Shingles Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.99 Billion |

| Market Size (2031) | USD 11.29 Billion |

| Growth Rate (2026 - 2031) | 13.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shingles Vaccine Market Analysis by Mordor Intelligence

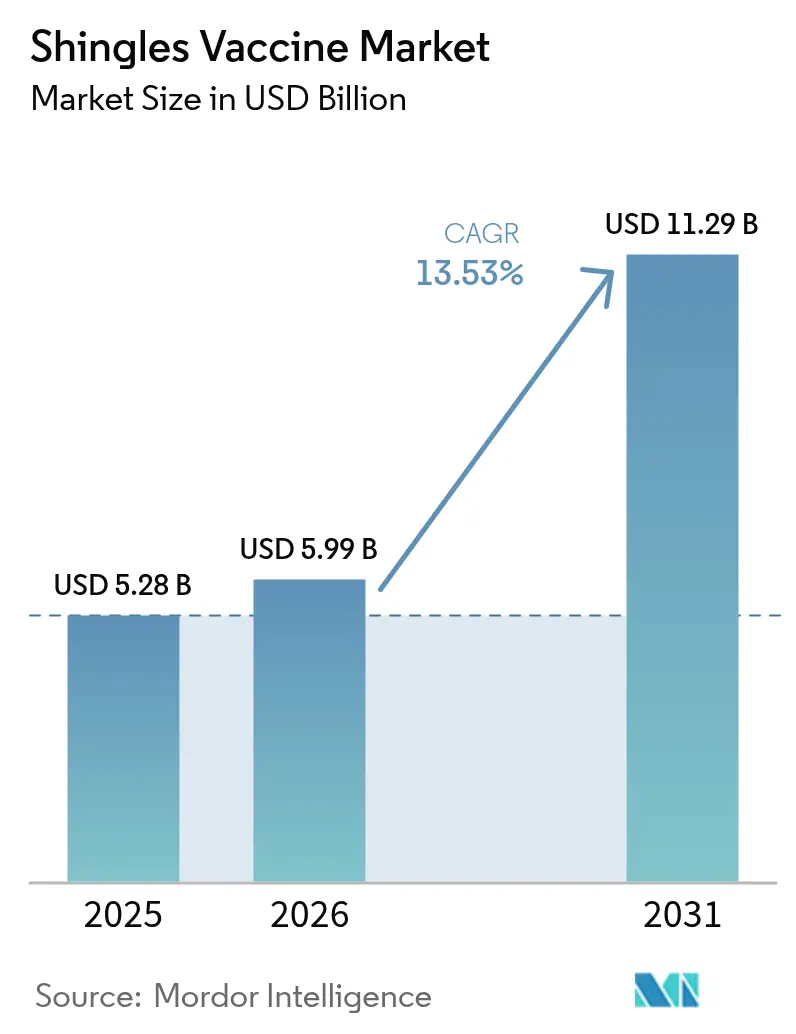

Shingles Vaccine market size in 2026 is estimated at USD 5.99 billion, growing from 2025 value of USD 5.28 billion with 2031 projections showing USD 11.29 billion, growing at 13.53% CAGR over 2026-2031.

The expansion stems from converging forces that include a rapidly growing population of adults aged 50 and above, wider government reimbursement, and steady innovation in recombinant subunit technologies that maintain effectiveness above 90%. Rising life expectancy, particularly in OECD economies, enlarges the clinical pool, while cost-sharing reforms such as the United States Inflation Reduction Act removed out-of-pocket payments for Medicare beneficiaries and triggered a 46% step-up in vaccinations in 2023. National immunization schedule inclusion across 39 countries, from Australia to the United Kingdom, turns discretionary shots into routine adult care, creating predictable procurement volumes for suppliers. Recombinant adjuvant platforms deliver immunogenicity that remains durable for at least seven years, a performance gap that continues to push live-attenuated competitors out of formularies. Meanwhile, mRNA candidates now in Phase 3 trials promise shorter production cycles and may further widen geographic access if stability targets are met.

Key Report Takeaways

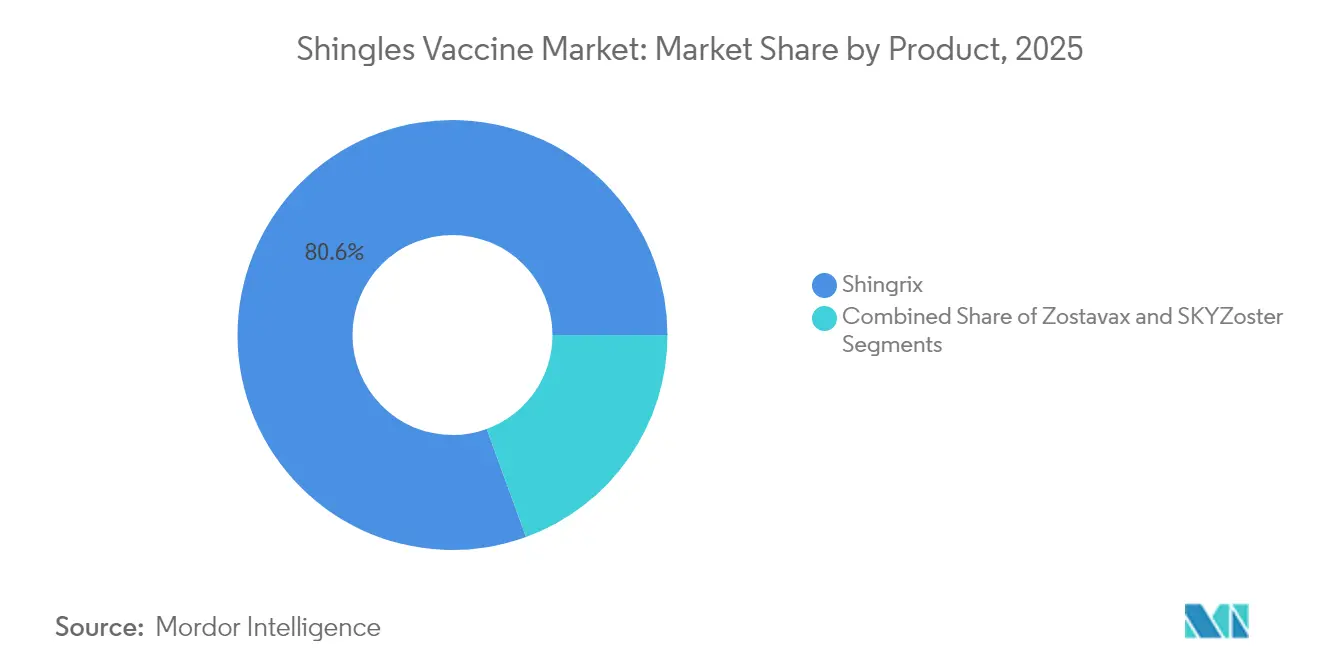

- By product, Shingrix led with 80.56% of the Shingles vaccine market share in 2025; are projected to post the fastest 14.03% CAGR through 2031.

- By vaccine type, recombinant subunit platforms accounted for 83.52% share of the Shingles vaccine market size in 2025 and are projected to grow at a 14.18% CAGR to 2031.

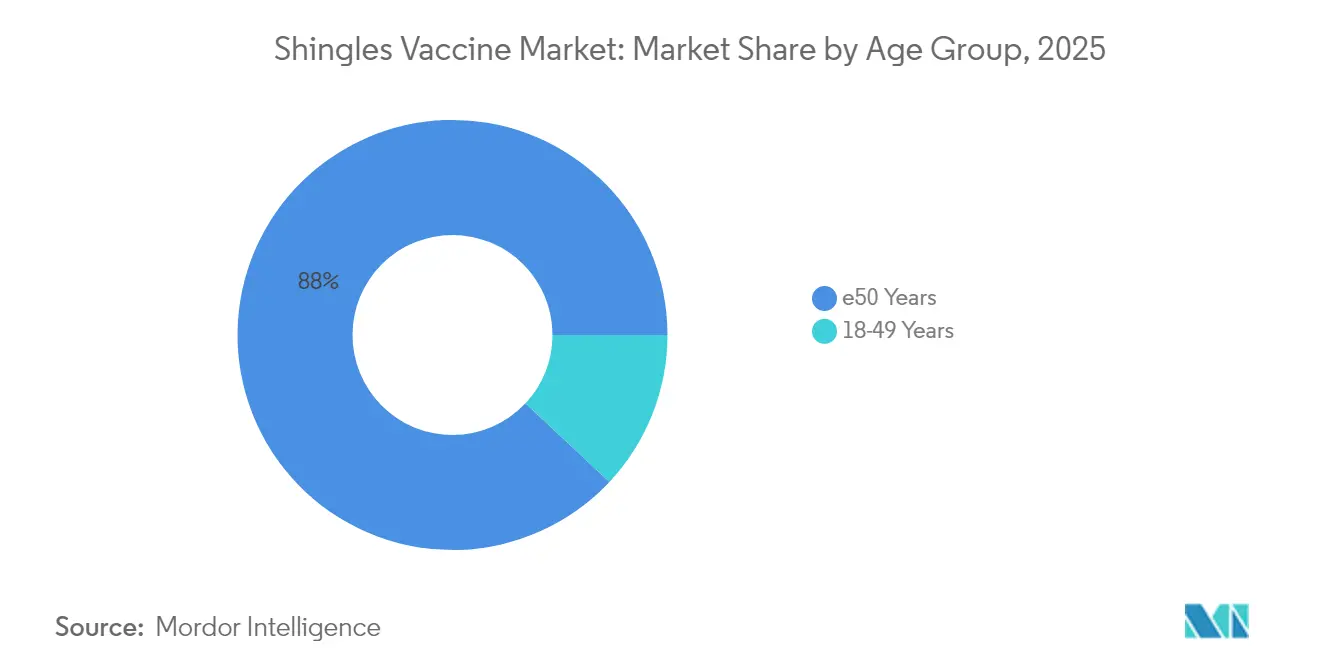

- By age group, adults ≥50 years captured 88.02% revenue share in 2025, while the immunocompromised 18-49 segment is forecast to expand at 15.55% CAGR through 2031.

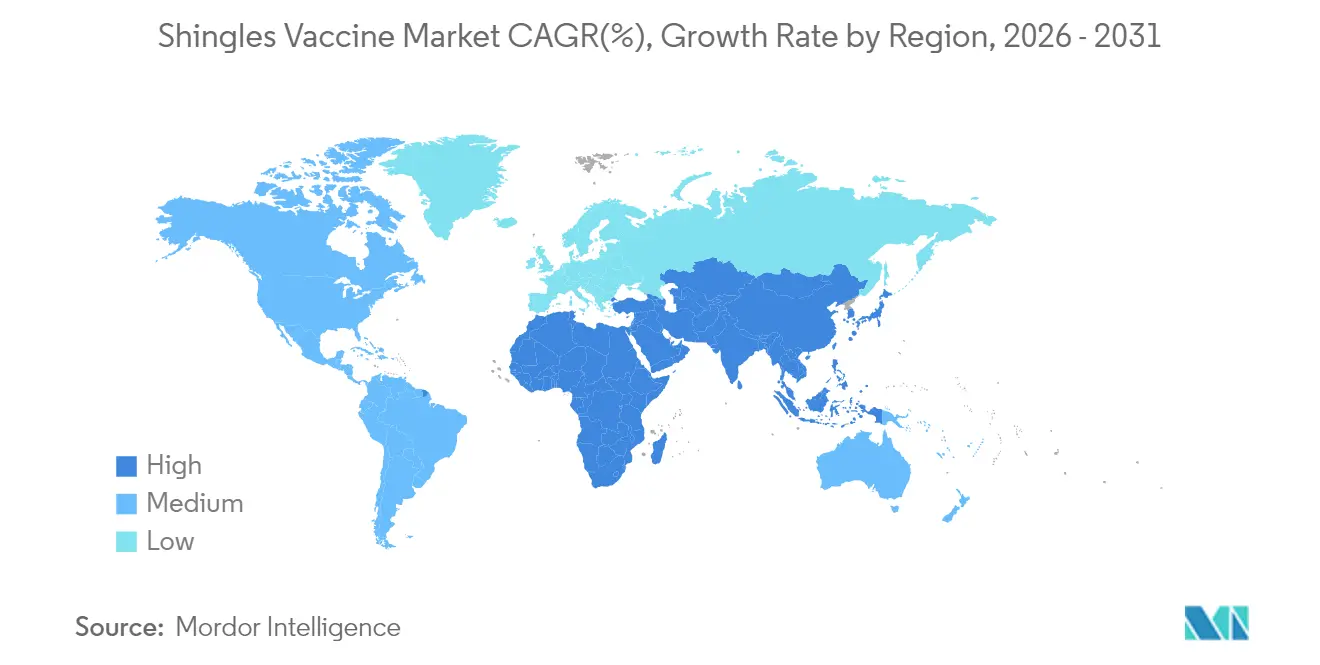

- By geography, North America held 42.86% of the Shingles vaccine market share in 2025; Asia-Pacific is set to register the strongest 18.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Shingles Vaccine Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inclusion of shingles vaccines in national immunization schedules | +3.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rising incidence in ≥50-year age group & growing elderly population | +4.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Superior cost-effectiveness of vaccination over treatment | +2.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Government reimbursement for recombinant adjuvanted vaccines | +2.3% | North America & EU core markets | Short term (≤ 2 years) |

| Fast-tracked regulatory pathways for mRNA-based shingles vaccines | +1.1% | Global, led by US & EU | Long term (≥ 4 years) |

| Government-led immunization programs targeting older adults | +1.8% | Global, with APAC acceleration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inclusion of Shingles Vaccines in National Immunization Schedules

Australia added Shingrix to its National Immunisation Program in November 2023, covering adults from 65 years and immunocompromised individuals from 50, a move that immediately lifted demand across pharmacies and primary-care clinics. In the United Kingdom, the 2023 shift from Zostavax to Shingrix extended eligibility to severely immunosuppressed adults aged 50 and immunocompetent adults from 60. Such public-funding decisions lower patient cost hurdles, guarantee multi-year tender volumes, and strengthen bargaining power for bulk procurement. Equally important, the World Health Organization plans to release updated herpes zoster recommendations in March 2025, a step likely to influence immunization roadmaps in emerging markets.[1]World Health Organization, “Herpes Zoster Vaccine Position Paper (Upcoming),” who.intCollectively, these actions convert what had been sporadic, self-paid uptake into an institutionalized public-health service, supporting a predictable revenue base for the Shingles vaccine market.

Rising Incidence in ≥50-Year Age Group & Growing Elderly Population

Global life expectancy gains spur a structural rise in the number of adults with waning cell-mediated immunity capable of reactivating latent varicella-zoster virus. The CDC counts around 1 million shingles cases in the United States each year, with 99% of adults >50 already harboring dormant virus.[2]Centers for Disease Control and Prevention, “Shingrix Recommendations,” cdc.govDemand is consequently insulated from macroeconomic cycles and aimed mainly at preventive care budgets. Studies noting potential cardiovascular and dementia risk reductions following vaccination broaden the value proposition and encourage payer support for adult immunization beyond the immediate avoidance of post-herpetic neuralgia.

Superior Cost-Effectiveness of Vaccination Over Treatment

From Canada to Latin America, health-economic modeling places the incremental cost-effectiveness ratio of recombinant shingles vaccination well inside typical willingness-to-pay thresholds. Canadian analyses among high-risk cancer cohorts show CAD 24,328 (USD 18,000) per quality-adjusted life-year gained, reaffirming fiscal prudence for ministries of health. Similar research across five Latin American countries projects prevention of 5 million herpes zoster cases if recombinant vaccines are adopted in national schedules. These data underpin policy approvals and guide insurers toward complete coverage, propelling the Shingles vaccine market size beyond reliance on consumer willingness to pay.

Government Reimbursement for Recombinant Adjuvanted Vaccines

Eliminating patient co-payments demonstrably boosts uptake. After the United States adopted this approach under the Inflation Reduction Act, monthly Medicare vaccinations jumped to 410,564 in 2023 from 281,283 in 2022.[3]Mihir Parikh et al., “Elimination of Medicare Cost Sharing and Adult Vaccination Uptake,” JAMA Network, jamanetwork.comBy December 2023, virtually every Medicare Part D recipient paid nothing out of pocket. The episode highlights the elasticity of demand and offers a blueprint for other countries weighing similar subsidy models.

Restraints Impact Analysis of Shingles Vaccine Market*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited public awareness in low- & middle-income countries | −2.1% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Supply-chain complexity for cold-chain, multi-dose recombinant products | −1.4% | Global, acute in tropical regions | Short term (≤ 2 years) |

| Adjuvant-related safety concerns driving vaccine hesitancy | −0.8% | Global, social-media-influenced demographics | Medium term (2-4 years) |

| Global bulk-antigen capacity constraints | −1.2% | Worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Public Awareness in Low- & Middle-Income Countries

In China, only 27.1% of surveyed urban residents expressed willingness to vaccinate, citing scant disease knowledge and the USD 446 price tag as deterrents. Similar gaps exist in Latin America, where under-reporting of herpes zoster incidence complicates policymaking. Without sustained public-health messaging and physician training, market penetration remains thin, slowing progress for the Shingles vaccine market in emerging economies.

Supply-Chain Complexity for Cold-Chain, Multi-Dose Recombinant Products

Recombinant shingles vaccines must remain between 2–8 °C at all times, a constraint that strains healthcare facilities in tropical regions with intermittent electricity. Shingrix presently ships as a two-vial kit requiring reconstitution, increasing handling errors and wastage. Although a pre-filled syringe is under FDA review, the necessity for cold-chain integrity persists. Investments in reliable refrigeration, temperature sensors, and backup generators are essential but costly, limiting reach into rural clinics and thus restraining the broader Shingles vaccine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Shingles Vaccine Market Segment Analysis

By Product:

Recombinant Leader Confronts Emerging mRNA AlternativesThe Shingles vaccine market size for recombinant Shingrix translating into an 80.56% market share in 2025 and validating its clinical advantage over live-attenuated predecessors. Uptake benefits from proven more than 90% efficacy and eligibility across immunocompromised cohorts. Despite this strong foothold, momentum is building around pipeline mRNA assets. Moderna’s mRNA-1468 moved into Phase 3 on the back of robust CD4+ T-cell activity and a tolerability profile that could match or exceed existing benchmarks. Dynavax’s Z-1018 combines its proprietary CpG 1018 adjuvant with recombinant glycoprotein E antigen to elicit comparable immunogenicity, with interim data due in 2025. Should either candidate gain approval, competitive forces could chip away at Shingrix’s large Shingles vaccine market share, though the incumbent’s entrenched reimbursement ties and seven-year real-world performance record form high entry barriers.

Once license holders scale up RNA manufacturing lines originally built for COVID-19, cost per dose could fall, enabling price competition or expanded access in resource-constrained geographies. However, the Shingles vaccine industry still faces the challenge of establishing cold-chain and ancillary-supply capacity for these new formats at parity with current recombinant offerings. For the medium term, therefore, recombinant formulations are expected to retain dominance even as mRNA varieties broaden choice for providers.

By Vaccine Type:

Recombinant Subunit Vaccines Maintain Commanding PositionRecombinant subunit vaccines captured 83.52% of Shingles vaccine market share in 2025 and are projected to sustain a 14.18% CAGR, buoyed by their suitability for immunocompromised recipients and strong immunogenic durability. Live-attenuated alternatives have lost favor after Zostavax discontinuation in several markets. Manufacturing advantages also accrue to recombinant platforms that leverage CHO cell lines and purified antigen processes, reducing the biosafety concerns inherent in live-virus cultures. Adjuvant systems such as AS01B, formulated with monophosphoryl lipid A and QS-21 saponin, stimulate potent CD4+ T-cell and antibody responses, extending protection. Recent breakthroughs in yeast-based QS-21 synthesis could lower raw-material costs, strengthening supply resilience.

Over the forecast horizon, live-attenuated contenders are unlikely to reclaim lost ground unless reformulated to address reduced efficacy in older adults. Instead, future competitive dynamics will likely revolve around whether mRNA or protein-based nanoparticles can match the data set accumulated by current recombinant options while improving dosing convenience. Until that occurs, the recombinant segment will continue to anchor revenue growth for the Shingles vaccine market.

By Age Group:

Core ≥50 Segment Steady, Immunocompromised 18-49 Cohort SurgesAdults aged ≥50 constituted an 88.02% slice of the Shingles vaccine market size in 2025, reflecting guideline recommendations and higher disease incidence. This age group will hold steady as the backbone of demand, supported by consistent public-health messaging on neuropathic pain prevention. In parallel, the immunocompromised 18-49 population stands out with a 15.55% CAGR to 2031, catalyzed by the CDC recommendation that expanded coverage to adults with weakened immunity starting at 19 years. These patients carry a 3-10× greater shingles risk and often face additional complications such as prolonged rash and disseminated infection arthritis.

Health systems are responding by tailoring vaccination campaigns to oncology and rheumatology clinics, enabling same-day immunization during routine visits. Pharmaceutical manufacturers, for their part, have begun sponsoring continuing-education modules to raise physician awareness of eligibility changes. As clarity around reimbursement grows, this younger high-risk segment could provide meaningful volume upside, reinforcing the diversified growth profile of the Shingles vaccine market.

Geography Analysis

North America Shingles Vaccine Market

North America, holding 42.86% of the Shingles vaccine market share in 2025, benefits from comprehensive insurance networks, mature retail-pharmacy vaccination channels, and early clinical adoption of recombinant technology. Medicare’s removal of cost sharing in 2023 caused a near-instant increase in monthly administrations, underscoring the potency of reimbursement levers. Yet absolute growth is moderating as coverage inches toward saturation; GSK’s 2024 U.S. Shingrix sales declined 18% in the fourth quarter as the pool of unvaccinated seniors dwindled and retail chains reset inventory priorities. Future upside therefore relies on broadening indications to younger immunocompromised groups and possibly bundling vaccination with chronic-disease management programs.

APAC Shingles Vaccine Market

Asia-Pacific represents the fastest-expanding opportunity with an 18.12% CAGR through 2031, driven by demographic aging and incremental improvements in adult-vaccination budgets. Australia’s 2023 public funding decision triggered above-trend uptake within the first six months, validating fiscal commitment as a catalyst. In China, where the incidence pool is massive, uptake remains modest due to high list prices and variable awareness; still, the recent extension of the GSK-Zhifei partnership through 2029 coupled with local competition from Changchun BCHT Biotechnology’s domestically produced vaccine is expected to expand access and potentially lower co-pay levels. Japan, South Korea, and Singapore continue to generate supportive real-world data that shape regional policy and encourage reimbursement.

Europe Shingles Vaccine Market

Europe follows a pattern of deliberate but widening adoption. The United Kingdom’s 2023 transition to Shingrix, paired with age-threshold adjustments, set a precedent for neighboring countries evaluating similar moves. Sweden’s nationwide epidemiological study indicating a 36.5% lifetime risk is pushing policymakers toward a cost-benefit review, though final funding decisions remain pending. Continental progress is also influenced by pan-European procurement mechanisms that seek volume discounts, an approach that could compress margins but enlarge total addressable volume. Overall, regional heterogeneity persists, but the trajectory for the Shingles vaccine market remains firmly upward.

Competitive Landscape

The Shingles vaccine market is highly concentrated, featuring an oligopoly where GSK’s Shingrix controls a significant share, Merck’s residual live-attenuated presence has faded, and future disruption is expected mainly from mRNA entrants. Barriers to entry are steep: multi-year clinical programs, specialized adjuvant supply chains, and stringent cold-chain validation add capital intensity. GSK fortifies its first-mover moat through continuous manufacturing investment, including the USD 800 million Pennsylvania expansion that doubles drug-substance output, and a Belgian site focused on freeze-dried formats designed to simplify field logistics.

Moderna seeks to leverage its experience scaling mRNA vaccines during the COVID-19 response, positioning mRNA-1468 for accelerated regulatory review and potential first-to-market status among the new wave of candidates. Dynavax’s Z-1018 bets on its CpG 1018 adjuvant, already used in Hepatitis B vaccination, to provide a differentiated safety profile that could appeal to younger or immunocompromised segments. Supply-chain advances, such as yeast-based QS-21 synthesis, could lower adjuvant costs and reduce GSK’s procurement advantage, yet full industrial-scale readiness is unlikely before 2028.

Regional manufacturers are also mobilizing. Changchun BCHT Biotechnology became the first domestic company to win Chinese approval for a shingles vaccine in June 2024, potentially securing provincial tenders where local preference rules apply. Similar in-country initiatives are surfacing in India and Brazil, though these remain at pre-clinical stages. Collectively, the next five years will see incremental erosion of incumbent dominance but not enough to overturn the leadership position, sustaining a premium-pricing environment for the Shingles vaccine market.

Shingles Vaccine Industry Leaders

Merck & Co., Inc.

SK bioscience

GSK plc

Curevo Inc

GeneOne Life Science

- *Disclaimer: Major Players sorted in no particular order

Shingles Vaccine Market Companies Covered in this Report

- GlaxoSmithKline

- Merck

- SK bioscience

- Changchun BCHT Biotech

- GeneOne Life Science

- Vaccitech

- CanSinoBIO

- Pfizer

- Curevo Inc.

- Jiangsu Recbio Technology

- Moderna

- BioNTech

- Novavax

- Valneva

- Bavarian Nordic

- Johnson & Johnson

- Daiichi Sankyo

- Bharat Biotech

- Sinovac

- Vaxart

Recent Industry Developments in Shingles Vaccine Market

- February 2025: GSK reported 1% increase in Shingrix sales despite overall 4% vaccine portfolio decline, with US cumulative immunization reaching 40% while international sales grew significantly driven by Australian public funding and Chinese market supply, though Q4 2024 sales declined 13% due to challenges reaching unvaccinated consumers and retail vaccine prioritization changes.

- January 2025: FDA accepted review of GSK's Shingrix prefilled syringe presentation, eliminating healthcare provider mixing requirements and potentially enhancing vaccination efficiency and reducing administration errors for the two-dose regimen.

- December 2024: GSK and Zhifei Biological Products extended their Chinese shingles vaccine partnership through 2029 with reduced financial commitment of 21.6 billion yuan (USD 3.01 billion) compared to original 20.6 billion yuan (USD 2.87 billion) over three years, reflecting market challenges and macroeconomic pressures.

- October 2024: GSK announced up to USD 800 million investment in Pennsylvania manufacturing site expansion, doubling capacity and creating 200 jobs with new drug substance facility utilizing novel MAPS technology expected operational by 2027.

- July 2024: Dynavax Technologies initiated Phase 1/2 clinical trial for investigational shingles vaccine Z-1018 utilizing CpG 1018 adjuvant, enrolling 440 healthy adults aged 50-69 in Australia with immunogenicity and safety data expected in 2025.

Shingles Vaccine Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the shingles vaccines market as revenue generated from all prophylactic human herpes-zoster vaccines, live-attenuated and recombinant subunit, sold through public immunization programs and private retail pharmacies across the 17 countries tracked by Mordor Intelligence; ancillary services, dosing devices, and treatment drugs are excluded. The current baseline values the market at USD 5.28 billion in 2025 and extends forecasts to 2030.

Scope exclusion: Therapeutic antivirals, pain relievers, and R&D pipeline spending are expressly outside this valuation.

Segments Covered in This Report

- By Product

- Shingrix

- Zostavax

- SKYZoster

- By Vaccine Type

- Recombinant Subunit

- Live-attenuated

- By Age Group

- ≥50 Years

- 18-49 Years

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with pharmacovigilance officers, national procurement officials, retail pharmacists, and infectious-disease clinicians across North America, Europe, Asia-Pacific, and Latin America helped us test underlying assumptions on dose wastage, payer mix, and reimbursement timing. Short web-based surveys of consumers aged 50+ further refined expected uptake after the U.S. Inflation Reduction Act removed out-of-pocket costs.

Desk Research

We began with population-at-risk estimates and vaccination uptake ratios reported by sources such as the World Health Organization, the U.S. CDC, the European Centre for Disease Prevention, and national immunization schedule databases, which together ground age-cohort penetration curves. Trade statistics from UN Comtrade and customs data supplied shipment values for finished doses, while peer-reviewed journals clarified durability and seroconversion rates that influence revaccination pools.

To size commercial flows, our analysts extracted historical sales from company 10-Ks, investor decks, and selected press releases, then validated manufacturer ASP trends using D&B Hoovers and Dow Jones Factiva price mentions. The sources listed illustrate the breadth consulted; many additional datasets were reviewed for corroboration and context.

Market-Sizing & Forecasting

We reconstructed demand using a top-down prevalence-to-treated-cohort model, layering country-specific >=50-year population counts, vaccine coverage rates, and two-dose compliance factors. Supplier roll-ups of Shingrix, Zostavax, and SKYZoster volumes provided a selective bottom-up check that narrowed variance to +/-4%. Key variables like elderly population growth, recombinant adoption share, public reimbursement breadth, list-price inflation, and booster interval evidence feed a multivariate regression that projects value to 2030. When bottom-up totals showed gaps (e.g., under-reported tenders in emerging Asia), proportional allocation from regional averages bridged missing datapoints before final alignment.

Data Validation & Update Cycle

Model outputs pass three analyst reviews, anomaly flags trigger recalls with respondents, and results are benchmarked against quarterly manufacturer disclosures. Reports refresh annually, while material events such as major reimbursement policy shifts prompt interim updates; a final validation sweep occurs just before client delivery.

How Mordor Intelligence's Shingles Vaccine Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick different geographies, channel mixes, or assume single-dose adherence.

Key gap drivers include: 1) some publishers model only hospital procurement, ignoring retail self-pay doses; 2) others cap recombinant penetration at 70% despite evidence of rapid live-attenuated replacement; 3) currency conversions fixed at prior-year averages instead of rolling quarterly rates; and 4) less frequent refresh cycles that miss policy catalysts such as Medicare's 2023 copay elimination.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.28 B (2025) | Mordor Intelligence | - |

| USD 5.62 B (2024) | Global Consultancy A | Excludes private pharmacy sales, older FX rates |

| USD 4.94 B (2024) | Research Firm B | Limits scope to 12 countries, assumes static ASP |

| USD 4.85 B (2024) | Industry Insights C | Uses conservative 55% recombinant uptake, biennial refresh |

External publications quote figures ranging from USD 4.85 billion to USD 5.62 billion for 2024, underscoring how narrower scopes and dated assumptions skew totals.

In summary, Mordor Intelligence delivers a balanced, transparent baseline anchored to verified population data, current pricing, and a disciplined update cadence, giving decision-makers an evidence-backed starting point they can reliably build upon.

Key Questions Answered in the Report

What is the projected value of the Shingles vaccine market by 2031?

The market is expected to reach USD 11.29 billion by 2031 on a 13.53% CAGR trajectory.

Which region shows the fastest growth for shingles vaccination?

Asia-Pacific is set to expand at 18.12% CAGR, reflecting demographic aging and recent public-funding decisions.

Why is Shingrix dominant in the Shingles vaccine market?

Its recombinant subunit design delivers >90% efficacy and allows use in immunocompromised adults, securing 80.56% market share in 2025.

How did U.S. policy changes influence vaccine uptake?

Eliminating Medicare Part D cost sharing led to a 46% rise in monthly vaccinations during 2023.

Are new technologies challenging current shingles vaccines?

Yes. mRNA candidates from Moderna and Dynavax are in clinical trials and could diversify the product mix after 2027.

What limits adoption in low-income countries?

Low public awareness, high out-of-pocket prices, and limited cold-chain infrastructure constrain uptake despite rising disease incidence.

Page last updated on: