Semiconductor And Electronic Parts Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

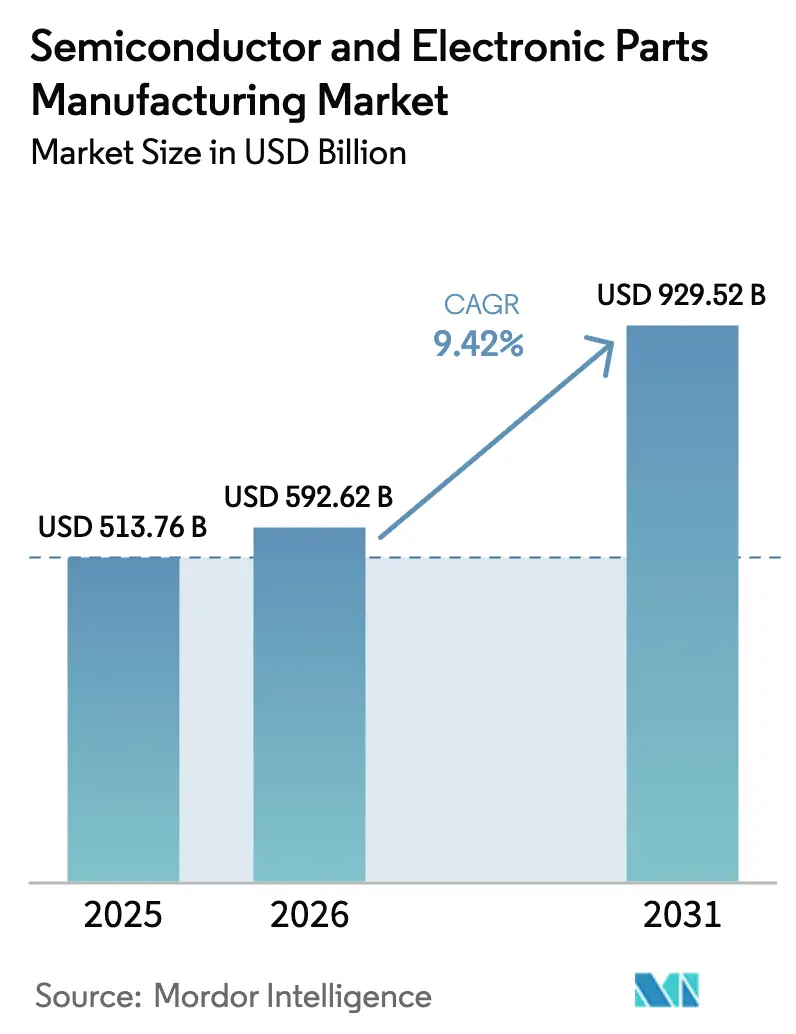

| Market Size (2026) | USD 592.62 Billion |

| Market Size (2031) | USD 929.52 Billion |

| Growth Rate (2026 - 2031) | 9.42% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semiconductor And Electronic Parts Manufacturing Market Analysis by Mordor Intelligence

The Semiconductor and Electronic Parts Manufacturing market size is expected to grow from USD 513.76 billion in 2025 to USD 592.62 billion in 2026 and is projected to reach USD 929.52 billion by 2031, expanding at a 9.42% CAGR over 2026-2031. This expansion translates into the swiftest absolute value creation the sector has recorded since the mid-2000s, confirming that structural supply-chain realignment, rather than post-pandemic recovery, is fueling capital formation. Accelerated deployments of artificial intelligence (AI) infrastructure are redefining semiconductor architecture priorities, favoring high-bandwidth memory and advanced packaging over additional node shrinks. Intensified electrification of transport, coupled with the migration to compound-semiconductor power devices, is unlocking premium revenue pools in silicon carbide (SiC) and gallium nitride (GaN). National subsidy programs- most notably the United States CHIPS and Science Act and the European Union Chips Act- have moved over USD 100 billion in direct incentives into fabrication construction pipelines, effectively re-shoring segments of the production footprint that exited these geographies three decades ago.[1]U.S. Department of Commerce, “CHIPS Act Grant Allocations,” commerce.gov Simultaneously, friend-shoring strategies are broadening mature-node capacity across Vietnam, India and Mexico, while export-control regimes raise compliance hurdles that favor vertically integrated leaders. Risk factors include escalating geopolitical constraints and a shortfall of process engineers specialized in sub-7 nm technologies.

Key Report Takeaways

- By product type, Logic ICs led with 36.54% revenue share in 2025, whereas the Discrete and Power segment is set to record a 10.42% CAGR through 2031.

- By component, Equipment captured 51.26% of the revenue in 2025 and Services are projected to grow at a 10.15% CAGR between 2026 and 2031.

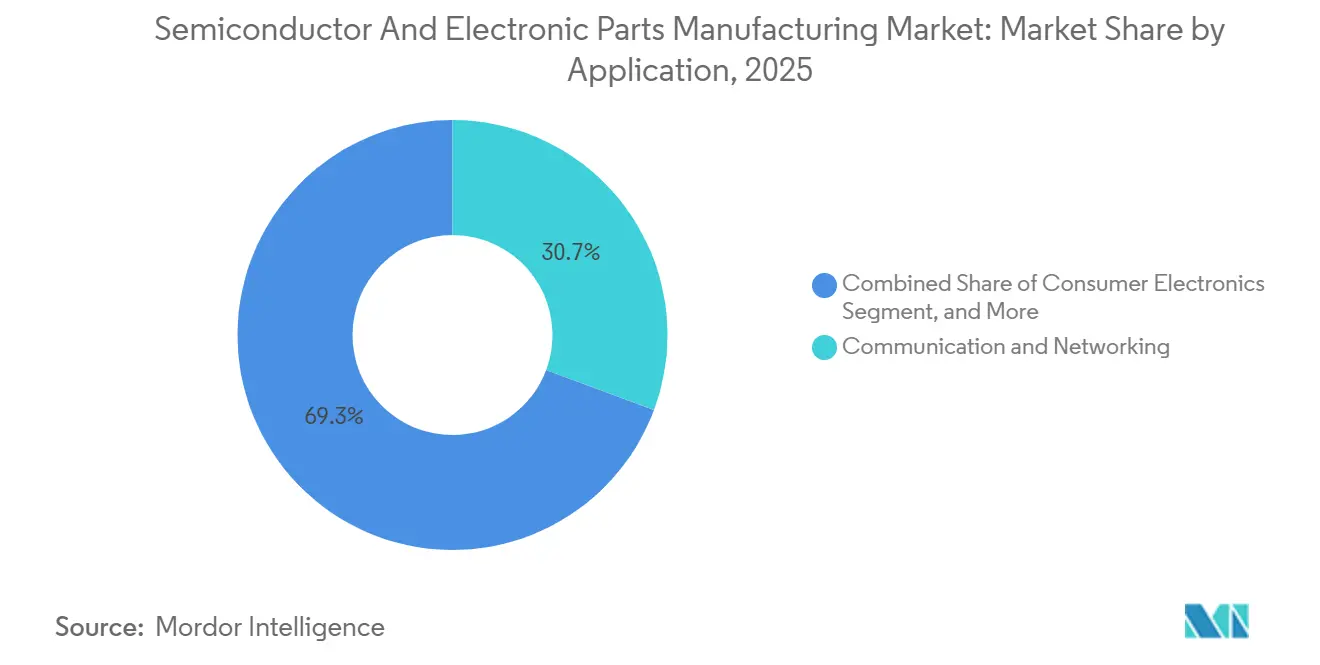

- By application, Communications and Networking captured 30.68% of the revenue in 2025, whereas Data Center and Cloud solutions are forecast to advance at a 10.86% CAGR through 2031.

- By technology node, sub-7 nm accounted for 43.48% of the 2025 revenue and is expected to expand at a 9.88% CAGR through 2031.

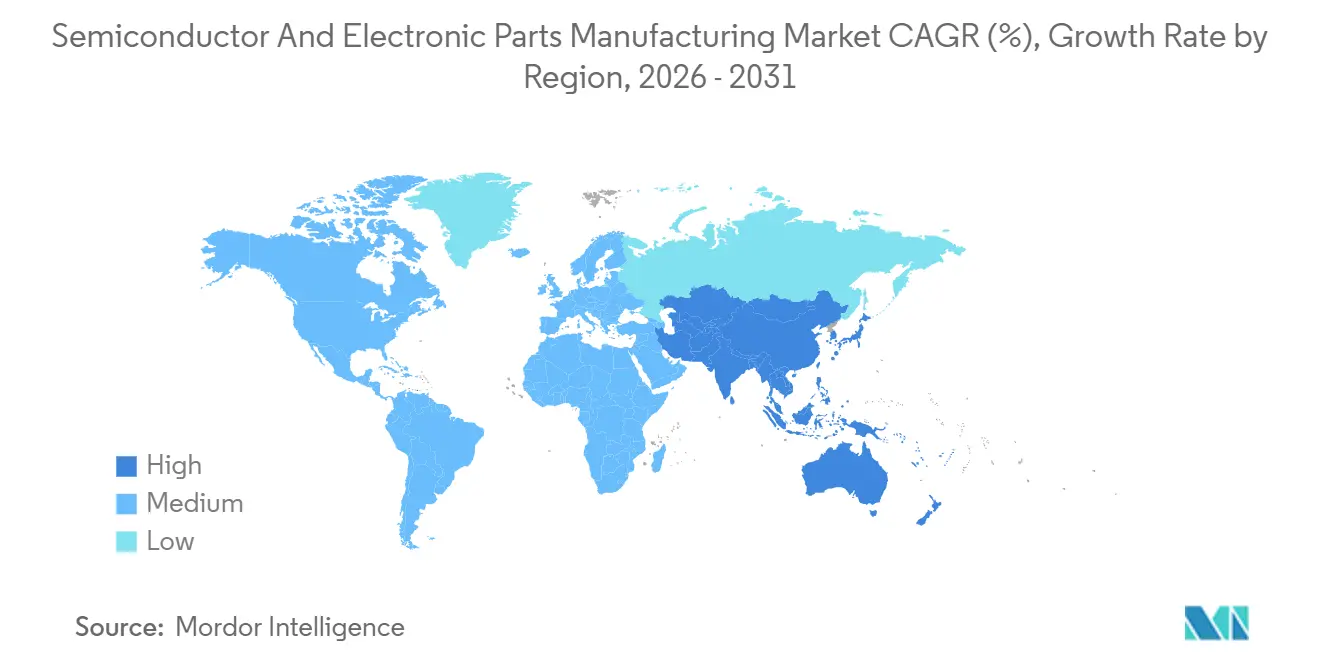

- By geography, the Asia-Pacific region accounted for 49.66% of 2025 revenue, while North America is expected to register the fastest regional CAGR of 11.26% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Semiconductor And Electronic Parts Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-led Demand for High-bandwidth Compute | +2.8% | Global, concentrated in North America and East Asia | Medium term (2–4 years) |

| Electrification of Transport Boosting SiC / GaN Content | +1.9% | Global, led by Europe, China and North America | Long term (≥ 4 years) |

| Government Fab-subsidy Race (CHIPS, EU Chips, K-Chips, etc.) | +2.1% | North America, Europe, South Korea, Japan | Short term (≤ 2 years) |

| 5G and Edge-IoT Device Proliferation | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2–4 years) |

| Chiplet and 3D Heterogeneous Integration Accelerating Node-agnostic Growth | +0.9% | Global, with R&D hubs in North America and Taiwan | Long term (≥ 4 years) |

| Friend-shoring Duplication of Critical Legacy-node Capacity | +0.5% | North America, Europe, Southeast Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

AI-Led Demand for High-bandwidth Compute

High-bandwidth memory (HBM) shipments expanded 150% year-over-year in 2025, reflecting generative-AI workloads that require 1.2 TB/s bandwidth per package. Hyperscalers have begun co-designing custom accelerators with foundries, compressing merchant GPU addressable markets and positioning advanced package technology as the next competitive frontier. Nvidia’s Blackwell architecture, entering volume shipments in 2026, integrates eight HBM3E stacks, straining clean-room capacity until late-2026 expansions materialize. Data-center retrofits now specify 1.5 MW racks, tripling 2024 power-density baselines and consequently driving demand for SiC modules in grid-tie inverters. Sovereign-AI programs in the United Arab Emirates, Saudi Arabia and India add a further USD 30 billion in localized compute budgets aimed at bypassing export-controlled GPUs. The multiplier extends into network fabrics and thermal-management subsystems, which together add USD 12,000 of semiconductor content per server rack.

Electrification of Transport Boosting SiC / GaN Content

Electric-vehicle semiconductor content reached USD 1,200 per unit in 2025, double the internal-combustion baseline, with SiC inverters contributing 35% of that uplift.[2]Infineon Technologies, “SiC Power Module Cost Trends,” infineon.com Tesla teardown data confirmed SiC module costs below USD 150 per kilowatt, catalyzing uptake in mass-market models priced under USD 30,000. Chinese automakers BYD and Geely are vertically integrating 200 mm SiC wafer lines, challenging Western vendors on cost while yield gaps persist at 25 percentage points. GaN devices, leveraged for on-board chargers, enable 30% volume reductions yet face reliability skepticism under automotive temperature cycling, limiting 2025 platform penetration to 15%. Euro 7 regulations mandating 48 V mild-hybrids across new passenger cars from July 2025 add incremental demand for 300,000 wafer starts per month of power discretes.

Government Fab-Subsidy Race

The United States disbursed USD 29 billion in CHIPS Act grants by December 2025, including USD 6.6 billion for TSMC’s Arizona Fab 21, which targets 3 nm output by 2027. The European Union committed EUR 15 billion (USD 16.4 billion) in direct support through mid-2025, directing EUR 10 billion (USD 10.9 billion) toward Intel’s Magdeburg complex. South Korea’s K-Chips program has pledged KRW 26 trillion (USD 19.5 billion) in tax offsets, accelerating Samsung’s Pyeongtaek P4 facility toward 2 nm volume output in late-2025. These subsidies dilute return-on-capital thresholds and embed overcapacity risks in 28 nm lines, where 1.2 million wafer starts per month are planned across Texas Instruments, GlobalFoundries and United Microelectronics by 2027. “guardrails” compel recipients to freeze expansions in “foreign countries of concern” for 10 years, structurally decoupling U.S. and Chinese ecosystems.

5G and Edge-IoT Device Proliferation

Global 5G subscriptions surpassed 1.9 billion in 2025, yet semiconductor upside pivots to Open RAN and private-network gateways where RF-front-end content stabilizes at USD 18 per handset. Industrial 5G deployments require time-sensitive networking, spurring ASIC integration by Broadcom and Marvell that melds modem and Ethernet functions, capturing 60% of the 2025 edge-switch silicon market. Edge AI inference multiplies compute density at towers tenfold, encouraging operator adoption of custom accelerators from Nvidia and AMD. IoT device consolidation is accelerating as Matter and Thread cut interoperability barriers, placing efficiency leadership with Nordic Semiconductor and Silicon Labs. 3GPP Release 18 mandates RedCap support, opening cost-optimized pathways for industrial sensors priced below USD 5 bill-of-materials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Geo-economic Export Controls | –1.4% | Global, acute in China–U.S. corridors | Short term (≤ 2 years) |

| IP-Rights Infringement and Cross-licensing Disputes | –0.6% | Global, concentrated in mobile and automotive | Medium term (2–4 years) |

| Acute Talent Shortages in Sub-7 nm Process Engineering | –0.9% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Neon and Advanced-gas Supply-chain Fragility | –0.7% | Global vulnerability in Europe and East Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Geo-Economic Export Controls

The U.S. Bureau of Industry and Security’s October 2024 rule expansion added 140 Chinese entities to the Entity List, curtailing access to sub-14 nm tools. ASML’s China revenue declined 35% in 2025 as High-NA EUV shipments pivoted to Europe and North America. China’s counter-measures on gallium and germanium disrupted GaN and SiC supply until Canada and Australia scaled output by mid-2025. Compliance costs now exceed USD 8 million annually for mid-tier suppliers, eroding margins and elongating design cycles to over 90 days. Dual-jurisdiction oversight under ITAR and EAR further slows time-to-market for dual-use innovations.

Acute Talent Shortages in Sub-7 nm Process Engineering

A global deficit of 67,000 process engineers is forecast by 2027, with sub-7 nm expertise concentrated in 12 fabs worldwide.[3]SEMI, “Global Semiconductor Workforce Forecast,” semi.org TSMC’s Arizona operations experienced six-month delays stemming from limited local yield-optimization skills, necessitating relocation of 500 Taiwanese engineers. Senior process-engineer compensation in Phoenix reached USD 350,000, a 60% premium over 2022, reducing fab operating margins. Intel’s USD 100 million university partnerships have yet to bridge a 40% graduation gap. Technician training pipelines are equally stressed, with only 3,000 community-college graduates available against 8,000 annual openings. CHIPS Act workforce funds trail construction schedules by 24 months, creating latent start-up risk for new lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Logic Anchors, Power Outpaces

The Semiconductor and Electronic Parts Manufacturing market size attributed to Logic ICs amounted to 36.54% of 2025 revenue, reflecting sustained demand for application processors and AI accelerators. Memory demand is expected to stabilize after 2026 as new HBM capacity alleviates supply constraints. Analog and mixed-signal components continue to generate significant revenue, driven by their extended life cycles in industrial and automotive applications. Discrete and power devices, are expected to outpace their peers by growing at a 10.42% CAGR, driven by the penetration of SiC and GaN in electric mobility.

Chiplet-based architectures blur these categories by embedding memory and I/O dies from mature nodes alongside cutting-edge compute chiplets, redistributing profit pools toward packaging specialists. Memory’s move to stacked configurations raises the cost of goods but earns pricing power, while analog suppliers defend margins via proprietary high-voltage flows. Chinese entrants are pressuring low-end discrete devices, forcing Western incumbents up-market into 1,200 V SiC, where yields and reliability create entry barriers.

By Component: Equipment Dominant, Services Ascendant

Equipment contributed 51.26% of 2025 component revenue, underpinned by multi-billion-dollar lithography outlays. High-NA EUV systems priced at USD 380 million each garnered unprecedented order backlogs. Software remains the strategic gatekeeper to sub-3 nm processes, with Synopsys and Cadence playing a dominant role in the advanced-node toolchain. Services will chart the fastest trajectory at a 10.15% CAGR in the forecast period, mirroring the growing intensity of design outsourcing.

The Semiconductor and Electronic Parts Manufacturing market size for Services is projected to eclipse USD 400 billion by 2031 as fabless firms deepen turnkey partnerships. Equipment vendors increasingly monetize installed bases through spares and predictive-maintenance analytics that carry gross margins exceeding 60%. Software is consolidating vertically, illustrated by Synopsys’ 2024 acquisition of Ansys. Geographic wage differentials steer routine verification tasks to India and Vietnam, while compliance frameworks such as ISO 26262 anchor higher-value audits in mature markets.

By Application: Communications Firm, Data Centers Surging

Communications and Networking remained the largest application at 30.68% of 2025 revenue, a share it sustains thanks to 5G infrastructure rollouts. Data Center and Cloud is the fastest-growing segment, with a 10.86% CAGR, driven by electric-vehicle inverter and ADAS compute needs. Consumer electronics, while mature, pocket incremental volume in wearables and smart-home devices. Industrial and Energy applications leverage Industry 4.0 automation and grid-modernization programs.

Automotive’s stringent zero-defect metrics necessitate process variants dedicated to functional safety, bifurcating fab utilization. Data-center buyers emphasize throughput per watt, spurring a pivot toward custom ASICs over GPUs for inference. Open RAN disaggregation in communications reallocates silicon value from turnkey base stations to merchant processors.

By Technology Node: Leading Edge Slows, Mature Nodes Thrive

Sub-7 nm capacity held 43.48% revenue share in 2025 yet will slow to a 9.88% CAGR as mask-set costs and yield headwinds erode economics. The 8-16 nm tier aligns with automotive and edge AI requirements. The 22-28 nm bracket is experiencing a resurgence driven by chiplet architectures, making it relevant in the Semiconductor and Electronic Parts Manufacturing market over the forecast period. Nodes beyond 28 nm, previously considered outdated, continue to see demand due to their applications in the analog and power markets.

TSMC’s 3 nm node yielded only 15% performance uplift at 2.5 times wafer cost, shrinking its accessible market, while Samsung’s 2 nm gate-all-around process promises gains but remains yield-limited. Intel’s 18A roadmap embeds backside power delivery to regain leadership by 2027. Chinese foundries expand mature nodes even under export restrictions, depressing 28 nm wafer pricing.

Geography Analysis

Asia-Pacific accounted for 49.66% of global revenue in 2025, with Taiwan and South Korea leading-edge logic and memory. The region’s growth is expected to be moderate as geopolitical diversification spreads capacity across India, Vietnam, and Malaysia. China remains the largest single-country buyer, yet export controls limit its access to advanced tools. Japan, boosted by double-digit subsidies, is resurgent in 22–28 nm lines through TSMC’s Kumamoto joint venture. India regains relevance in the back end as Micron and AMD build test and assembly campuses.

North America is set to record the swiftest CAGR of 11.26% through 2031, as CHIPS Act subsidies underwrite 12 new front-end fabs. The United States’ Semiconductor and Electronic Parts Manufacturing market size is estimated to grow rapidly by 2031, reversing a three-decade offshoring trend. Canada advances as a SiC materials hub, while Mexico scales OSAT capacity for near-shore automotive supply chains.

Europe is aiming to increase its global presence by 2030 through a EUR 43 billion subsidy pool. Germany hosts the flagship Intel Magdeburg plant, while France specializes in SiC through STMicroelectronics. The Middle East channels sovereign wealth toward AI-focused fabs, though domestic ecosystems remain at pilot scale. Africa’s footprint is nascent but growing via consumer-electronics assembly in South Africa and Nigeria.

Competitive Landscape

The leading edge is oligopolistic: TSMC, Samsung and Intel own 85% of sub-7 nm capacity. Conversely, the legacy tier remains fragmented across more than 15 players, giving automotive and industrial customers leverage to dual-source. Foundries are monetizing process IP licensing as fabless designers forego proprietary node development. Capital intensity shifts margin pressure to equipment vendors that must commit to multi-generational backward compatibility.

Chiplet ecosystems unlock greenfield niches for startups capable of delivering specialized dies that integrate via UCIe interfaces without building fabs. Chinese producers SMIC and Hua Hong push mature-node performance envelopes through advanced packaging, approximating 7 nm results at 14 nm geometry. Analog leaders Texas Instruments and Analog Devices defend 65% combined gross margins via differentiated high-voltage flows. RISC-V adoption eclipses 10 billion shipped cores, challenging Arm’s incumbent royalty model. Patent trends show TSMC filing 1,200 gate-all-around and backside-power patents in 2025, cementing IP leadership through the decade.

Semiconductor And Electronic Parts Manufacturing Industry Leaders

Intel Corporation

Samsung Electronics Co. Ltd

Taiwan Semiconductor Manufacturing Co. Ltd.

SK Hynix Inc.

Micron Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: TSMC announced a USD 12 billion expansion of Arizona Fab 21 to add 2 nm production by 2028, including a CoWoS packaging plant.

- November 2025: Intel secured USD 7.9 billion in CHIPS Act grants plus USD 11 billion in loans for its Ohio megasite, scheduled for Intel 18A output in 2027.

- October 2025: Samsung Electronics commenced volume 2 nm gate-all-around production at Hwaseong, supplying Qualcomm smartphone SoCs.

- September 2025: Micron broke ground on a USD 15 billion HBM3E fab in Boise, Idaho, backed by USD 6.1 billion in CHIPS funding.

- August 2025: Nvidia partnered with Foxconn to establish USD 10 billion AI-server assembly in Mexico for North American cloud clients.

Global Semiconductor And Electronic Parts Manufacturing Market Report Scope

The global semiconductor and electronic parts manufacturing market report tracks the revenues accrued from the vendors of the semiconductor and electronics manufacturing industry. As the integration and collaboration of semiconductor and electronic products with different applications are increasing, the need for manufacturing activities of semiconductor and electronics parts has been growing on a similar pattern.

The Semiconductor and Electronic Parts Manufacturing Market Report is Segmented by Product Type (Logic IC, Memory, Analog and Mixed-Signal, Discrete and Power, Sensors and Optoelectronics), Component (Equipment, Software, Services), Application (Communications and Networking, Transportation and Mobility, Consumer Electronics, Industrial and Energy, Data-Center and Cloud), Technology Node (Less than 7nm, 8-16nm, 22-28nm, Greater than 28nm), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Logic IC |

| Memory (DRAM, NAND, Emerging) |

| Analog and Mixed-Signal |

| Discrete and Power (SI, SiC and GaN) |

| Data- Center and Cloud |

| Equipment (Front-end, Back-end) |

| Software (EDA, IP Cores) |

| Services (Design, Assembly, Test) |

| Communications and Networking |

| Transportation and Mobility |

| Consumer Electronics |

| Industrial and Energy |

| Data- Center and Cloud |

| Less than 7nm |

| 8- 16 nm |

| 22- 28 nm |

| Greater than 28 nm |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Logic IC | |

| Memory (DRAM, NAND, Emerging) | ||

| Analog and Mixed-Signal | ||

| Discrete and Power (SI, SiC and GaN) | ||

| Data- Center and Cloud | ||

| By Component | Equipment (Front-end, Back-end) | |

| Software (EDA, IP Cores) | ||

| Services (Design, Assembly, Test) | ||

| By Application | Communications and Networking | |

| Transportation and Mobility | ||

| Consumer Electronics | ||

| Industrial and Energy | ||

| Data- Center and Cloud | ||

| By Technology Node | Less than 7nm | |

| 8- 16 nm | ||

| 22- 28 nm | ||

| Greater than 28 nm | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global semiconductor and electronics parts sales be by 2031?

Revenue is forecast to reach USD 929.52 billion by 2031, expanding at a 9.42% CAGR from the 2026 baseline.

Which regional market is set to grow the fastest over the next five years?

North America posts the quickest trajectory at an 11.26% CAGR, fueled by CHIPS Act–backed fab construction.

What component category shows the highest growth potential?

Services, encompassing outsourced physical design and verification, are projected to rise at a 10.15% CAGR.

How do export-control rules affect Chinese semiconductor manufacturers?

Expanded Entity List restrictions deny advanced lithography tools, causing a 35% revenue hit for top equipment vendors in China and compelling local firms to innovate at mature nodes.

What is driving the surge in high-bandwidth memory demand?

Generative-AI training clusters and data-center GPUs require multi-terabyte per second bandwidth, pushing HBM shipments up 150% year-over-year in 2025.

Page last updated on: