Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 88.72 Billion |

| Market Size (2031) | USD 109.72 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

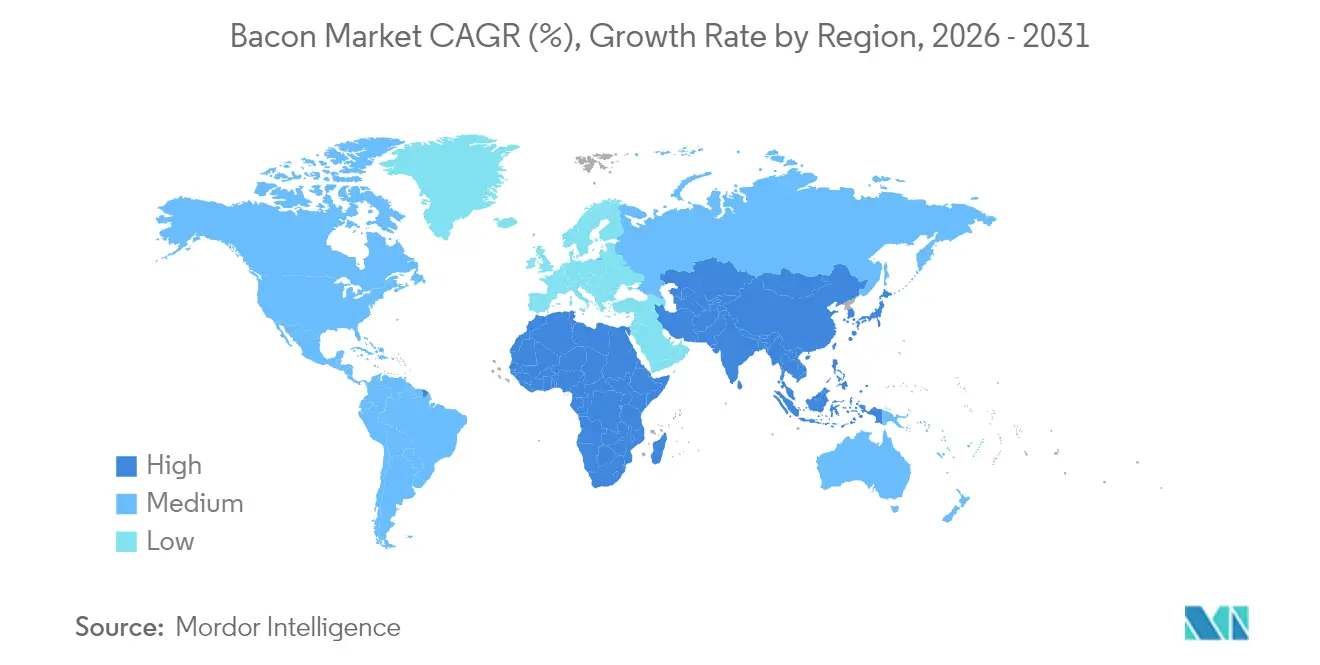

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

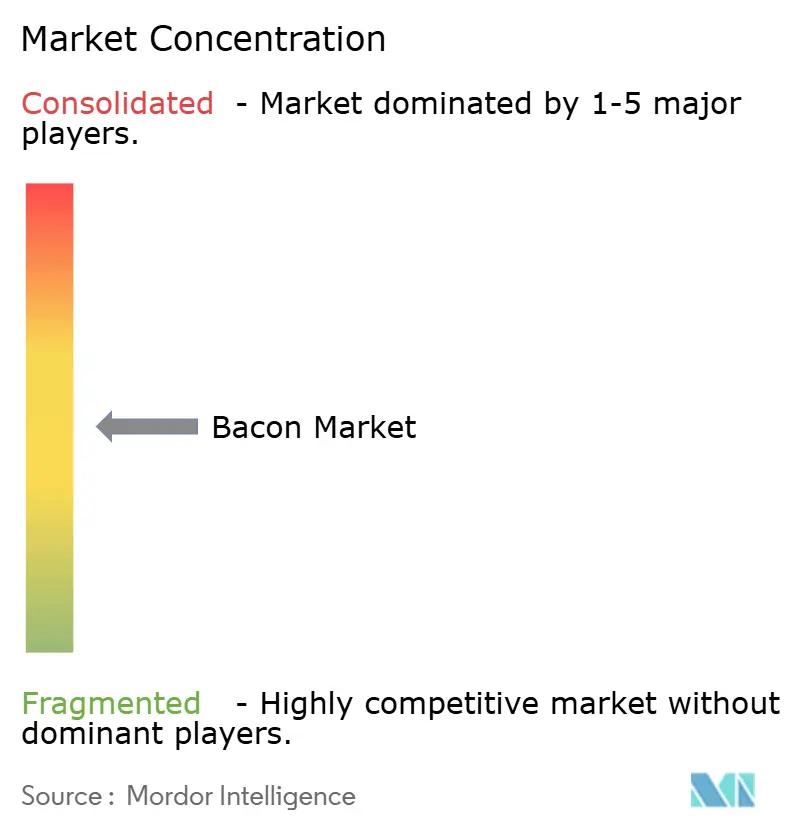

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bacon Market Analysis by Mordor Intelligence

The bacon market size was valued at USD 85.03 billion in 2025 and estimated to grow from USD 88.72 billion in 2026 to reach USD 109.72 billion by 2031, at a CAGR of 4.34% during the forecast period (2026-2031). The market growth is driven by bacon's established position as a breakfast food and its increasing use as a flavor enhancer in various dishes. The expansion of quick-service restaurants (QSRs) globally has significantly contributed to bacon consumption, particularly in sandwiches, burgers, and other menu items. Rising disposable incomes in urban Asian markets have led to increased Western food adoption, including bacon-based products. Product innovations, including low-sodium variants, flavored options, and pre-cooked products, have expanded consumer choices and convenience. The market shows distinct regional patterns, with mature Western markets focusing on premium products, artisanal preparations, and organic variants, while emerging economies experience volume-driven growth through modern retail channels and growing foodservice sectors. These trends reflect the influence of evolving consumer preferences, retail development, and changing dietary habits across different regions.

Key Report Takeaways

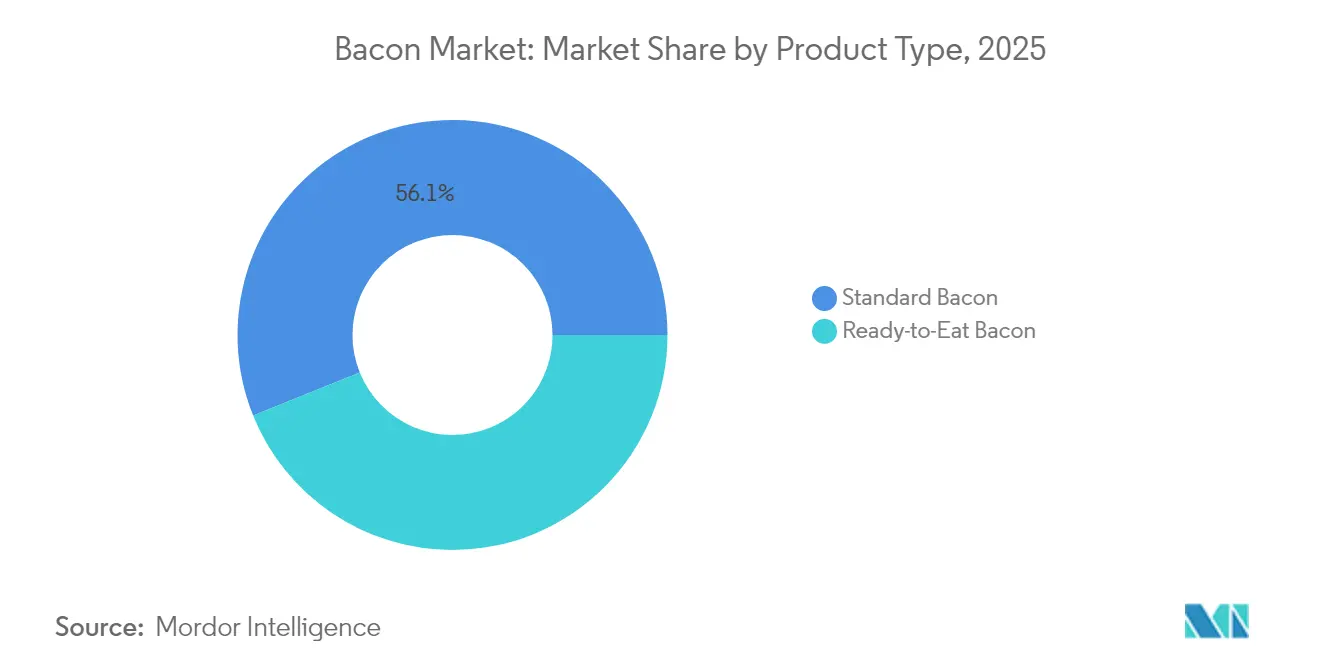

- By product type, standard bacon held 56.10% of the bacon market share in 2025, while ready-to-eat bacon variants are projected to expand at a 6.49% CAGR to 2031.

- By meat type, pork dominated with 92.45% of the bacon market share in 2025, with beef being forecasted to grow at 5.32% CAGR through 2031.

- By cut type, sliced bacon led with a 41.62% share in 2025, and pre-cooked formats are poised for the highest 6.29% CAGR.

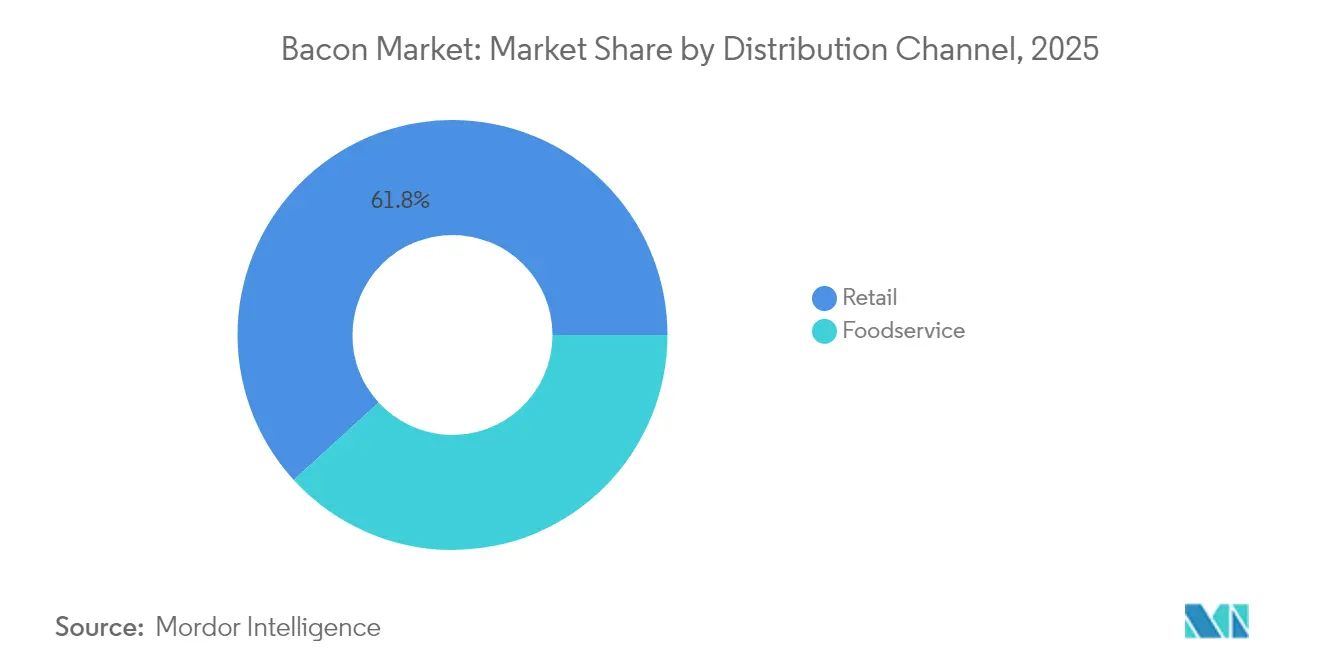

- By distribution channel, retail channel accounted for 61.78% share of the bacon market size in 2025, whereas foodservice is advancing at 6.11% CAGR between 2026-2031.

- By geography, North America captured 38.10% of the 2025 share, while Asia-Pacific is set to post the strongest 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bacon Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Protein-Rich and Savory Foods Drives Demand | +0.8% | Global, with strongest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Product Innovation With Flavors and Healthier Options Drives Growth | +0.6% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growth of Quick-Service and Fast-Food Restaurants Boosts Demand | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Retail Expansion in Emerging Markets Drives Sales | +0.7% | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Expansion of Ready-to-Eat and Convenience Foods Boosts Demand for Bacon | +0.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Increasing Popularity of Western Cuisines Worldwide Surges Demand | +0.4% | Asia-Pacific, Middle East and Africa, with selective impact in Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Protein-Rich and Savory Foods Drives Demand

Protein consumption patterns across emerging markets demonstrate accelerating demand for high-quality animal proteins, with bacon benefiting from its concentrated protein content and umami-rich flavor profile. Brazil's pork production is forecasted to increase by 2% in 2025 to 4.73 million metric tons in 2025, driven by lower feed costs and strong external demand, according to the United States Department of Agriculture [1]United States Department of Agriculture Foreign Agricultural Services, “Livestock and Poultry: World Markets and Trade", www.fas.usda.gov. The protein premiumization trend particularly benefits bacon producers, as consumers increasingly view bacon as a flavor enhancer rather than merely a breakfast item. Asian markets show a remarkable appetite for Western protein formats, with Thailand's foodservice sector sourcing 30-35% of products through imports, including significant volumes of United States beef and bacon in 2024, according to the United States Department of Agriculture [2]United States Department of Agriculture Foreign Agricultural Services, "Foodservice - Hotel Restaurant Institutional Annual", www.fas.usda.gov. This dietary evolution creates sustained demand momentum, particularly in urban centers where disposable income growth enables premium protein purchases. The combined effect of higher protein aspirations, umami-driven taste preferences, and premiumization of meal occasions underpins a durable uptick in bacon consumption across varied demographics.

Product Innovation With Flavors and Healthier Options Drives Growth

Innovation cycles in bacon manufacturing accelerated significantly in 2024, with major producers launching differentiated products targeting health-conscious consumers and flavor experimentation. Hormel Foods introduced Oven-Ready Thick-Cut Bacon with simplified cooking methods in September 2024. In a similar vein, in March 2024, Applegate Farms released Fully Cooked Sunday Bacon, specifically targeting health-conscious demographics, highlighting a shift in the industry, i.e., wellness trends can coexist with bacon consumption, leading to reimagined product formulations. Brands are ramping up research and development investments, delving into reduced sodium content, natural curing agents, and cleaner ingredient lists, all in a bid to align with shifting consumer expectations. Further, the innovation pipeline extends beyond flavor and ingredient enhancements to include advancements in processing technologies, with companies investing in automated packaging systems such as JLS Automation's Harrier bacon draft loading system, introduced in May 2025, which improves food safety and reduces labor costs. These technological advances enable producers to deliver consistent quality while meeting diverse consumer preferences, creating competitive differentiation in an otherwise commoditized market.

Growth of Quick-Service and Fast-Food Restaurants Boosts Demand

Foodservice channel expansion represents the most significant demand driver for bacon consumption, with quick-service restaurants increasingly incorporating bacon as a premium ingredient across menu categories. The foodservice channel significantly outpaces retail growth, driven by operational efficiency gains from precooked bacon products that reduce kitchen preparation time and labor costs. Restaurant chains leverage bacon's flavor intensity to justify premium pricing while maintaining cost efficiency through centralized procurement and standardized preparation protocols. Bacon-based menu innovations in limited-time offers (LTOs) have successfully driven traffic and boosted average ticket sizes. The versatility of bacon seamlessly integrates into diverse cuisines and menu formats, from gourmet burgers and sandwiches to loaded fries and salads, broadening its demographic appeal. With a strong consumer demand for indulgent comfort foods, foodservice operators prioritize bacon, recognizing it as a dependable profit generator that aligns with consumer cravings and operational feasibility. This dynamic creates sustained volume growth that transcends traditional breakfast dayparts, extending bacon consumption across lunch, dinner, and snacking occasions.

Retail Expansion in Emerging Markets Drives Sales

Retail infrastructure development in emerging economies creates unprecedented access points for bacon consumption, particularly through modern trade formats that emphasize food safety and convenience. The retail channels reflect established distribution networks, while emerging market penetration remains constrained by cold storage infrastructure and consumer education requirements. However, modern retail formats increasingly feature bacon in prepared food sections, expanding consumption occasions beyond traditional home cooking applications. The shift from traditional wet markets to supermarkets and hypermarkets enables bacon producers to reach consumers previously limited by cold chain constraints and product awareness. In a bid to capture a broader audience, brands are offering their products via supermarket chains such as Spinneys and Waitrose, among others, in key emerging nations like the United Arab Emirates. Further, convenience store expansion particularly benefits ready-to-eat bacon segments, as these formats prioritize grab-and-go products that align with urban lifestyle patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Related to High Fat Content Hinders Demand | -0.6% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Vegan and Plant-Based Diets Slows Demand | -0.4% | North America & Europe, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Growing Awareness of Animal Welfare And Ethics Restricts Growth | -0.3% | Europe and North America, selective urban markets globally | Long term (≥ 4 years) |

| Availability of Meat Alternatives Reduces Bacon Demand | -0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Related To High Fat Content Hinders Demand

In 2024, the Food Safety and Inspection Service (FSIS) heightened its regulatory scrutiny. This came on the heels of FSIS issuing public health warnings about bacon products surpassing sodium nitrite regulatory limits, underscoring ongoing health concerns that hinder market growth. The United Kingdom's mandatory nutritional labeling requirements influence consumer purchasing decisions, creating pressure for manufacturers to develop reformulated products that maintain taste while reducing health-negative attributes. Bacon's positioning as a flavor enhancer rather than primary protein source partially mitigates health concerns through portion control, yet sustained medical evidence linking processed meat consumption to cardiovascular disease creates persistent headwinds. According to the American Journal of Clinical Nutrition, consuming processed meat elevates the risk of mortality and significant cardiovascular events, in contrast to those who abstain from such meats. Companies respond through product innovation, developing lower-sodium and nitrite-free variants, though these alternatives often command premium pricing that limits mass market adoption.

Rising Adoption of Vegan and Plant-Based Diets Slows Demand

Plant-based alternatives experienced significant growth in 2024, as demonstrated by Cocuus's plans to 3D print 1,000 tons of plant-based bacon, showcasing technological advancements in alternative protein production. The company's manufacturing capabilities represent a substantial increase in production capacity for plant-based bacon alternatives. On the other hand, Oregon's food company, Thrilling Foods, has secured the United States patents for developing protein-streaked plant-based bacon that replicates the fatty-lean composition of traditional bacon, marking a breakthrough in texture and appearance replication. Venture capital and food-tech incubators are ramping up investments, fueling swift innovations and allowing startups to quickly cater to surging consumer demands for plant-based meat. Retailers and foodservice entities are expanding their plant-based offerings, as plant-based bacon increasingly graces mainstream grocery shelves and fast-casual restaurants, underscoring its market acceptance. These barriers remain significant factors affecting market penetration and widespread adoption of plant-based bacon products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standard Bacon Dominates Market while Ready-to-Eat Bacon Drives Innovation

Standard bacon maintains market leadership with 56.10% share in 2025, while ready-to-eat bacon commands the fastest growth trajectory at 6.49% CAGR through 2031. This dynamic reflects fundamental shifts in consumer behavior toward convenience-oriented food solutions, where time constraints increasingly outweigh traditional preparation preferences. Standard bacon's dominant position stems from its versatility across cooking applications and established consumer familiarity, yet ready-to-eat variants capture premium pricing through value-added processing and packaging innovations. Retail stores are allocating more shelf space to ready-to-eat products that feature resealable packaging, microwave-ready options, and controlled portions to improve consumer convenience.

The convenience segment benefits from foodservice adoption, where precooked bacon reduces kitchen labor costs and preparation time while maintaining consistent quality standards. Ready-to-eat products enable manufacturers to capture higher margins while addressing operational efficiency demands from restaurant chains and institutional buyers. Manufacturers and quick-service restaurant (QSR) chains have formed strategic partnerships to develop customized bacon products that meet specific menu requirements. The segment's growth trajectory suggests sustained consumer willingness to pay premiums for convenience, creating opportunities for continued product innovation and market expansion.

By Meat Type: Pork Retains Market Leadership While Beef Alternatives Gain Traction

Pork holds a dominant 92.45% market share in 2025, reflecting bacon's traditional pork-based production and established supply chain networks. Beef bacon demonstrates the highest growth potential with a 5.32% CAGR through 2031, supported by dietary diversification and religious requirements in various markets. This growth indicates consumer acceptance of bacon alternatives that deliver similar taste experiences while meeting specific dietary needs. Turkey and chicken bacon occupy niche segments, primarily targeting health-conscious consumers seeking reduced-fat options. Rising awareness of clean-label and ethically sourced meats is also prompting consumers to explore alternative bacon formats.

Beef bacon's growth stems from its premium market position and distinct flavor profile, attracting consumers interested in alternative protein options. In Muslim-majority countries, religious dietary guidelines create consistent demand for non-pork alternatives, strengthening beef bacon's market presence. While established processing infrastructure and cost advantages support pork bacon's market position, beef bacon's growth indicates sufficient market demand to support dedicated production facilities. Foodservice operators such as The Cheese Cake Factory in Middle Eastern countries are increasingly integrating beef bacon into diverse menu offerings, enhancing its visibility and mainstream acceptance.

By Cut Type: Sliced Bacon Dominates Sales as Pre-Cooked Options Drive Product Innovation

Sliced bacon holds the largest market share at 41.62% in 2025, while pre-cooked bacon is projected to grow at a 6.29% CAGR through 2031. Due to its widespread use in both retail and foodservice sectors and versatility in cooking applications, from breakfast dishes to sandwiches and salads, sliced bacon maintains its dominant position in the market. On the other hand, the demand for pre-cooked bacon is driven by increasing consumer preference for convenient meal solutions, along with addressing the foodservice's two major trends, i.e., time scarcity and kitchen labor rationalization. This growth reflects the broader shift toward ready-to-eat products that save preparation time while maintaining quality, particularly among urban consumers with busy lifestyles.

Bacon bits and crumbled bacon primarily serve the food manufacturing and restaurant segments, offering consistent portion control and easy integration into various recipes. Bacon rashers target premium market segments, appealing to consumers who value traditional preparation methods and presentation. Pre-cooked bacon's higher price positioning allows manufacturers to achieve better profit margins while meeting consumer demands for time-saving options. The segment's expansion demonstrates successful product development that preserves bacon's core qualities while offering improved convenience, supported by advances in packaging technology and preservation methods.

By Distribution Channel: Retail Holds Market Share While Foodservice Momentum Accelerates

Retail channels hold 61.78% market share in 2025, while the foodservice channels are projected to grow at a higher rate of 6.11% CAGR through 2031. The retail market is driven by established consumer purchasing habits and extensive supermarket networks in developed markets, while the foodservice channel is supported by quick-service restaurant expansion and increased bacon usage across menu categories. This growth reflects bacon's transition from a breakfast staple to a versatile ingredient used throughout the day. The foodservice segment benefits from precooked bacon products that improve operational efficiency and ensure consistent quality. In fact, companies such as Hormel, Smithfield, and Clemens offer varied bacon products in flexible pack sizes and formats to meet the diverse needs of foodservice operators.

Supermarkets and hypermarkets remain the primary retail distribution channels due to their robust cold chain infrastructure and established consumer shopping patterns. Online retail continues to gain market share by catering to convenience-focused consumers. Convenience stores show growth through ready-to-eat bacon products, particularly in urban areas where time-conscious consumers seek quick purchasing options. Private-label bacon brands are also expanding in retail, offering competitive pricing and attracting price-sensitive shoppers. In-store promotions, bundle deals, and product sampling are playing an increasing role in influencing consumer choices, particularly in large-format retail settings.

Geography Analysis

North America holds a dominant 38.10% market share in 2025, supported by established bacon consumption patterns and a comprehensive foodservice infrastructure that makes bacon a consistent menu item across restaurants. The region leverages well-developed supply chains, modern processing technologies, and strong consumer acceptance that enables both mass-market and premium product sales. Further, in 2024, the United States exported a record 3.03 million metric tons (mt) of pork and pork variety meat, valued at USD 8.63 billion . The mature market environment limits volume growth, pushing companies to focus on product innovation and premium segment development.

Asia-Pacific demonstrates the highest growth rate at 6.18% CAGR through 2031, reflecting the effects of urbanization and increasing Western food adoption on traditional protein consumption. According to the United States Department of Agriculture, China's pork import is expected to remain stable, mainly due to flat domestic consumption and ample production. Further, the Japanese food processing sector shows increasing demand for pre-prepared foods, driven by an aging population and convenience preferences. In Southeast Asia, as disposable incomes rise and modern retail channels expand, the demand for value-added meat products, such as flavored and precooked bacon, is surging.

European markets experience growth limitations despite traditional bacon consumption and advanced food processing capabilities, due to increased input costs, environmental regulations, and animal health concerns. Regulatory requirements increase operational expenses while environmental compliance necessitates production system changes that affect operational efficiency.

The Middle East and Africa present growth potential through economic development and urbanization, with product development and marketing addressing specific cultural and religious requirements. South America, with Brazil at the forefront, is expanding its pork production and export capabilities through cost-effective operations, enhanced processing facilities, and rising global demand for pork products.

Regulatory Landscape

Regulatory landscape for bacon as a cured, processed meat centers on additive limits, product standards, and labeling compliance. In the United States, USDA-FSIS requirements anchor how nitrites are used and how claims are substantiated, with references to 9 CFR 319.107 and 9 CFR 424.22 guiding cured meat standards and process controls.

Cross-border trade highlights divergences, notably the European Union's tighter maximum residual nitrite levels that apply from October 9, 2025 under the EU food additive framework, which increases reformulation and verification needs for exporters. In the United States, the January 1, 2026 uniform compliance date for the FSIS final rule on voluntary U.S.-origin claims creates an additional checkpoint for processors labeling origin on bacon sold domestically and across channels.

Value Chain Analysis

The bacon value chain runs from hog farming and feed inputs (corn and soybean meal) through slaughter, belly procurement, curing (salt, nitrite/nitrate systems, sugar, seasonings), smoking/thermal processing, slicing, packaging, and refrigerated distribution to retail and foodservice. The chain depends heavily on cold-chain integrity and packaging performance (vacuum and modified-atmosphere formats) to protect shelf life and food safety during distribution. USDA-FSIS standards such as 9 CFR 319.107 and 9 CFR 424.22 ground the chain in defined curing parameters and product specs, shaping supplier requirements and line controls.

Two structural pressure points drive operational decisions: input-cost volatility and compliance-driven process control. Feed and energy costs influence hog supply economics and processing costs, while cured-meat additive limits and labeling rules (notably nitrite controls and claim substantiation) increase testing, documentation, and line discipline for massaged/pumped and dry-cured bacon. Processors invest in automation and inspection to protect margins and consistency, while distributors and retailers prioritize suppliers that can provide reliable refrigerated logistics, consistent specifications, and formats that reduce labor in foodservice (pre-cooked and portion-controlled packs).

Competitive Landscape

The bacon market exhibits moderate fragmentation, indicating substantial competitive intensity among established players while creating entry opportunities for specialized producers and regional competitors. Market leaders leverage vertical integration strategies to control supply chains from hog production through processing and distribution, enabling cost optimization and quality consistency that smaller players struggle to match. Established players, bolstered by brand equity, enduring retail partnerships, and robust consumer loyalty, fortify their market position, erecting barriers for newcomers.

Technology adoption accelerates competitive differentiation, with companies investing in automated packaging systems and processing innovations that enhance food safety while reducing labor costs. Manufacturers are now harnessing advanced data analytics and AI-driven demand forecasting in their production planning, aiming to cut waste and boost operational efficiency. The competitive landscape increasingly favors companies capable of navigating regulatory compliance requirements, particularly regarding sodium nitrite levels and food safety standards that require specialized expertise and capital investments.

Operational agility is demonstrated through the vertical integration of supply chains and investment in advanced processing facilities. Strategic moves include expanding distribution networks through e-commerce platforms and third-party partnerships while strengthening direct-to-consumer models. Geographic expansion remains a key focus, with companies targeting emerging markets in Asia and establishing production facilities in strategic locations to optimize their supply chain networks. The industry is witnessing significant investment in research and development to develop new processing technologies and innovative product formulations.

Bacon Industry Leaders

-

Hormel Foods Corporation

-

Tyson Foods Inc.

-

The Kraft Heinz Company

-

WH Group Limited

-

Fresh Mark Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Convenience-led formats continue to open up whitespace across both retail and foodservice, particularly where operators prioritize labor reduction and standardized output. In the United States, Kraft Heinz opened Maple Bourbon Bacon in April 2026 as its first bacon innovation in five years, indicating premiumization and broader usage occasions beyond breakfast.

Process technology adoption is also visible as producers target yield improvements and formulation flexibility amid tighter additive scrutiny. In 2026, equipment makers highlighted automated line concepts from Provisur Technologies and brine injection solutions such as GEA MultiJector 500 to support higher-throughput ready-to-eat formats, tighter nitrite control, and more consistent labeling compliance.

Recent Industry Developments

- April 2026: The Kraft Heinz Company, under its Oscar Mayer brand, launched Maple Bourbon Bacon in partnership with Evan Williams Bourbon, positioned as the brand's first bacon innovation in five years. The release reinforces flavor-led premiumization and co-branding as a way to expand usage occasions beyond breakfast and create higher-margin, limited-time demand spikes.

- October 2025: Hormel Foods introduced a limited-edition collaboration between HORMEL BLACK LABEL bacon and Frank's RedHot, extending bacon into a heat-forward flavor platform tied to branded condiments. The move supports faster innovation cycles in a mature category and strengthens merchandising options for retail and promotional activation.

- January 2024: Tyson Foods opened a USD 355 million, 400,000-square-foot production facility in Bowling Green, Kentucky, with capacity of over two million pounds of bacon per week for Jimmy Dean and Wright Brand. The added scale enhances supply reliability for high-volume channels and supports broader distribution of branded bacon and bacon-adjacent offerings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the bacon market is defined as the value of packaged bacon products that are cured (and often smoked), made mainly from pork belly cuts, and sold through retail and foodservice channels for end consumption.

Scope exclusions: We exclude fresh, unprocessed pork belly, ham, non-pork bacon analogs, plant-based substitutes, and standalone bacon flavorings.

Segmentation Overview

-

By Product Type

- Standard Bacon

- Ready-to-Eat Bacon

-

By Meat Type

- Pork

- Beef

- Other Meat Types

-

By Cut Type

- Sliced Bacon

- Bacon Bits/Crumbled Bacon

- Bacon Rashers/Whole Slabs

- Pre-Cooked Bacon

-

By Distribution Channel

-

Retail

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty and Butcher Shops

- Online Retail Stores

- Other Distribution Channels

- Foodservice

-

Retail

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear fact base for pork supply, processed meat output, and consumption patterns that can explain bacon demand by region. We typically use public sources such as FAOSTAT for livestock and meat balance sheets, USDA market and cold storage updates, Eurostat production and trade series, UN Comtrade for cross-border product flows, and Codex or similar food labeling references for what can be sold as bacon.

Once the public data is organized, we cross-check it with company annual reports, investor presentations, association websites, and reputable press coverage to track pricing shifts and capacity changes that could affect bacon value. A few paid subscriptions are used only for structured company financials, patent search, and shipment or trade visibility, where they help validate volumes and value assumptions. The sources listed above are illustrative and not exhaustive, and many other references are also used to collect data, validate findings, and clarify open questions.

Primary Interviews and Surveys

Fieldwork is used to confirm what is counted as bacon in day-to-day trade, how pricing is set across retail and foodservice, and how mix shifts (standard vs ready-to-eat, sliced vs bits) affect value. We speak with processors, distributors, retailers, foodservice participants, and industry experts across major consuming regions so desk assumptions can be corrected and final totals can be stress-tested.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 41% | EMEA: 34% |

| Smaller Players: 14% | Managers: 47% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up sequence where processed pork output, relevant trade lines, and consumption indicators are used to reconstruct the addressable bacon demand pool by region, and then value is formed using price benchmarks. To keep the totals realistic, results are corroborated with selective bottom-up approximations such as sampled retail shelf prices, foodservice menu pricing signals, and roll-ups from a limited set of suppliers and channels where coverage is clear.

Key model inputs include pork belly availability and conversion yields into bacon, curing and smoking penetration in processed pork, retail versus foodservice split, average pack sizes and typical price per kilogram, and import dependence in markets that under-produce pork. For forecasting, scenario analysis is applied and guided by expert views on variables like feed cost direction, processed meat capacity additions, and expected premiumization for ready-to-eat formats. When a bottom-up check is incomplete for smaller countries, we handle the gap using proxy ratios from similar markets, then revalidate with trade and price reality checks.

Data Validation & Update Cycle

Outputs are checked from more than one angle, including internal consistency tests across volume, price, and channel mix, and also external sense checks against independent signals like pork production trends and trade movements. Any outliers are reviewed in detail, and if a shift cannot be explained with available evidence, we trigger follow-up calls to recheck assumptions.

Before sign-off, a separate analyst review is completed so major inputs, calculations, and conversions are rechecked for errors and timing mismatches. Reports are refreshed annually, and interim updates are done when material events occur that can move pricing, supply, or channel demand. Right before delivery, a final review pass is made so clients receive the most current view possible.

Mordor Intelligence's Bacon Market Estimate Compared With Other Published Estimates

Published bacon market estimates often vary because different studies do not always count the same products, selling channels, or pricing levels, and they also anchor their base year and currency assumptions differently. Those choices can move the total even when the direction of growth looks similar.

Some external totals blend fresh pork cuts or adjacent processed meats into their definition, and they may also use broad retail averages that do not separate ready-to-eat premiums from standard sliced packs. Packaged, cured (and often smoked) bacon sold through retail and foodservice is what Mordor Intelligence counts, with fresh pork belly and ham kept out so the number stays tied to actual bacon purchase behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 88.72 B (2026) | |

| Industry Research Publisher A | USD 71.97 B (2024) | Anchors the series in an earlier base year and leans more on retail revenue capture, which can understate value where foodservice demand and ready-to-eat mix lift realized prices. |

| Industry Research Publisher B | USD 63.92 B (2024) | Uses a broad product description and conservative price progression, which can compress the value estimate when cured and smoked bacon is not cleanly separated from nearby pork categories. |

Across the three figures, most of the spread comes from base-year timing and how tightly each estimate separates cured bacon from adjacent pork items that can inflate or dilute totals. The model stays repeatable by linking demand to observable supply, trade, and channel pricing inputs, and then validating key mix assumptions through expert rechecks before totals are finalized.

Key Questions Answered in the Report

What is the current value of the bacon market?

The bacon market size is USD 88.72 billion in 2026 and is forecast to reach USD 109.72 billion by 2031 at a 4.34% CAGR.

Which region is growing fastest in bacon consumption?

Asia-Pacific is projected to register the highest regional CAGR of 6.18% between 2026 and 2031, fueled by urbanization and Western cuisine adoption.

What product segment is expanding most quickly?

Ready-to-eat bacon leads growth with a 6.49% CAGR, supported by consumer demand for convenience and foodservice efficiency gains.

How significant is beef bacon in the market?

While pork retains 92.45% share, beef bacon is the fastest-growing alternative at 5.32% CAGR, driven by dietary and religious preferences in select markets.

Page last updated on: