Small Caliber Ammunition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.17 Billion |

| Market Size (2031) | USD 10.72 Billion |

| Growth Rate (2026 - 2031) | 3.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

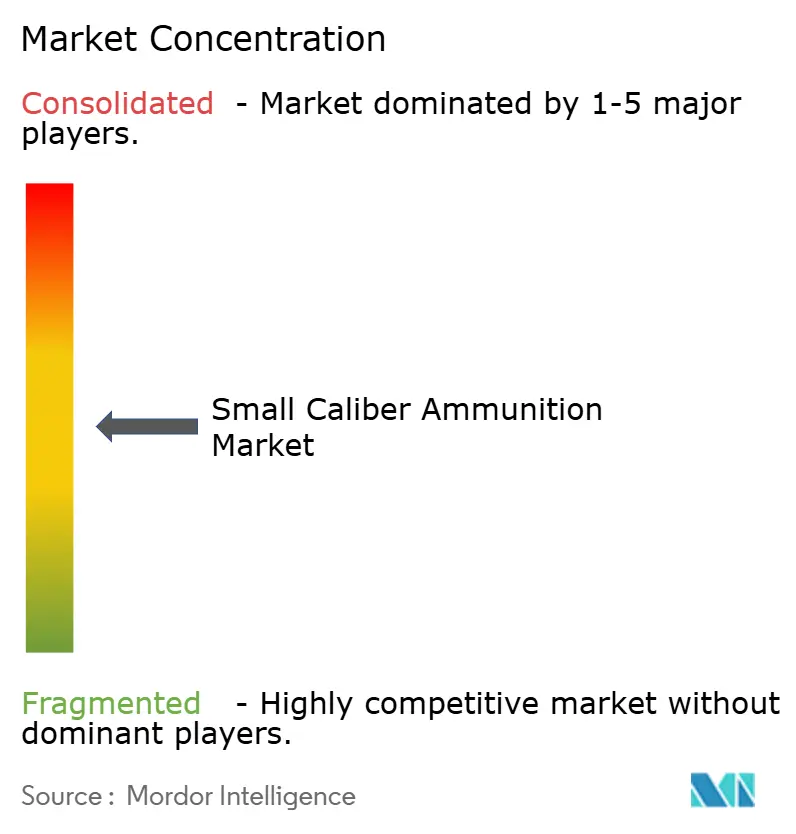

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Small Caliber Ammunition Market Analysis by Mordor Intelligence

The small caliber ammunition market size is expected to grow from USD 8.9 billion in 2025 to USD 9.17 billion in 2026 and is forecast to reach USD 10.72 billion by 2031 at a 3.17% CAGR over 2026-2031. Key growth drivers include structural changes such as the US Army's transition to 6.8 mm cartridges, increased civilian participation in shooting sports, and the adoption of lead-free designs driven by environmental regulations. Additionally, government stockpile replenishment following large-scale transfers to Ukraine and India's push for self-reliance provides market stability despite potential budget fluctuations. However, supply chain vulnerabilities persist due to limited primer and propellant availability, stemming from China's antimony export restrictions and the closure of nitrocellulose plants in North America. In response, manufacturers are focusing on vertical integration, plant automation, and the development of polymer or hybrid cases, which reduce weight by up to 30% and offer opportunities for premium pricing.

Key Report Takeaways

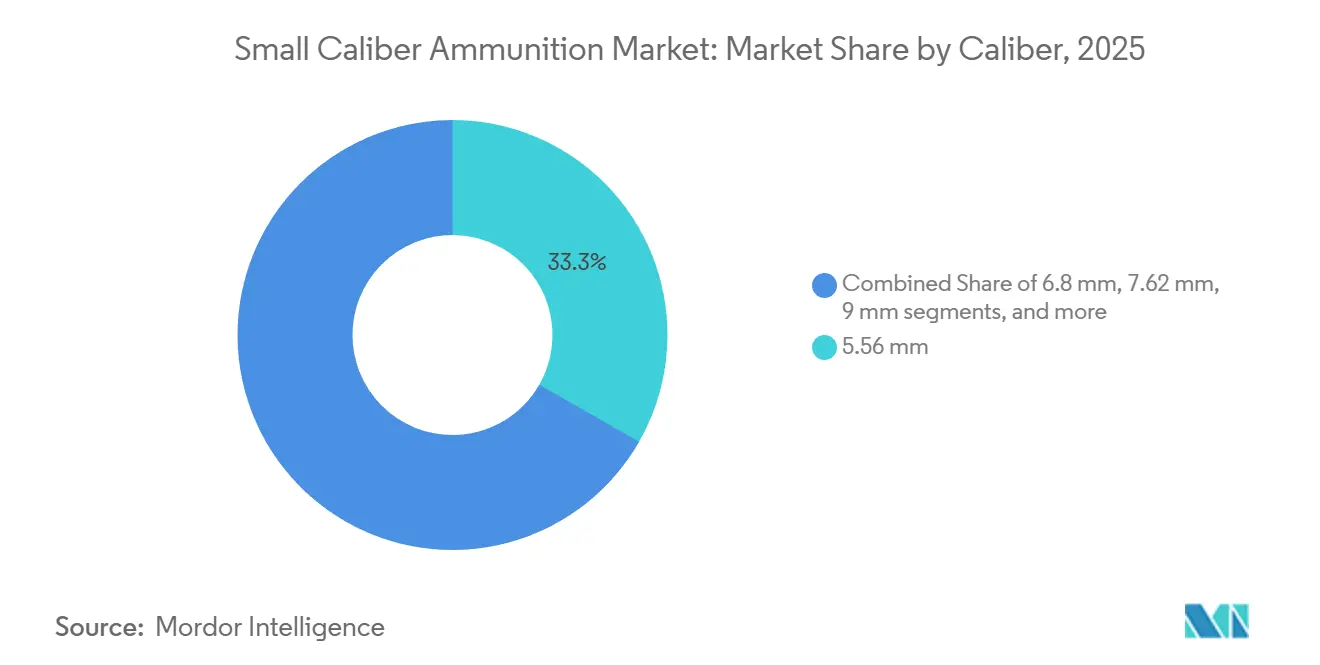

- By caliber, the 5.56 mm caliber is projected to capture 33.28% of the 2025 revenue. Meanwhile, 6.8 mm rounds, associated with the Next Generation Squad Weapon (NGSW), are forecasted to grow at a CAGR of 7.12% through 2031.

- By weapon platform, rifles are expected to dominate the market, accounting for 41.28% of the revenue in 2025. Sub-machine guns are expected to exhibit the fastest growth, with a CAGR of 4.98% during the forecast period up to 2031.

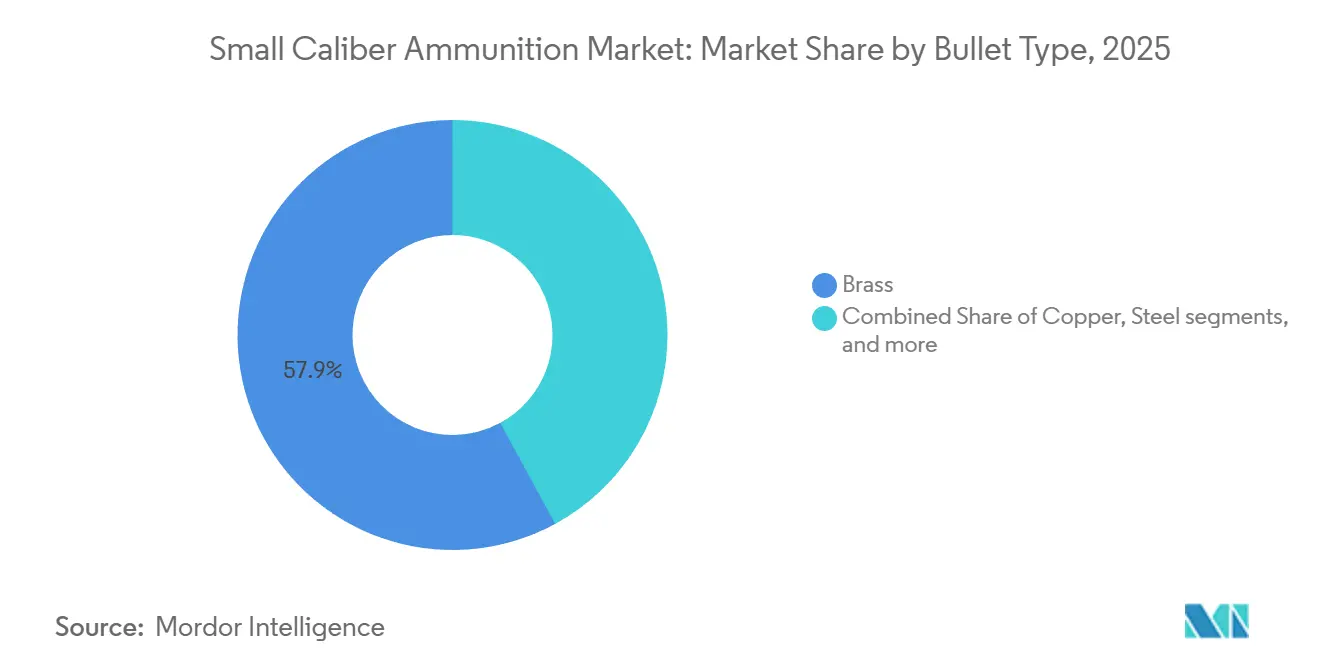

- By bullet type, brass cases are expected to account for 57.93% of 2025 revenue. Copper-based, lead-free rounds are projected to achieve the highest growth, with a 5.14% CAGR, driven by environmental regulations in the US and EU.

- By lethality, lethal ammunition is anticipated to account for 90.58% of the 2025 revenue. However, the less-lethal ammunition segment is projected to grow at a CAGR of 6.85% through 2031, as police agencies enhance their de-escalation capabilities.

- By end use, military applications are projected to account for 66.95% of 2025 revenue, while the civilian segment is expected to grow at a CAGR of 3.90% through 2031.

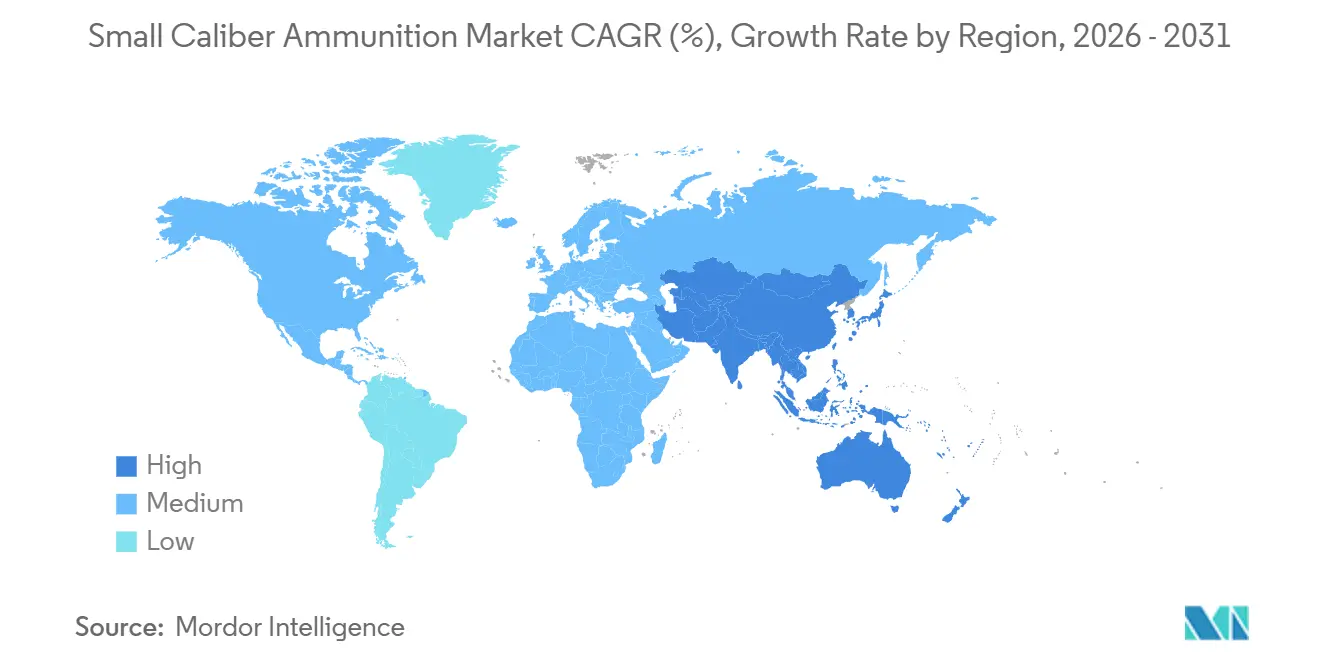

- By geography, North America is expected to account for 29.95% of the revenue share in 2025. The Asia-Pacific region is projected to experience the fastest growth, with a CAGR of 4.12% through 2031, driven by increased defense spending in India and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small Caliber Ammunition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Military ammunition modernization anchored in high-performance calibers | +0.9% | NATO members and allies | Medium term (2-4 years) |

| Defense budget growth fueling sustained demand for operational and training rounds | +0.8% | Global (North America, Europe, Asia-Pacific) | Medium term (2-4 years) |

| Rising civilian ownership and sporting interest sustaining commercial ammunition sales | +0.6% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Environmental regulations accelerating transition to lead-free ammunition | +0.5% | Europe, select US states, expanding worldwide | Long term (≥ 4 years) |

| Lightweight polymer and hybrid casings driving multi-nation trials | +0.4% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Simulation and indoor training demand boosting specialized rounds | +0.3% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Military Ammunition Modernization Anchored in High-Performance Calibers

The US Army’s NGSW program allocated USD 20.4 million to upgrade Lake City facilities for mass production of 6.8 mm rounds, marking the first caliber change for frontline US infantry since 1963. The new cartridge delivers 30% greater down-range energy, enabling penetration of advanced body armor. Allied forces are evaluating the costs of transitioning from entrenched 5.56 mm platforms. For instance, Australia postponed its rifle modernization in September 2024, pending the collection of field data, due to concerns about interoperability. If three NATO members adopt the 6.8 mm caliber by 2027, the segment could double the growth rate of the small-caliber ammunition market. However, the lack of a NATO standard complicates logistics and may slow adoption outside the US.

Defense Budget Growth Fueling Sustained Demand for Operational and Training Rounds

Defense ministries increased small-arms ammunition allocations by 12% in 2024, with the US Department of Defense (DoD) requesting USD 1.8 billion for FY 2025 procurement to replenish stocks sent to Ukraine and enhance training throughput. NATO partners, including Poland, are committed to tripling wartime reserves by 2027, adding 400 million additional rounds annually. Government contracts now account for 85% of Lake City’s 1.6 billion-round capacity, reducing availability for the commercial market and raising retail prices by 15-20% since 2023. Elevated baseline orders shield the small-caliber ammunition market from cyclical downturns. Training consumption, already exceeding 350 million rounds annually for the US Army, is expected to rise as readiness standards become stricter. Consequently, defense appropriations provide a stable demand foundation, ensuring supplier revenue visibility in the medium term.

Rising Civilian Ownership and Sporting Interest Sustaining Commercial Ammunition Sales

The US recorded 434 million privately owned firearms in 2024, with first-time buyers accounting for 22% of transactions. Active concealed-carry permits reached 21.5 million in the same year, sustaining steady demand for 9 mm and .45 ACP cartridges. Competitive shooting disciplines, such as USPSA and 3-Gun, which require approximately 15,000 rounds per shooter per year, saw a 9% increase in participation in 2024. Retail demand surged during policy debates, with the 2024 US presidential election driving a 30% increase in Q4 ammunition sales, straining distributor inventories already impacted by defense contracts. Civilian consumption provides revenue diversification and higher margins but remains vulnerable to political and regulatory changes.

Environmental Regulations Accelerating Transition to Lead-Free Ammunition

California’s statewide lead-free ammunition rule for hunting and target shooting took effect in January 2024, while the EU’s REACH directive will impose similar restrictions starting in 2026.[1]California Department of Fish and Wildlife, “Lead-Free Hunting Requirements,” wildlife.ca.gov Manufacturers have expanded their copper-jacketed and solid-copper product lines despite 20-30% higher input costs and ongoing issues with primer reliability in sub-zero temperatures. The US DoD’s USD 45 million Low-Collateral-Effects Ammunition program highlights compliance pressures on military stocks. Although 38% of recreational shooters reported reducing range time due to higher costs, legal mandates are expected to drive copper demand, supporting a 5.14% CAGR for lead-free ammunition through 2031.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter firearm and ammunition export controls limiting international trade flows | -0.70% | Global, with acute impact on North America-to-Asia and Europe-to-Middle East corridors | Short term (≤ 2 years) |

| Ongoing supply chain disruptions affecting primer and propellant availability | -0.50% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising raw material costs for copper and antimony inflating manufacturing expenses | -0.40% | Global, with pass-through pricing challenges in civilian markets | Short term (≤ 2 years) |

| Gradual defense pivot toward directed-energy weapons and unmanned system lethality reducing long-term demand | -0.30% | North America and Europe, with limited Asia-Pacific impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Firearm and Ammunition Export Controls Limiting International Trade Flows

Revised US ITAR regulations in March 2024 reclassified key cartridge components, adding 60–90 days to licensing processes and delaying a USD 45 million order from the Philippines. Similarly, the EU’s July 2024 dual-use update now requires end-user certificates for sales to non-NATO buyers, which has blocked a EUR 30 million (USD 35.32 million) shipment to Saudi Arabia. These regulatory bottlenecks are redirecting contracts to producers in less-regulated jurisdictions, resulting in an 8-12% reduction in the margins of Western firms due to higher compliance costs.

Ongoing Supply Chain Disruptions Affecting Primer and Propellant Availability

China’s August 2024 antimony export restrictions reduced global supplies by 30%, driving prices from USD 11,000 to USD 18,500 per ton within five months.[2]Bloomberg, “China Antimony Export Curbs,” bloomberg.com Concurrently, the closure of a Quebec plant led to nitrocellulose shortages, leaving the US with only 90 days of propellant stock, prompting a proposed USD 50 million federal reshoring initiative. Reformulated primers that reduce antimony usage exhibit 10–15% higher misfire rates in humid climates, limiting their acceptance for military applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Caliber: NGSW Adoption Accelerates 6.8 mm Segment

The 5.56 mm caliber accounted for 33.28% of the 2025 revenue, representing the largest share of the small-caliber ammunition market. This dominance is attributed to its widespread use in nearly all NATO service rifles and millions of civilian carbines. Its unit cost of USD 0.38 supports a global inventory exceeding 10 billion cartridges, ensuring the resilience of legacy calibers in the market.

In contrast, the newer 6.8 mm cartridge, priced at approximately USD 1.20 per unit, delivers 30% higher energy at 500 meters, capable of penetrating Level IV armor. This meets the overmatch requirements of the US Army’s Next Generation Squad Weapon (NGSW) program. A USD 20.4 million retrofit at Lake City is expected to increase production by 6.8 million rounds to 50 million by 2026. However, price parity with 7.62 mm rounds is unlikely before 2029, when production capacity exceeds 200 million rounds, and scrap rates drop below 3%.

While low-cost, high-volume 5.56 mm contracts ensure factory utilization, smaller production runs of 6.8 mm rounds yield margins 600–800 basis points higher. Competitive shooters are exploring the 6.8 mm caliber for its flat trajectory, indicating potential aftermarket demand as reloading components become more accessible. If three NATO allies adopt the caliber by 2027, the 6.8 mm segment could account for over 8% of the small caliber ammunition market by 2031.

Without broader adoption, demand is expected to plateau after the US completes its fielding. Legacy 7.62 mm rounds remain relevant for machine guns and marksman rifles. In comparison, the 9 mm caliber, supported by 21.5 million US carry permits, moves approximately 18.7 billion cartridges annually, benefiting from unmatched economies of scale. A key operational risk is interoperability; without a NATO standard for 6.8 mm, coalition logistics could face duplicated supply lines, resulting in increased expeditionary costs of 12–15%.

By Weapon Platform: Rifles Dominate, SMGs Surge

Rifles accounted for 41.28% of 2025 revenue, maintaining their dominance in the small-caliber ammunition market, despite incremental upgrades that rarely alter ammunition requirements. Sub-machine guns (SMGs) are projected to grow at a 4.98% CAGR, driven by USSOCOM’s 15,000-unit MCX Rattler order, which has spurred wider adoption among agencies.

The affordability of 9 mm cartridges, at one-quarter the cost of 5.56 mm rounds, supports higher training throughput within fixed budgets. Handguns contribute approximately 28% of platform-linked demand, with each additional million permit holders driving up to 650 million extra rounds over five years. Light machine guns generate significant training consumption but are constrained by the lack of major replacement programs.

Suppressed short-barrel rifles firing subsonic 5.56 mm rounds are increasingly overlapping with SMGs, requiring logisticians to optimize stocking plans to avoid inflated costs from mixed-caliber inventories. Integrated forecasting software indicates that elite units overstock niche calibers by 8–10%, an inefficiency expected to decline as data-driven supply tools mature by 2028.

Shotguns remain a niche platform but command 50% premiums on specialty breaching slugs, ensuring profitability even at modest volumes. While rifles will continue to lead in volume, SMGs and specialized platforms are diversifying revenue streams and mitigating fluctuations in cyclic demand.

By Bullet Type: Brass Leads, Copper Gains

Brass cases accounted for 57.93% of 2025 revenue due to their balance of ductility, reloadability, and cost-effectiveness. Civilian reloaders typically reuse brass cases up to six times, enhancing their perceived value.

Copper-based, lead-free rounds are expected to grow at a 5.14% annual rate as California and EU regulations phase out lead use on public lands, prompting hunters to shift toward alternatives that are 20–30% more expensive. Producers are mitigating copper price volatility through closed-loop scrap recovery systems, which capture 92% of machining waste and save USD 28 per thousand rounds.

Steel-case imports remain attractive to budget-conscious shooters at approximately USD 0.25 per round, but concerns about extraction limit their share to under 10% of Western military contracts. Polymer cases offer a 30% weight reduction but deform above 180 °C, restricting their use to semi-automatic and designated sharpshooter roles.

Hybrid steel-aluminum designs reduce weight by 20% but only lower costs by 6–8%, limiting their appeal. Bismuth-tipped, non-toxic rounds for waterfowl could create a USD 110 million micro-segment by 2031, though current supply contracts are still in the prototype stage. To protect margins, leading manufacturers are sourcing up to 40% of their brass feedstock from reclaimed range scrap, thereby reducing their exposure to fluctuations in the London Metal Exchange.

By Lethality: Lethal Prevails, Less-Lethal Niche Expands

Lethal ammunition accounted for 90.58% of 2025 revenue, driven by the prioritization of immediate stopping power by both military and civilian users. Premium defensive pistol loads generate 10–12 percentage-point higher margins compared to standard full metal jacket (FMJ) rounds.

Less-lethal ammunition, while comprising only 9.42% of sales, is projected to grow at a 6.85% annual rate due to policing reforms. For instance, Los Angeles mandates ten kinetic-impact projectiles per patrol car, resulting in a yearly increase in replenishment demand of 1.2 million units.

Although accuracy declines significantly beyond 30 meters and injury variability remains a concern, chemical irritant and marker rounds provide additional options. Specialty training rounds compatible with virtual reality simulators command premiums of 40-60%, mitigating volume risks.

Manufacturers view this segment as a testing ground for innovations such as biodegradable sabots and reduced-energy payloads, which can later be adapted for lethal ammunition, fostering cross-segment innovation.

By End-Use: Military Dominates, Civilian Segment Outpaces

Military orders accounted for 66.95% of 2025 revenue, with NATO training alone consuming over 2 billion rounds annually, providing a stable demand base. Civilian purchases are expected to grow at a 3.90% annual rate, adding USD 690 million to the small caliber ammunition market by 2031, equivalent to the output of two mid-scale plants. In 2024, the 16.3 million US background checks drove an average of 63 rounds of first-year consumption, further compounding replacement demand.

Competitive shooting acts as a demand multiplier, with one USPSA Grand Master consuming approximately 25,000 rounds annually, equivalent to the usage of forty casual shooters. Homeland security agencies are reallocating budgets toward surveillance technologies, resulting in an 8% reduction in ammunition purchases for FY 2025.

Civilian channels yield gross margins of up to 28%, supported by branded packaging and accessory tie-ins, which offset the thinner margins of military contracts. However, political risks persist; for example, a proposed USD 0.05 excise surcharge could reduce civilian volumes by 14%. To mitigate this risk, producers limit commercial exposure to around 55%, balancing growth opportunities with regulatory uncertainties.

Geography Analysis

North America led with a 29.95% revenue share in 2024, powered by the US's USD 849.8 billion defense budget and a vibrant civilian shooting culture. The Lake City Army Ammunition Plant alone supplies approximately 85% of the US military's small-caliber requirements, while selling commercial overruns to the market. Federal and state programs promoting lead-free hunting keep product diversity high, forcing local producers to allocate R&D funds toward non-toxic formulas.

The Asia-Pacific region shows the fastest trajectory, with a 4.12% CAGR through 2031. India's Atmanirbhar Bharat policy has directed substantial investment toward indigenous ammunition lines, and procurement delays from traditional suppliers are pushing New Delhi to expand its vendor base. Regional flashpoints in the South and East China Seas further motivate nations to build up their stockpiles. South Korea, for instance, maintains one of the world's largest inventories of 105 mm ammunition and has signaled its willingness to provide it to partners.[3]Center for Strategic and International Studies, “South Korean Munitions Supply Assessment,” csis.org

Europe is retooling its industrial base after the Ukraine conflict exposed supply shortfalls. Rheinmetall has increased its annual artillery shell output by an order of magnitude, and the nine-country SAAT initiative aims to establish a harmonized ammunition standard to ensure interoperability. At the same time, the European Chemicals Agency's lead-restriction roadmap compels European manufacturers to retrofit lines for copper-based bullets.

Competitive Landscape

The five largest suppliers, Northrop Grumman’s Lake City operations, Olin’s Winchester, BAE Systems, Rheinmetall, and Nammo, account for approximately 40% of global revenue, reflecting a moderately concentrated market. Olin secured a stable primer feedstock supply by acquiring a 30% stake in a Bolivian antimony mine, thereby mitigating risks associated with Chinese export restrictions. Both Winchester and Rheinmetall have announced significant capacity expansions, each involving nine-figure investments, to address rising NATO and civilian demand.

Emerging players are focusing on niche technologies. Actual Velocity’s polymer-case 6.8 mm round, selected by the US Army, faces challenges related to heat dissipation that must be resolved before scaling production. Barnes Bullets markets premium all-copper TAC-X loads with 95% weight retention, catering to police agencies restricted by lead bans. Nammo has implemented robotic production lines, resulting in a 35% reduction in labor costs, demonstrating how automation can counteract wage inflation.

In summary, resilience to material shortages and adherence to environmental regulations are becoming more critical than traditional cost advantages. Companies that secure upstream inputs, adopt automation, and develop lead-free or lightweight products are well-positioned to gain market share as the small-caliber ammunition market continues to evolve.

Small Caliber Ammunition Industry Leaders

-

Olin Corporation

-

Nammo AS

-

Northrop Grumman Corporation

-

BAE Systems plc

-

Rheinmetall AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Winchester Ammunition (Olin Corporation) announced a USD 100 million expansion of its Oxford, MS, plant. This expansion aims to add 500 million rounds of production capacity by 2027, addressing increased demand from civilian and law enforcement markets following the 2024 election.

- February 2025: The US Army commenced construction of a 450,000-square-foot ammunition facility at the Lake City Army Ammunition Plant in Missouri. Operated by Olin Winchester, the facility is designed to produce 385 million cartridges and 490 million projectiles annually for the Next Generation Squad Weapons program.

- January 2025: FN Herstal initiated the SAAT project, which secured EUR 8.30 million (USD 9.63 million) in funding from nine European states. The project aims to develop standardized small-arms ammunition, including advanced projectile prototypes.

- April 2024: Rheinmetall invested approximately EUR 500 million (USD 588.72 million) in a new ammunition plant in Unterlüß, Germany.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the small-caliber ammunition market as factory-produced cartridges of <= 12.7 mm (.50) used in handguns, rifles, shotguns, light machine guns, and sub-machine guns for military, homeland security, and civilian purposes. The sizing captures only fresh production revenues booked at the manufacturer level.

Scope exclusion: reloaded rounds, pyrotechnic flares, and medium or larger calibers lie outside this assessment.

Segmentation Overview

-

By Caliber

- 5.56 mm

- 6.8 mm

- 7.62 mm

- 9 mm

- 12.7 mm

- Other Calibers

-

By Weapon Platform

- Handguns

- Rifles

- Light Machine Guns (LMGs)

- Sub-Machine Guns (SMGs)

- Shotguns

-

By Bullet Type

- Brass

- Copper

- Steel

- Others

-

By Lethality

- Less Lethal

- Lethal

-

By End Use

- Military

- Homeland Security

- Civilian

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview ordnance officers, procurement planners, range owners, and ammunition distributors across North America, Europe, Asia-Pacific, and the Middle East. These conversations test secondary assumptions on average selling price, training-round share, and new 6.8 mm adoption, while short web surveys of civilian shooters reveal demand seasonality and e-commerce shifts.

Desk Research

We begin with structured mining of open sources such as UN Comtrade shipment codes, SIPRI military-expenditure tables, the US ATF Annual Firearms Manufacturing & Export Report, and regional police procurement gazettes. These provide hard counts on production, trade, and licensed firearm stocks. Trade association briefs from SAAMI and the European Sporting Arms Federation, together with patent families pulled from Questel, help us follow caliber innovation and material shifts. Company 10-Ks, investor decks, and press releases add unit prices and backlog clues. Select data cuts from D&B Hoovers and Dow Jones Factiva anchor financials and news flow. This list is illustrative; many further sources support data collection, validation, and clarification.

Market-Sizing & Forecasting

We apply a top-down and bottom-up blend. First, national production and import-export balances reconstruct the 2025 demand pool, which is then calibrated with sampled average selling prices and verified shipment receipts. Supplier roll-ups for nine leading manufacturers act as a bottom-up reasonableness check and guide minor adjustments. Key model drivers include (1) defense budget outlays earmarked for small arms, (2) active-duty troop counts, (3) civilian concealed-carry permit growth, (4) average rounds expended per soldier in training cycles, and (5) lead-to-copper material substitution trends that nudge ASPs. Multivariate regression overlays these variables on a five-year history to generate forecast coefficients; scenario analysis captures conflict-driven demand spikes. Missing datapoints are bridged using regional analogs vetted in expert calls.

Data Validation & Update Cycle

Outputs pass variance checks against import unit values and quarterly manufacturer sales. A senior analyst reviews anomalies before sign-off. Reports refresh yearly, and we trigger mid-cycle revisions if major procurement contracts or policy shifts emerge.

Why Mordor's Small Caliber Ammunition Baseline Commands Trust

Published estimates often diverge; some studies widen caliber bands or mix refurbished rounds, while others apply static price decks or infrequent updates.

Key gap drivers include scope drift beyond 12.7 mm, aggressive volume uplift from unverified retail surveys, or single-scenario forecasts that ignore ammunition spend caps. Mordor's disciplined scope, annual refresh, and variable selection minimize these skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.90 B (2025) | Mordor Intelligence | - |

| USD 13.46 B (2025) | Global Consultancy A | Includes shotgun shells and polymer-cased prototypes not yet commercialized |

| USD 5.70 B (2024) | Industry Association B | Excludes civilian sport-shooting demand outside North America |

| USD 10.39 B (2025) | Trade Journal C | Applies uniform ASP across regions and uses 2023 volume growth as proxy for 2025 |

These contrasts show that Mordor's calibrated scope, live price tracking, and multi-source validation deliver a balanced, transparent baseline that decision-makers can readily audit and replicate.

Key Questions Answered in the Report

What is the projected value of the small caliber ammunition market by 2031?

Forecasts indicate the small caliber ammunition market, valued at USD 9.17 billion in 2026, is poised to ascend to USD 10.72 billion by 2031, marking a steady CAGR of 3.17% during the period.

Which caliber is forecast to grow fastest?

The 6.8 mm category, supported by the US Army’s NGSW adoption, is set for a 7.12% CAGR.

Why are copper-based bullets gaining traction?

California and EU lead-free mandates are driving a shift to copper, pushing this segment to a 5.14% CAGR despite higher costs.

Which region will post the highest growth?

Asia-Pacific, led by India and Japan, is projected to grow at a 4.12% CAGR through 2031.

How are supply-chain risks being mitigated?

Major firms are bolstering their positions by investing in upstream assets like antimony mines and ramping up automation to lessen reliance on labor and materials.

What technology trend could disrupt long-term ammunition demand?

Directed energy weapons (DEWs) funded at USD 1.4 billion in FY 2025 may reduce reliance on kinetic rounds after 2035 once power and cost hurdles fall.

Page last updated on: