Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

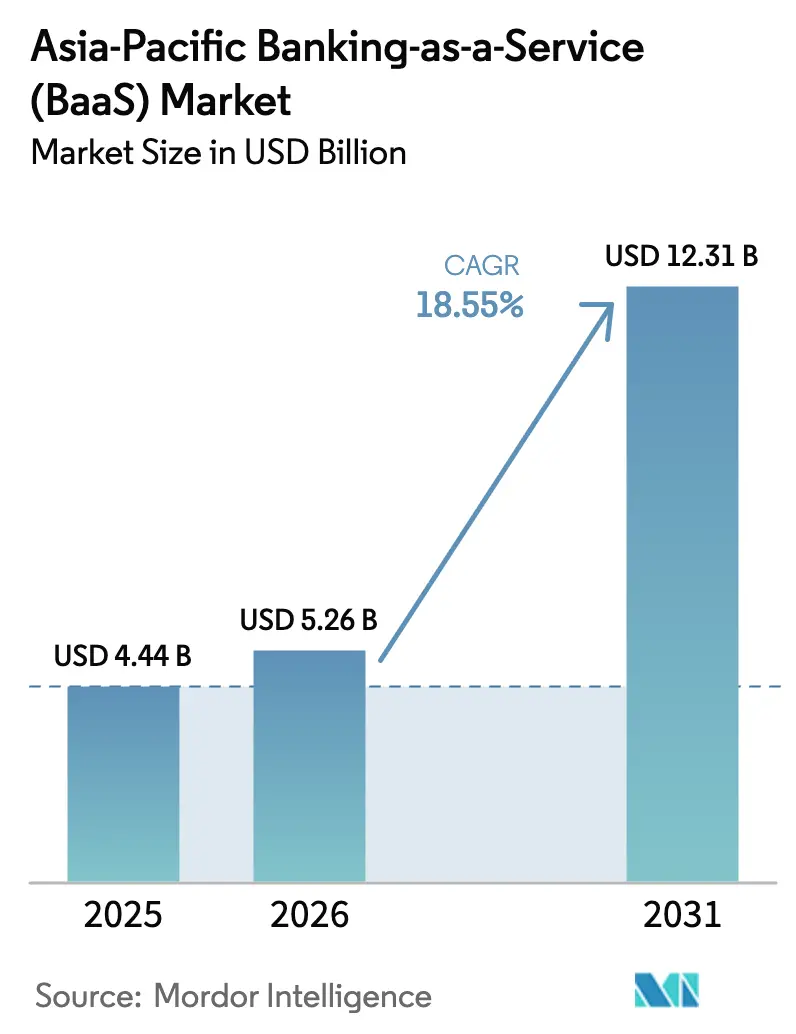

| Base Year Market Size (2025) | USD 4.44 Billion |

| Market Size (2026) | USD 5.26 Billion |

| Market Size (2031) | USD 12.31 Billion |

| Growth Rate (2026 - 2031) | 18.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Banking-as-a-Service (BaaS) Market Analysis by Mordor Intelligence

The Asia-Pacific Banking as a Service market size in 2026 is estimated at USD 5.26 billion, growing from 2025 value of USD 4.44 billion with 2031 projections showing USD 12.31 billion, growing at 18.55% CAGR over 2026-2031. This market size reflects the region’s rapid shift toward API-driven financial infrastructure, where traditional banks increasingly monetize core systems through white-label services and fintech platforms embed banking functions directly into customer workflows. The confluence of proactive open-banking regulation, the surge in real-time payment rails, and the spread of low-code development tools is restructuring financial service delivery models at speed. Incumbent institutions are responding by building API marketplaces, while tier-2 and tier-3 banks turn balance sheets into revenue-generating BaaS channels. Fintech demand for embedded payments, KYC automation, and digital lending modules continues to outpace expectations, creating positive network effects that compound existing growth drivers. As a result, strategic partnerships between banks, infrastructure vendors, and hyperscale cloud providers are becoming the centerpiece of the Banking as a Service market rather than isolated corporate initiatives.

Key Report Takeaways

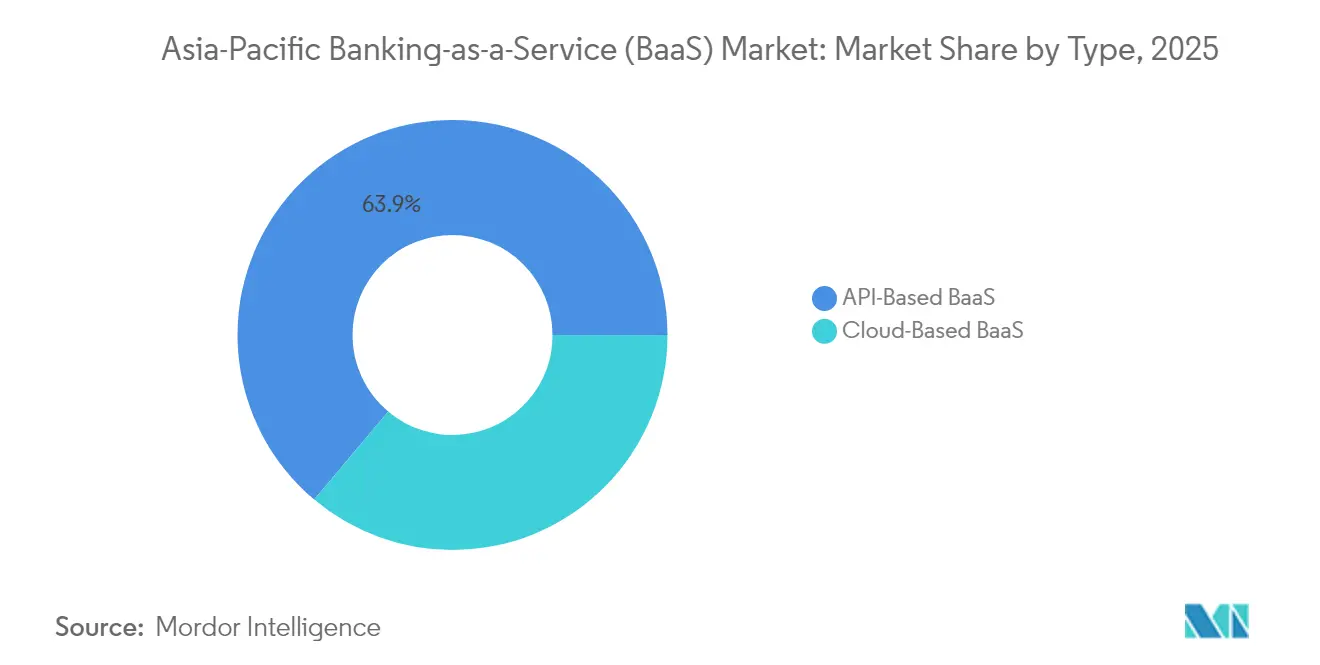

- By type, the API-based segment commanded 63.88% of the Asia-Pacific Banking as a Service market share in 2025; the cloud-based segment is projected to advance at 22.95% CAGR to 2031.

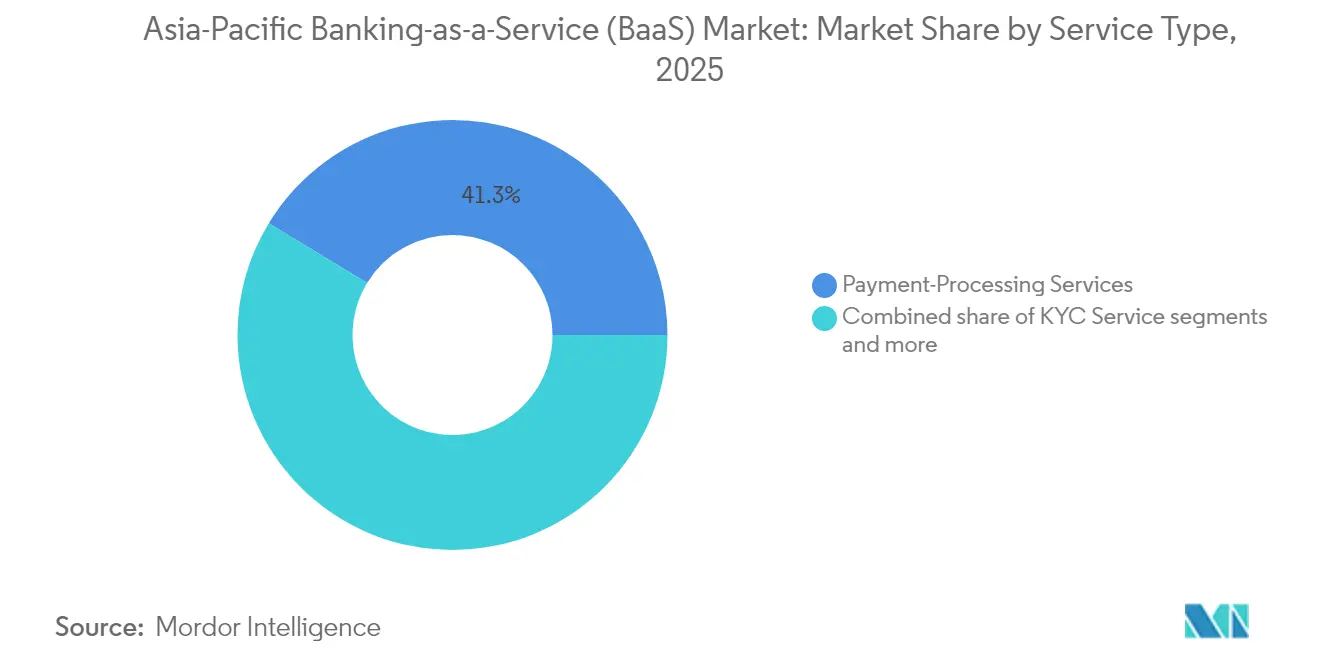

- By service type, payment-processing services led with 41.30% of the Asia-Pacific Banking as a Service market share in 2025, whereas KYC services are on track for a 25.35% CAGR through 2031.

- By enterprise size, large enterprises accounted for 54.60% of the Asia-Pacific Banking as a Service market share in 2025, yet SMEs represent the fastest-growing cohort at 19.05% CAGR to 2031.

- By geography, China held a 31.85% of the Asia-Pacific Banking as a Service market share in 2025, while India is forecast to expand at a 20.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Banking-as-a-Service (BaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating open-banking & regulatory support | +3.2% | India, Singapore, Australia, Philippines | Medium term (2-4 years) |

| Embedded-finance demand from e-commerce & super-apps | +4.1% | China, Southeast Asia, India | Short term (≤ 2 years) |

| Expansion of real-time payment rails | +3.8% | India, Singapore, Thailand, Malaysia | Short term (≤ 2 years) |

| Cloud-infrastructure cost reduction | +2.9% | Pan-regional | Long term (≥ 4 years) |

| Tier-2/3 banks monetizing balance sheets | +2.4% | India, Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Low-/no-code toolkits for SME integrations | +2.1% | Urban APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Open-Banking & Regulatory Support Across APAC

Regulators across APAC increasingly require banks to expose standardized APIs, turning former compliance obligations into commercial opportunities for BaaS vendors. India’s Account Aggregator framework processed 1.2 billion data requests in 2024, proving that mandated interoperability can scale securely[1]Reserve Bank of India, “Account Aggregator Framework – Implementation Guidelines,” RBI Press Release, rbi.org.in. . Singapore’s Monetary Authority updated third-party risk guidelines the same year, giving banks a formal playbook for partnering with fintechs. Australia expanded its Consumer Data Right beyond banking into energy and telecom, widening the addressable footprint for API-linked financial products. The Philippines and Malaysia launched open-finance roadmaps that echo European PSD2 objectives but adapt to local unbanked populations. As legal certainty rises, early-mover banks that already monetize APIs are enjoying recurring fee income, while late adopters risk customer attrition to digital-first competitors. The broader policy consensus now frames BaaS as an engine of financial inclusion rather than a threat to banking stability.

Rapid Rise of Embedded-Finance Demand from E-Commerce & Super-Apps

E-commerce giants and super-apps are embedding credit, insurance, and wealth products natively, forcing high-volume, low-latency API stacks into the spotlight. Grab’s financial arm processed USD 8.2 billion in transaction value during 2024 through BaaS partnerships, proving the model’s commercial viability. GCash, Alipay, and ShopeePay use the same approach to extend customer lifetime value beyond payments alone. Platform operators favor BaaS because it eliminates banking license complexity yet unlocks revenue-share economics that can exceed core marketplace margins. As cross-border shopping rises, super-apps also need multicurrency wallets and risk engines, further stimulating demand for regional payment orchestration APIs. The virtuous circle—more users, more data, more tailored products—cements embedded finance as the dominant distribution model in consumer segments across the Asia-Pacific Banking as a Service market.

Surge in Real-Time Payment Rails (UPI, PayNow, PromptPay)

Real-time payment systems are a catalyst for transaction-heavy BaaS services. India’s UPI handled 14.44 billion transactions worth USD 200 billion in December 2024 alone, stretching incumbent switch infrastructure and creating monetization room for API-native processors[2]National Payments Corporation of India, “UPI Product Statistics December 2024,” npci.org.in. . Singapore’s PayNow and Thailand’s PromptPay connect via Project Nexus, giving fintechs a regional instant-transfer backbone without bilateral clearing agreements. BaaS players capitalize by bundling settlement, FX, and compliance features around these RTP rails, effectively offering a one-stop gateway. Banks leverage external APIs for overflow capacity during festival peaks, offloading both operational risk and cost. Consequently, payment-processing remains the lead revenue driver across the Asia-Pacific Banking as a Service market even as margins compress, because scale volumes more than offset fee pressure.

Cloud-Infrastructure Expansion Lowering BaaS Deployment Costs

Hyperscaler investments in Jakarta, Kuala Lumpur, and Seoul remove latency bottlenecks and satisfy data-sovereignty rules, enabling cloud-native BaaS entrants to launch without owning physical data centers[3]Google Cloud, “Google Cloud Expands in Indonesia with New Jakarta Region,” cloud.google.com. . AWS, Google Cloud, and Azure now certify specialized financial-services regions with hardware security modules and regulatory attestations, lowering time-to-market by months. According to Infosys, cloud-based banking cores cut operating costs by 30-40% versus on-premise stacks. Smaller banks that struggled with capital expense are adopting “banking-in-a-box” solutions hosted in the region, democratizing access to sophisticated treasury, KYC, and ledger services. The cost deflation also fuels price competition, allowing BaaS providers to tier pricing for SMEs without sacrificing gross margin. Long-term, cloud ubiquity is expected to keep the Asia-Pacific Banking as a Service market on its high-growth trajectory even if topline API fees trend lower.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened regulatory scrutiny & third-party risk oversight | -2.8% | Singapore, Australia, India, Japan | Medium term (2-4 years) |

| Rising cybersecurity & data-localization compliance costs | -2.1% | China, India, pan-regional | Long term (≥ 4 years) |

| Legacy core-bank systems limiting API performance | -1.9% | Regional banks across Southeast Asia and Japan | Medium term (2–4 years) |

| Volatile VC funding constraining fintech client pipeline | -1.6% | APAC-wide, with pronounced impact in early-stage hubs like Singapore and Bengaluru | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Regulatory Scrutiny & Third-Party-Risk Oversight

Supervisors from Singapore’s MAS to Australia’s APRA now hold banks accountable for vendor resiliency, demanding deep audits of BaaS partners [4]\Monetary Authority of Singapore, “Guidelines on Technology Risk Management,” mas.gov.sg. . New frameworks require real-time visibility into uptime, penetration testing, and sub-processor chains, raising onboarding costs and lengthening procurement cycles. Japanese regulators proposed similar guidelines in late 2024, emphasizing board-level responsibility for outsourced IT. These measures protect consumers but introduce friction that may deter smaller institutions from adopting third-party cores. Compliance workloads often duplicate between bank and provider, eroding the time-to-profit advantage that once defined BaaS value. Over the medium term, intensified oversight will likely consolidate the Asia-Pacific Banking as a Service market around vendors with mature governance processes, thereby cooling headline CAGR by an estimated 2.8%.

Rising Cybersecurity & Data-Localization Compliance Costs

APAC jurisdictions are tightening data-residency and breach-notification rules, escalating capex for multi-region BaaS architectures. India’s Digital Personal Data Protection Act and China’s Cybersecurity Law force providers to establish local instances, sacrificing economies of scale. PwC’s 2024 survey reports 69% of financial-services executives boosting cyber outlays by over 10% YoY, with API security the fastest-expanding line item. Smaller vendors lacking global SOC teams face an uneven burden, driving M&A as a survival strategy. Deployment delays of 6-12 months are common where security assessments are mandatory before launch. While these costs strengthen consumer trust, they also slow rollouts and compress margins, subtracting roughly 2.1% from forecast CAGR across the Asia-Pacific Banking as a Service market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: API-Based Dominance Drives Enterprise Adoption

API-based platforms captured 63.88% of the Asia-Pacific Banking as a Service market share in 2025, underscoring the value enterprises place on granular control and direct system-to-system integration. Large organizations favor endpoint modularity, which lets them mesh banking functions with existing ERP, treasury, and risk engines while preserving data sovereignty. In contrast, cloud-based platforms are winning digital-native customers at a 22.95% CAGR, leveraging pre-configured cores to compress product-launch cycles. DBS Bank’s marketplace alone lists more than 200 APIs, accounting for USD 25 million in annual revenue and validating demand for high-touch integration. The dichotomy mirrors broader IT adoption curves: incumbents retrofit API layers onto legacy systems, while challenger banks and fintechs jump straight to multitenant clouds. Temenos Banking Cloud logged 40% growth in new sign-ups during 2024, driven mainly by mid-market banks seeking turnkey BaaS entry. Regulators tend to prefer API-first models for their transparency, yet they now accept cloud equivalents provided robust audit trails exist. Consequently, the coexistence of both architectures will persist, ensuring that the Banking as a Service market retains multiple growth avenues rather than a single-technology path.

By Service Type: Payment Processing Leads While KYC Automation Surges

Payment-processing accounted for 41.30% market revenue in 2025 and remains the core monetization layer for most BaaS vendors. Transaction volume elasticity allows providers to price aggressively while cross-selling higher-margin services like FX conversion and settlement optimization. However, compliance automation is rising fastest, with the KYC category tracking a 25.35% CAGR as fintechs scale across borders. Brankas recorded a 180% spike in KYC API calls during 2024, reflecting this trend. Digital banking APIs covering account creation and ledger maintenance hold a meaningful share, buoyed by public-sector financial-inclusion campaigns in India and Indonesia. Customer-support APIs remain a niche but are gaining as enterprises realize that unified service experiences reduce churn. Emerging subsectors—credit scoring, fraud analytics, and tokenized-asset custody—sit in the “others” bucket but show promise as standalone lines once regulatory clarity improves. Collectively, the breadth of service demand signals that the Asia-Pacific Banking as a Service market is evolving from single-function gateways to full-stack financial infrastructure providers.

By Enterprise Size: SME Growth Accelerates Through Low-Code Integration

Large enterprises retained 54.60% of the Banking as a Service market size in 2025, driven by complex multi-region integrations and substantial transaction flow. Their projects often span digital-bank launches, supply-chain financing, and real-time treasury, locking in high average-contract values. Nonetheless, SMEs are the growth engine at 19.05% CAGR thanks to low-/no-code tools that reduce technical barriers to entry. Stripe’s simplified onboarding funnels empowered thousands of small sellers to embed split-payment and working-capital features during 2024, highlighting latent demand. SME adoption also benefits from subscription pricing that aligns with variable cash flow, unlike capex-heavy legacy solutions. Regulatory sandboxes in Singapore and Malaysia further ease experimentation by granting temporary exemptions from full licensing. Over the forecast horizon, SME penetration will likely raise competitive intensity, prompting vendors to differentiate on customer success, localized documentation, and vertical templates rather than pure API count. Despite this fragmentation, large-enterprise contracts will continue to anchor revenue stability for the Banking as a Service market.

Geography Analysis

China held 31.85% of the Asia-Pacific Banking as a Service market revenue in 2025, leveraging a mature super-app ecosystem and regulatory sandboxes that legitimize bank-fintech experimentation. Ant Group’s developer tools monetize Alipay’s payment rails while extending reach to provincial banks that lack digital muscle. Yet growth is moderating as new cybersecurity checks lengthen release cycles and data-interchange rules tighten. Domestic BaaS vendors are responding by exporting expertise to Belt-and-Road partner nations, sustaining regional influence even as home-market acceleration cools. India stands out as the fastest-growing territory, advancing at a 20.85% CAGR to 2031 amid exploding UPI volume and the Account Aggregator model that standardizes data portability. ICICI Bank’s 600-plus APIs show how incumbents pivot from branch expansion to platform distribution, unlocking USD 15 million in API fees while widening rural reach. The government's push for financial inclusion under the Jan Dhan Yojana keeps addressable demand high, and the recent Digital Personal Data Protection rules provide clear guardrails on localization without stifling innovation. These dynamics place India at the strategic center of the Banking as a Service market going forward.

Southeast Asia collectively offers the largest white-space opportunity. Singapore acts as a regional hub, providing regulatory clarity and cloud infrastructure, while neighbors such as Indonesia and Vietnam chase mobile-first consumers. The ASEAN Payment Connectivity initiative sets standardized cross-border API guidelines that lower technical friction. Malaysia’s DuitNow and Thailand’s PromptPay interoperability further underscore the role of real-time rails in catalyzing BaaS uptake. Australia and Japan remain important but slower-moving: their high-income demographics support premium BaaS use cases, yet conservative risk postures temper near-term velocity. Across the bloc, regional heterogeneity guarantees that the Asia-Pacific Banking as a Service market will evolve in staggered waves rather than a single uniform surge.

Competitive Landscape

The Asia-Pacific Banking as a Service (BaaS) market remains moderately fragmented, with the top five providers commanding a sizeable, though not overwhelming, portion of total industry revenue. Stripe leads the segment, with Ant Group and Airwallex close behind, each building on unique strengths. These major players distinguish themselves through wide-ranging API offerings, broad geographic footprints, and strong compliance frameworks that position them as preferred partners for multinational clients. In contrast, mid-sized firms are carving out their own space by specializing in underserved niches, such as cross-border disbursements, Islamic finance solutions, or SME invoicing tools. This mix of scale and specialization is shaping a dynamic, competitive environment across the region.

Strategic activity in 2024 highlighted the differing approaches among key players. Stripe’s acquisition of Bridge for USD 1.1 billion expanded its capabilities into stablecoin settlements, indicating a clear shift toward digital asset rails favored by global exporters. Airwallex focused on deepening its relationships with regional acquiring banks to enhance onshore licensing coverage and regulatory alignment. Ant Group introduced a high-volume AI risk engine that processes over a billion decisions daily, with exceptionally low fraud losses, demonstrating its emphasis on performance at scale. Meanwhile, traditional banks are staying in the game through partnerships—exemplified by HSBC’s collaboration with Ant International on tokenized deposit trials aimed at corporate treasury functions.

As competition intensifies, enterprise clients are placing increasing weight on technical certifications and service-level guarantees. Achievements such as ISO 27001, PCI-DSS, and SOC 2 compliance are becoming minimum requirements, while guaranteed uptimes and system responsiveness are emerging as new differentiators. Providers able to demonstrate ultra-low latency, geographic redundancy, and five-nines availability are winning higher-value contracts. At the same time, smaller players are pursuing vertical integration by embedding their services within sector-specific software like POS systems or logistics ERP platforms. These trends suggest that while the market will remain competitive, rising compliance costs and client expectations will gradually drive consolidation among providers.

Asia-Pacific Banking-as-a-Service (BaaS) Industry Leaders

Stripe

Ant Group (Alipay)

Airwallex

GrabFin

Rapyd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: HSBC partnered with Ant International to launch tokenized deposits for institutional clients across Asia-Pacific, enabling programmable money transfers through smart contracts that automate complex treasury operations. This collaboration demonstrates how traditional banks leverage fintech partnerships to offer innovative BaaS capabilities without building proprietary blockchain infrastructure.

- November 2024: Stripe acquired Bridge for USD 1.1 billion to enhance its stablecoin and cryptocurrency payment capabilities across APAC markets, positioning the company to capture growing demand for digital asset integration within BaaS platforms. The acquisition provides Stripe with blockchain infrastructure that enables cross-border payments with reduced settlement times and foreign exchange costs.

- October 2024: KPay raised USD 55 million in Series A funding to expand its BaaS platform across Southeast Asia, with specific focus on embedded lending and insurance products for e-commerce platforms. The funding round demonstrates investor confidence in vertical-specific BaaS solutions that address regional market needs through localized product offerings.

- September 2024: Grab injected USD 60 million into GXS Bank to accelerate digital banking services across Singapore and Malaysia, leveraging BaaS partnerships to offer embedded financial products within the Grab super-app ecosystem. This investment highlights how platform companies use BaaS infrastructure to monetize their customer base without obtaining banking licenses directly.

Asia-Pacific Banking-as-a-Service (BaaS) Market Report Scope

The banking as-a-services (baas) market is an end-to-end model that enables digital banks and other third parties to connect directly with bank systems via API, allowing them to build their banking offerings using the bank-regulated infrastructure while also unlocking the open banking opportunity and reshaping the financial services landscape.

The APAC banking-as-a-service market is segmented by type, by service type, by enterprise size, and by country. By service type the market is segmented into api-based baas and cloud-based baas). By service type, the market is segmented into payment process services, digital banking services, KYC services, customer support services, and others. By enterprise size, the market is segmented into large enterprises and small & medium enterprises. By country, the market is segmented into China, India, Japan, South Korea, Indonesia, Vietnam, Malaysia, Australia, New Zealand, and the rest of Asia-Pacific. The report offers market size and forecasts for the Asia Pacific banking as-a-services market in value (USD) for all the above segments.

By Type

| API-Based BaaS |

| Cloud-Based BaaS |

By Service Type

| Payment-Processing Services |

| Digital Banking Services |

| KYC Service |

| Customer Support Services |

| Others |

By Enterprise Size

| SMEs |

| Large Enterprises |

By Geography

| India | |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | Singapore |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

| By Type | API-Based BaaS | |

| Cloud-Based BaaS | ||

| By Service Type | Payment-Processing Services | |

| Digital Banking Services | ||

| KYC Service | ||

| Customer Support Services | ||

| Others | ||

| By Enterprise Size | SMEs | |

| Large Enterprises | ||

| By Geography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Banking as a Service market in Asia-Pacific?

The market is valued at USD 5.26 billion in 2026, with an 18.55% CAGR forecast toward USD 12.31 billion by 2031.

Which country is growing fastest in adopting Banking as a Service solutions?

India is the fastest-growing territory, projected to advance at a 20.85% CAGR through 2031 due to UPI adoption and open-banking regulation.

Which segment contributes the largest revenue within Banking as a Service platform?

Payment-processing services lead with 41.30% share, driven by high transaction volumes and demand for real-time settlement.

What major driver will shape Banking as a Service growth over the next two years?

Rising embedded-finance demand from e-commerce and super-apps is expected to add about 4.1% points to the market’s CAGR in the short term.

Which deployment model is preferred by large enterprises?

Large enterprises favor API-based platforms for granular control, accounting for 63.88% of market revenue in 2025.

Page last updated on: