Market Overview

| Study Period | 2020 - 2031 |

|---|---|

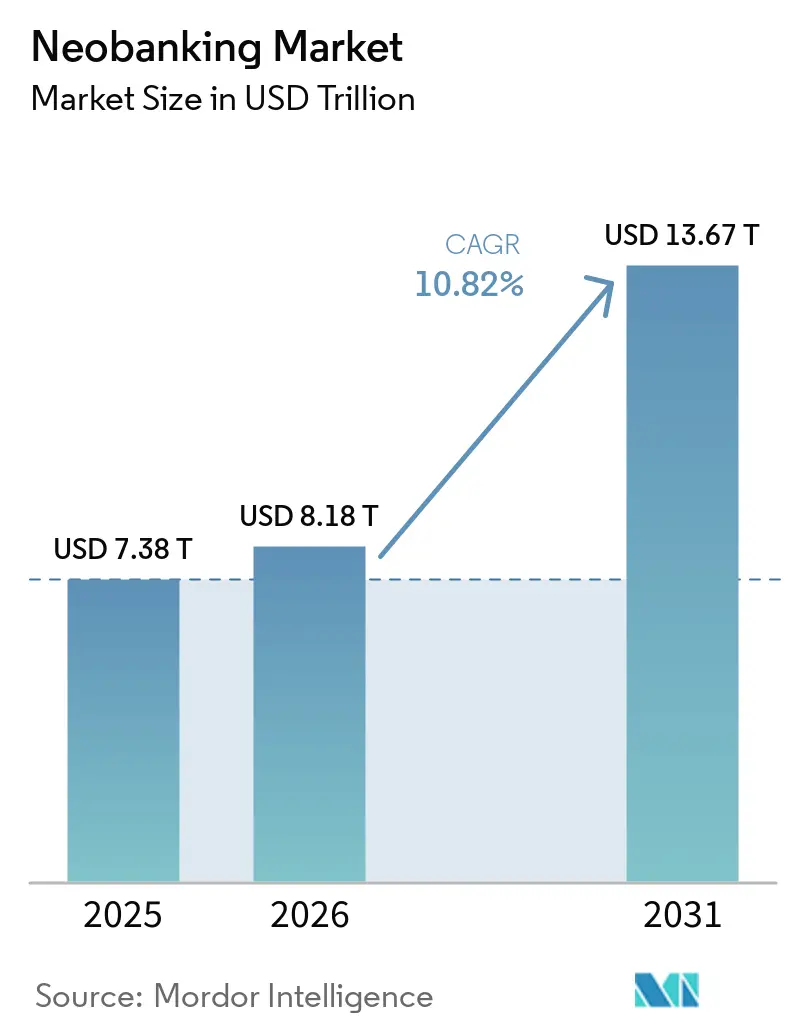

| Market Size (2026) | USD 8.18 Trillion |

| Market Size (2031) | USD 13.67 Trillion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

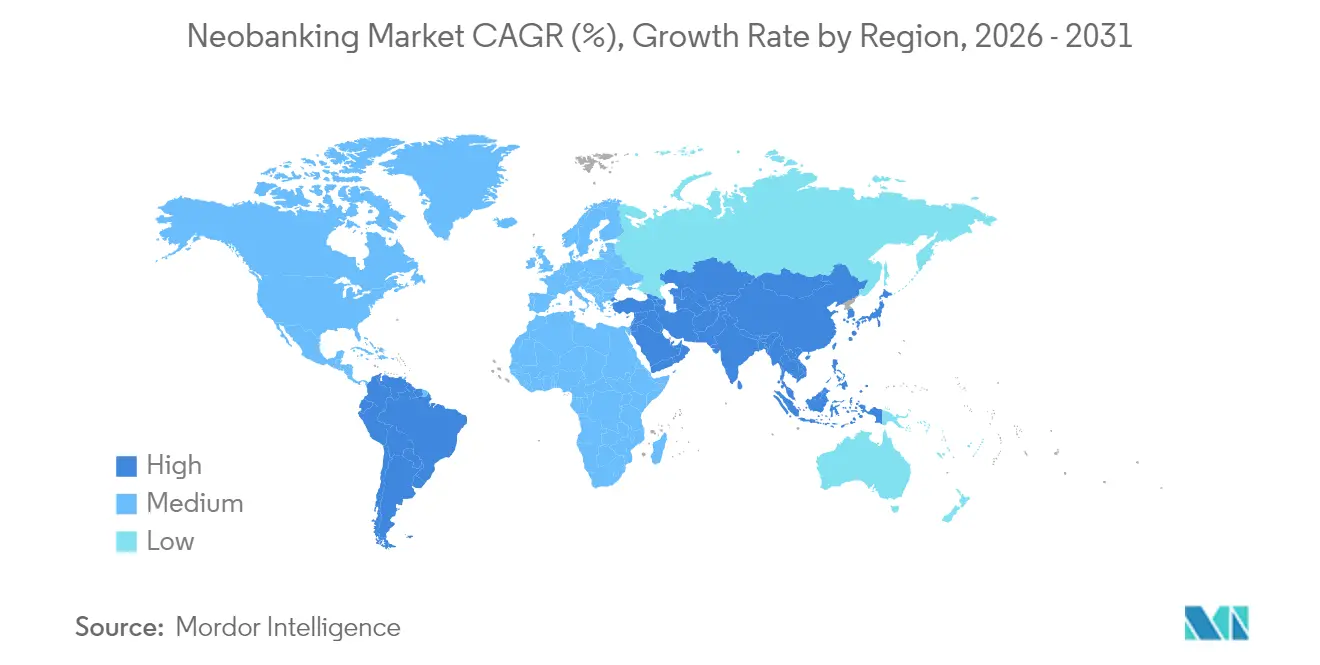

| Fastest Growing Market | Asia |

| Largest Market | Europe |

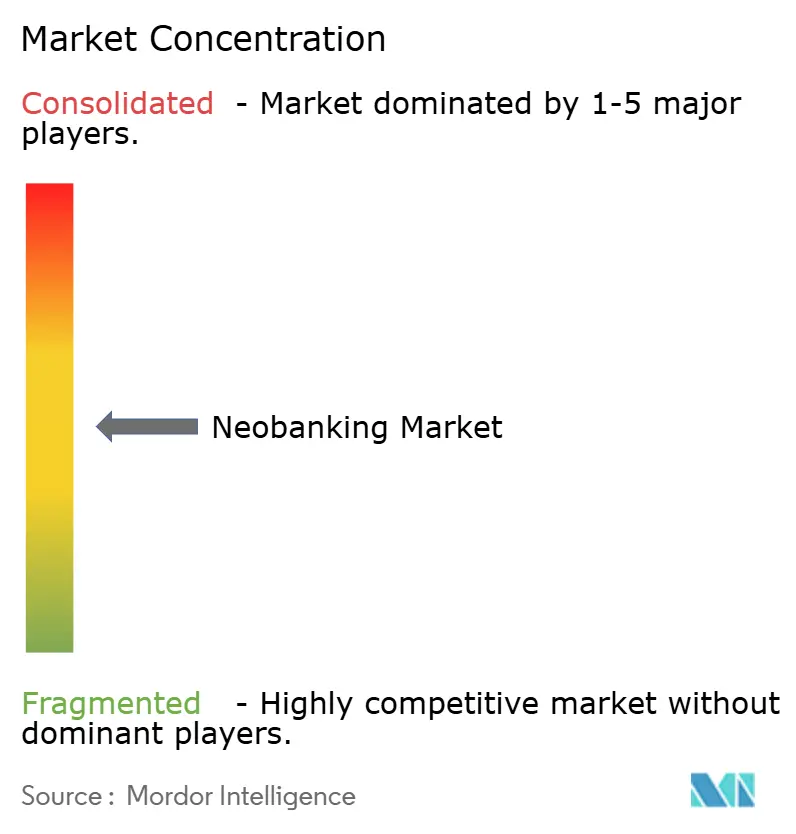

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neobanking Market Analysis by Mordor Intelligence

The neobanking market size is expected to grow from USD 7.38 trillion in 2025 to USD 8.18 trillion in 2026 and is forecast to reach USD 13.67 trillion by 2031 at 10.82% CAGR over 2026-2031. Rapid smartphone adoption, supportive open-banking rules, and customer demand for intuitive digital journeys fuel this expansion. Leading institutions such as Nubank, which now serves more than 110 million customers, and Chime, which completed a USD 864 million public offering in May 2025, show how digital-first models are moving into the financial mainstream[1]Nubank Investor Relations, “Q1 2025 Results,” n ubank.com. . Advances in artificial intelligence, real-time payments, and embedded-finance partnerships create multiple growth vectors that reinforce the neobanking market trajectory. Meanwhile, regulations like Europe’s Digital Operational Resilience Act standardize risk controls, sharpen competitive focus, and may accelerate consolidation as compliance costs rise.

Key Report Takeaways

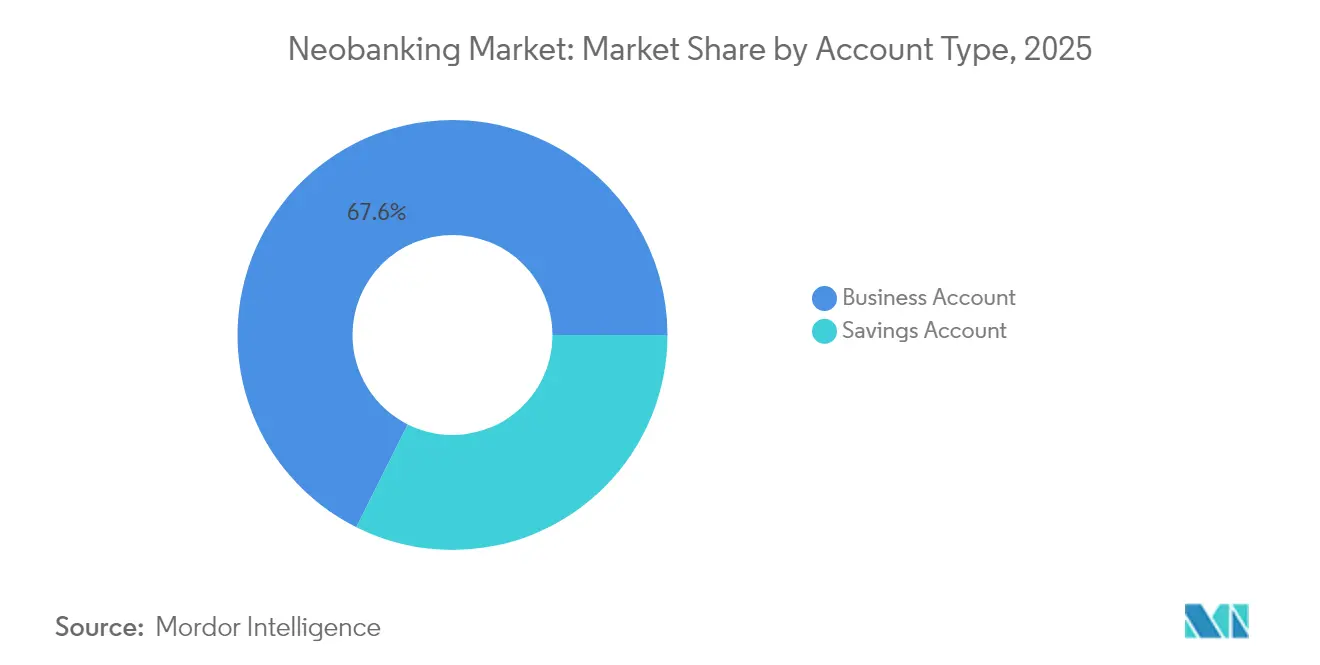

- By account type, business accounts held 67.62% of the neobanking market share in 2025; savings accounts are projected to expand at a 51.20% CAGR through 2031.

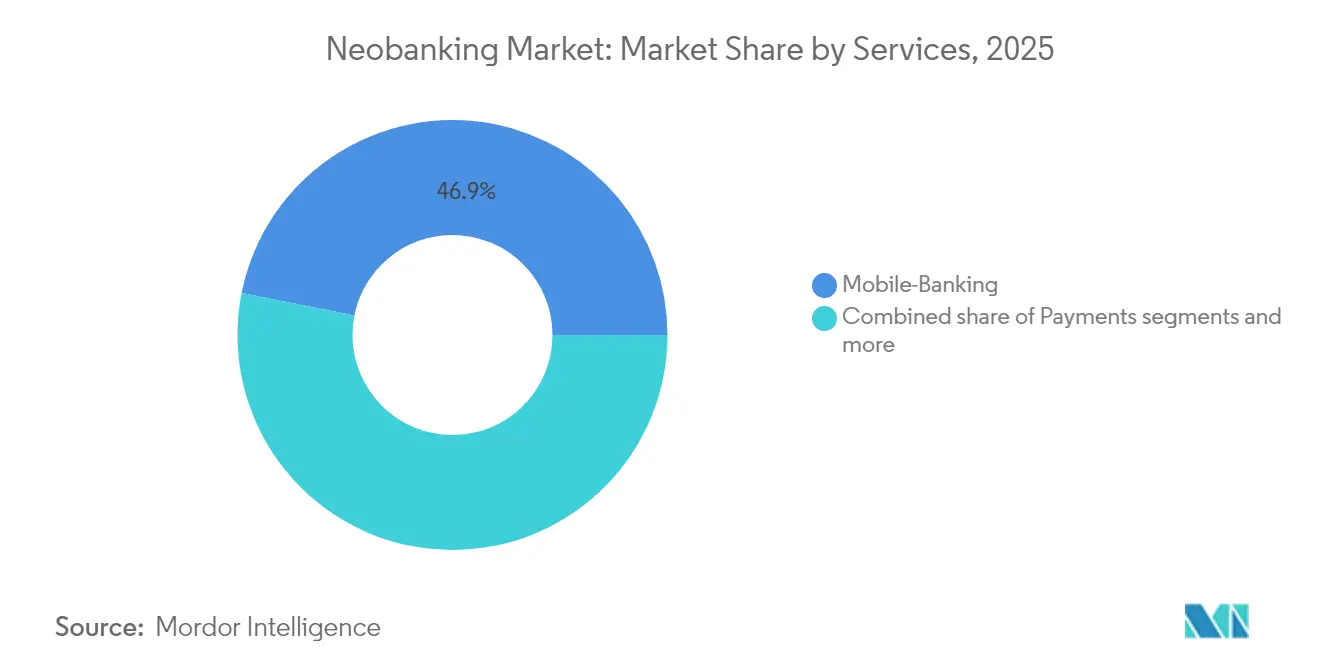

- By services, mobile banking captured 46.88% revenue in 2025 of the neobanking market, while the loans segment is forecast to grow at a 52.35% CAGR to 2031.

- By application, enterprise use commanded 69.45% share of the neobanking market size in 2025; personal banking is advancing at a 55.10% CAGR through 2031.

- By geography, Europe led with 35.96% revenue share of the neobanking market in 2025, whereas Asia-Pacific is projected to post a 51.80% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neobanking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartphone & internet penetration | 2.8% | Global, with strongest impact in APAC and Latin America | Medium term (2-4 years) |

| Cost advantage of branch-less operating model | 1.5% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Regulatory support for open banking & fintech licenses | 0.8% | Europe, UK, Brazil, with expanding to APAC | Long term (≥ 4 years) |

| SME demand for integrated financial tools | 0.7% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Real-time payment rails accelerating scale | 0.6% | Brazil (Pix), India (UPI), US (FedNow), Europe (SEPA Instant) | Short term (≤ 2 years) |

| AI-driven hyper-personalization boosting retention | 0.5% | Global, led by technology-advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Smartphone and Internet Penetration

Latin America counted 418 million mobile internet users in 2023, equal to 65% of its population, while new 5G rollouts support richer mobile-banking experiences that include video KYC and instant risk scoring. GSMA’s Open Gateway program, with 49 operators worldwide, processes millions of network-API calls each month, streamlining identity checks essential for account onboarding. Satellite partnerships with Starlink and OneWeb increasingly serve remote areas, widening neobanking market reach. Yet 225 million people in the region remain offline, pointing to an adoption gap that digital literacy initiatives must bridge. eSIM connections are projected to hit 75% of smartphones by 2030, simplifying cross-device account migration and reducing acquisition friction[2]GSMA, “Mobile Economy Latin America 2024,” gsma.com..

Cost Advantage of Branchless Operating Model

Digital banks avoid branch overheads and achieve lower cost-to-income ratios than legacy peers. N26 recorded 40% revenue growth to EUR 440 million in 2024 after converting to a single European legal entity, enabling lean expansion across 24 markets. 73% of new users came from referrals, underscoring the low-cost viral loop possible in a pure mobile channel. Automation and AI promise further savings, with N26 targeting a 50% cut in customer service spending within five years. Nevertheless, compliance spending rises; N26 invested EUR 100 million in anti-financial-crime controls since 2022, a reminder that scale efficiencies rely on sustained risk management[3]N26, “Company Blog and Annual Report 2024,” n26.com..

Regulatory Support for Open Banking and Fintech Licenses

Brazil recorded 4.8 billion successful open-finance API calls by June 2023, illustrating how mandatory data sharing can spark product innovation. Europe’s DORA framework harmonizes operational-resilience standards, giving digitally native firms an edge over incumbents burdened by legacy IT. Mexico’s 2018 fintech law covers account-information services but still lacks payment-initiation standards, so aggregators fill gaps through screen scraping. OECD research finds that markets with lower banking concentration, such as Brazil, show faster fintech adoption because open-data rules encourage competition[4]OECD, “FinTech and the Future of Finance 2024,” oecd.org. . Moving toward open finance across insurance and investments enlarges addressable revenue pools while increasing regulatory complexity.

SME Demand for Integrated Financial Tools

Small businesses need unified platforms that blend payments, lending, treasury, and analytics. N26 opened a business-account waitlist to serve this need, signaling strategic emphasis on enterprise deposits. Banking-as-a-Service player Unit partners with community banks to deliver white-label accounts to vertical SaaS providers, enabling SME clients to embed financial workflows in core software. Cross-border commerce also lifts demand: Latin American e-commerce is projected to hit 20% of retail sales by 2026, driving SMEs to seek lower-cost multi-currency solutions. OECD notes that three-quarters of digital-bank clients in Latin America were previously unbanked or underbanked, proving the inclusive potential of data-driven credit models. The challenge is delivering broad functionality without overwhelming users or inflating operating complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & data-privacy concerns | 1.2% | Global, with heightened focus in Europe (GDPR) and US | Short term (≤ 2 years) |

| Profitability & high CAC pressures | 0.9% | Global, particularly affecting venture-backed neobanks | Medium term (2-4 years) |

| Interchange-fee caps in key jurisdictions | 0.8% | Europe, UK, Australia, with potential US expansion | Medium term (2-4 years) |

| Dependence on partner banks for licenses | 0.7% | Global, concentrated in markets with restrictive banking licenses | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Privacy Concerns

Financial entities face rising AML alerts and scam attempts; regulators demand stronger controls that can strain smaller balance sheets. Europe’s GDPR sets strict consent rules, and DORA widens oversight to cloud vendors, forcing continuous investment in security layers. Shared service providers create concentration risk, so third-party management becomes a board-level duty. Past growth caps placed on N26 by Germany’s BaFin underscore how deficiencies can stall expansion until remedial action is verified. Customer trust hinges on transparent data-handling disclosures and rapid breach-response protocols.

Profitability and High Customer-Acquisition Costs

Interchange-fee caps in Europe squeeze a traditional revenue pillar, compelling digital banks to rely more on interest income that in turn demands prudent credit skills. Chime’s public filing shows heavy marketing spends ahead of listing, illustrating the cost of brand visibility in a crowded field. Some Banking-as-a-Service firms, facing margin compression, accepted rescue financing that signals stress in upstream infrastructure economics. Loan delinquencies exceeded 10% at several Brazilian neobanks in late 2022, reminding operators that fast growth cannot outpace risk assessment. Venture funding has cooled, so management teams prioritize breakeven timelines over headline customer metrics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Account Type: Business Banking Drives Market Leadership

Account TypeBusiness accounts contributed 67.62% of neobanking market revenue in 2025, a share that underscores corporate appetite for unified money-management tools. Enterprise users generate higher transaction values and more predictable fee streams than retail customers, sustaining attractive unit economics. Savings accounts, supported by competitive deposit rates such as N26 Instant Savings’ 4% offer across 13 European markets, are projected to grow at a 51.20% CAGR and broaden funding sources. Embedded-finance tie-ups allow software vendors to bundle specialized accounts for freelancers and online merchants. These dynamics keep the neobanking market positioned to capture evolving treasury needs among digitally native firms.

Personal customers benefit as institutions repurpose business-grade infrastructure into consumer-friendly experiences, fostering cross-sell into credit and investment. The integration of Personal Finance Tools within neobanking platforms is enhancing customer engagement through budgeting, expense tracking, and automated financial management features. Alternative data builds richer underwriting profiles, while automated routines simplify budgeting and bill pay. Raising real-time rails shortens settlement cycles and encourages account primacy in day-to-day spending. Compliance frameworks built for corporate users naturally extend to retail, raising overall trust levels. In turn, the enlarged deposit base lowers funding costs and supports profitable lending expansion.

By Services: Mobile Banking Leadership Faces Lending Disruption

Mobile banking retained 46.88% revenue leadership in 2025, reflecting its role as the gateway product for first-time users. Yet lending services are on track for a 52.35% CAGR as AI models mine cash-flow data to approve small-ticket credit in seconds. Real-time payment systems reduce collection friction and enable micro-repayments that fit gig-worker income streams. Cross-border transfers leverage partnerships with specialized firms such as Wise, giving customers transparent FX pricing while increasing transaction frequency. Neobanks invest in modular architecture so they can add wealth, insurance, and crypto features under one login, reinforcing customer stickiness.

The scaling of loan books requires careful capital management. Many digital banks pursue partnerships with balance-sheet providers or obtain llimited-purposebank bank charters to lower funding costs. Regulatory expectations around responsible lending drive investment in explainable AI. Markets with open-finance data allow lenders to confirm income across multiple sources, improving approval accuracy. Overall, diversified service arrays strengthen the neobanking market position against single-product fintech rivals.

By Application: Enterprise Dominance Challenged by Personal Growth

Enterprise applications captured 69.45% of the neobanking market size in 2025 owing to strong demand for automated payables, receivables, and cash-flow forecasting. Businesses pay for analytics dashboards that transform raw transaction feeds into working-capital insights. Payroll integrations further embed accounts into daily operations, raising exit barriers. Regulatory calls for real-time VAT reporting in Europe encourage digital statement feeds that legacy banks struggle to produce quickly. Consequently, the enterprise segment will remain the profit anchor for the neobanking industry.

Personal-banking usage, though smaller, is climbing at a 55.10% CAGR as mainstream consumers embrace digital-only relationships. Feature parity with legacy banks now includes overdrafts, travel insurance, and savings goals. AI chatbots and gamified budgeting cultivate daily engagement that deepens loyalty. Super-app concepts combine ride-hailing, shopping rewards, and banking within one interface, a trend visible in Asia-Pacific markets. Over time, converged platforms may blur the line between personal and enterprise contexts, letting sole proprietors run business and household finances from a single dashboard.

Geography Analysis

Europe’s 35.96% revenue lead in 2025 rests on harmonized regulations such as PSD2 and GDPR that spur secure data exchange while leveling competitive conditions. N26 reached its first profitable quarter in Q3 2024 after BaFin lifted growth caps, proof that scale and compliance can coexist. Payment Services Regulation 3, which tightens interchange caps, encourages product diversification into savings and credit. Starling Bank’s acquisition of Ember shows how incumbents use M&A to add accounting automation for SMEs. Real-time SEPA Instant adoption is widening, letting neobanks settle euro transfers in seconds across 36 countries.

Asia-Pacific is set to outpace peers with a 51.80% CAGR to 2031, powered by India’s UPI ecosystem and China’s established digital banks such as WeBank. Regulatory sandboxes in Singapore and Australia foster controlled experimentation with new products, reducing time to market. Southeast Asia’s first mobile populace drives leapfrog adoption that bypasses legacy desktop banking. Japan and South Korea leverage super-apps to integrate payments and social media, raising daily transaction velocity. Demographic dividends, especially among under-30 consumers, create a large addressable base for purely digital accounts.

North America presents a mature yet dynamic arena. Chime’s USD 864 million IPO validates investor confidence in the neobanking market, though heightened scrutiny requires clear profitability paths. FedNow’s launch extends instant payments nationwide, supporting innovations such as earned wage access. Canada’s ongoing open-banking consultation suggests future harmonization that would lower entry barriers. South America remains an inclusion hotspot; Brazil’s Pix and open-finance mandates propel Nubank beyond 110 million users and illustrate the power of policy-enabled disruption. Mexico’s partially implemented standards create room for specialized entrants to differentiate on faster payment initiation.

The Middle East and Africa trail in volume but show strong potential. GCC regulators issue digital-bank licenses that focus on cross-border commerce, while Nigeria’s population scale attracts venture capital despite infrastructure gaps. Pan-African payment initiatives aim to unify regional rails and reduce remittance costs. Collectively, these dynamics ensure that the neobanking market expands on multiple fronts, adapting to varied regulatory and consumer landscapes worldwide.

Competitive Landscape

Market concentration is moderate, with a handful of hyperscale’s controlling substantial customer bases yet leaving room for niche challengers. Nubank surpasses 110 million users by exploiting Brazil’s real-time rails and transparent fee model. Revolut and Klarna together serve about 135 million clients, leveraging global card schemes and merchant networks. WeBank invests more than 10% of annual revenue in R&D, creating proprietary AI and cloud infrastructure that raises technical barriers. Traditional banks respond by launching digital-only spin-offs or embedding finance through API suites, intensifying rivalry.

Strategic partnerships dictate scale. Banking-as-a-Service operators provide turnkey compliance and ledger tools, letting brands add accounts without charters, though funding pressures are driving consolidation. Embedded-finance corridors expand into payroll platforms, marketplace ecosystems, and creator-economy apps, converting everyday touchpoints into account-opening funnels. Data ownership and analytics become the battleground; institutions with granular transaction insights can price risk, tailor rewards, and detect fraud faster.

Regulatory mastery emerges as a competitive moat. Entities like N26 that proactively upgrade AML systems avoid growth pauses, while under-invested peers face penalties. Cyber-resilience requirements under DORA compel all players to audit cloud vendors and institute business-continuity testing. Institutions that meet these standards gain credibility with enterprise clients and larger depositors, reinforcing virtuous growth cycles in the neobanking market.

Neobanking Industry Leaders

Nubank

Revolut

Chime

N26

Starling Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: N26 completed its conversion from a German stock corporation to a European Company (Societas Europaea), aligning governance with pan-European growth goals.

- November 2024: Starling Bank acquired Ember, and Monzo raised additional capital, exemplifying continued M&A and fundraising momentum in Europe’s digital-banking arena.

- March 2024: N26 launched Instant Savings in 13 European markets, offering up to 4% annual interest with tiered rates and no deposit limits.

- March 2024: Green Dot Network partnered with REPAY, FACEBANK, and a Y Combinator-backed startup to enable cash transactions through 90,000 retail locations.

Global Neobanking Market Report Scope

The Global Neo banking market is segmented by account type (Business account, Savings account), by services (Mobile-banking, Payments and money transfers, savings, Loans, Others), by application type (Personal, Enterprises, Other applications), and by Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers market size and forecast values for the Neobanking Market in USD billion for the above segments.

By Account Type

| Business Account |

| Savings Account |

By Services

| Mobile-Banking |

| Payments |

| Money-Transfers |

| Savings Account |

| Loans |

| Others |

By Application

| Personal |

| Enterprise |

| Other Application |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Account Type | Business Account | |

| Savings Account | ||

| By Services | Mobile-Banking | |

| Payments | ||

| Money-Transfers | ||

| Savings Account | ||

| Loans | ||

| Others | ||

| By Application | Personal | |

| Enterprise | ||

| Other Application | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the neobanking market?

The neobanking market size is USD 8.18 trillion in 2026.

How fast is digital-first banking expected to grow?

Global revenue is forecast to rise to a 10.82% CAGR by 2031.

Which region will see the fastest expansion?

Asia-Pacific is projected to register a 51.80% CAGR from 2026-2031.

What segment leads by account type?

Business accounts held 67.62% of neobanking market share in 2025.

Who are the largest players?

Nubank, Revolut, Klarna, WeBank, and Chime are among the market leaders.

What regulation shapes European digital banks?

The Digital Operational Resilience Act sets unified operational-risk standards.

Page last updated on: