Size and Share of Semiconductor Device Market in Aerospace and Defense Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

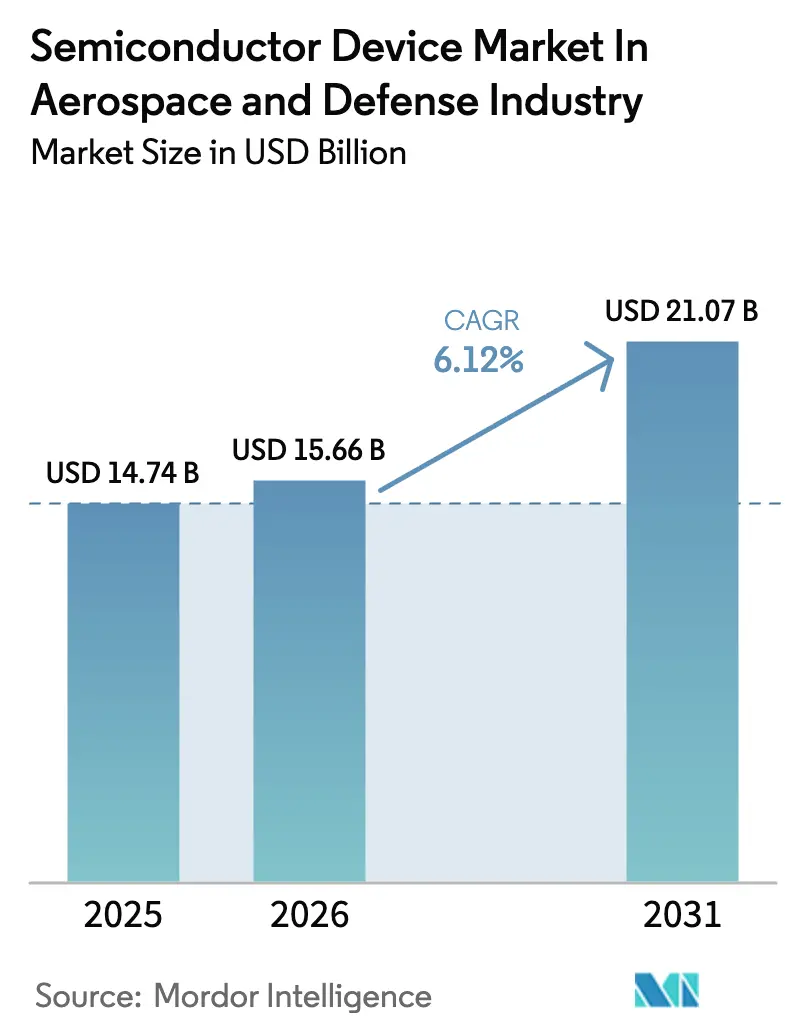

| Market Size (2026) | USD 15.66 Billion |

| Market Size (2031) | USD 21.07 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

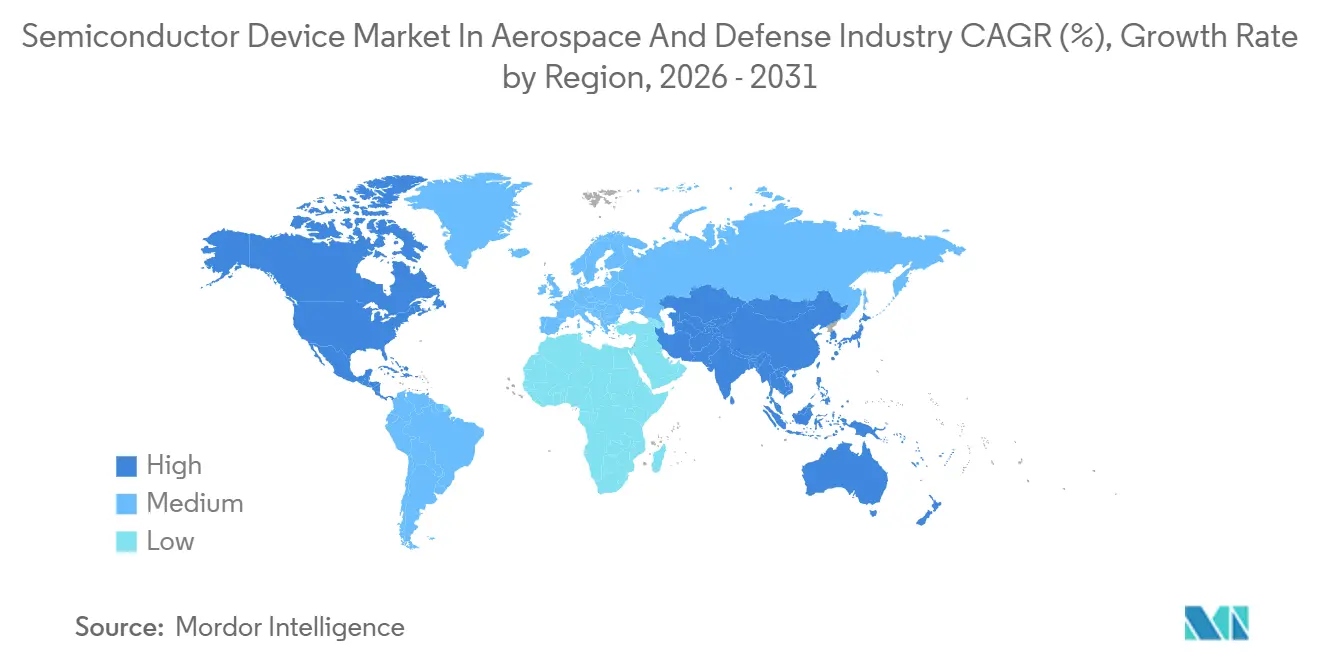

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Semiconductor Device Market in Aerospace and Defense Industry by Mordor Intelligence

The Semiconductor Device Market in the Aerospace and Defense Industry market size is expected to increase from USD 14.74 billion in 2025 to USD 15.66 billion in 2026 and reach USD 21.07 billion by 2031, growing at a CAGR of 6.12% over 2026-2031. Behind the steady trajectory lies a decisive shift toward wide-bandgap materials, large-scale appetites for radiation-tolerant chips in Low-Earth-Orbit (LEO) constellations, and open-architecture mandates that favor commercial off-the-shelf integrated circuits over bespoke ASICs. Military aviation remains the costliest platform, yet unmanned aerial vehicles (UAVs) are rising fastest as ministries field attritable swarms. Gallium nitride (GaN) is displacing gallium arsenide in RF power amplifiers above 40 GHz, while silicon carbide (SiC) enables lighter, cooler converters vital for hypersonic glide vehicles and directed-energy weapons. Meanwhile, export-control headwinds below 7 nm prompt designers to recycle 28 nm and 65 nm processes, trading lithographic edge for assured supply.[1]DARPA, “Electronics Resurgence Initiative Program Overview,” darpa.mil

Key Report Takeaways

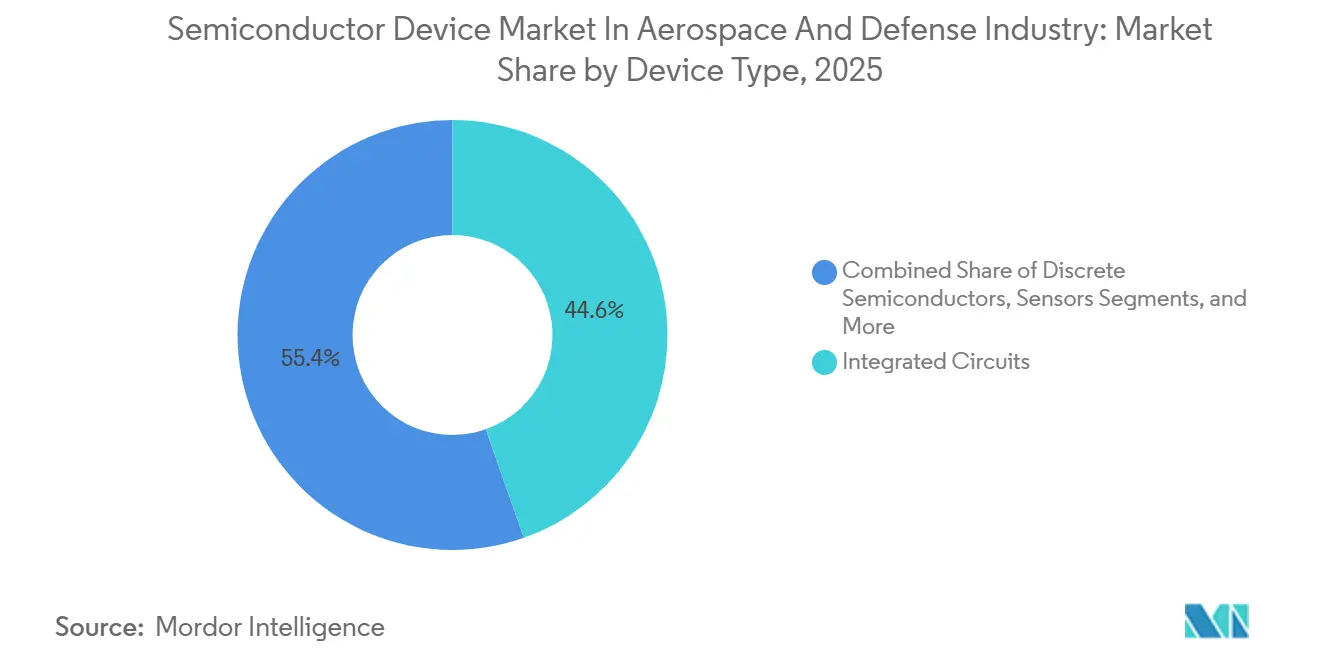

- By device type, integrated circuits led with 44.61% of the Semiconductor Device Market in the Aerospace and Defense Industry market share in 2025.

- By device type, optoelectronics are projected to expand at an 8.13% CAGR through 2031.

- By end-use platform, military aviation held 31.43% of the Semiconductor Device Market in the Aerospace and Defense Industry market size in 2025.

- By end-use platform, UAVs are forecast to register the highest growth at a 9.43% CAGR to 2031.

- By material, silicon commanded 62.13% of revenue in 2025, while GaN is projected to rise at a 7.36% CAGR through 2031.

- By geography, North America retained a 36.91% share in 2025, yet Asia-Pacific is expected to grow at an 8.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Semiconductor Device Market in Aerospace and Defense Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Wide-Bandgap (SiC and GaN) Adoption for Next-Gen Military and Space Power Systems | +1.2% | North America, Europe | Medium term (2-4 years) |

| LEO Satellite Mega-Constellations Driving Radiation-Tolerant RFIC Demand | +1.0% | North America rising in Asia-Pacific | Long term (≥ 4 years) |

| Embedded AI Mission Computers in Multi-Domain Operations | +0.9% | North America, Europe | Medium term (2-4 years) |

| Hypersonic and Directed-Energy Programs Requiring Ultra-High-Frequency GaN RF Power Amplifiers | +0.8% | North America, China, Russia | Short term (≤ 2 years) |

| Open-Architecture Avionics Refresh Cycles Expanding COTS IC Spend | +0.7% | North America, Europe | Medium term (2-4 years) |

| Indigenous Fighter and UAV Platforms in Indo-Pacific Boosting Local Sourcing | +0.6% | India, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Wide-Bandgap (SiC and GaN) Adoption for Next-Gen Military and Space Power Systems

SiC and GaN devices tolerate higher voltages, switch faster, and dissipate heat more efficiently than silicon, enabling lighter power supplies in missiles and satellites. Wolfspeed qualified 1,700 V SiC MOSFETs for the U.S. Air Force’s next-generation fighter, cutting converter mass by 30%. The European Space Agency selected GaN-on-silicon power ICs that reduced a 1 kW solar regulator’s mass by 40%. Northrop Grumman executed long-term wafer purchases to secure SiC supply for AESA radars, underscoring its strategic forward purchasing. Qorvo reported GaN amplifiers rising from 11% to 18% of defense revenue between 2023 and 2025, driven by hypersonic weapons. SiC’s three times higher thermal conductivity than silicon also reduces the size of heat sinks on weight-critical airborne payloads.

LEO Satellite Mega-Constellations Driving Radiation-Tolerant RFIC Demand

Mega-constellations demand radiation resilience at commercial price points. Starlink Gen2 satellites launched in 2025 carry more than 1 200 GaN RFICs each, multiplying total-ionizing-dose-hardened demand. Amazon’s Project Kuiper awarded Microchip Technology a contract for RTG4-based FPGAs that survive 300 krad while halving power use. OneWeb’s restart stretched wafer starts at Teledyne e2v by 35%, exposing sub-90 nm scarcity. The U.S. Space Force’s Tranche 2 satellites embed AI routing on Versal AI Core FPGAs, reinforcing acceptance of “good-enough” rad tolerance. Traditional vendors now license commercial foundries to stay price-competitive.

Embedded AI Mission Computers in Multi-Domain Operations

Edge AI has moved from demo to deployment. BAE Systems is installing AI computers in F-16 Block 70 jets, lowering pilot workload by 40% during suppression-of-enemy-air-defense tasks. Mercury Systems’ Ensemble 6000 delivers 256 TOPS INT8 using Jetson Orin modules in rugged form factors. Project Convergence cut artillery kill chains from 20 minutes to under 90 seconds via Versal AI Edge processors. L3Harris fielded Intel Xeon-based mission computers to P-8A aircraft with AVX-512 acceleration.[2]L3Harris Technologies, “SDA Tranche 2 Contract Release,” l3harris.com Certification remains a hurdle: deterministic flight controls must be isolated from probabilistic AI inference under DO-178C.

Hypersonic and Directed-Energy Programs Requiring Ultra-High-Frequency GaN RF Power Amplifiers

GaN-on-SiC delivers >100 W above 40 GHz and endures junction temperatures over 225 °C. The U.S. Army’s hypersonic weapon uses Qorvo’s 44 GHz GaN amplifiers with 150 W output and 50% efficiency. Lockheed Martin’s HELIOS laser relies on GaN RF drivers to energize a 60 kW beam. U.S. export controls now cover GaN-on-diamond substrates because diamond enables 200 W/mm power density. MACOM qualified a 94 GHz GaN MMIC for the Next-Generation Jammer, replacing traveling-wave tubes. Only three foundries supply 150 mm GaN-on-SiC wafers at scale, keeping capacity tight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Rad-Hard Foundry Capacity Below 90 nm | -0.9% | North America, Europe | Medium term (2-4 years) |

| Export-Control Tightening on Advanced Nodes | -0.7% | Asia-Pacific, Global | Long term (≥ 4 years) |

| High QML-V and JANS Qualification Cost Burden | -0.5% | North America, Europe | Medium term (2-4 years) |

| Thermal Management Limits in 3D-Packaged Space-Grade Chips | -0.4% | Global spacecraft programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Rad-Hard Foundry Capacity Below 90 nm

Only BAE Systems’ New Hampshire fab and Tower Semiconductor’s Newport Beach site run volume rad-hard processes under 90 nm, both above 95% utilization. Lead times for RTG4 FPGAs stretched to 52 weeks in 2025.[3]Microchip Technology, “MPFS500T QML-V Qualification,” microchip.com Qualifying a new rad-hard line costs up to USD 80 million and three years, discouraging entrants. Teledyne e2v even declined EUR 40 million orders as 65 nm slots were consumed by ESA missions. Designers therefore revert to 180 nm processes, accepting density and power trade-offs.

Export-Control Tightening on Advanced Nodes

In October 2024, the U.S. government added 140 Chinese firms to its Entity List, specifically targeting radiation-hardened ASICs and GaN RF components. This move aimed to restrict access to critical technologies that could potentially enhance adversarial capabilities. Following this development, Japan implemented similar restrictions, focusing on EUV tools to further tighten control over advanced semiconductor manufacturing equipment. Airbus encountered significant delays with Versal FPGAs intended for allied nations. To mitigate these disruptions, the company established inventory hubs in strategic locations, including Singapore and Dubai, to ensure smoother supply chain operations. Meanwhile, India responded to the loss of access to 28 nm nodes by redesigning the guidance computer for its Astra Mk2 missile to operate on 65 nm nodes, showcasing adaptability in the face of export restrictions. While these export regulations effectively slow down adversaries, they also encourage allied nations to enhance their self-reliance in critical technologies. Over time, this shift is expected to erode U.S. vendors' market share in the global landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Anchor Platform Complexity

Integrated circuits captured 44.61% of Semiconductor Device Market In Aerospace And Defense Industry market size in 2025, supplying processors, FPGAs, and mixed-signal front-ends for avionics and payloads. Optoelectronics, though smaller, will outpace others at 8.13% CAGR as LiDAR munitions and optical inter-satellite links spread. Raytheon’s StormBreaker employs indium-gallium-arsenide photodetectors for laser targeting. Discrete power devices and sensors cover the remainder, accelerated by hyperspectral imagers on next-gen drones.

Optoelectronics’ rise is structural. Optical links transmit gigabits per second and evade RF congestion. L3Harris achieved a 10 Gbps optical downlink in 2025 using lasers that survived 18 months on orbit. Discrete SiC MOSFETs stay vital for 1700 V switching in truck-mounted lasers. Hybrid packaging now micro-prints III-V lasers onto silicon CMOS, shrinking form factors at a 20-30% cost premium.

By Material: Silicon Dominance Erodes as Wide-Bandgap Gains

Silicon held 62.13% of Semiconductor Device Market In Aerospace And Defense Industry market share in 2025 thanks to supply depth and qualification heritage. GaN is projected to climb 7.36% annually as hypersonic, jammer, and phased-array programs exceed GaAs limits. The Air Force’s next-gen jammer emits 1 kW across 6-18 GHz exclusively via GaN modules. SiC serves power conversion where 98% efficiency at 150 °C justifies its 3-5× cost premium.

Indium phosphide dominates millimeter-wave above 60 GHz; diamond substrates, though costly, enable 200 W/mm GaN densities. Qorvo showed 150 W at 44 GHz on GaN-on-diamond, 50% higher than GaN-on-SiC, though wafers exceed USD 10 000 each. Converting a GaN fab to SiC substrates needs about USD 250 million in tools, limiting participation to the largest players.

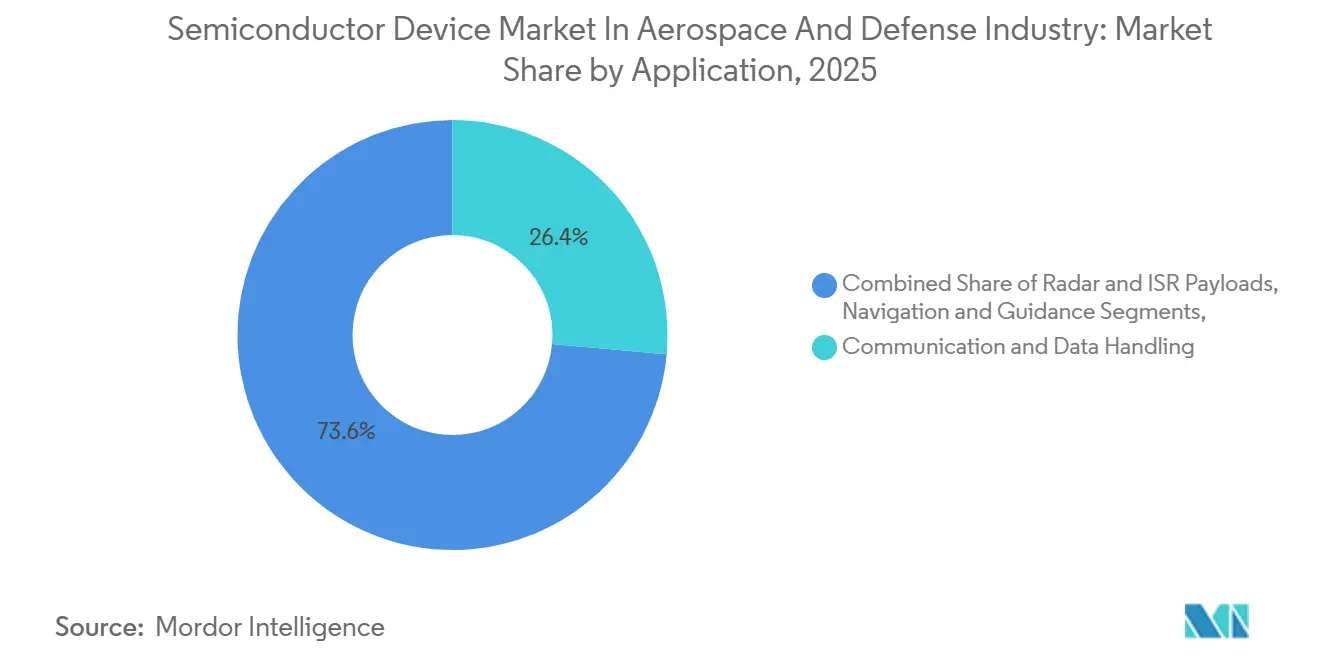

By Application: Communication Leads, Electronic Warfare Surges

Communication and data handling commanded 26.43% of Semiconductor Device Market In Aerospace And Defense Industry market size in 2025. Electronic warfare will log a 9.12% CAGR as cognitive jammers gain priority. The Navy’s low-band jammer pod processes 256 TOPS for adaptive waveforms. AESA radars elevate GaN demand; each F-35 radar packs 1 600 T/R modules.

Navigation integrates inertial, terrain, and celestial cues to resist GPS denial. Power management buses such as Maxar’s 1300-class adopt SiC converters, trimming 18 kg versus silicon units. Sensors broaden with quantum-dot infrared detectors slated for the Space Force’s Silent Barker constellation.

By End-Use Platform: Military Aviation Dominates, UAVs Accelerate

Military aviation held 31.43% of Semiconductor Device Market In Aerospace And Defense Industry market share in 2025, yet UAVs will rise fastest at 9.43% CAGR as Collaborative Combat Aircraft targets 1 000 autonomous wingmen. Spacecraft stay important via mega-constellations; a Starlink Gen2 unit embeds more than 1 200 GaN parts.

Commercial aviation gains chip content through fly-by-wire and cabin connectivity, while ground and naval systems embed AI to shrink crews. Missiles such as Lockheed’s AGM-183 rely on SiC devices that survive 225 °C boost-phase heating. The Replicator initiative’s thousands of drones require low-cost semiconductors that legacy aerospace suppliers struggle to scale.

Geography Analysis

North America retained 36.91% share in 2025, anchored by the USD 842 billion U.S. defense budget and DARPA’s USD 1.5 billion Electronics Resurgence Initiative for 3D packaging. The CHIPS Act directs USD 39 billion in subsidies; BAE Systems expanded its New Hampshire fab by 25% wafer capacity, the nation’s lone sub-90 nm rad-hard source. Canada’s NORAD upgrade earmarks USD 3.6 billion for Arctic surveillance satellites using MDA Space processors.

Asia-Pacific will post the highest CAGR at 8.47% through 2031. India’s USD 10 billion semiconductor mission drew Tower Semiconductor to propose a 65 nm trusted fab. Japan placed an USD 800 million order with Mitsubishi Electric for indigenous radiation-tolerant F-3 processors. South Korea partners Samsung Foundry to qualify 28 nm FD-SOI for the KF-21 mission computer. China’s CETC produced 28 nm rad-hard FPGAs domestically in 2025, signaling reduced import reliance. Australia’s AUD 3.5 billion missile-and-drone plan under AUKUS fuels demand for domestic assembly.

Europe relies on the EUR 43 billion EU Chips Act aiming to double regional share by 2030. ESA’s ARIEL and PLATO missions sustain SiC and rad-tolerant demand. Germany’s EUR 2.3 billion Typhoon radar upgrade uses GaN modules from United Monolithic Semiconductors. The Tempest fighter mandates FACE-compliant COTS processors from Texas Instruments and NXP, trading proprietary hardware for faster refresh.

Mordor Intelligence provides coverage of the semiconductor device market in aerospace and defense industry across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

In the Aerospace and Defense sector, the semiconductor device market showcases a moderate concentration. The top ten suppliers collectively command a 55% market share, with none exceeding 15%. Established players like Analog Devices, Microchip Technology, and Texas Instruments leverage their decades-long heritage rooted in QML-V and MIL-STD-883. Meanwhile, newcomers like Vorago Technologies and CAES are capitalizing on niches, focusing on extreme-temperature SiC MOSFETs and 3D-stacked processors.

Horizontal integration is on the rise. Mercury Systems acquired Pentek for USD 320 million, aiming to pair MOSA-ready radio cards with their chassis. Lockheed Martin made a strategic move, pre-funding USD 150 million for tool upgrades at GlobalFoundries, securing a decade-long wafer agreement. In a collaborative effort, Qorvo and the Air Force Research Laboratory are pushing the boundaries of GaN-on-diamond technology, with the latter enjoying royalty-free rights. Disruptors like SiMa.ai, buoyed by venture capital, recently secured USD 70 million to develop sensor-integrated AI accelerators.

The market is also witnessing advancements in material science and manufacturing processes. Companies are increasingly adopting wide-bandgap semiconductors, such as gallium nitride (GaN) and silicon carbide (SiC), to enhance performance in high-power and high-frequency applications. These innovations are critical for meeting the demanding requirements of aerospace and defense systems, including improved thermal management, efficiency, and reliability.

Leaders of Semiconductor Device Market in Aerospace and Defense Industry

Texas Instruments Inc.

Microchip Technology Inc.

Infineon Technologies AG

Analog Devices Inc.

onsemi (ON Semiconductor)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microchip Technology qualified the MPFS500T PolarFire FPGA to QML-V Class V, offering 500 k logic elements with embedded RISC-V cores at 50% lower power, aimed at satellites and missile seekers.

- November 2025: Wolfspeed and the Air Force Research Laboratory agreed on USD 45 million to develop 200 mm SiC substrates, targeting 40% wafer-cost cuts for hypersonic RF parts.

- October 2025: L3Harris won USD 1.8 billion to deliver 72 Tranche 2 satellites with Versal AI Core FPGAs qualified to MIL-STD-883.

- September 2025: BAE Systems expanded its Nashua fab by 25% sub-90 nm capacity, ramping Q1 2026.

Scope of Report on Semiconductor Device Market in Aerospace and Defense Industry

The semiconductor device is an electronic component that relies on the physical properties of semiconductor materials, mainly silicon, germanium, gallium arsenides, and oxide semiconductors, to function. Its conductivity lies between conductors and insulators. In the aerospace and defense industry, semiconductor devices are widely used in manufacturing numerous devices and systems, such as communication and navigation systems, safety equipment, engine and flight control systems, missiles, avionics, and many more.

The Semiconductor Device Market In Aerospace And Defense Industry Report is Segmented by Device Type (Discrete Semiconductors, Optoelectronics, Sensors, and Integrated Circuits), Material (Silicon, Silicon Carbide, Gallium Nitride, and More), Application (Communication and Data Handling, Radar and ISR, Navigation, Power Management, Flight Control, Electronic Warfare, and Sensors), End-Use Platform (Commercial Aviation, Military Aviation, Spacecraft, UAVs, Ground and Naval, and Missiles), and Geography. Market Forecasts are Provided in Terms of Value (USD).

| Discrete Semiconductors |

| Optoelectronics |

| Sensors |

| Integrated Circuits |

| Silicon |

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Others (GaAs, SiGe, InP, Diamond) |

| Communication and Data Handling |

| Radar and ISR Payloads |

| Navigation and Guidance |

| Power Management and Propulsion Control |

| Flight Control and Avionics |

| Electronic Warfare and Counter-Measures |

| Sensors and Scientific Payloads |

| Commercial Aviation |

| Military Aviation |

| Spacecraft and Satellites |

| Unmanned Aerial Vehicles (UAVs) |

| Ground and Naval Defense Systems |

| Missiles and Precision Munitions |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Device Type | Discrete Semiconductors | |

| Optoelectronics | ||

| Sensors | ||

| Integrated Circuits | ||

| By Material | Silicon | |

| Silicon Carbide (SiC) | ||

| Gallium Nitride (GaN) | ||

| Others (GaAs, SiGe, InP, Diamond) | ||

| By Application | Communication and Data Handling | |

| Radar and ISR Payloads | ||

| Navigation and Guidance | ||

| Power Management and Propulsion Control | ||

| Flight Control and Avionics | ||

| Electronic Warfare and Counter-Measures | ||

| Sensors and Scientific Payloads | ||

| By End-Use Platform | Commercial Aviation | |

| Military Aviation | ||

| Spacecraft and Satellites | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Ground and Naval Defense Systems | ||

| Missiles and Precision Munitions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will GaN revenue grow within the Semiconductor Device Market in Aerospace and Defense Industry?

GaN revenue is projected to rise at a 7.36% CAGR from 2026 to 2031 as hypersonic and electronic-warfare programs transition away from GaAs.

Which platform will generate the most new semiconductor demand by 2031?

UAVs are set to expand at a 9.43% CAGR, driven by programs such as the Collaborative Combat Aircraft that aim for 1,000 autonomous wingmen.

What regional share does North America hold?

North America accounted for 36.91% of 2025 spending, supported by DARPA funding and CHIPS Act incentives.

Why are optoelectronics outpacing other device types?

Free-space optical links and LiDAR-guided munitions require photonic components that deliver higher data rates and precision than RF alternatives.

Page last updated on: