Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

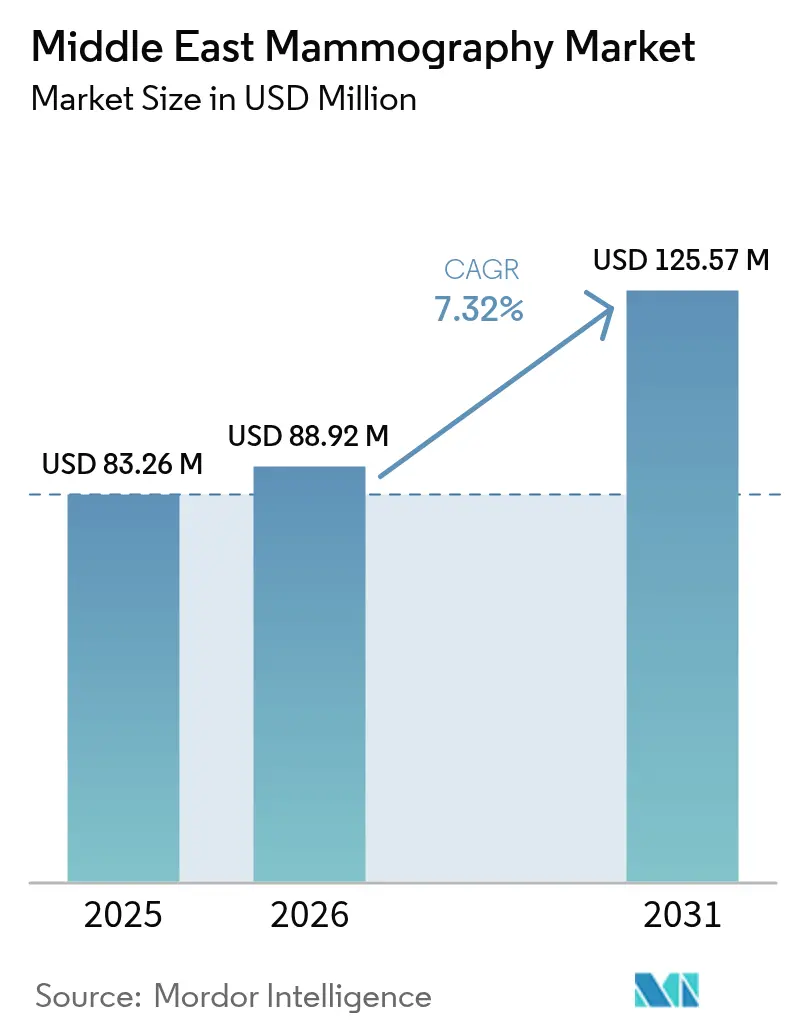

| Base Year Market Size (2025) | USD 83.26 Million |

| Market Size (2026) | USD 88.92 Million |

| Market Size (2031) | USD 125.57 Million |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Mammography Market Analysis by Mordor Intelligence

The Middle East Mammography Market size was valued at USD 83.26 million in 2025 and is estimated to grow from USD 88.92 million in 2026 to reach USD 125.57 million by 2031, at a CAGR of 7.32% during the forecast period (2026-2031).

A younger median age at breast cancer diagnosis, widening government screening mandates, and the fast diffusion of AI-enabled digital breast tomosynthesis are converging to keep demand resilient despite capital budget caution in parts of Egypt and Turkey. Three trends dominate: (1) multi-year equipment-refresh cycles at tertiary hospitals in Saudi Arabia and the United Arab Emirates that favor premium 3-D platforms with open APIs, (2) expanding public tenders for full-field digital mammography systems that balance cost and throughput, and (3) private-sector investments in CAD and AI workstations that promise shorter read times and lower recall rates. Competitive pressure is rising as Chinese entrants are undercutting list prices by 30-40%, forcing incumbents to defend their share through multi-year service contracts and bundled software subscriptions.

Key Report Takeaways

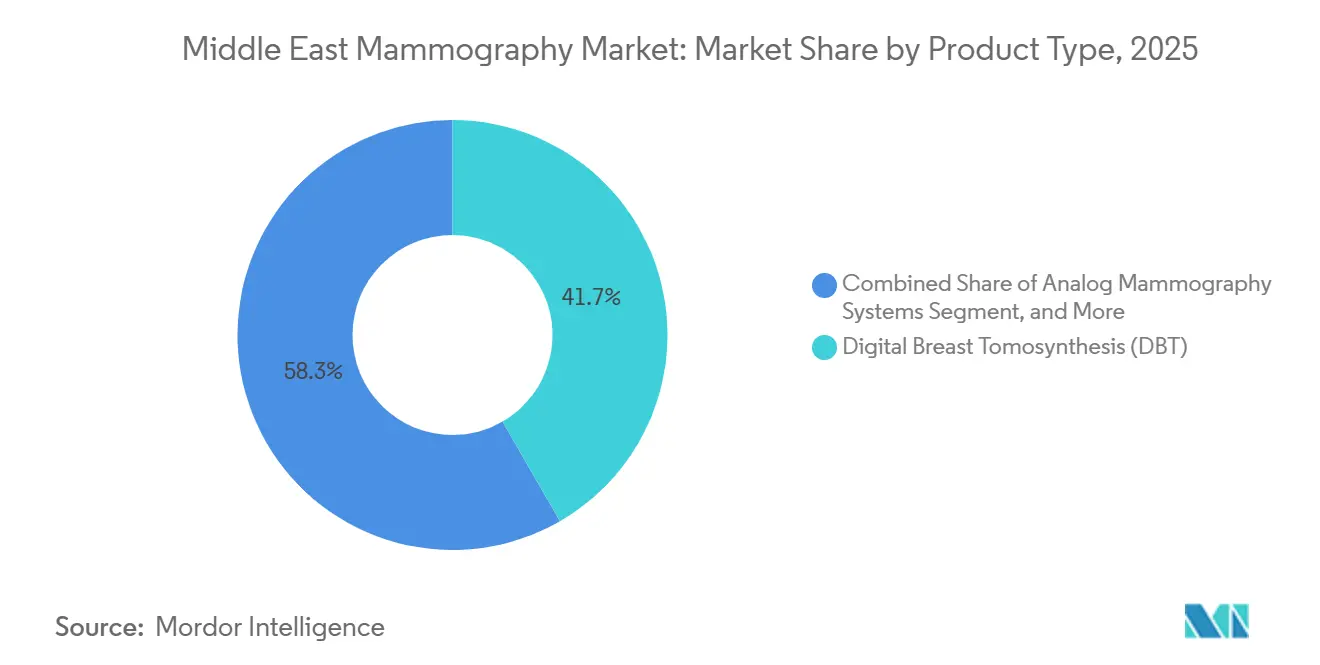

- By product type, digital breast tomosynthesis led with 41.67% of Middle East mammography market share in 2025, while full-field digital mammography is set to post the fastest 8.06% CAGR through 2031.

- By technology, 3-D digital tomosynthesis accounted for 46.21% of revenue in 2025, whereas CAD- and AI-assisted mammography is projected to expand at a 9.63% CAGR through 2031.

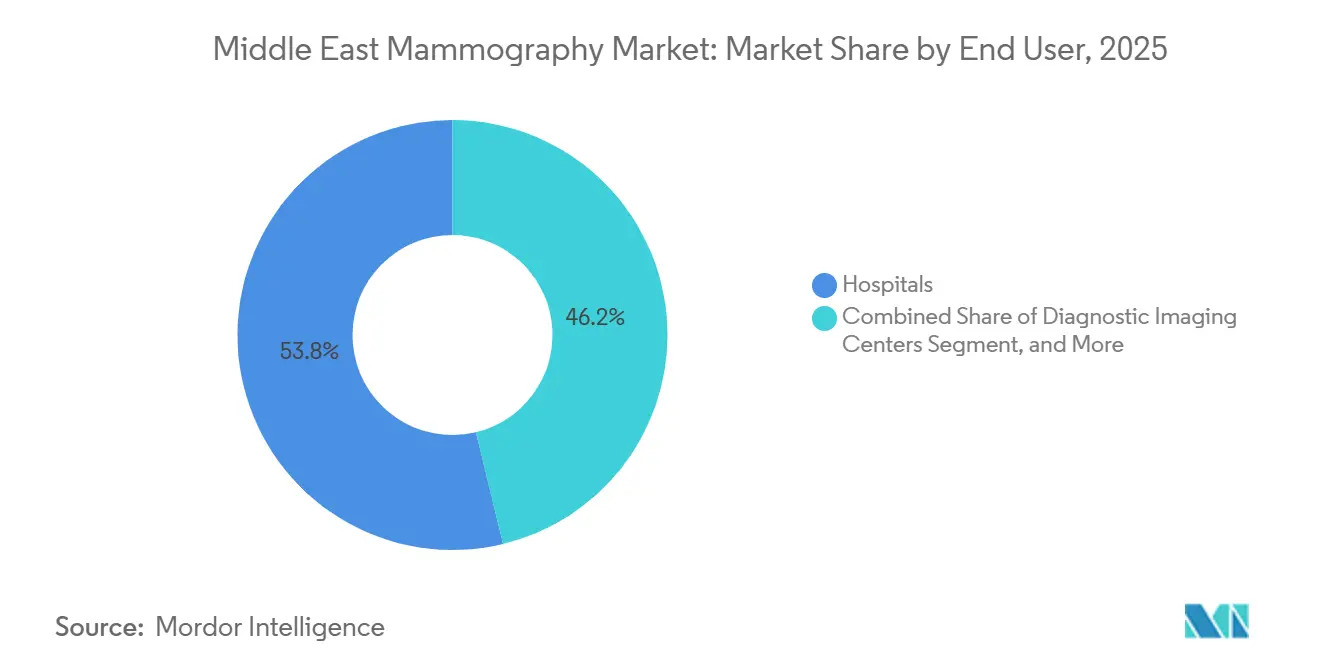

- By end user, hospitals captured 53.78% of 2025 revenue; breast care clinics are advancing at an 8.76% CAGR through 2031.

- By geography, Saudi Arabia accounted for 29.03% of 2025 revenue, while the United Arab Emirates is forecast to record the highest CAGR of 9.41% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of breast cancer across Middle East | +1.8% | GCC core, Egypt, Turkey | Long term (≥ 4 years) |

| Expansion of government-funded screening programs | +1.5% | Saudi Arabia, UAE, Qatar, Kuwait, Bahrain | Medium term (2-4 years) |

| Rapid adoption of digital breast tomosynthesis systems | +1.3% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Growing medical tourism for oncology diagnostics | +0.9% | UAE, Saudi Arabia, Turkey | Short term (≤ 2 years) |

| Surge in private-sector AI-enabled reading centers | +0.7% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| GCC-wide AI teleradiology reimbursement pilots | +0.5% | GCC countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Breast Cancer Across Middle East

Breast cancer is now the top malignancy among women in the region, and median diagnosis ages of 48-51 compress the screening window, driving urgent demand for higher-sensitivity imaging platforms.[1]Cross-Sectional Study Team, “Breast Cancer Screening Barriers and Facilitators Among Women in Kuwait,” BMC Women’s Health, biomedcentral.com Case numbers in Egypt climbed 12% between 2024-2025, prompting a USD 1.8 billion boost in oncology capacity and accelerating equipment procurement. Governments now mandate biennial screening from age 40, favoring digital breast tomosynthesis systems that detect small, dense-tissue lesions that are invisible on legacy analog units. The epidemiological shift anchors long-term demand for the Middle East mammography market.

Expansion of Government-Funded Screening Programs

Saudi Arabia aims to achieve 70% screening coverage by 2030 and has deployed mobile units across remote provinces to reach women who previously lacked access. The UAE integrated AI-equipped portable systems into school health checks, reducing diagnostic wait times to a single day and demonstrating cost-effective opportunistic screening.[2]Emirates Health Services, “AI-Powered Mobile Mammography for Teachers,” Zawya, zawya.com Qatar’s partnership with Lunit demonstrates how integrating AI at the primary-care level improves sensitivity and throughput. Together, these programs expand the Middle East mammography market footprint and sustain vendor pipelines.

Rapid Adoption of Digital Breast Tomosynthesis Systems

Digital breast tomosynthesis accounted for 41.67% of 2025 product revenue, as facilities favored 3-D imaging that lowers recall rates in dense-breast cohorts. Hologic’s 3Dimensions with Genius AI, installed first in the UAE in 2025, claims up to 65% higher invasive-cancer detection, setting a new benchmark for premium platforms. Siemens and Fujifilm similarly stress workflow automation and dose optimization, attributes prized by administrators confronting technician shortages. High capital outlays persist, yet the upside of pay-per-scan leasing and medical tourism motivate adoption across the Middle East mammography market.

Growing Medical Tourism for Oncology Diagnostics

Dubai and Abu Dhabi attracted more than 600,000 medical tourists in 2024, with oncology evaluation gaining share as hospitals advertise AI-assisted same-day reporting. Saudi Arabia’s Vision 2030 seeks 1 million medical tourists annually, catalyzing joint ventures that bundle mammography with genetic testing and MRI follow-up. Turkey leverages competitive pricing and geographic proximity to Central Asia, further widening regional referral flows. Cross-border demand obliges hospitals to hold state-of-the-art equipment, reinforcing hardware refresh cycles in the Middle East mammography market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced mammography equipment | -1.2% | Egypt, Turkey, Oman, Bahrain | Medium term (2-4 years) |

| Shortage of trained radiologists and technicians | -0.9% | Saudi Arabia, UAE, Kuwait | Long term (≥ 4 years) |

| Cultural barriers reducing screening uptake | -0.7% | Kuwait, Saudi Arabia, rural areas | Long term (≥ 4 years) |

| Supply-chain risks for flat-panel detectors | -0.4% | Global, acute in Egypt and Turkey | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Mammography Equipment

Premium 3-D systems carry price tags of USD 215,000-275,000 and annual service fees of up to USD 45,000, costs that many public hospitals cannot meet. Egypt’s 25% health-budget rise prioritizes brick-and-mortar expansion over equipment upgrades, sustaining two-dimensional demand at USD 55,000-75,000 per unit. Even in Gulf states, shifting resources to software subscriptions and teleradiology narrows the headroom for hardware capex, moderating the Middle East mammography market's acceleration.

Shortage of Trained Radiologists & Technicians

WHO projects a regional health-worker gap of 2.1 million by 2030, with breast radiology among the scarcest specialties.[3]WHO EMRO, “Regional Initiative to Strengthen Health Workforce,” emro.who.int Saudi Arabia houses fewer than 300 dedicated breast radiologists, insufficient for its screening targets. Reliance on expatriate staff increases turnover and lowers utilization rates, restraining growth in the Middle East mammography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tomosynthesis Leads, FFDM Accelerators

Digital breast tomosynthesis generated 41.67% of 2025 sales as tertiary hospitals upgraded to 3-D imaging to cut recall rates and attract medical tourists. Full-field digital mammography is forecast to log the fastest 8.06% CAGR through 2031, driven by public tenders in Egypt, Turkey, and emerging GCC markets seeking lower capex and proven throughput. Analog systems persist in rural clinics but are declining steadily as digital archiving and picture-archiving mandates spread. The Middle East mammography market size for full-field digital mammography is expected to climb alongside Egypt’s 58-hospital build-out, underscoring a budget-balanced adoption curve.

By Technology: AI Platforms Outpace Legacy Modalities

Three-dimensional tomosynthesis retained 46.21% of 2025 technology revenue, but CAD and AI-assisted mammography will record the highest 9.63% CAGR to 2031 as private networks monetize faster diagnostics. Hospitals continue to rely on two-dimensional digital units for mass screening; however, once AI reimbursement codes emerge, systems with vendor-neutral integration will command premium valuations across the Middle East mammography market. The Middle East mammography industry is thus pivoting toward software-centric value pools, even as hardware refreshes continue in parallel.

By End User: Breast Care Clinics Gain Share

Hospitals accounted for 53.78% of 2025 revenue, yet breast care clinics will expand at an 8.76% CAGR as patients gravitate toward specialized environments offering genetic counseling, MRI, and same-day biopsy. Diagnostic imaging centers and mobile units fill access gaps, particularly for self-pay expatriates and rural segments—but they battle thin margins and supply-chain risks. The Middle East mammography market for breast care clinics is set to grow fastest, capitalizing on private equity funding and AI-enhanced patient experiences.

Geography Analysis

Saudi Arabia generated 29.03% of 2025 revenue, anchored by a population of 36 million and a government program aiming for 70% screening coverage by 2030. The Middle East mammography market share concentrated in the Kingdom benefits from tenders that stipulate domestic service hubs within 48 hours, favoring multinationals with regional logistics.

The United Arab Emirates is forecast to post a 9.41% CAGR through 2031, underpinned by AI-enabled workflows that cut turnaround time from 19 days to 1 day and by medical tourism inflows seeking same-day breast imaging.

Qatar, Kuwait, Oman, and Bahrain together form a smaller yet strategically significant cluster. Qatar’s AI pilots aim for 30% faster reads; Kuwait grapples with low uptake, while Bahrain upgrades legacy units to boost the Middle East mammography market's size for dense-breast detection accuracy. Egypt’s 25% budget jump and Turkey’s medical-tourism windfall round out a region where political commitment, foreign-exchange volatility, and tourism pipelines shape procurement cycles.

Competitive Landscape

The Middle East mammography market hosts multinationals Hologic, GE HealthCare, Siemens Healthineers, Fujifilm, and Philips, defending their installed bases through long-term service contracts and AI subscriptions, while lower-priced Chinese systems erode hardware margins. Blackstone and TPG’s USD 18.3 billion buy-out of Hologic in 2025 indicates rising private-equity confidence in AI-fortified breast imaging. Siemens’ MoU with Egypt’s Ministry of Health bundles hardware, training, and teleradiology in a pay-for-outcome model, reflecting a shift from transactional sales to lifecycle partnerships. Chinese entrants leverage 30-40% list-price discounts but struggle with ISO 13485 and data-localization compliance, barriers that Abu Dhabi’s 2024 standard has now codified. AI-native firms such as Lunit pursue software-as-a-service, bypassing hardware entirely and capturing value from algorithm licensing across the Middle East mammography market.

Middle East Mammography Industry Leaders

Hologic Inc.

Fujifilm Holdings Corporation

Planmed Oy

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hologic Inc. announced a multi-year framework agreement with Saudi Arabia's Ministry of Health to supply 3D Mammography systems with AI-powered Intelligent 2D imaging technology across 30 new primary-care centers under Vision 2030, valued at approximately USD 45 Million. The contract includes technologist training, teleradiology infrastructure, and a ten-year service commitment, positioning Hologic to capture incremental replacement cycles as analog units are decommissioned in secondary cities.

- January 2025: Lunit signed a five-year contract with Abu Dhabi Health Services Company (SEHA) to deploy Lunit INSIGHT MMG across 14 hospitals and 70 clinics, covering more than 3,000 beds.

Middle East Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer.

The Middle East Mammography Market Report is Segmented by Product Type (Analog Mammography Systems, Full-Field Digital Mammography, Digital Breast Tomosynthesis), Technology (2-D Digital Mammography, 3-D Digital Tomosynthesis, CAD & AI-Assisted Mammography), End User (Hospitals, Diagnostic Imaging Centers, Breast Care Clinics, Mobile Screening Units), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Turkey, Israel, Egypt, Rest of Middle East). Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Analog Mammography Systems |

| Full-Field Digital Mammography (FFDM) |

| Digital Breast Tomosynthesis (DBT) |

By Technology

| 2-D Digital Mammography |

| 3-D Digital Tomosynthesis |

| CAD & AI-Assisted Mammography |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Breast Care Clinics |

| Mobile Screening Units |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Turkey |

| Israel |

| Egypt |

| Rest of Middle East |

| By Product Type | Analog Mammography Systems |

| Full-Field Digital Mammography (FFDM) | |

| Digital Breast Tomosynthesis (DBT) | |

| By Technology | 2-D Digital Mammography |

| 3-D Digital Tomosynthesis | |

| CAD & AI-Assisted Mammography | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Breast Care Clinics | |

| Mobile Screening Units | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Turkey | |

| Israel | |

| Egypt | |

| Rest of Middle East |

Key Questions Answered in the Report

How large will screening demand be for digital breast tomosynthesis in Gulf hospitals by 2031?

Purchases of premium 3-D systems in Saudi Arabia and the UAE will keep annual sales growing at 7.32% overall, with tomosynthesis still holding the largest Middle East mammography market share by 2031.

Will AI-assisted mammography become reimbursable before 2031?

Regulatory pilots in Abu Dhabi and Saudi Arabia indicate fee codes could arrive around 2028, likely making AI capability a purchase prerequisite for new systems.

Which country is expected to grow fastest in breast-imaging capex?

The United Arab Emirates shows the highest forecast CAGR at 9.41%, driven by medical-tourism positioning and AI-enabled workflow investments.

Do mobile screening units offer a sustainable business model?

Mobile fleets fill rural gaps, yet diesel costs, staff turnover, and USD 400,000-600,000 vehicle prices limit profitability unless volumes are underwritten by government programs or corporate wellness contracts.

How severe is the radiologist shortage for breast imaging?

GCC nations employ fewer than 300 breast-focused radiologists in total; AI-assisted teleradiology is therefore key to scaling coverage without proportional workforce growth.

Page last updated on: