Air-to-Air Missiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 7.36 Billion |

| Market Size (2030) | USD 10.74 Billion |

| Growth Rate (2025 - 2030) | 7.85% CAGR |

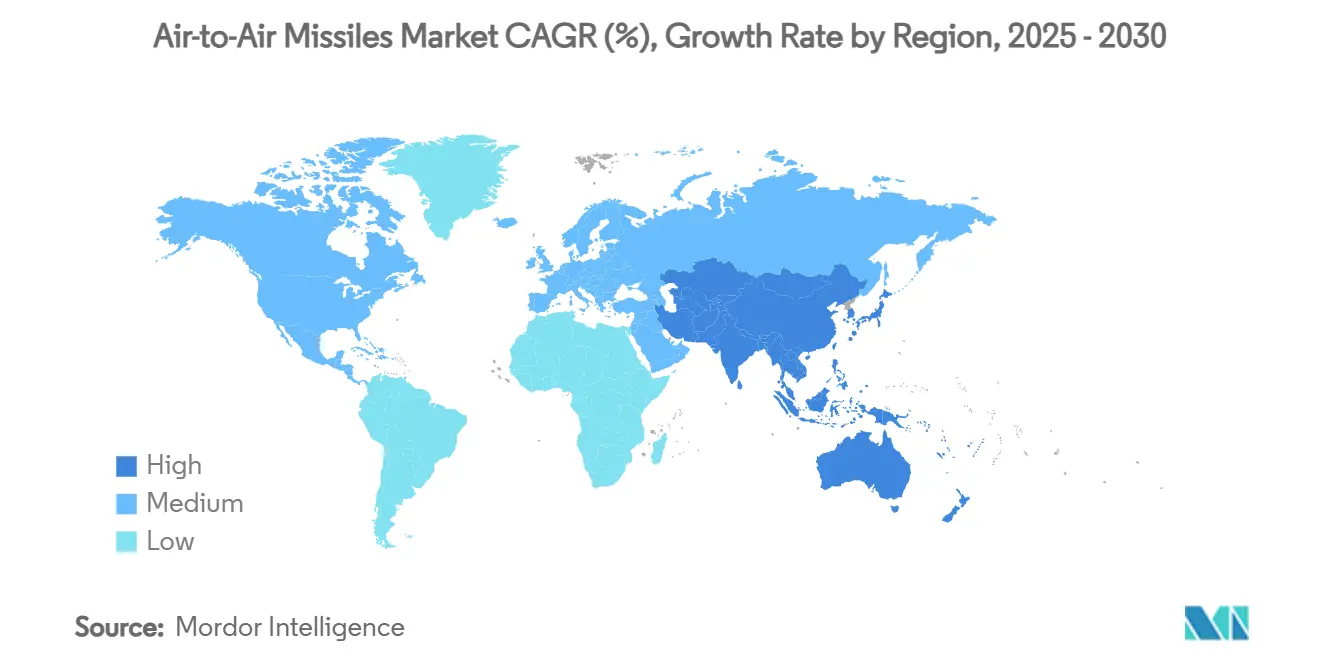

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air-to-Air Missiles Market Analysis by Mordor Intelligence

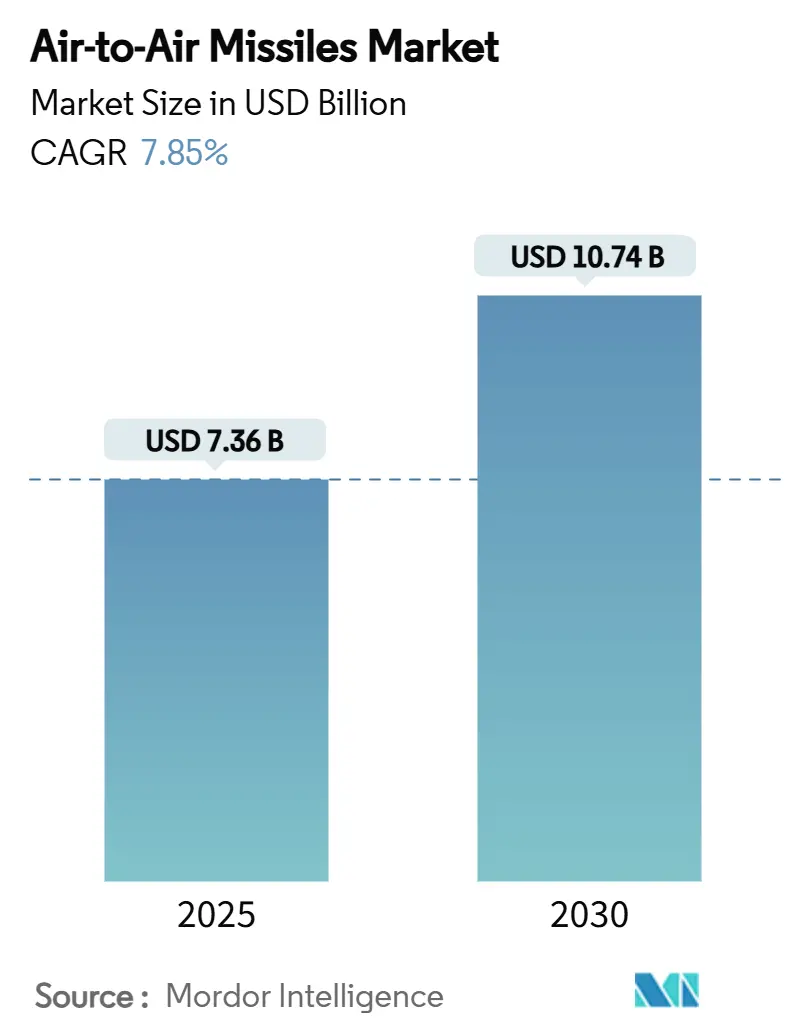

The air-to-air missiles market size stands at USD 7.36 billion in 2025 and is forecasted to reach USD 10.74 billion by 2030, registering a 7.85% CAGR over 2025-2030. The acceleration mirrors governments' reordering of procurement budgets toward next-generation air-combat capabilities, a trend reinforced by the January 2025 revision of the Missile Technology Control Regime (MTCR) that simplifies exports to trusted allies. Asia-Pacific supplies the fastest expansion at a 9.45% CAGR on the back of Chinese military modernization, whereas North America retains the most significant regional foothold with 28.58% 2024 revenue share. Hypersonic missiles headline the technology race with a 10.76% CAGR, reflecting the premium on systems that defeat layered air defenses. Fixed-wing aircraft dominate launch platforms at 74.85% 2024 share, yet unmanned aerial vehicles (UAVs) are rising 9.71% per year as autonomous concepts mature. Competitive pressure has intensified, with MBDA doubling missile output in 2024 to post a record EUR 4.9 billion (USD 5.76 billion) revenue. Meanwhile, component shortages force incumbents like Raytheon to forge European partnerships for rocket-motor supply continuity.

Key Report Takeaways

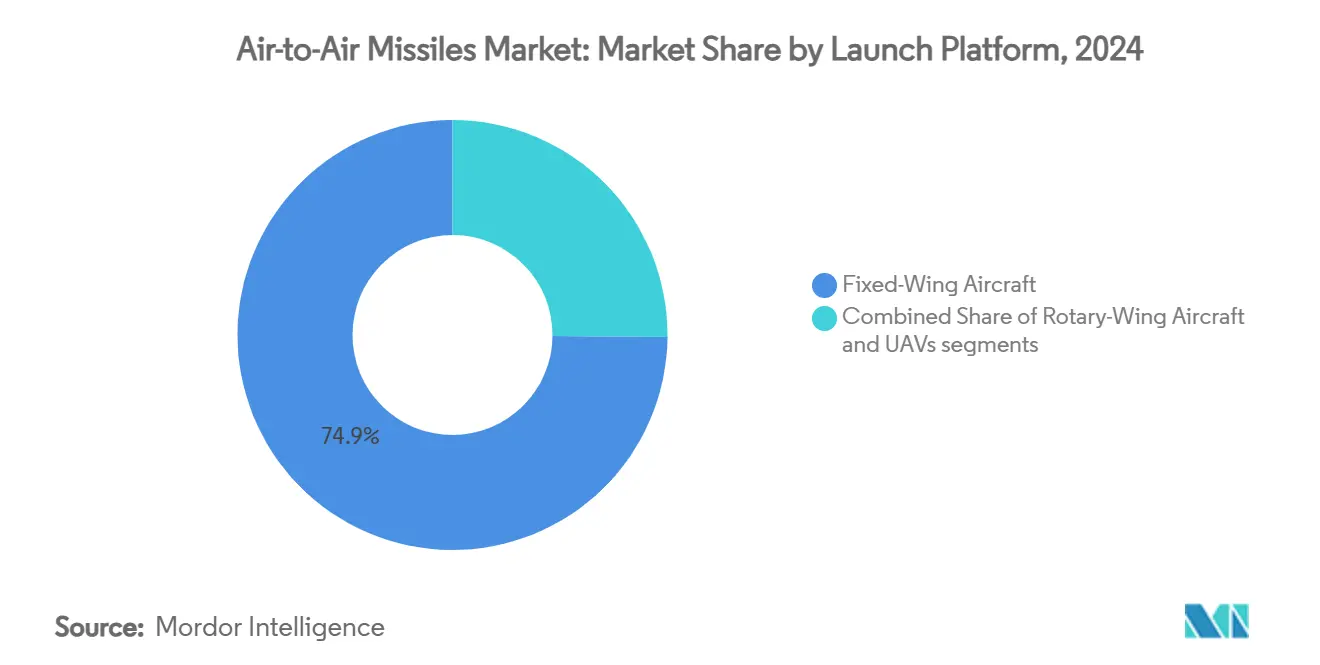

- By launch platform, fixed-wing aircraft commanded 74.85% revenue share in 2024, while UAV-based launches posted the fastest 9.71% CAGR to 2030.

- By range, beyond-visual-range (BVR) systems held 57.61% of the air-to-air missiles market share in 2024 and are advancing at an 8.24% CAGR through 2030.

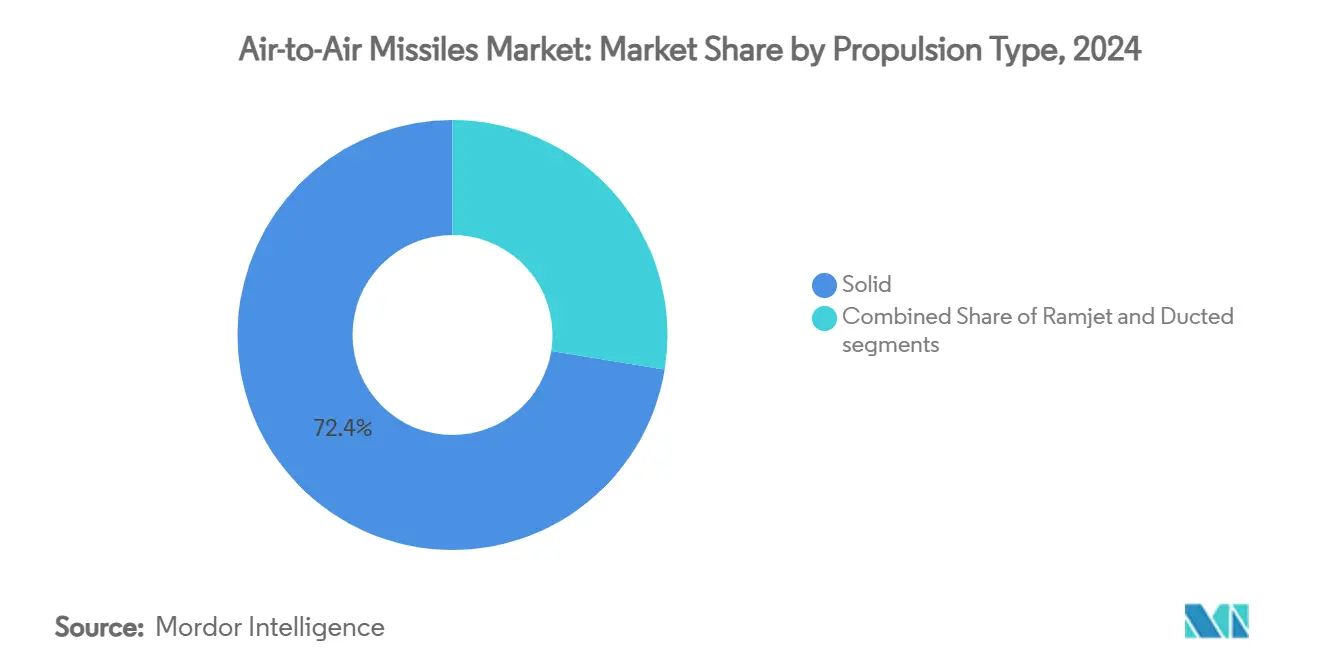

- By propulsion, solid-fuel designs accounted for 72.43% of the 2024 air-to-air missiles market size, whereas ramjet propulsion is projected to expand at a 9.88% CAGR by 2030.

- By guidance, active-radar homing seized 48.34% market share in 2024, and dual-mode seekers are forecasted to grow 9.22% annually to 2030.

- By speed class, supersonic weapons led with 58.22% 2024 revenue, yet hypersonic missiles will post the quickest 10.76% CAGR during the outlook.

- By geography, North America held 28.58% revenue share in 2024, while Asia-Pacific is set to deliver the highest 9.45% CAGR over 2025-2030.

Global Air-to-Air Missiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geopolitical tensions driving modernization of fighter aircraft fleets | +1.2% | Global, concentrated in Asia-Pacific and Eastern Europe | Medium term (2-4 years) |

| Rising global defense investments supporting advanced air combat capabilities | +1.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Increasing adoption of network-centric warfare fueling demand for beyond-visual-range (BVR) missiles | +1.5% | NATO and Five-Eyes states | Medium term (2-4 years) |

| Advances in missile miniaturization enabling increased payload capacity per aircraft | +0.9% | US, Europe, Israel | Long term (≥ 4 years) |

| Integration of dual-pulse motors improving end-game maneuverability and kill probability | +0.7% | Nations with indigenous programs | Long term (≥ 4 years) |

| Expanding need for air-launched missile solutions to counter unmanned aerial threats | +0.6% | Conflict zones and border regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Geopolitical Tensions Driving Modernization of Fighter Aircraft Fleets

Russia’s war in Ukraine has moved many European states from gradual upgrades to urgent replacement of Cold War stockpiles. Germany green-lighted IRIS-T Block II and the United Kingdom approved a GBP 6.5 billion (USD 8.76 billion) complex-weapons framework with MBDA in 2025, underscoring how conflict proximity galvanizes missile demand. Japan’s USD 3.64 billion AMRAAM order aligns its air arm with US systems, highlighting the linkage between alliance strategy and procurement choices. The cumulative effect keeps backlogs robust for at least the medium term, especially as alliance partners insist on interoperable inventories.

Rising Global Defense Investments Supporting Advanced Air Combat Capabilities

NATO counted 23 members at the 2%-of-GDP defense-spend threshold in 2025, ensuring predictable funding streams for missile modernizations. Washington’s USD 886 billion FY 2025 defense bill carves out dedicated lines for AIM-260, Sidewinder Block II, and early hypersonic increments. Similar moves in Australia, South Korea, and India anchor longer-cycle R&D budgets, giving suppliers the confidence to expand capacity despite inflationary cost headwinds.

Increasing Adoption of Network-Centric Warfare Fueling Demand for Beyond-Visual-Range Missiles

Fourth- and fifth-generation fighters now share real-time track files via improved Link-16 and MADL, which allows missiles to receive mid-course updates from remote sensors. Lockheed Martin’s Sniper networked pod and L3Harris tactical data-link upgrades turn missiles into distributed nodes rather than single-platform assets.[1]L3Harris, “Link-16 Tactical Data Link Upgrades,” l3harris.com The shift multiplies lethality: fewer shooters can police wider airspace, thereby raising volume requirements for BVR rounds able to exploit external cueing.

Advances in Missile Miniaturization Enabling Increased Payload Capacity Per Aircraft

Programs such as the Compact Medium-range Missile Technology demonstrator shrink length and diameter while preserving range, enabling stealth aircraft to carry double or triple the usual allotment inside bays.[2]US DoD, “DOT&E FY 2023 Annual Report,” dote.osd.mil Higher load-outs per sortie let operators saturate defenses, a key advantage against numerically superior adversaries. Miniaturized airframes also slash storage footprints aboard carriers and dispersed forward bases, appealing to navies and expeditionary forces constrained by magazine depth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy development timelines and complex qualification processes | -0.8% | Global, especially new entrants | Long term (≥ 4 years) |

| Stringent export control regimes limiting global market access | -0.5% | Non-allied nations | Medium term (2-4 years) |

| Electromagnetic spectrum congestion affecting radar seeker performance | -0.4% | Global, with concentration in high-density military regions | Short term (≤ 2 years) |

| Constraints imposed by stealth doctrines due to visible exhaust plume signatures | -0.3% | Advanced military nations with stealth aircraft programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Development Timelines and Complex Qualification Processes

Advanced missiles often require 8-12 years from concept to fielding because propulsion, seeker, and control subsystems demand sequential testing under extreme conditions. The US Air Force’s scrapping of the ARRW hypersonic project after multiple failures highlights how setbacks can wipe out a decade of R&D in one budget cycle. Smaller suppliers struggle to finance such long gestations, which curtails market dynamism and keeps incumbents entrenched.

Stringent Export Control Regimes Limiting Global Market Access

Even after the 2025 MTCR refresh, US ITAR, EU Dual-Use, and national rules restrict range, payload, and seeker exports. Licensing can still last 6-12 months and often ends with technology downgrades for third-party customers. Vendors must, therefore, maintain variant lines to comply with disparate rules, raising unit costs and complicating inventory management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Launch Platform: Fixed-Wing Dominance Faces UAV Disruption

Fixed-wing aircraft generated 74.85% of 2024 revenue, confirming their continuing centrality to airpower doctrine. The ongoing F-35, Rafale, and KF-21 procurement waves drive the segment's market growth. Yet UAV integrations are scaling rapidly: General Atomics teamed with Rafael to adapt the Bullseye missile for MQ-9, offering manned-unmanned teaming where Reapers feed data to F-35s that then delegate shots back to unmanned shooters.[3]General Atomics, “GA-ASI and Rafael to Integrate Bullseye Air-to-Air Missile,” ga-asi.com This paradigm boosts magazine depth without risking pilots, explaining the 9.71% CAGR attached to UAV launches through 2030.

The disruptive potential of UAV carriage reshapes force-structure math. A single tanker-supported drone orbit can loiter with half a dozen BVR rounds, freeing fighters for penetration tasks. Emerging swarming concepts even envisage attritable loyal-wingman drones armed with two mini-missiles apiece, creating layered shot-density that classical force planners lacked. Suppliers respond with interface-agnostic pylons, common data layers, and lighter thermal batteries. These innovations point to a blended fleet where fixed-wing aircraft remain the high-value sensor-shooter hubs while UAVs provide the expendable volume-fire component, re-balancing the air-to-air missiles market toward distributed lethality.

By Range: Beyond-Visual-Range Systems Drive Strategic Advantage

Beyond-visual-range (BVR) rounds captured 57.61% of the air-to-air missiles market share in 2024, thanks to their ability to neutralize threats beyond 100 km. The segment is projected to grow at an 8.24% CAGR to 2030 as integrated sensor networks feed mid-course updates and electronic protection suites improve end-game tracking. Short-range missiles preserve a vital backstop for within-visual-range knifefights; demand remains tied to nations operating legacy aircraft fleets without the radar aperture to exploit long-range shots.

BVR ascendancy links directly to the proliferation of active-electronically scanned array radars and off-board cueing from airborne early-warning and ground-based sensors. The kill-web concept means a missile launched from one fighter can ride guidance data from a second platform, complicating adversary defense and squeezing reaction windows. As air forces adopt doctrines that avoid close-in merges, BVR stock levels swell and drive supplier focus toward improved loft trajectories, seeker sensitivity, and data-link hardening against jamming.

By Propulsion Type: Solid Reliability Meets Ramjet Innovation

Solid-fuel motors delivered 72.43% of 2024 revenue due to their storability, simple logistics, and decades of incremental refinement. Still, the air-to-air missiles market size for ramjet-powered weapons is forecasted to expand at a 9.88% CAGR through 2030 as nations seek to outrange adversary interceptors.[4]GE Aerospace, “Dual-Mode Ramjet Propulsion Advances,” geaerospace.com Ducted rocket concepts provide a hybrid middle ground but remain costlier than solid motors and less range-efficient than true ramjets.

Ramjet adoption hinges on material advances: new high-temperature composites and additive-manufactured combustors sustain burn well above Mach 3. The technology unlocks 200-plus kilometer no-escape zones, empowering fighters to target tankers, AWACS, and ISR assets whose removal blunts an opponent’s situational awareness. Suppliers acknowledge the niche orientation—only major powers field the sensors and tactics to employ such weapons—yet see premium pricing and sovereign-capability appeal as enough to justify production lines. Solid motors will continue to dominate bulk purchases, particularly for export variants that prioritize simplicity and cost control.

By Guidance: Active Radar Homing Leads Dual-Mode Evolution

Active radar seekers held 48.34% of 2024 sales because “fire-and-forget” shots free the launch platform to evade. Meanwhile, dual-mode seekers—typically radar plus imaging-infrared—will post a 9.22% CAGR as electronic-warfare contests intensify. MBDA’s AI-enabled Orchestrike architecture lets the SPEAR family switch between modes in flight, maintaining track even under targeted jamming. Infrared-only designs persist for low-signature engagements but lag growth owing to their weather sensitivity.

Artificial intelligence now supervises target discrimination, clutter rejection, and even last-second fuze optimization, lifting kill performance by double-digit percentages in trials. Dual-mode packages mitigate single-spectra weakness; the infrared channel takes over if a target pops chaff against radar. The approach boosts inventory resilience, a selling point for nations facing adversaries fielding complex decoys or next-gen DIRCM (directed infrared countermeasure) defenses.

By Speed Class: Supersonic Dominance Yields to Hypersonic Innovation

Supersonic rounds still anchor 58.22% of 2024 turnover, offering the best compromise between cost, size, and manufacturing maturity. Hypersonic weapons, however, are on a 10.76% CAGR trajectory as operators chase first-shot, first-kill advantages against peer air defenses. Subsonic missiles remain specialty tools for long-endurance and low-observable missions where speed trades off for stealth and persistence.

Hypersonics compress engagement timelines to mere seconds; defending aircraft may lack sufficient time to dispense countermeasures or maneuver. Development risk remains high—ARRW cancellation underscores propulsion and guidance hurdles—but joint US Army-Navy programs show the industrial base maturing beyond laboratories. Early operational capability could tilt regional balances, incentivizing rivals to accelerate counter-hypersonic research and ensuring a sustained innovation cycle that keeps the air-to-air missiles market dynamic.

Geography Analysis

North America preserved a 28.58% 2024 revenue lead, powered by the United States’ USD 886 billion defense budget and its multibillion-dollar AIM-260 and AIM-9X Block II programs. Canada’s NORAD modernization adds a modest uptick, but the region’s growth is mainly based on US procurement stability. Supply bottlenecks—specifically rocket-motor casings—delay deliveries, prodding prime contractors to secure secondary sources across Europe in 2025.

Asia-Pacific recorded the highest 9.45% regional CAGR forecast as China’s force expansion spurs neighbors to rearm. Japan’s USD 3.64 billion AMRAAM buy includes co-production that anchors a domestic missile line and embeds US-Japan interoperability. South Korea integrates Meteor rounds on KF-21 prototypes while India’s Astra Mk-II tests move toward serial production, showing regional states’ dual foreign acquisition and indigenous development strategy. ASEAN buyers such as Indonesia weigh BrahMos and other Indo-Pacific offerings, underscoring how local supply chains support growth momentum.

Europe advances steadily, lifted by NATO’s 2% target and Ukraine-driven urgency. The United Kingdom’s GBP 6.5 billion (USD 8.76 billion) complex-weapons agreement and Germany’s IRIS-T Block II upgrades exemplify accelerated funding. EU Defence-Industrial policy tilts major procurements toward continental suppliers, which helped place MBDA on the SAMP/T NG shortlist against the US Patriot in 2025. Middle East and Africa register lower absolute volumes yet attract premium-value deals such as the UAE’s 300-round Meteor package for Rafale—a signal that wealthy regional air forces seek parity with peer coalitions.

Competitive Landscape

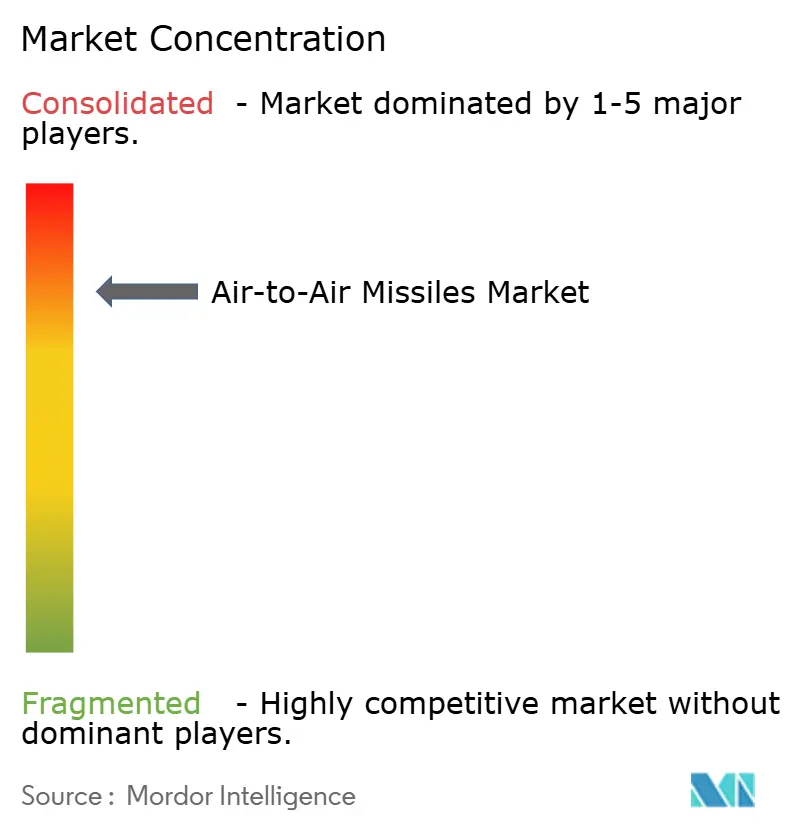

Market concentration remains high. The top five vendors account for over 65% of 2024 shipments, led by MBDA, RTX Corporation, Lockheed Martin Corporation, Rafael Advanced Defense Systems Ltd., and China’s CASIC. MBDA’s EUR 4.9 billion (USD 5.76 billion) 2024 turnover and doubled output reveal how European houses are scaling to exploit NATO demand. Rocket-motor deficits prompted Raytheon to sign co-production memoranda with Avio (Italy) and Nammo (Norway), illustrating how supply-chain resilience now rivals seeker sophistication as a success factor.

Strategic cooperation blurs competition lines. General Atomics collaborates with Rafael on a UAV-launched Bullseye missile, while Kratos pairs with Israel’s Prometheus Energetics to refine air-breathing propulsion for attributable drones. AI integration emerges as a differentiator; MBDA’s Orchestrike and Lockheed’s LIFT seeker logic promise adaptive engagement, raising customer switching costs once embedded. Niche challengers concentrate on guidance miniaturization and modular seekers but face steep certification hurdles, meaning incumbent share erosion will be gradual.

Air-to-Air Missiles Industry Leaders

RTX Corporation

MBDA

Lockheed Martin Corporation

Rafael Advanced Defense Systems Ltd.

China Aerospace Science and Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Raytheon, a part of RTX Corporation, received a contract from the US Navy for AIM-9X-4 Block II All Up Round (AUR) air-to-air missiles. The contract encompasses 492 rockets for the US Navy, 456 for the US Air Force, and 808 for Foreign Military Sales (FMS) partners, strengthening air combat capabilities for US and allied forces.

- October 2024: Raytheon received a USD 736 million contract from the US Navy to manufacture AIM-9X SIDEWINDER missiles. The contract focuses on the Block II variant, which includes hardware upgrades to resolve obsolescence issues and enhance performance and reliability.

Global Air-to-Air Missiles Market Report Scope

| Fixed-Wing Aircraft |

| Rotary-Wing Aircraft |

| Unmanned Aerial Vehicles (UAVs) |

| Short-Range |

| Beyond Visual Range |

| Solid |

| Ramjet |

| Ducted |

| Infrared (IR) Homing |

| Active Radar Homing |

| Semi-Active Radar |

| Dual-Mode |

| Subsonic |

| Supersonic |

| Hypersonic |

| North America | United States | |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Launch Platform | Fixed-Wing Aircraft | ||

| Rotary-Wing Aircraft | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Range | Short-Range | ||

| Beyond Visual Range | |||

| By Propulsion Type | Solid | ||

| Ramjet | |||

| Ducted | |||

| By Guidance | Infrared (IR) Homing | ||

| Active Radar Homing | |||

| Semi-Active Radar | |||

| Dual-Mode | |||

| By Speed Class | Subsonic | ||

| Supersonic | |||

| Hypersonic | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current global value of air-to-air missile procurement?

The air-to-air missiles market stands at USD 7.36 billion in 2025 and is projected to hit USD 10.74 billion by 2030 at a 7.85% CAGR.

Which region is expanding fastest in terms of new missile orders?

Asia-Pacific leads growth with a 9.45% CAGR through 2030 on the back of Chinese military modernization and regional arms races.

Why are hypersonic missiles attracting large R&D budgets?

Hypersonic speeds cut target reaction time to seconds, giving operators first-shot advantages that can neutralize high-value assets before defenses respond.

How are UAVs changing missile-launch concepts?

Armed drones add magazine depth, enable attritable swarms, and let manned fighters off-load engagements to unmanned teammates, enhancing survivability.

What supply-chain issues currently constrain production?

A worldwide shortage of rocket-motor castings and propellant mixers has delayed deliveries, prompting prime contractors to partner with additional European manufacturers.

How will MTCR policy updates influence export opportunities?

The recent guidelines relax licensing requirements for allied nations with robust oversight, which may speed up shipments while ensuring that technology protections remain secure.

Page last updated on: