Silt Curtain Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.18 Million |

| Market Size (2031) | USD 12.26 Million |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silt Curtain Market Analysis by Mordor Intelligence

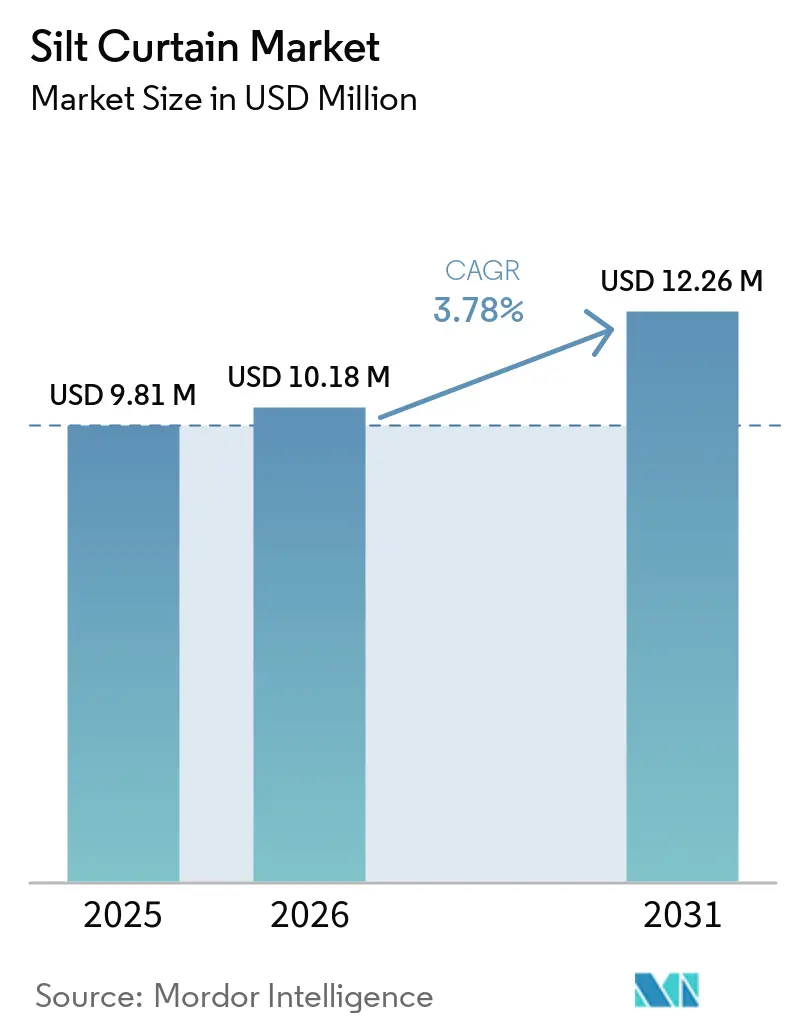

The Silt Curtain Market size is projected to be USD 9.81 million in 2025, USD 10.18 million in 2026, and reach USD 12.26 million by 2031, growing at a CAGR of 3.78% from 2026 to 2031. Procurement cycles for silt curtains align with long-duration infrastructure programs rather than consumer sentiment, with demand driven by multi-year budgets for port expansion, beach nourishment, and offshore decommissioning projects. Type I barriers for calm water accounted for the largest market share in 2025. However, the increasing offshore wind capacity and North Sea platform removals are shifting demand toward Type III curtains, which are designed to withstand currents of 3 to 5 knots. Polyurethane fabrics are increasingly preferred due to their extended service life in corrosive saltwater environments, which is critical for beach stabilization and mangrove restoration projects that require long-term maintenance. The Asia-Pacific region experienced significant growth, supported by India’s INR 192,390 million (USD 2,062.92 million) Vadhavan Port development and China’s 40 million-ton Ningbo-Zhoushan terminal upgrade. While dredging remains a key application, offshore energy projects are expanding at a faster pace, driven by the United Kingdom's enforcement of sediment-plume controls for decommissioning and wind-farm cabling activities.

Key Report Takeaways

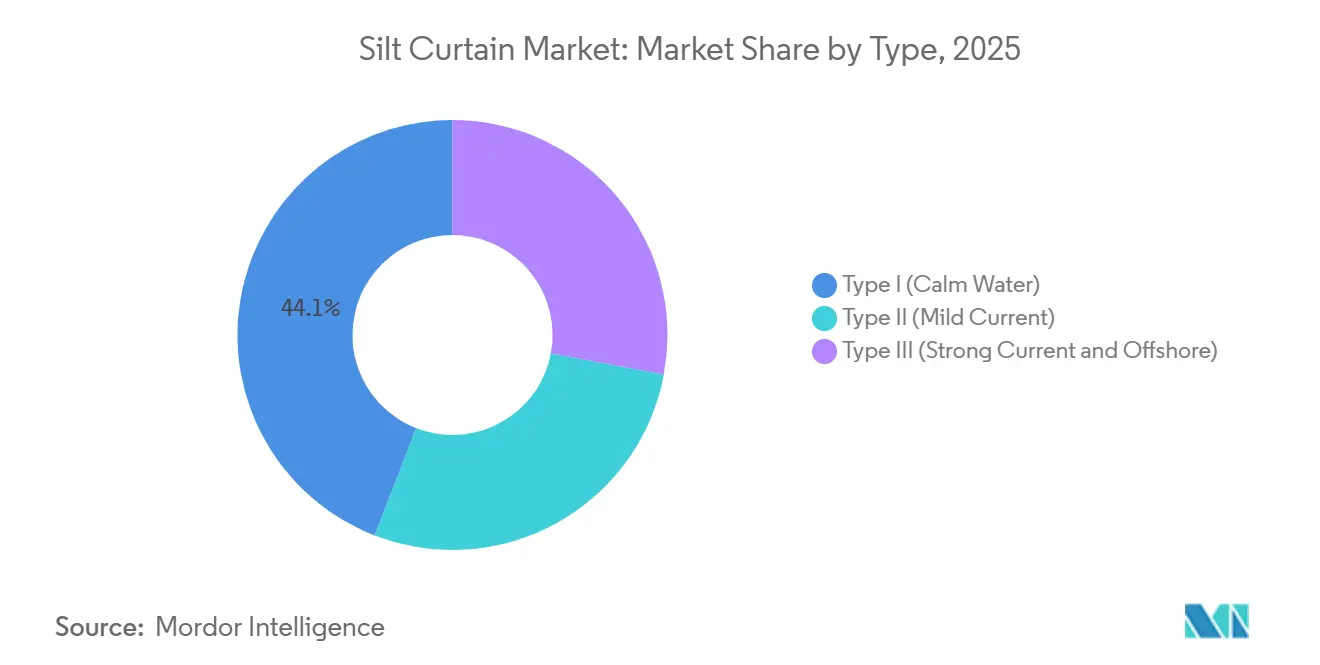

- By type, Type I calm-water curtains led with 44.11% of the silt curtain market share in 2025, while Type III strong-current barriers are projected to expand at a 4.41% CAGR through 2031.

- By material, polyvinyl chloride accounted for 48.24% of the silt curtain market size in 2025; polyurethane is advancing at 4.56% CAGR to 2031.

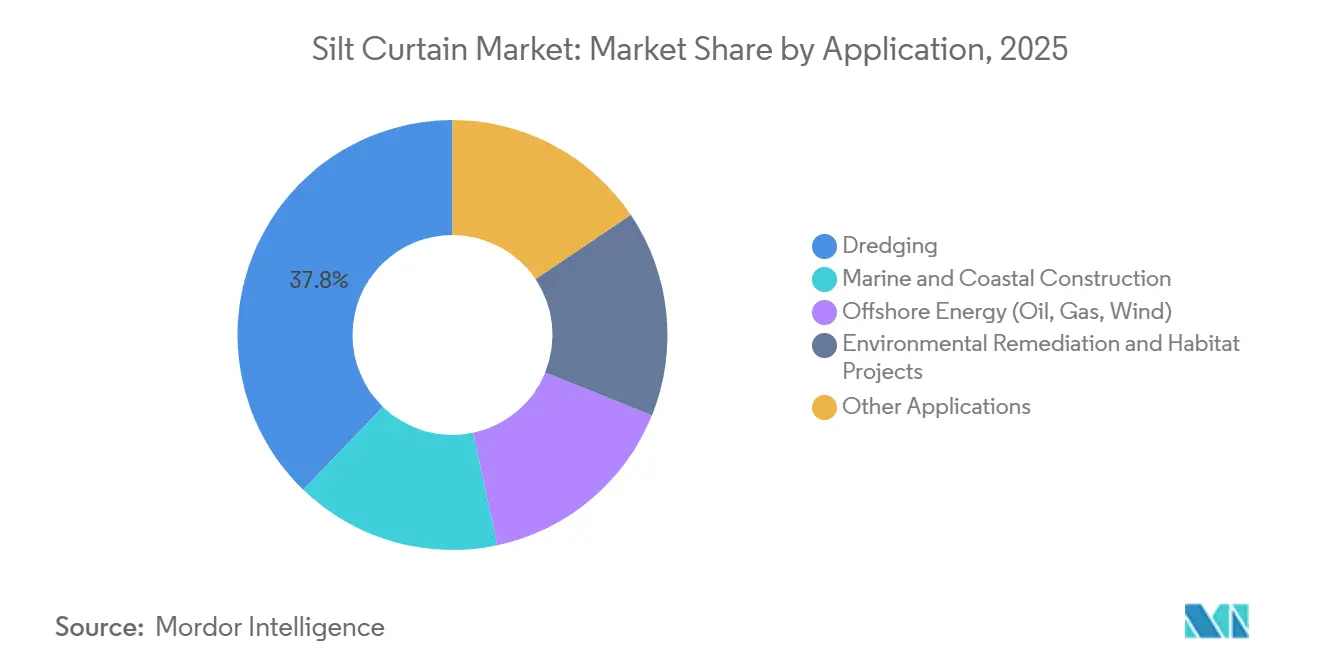

- By application, dredging held 37.78% of the silt curtain market share in 2025, whereas offshore energy is the fastest-growing segment at 3.87% CAGR during 2026-2031.

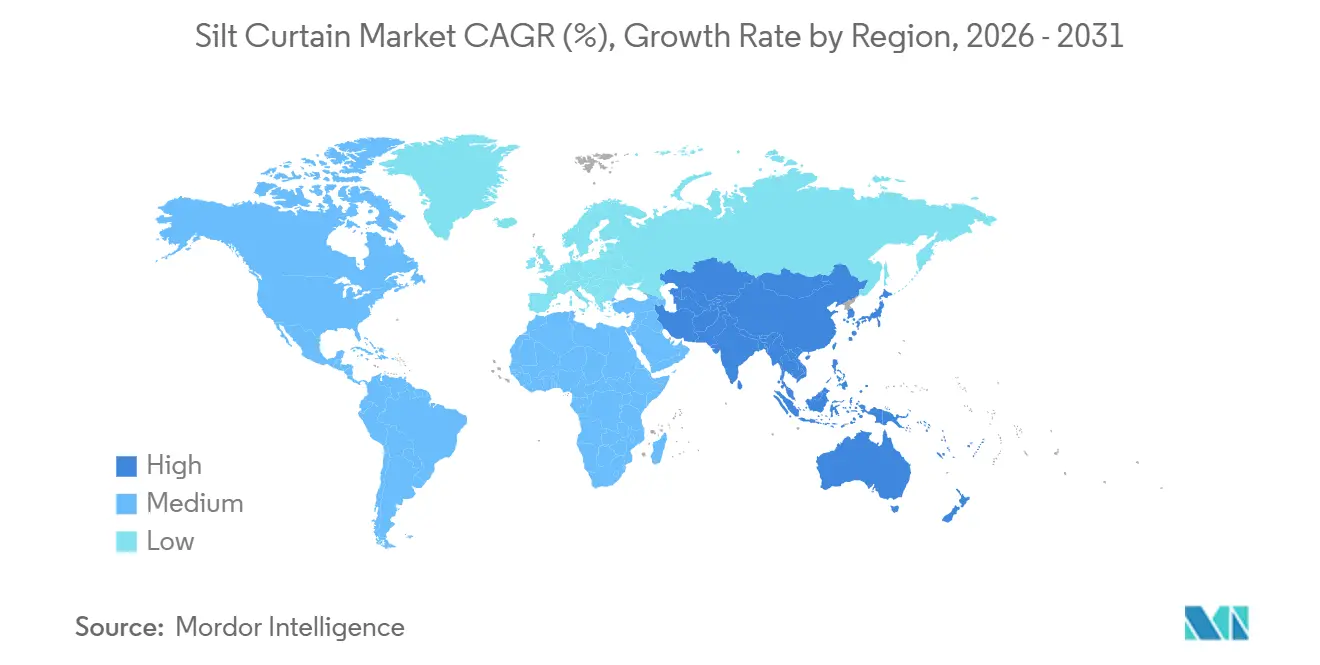

- By geography, Asia-Pacific generated 41.11% revenue in 2025 and is recording a 5.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silt Curtain Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Water-Quality Mandates in Emerging Economies | +1.2% | Asia-Pacific core, spillover to the Middle East & Africa | Medium term (2-4 years) |

| Surging Offshore Wind Farm Construction Needing Sediment Containment | +0.9% | Europe & Asia-Pacific, selective North America coastal zones | Long term (≥ 4 years) |

| Climate-Adaptation Investments in Beach Nourishment and Mangrove Restoration | +0.7% | Global, with concentration in the North America Atlantic coast, and Southeast Asia deltas | Medium term (2-4 years) |

| Rise in In-Situ Capping of Contaminated Sediments in Brownfield Ports | +0.5% | North America & Europe legacy industrial harbors, emerging in the China Yangtze corridor | Long term (≥ 4 years) |

| Insurance Premium Discounts for Contractors Using Verified Turbidity Controls | +0.4% | Global, early adoption in the United States, Canada, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Water-Quality Mandates in Emerging Economies

India's Central Pollution Control Board transitioned from voluntary advisories to mandatory nephelometric thresholds in 2024, requiring dredging contractors to implement real-time monitoring for projects exceeding 10,000 cubic meters. This regulation was first applied to the INR 1,228 million (USD 13.16 million) Paradip maintenance project, scheduled for fiscal 2026-27. In China, the Yangtze River Protection Law was extended to mandate curtain deployment at the Yangshan Phase IV terminal, which added 2.23 million twenty-foot equivalent unit (TEU) capacity in 2025[1]Ministry of Ecology and Environment, “Yangtze River Protection Law,” mee.gov.cn. Thailand's Southern Land Bridge, a USD 28 billion corridor, includes 4.63 kilometers of marine works with mandatory turbidity controls from 2025 to 2030. By the end of 2025, 68% of ports in the region had obtained International Organization for Standardization (ISO) 14001 certification, and bid documents now pre-qualify certain specifications, reducing change-order risks for suppliers.

Surging Offshore Wind Farm Construction Needing Sediment Containment

Monopile driving and cable trenching activities in the North Sea, Yellow Sea, and U.S. Atlantic lease blocks generate sediment plumes that require containment. At Dogger Bank, reinforced polyurethane skirts were mandated during 130 kilometers of cable work due to wave heights exceeding 4 meters[2]Dogger Bank Wind Farm, “Project Overview,” doggerbank.com. In 2024, Japan's Science Council highlighted typhoon-driven scour risks, prompting project owners to adopt Type III curtains for planned 10 gigawatts (GW) of capacity. South Korea approved 8.2 GW of leases through 2030, incorporating sediment-containment requirements. In the U.S., the Bureau of Ocean Energy Management (BOEM) now delays environmental reviews by an average of nine months if developers fail to demonstrate barrier performance below 40 meters in depth. Manufacturers, including GEI Works, introduced composite-laminate Triton curtains in October 2024 to address these challenges.

Climate-Adaptation Investments in Beach Nourishment and Mangrove Restoration

New Jersey allocated USD 50 million in 2025 to nourish 22 kilometers of Atlantic shoreline, incorporating four-hourly turbidity reporting into contracts. Massachusetts committed USD 30 million for 120 hectares of salt-marsh rehabilitation, requiring silt curtains to protect eelgrass during dredge-spoil placement. In 2024, the United Nations Environment Program (UNEP) recognized BASF's Elastocoast polyurethane armor for its 80-to-100-year durability, facilitating green-bond financing for soft-engineering projects. Florida expedited 14 renourishment projects totaling 3.8 million cubic meters of sand but maintained a May-October nesting blackout, compressing contractor timelines. Indonesia initiated a pilot program for 5,000 hectares of mangrove replanting, utilizing lightweight, hand-carried curtains during monsoon periods.

Rise in In-Situ Capping of Contaminated Sediments in Brownfield Ports

In 2025, the Hunters Point Naval Shipyard used composite curtains with 0.5-millimeter apertures to contain heavy metals during tidal cycles. At the Duwamish Superfund site, 45,000 cubic meters of sediment were capped in 2024, achieving a 60% reduction in disposal costs compared to off-site landfill alternatives. The cleanup of Portland Harbor, spanning 16 kilometers, required double-curtain spacing to maintain turbidity levels below the 10 nephelometric turbidity unit (NTU) threshold. In China, the 23-port brownfield program under the Yangtze Economic Belt has focused on capping to mitigate the risks of downstream dispersal. Market demand has shifted toward fabrics with hydraulic conductivity, though only about 30% of off-the-shelf curtains meet this standard without requiring customization.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational Failures in High-Current and Deep-Water Conditions | -0.6% | Global offshore zones, acute in the North Sea, the South China Sea, Gulf of Mexico | Short term (≤ 2 years) |

| Lengthy Environmental-Permit Delays When Barriers Affect Migratory Species | -0.4% | North America, Atlantic and Pacific coasts, the North Sea, and the Asia-Pacific turtle nesting zones | Medium term (2-4 years) |

| Lack of Universal Testing Standards Causing Procurement Hesitancy | -0.3% | Global fragmentation is most severe across the Asia-Pacific and the Middle East jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Operational Failures in High-Current and Deep-Water Conditions

Standard polyvinyl chloride (PVC) curtains face structural issues, such as bowing or tearing, when exposed to currents exceeding 2 knots or depths beyond 12 meters. In the North Sea, pilots reported anchor pullouts under wave loads of 15 kilonewtons (kN), which doubled mobilization costs for hybrid moorings. Retrofitting weighted ballasts for Five Estuaries wind-farm cables resulted in a 35% cost increase when estuary currents reached 3.2 knots. In the Gulf of Mexico, decommissioning projects in water depths of 60 to 90 meters now require composite laminates with integrated buoyancy chambers. Additionally, fewer than 20% of deployments include real-time turbidity sensors, leading to undetected breaches that extend beyond containment zones.

Lengthy Environmental-Permit Delays When Barriers Affect Migratory Species

The National Marine Fisheries Service (NMFS) mandates acoustic and vessel-strike studies within 50 kilometers of right-whale corridors, causing delays of up to a year for three Massachusetts wind projects scheduled for 2025. In Florida, beach construction is restricted from May to October along 1,600 kilometers of shoreline, forcing work into hurricane season and increasing insurance costs. Under Australia’s Environment Protection and Biodiversity Conservation (EPBC) Act, Brisbane dredging faced a four-month delay following a 90-day consultation on dugong habitats. To mitigate delays, contractors are stockpiling curtain inventory at nearby ports to commence work as soon as permits are approved, creating challenges for smaller firms unable to manage such capital-intensive preparations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Offshore Deployments Accelerate Despite Calm-Water Dominance

Type I silt curtains, designed for calm harbor conditions, accounted for 44.11% of the market share in 2025, driven by routine maintenance dredging in protected ports. Meanwhile, Type III curtains are expanding at a compound annual growth rate (CAGR) of 4.41%, supported by applications in North Sea wind farms, Gulf of Mexico decommissioning projects, and Japan’s typhoon-prone wind zones. These factors are contributing to higher average selling prices, thereby increasing the overall silt curtain market size. GEI Works’ Triton launch introduced a reinforced polyvinyl chloride (PVC) design with a six-foot skirt, rated for five-knot currents, positioning the company to secure contracts for deep-water projects.

The cost disparity between Type I and Type III curtains ranges from USD 60-80 to USD 180-220 per linear meter, reflecting a 30-40% premium due to the inclusion of ballast chains, hybrid anchors, and sensor packages. Deep-water operations beyond 12 meters are driving demand for specialized contractors, reducing addressable volume but increasing profit margins.

By Material: Polyurethane Gains Ground on Durability, PVC Retains Cost Edge

PVC held a 48.24% market share in 2025, as short-term dredging projects typically retire silt curtains within six months. However, polyurethane is growing at a CAGR of 4.56%, driven by its suitability for long-term applications such as beach protection and mangrove rehabilitation, which require materials with a lifespan exceeding 20 years. This trend is boosting the market size for premium materials. BASF’s Elastocoast system, offering 80-100 years of durability and 50% bio-based content, has gained attention for its compatibility with climate-bond financing.

A field survey conducted in Singapore and Vietnam revealed that woven geotextile bags lost up to 60% of their tensile strength within six years due to ultraviolet degradation. This has prompted project owners to adopt ultraviolet-stabilized polyurethane. While Asia’s large-scale PVC production keeps costs 15-20% lower than polyurethane, European sustainability regulations and North American grant funding are gradually narrowing this cost gap.

By Application: Dredging Leads, Offshore Energy Segments Fastest

Dredging accounted for 37.78% of market demand in 2025, driven by predictable port maintenance cycles that generate recurring orders. Offshore energy applications are projected to grow at a CAGR of 3.87% through 2031, fueled by over 2,000 United Kingdom platform removals and 8.2 gigawatts (GW) of Korean wind leases, which require containment solutions for currents ranging from 3 to 5 knots. Environmental remediation and habitat restoration projects, though smaller in scale, are expanding rapidly due to United States and Association of Southeast Asian Nations (ASEAN) climate-resilience funding, further contributing to the growth of the silt curtain market.

The Vadhavan Port project, involving 225 million cubic meters of reclamation and 7 million cubic meters of channel dredging, exemplifies a blended use case that integrates dredging and marine construction. This project secures long-term replacement revenue for silt curtain suppliers under India’s hybrid annuity model.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 41.11% of global revenue and is projected to grow at a compound annual growth rate (CAGR) of 5.89%. This growth is driven by large-scale port expansions, brownfield remediation projects, and offshore wind allocations. India’s hybrid annuity financing model, which allocates 60% of funds during construction and 40% over a 10-year period, enhances cash cycles for domestic barrier manufacturers, thereby increasing the regional silt curtain market share. In China, the 23-port remediation program under the Yangtze Economic Belt prioritizes low-permeability geotextiles. Meanwhile, Thailand’s USD 28 billion Southern Land Bridge project ensures six years of consistent demand.

North America’s market dynamics are influenced by the Bureau of Ocean Energy Management (BOEM) lease pipeline and state-level beach-resilience budgets. New Jersey’s USD 50 million nourishment portfolio and Massachusetts’ USD 30 million marsh restoration program contribute to increased near-shore volume. However, Florida’s May-October nesting blackout restricts the construction window, leading to higher project insurance costs. Additionally, Canada’s Canadian Standards Association (CSA) standard, which differs from the American Society for Testing and Materials (ASTM), complicates import logistics but provides a competitive advantage to local suppliers.

Europe’s market growth is primarily driven by offshore wind projects. Leases in areas such as Dogger Bank, Five Estuaries, and the German North Sea require sediment curtains for depths under 30 meters, boosting demand for Type III silt curtain products. The United Kingdom also faces long-term opportunities with the decommissioning of 2,000 offshore platforms, creating a multi-decade growth driver. Incremental opportunities arise from Mediterranean dredging projects in Spain and Italy, as well as Arctic liquefied natural gas (LNG) activities in Russia, though these are constrained by sanctions.

In South America, Brazil’s port privatization initiatives are the primary focus of market activity. The Middle East and Africa regions benefit from Saudi Arabia’s NEOM coastal developments and South Africa’s Durban port deepening projects. Turkey’s Kanal Istanbul project remains a potential long-term growth catalyst, pending permit approvals.

Competitive Landscape

The silt curtain market is moderately consolidated. Lamor Corporation acquired Elastec in May 2024, while Solmax purchased Layfield Environmental Systems, enabling cross-selling opportunities across oil-spill equipment, geomembranes, and silt curtains. Calm-water polyvinyl chloride (PVC) curtains are facing pricing challenges, reducing gross margins. In contrast, Type III offshore systems maintain higher margins due to their custom engineering and integrated monitoring features. Currently, only a small portion of installed curtains are equipped with Internet of Things (IoT) sensors, providing a competitive advantage for companies that offer bundled compliance analytics.

Regional fragmentation continues due to differing American Society for Testing and Materials (ASTM), Canadian Standards Association (CSA), and local specifications. However, multinational contractors increasingly prefer suppliers with pan-jurisdictional certifications, creating opportunities for well-capitalized incumbents. There is a market gap in lightweight, hand-deployed fabrics for mangrove and marsh projects, which remains underserved by heavy dredging specialists. GEI Works’ reinforced Triton curtain highlights product innovation targeting offshore wind and decommissioning applications, where the operational failures of standard curtains have led to higher tolerance requirements.

Silt Curtain Industry Leaders

Elastec

GEI Works

ACME Environmental

Silt Management Supplies, LLC.

Texas Boom Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Thailand’s Cabinet has approved the USD 28 billion Southern Land Bridge project, requiring the use of silt curtains, also known as turbidity curtains, at the Ranong and Chumphon dredging sites to manage sediment displacement until 2030.

- March 2025: India’s Vadhavan Port awarded the near-shore reclamation package to Jan De Nul (JDN) and Dredging, Environmental and Marine Engineering (DEME). The project involved substantial land reclamation, and work commenced in the third quarter of 2025. A silt curtain was deployed during the reclamation process to control sediment dispersion and safeguard the surrounding marine environment.

Global Silt Curtain Market Report Scope

A silt curtain is a floating geotextile barrier designed to contain sediment and pollutants within a designated area of a waterway. It is used to prevent the spread of these materials during construction, dredging, or other marine projects, serving as an environmental protection measure to reduce turbidity and its impact on marine ecosystems.

The silt curtain market is segmented by type, material, application, and geography. By type, the market is segmented into type I (calm water), type II (mild current), and type III (strong current and offshore). By material, the market is segmented into polyvinyl chloride, polyurethane, geotextile fabric, and composite laminates. By application, the market is segmented into dredging, marine and coastal construction, offshore energy (oil, gas, wind), environmental remediation and habitat projects, and other applications. The report also covers the market size and forecasts for silt curtains in 20 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Type I (Calm Water) |

| Type II (Mild Current) |

| Type III (Strong Current and Offshore) |

| Polyvinyl Chloride |

| Polyurethane |

| Geotextile Fabric |

| Composite Laminates |

| Dredging |

| Marine and Coastal Construction |

| Offshore Energy (Oil, Gas, Wind) |

| Environmental Remediation and Habitat Projects |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Turkey | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Type I (Calm Water) | |

| Type II (Mild Current) | ||

| Type III (Strong Current and Offshore) | ||

| By Material | Polyvinyl Chloride | |

| Polyurethane | ||

| Geotextile Fabric | ||

| Composite Laminates | ||

| By Application | Dredging | |

| Marine and Coastal Construction | ||

| Offshore Energy (Oil, Gas, Wind) | ||

| Environmental Remediation and Habitat Projects | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Turkey | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Silt Curtain Market?

The Silt Curtain Market size is projected to be USD 9.81 million in 2025, USD 10.18 million in 2026, and reach USD 12.26 million by 2031, growing at a CAGR of 3.78% from 2026 to 2031.

Which geographic region leads demand?

Asia-Pacific generated 41.11% of global revenue in 2025 and is expanding at a 5.89% CAGR thanks to large port and remediation programs.

Which application segment is expanding fastest?

Offshore energy, anchored by wind-farm construction and platform decommissioning, is the fastest-growing use case at 3.87% CAGR.

What material is gaining share over PVC?

Polyurethane curtains are advancing at 4.56% CAGR because they last longer in corrosive saltwater and qualify for green-finance mandates.

Page last updated on: