Silica Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

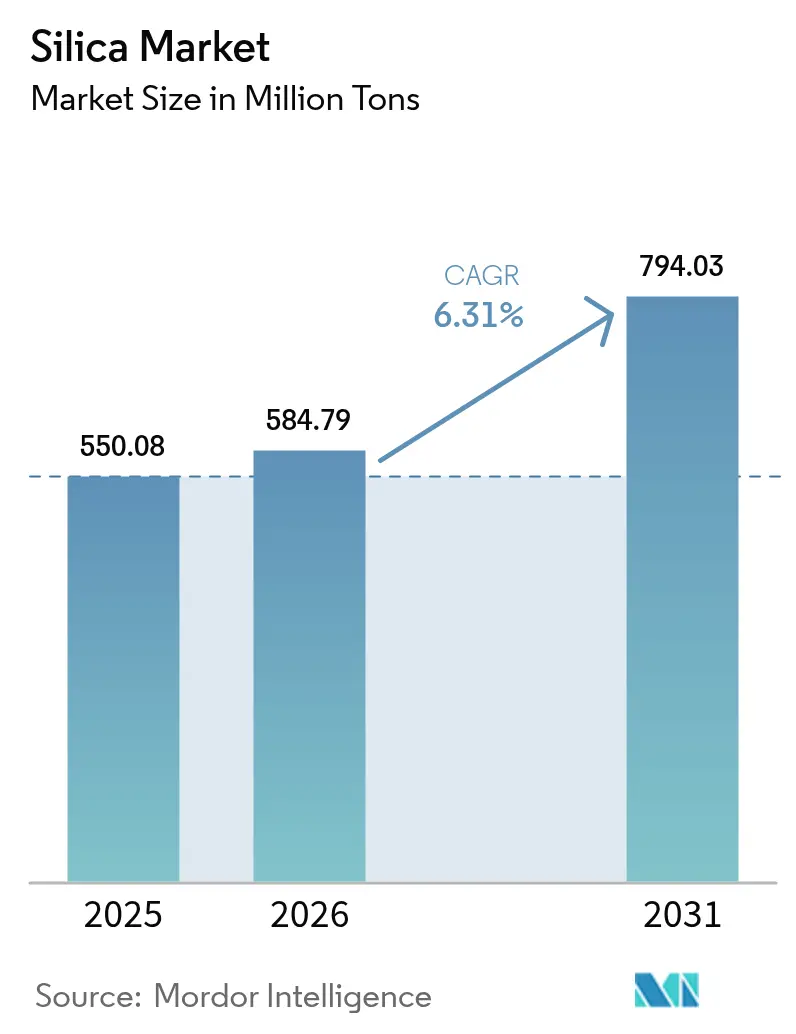

| Market Volume (2026) | 584.79 Million tons |

| Market Volume (2031) | 794.03 Million tons |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silica Market Analysis by Mordor Intelligence

The Silica market size is expected to grow from 550.08 Million tons in 2025 to 584.79 Million tons in 2026 and is forecast to reach 794.03 Million tons by 2031 at 6.31% CAGR over 2026-2031. This robust expansion mirrors the mineral’s central role in construction materials, energy-efficient tires, solar glass, and semiconductor substrates. Rising infrastructure spending in Asia-Pacific, the global push for low-rolling-resistance tires, and accelerating photovoltaic build-outs are amplifying demand, while specialty-grade suppliers secure pricing premiums through high-purity and surface-modified offerings. Freight-cost volatility and occupational-health regulations temper growth, yet investment in bio-based processing and regional beneficiation reinforce a resilient long-term outlook for the silica market.

Key Report Takeaways

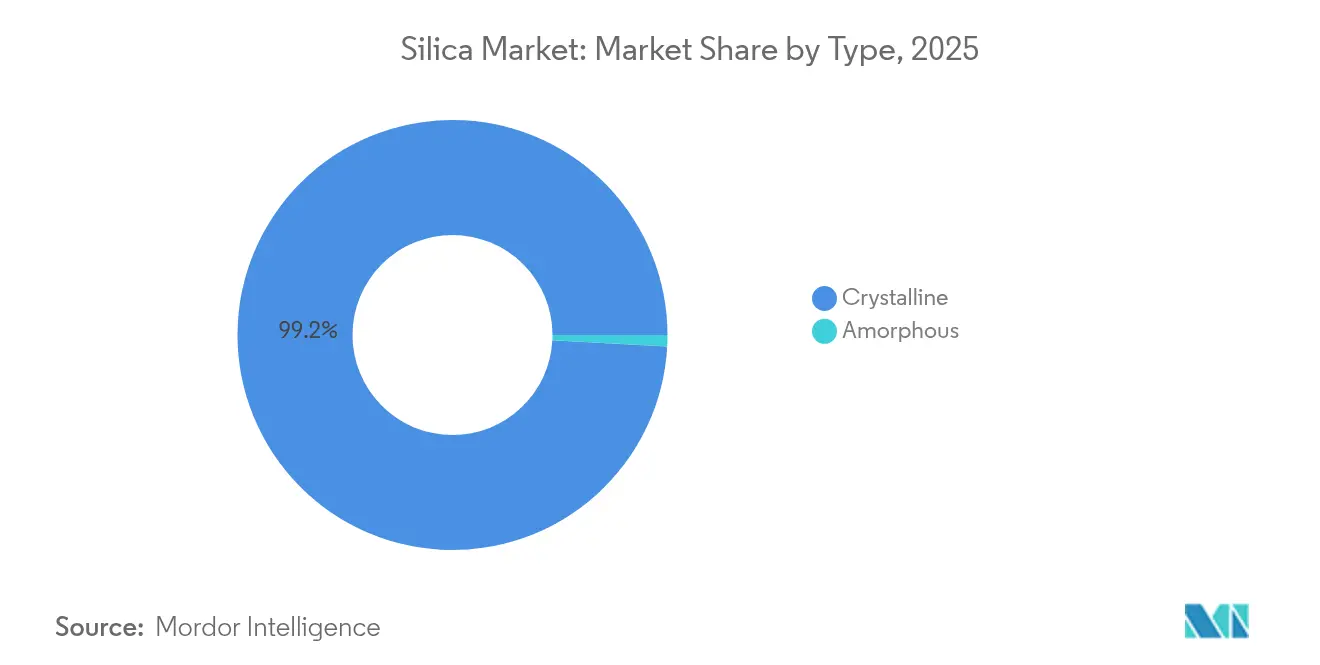

- By type, crystalline silica held 99.15% of silica market share in 2025 and is advancing at a 6.22% CAGR through 2031.

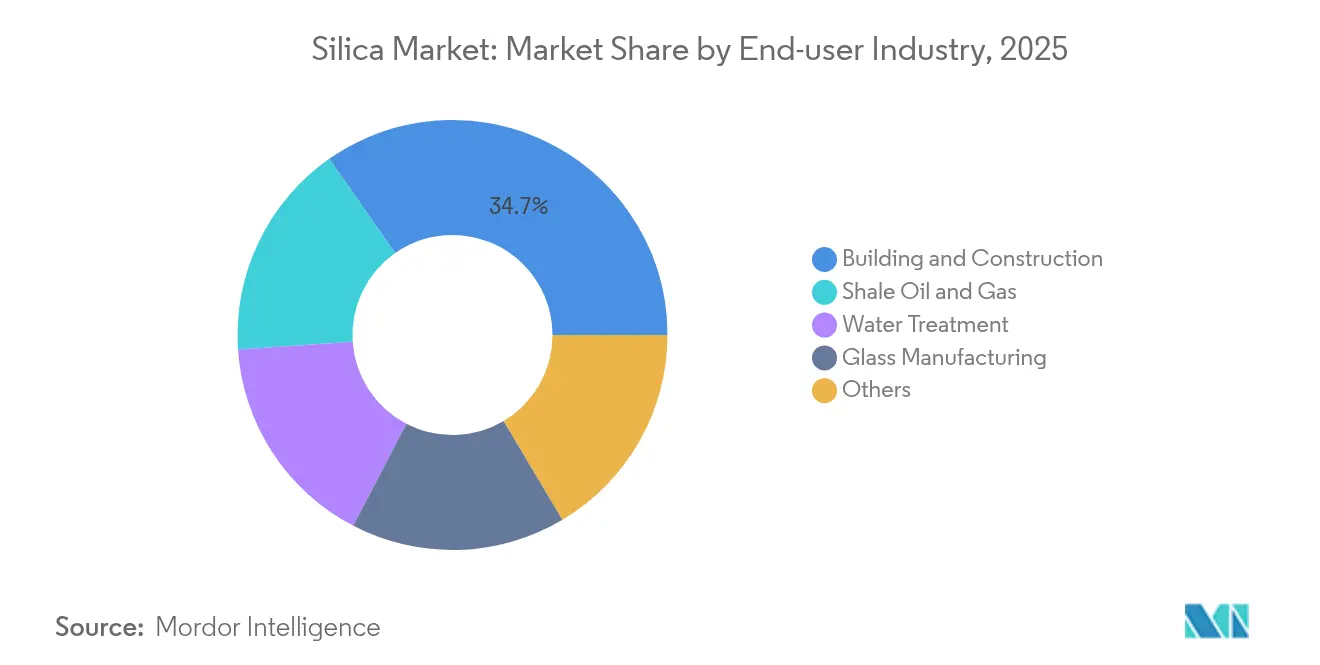

- By end-user industry, building and construction accounted for 34.72% of the silica market size in 2025, while shale oil and gas is projected to expand at a 7.62% CAGR between 2026 and 2031.

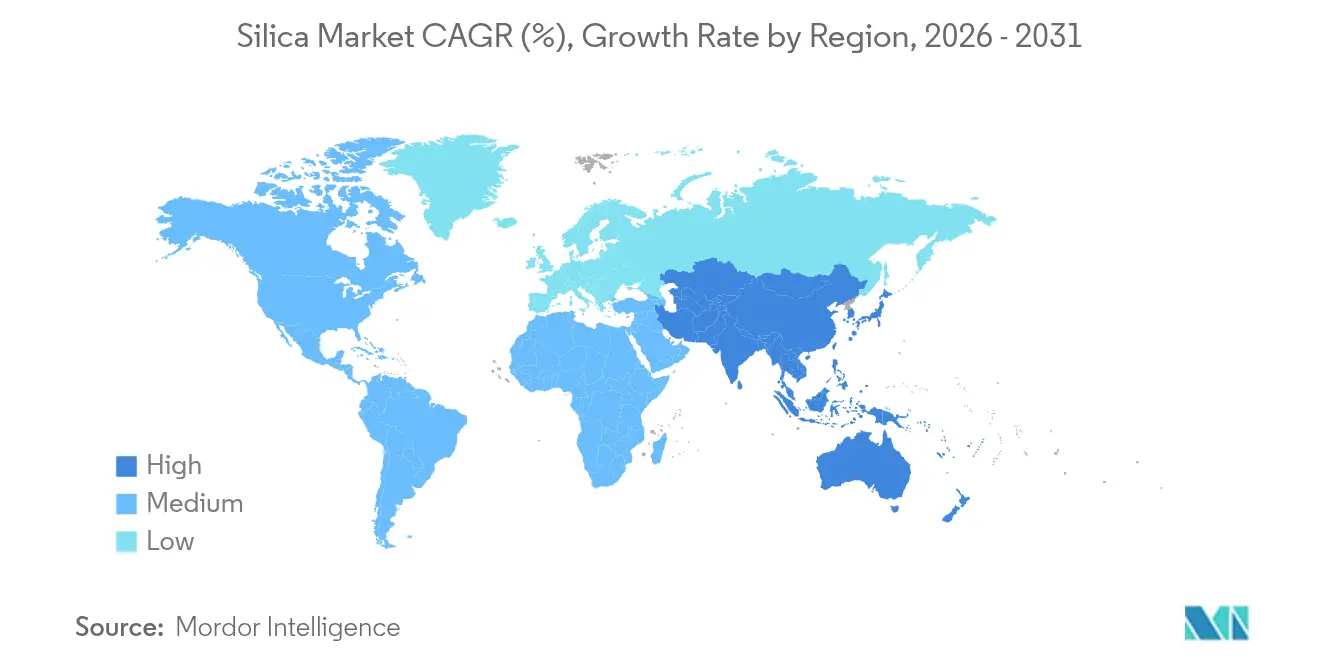

- By geography, Asia-Pacific commanded 41.00% of the silica market share in 2025 and is growing at an 8.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silica Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-tire demand for precipitated silica | +1.5% | Europe, North America, China | Medium term (2-4 years) |

| Photovoltaic glass capacity expansion | +0.8% | China, India, Southeast Asia | Long term (≥4 years) |

| High-purity silica for advanced semiconductors | +1.2% | Asia-Pacific, North America, Europe | Short term (≤2 years) |

| Rice-husk silica to cut carbon footprint | +0.9% | India, Thailand, Vietnam | Medium term (2-4 years) |

| Fumed silica for high-solids battery slurries | +1.1% | China, South Korea, Germany | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Robust Demand for Precipitated Silica in Energy-Efficient Green Tires

Low-rolling-resistance tires improve fuel economy by 3-7%, and European regulations that mandate tire-efficiency labeling spur higher silica loadings in tread compounds. Premium passenger-car tires now contain up to 90 phr of precipitated silica, double typical 2020 levels. Commercial fleets adopt similar formulations to lower diesel costs, while electric-vehicle makers intensify the trend to extend driving range.

Ongoing Build-Out of Photovoltaic Glass Manufacturing Capacity

Each gigawatt of solar deployment requires 15,000-20,000 tons of ultra-clear silica-based glass with iron content below 120 ppm. China commands over 85% of global PV-glass capacity and is pairing new float-glass lines with captive silica-beneficiation plants to guarantee feedstock quality. Thinner bifacial-panel glass further tightens purity specifications, driving investment in advanced beneficiation[1]Royal Society of Chemistry, “Photovoltaic Glass Supply Challenges at Multiterawatt Scale,” rsc.org.

Rising Adoption of High-Purity Silica in Advanced Semiconductor Nodes

Sub-3 nm logic chips need metallic-impurity levels below 1 ppb in CMP slurries, photomasks, and underfill materials. Evonik’s USD 220 million Michigan expansion targets this niche, where electronics-grade material secures 3-5 times commodity pricing. U.S. and European fabs seek local supply to de-risk Asian dependence[2]Evonik Industries, “Evonik Invests USD 220 Million in Colloidal Silica,” evonik.com.

Shift Toward Bio-Based Rice-Husk Silica in Asia to Cut Carbon Footprint

India alone generates more than 45 million tons of rice husk a year. Controlled combustion yields amorphous silica with 150-300 m²/g surface area, suitable for tire and rubber applications while lowering process emissions by 60%. Government incentives and carbon credits promote commercial adoption.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive threat from aluminosilicate and calcium-silicate fillers | -0.7% | Global, with higher impact in cost-sensitive applications | Medium term (2-4 years) |

| Volatility in freight cost for bulk silica sand | -0.4% | Global, particularly affecting long-distance trade routes | Short term (≤ 2 years) |

| Tightening respirable-crystalline-silica exposure limits (OSHA, EU) | -0.3% | North America and Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competitive Threat from Aluminosilicate and Calcium-Silicate Fillers

Calcined-clay and metakaolin products undercut commodity-grade silica by up to 25% while offering comparable reinforcement in concrete and polymer composites. Suppliers invest in particle-surface treatments that narrow historical performance gaps, with micronized aluminosilicates gaining share in cost-sensitive construction mixes.

Volatility in Freight Cost for Bulk Silica Sand

Dry-bulk rates on trans-Pacific routes swing by 40-60% within quarters, raising delivered costs for glassmakers and construction users. Freight can represent 30% of landed silica value on long hauls, incentivizing regional processing hubs and take-or-pay shipping contracts that sacrifice flexibility for cost stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Crystalline Dominance Drives Volume Growth

Crystalline grades account for 99.15% of the silica market in 2025 and are expanding at a 6.22% CAGR through 2031. Quartz remains indispensable in concrete, glass, and foundry molds thanks to thermal stability and a well-established supply chain. Tridymite and cristobalite fill smaller high-temperature ceramics niches, but their complex phase-conversion processing limits scale. Amorphous grades, while minor by tonnage, command premium pricing in green-tire compounds, high-solids battery slurries, and semiconductor CMP slurries. Specialty suppliers leverage hydrophilic and hydrophobic surface treatments that capture value beyond bulk tonnage.

Elevated environmental scrutiny encourages migration from mined crystalline inputs toward engineered amorphous forms with lower respirable-dust risk. Bio-based rice-husk silica meets this requirement while offering life-cycle carbon savings and proximity to Asian tire-manufacturing centers. Investment in vacuum flash reactors and low-alkali purification lines underscores the strategy of targeting smaller, higher-margin parcels rather than chasing commodity volume. As a result, the silica market continues bifurcating into high-purity, application-specific grades and bulk construction sand, with pricing divergence expected to widen through 2030.

By End-user Industry: Construction Leadership Meets Energy Transition

Building and construction retained 34.72% of the silica market share in 2025 and posts steady tonnage gains aligned with global infrastructure spending. Urbanization in China, India, and Indonesia fuels concrete and flat-glass demand, while European renovation codes elevate high-silica fiber-reinforced mortars that enhance structural durability. In North America, green-building certifications spur uptake of recycled and bio-based silica additives in low-carbon cement blends as architects pursue net-zero targets.

Shale oil and gas stands out with a 7.62% CAGR, reflecting sustained North American fracturing intensity and rising proppant loads per lateral well. Premium-grade Northern White sand, prized for crush strength and sphericity, competes with in-basin sands that reduce haul distances by 500 miles or more. Glass manufacturing maintains mid-single-digit growth as container-light-weighting partly offsets rising beverage and pharmaceutical consumption.

Geography Analysis

Asia-Pacific dominates the silica market with 41.00% share in 2025 and an 8.10% CAGR to 2031. China consumes over 200 million tons annually across construction, photovoltaic glass, and chemical derivatives, underpinned by strategic reserves and integrated beneficiation hubs. India’s highway expansion and smart-city programs lift domestic demand, while government subsidies accelerate rice-husk silica ventures that feed both local tire plants and export outlets.

North America holds a pivotal position in shale proppant supply, with Wisconsin, Texas, and Alberta deposits meeting stringent crush-strength specifications. Regional processing plants shorten supply chains for Gulf Coast glass furnaces, while Canadian producers capture demand from LNG construction and green-hydrogen infrastructure. Regulatory drivers, notably OSHA respirable-silica limits, push miners toward wet-processing and enclosed-handling systems that boost capex but lower insurance liabilities.

Europe presents stable, value-added demand centered on Germany, France, and the United Kingdom. Automotive and chemical users specify high-purity grades, and EU circular-economy directives promote recycled and bio-based inputs. Eastern European suppliers, led by Qemetica’s expanded Polish site, benefit from proximity to both Western OEMs and growing Turkish and North African construction markets. Investments in energy-efficient kiln technology and on-site solar arrays align with EU decarbonization rules, anchoring long-term regional competitiveness.

Competitive Landscape

The silica market is highly fragmented. Global leaders such as Cabot, Evonik, Wacker Chemie, and PPG’s divested precipitated-silica unit emphasize technology leadership and downstream integration. Regional specialists exploit geological advantages or niche purification know-how, while bio-based entrants pursue low-carbon positioning. Vertical integration gains momentum; glassmakers co-locate beneficiation plants, and tire companies ink long-term offtake deals to lock in precipitated-silica supply. Sustainability differentiates competitive positioning. Companies invest in closed-loop water circuits, low-NOx burners, and rice-husk ash valorization to meet investor ESG metrics.

Silica Industry Leaders

Sibelco

Covia Holdings LLC

Evonik Industries AG

QEMETICA

U.S. Silica (Apollo Funds)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: PPG completed the sale of its precipitated-silica products business to Qemetica for USD 310 million, including Lake Charles and Delfzijl plants.

- July 2024: U.S. Silica Holdings was acquired by Apollo funds for USD 1.85 billion, taking the producer private after 124 years of public operation.

Global Silica Market Report Scope

Silica, also known as silicon dioxide, is a compound of two elements in the earth's crust: silicon and oxygen. Currently, silica can be used in a wide range of applications. Silica sand is used in the form of Portland cement, mortar, and concrete, and sandstone is used in the construction of buildings and roads.

The market is segmented by type, end-user industry, and geography. By type, the market is segmented into amorphous and crystalline. By end-user industry, the market is segmented into building and construction, shale oil and gas, glass manufacturing, water treatment, and other end-user industries (paints and coatings, etc.). The report also covers the market sizes and forecasts for the silica market in 27 countries worldwide. For each segment, the market sizing and forecasts have been done based on volume (tons).

| Amorphous | Fumed/Pyrogenic |

| Hydrated | |

| Crystalline | Quartz |

| Tridymite | |

| Cristobalite |

| Building and Construction |

| Shale Oil and Gas |

| Glass Manufacturing |

| Water Treatment |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Qatar | |

| United Arab Emirates | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Type | Amorphous | Fumed/Pyrogenic |

| Hydrated | ||

| Crystalline | Quartz | |

| Tridymite | ||

| Cristobalite | ||

| By End-user Industry | Building and Construction | |

| Shale Oil and Gas | ||

| Glass Manufacturing | ||

| Water Treatment | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Qatar | ||

| United Arab Emirates | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What will global silica demand be in 2031?

The silica market size is projected to reach 794.03 million tons by 2031, reflecting a 6.31% CAGR.

Which region is growing fastest?

Asia-Pacific leads with an 8.10% CAGR, supported by construction, electronics, and downstream beneficiation policies.

Why are green tires important for silica suppliers?

Low-rolling-resistance tires use higher precipitated-silica loadings to cut vehicle energy loss, driving incremental specialty-silica volume.

How do occupational regulations affect producers?

OSHA and EU exposure limits require wet-processing, dust-suppression, and monitoring systems that raise operating costs but improve worker safety.

What is the outlook for bio-based rice-husk silica?

Commercial rice-husk ash projects in India and Southeast Asia lower carbon footprints by up to 60% and satisfy regional specialty-grade demand.

Page last updated on: