Short-Range Air Defense System (SHORAD) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 17.25 Billion |

| Market Size (2030) | USD 23.32 Billion |

| Growth Rate (2025 - 2030) | 6.22% CAGR |

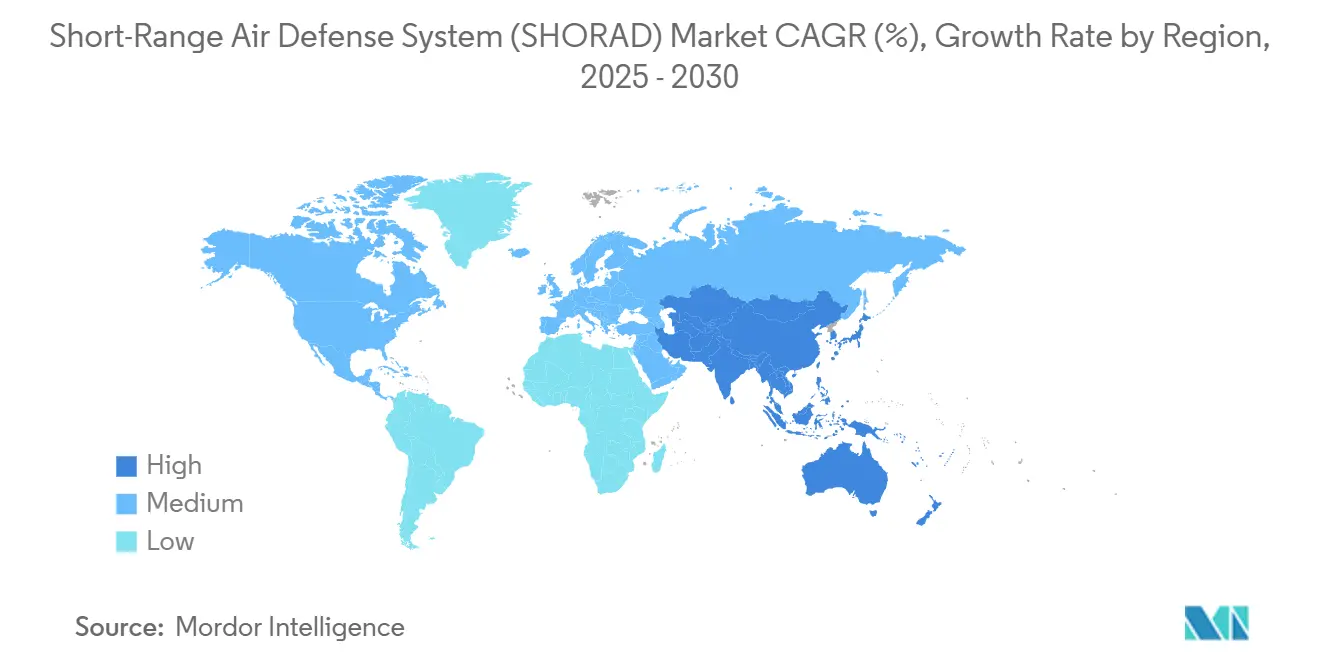

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

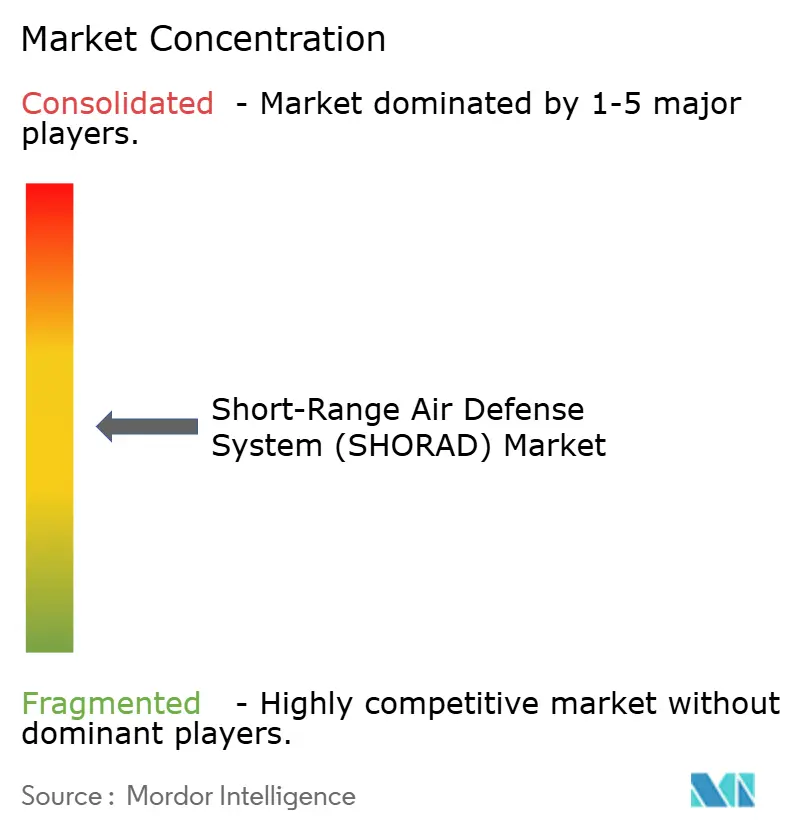

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Short-Range Air Defense System (SHORAD) Market Analysis by Mordor Intelligence

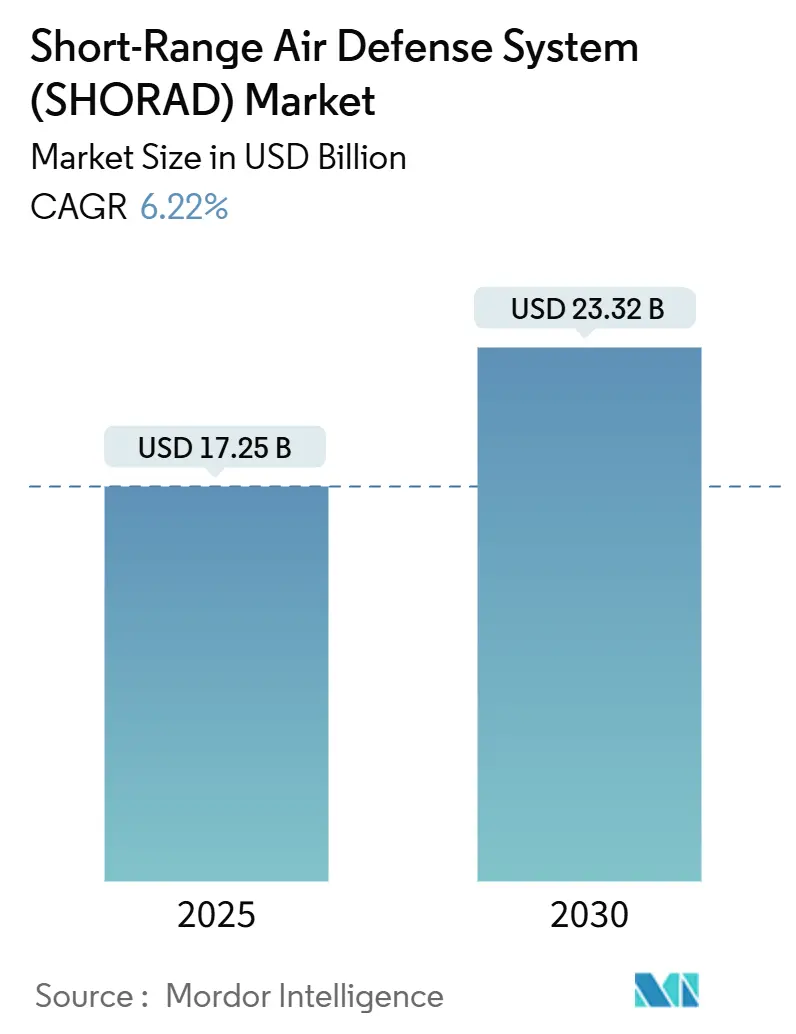

The short-range air defense system (SHORAD) market size stood at USD 17.25 billion in 2025 and is forecasted to reach USD 23.32 billion by 2030, reflecting a 6.22% CAGR that underscores defense agencies’ pivot toward layered, cost-effective air-defense architectures capable of defeating high-volume, low-cost aerial threats. Escalating drone warfare, stringent modernization roadmaps, and interoperability mandates combine to move procurement priorities away from large, single-purpose interceptors toward agile, modular solutions that integrate kinetic, electronic, and directed-energy effectors within common command-and-control networks. The cost asymmetry crisis, where missiles priced in the millions intercept drones costing thousands, amplifies demand for affordable munitions and drives investment in AI-enabled engagement automation that lowers workforce burdens and preserves inventories. As supply-chain fragility limits surge capacity for specialty components, multi-year contracts and allied co-production deals help ensure availability while spreading risk. At the same time, the emergence of vehicle-mounted laser demonstrators and man-portable VSHORADS prototypes accelerates the innovation cycle, giving smaller vendors a chance to disrupt incumbents through novel sensor-fusion software, open architectures, and rapid field-reconfiguration kits.

Key Report Takeaways

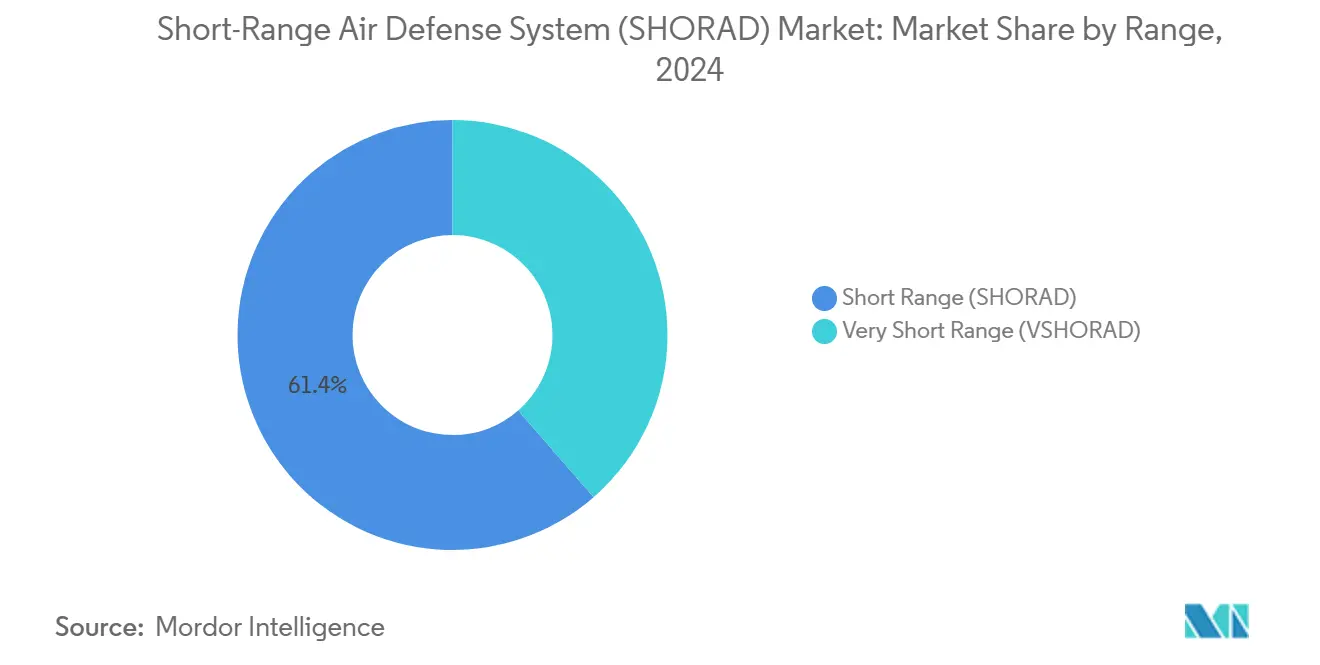

- By range, short-range platforms led with 61.40% of SHORAD market share in 2024; very short-range platforms are projected to expand at an 8.45% CAGR through 2030.

- By platform, land-based solutions accounted for 64.68% of the SHORAD market size in 2024, while air-based solutions registered the fastest 7.81% CAGR to 2030.

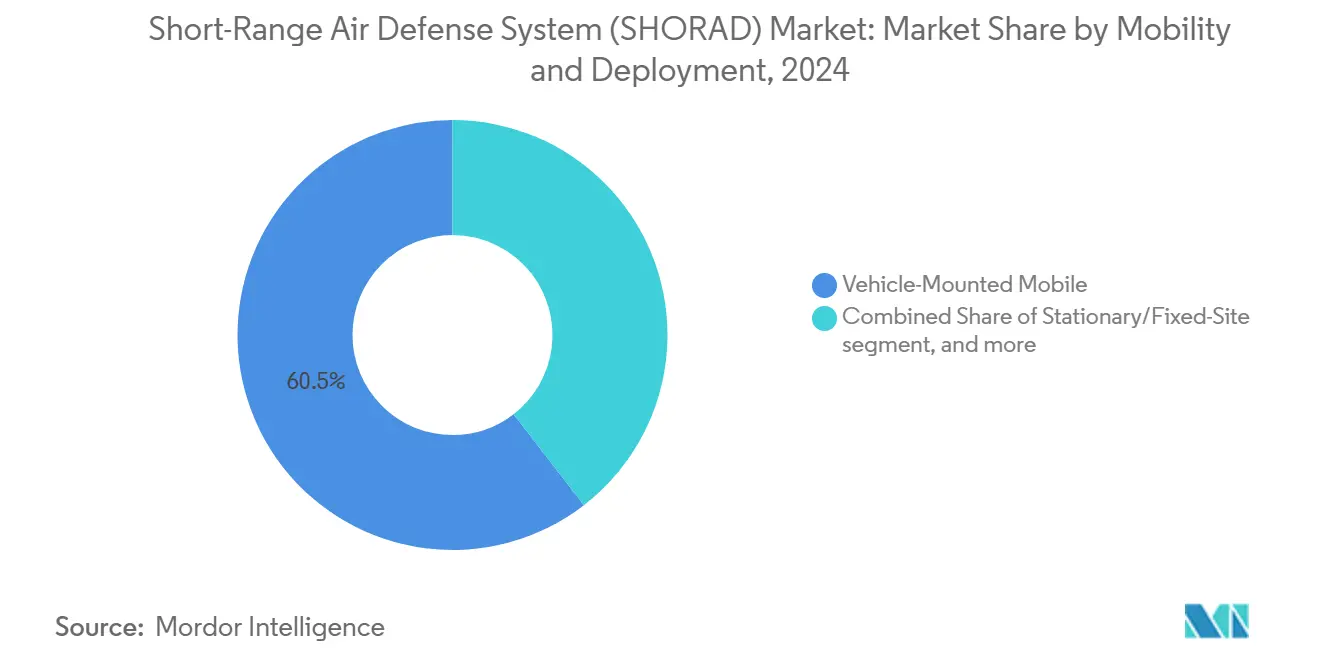

- By mobility, vehicle-mounted mobile configurations commanded 60.47% share of the SHORAD market size in 2024 and are advancing at a 7.30% CAGR through 2030.

- By guidance technology, radar-guided interceptors captured 53.78% share of the SHORAD market size in 2024; EO/IR guidance exhibits the fastest 8.74% CAGR between 2025 and 2030.

- By end user, military organizations held 83.41% of the SHORAD market size in 2024, whereas homeland security users are growing at a 9.74% CAGR over the same period.

- By geography, North America commanded 34.90% revenue share in 2024, whereas Asia-Pacific is advancing at a 7.57% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Short-Range Air Defense System (SHORAD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in drone and loitering-munition threats expanding mobile SHORAD procurement | +1.8% | Global, concentrated in Eastern Europe, Middle East, Indo-Pacific | Short term (≤ 2 years) |

| Modernization roadmaps (e.g., M-SHORAD, European ESSI) unlocking budgets | +1.2% | North America and EU, spill-over to NATO partners | Medium term (2-4 years) |

| Networked C2/sensor-fusion boosting SHORAD effectiveness | +0.9% | NATO core, expanding to AUKUS and Indo-Pacific allies | Medium term (2-4 years) |

| Counter-UAS layer now mandatory in layered air-defense architectures | +1.1% | Global, early adoption in conflict zones | Short term (≤ 2 years) |

| Modular gun-missile turrets enabling affordable legacy-vehicle upgrades | +0.7% | Global, emphasis on budget-constrained militaries | Long term (≥ 4 years) |

| Directed energy interceptors lowering cost-per-kill and sustainment load | +0.5% | Advanced militaries (US, UK, Israel, Japan) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Drone and Loitering-Munition Threats Expanding Mobile SHORAD Procurement

Russia’s AI-assisted Shahed drone variants, able to navigate under jamming and autonomously prioritize targets, have exposed vulnerabilities in static defenses and compelled armies to prioritize mobile SHORAD market procurements that blend electronic warfare, guns, missiles, and lasers into a single, truck-borne package. Accelerated fielding of the US M-SHORAD and Norwegian NOMADS programs exemplifies the urgency, with acceptance trials truncated to place vehicles in European units ahead of scheduled milestones. Doctrinal updates now emphasize shoot-on-the-move tactics and distributed sensor nodes to counter saturation attacks, incentivizing industry to design plug-and-play architectures that accept new radars or effector pods without hull redesign. The economics favor this agility; intercepting a USD 2,000 drone with a USD 12 laser shot versus a USD 150,000 missile preserves magazine depth and reduces operations-and-support costs.[1]Source: James Black, “David vs. Goliath: Cost Asymmetry in Warfare,” RAND Corporation, rand.org Consequently, procurement cycles that once spanned a decade now compress into three- to five-year bursts, benefiting suppliers capable of rapid prototype maturation and spiral upgrades.

Modernization Roadmaps Unlocking Defense Budgets

The US incremental approach to M-SHORAD, moving from gun-and-Stinger loadouts toward Stinger-HELLFIRE hybrids, demonstrates how defined roadmaps sustain recurring orders and budget lines regardless of near-term performance setbacks. Europe’s ESSI and EUR 500 million (USD 586.73 million) ammunition-production stimulus further cements long-run demand certainty, allowing tier-two contractors to invest in new propellant lines and qualified warhead casings that feed the SHORAD market. Governments endorse multiyear frameworks that reward on-time delivery with option tranches, reducing funding volatility and aligning contractor incentives with readiness targets. Standardization on Rheinmetall Skyranger 30 among five NATO nations illustrates cost savings through common spares and training pipelines. As a result, even smaller allies gain affordable access to advanced capabilities without bearing full non-recurring engineering expenses.

Networked C2/Sensor-Fusion Boosting SHORAD Effectiveness

NASAMS-derived command-and-control (C2) packages transplanted into wheeled platforms such as NOMADS allow compact fire units to tap remote radar tracks and battery-level engagement algorithms that allocate interceptors where they achieve the highest probability of kill. Growing adoption of NATO Mode 5 Level 2 IFF and STANAG-compliant data links ensures disparate launchers, radars, and electro-optics form a resilient mesh that shrugs off single-node losses. Machine-learning classifiers inside the engagement manager cross-cue sensors, reducing operator workload and accelerating decision loops essential for countering multi-axis drone swarms. Because software rather than hardware defines capability, field upgrades arrive via secure patches, keeping deployed formations current without forward-depot retrofits. These efficiencies persuade budget managers to extend networked upgrades to legacy batteries, broadening the addressable SHORAD market across new builds and recapitalizations.

Counter-UAS Layer Now Mandatory in Layered Air-Defense Architectures

Army test events, such as DoD TREX 24-2, validated fully autonomous gun turrets that closed kill chains against 20-drone swarms in under 30 seconds. This set a doctrinal precedent: every maneuver brigade must travel with an organic, counter-UAS-capable fire team. NATO’s 2024 air-and-missile-defense posture update elevated short-range counter-UAS capability from optional to “core task,” pushing member states to reprogram funds away from legacy medium-range systems toward flexible short-range air defense systems market solutions.[2]Source: NATO Parliamentary Assembly, “NATO’s Evolving Air and Missile Defence Posture,” nato-pa.int Vendors now bundle drone-detection radars, RF jammers, and soft-kill spoofers as standard subsystem options, lowering integration risk. Consequently, acquisition staffs evaluate bids on all-domain coverage metrics rather than interceptor range alone, intensifying competition among primes and niche EW specialists.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and lifecycle cost amid budget ceilings | -0.8% | Global, acute in developing nations | Medium term (2-4 years) |

| Multi-sensor integration complexity causing schedule overruns | -0.6% | Advanced militaries pursuing networked solutions | Short term (≤ 2 years) |

| Export-control/ITAR barriers throttling technology transfer | -0.4% | Global, concentrated in allied partnerships | Long term (≥ 4 years) |

| Shortage of trained SHORAD crews delaying operational readiness | -0.5% | NATO and allied nations expanding air defense | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Cost Amid Budget Ceilings

Flat defense toplines force ministries to prioritize across competing needs, and analysts warn that sustained high-intensity operations would exhaust current US missile inventories within one week, a pressure that curtails procurement of premium interceptors and channels money toward lower-cost options.[3]Source: Wilson Beaver & Jim Fein, “America Must Remedy Its Dangerous Lack of Munitions Planning,” The Heritage Foundation, heritage.org European treasuries likewise juggle ammunition-production investments against immediately deployable capability gaps, prompting questions over whether short-range air defense systems industry programs can scale fast enough without cannibalizing other modernization plans. Lifecycle costs, training, spares, and depot-level maintenance often triple initial purchase prices, discouraging cash-constrained buyers from ordering state-of-the-art solutions. OEMs respond with performance-based logistics contracts and subscription-style software updates to flatten expenditure curves, yet skepticism persists among acquisition officers wary of vendor lock-in.

Multi-Sensor Integration Complexity Causing Schedule Overruns

M-SHORAD’s early software instability, rooted in the fusion of radar, EO/IR, and electronic-warfare feeds, underscores the engineering complexity of real-time target-classification pipelines. Verification in contested electromagnetic environments requires exhaustive test matrices that extend development times and drive cost growth. Cyber-hardening features, mandatory under new NATO AQAP guidelines, further complicate architecture, demanding redundancy that may reduce payload capacity. Smaller vendors with cutting-edge algorithms often lack the certification infrastructure to satisfy these standards, narrowing the supplier base and slowing innovation diffusion across the short-range air defense systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: VSHORADS Drive Growth Despite SHORAD Dominance

Short-range batteries captured 61.40% of the SHORAD market share in 2024, reflecting decades-old investments in missile-gun hybrids optimized for maneuver brigades. Nevertheless, very short-range systems post an 8.45% CAGR through 2030 as infantry units demand agile, man-portable defenses that negate quadcopter and loitering-munition penetrations at sub-5 km envelopes. India’s 20.5 kg VSHORADS prototype proved lethal against 400 m/s drones, validating lightweight dual-band seekers that close the performance gap with larger missiles. The short-range air defense system market size for VSHORADS thus expands beyond special forces to regular battalions, especially where air dominance is contested.

The surge stems from doctrinal emphasis on distributed operations requiring every platoon to self-protect rather than rely solely on brigade-level umbrellas. As soft-launch motors reduce back-blast and allow firing from enclosures, urban-operation suitability rises, further widening the addressable short-range air defense system market. Meanwhile, SHORAD incumbents preserve relevance by integrating proximity-fused airburst rounds and AI fire control, ensuring kill probability against swarms. Convergence between range classes will likely create hybrid procurement patterns where armies blend wrist-strap VSHORADS with truck-mounted SHORAD, mirroring combined-arms philosophy.

By Platform: Land-Based Supremacy Challenged by Air-Based Innovation

Land configurations commanded 64.68% of 2024 revenue, testifying to the enduring requirement to shield columns, bases, and depots. Yet air-based solutions grow 7.81% annually as rotary-wing and UAV carriers host podded launchers, extending protective bubbles ahead of convoys. Kongsberg’s NOMADS air-transportable launcher offsets the limited deck space on light utility helicopters by using remote, ground-launched micro-missiles cued from airborne sensors, illustrating cross-domain synergy.

Sea-based programs move cautiously due to integration costs and shipboard power constraints, though Japan’s destroyer-class lasers signal a coming upturn once megawatt-class generators proliferate. Air-mobility drives suppliers to reduce weight via composite canisters and GaN radars, innovations that feed back into land variants, making platform lines increasingly interdependent within the short-range systems industry.

By Mobility and Deployment: Vehicle-Mounted Mobile Dominance Reflects Operational Reality

Vehicle-mounted solutions accounted for 60.47% of 2024 revenue and outpaced all others at 7.30% CAGR, confirming that survivability in contested theaters hinges on shoot-and-scoot profiles. Wheeled 8×8s with independent suspensions traverse unprepared roads, keeping pace with mechanized brigades and reducing logistical drag. Skyranger 30’s acceptance across five NATO armies highlights shared confidence in twin-gun turrets and ready-rack missile cells.

Fixed-site arrays remain essential for strategic infrastructure but relinquish budget share as their stationary emissions make them prime targets for anti-radiation weapons. Man-portable systems fill urban and mountainous gaps yet struggle with sustained firing rates, limiting their contribution to the overall short-range air defense systems market size. Trends indicate future architectures will layer vehicle-mounted kinetic interceptors with tethered UAV sensors and truck-mounted high-energy lasers, fusing mobility with persistent surveillance.

By Guidance Technology: Radar-Guided Leadership Faces IR/EO Challenge

Radar-guided interceptors held 53.78% of the 2024 value because active seekers deliver all-weather, fire-and-forget capability, a critical trait against cruise-missile profiles. However, infrared/electro-optical missiles grow faster at 8.74% CAGR as passive homing sidesteps jamming and reduces RF signature. VSHORADS dual-band imagers extend lock-on range beyond 6 km, narrowing performance gaps with costlier radar variants.

Beam-riders retain niche roles defending static assets where limited line-of-sight simplifies guidance. Still, emerging AI fusion allows multi-mode seekers to toggle between RF and IR depending on the countermeasure environment. Consequently, procurement splits will soften, with composite seeker packages blurring categorical distinctions and enlarging overall short-range air defense systems market capability.

By End User: Military Dominance Faces Homeland-Security Growth

Military buyers contributed 83.41% of 2024 revenue, buoyed by national-defense allocations and multinational exercises that validate interoperability standards. Yet homeland-security agencies expand at 9.74% CAGR, adding stadium, refinery, and airport protection contracts that require low-collateral, radio-frequency, or net-capture solutions integrated into civil air-traffic systems.

Civil authorities prioritize discriminate engagement and minimal electromagnetic spillover, prompting suppliers to adapt military sensors with software-defined geofencing and escalation-of-force protocols. The short-range air defense systems market responds with scalable offerings from tripod-mounted RF jammers to integrated drone-detection radars priced within municipal budgets, broadening the customer base beyond defense ministries.

Geography Analysis

North America led with a 34.90% share in 2024, anchored by the US Army's accelerated fielding of M-SHORAD battalions to Europe and the Indo-Pacific. NORAD modernization funds buoy Canadian procurement of Stinger reloads and mobile launchers, while Mexico explores anti-drone jammer arrays for border infrastructure. High domestic R&D outlays nurture directed-energy prototypes, positioning regional primes to export second-generation laser modules as power-pack densities improve. However, specialty steel and solid-rocket motor bottlenecks may dampen future output unless bilateral supply-base initiatives materialize.

Asia-Pacific registers the fastest 7.57% CAGR through 2030, driven by India's indigenous VSHORADS rollout, Japan's shipboard laser deployments, and South Korea's M-SAM export surge. Regional tension over contested airspace stimulates multisource procurement strategies, blending US, Israeli, and domestic systems to hedge embargo risks. Australia's LAND 19 Phase 7B boosts joint intercept-network design, creating opportunities for data-link suppliers. With diverse climates from tropical archipelagos to Himalayan plateaus, platforms must tolerate temperature extremes, encouraging ruggedized designs unique to this theater.

Europe maintains robust demand through coordinated ESSI frameworks and Rheinmetall Skyranger deliveries, targeting 50-vehicle fleets among five NATO members by 2027. The EU's ammunition-production incentive accelerates propellant line expansion, strengthening regional autonomy from external suppliers. Operational lessons from Ukraine propel interim buys such as the UK's search for a Stormer replacement that favor available, proven platforms. Nordic countries pursue joint acquisitions to spread costs and ensure standard sustainment pipelines, reinforcing long-term growth for the continent's short-range air defense systems market.

Competitive Landscape

The short-range air defense system (SHORAD) market is moderately fragmented. Five leading firms, RTX Corporation, Lockheed Martin Corporation, Saab AB, MBDA, and Thales Group, collectively hold the semi-consolidated market concentration. At the same time, dozens of specialized radar, effector, and software houses compete for subsystem slots. Traditional primes exploit extensive certification pipelines and secure facility footprints, yet newcomers leverage venture-capital agility to iterate AI algorithms faster. Anduril’s purchase of Numerica’s C2 unit offers a case study in private-equity-funded vertical integration that challenges legacy time lines.

Competition increasingly hinges on open-architecture compliance and software-upgradability. General Dynamics capitalizes on its RIwP turret’s chassis-agnostic design to pitch the same weapon station across US and European vehicle programs, reducing unit costs through volume production. Rheinmetall’s Skynex marketing highlights plug-and-play data-link adapters that tie into existing NATO fire-control loops without proprietary gateways, reflecting customer demand for interoperability over standalone performance metrics. Contract evaluations now score cyber-resilience and AI transparency alongside magazine depth, inviting partnerships between code-first startups and hardware incumbents to satisfy multifaceted bid criteria.

Supply-chain resilience becomes a differentiator as governments scrutinize single-source vulnerabilities. Firms offering multi-site manufacturing, such as RTX’s co-production with Polish partners for Patriot components, gain favor in source-selection boards aiming to de-risk political dependencies. Consequently, the competitive landscape remains fluid, with alliances forming around regional offset requirements and technology-sharing agreements that realign market positions annually.

Short-Range Air Defense System (SHORAD) Industry Leaders

RTX Corporation

Lockheed Martin Corporation

MBDA

Thales Group

Saab AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Sweden signed a EUR 274 million (USD 321.53 million) deal with Polish manufacturer Mesko to procure Piorun MANPADS. Starting in 2026, deliveries will enhance Sweden’s air defense capabilities, joining nations like the US and Norway in utilizing this system, praised for its portability and effectiveness.

- January 2025: Saudi Arabia discreetly acquired 39 Russian-made Pantsir-S1M air defense systems in a USD 2.3 billion deal. The contract includes 10 mobile command posts, missiles, transport vehicles, and communication systems, with payments made to Russian arms exporter ROSOBORONEXPORT under the agreement.

Global Short-Range Air Defense System (SHORAD) Market Report Scope

| Very Short Range (VSHORAD) |

| Short Range (SHORAD) |

| Land-Based |

| Sea-Based |

| Air-Based |

| Stationary/Fixed-Site |

| Vehicle-Mounted Mobile |

| Man-Portable (MANPADS) |

| Radar-Guided |

| Electro-Optical/Infrared (EO/IR) |

| Command Link/Beam-Rider |

| Other |

| Military |

| Homeland Security |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Range | Very Short Range (VSHORAD) | ||

| Short Range (SHORAD) | |||

| By Platform | Land-Based | ||

| Sea-Based | |||

| Air-Based | |||

| By Mobility and Deployment | Stationary/Fixed-Site | ||

| Vehicle-Mounted Mobile | |||

| Man-Portable (MANPADS) | |||

| By Guidance Technology | Radar-Guided | ||

| Electro-Optical/Infrared (EO/IR) | |||

| Command Link/Beam-Rider | |||

| Other | |||

| By End User | Military | ||

| Homeland Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is global demand growing for short-range air-defense solutions?

The short-range air defense system (SHORAD) system market is expanding at a 6.22% CAGR between 2025 and 2030, rising from USD 17.25 billion to USD 23.32 billion.

Which region will record the strongest spending increase?

Asia-Pacific posts the highest 7.57% CAGR as India, Japan, and South Korea accelerate indigenous programs and export partnerships.

What technology shift is most influencing new purchase decisions?

Adoption of AI-enabled sensor fusion and autonomous engagement is reshaping requirements, emphasizing software-centric upgrades over hardware-only specs.

Why are vehicle-mounted launchers favored over fixed sites?

Mobile platforms offer shoot-and-scoot survivability against precision strikes, commanding 60.47% of 2024 revenue and the highest 7.30% CAGR.

How are cost pressures being mitigated in procurement?

Modular turrets, directed-energy interceptors at USD 12 per shot, and performance-based logistics contracts help flatten lifecycle expenses.

What is the outlook for homeland-security applications?

Civil agencies are expected to grow at a 9.74% CAGR as airports, stadiums, and energy facilities adopt low-collateral drone-defense systems.

Page last updated on: