Alma, enabling e-merchants to offer 3- or 4-part instalments, achieving 89% conversion.

- January 2025: Younited Financial completed its business combination with Iris Financial, listing on Euronext Amsterdam and Paris.

- April 2024: Groupe BPCE enhanced its consumer-loan suite with instant personal loans and digital revolving credit.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the France buy now, pay later market as the total gross merchandise value of short-term, interest-free installment plans (typically pay-in-3 or pay-in-4) offered at checkout by fintechs, banks, and card networks across online and physical points of sale.

Scope exclusion: Long-duration consumer loans exceeding twelve monthly installments and revolving credit cards are not counted within this market.

Segmentation Overview

- By Channel

- Online

- Point-of-Sale (In-store)

- By End-Use Industry

- Consumer Electronics

- Fashion & Apparel

- Healthcare & Wellness

- Home Improvement

- Travel & Leisure

- Media & Entertainment

- Other End-Use Industries

- By Age Group

- Generation Z (18-28 Years)

- Millennials (29-44 Years)

- Generation X (45-60 Years)

- Baby Boomers (61-79 Years)

- Silent Generation (80 Years and Above)

- By Provider

- Fintechs

- Banks

- Others

Detailed Research Methodology and Data Validation

Primary Research

Analysts held structured interviews with BNPL executives, tier-1 and SME merchants, consumer-finance lawyers, and Paris-based regulators. They then ran short surveys among Millennial and Gen Z shoppers nationwide. These discussions helped us validate usage frequency, average ticket sizes, and likely CCD2 compliance costs before finalizing assumptions.

Desk Research

We begin by mining trustworthy public datasets such as Banque de France consumer credit releases, FEVAD e-commerce turnover surveys, Eurostat household expenditure panels, ACPR compliance filings, and IMF macro indicators. We then enrich them through news and company filings captured in Dow Jones Factiva, D&B Hoovers, and BuiltWith merchant analytics. Government import-export logs, OECD household debt tables, and trade association white papers on retail payments further anchor historic penetration, pricing spreads, and delinquency ratios. These examples illustrate the open-source backbone; numerous additional references supported data collection, verification, and clarification.

A second sweep uses France's patent office registers, CCD2 consultation papers, and Questel's patent families to gauge innovation velocity, while press archives track launch timelines and fee structures that influence adoption curves.

Market-Sizing & Forecasting

We apply a top-down reconstruction. National online and in-store retail sales are segmented, BNPL penetration rates are modeled from payment-method splits, and transaction values are adjusted for average installment cycle length. Select bottom-up checks, such as reported volumes from leading providers and sampled merchant counts, keep totals realistic and expose outliers. Inputs most sensitive to growth, such as youth debit card penetration, smartphone wallet usage, interchange fee caps, unemployment trends, and CCD2 phased enforcement, feed a multivariate regression that projects values to 2030. Where provider disclosure is thin, gaps are bridged using calibrated adoption proxies from comparable retail verticals.

Data Validation & Update Cycle

Mordor analysts triangulate every output against independent payment volumes and household credit balances. They then escalate anomalies for peer review. Models refresh annually, with interim adjustments triggered by material events, ensuring clients receive the latest vetted view.

Credibility Anchor: Why Our France Buy Now Pay Later Services Baseline Commands Confidence

Published estimates often vary because firms choose dissimilar scopes, reference years, and adoption multipliers. We disclose our variables, refresh cadence, and validation tests so decision-makers see exactly how our USD 20 billion 2025 benchmark emerged.

Key gap drivers include narrower e-commerce-only scopes, earlier base years, and untested survey samples used by other studies, which tend to pull their totals lower than ours.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20 B (2025) | Mordor Intelligence | |

| USD 8.9 B (2024) | Regional Consultancy A | Excludes in-store BNPL and bank-run plans; relies on limited merchant survey |

| USD 3.92 B (2023) | Trade Journal B | Uses pre-launch base year and extrapolates growth without channel validation |

The comparison shows how Mordor Intelligence balances comprehensive scope with current-year data and cross-checks, giving stakeholders a transparent, reproducible baseline they can trust for strategic planning.

Key Questions Answered in the Report

What is the 2026 value of the France BNPL services market?

It stands at USD 23.16 billion and is forecast to reach USD 48.28 billion by 2031.

Which sales channel leads BNPL adoption in France?

Online checkouts hold 69.12% share, although in-store options grow fastest at an 17.6% CAGR.

Which demographic group drives the most BNPL volume?

Millennials account for 44.15% of volume, while Generation Z is expanding quickest at a 18.92% CAGR.

How will EU CCD2 reshape the BNPL landscape?

CCD2 enforces stricter credit checks and disclosures, raising operating costs by up to 20% and encouraging market consolidation post-2025.

Why are merchants embracing BNPL despite higher fees than cards?

Instalments raise conversion rates by 30% and average basket values by 45%, offsetting fee differentials and lifting revenue.

Which industry vertical shows the fastest BNPL growth?

Travel & leisure is projected to log a 18.55% CAGR to 2031 as flexible plans encourage higher-value bookings.

Page last updated on: