Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.70 Billion |

| Market Size (2026) | USD 9.06 Billion |

| Market Size (2031) | USD 11.23 Billion |

| Growth Rate (2026 - 2031) | 4.40% CAGR |

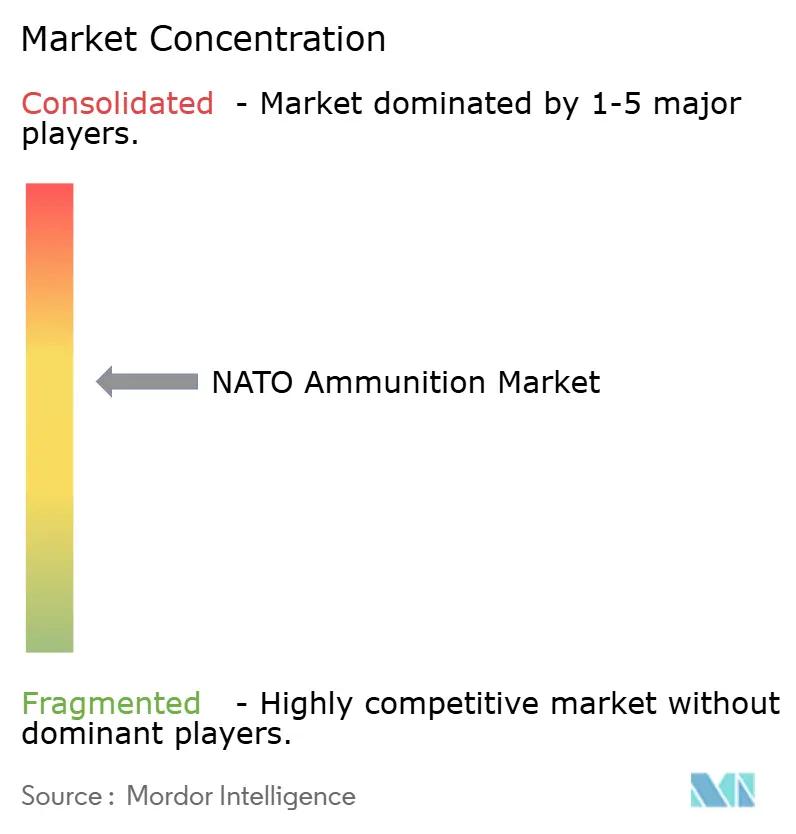

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NATO Ammunition Market Analysis by Mordor Intelligence

The NATO ammunition market size is expected to grow from USD 8.7 billion in 2025 to USD 9.06 billion in 2026 and is forecasted to reach USD 11.23 billion by 2031 at a 4.4% CAGR over 2026-2031. This growth highlights a structural shift as member states replenish inventories depleted by transfers to Ukraine, while simultaneously building multi-year stockpiles in alignment with updated defense planning assumptions. Increased defense budgets, a renewed focus on artillery-centric doctrines, and streamlined contract procedures through the NATO Support and Procurement Agency (NSPA) are driving demand.

Prime contractors are accelerating capacity investments, supported by government-guaranteed minimum volumes through long-term framework agreements. Environmental regulations are influencing demand for small-caliber ammunition, encouraging the adoption of lead-free projectiles, while compliance with STANAG 4439 standards is promoting the use of insensitive munition fills. These factors are shifting market dynamics from price competition to a focus on surge-capacity differentiation, raising the competitive standards across the NATO ammunition market.

Key Report Takeaways

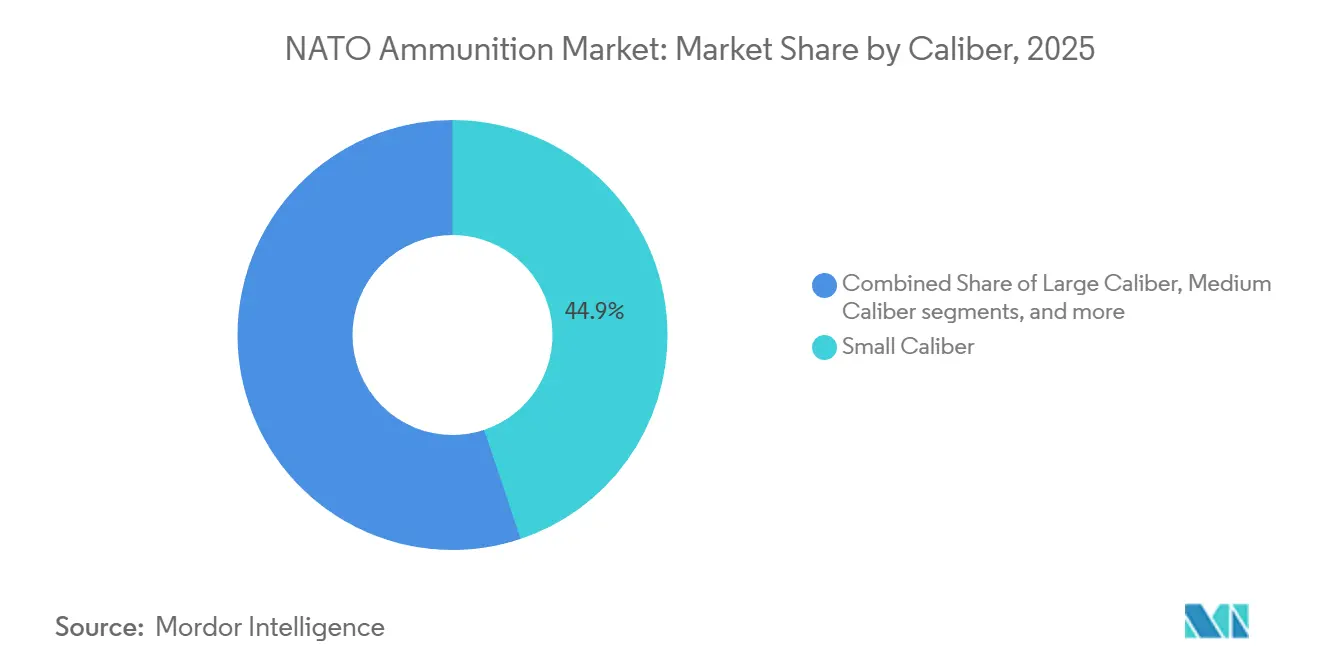

- By caliber, small-caliber ammunition accounted for 44.87% of the market share, while large-caliber shells are forecasted to record the highest 6.10% CAGR through 2031.

- By product, bullets and cartridges accounted for 45.93% of revenue in 2025; artillery shells and mortars are projected to achieve the fastest growth, with a 5.90% CAGR through 2031.

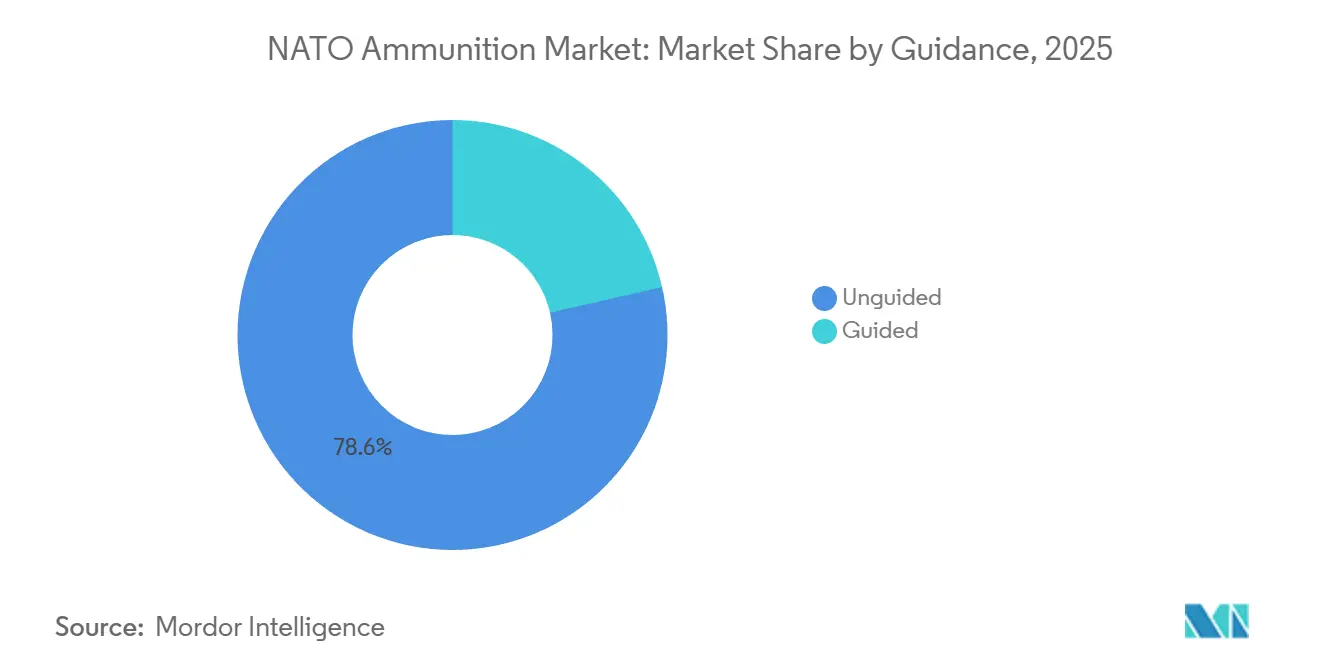

- By guidance, unguided ammunition dominated the NATO ammunition market with a 78.58% share in 2025, while guided rounds are anticipated to grow at an 8.57% CAGR between 2026 and 2031.

- By end user, military demand accounted for 75.90% of the NATO ammunition market in 2025; civil and sport shooting is expected to grow at a 4.78% CAGR through 2031.

- By platform, land platforms accounted for around 56.34% of the NATO ammunition market in 2025, while airborne ammunition is projected to grow at a 4.93% CAGR through 2031.

- The United States accounted for 35.25% of the NATO ammunition market size in 2025. Poland, on the other hand, is expected to experience the fastest growth, with a projected CAGR of 9.41% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

NATO Ammunition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened NATO defense-spending commitments | +1.20% | Global, concentrated in Poland, Germany, UK | Medium term (2-4 years) |

| Inventory replenishment after Ukraine conflict | +0.90% | United States, Germany, France, UK, Poland | Short term (≤ 2 years) |

| Multiyear framework contracts for 155 mm rounds | +0.80% | Germany, United States, Poland, France | Medium term (2-4 years) |

| Allied call-off options for smart cartridge fuzes | +0.60% | United States, Germany, France, UK, Poland | Medium term (2-4 years) |

| Accelerated NSPA procurement processes | +0.50% | Global NATO membership | Short term (≤ 2 years) |

| Shift toward insensitive-munition fillers | +0.40% | United States, Germany, France, UK, with spillover to Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened NATO Defense-Spending Commitments

Member-state budgets are increasing at the fastest rate since the end of the Cold War. In 2024, twenty-three out of thirty-two allies met the 2% of GDP defense spending benchmark, a significant rise from just six a decade earlier. European defense expenditures grew by 18% in 2024, with artillery, small arms, and air-defense munitions receiving a substantial share of the additional funds. Discussions around a potential 5% GDP target by 2035 could unlock a further EUR 100 billion (USD 117.22 billion) annually, with 15-20% of this likely allocated to ammunition procurement. Poland’s 4.7% of GDP defense spending highlights this trend, with significant investments in 155 mm and small-caliber ammunition production. Meanwhile, southern-flank members remain focused on naval priorities, creating regional demand disparities that suppliers must address when planning NATO ammunition production runs.

Inventory Replenishment After Ukraine Conflict

Transfers to Kyiv have significantly depleted alliance stockpiles, falling below planned levels. By mid-2024, the US had shipped over 2 million 155 mm rounds, prompting a surge plan to produce 100,000 shells per month by the end of 2024. Germany’s stockpile dropped below 30,000 rounds, leading to an EUR 8.5 billion (USD 9.96 billion) contract with Rheinmetall for 220,000 shells and a 700,000-round annual baseline starting in 2026.[1]Rheinmetall, “Framework Contract for 155 mm Ammunition,” rheinmetall.com Allies are shifting away from just-in-time inventory models in favor of maintaining 90-180 day reserves, a move expected to increase baseline demand by approximately 40% through 2027. This replenishment effort is accelerating the adoption of advanced technologies, as governments prioritize refilling stockpiles with insensitive or programmable rounds, despite their 20-30% higher costs compared to legacy munitions.

Multiyear Framework Contracts for 155 mm Rounds

Long-term agreements ensure minimum production volumes, enabling investments in new production lines. Germany’s EUR 8.5 billion (USD 9.96 billion) contract secures 220,000 shells initially, with options for up to 700,000 annually, supporting the establishment of a greenfield production line in Unterlüß. Similarly, the US Army issued USD 961 million in indefinite-delivery contracts in 2024, providing buyers with pricing leverage and suppliers with revenue predictability.[2]US Department of Defense, “DoD Announces Additional Security Assistance for Ukraine,” defense.gov Poland, France, and the UK have adopted similar contract structures. These frameworks reduce unit costs by 15-25% compared to spot purchases, ensuring NATO ammunition demand is met through domestic or allied supply chains.

Allied Call-Off Options for Smart Cartridge Fuzes

Programmable fuzes are transitioning from niche applications to mainstream use. The XM1147 AMP round for the Abrams tank consolidates four legacy variants through airburst programming. Rheinmetall’s AHEAD technology enables in-flight programming of 35 mm rounds, creating precise sub-projectile clouds. In 2024, the US Army awarded contracts exceeding USD 200 million to extend airburst capabilities to 155mm artillery. However, export controls, particularly those tied to US semiconductors subject to ITAR licensing, extend delivery timelines by 6-12 months.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Press-powder and primer feed-stock shortages | -0.70% | United States, Western Europe | Short term (≤2 years) |

| Ageing case-line tooling at legacy factories | -0.60% | United States, France, United Kingdom | Medium term (2-4 years) |

| Tightened ITAR / export-control bottlenecks | -0.50% | United States, Europe | Short term (≤2 years) |

| Range-environmental restrictions on lead propellants | -0.40% | United States, European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Press-Powder and Primer Feed-Stock Shortages

The global supply of nitrocellulose and antimony remains constrained. China accounts for 70% of antimony exports, and periodic export restrictions have driven primer prices up by 40-60% since 2022.[3]Nikhil Patel, “China’s Antimony Export Restrictions Threaten US Ammunition Supply,” Reuters, reuters.com In the West, only a limited number of plants produce propellant powder, and establishing new capacity requires 3-5 years for environmental permitting. General Dynamics allocated USD 50 million in 2024 to expand propellant production, but full operational capacity is not expected until 2027. Producers are prioritizing allocations, focusing on 155 mm shells over small-arms training rounds, which has tightened the NATO ammunition market in the short term.

Range-Environmental Restrictions on Lead Propellants

The US Environmental Protection Agency implemented a ban on lead ammunition on federal lands in 2024, affecting approximately one-third of military training consumption. Similarly, the EU’s REACH framework is phasing out lead projectiles in wetlands, with broader outdoor bans under consideration for 2028. Manufacturers are transitioning to copper or tungsten rounds, which are 30-50% more expensive than the traditional materials. The process of ballistic re-qualification further delays adoption. Winchester invested USD 35 million in 2024 to expand lead-free production lines, but current capacity remains insufficient to meet the growing demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Caliber: Large-Caliber Artillery Drives Growth

Large-caliber rounds are projected to grow at a 6.10% CAGR through 2031, surpassing growth in other caliber categories as 155 mm fire support regains doctrinal importance. The NATO ammunition market for large-caliber munitions is bolstered by the US Army’s plan to sustain production of 100,000 shells per month, significantly exceeding historical peaks. Small-caliber ammunition, while maintaining a 44.87% market share in 2025, faces margin pressures due to mandatory transitions to lead-free cartridges.

Unit cost differences influence budgeting priorities. Conventional ball rounds cost less than USD 1.50, while high-explosive 155 mm shells range from USD 3,000 to USD 8,000, and Excalibur precision-guided variants exceed USD 68,000. Despite these costs, the lethality of large-caliber rounds at a 40 km range remains critical in contested maneuver corridors. Mid-caliber growth is uneven, driven by vehicle upgrade cycles such as the Puma IFV and Bradley A4 cannon enhancements.

By Product: Artillery Shells Capture Framework Spending

Artillery shells and mortars are expected to grow at a 5.90% CAGR from 2026 to 2031, supported by multi-year contracts from Germany, the US, and Poland that secure minimum production volumes. Bullets and cartridges continue to generate the highest throughput, accounting for 45.93% of 2025 revenue. However, environmental compliance costs and surplus stock sell-offs are flattening demand trends.

Supply chain structures vary significantly. Small-caliber ammunition is produced in vertically integrated facilities, such as Lake City, whereas artillery cases, fills, and fuzes rely on a three-tier network that is susceptible to bottlenecks. US 155 mm indefinite-delivery contracts worth USD 961 million in 2024 demonstrate risk pooling, enabling the Army to adjust production without the need for renegotiation.

By Guidance: Smart Fuzes Justify Cost Premiums

Guided munitions are forecasted to grow at an 8.57% CAGR, the fastest among guidance categories, even though unguided rounds accounted for 78.58% of 2025 volume. The NATO ammunition market for guided rounds is supported by programmable fuzes that triple the first-hit probability, justifying unit costs that are 50-100% higher.

Export restrictions under ITAR regulations slow international sales, as semiconductor-equipped fuzes require separate licensing, potentially delaying deliveries by up to a year. In response, companies such as France’s Nexter and Poland’s MESKO are developing domestic variants to circumvent these delays, reflecting a broader trend toward regionalized electronics supply chains.

By End-User: Civilian Shooting Absorbs Surplus Stocks

Military customers accounted for 75.90% of 2025 demand, but civil and sport shooting is growing at a 4.78% CAGR due to rising firearms ownership in Central and Eastern Europe. Surplus 5.56 mm and 7.62 mm rounds are now retailing for less than USD 0.50, undercutting new production and widening price differentials for civilian buyers.

Performance requirements vary: law enforcement prioritizes frangible or reduced-ricochet projectiles, while civilian shooters focus on affordability, often accepting minor accuracy trade-offs. EU REACH regulations phasing out lead shot are driving investments, such as Olin’s USD 35 million copper-composite expansion in Mississippi.

By Platform: Airborne Systems Gain Share

Land platforms represented 56.34% of 2025 consumption, reflecting artillery’s pivotal role in the Ukraine conflict and ongoing fleet modernization efforts. Airborne ammunition is growing at a 4.93% CAGR, driven by the proliferation of loitering munitions and armed drones. For example, AeroVironment’s Switchblade 600 demonstrates how miniature warheads can replicate anti-tank effects in a 50-lb package.

Naval ordnance remains a niche segment, constrained by a shift toward missile-centric surface warfare and the anticipated adoption of directed energy weapons (DEWs). However, demand for 127 mm guns persists for shore bombardment and cost-effective area denial operations.

Geography Analysis

The US held a 35.25% market share in 2025, driven by plans to increase the monthly production of 155 mm shells to 100,000 and sustained demand for small-caliber ammunition from Army and Marine units. Long-term industrial-based investments at facilities in Radford and Scranton are set to support future production capacity. Germany ranked second, backed by an EUR 8.5 billion (USD 9.96 billion) framework agreement, establishing a 700,000-shell annual production baseline by 2026, reflecting a shift toward enhanced artillery capabilities across Europe.

Poland is the fastest-growing market, with a projected CAGR of 9.41% through 2031, fueled by defense spending equivalent to 4.7% of GDP and the establishment of new joint-venture plants for 155 mm and medium-caliber ammunition production. France, the United Kingdom, Italy, and Spain are pursuing moderate growth within budgetary constraints, channeling their orders through the NSPA to achieve economies of scale. Turkey’s MKE complex is expanding its production capacity for both small-caliber and artillery ammunition, catering to domestic needs and export demands within the NATO ammunition market.

Smaller eastern-flank NATO members, including the Baltic states, Romania, and Bulgaria, are replenishing stockpiles transferred to Ukraine and pre-positioning munitions to deter potential Russian aggression. These countries rely heavily on NSPA frameworks, benefiting from standardized technical specifications and guidelines that provide a consistent approach. Meanwhile, southern-flank NATO allies are prioritizing investments in naval interceptors and air-defense ammunition, creating a diverse demand landscape that requires suppliers to maintain adaptable, multi-caliber production capabilities.

Competitive Landscape

The NATO ammunition market exhibits moderate concentration. The top three companies, Rheinmetall, BAE Systems, and General Dynamics, account for approximately 40-45% of large-caliber production capacity. Mid-tier firms, such as Nammo and MESKO S.A., are expanding modular production lines to secure new framework contracts. Contract awards are increasingly determined by production capacity rather than price, as governments prioritize the ability to scale production. For instance, Rheinmetall’s new Unterlüß plant is projected to produce up to 700,000 shells annually by 2026, reducing unit costs by 15-20% through complete automation.

Vertical integration enhances market resilience. BAE Systems operates its own propellant production lines, while General Dynamics controls Radford powder output, insulating both companies from feedstock supply disruptions. Emerging market opportunities focus on insensitive munition retrofits, programmable fuzes, and conversion kits that enable guidance for unguided artillery. Companies with expertise in STANAG 4439 explosive chemistry and digital fuze design hold a first-mover advantage. Additionally, tighter export controls are driving European nations to develop indigenous supply chains, encouraging intra-EU collaborations and prompting transatlantic ventures to localize electronics production.

Ongoing modernization programs are placing pressure on facilities still operating with 1970s-era tooling. Suppliers unwilling to invest approximately EUR 200 million (USD 234.38 million) per production line risk exclusion, as buyers increasingly demand insensitive fills and programmable fuzes. Nammo’s Raufoss plant exemplifies a challenger strategy, utilizing modular production lines near customer arsenals to meet offset requirements and reduce logistics costs. Competitive intensity is expected to increase through 2030 as the NATO ammunition market navigates the balance between replenishment cycles and the adoption of new technologies.

NATO Ammunition Industry Leaders

Rheinmetall AG

General Dynamics Corporation

BAE Systems plc

Nammo AS

MESKO S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rheinmetall commenced operations at Europe's largest ammunition factory, located in Lower Saxony, to address the urgent requirements of armed forces across Europe. The company invested nearly EUR 500 million (approximately USD 586 million) in constructing the production facility at its Unterlüß site in the Celle district, completing the project in a record 15 months.

- December 2024: The government of Kosovo agreed with the Turkish state-owned defense manufacturer, Makine ve Kimya Endüstrisi A.Ş., to operationalize an ammunition factory in Kosovo. The facility will produce various calibers of ammunition in compliance with NATO standards.

NATO Ammunition Market Report Scope

NATO-standard ammunition includes cartridges, shells, bombs, grenades, and related ordnance that are produced, tested, and certified to comply with the alliance’s STANAG interoperability and safety standards. These munitions are designed for use by the land, naval, and airborne forces of all 32 member states. The analysis of the NATO ammunition market encompasses the procurement, stockpiling, and usage of live-fire munitions, along with component-level maintenance activities, across military, law enforcement, and civilian end-users within alliance territories.

The NATO ammunition market is segmented by caliber, product type, guidance system, end user, platform, and geography. By caliber, the market is categorized into small-caliber, medium-caliber, large-caliber, and other specialized rounds. By product, it is divided into bullets and cartridges, artillery shells and mortars, and aerial bombs and grenades. Based on guidance, the market is segmented into unguided and guided munitions. By end user, it is classified into military, law enforcement, and civil & sport shooting segments. Platform segmentation includes land, naval, and airborne ammunition. Geographically, the study covers the United States, Canada, Germany, France, the United Kingdom, Italy, Poland, Spain, Turkey, and other NATO member countries. Market sizing and forecasts are presented in value terms (USD billion) for all these segments.

By Caliber

| Small Caliber |

| Medium Caliber |

| Large Caliber |

| Others |

By Product

| Bullets and Cartridges |

| Artillery Shells and Mortars |

| Aerial Bombs and Grenades |

By Guidance

| Guided |

| Unguided |

By End-User

| Military |

| Law-Enforcement |

| Civil and Sport Shooting |

By Platform

| Land Platform |

| Naval Platform |

| Airborne Platform |

By Geography

| United States |

| Canada |

| United Kingdom |

| France |

| Germany |

| Italy |

| Poland |

| Spain |

| Turkey |

| Rest of NATO Countries |

| By Caliber | Small Caliber |

| Medium Caliber | |

| Large Caliber | |

| Others | |

| By Product | Bullets and Cartridges |

| Artillery Shells and Mortars | |

| Aerial Bombs and Grenades | |

| By Guidance | Guided |

| Unguided | |

| By End-User | Military |

| Law-Enforcement | |

| Civil and Sport Shooting | |

| By Platform | Land Platform |

| Naval Platform | |

| Airborne Platform | |

| By Geography | United States |

| Canada | |

| United Kingdom | |

| France | |

| Germany | |

| Italy | |

| Poland | |

| Spain | |

| Turkey | |

| Rest of NATO Countries |

Key Questions Answered in the Report

What is the current value of the NATO ammunition market?

The NATO ammunition market is valued at USD 9.06 billion as of 2026 and is expected to reach USD 11.23 billion by 2031.

How fast is artillery ammunition demand growing within NATO?

Large-caliber rounds, primarily 155 mm artillery, are forecasted to expand at a 6.10% CAGR during 2026-2031 as fires doctrine regains prominence.

Which NATO member is experiencing the fastest ammunition spending growth?

Poland leads with a projected 9.41% CAGR through 2031, supported by defense spending equal to 4.7% of GDP.

Why are programmable fuzes becoming important in NATO stocks?

Programmable ammunition improves target effects three-to-fivefold and reduces the number of rounds needed, making it cost-effective despite higher unit prices.

How are environmental regulations affecting small-caliber procurement?

The US and EU bans on lead projectiles are pushing buyers toward copper or tungsten rounds, lifting costs 30-50% and triggering new production-line investments.

What supply-chain risks worry NATO buyers?

Antimony dependence, nitrocellulose capacity limits, and ITAR licensing delays present the most acute bottlenecks over the next two years.

Page last updated on: