Service Handgun Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

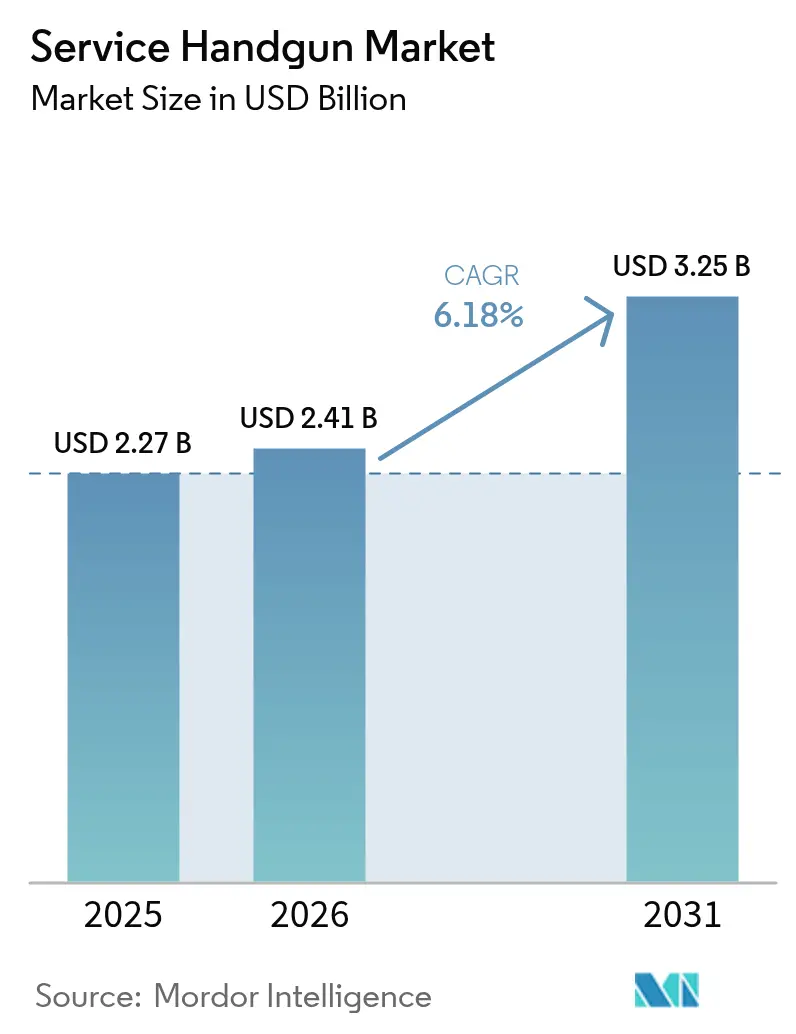

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.25 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Service Handgun Market Analysis by Mordor Intelligence

service handgun market size in 2026 is estimated at USD 2.41 billion, growing from 2025 value of USD 2.27 billion with 2031 projections showing USD 3.25 billion, growing at 6.18% CAGR over 2026-2031. Strong defense modernization, synchronized law-enforcement fleet upgrades, and the rapid displacement of double-action pistols by striker-fired platforms continue to sustain demand across mature and emerging procurement programs. Modular optics-ready designs now dominate specification lists, enabling fast technology refresh without entire weapon replacement. Regional momentum is uneven: North America retains the largest installed base, yet Asia-Pacific exhibits the quickest expansion as Indigenous manufacturing ramps up and strategic stockpiling gains urgency. Consolidation activity led by vertically-integrated ammunition-to-firearm groups and supply-chain fragilities in critical materials such as nitrocellulose reshape bargaining power along the value chain.

Key Report Takeaways

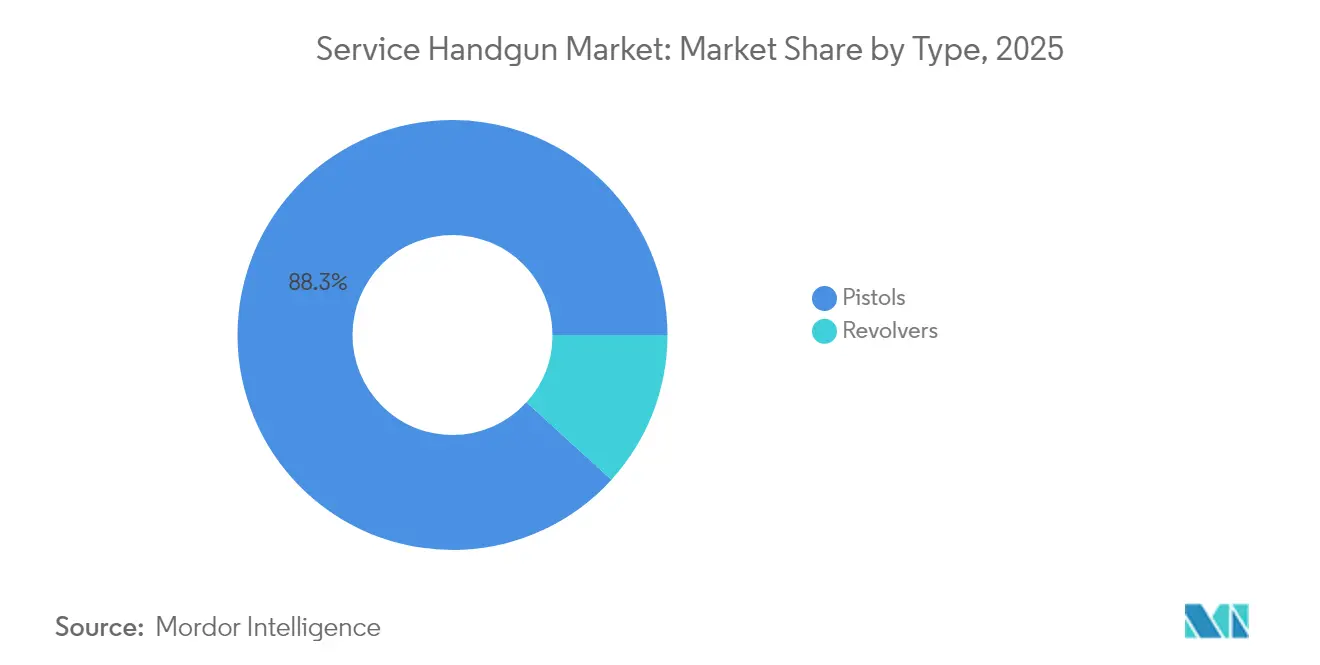

- By type, pistols led the service handgun market with 88.25% share in 2025, while revolvers are projected to post a 6.74% CAGR through 2031.

- By operation mechanism, striker-fired systems commanded 72.06% share of the service handgun market size in 2025 and will expand at a 6.79% CAGR during the forecast window.

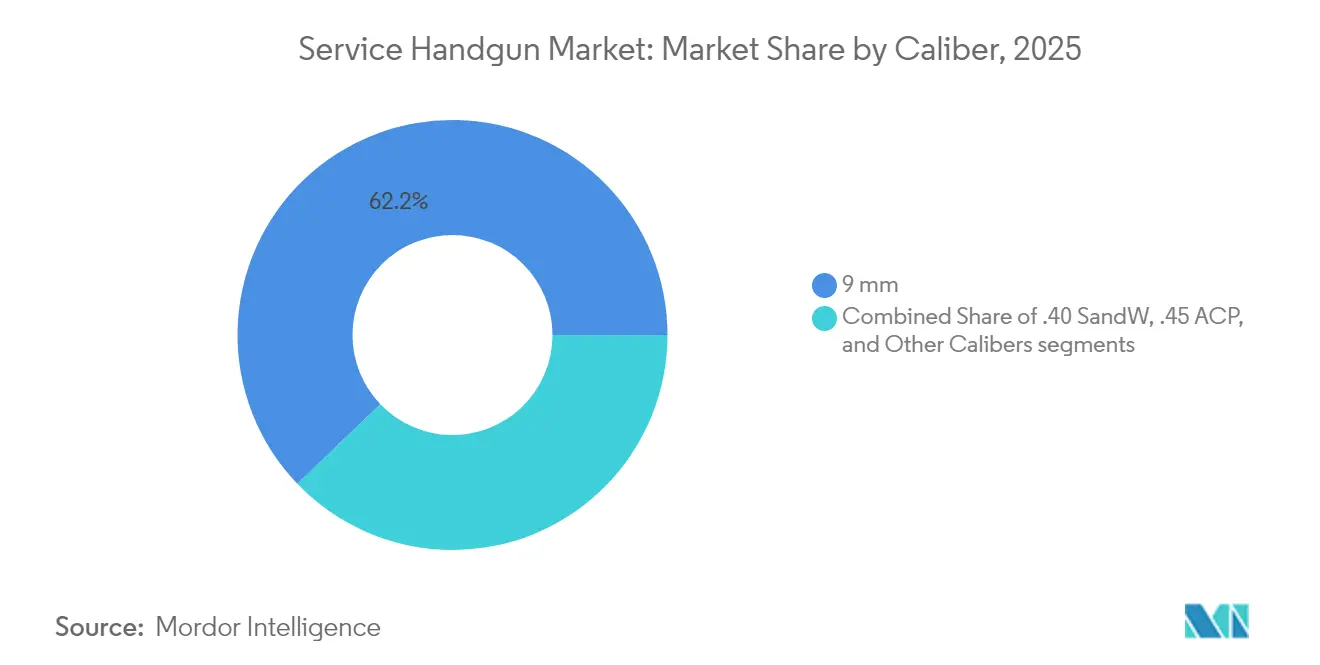

- By caliber, 9 mm held a 62.17% share of the service handgun market in 2025 and is forecast to grow at a 6.93% CAGR to 2031.

- By material, polymer frames accounted for 65.62% of the service handgun market size in 2025 and are advancing at a 7.05% CAGR.

- By end-user, law enforcement captured 63.05% revenue share in 2025, whereas military demand is set to record the highest 6.55% CAGR to 2031.

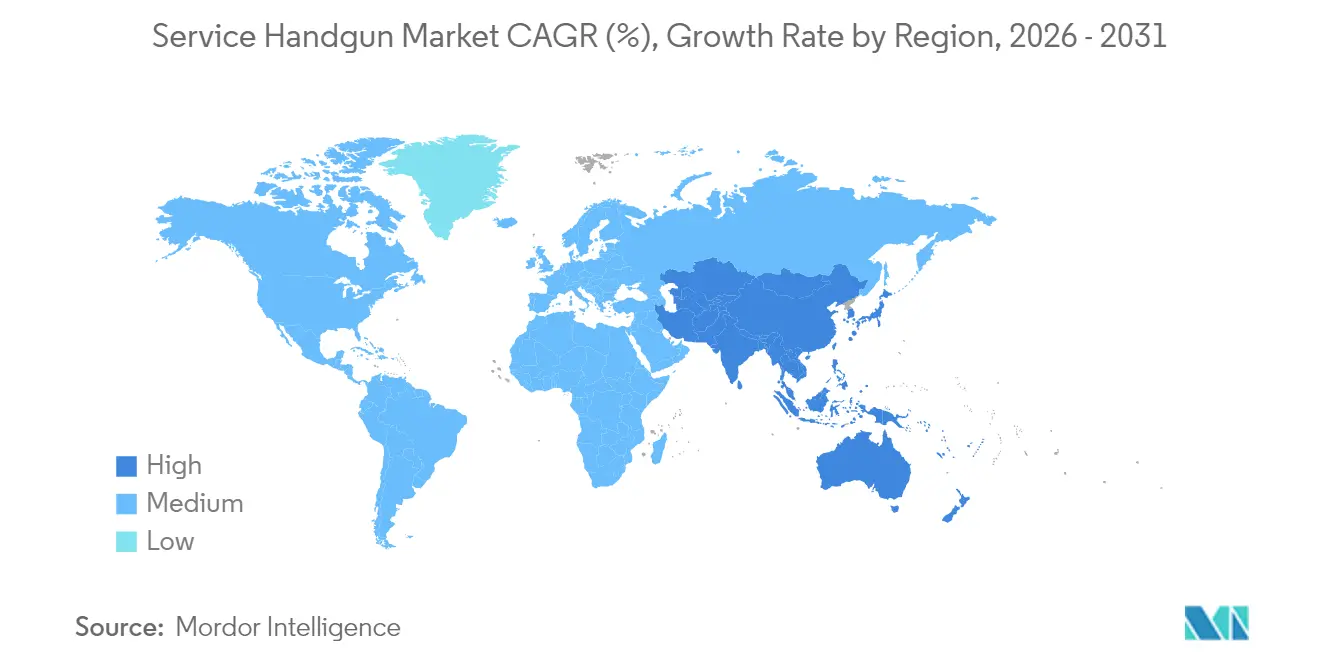

- By geography, North America dominated with 39.60% revenue share in 2025; Asia-Pacific is projected to register the fastest 7.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Service Handgun Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization initiatives driving military sidearm upgrades | +1.8 | Global, early NATO uptake | Medium term (2-4 years) |

| Law enforcement fleet renewals boosting demand for striker-fired handguns | +1.5 | North America and EU core | Short term (≤ 2 years) |

| Growing adoption of concealed-carry firearms among civilian users | +1.2 | North America expanding to select EU | Long term (≥ 4 years) |

| Procurement preference shifting toward factory-equipped optic-ready pistols | +0.9 | Global, developed markets concentration | Medium term (2-4 years) |

| Pilot programs exploring biometric smart-gun integration in government use | +0.4% | North America, limited EU trials | Long term (≥ 4 years) |

| Renewed interest in revolvers for training and specialized operational roles | +0.3% | Regional, primarily North America and select APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Modernization initiatives driving military sidearm upgrades

Defense agencies have moved beyond incremental overhauls, favoring complete sidearm replacement to secure interoperability, accessory rail compatibility, and sensor integration. Germany ordered 3,200 Walther P14 and 3,300 P14K pistols with enclosed-emitter optics and enhanced triggers that standardize special-forces equipment. Australia’s Project Land 300 fielded the SIG P320-based F9 system with red-dot sights, tactical lights, and non-lethal training mods under a single architecture.[1]Australian Department of Defence, “Project Land 300 Phase 3 Update,” defence.gov.au These programs underscore that legacy service pistols cannot absorb future capability inserts, prompting contiguous procurement cycles that underpin the service handgun market.

Law-enforcement fleet renewals boosting demand for striker-fired handguns

Police agencies prioritize consistent trigger pull, straightforward maintenance, and optics readiness. Pennsylvania State Police chose the Walther PDP, citing direct-milled Aimpoint ACRO compatibility and ergonomic improvements. Hartford Police transitioned from .40 caliber Glock 22/23 Gen4 to 9 mm Glock 17/19 Gen5, referencing improved terminal performance, lower recoil, and cheaper ammunition. Notwithstanding isolated safety concerns tied to specific striker-fired models, the broader trajectory still favors striker mechanisms, reinforcing growth across the service handgun market.

Growing adoption of concealed-carry firearms among civilian users

Civilian uptake of concealed-carry permits spills into the service handgun market because many customers buy duty-grade pistols proven in uniformed service. Manufacturers that share modular fire-control units across military, law enforcement, and commercial lines benefit from economies of scale, allowing wider SKU ranges without cost inflation. Civilian channels stabilize high-volume production runs initially justified by government contracts, supporting margin resilience.

Procurement preference shifting toward factory-equipped optic-ready pistols

Optics capability, once an aftermarket upgrade, is now mandatory in new solicitations. GLOCK’s 2025 portfolio shipped with integrated Aimpoint COA red dots, ensuring holster compatibility and minimizing adapter weight. Agencies increasingly specify direct slide milling instead of plate systems to protect zero retention over prolonged duty cycles. As agency bids codify optic readiness, platform selection narrows toward models integrating sighting technology from day one, amplifying premium SKU penetration in the service handgun market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter firearm regulations and export compliance limiting market accessibility | -1.1% | Global variance by jurisdiction | Long term (≥ 4 years) |

| Unstable ammunition supply chains and rising material costs impacting procurement | -0.8% | Worldwide, import-dependent regions acute | Short term (≤ 2 years) |

| Growing preference for non-lethal tools diminishing handgun adoption in law enforcement | -0.5% | EU core, selective adoption in North America | Medium term (2-4 years) |

| Budget prioritization shifting toward wearable tech and conflict de-escalation programs | -0.4% | Developed markets, limited emerging market impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tighter firearm regulations and export compliance limiting market accessibility

Shifting from ITAR to EAR oversight requires a full compliance overhaul even for unchanged product lines. The Bureau of Industry and Security’s larger audit force heightens enforcement risk, and most handgun exports still need licenses, extending lead times. Complex dual-use technology rules add bureaucratic friction that deters smaller producers, setting thresholds that inadvertently consolidate the service handgun market around firms with mature compliance infrastructure.

Unstable ammunition supply chains and rising material costs impacting procurement

Nitrocellulose, antimony restrictions from China, and surge demand triggered by the Ukraine conflict have squeezed primer and propellant supplies.[2]“Nitrocellulose Export Control Measures,” Ministry of Commerce People’s Republic of China, mofcom.gov.cn Lake City Army Ammunition Plant accounts for 85% of US military small-caliber rounds, exposing a single-node vulnerability. Agencies now weigh long-term ammunition availability alongside upfront pistol cost, occasionally deferring handgun purchases when munition budget shortfalls threaten training cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pistols Dominate Through Tactical Versatility

Pistols delivered 88.25% of 2025 revenue, cementing their status as the default sidearm for armed professionals thanks to greater magazine capacity and faster reloads than revolvers. Revolvers secured only 11.75% yet will outpace overall service handgun market growth at a 6.74% CAGR because specialized units still value their mechanical simplicity and non-recoverable brass advantages in sensitive operations. Historically, shared stability shows that innovation drives procurement rather than platform switching. The service handgun market continues to reward pistol makers that offer interchangeable backstraps, modular frames, and optics cuts, whereas revolver suppliers carve niche roles in training and covert scenarios.

Although revolvers are making a tactical comeback in limited contexts, pistols retain institutional preference. Large procurement programs like Australia’s replacement of Browning Hi-Power variants cited the need for 17-round magazines versus the legacy platform’s 13-round capacity. As newer striker-fired pistols furnish enhanced ergonomics and accessory rails, they further distance themselves from alternatives. Nevertheless, revolver makers responding with modern metallurgy and improved double-action triggers will likely keep the sub-segment profitable, sustaining a diverse service handgun market.

By Operation Mechanism: Striker-Fired Systems Achieve Dual Dominance

Striker-fired pistols captured 72.06% 2025 revenue and are forecasted to notch a 6.79% CAGR, a rare instance where the top-share design is also the fastest grower within the service handgun market. Consistent trigger pull across every shot simplifies training, and fewer parts cut maintenance costs for resource-constrained departments. Single-action pistols at 15.47% share cater to precision-oriented teams, while double-action systems with 12.47% share endure mainly because some agencies have yet to refresh legacy inventories.

The striker-fired rise intensifies as procurement documents embed drop-safety mandates and field-gauge standards that current designs already exceed. The service handgun market, therefore, sees a self-reinforcing loop: agencies switch to striker-fired platforms, aftermarket holster and optic ecosystems concentrate there, and fresh bids lean toward the better-supported configuration. Double-action platforms will persist in limited roles, but capital investment tilts toward striker development roadmaps.

By Caliber: 9 mm Achieves Universal Adoption

The 9 mm round dominated 2025 with 62.17% revenue and will expand at a 6.93% CAGR, propelled by NATO standardization and ballistic enhancements that overcame earlier penetration doubts. Agencies swapping from .40 S&W to 9 mm cite 2- to 3-round extra capacity and lower recoil that cuts qualification failures. The .40 S&W segment, holding 23.10%, remains relevant where existing inventories and contractual obligations linger. The .45 ACP niche at 14.73% sustains units prioritizing barrier performance over capacity.

Barrier-blind 9 mm loads adopted by the US Navy and Marine Corps validate terminal effectiveness, influencing allied purchase criteria. Ammunition cost per thousand rounds stays approximately 35% lower for 9 mm than .40 S&W, a decisive factor when ammunition budgets include duty, training, and reserve stockpiles. As more militaries co-align with NATO logistics, 9 mm’s share inside the service handgun market should widen further.

By Material: Polymer Frames Lead Innovation

Polymer frames delivered 65.62% of 2025 revenue and led growth at 7.05% CAGR. Weight savings of 100–150 g over comparable metal frames reduce soldier load, and molding flexibility allows aggressive texturing and interchangeable grip modules without machining. Stainless steel frames at 22.23% stay relevant where corrosion resistance is mission-critical, while aluminum alloys retain a 12.15% share for buyers balancing weight with the perceived longevity of metal.

Metal Injection Molding trims individual polymer frame part costs USD 2.50 compared with USD 8.25 for a CNC-machined metal equivalent, translating to multimillion-dollar savings on high-volume contracts. Consequently, budget-constrained ministries still demand performance features that increasingly align with polymer, reinforcing their dominance in the service handgun market.

By End-User: Military Growth Challenges Law-Enforcement Dominance

Law-enforcement bodies held 63.05% revenue leadership in 2025, supported by predictable refresh cycles and standardized sidearm policies across municipalities. Military organizations, however, will post a faster 6.55% CAGR as integrated optics, threaded barrels, and modular fire-control units make sidearms relevant beyond traditional backup roles.

Joint programs like the SIG P320-based M17/M18 platform enable barrel-length swaps and suppressor integration without new serial-numbered frames, simplifying armory logistics. Military branches also anchor large ammunition contracts, making vendors keen to tailor variants for tactical crews, special operations forces, and rear-echelon personnel. The resulting volume will steadily erode law enforcement’s share inside the service handgun market while expanding the total addressable base.

Geography Analysis

North America retained 39.60% 2025 revenue thanks to agency modernization budgets and federal grants that support local police upgrades. US Customs and Border Protection’s switch to new-generation GLOCK 9 mm pistols reflects procurement programs that ripple across training academies, armorers, and aftermarket suppliers. Canada’s CAD 19.4 million (USD 14.22 million) order for SIG P320 pistols underscores regional interoperability aims. Although the region’s 5.63% CAGR trails global momentum, its mature acquisition frameworks continue to generate steady baseline demand across the service handgun market.

Asia-Pacific will achieve the fastest 7.92% CAGR as self-reliance policies and threat perceptions accelerate funding. Australia’s F9 adoption embeds virtual training modules, while India’s “Make in India” doctrine lures foreign primes into local joint ventures. Indigenous machine-pistol programs such as “Asmi” signal that governments see in-country capacity as strategic. These factors combine to make the region the growth engine and potential manufacturing hub of the service handgun market.

Europe closed 2025 with a 28.55% share, powered by NATO harmonization and multi-nation tenders. Germany’s P13 competition and Denmark’s SIG P320 adoption illustrate rigorous but collective procurement that maximizes volume discounts. The Middle East and Africa, holding 15.35%, remain opportunity centers where large defense budgets converge with domestic manufacturers like Caracal, which doubled export ratios by forging Indonesian and Indian production tie-ups. Supply-chain sovereignty themes mean that even smaller states pursue localized assembly, keeping the region attractive to global OEMs seeking diversified revenue streams across the service handgun market.

Regulatory Landscape

Service handguns sit at the intersection of national procurement rules and tightly controlled cross-border transfers. In the United States, the Arms Export Control Act (AECA) governs defense-article trade, while Department of Defense handgun and small-arms acquisition is channeled through the Defense Federal Acquisition Regulation Supplement (DFARS), including DFARS 225.7702-1 covering acquisition of small arms with requirements around competition and protection of domestic industrial capabilities. For law-enforcement specifications, National Institute of Justice (NIJ) baseline guidance influences durability, safety, and reliability expectations that commonly show up in bid requirements.

Internationally, compliance frameworks such as the UN Firearms Protocol and the Arms Trade Treaty (ATT) require marking, record-keeping, and import-export authorization controls intended to reduce diversion, shaping OEM serialization processes and distributor due diligence. In Europe, EU Regulation 258/2012 sets rules for export, import, and transit measures for civilian firearms, which feeds into how manufacturers structure compliance documentation and distribution controls for duty-grade handguns. In 2026, the US Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) advanced a modernization package, including proposed and direct final rules with technical amendments to align ATF import and defense-trade processes with State and Commerce administered regimes, changing the practical compliance workload for exporters and importers.

Value Chain Analysis

The service handgun value chain begins with regulated raw materials and precision components (steel and alloy for slides and barrels, polymer compounds for frames, springs, and small parts), and it is supported by high-tolerance manufacturing such as CNC machining, forging/stamping, heat treatment, and barrel making. OEM assembly integrates optics-ready slide cuts, accessory rails, and serialized fire-control components, followed by proofing, quality assurance, and acceptance testing aligned to government QA provisions. Specialized upstream suppliers add precision fabrication and certified quality systems, with some component makers operating under standards such as AS9100D for defense-adjacent machining and fabrication.

Downstream, distribution splits into government procurement channels and commercial networks. Government contracts often bundle pistols with red-dot optics, holsters, lights, spares, armorer support, and training aids. Recent European selections also point to a growing lifecycle-services layer and a shift toward localized production and sustainment, such as Switzerland selecting the SIG Sauer P320 as its new standard service pistol with production localized in Switzerland, and Germany selecting a CZ P-10 C OR-based pistol designated P13 with fulfillment supported through an authorized local partner. These program structures shift value toward OEMs and integrators that can provide domestic assembly, depot-level maintenance, and long-term parts provisioning over multi-decade service horizons.

Competitive Landscape

Competition is tightening as technology cycles shorten and vertical integration reshapes supplier hierarchies. GLOCK’s reliability reputation secures long-term US law enforcement contracts, while SIG Sauer leverages modularity to lock in multi-year military deals. Smith & Wesson maintains civilian and police niches by capitalizing on broad caliber offerings.

The Czechoslovak Group’s USD 2.225 billion acquisition of The Kinetic Group integrated ammunition makers such as Remington and Federal, giving the parent control over two critical consumables: firearms and cartridges.[4]Czechoslovak Group, “Acquisition of The Kinetic Group Completed,” czechoslovakgroup.com Colt CZ Group posted 50.3% revenue growth in Q1 2025 following handgun sales of 97,786 units, validating the synergy playbook. Turkish challengers like Sarsılmaz broke into US police sales, demonstrating that competitive barriers are falling for cost-effective entrants.

Technology themes center on optic integration, factory-milled slides, and reduced production costs through automated polymer molding. GLOCK’s 2025 models shipped with built-in Aimpoint optics and a 600-lumen tactical light, indicating that accessories once bought separately now arrive bundled. Biofire’s biometric smart gun shows early proof of personalized-firearm feasibility, yet institutional buyers remain cautious until durability and battery life match duty standards. The net result is an innovation race that continuously lifts baseline specifications across the service handgun market.

Service Handgun Industry Leaders

GLOCK, Inc.

SIG SAUER, Inc.

Heckler & Koch GmbH

Fabbrica d’Armi Pietro Beretta S.p.A.

Smith & Wesson Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement bundles that combine the sidearm, optics, holsters, and accessories create room for OEMs and ecosystem partners to deliver standardized, agency-wide kits rather than standalone pistols. A concrete signal comes from Canada, where a March 2026 award covered a new service pistol program with optics and holsters under a long-duration contract term, reinforcing demand for factory optics-ready pistols and duty-optic interfaces. For suppliers, this expands the addressable scope to include approved optic footprints, duty holster compatibility, armorer tooling, and training conversion solutions tied to a single platform.

European modernization and sovereignty-driven sourcing also supports localized production, licensing, and in-country sustainment partnerships. Switzerland selected the P320 with domestic production in Neuhausen am Rheinfall and a stated long lifecycle requirement, and Germany moved to the CZ P13 as the replacement for the Heckler & Koch P8 under a framework approach that can scale in volume. These procurement patterns increase opportunities in modular striker-fired 9 mm platforms that support iterative upgrades (optics, triggers, grip modules) while keeping serialized core components consistent, and they reward manufacturers able to meet national industrial participation requirements alongside export-control compliance.

Recent Industry Developments

- June 2026: The German Bundeswehr unveiled the CZ P13 service pistol (based on the CZ P-10 C OR) at Eurosatory as the selected replacement for the Heckler & Koch P8. The program uses a framework-contract approach that can scale to large unit volumes, reinforcing demand for optics-ready striker-fired 9 mm pistols and long-term sustainment capacity in Europe.

- December 2025: Armasuisse selected the SIG Sauer P320 as the new standard service pistol for the Swiss Armed Forces with production localized in Switzerland. The decision highlights how industrial participation, domestic assembly, and lifecycle support commitments influence sidearm awards alongside technical specifications.

- February 2024: The Pennsylvania State Police selected the Walther PDP and PDP F-Series as official duty pistols. The choice supported the ongoing shift toward striker-fired, duty-optimized platforms designed around modern ergonomics and agency training and maintenance simplification.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the service handgun market is defined as the value of handguns procured and issued for official duty use, mainly by military and law enforcement agencies, across key geographies.

Scope exclusions: We exclude ammunition, accessories, and aftermarket services, and we also exclude long guns and other small arms that are not handguns.

Segmentation Overview

- By Type

- Revolvers

- Pistols

- By Operation Mechanism

- Single-Action

- Double-Action

- Striker-Fired

- By Caliber

- 9 mm

- .40 S&W

- .45 ACP

- Other Calibers

- By Material

- Stainless Steel

- Polymer Frame

- Aluminum Alloy

- By End-User

- Military

- Law Enforcement

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand and supply context for service handgun procurement, and to understand how spending and procurement activity moves by region over time. We relied on public defense procurement releases and budget documents, and we also used official trade statistics where handgun-related codes are available and consistently reported.

Common source types included government budget and procurement portals, customs and trade datasets, defense and public safety agencies' publications, and standards or regulatory guidance related to firearms ownership and duty carry. We also reviewed company annual reports and investor presentations for product mix signals, along with reputable press coverage of contract awards, replacement cycles, and policy changes, and we selectively used paid database subscriptions for company financials, patent checks, and contracts and tenders screening to reduce missed programs. These desk sources are illustrative, and many other public documents and data points were referenced to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as a service handgun sale, how replacement and new-issue programs are timed, and how pricing differs by contract size and specifications. We spoke with a mix of manufacturers, distributors, procurement-linked experts, and end-user informed participants across Americas, EMEA, and APAC so gaps from desk research could be closed and key assumptions could be checked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 22% | Managers: 52% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started from a top-down reconstruction of the addressable demand pool by combining defense and public safety spending signals with procurement timing, and then mapping that to service handgun issuance and replacement cycles. Once the regional totals were formed, the results were cross-checked using selective bottom-up approximations such as sampled contract values, observed unit volumes from public tenders, and price bands by handgun type to adjust for obvious undercounts.

The model used a practical set of inputs that could be traced back to repeatable indicators, including (illustratively) active duty and law enforcement headcount trends, replacement cycle lengths, tender cadence, average unit price progression by pistol versus revolver, and the share of procurements routed through centralized contracts versus decentralized purchases. For forecasting, scenario analysis was used so policy shifts, procurement delays, and step-changes in contract timing could be reflected without overfitting the history. Where bottom-up signals were incomplete (for example, smaller tenders not publicly disclosed), the gap was handled through calibrated ratios based on comparable programs and then validated again in follow-up expert checks.

Data Validation & Update Cycle

Validation was done through multi-step checks so the final number matched common market signals and did not jump due to one-off contract noise. We compared totals against independent indicators such as procurement announcements, budget movements, and observable tender pipelines, and then investigated variances that fell outside expected ranges for replacement-driven markets.

Before sign-off, the model and assumptions go through analyst review, and primary respondents are re-contacted if a major anomaly appears or if a material event is observed. The report is refreshed annually, and interim updates are made when large contracts, regulatory changes, or conflict-driven demand shifts materially change the outlook. Prior to delivery, a final review pass is done so clients receive the latest updated view.

Mordor Intelligence's Service Handgun Market Sizing Compared With Other Published Estimates

Published market sizes for service handguns do not always match because firms define the market differently and they also take different views on pricing and procurement timing. Even when the product looks similar on paper, the year chosen, currency handling, and how contracts are recognized can shift the reported value.

A common gap driver is scope, where some sources broaden the total by folding in adjacent firearm categories, wider commercial channels, or service-related spending beyond the handgun itself. Another driver is the base case stance, since some estimates assume faster replacement cycles or higher price escalation without re-checking those assumptions against tender schedules and budget approvals, which are then reflected as a higher current-year number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.41 B (2026) | |

| Global Consultancy A | USD 3.19 B (2024) | Uses an earlier base year and applies a broader segmentation lens that can pull in a wider set of handgun-related demand signals, and it may recognize procurement activity at a different point in the contracting cycle. |

| Regional Consultancy B | USD 2.43 B (2026) | Assumes a slightly different inclusion set across applications and then carries pricing forward using generalized material and safety segment mixes, which can shift the implied average price versus contract-led duty issuance. |

The table shows that much of the spread comes from how widely the market is defined and how contract timing is converted into annual market value. Some estimates expand the total to include broader handgun demand signals, then in Mordor Intelligence the count is limited to official duty issuance and procurement-linked value, with non-handgun weapons and related add-ons kept out so the inputs stay traceable.

Key Questions Answered in the Report

What is the current value of the service handgun market?

The service handgun market size reached USD 2.41 billion in 2026 and is forecasted to climb to USD 3.25 billion by 2031, reflecting a 6.18% CAGR.

Which segment holds the largest share of the service handgun market?

Pistols dominate, accounting for 88.25% revenue in 2025 due to higher magazine capacity and faster reload capability.

Why is the 9 mm caliber gaining preference over .40 S&W?

Modern 9 mm barrier-blind ammunition delivers improved penetration, carries lower recoil, and costs about one-third less per thousand rounds, prompting agencies to transition.

Which geographic region is expanding the fastest?

Asia-Pacific leads with an anticipated 7.92% CAGR through 2031, driven by Indigenous manufacturing initiatives and rising defense budgets.

How technology is reshaping procurement specifications?

Agencies now list factory-milled optics cuts, modular fire-control units, and polymer frames as baseline requirements, reflecting the need for future-proof sidearms.

What is driving consolidation in the service handgun industry?

Vertical integration, such as the Czechoslovak Group’s acquisition of The Kinetic Group, allows companies to control both firearms and ammunition supply, reducing vulnerability to input shortages and increasing bargaining power.

Page last updated on: