Selective Laser Sintering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

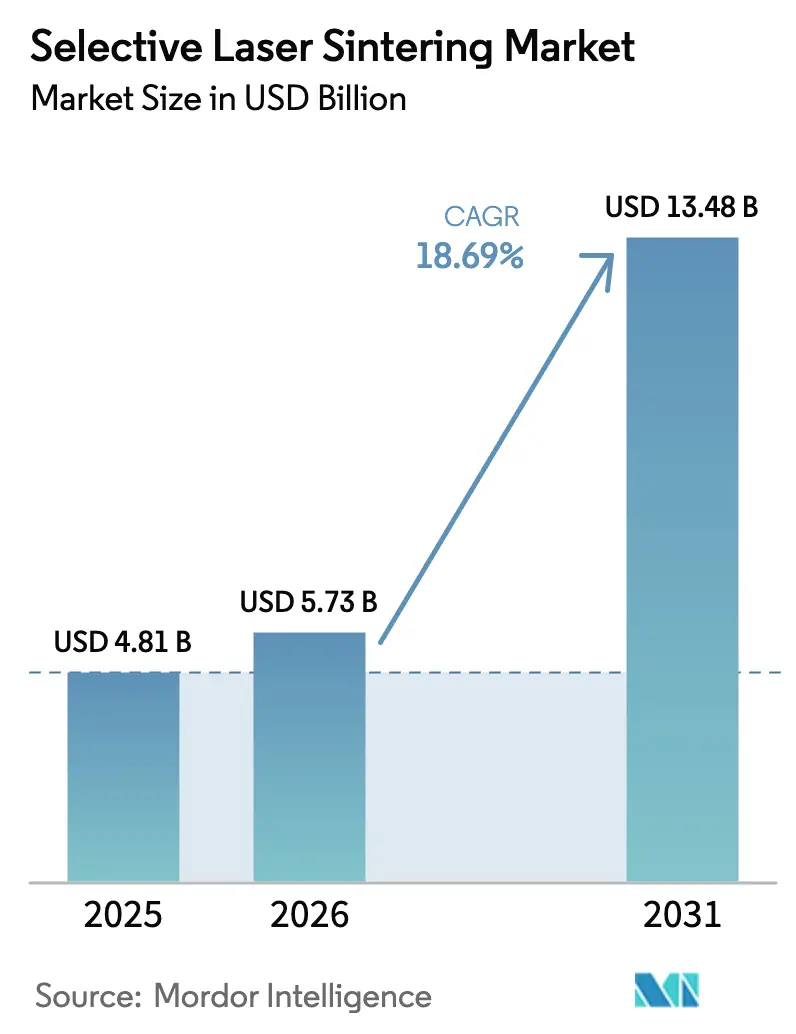

| Market Size (2026) | USD 5.73 Billion |

| Market Size (2031) | USD 13.48 Billion |

| Growth Rate (2026 - 2031) | 18.69% CAGR |

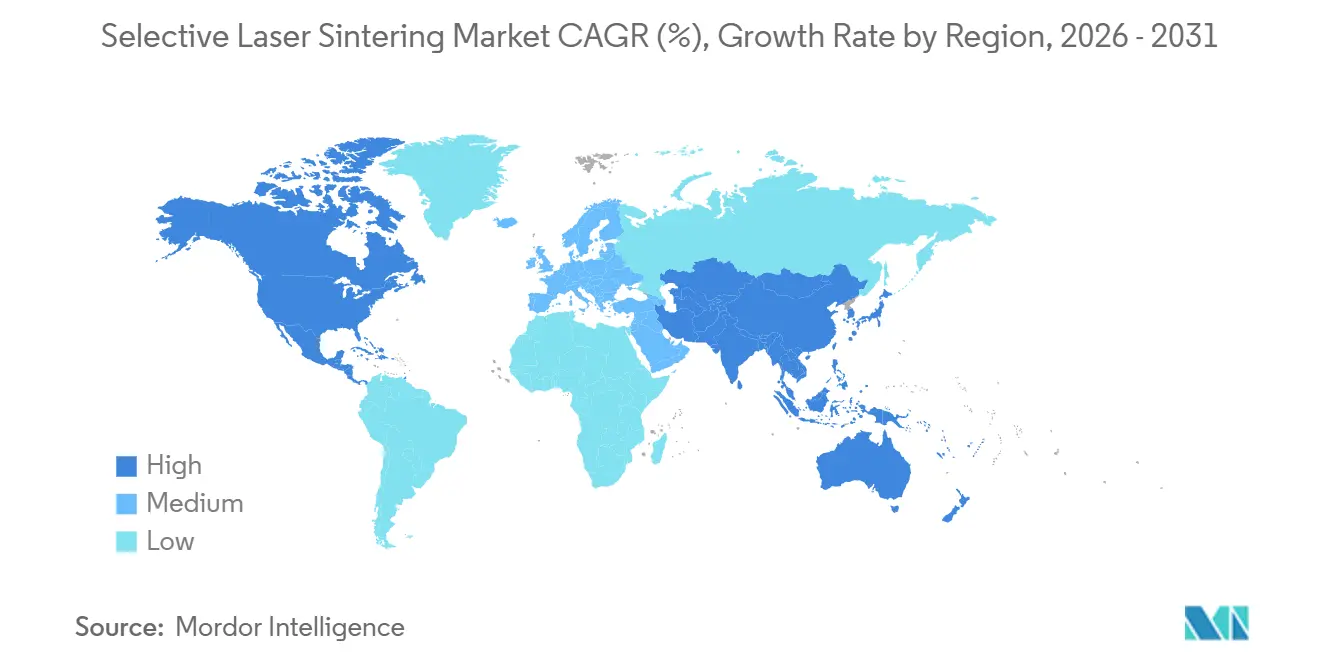

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

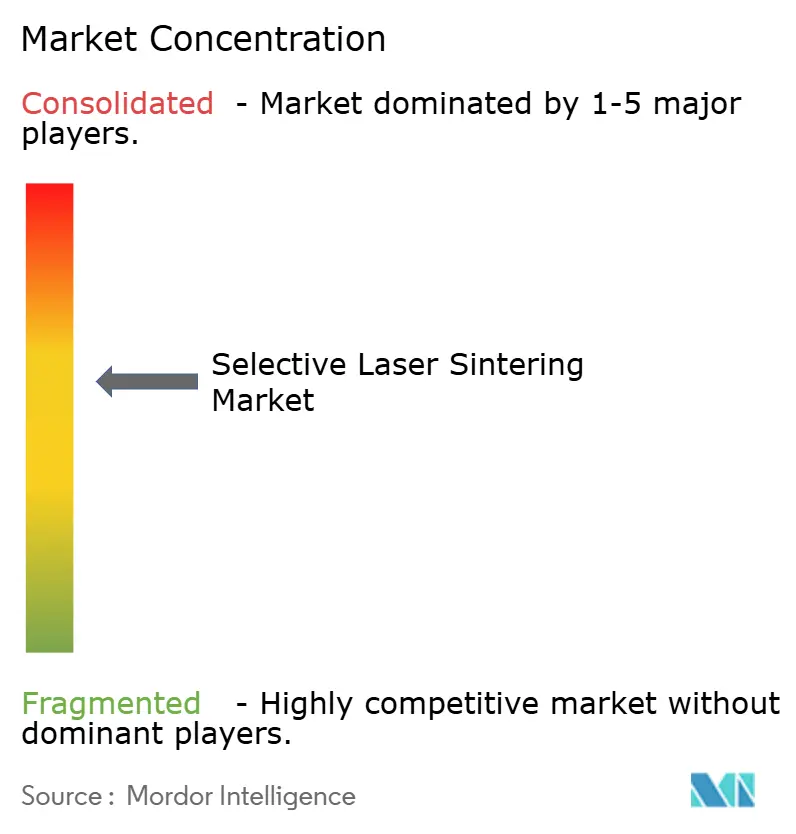

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Selective Laser Sintering Market Analysis by Mordor Intelligence

The Selective Laser Sintering Market size was valued at USD 4.81 billion in 2025 and estimated to grow from USD 5.73 billion in 2026 to reach USD 13.48 billion by 2031, at a CAGR of 18.69% during the forecast period (2026-2031). Early adopters are shifting from prototyping to serial production, converting physical stock into digital files and building parts on demand, which frees working capital. Automakers favor SLS’s ability to create complex cooling channels and lightweight brackets that traditional tooling cannot match. Hospitals now rely on FDA-cleared printers for patient-specific implants that reduce operating-room time and imaging artifact.[1]U.S. Food and Drug Administration, “510(k) Premarket Notification K240807,” fda.gov Service bureaus are growing as enterprises outsource powder handling, while material suppliers race to qualify medical-grade polymers to capture the customization premium. Consolidation among hardware vendors seeks to secure multi-material intellectual property and close the throughput gap between desktop and industrial platforms.

Key Report Takeaways

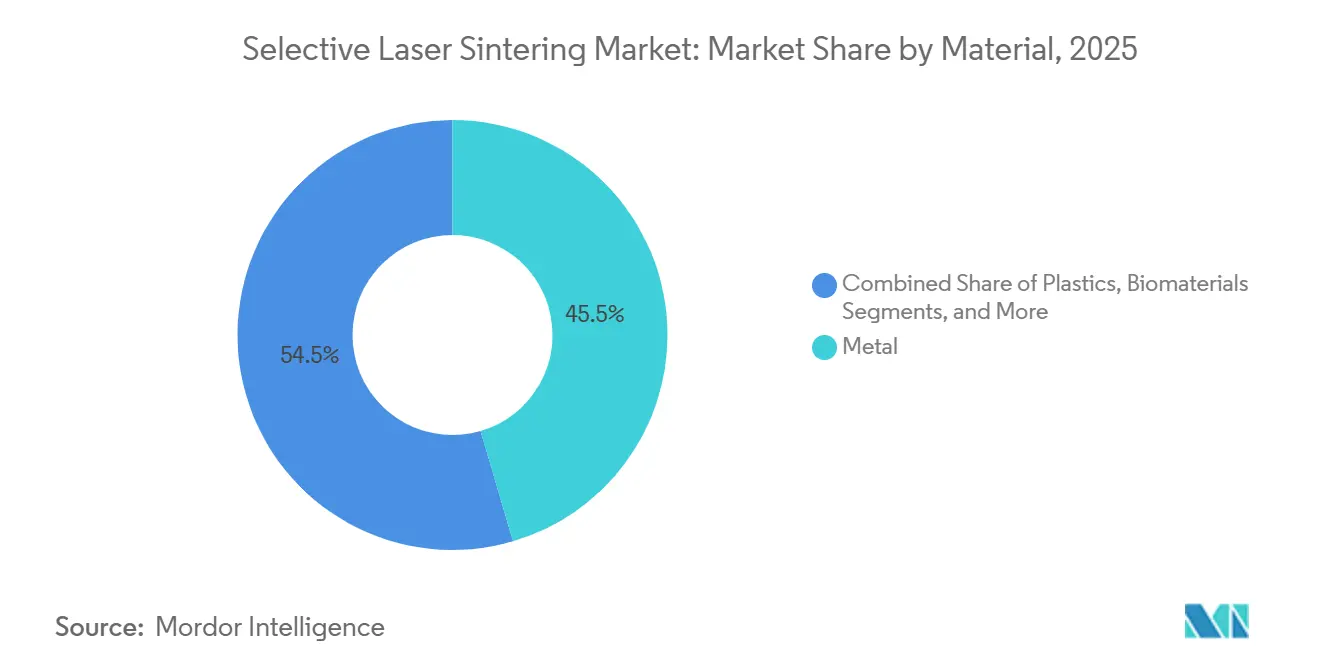

- By material, metal held 45.71% of the selective laser sintering market share in 2025; biomaterials are forecast to advance at an 19.43% CAGR to 2031.

- By component, hardware commanded 73.27% of the selective laser sintering market size in 2025, while services post the fastest projected CAGR at 18.71% through 2031.

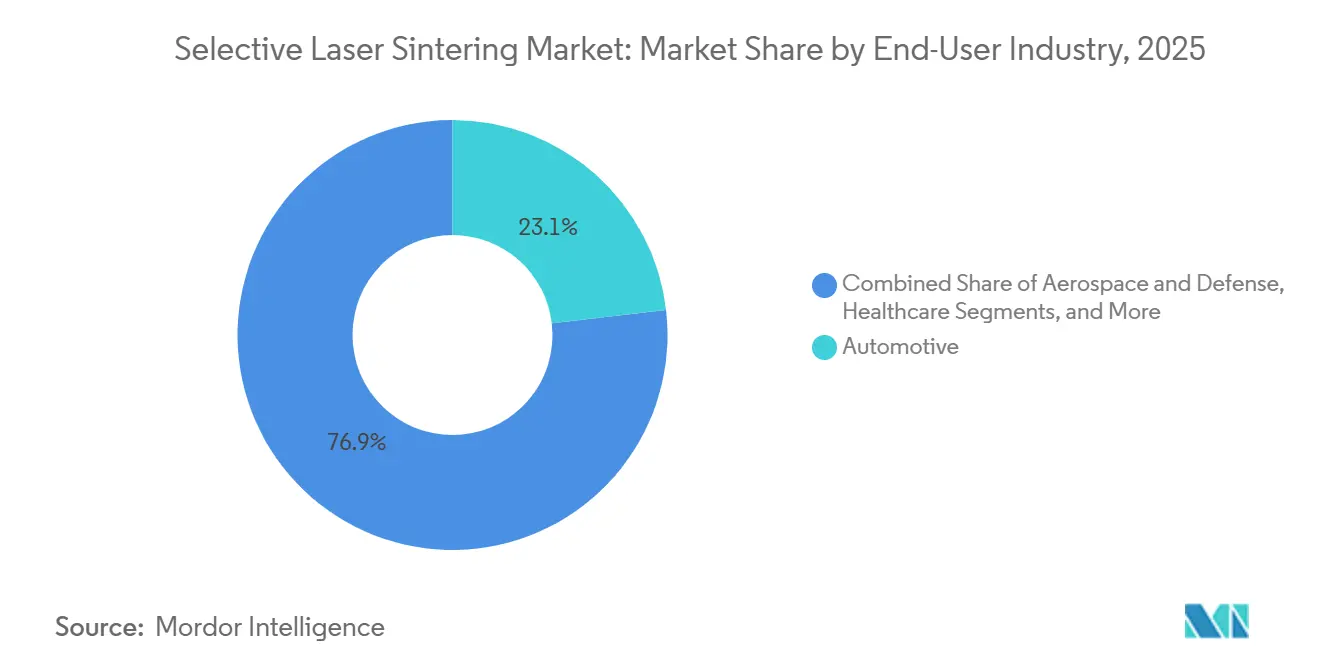

- By end-user, automotive led with 23.14% revenue share in 2025; healthcare records the highest anticipated CAGR at 18.92% to 2031.

- By printer type, industrial platforms captured 71.37% of 2025 revenue, whereas desktop SLS systems are projected to grow at 18.72% over 2026-2031.

- By geography, North America accounted for 36.34% of 2025 value; Asia-Pacific is poised for the quickest expansion at 19.11% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Selective Laser Sintering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift Toward Digital Spare-Parts Warehousing | +3.2% | Global, early adoption in North America aerospace and European automotive | Medium term (2-4 years) |

| Mainstream Adoption of SLS for Lightweight EV Components | +3.8% | APAC core (China, South Korea) with spill-over to North America and Europe | Medium term (2-4 years) |

| Government Grants Fueling Additive Manufacturing R&D | +2.1% | North America, Europe, China | Long term (≥4 years) |

| Integration of AI-Driven Process Monitoring in SLS Printers | +2.4% | Global, led by U.S. and EU industrial clusters | Short term (≤2 years) |

| Expansion of Medical-Grade Polymer Powders Portfolio | +2.9% | North America and Europe, emerging uptake in APAC medical hubs | Medium term (2-4 years) |

| Near-Net-Shape Production Reducing Material Waste | +2.6% | Global, especially high-material-cost aerospace and medical applications | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Digital Spare-Parts Warehousing

Manufacturers are replacing slow-moving stock with encrypted CAD files stored in cloud libraries and printing parts only after failure events. ABB cut turbocharger lead time from nine weeks to one week under this strategy, reducing downtime penalties.[2]ABB Group, “Turbocharging 3D-Printed Spare Parts,” abb.com Low-runner aerospace and railway components benefit most because SLS removes the need for expensive molds that never amortize at volumes below 50 units. Liability remains unsettled as regulators decide whether file custodians or print operators bear responsibility for safety-critical failures, yet insurers are piloting coverage tied to verified build logs, which could accelerate adoption once actuarial benchmarks mature.

Mainstream Adoption for Lightweight EV Components

Electric-vehicle OEMs increasingly specify PA12-CF brackets and conformal-cooled housings that reduce mass by 20-30% while improving thermal efficiency.[3]Formlabs, “SLS 3D Printing for Automotive,” formlabs.com SLS eliminates tooling and delivers validated parts within 72 hours, truncating design cycles that once spanned six to nine months. Although per-part economics still favor injection molding above 5 000 units, platform proliferation in the EV sector is driving lower annual volumes per SKU, broadening SLS’s addressable market. Battery-pack redesign frequency now averages 18 months; avoiding new tooling each cycle amplifies the value proposition.

AI-Driven Process Monitoring

Neural-network models trained on melt-pool imagery detect curl and porosity with 99.1% accuracy, allowing printers to modulate laser power mid-build and cut scrap from 8% to 3% on typical powder budgets. Reduced scrap stabilizes delivery commitments, making SLS attractive for tier-one automotive suppliers that operate on just-in-time calendars. Proprietary datasets limit widespread tuning of exotic materials, so collaborations between universities and OEMs are forming to create open defect libraries, bolstering the competitiveness of smaller bureaus.

Expansion of Medical-Grade Polymer Powders

Evonik’s GMP-certified RESOMER powder supports resorbable scaffolds that dissolve after bone regeneration, replacing permanent titanium meshes and eliminating secondary surgeries . U.S. and German payers are gradually classifying printed spinal cages under reimbursable DRG codes, which unlocks high-margin recurring demand. Imaging artifacts decline when PEEK instead of metal is implanted, simplifying oncology follow-ups and reducing MRI rescans. Powder vendors are scaling multi-ton annual output, but capacity remains tight, so hospitals often book allotments six months ahead to secure inventory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Consumption per Build Cycle | -2.1% | Global, acute in Europe and Japan | Short term (≤2 years) |

| Skilled Operator Shortage in Emerging Economies | -1.8% | APAC emerging markets, Africa, Latin America | Medium term (2-4 years) |

| Powder Supply Chain Volatility Amid Trade Tariffs | -1.4% | Global, heightened for North America and APAC importers | Short term (≤2 years) |

| Surface-Finish Limitations Requiring Costly Post-Processing | -1.6% | Global, especially consumer and medical applications | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption per Build Cycle

Polymer SLS platforms draw 60-70 kWh over a 12-hour run, triple the energy required for comparable injection-molded volumes. European operators paying EUR 0.22/kWh mitigate exposure with off-peak scheduling or colocating alongside solar arrays. Metal DMLS machines intensify the burden by adding argon floods and stress-relief furnaces, pushing breakeven volumes above 500 units in non-aerospace applications. Energy taxes under the EU Green Deal, if expanded, could widen regional operating-cost gaps and encourage trans-Atlantic relocation of large-volume projects.

Skilled Operator Shortage in Emerging Economies

MIT research projects 27,300 cumulative U.S. openings for additive-manufacturing technicians by 2031, and similar ratios apply across India, Indonesia, and Mexico. Courses that integrate SLS powder handling, thermal-camera interpretation, and post-processing remain rare. India’s government earmarked USD 48 million for ten SLS training centers, yet seat capacity covers barely half the annual requirement. Bureaus now redesign workflows around automated depowdering and sealed hoppers to lower skill thresholds, but that capital upgrade inflates service fees by 8-12%, partially offsetting labor savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biomaterials Diminish Metal’s Lead

Metal retained 45.71 of % selective laser sintering market share in 2025 as aerospace-qualified titanium and Inconel parts transitioned from prototypes to flight hardware. Biomaterials, however, are projected to outpace all peers at a 19.43% CAGR, fueled by demand for resorbable cranial and spinal implants that command USD 2,000-5,000 per unit and ride favorable reimbursement frameworks. The selective laser sintering market for biomaterials is set to surpass USD 1 billion before 2031 if hospital procurement pipelines continue at current rates.

Plastics, chiefly PA12 and PA11, still dominate functional prototyping because powder costs stay below USD 60/kg and 50% recycled content remains process-safe. Composite nylons reinforced with carbon fibers are moving into drone frames, providing aluminum-like stiffness at 40% lower density. Meanwhile, binder-jet metal lines threaten metal SLS in commodity brackets, but SLS preserves an edge where >99.5% density and fatigue life matter.

By Component: Services Shift the Revenue Mix

Hardware contributed 73.27% of 2025 sales, but declining printer ASPs and desktop entry models under USD 20 000 pressure the segment. The selective laser sintering market size associated with services is forecast to jump as enterprises outsource powder logistics, ISO-13485 documentation, and vapor smoothing. Services already capture 26.73% share and will gain roughly one percentage point annually, whereas hardware ASP erosion accelerates.

Software lags in dollar terms yet underpins value; AI-subscription bundles that trim scrap unlock 15-25% margin swings and justify USD 5,000-20,000 annual licenses. Industrial OEMs now bundle slicers, remote monitoring, and predictive maintenance to lock users into ecosystems, blunting desktop cannibalization.

By End-User Industry: Hospitals Overtake Toolrooms

Automotive held 23.14% revenue share in 2025 on jigs and prototype brackets, but healthcare receipts are on course for the fastest growth, propelled by patient-matched implants cleared under new FDA guidelines. The selective laser sintering market size booked by hospitals is projected to eclipse automotive by 2029 if payer coverage continues to spread.

Aerospace adoption slows as legacy fleets complete retrofit cycles, but the sector still values weight savings that cut fuel burn by 15% in LEAP engines. Electronics players print thin-wall wearable housings where integrated snap-fits remove assembly cost. Energy firms print pump impellers on-site, compressing lead time from 12 weeks to 72 hours, though surface roughness remains a hurdle without vapor smoothing.

By Printer Type: Desktop Platforms Democratize Access

Industrial systems account for 71.37% revenue thanks to build volumes >300 l and validated material sets exceeding 30 polymers and metals. Yet desktop units grow at an 18.72% CAGR as contract manufacturers and universities adopt sub-USD 20 000 machines that run on standard power and occupy 1.2 m² footprints.

Hybrid SLS/CNC systems remain niche but entice aerospace suppliers needing ±0.05 mm tolerances without repositioning. High-speed sintering gains momentum for PA12 consumer goods, although 20-30% rougher surfaces mandate extra tumbling that narrows its throughput advantage. The selective laser sintering market share held by desktop models is projected to reach double digits by 2031 as powder recyclers and closed build chambers reduce operator touchpoints.

Geography Analysis

North America represented 36.34% of 2025 value, anchored by over 2 000 installed industrial printers in aerospace hubs of Seattle and Los Angeles. Hospitals in Massachusetts run FDA-cleared systems that print surgical guides within 48-72 hours, trimming pre-operative planning cycles by two weeks. Skilled-labor deficits intensify as vacancies linger for 60 days on average, driving automation investments in powder handling and CT scanning. Canada’s business-jet programs and Mexico’s automotive jig lines add incremental volumes but lack sufficient engineering pipelines to scale.

Asia-Pacific is forecast to post a 19.11% CAGR as China’s CNY 20 billion additive-manufacturing initiative funds production plants, and India dedicates USD 48 million toward operator training. Chinese EV OEMs exploit PA12-CF brackets to shave kilograms and extend range, while Japan’s hospitals trial PEEK cranial plates that reduce MRI artifacts. South Korean electronics majors evaluate SLS for smartwatch shells, although vapor-smooth steps add USD 20-50 per part and can offset cost gains.

Europe’s automotive corridor in Baden-Württemberg specifies glass-filled PA12 manifolds that meet UN ECE R100 flammability rules. The United Kingdom maintains titanium DMLS capacity for turbine blades but faces 8-12% material-cost hikes after powder-import tariffs post-Brexit. France’s DRG codes already reimburse 3D-printed spinal cages, spurring Lyon clinics to internalize printing. Middle Eastern oil producers and Australian miners run pilot programs, yet installed bases remain below 50 machines each due to high ambient-temperature challenges.

Regulatory Landscape

Regulation for SLS spans medical-device oversight, workplace safety for powders, and machinery/product safety requirements for the equipment itself. In the United States, patient-specific devices produced via powder bed fusion commonly route through FDA pathways such as 510(k) under the Quality System Regulation (21 CFR 820), reinforcing traceability expectations for build records, material controls, and validation when SLS shifts from prototyping to serial production.

In Europe, the Machinery Regulation (EU) 2023/1230 adds compliance complexity for machinery with AI-based or self-evolving safety functions, including requirements that can trigger mandatory third-party conformity assessment; an amendment, Regulation (EU) 2024/2748, applies from 29 May 2026 and introduces emergency procedures for crisis-relevant machinery. Standards frameworks also shape qualification approaches in tightly regulated end uses: ISO/ASTM 52931-23 anchors EHS principles for metallic powders in additive manufacturing environments, while space and defense-grade deployments face stringent machine-and-facility-specific qualification regimes referenced in bodies such as NASA (NASA-STD-6033) and ECSS (ECSS-Q-ST-70-80C).

Value Chain Analysis

The SLS value chain begins with feedstocks and critical subsystems, including polymer and metal powders (often qualified to specific machine parameter sets), lasers and optics, motion/control electronics, and inert-gas and filtration components for metal platforms. Hardware OEMs integrate these into printer platforms alongside software stacks (slicers, nesting, monitoring, and quality documentation), then distribute through direct sales and channel partners to end users and service bureaus; downstream, post-processing (depowdering, blasting, vapor smoothing, heat treatment for metals) and inspection/traceability (CT, metrology, build-log retention) convert printed builds into production-ready parts.

Cost and lead-time bottlenecks concentrate around qualified powders and precision optics, and operators respond by increasing powder recycling rates, investing in sealed handling to reduce contamination and labor risk, and adopting hybrid workflows that pair SLS builds with conventional finishing. Trade and tariff dynamics add friction to cross-border sourcing of feedstocks and components, pushing more regionalized procurement and localized production ecosystems, while the rising share of services reflects outsourcing of powder logistics, documentation (for example, ISO-13485-related work in healthcare supply), and specialized finishing when enterprises scale from R&D to repeatable production lots.

Competitive Landscape

Roughly 55-60% of hardware revenue sits with EOS, 3D Systems, and HP, indicating moderate market concentration. Desktop challengers such as Formlabs and Sinterit erode entry-level profit pools, while Nano Dimension’s USD 183 million acquisition of Desktop Metal secured binder-jet patents that allow graded powder deposition and cemented a first-mover edge in multi-material builds. Stratasys followed by carving out the Aerosint division, signaling an arms race for selective powder-placement IP.

Material suppliers pursue exclusivity; BASF’s Ultrasint TPU 88A FR, certified UL 94 V-0, gives partners a protected inflow to EV battery-housing contracts. Software ecosystems emerge as the new moat: Materialise nesting algorithms raise throughput 25%, tying users to annual licenses and data clouds. Service bureaus confront vertical integration as hospitals and automakers bring printing onsite; to survive, many pivot to validation services and post-processing specialization.

Emerging AI inspection suites reduce scrap and bolster delivery confidence. EOS’s closed-loop control adjusts laser power based on real-time thermal imagery, demonstrating 5-percentage-point margin lifts in aerospace contracts. Vendor strategies now split between throughput-optimized industrial lines and agile desktop offerings, forcing dual-portfolio management.

Selective Laser Sintering Industry Leaders

3D Systems Inc.

EOS GmbH Electro Optical Systems

Farsoon Technologies

Prodways Group

Formlabs Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clear whitespace sits at the intersection of production-scale reliability and total workflow automation, particularly in post-processing and quality data capture where many users still face labor-intensive depowdering and finishing. Evidence of this shift appears in service-bureau operations such as FORMRISE integrating AM Solutions S1 automated blasting systems and reporting a 50% reduction in post-processing time for SLS components, which strengthens the business case for serial runs by pulling cycle time and labor content out of the bottleneck stage.

Hardware and materials opportunities are also expanding through both ends of the platform spectrum: large-format systems that bring higher throughput and build volumes into SME-accessible footprints, and compact, open-ecosystem platforms that lower barriers for labs and job shops developing their own parameter sets. Formlabs launch activity around its Fuse X1 large-format SLS ecosystem (with AI-driven print controls) and Sinterit positioning with an open-material compact SLS platform illustrate the bifurcation. On the industrial side, qualification partnerships such as Farsoon working with ALM on material expansion and process steps for PEBA highlight how material breadth and validated recipes remain central to unlocking repeatable end-use production, especially as regulated and performance-critical applications demand tighter process windows and documented control.

Recent Industry Developments

- June 2026: Formlabs unveiled the Fuse X1 large-format SLS ecosystem, opening orders with deliveries scheduled to begin in Q4 2026. The launch expands access to larger build volumes and integrates AI-driven controls aimed at stabilizing production outcomes, supporting the market shift from prototyping to repeatable small-batch manufacturing.

- May 2026: Sinterit launched the BIANCO2 compact SLS platform powered by a 30W RF CO2 laser, with shipments planned for Q4 2026. Its positioning around a more open material approach broadens options for service bureaus and labs seeking to qualify alternative powders and reduce dependence on vendor-locked materials.

- May 2026: Regulation EU 2024/2748 applies from 29 May 2026 and introduces emergency procedures for crisis-relevant machinery, adding compliance requirements for safety and conformity assessment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the revenues generated from selective laser sintering used to build parts by fusing powdered materials using a laser, including the related hardware, software, and services sold for industrial and prototyping use.

Scope exclusions: Revenues from non-SLS additive processes and general 3D printing consumables not used in SLS builds are excluded.

Segmentation Overview

- By Material

- Metal

- Plastics

- Composite and Advanced Polymers

- Biomaterials

- By Component

- Hardware

- Software

- Services

- By End-User Industry

- Automotive

- Aerospace and Defense

- Healthcare

- Electronics

- Energy and Industrial Equipment

- Education and Research

- By Printer Type

- Powder-Bed Polymer SLS

- Metal SLS / DMLS

- High-Speed Sintering

- Hybrid SLS Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for the model, especially on manufacturing activity, trade flows, and the policy environment that shapes adoption of additive processes. We reviewed public sources such as US Census Bureau manufacturing series, US International Trade Commission trade statistics, Eurostat industrial production data, and OECD indicators for investment and output.

To connect the SLS story to what buyers actually do, we also checked sources such as ASTM additive manufacturing standards publications, patent databases for technology activity signals, and peer reviewed journals that discuss material qualification and part performance. Company filings, investor presentations, and reputable press were used to sense check product positioning and demand commentary, supported by paid subscriptions for company financials and news intelligence where it helped fill disclosure gaps. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the sizing logic and to confirm what is counted as SLS revenue across hardware, software, and services. We spoke with a mix of equipment and material ecosystem participants, service providers, and end users to validate adoption timing, typical buying cycles, and the practical split between prototyping and production parts across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 42% |

| Mid tier: 43% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 22% | Managers: 53% | Americas: 25% |

Market-Sizing & Forecasting

Market size is built using a top-down approach where additive manufacturing demand pools are reconstructed using manufacturing output signals, installed base direction, and adoption rates for powder bed processes, and then filtered to what is attributable to SLS spending. To keep the totals realistic, we also run selective bottom-up checks using sampled price bands and unit volumes for SLS systems, along with channel feedback on typical service revenue attachments.

Key inputs used in the model include SLS system shipment momentum, average selling price progression for industrial printers, powder material consumption per build and utilization ranges, penetration of SLS in aerospace, automotive, healthcare, and electronics workflows, and regional investment cycles that affect capital purchases. Where company disclosures are thin, gaps are handled through conservative ranges agreed during interviews, which are then narrowed using cross checks like patenting intensity and visible production ramp patterns. Forecasts are generated using scenario analysis supported by trend lines on the above variables, and the final curve is tuned after confirming expected constraints like qualification timelines for new materials and the pace of capacity additions at service bureaus.

Data Validation & Update Cycle

Outputs are validated through multiple cross checks, including comparing implied system demand with manufacturing activity indicators and checking whether revenue splits align with what respondents see in real buying decisions. Any major variance triggers a second pass on assumptions such as utilization, pricing, and regional adoption timing, followed by re-contacting a small set of experts when a mismatch stays unresolved.

Before sign-off, the model is reviewed in steps so that calculation logic, unit consistency, and currency handling are checked independently. Reports are refreshed annually, and interim updates are made when material events occur such as policy shifts, sharp pricing resets, or visible changes in capacity and demand. Right before delivery, a final update pass is completed so clients receive the latest view available at that time.

Mordor Intelligence's Selective Laser Sintering Market Size Measured Against Other Published Estimates

Published market sizes for selective laser sintering often do not match because the boundaries are set differently and the same spending can be counted in more than one way. Differences usually come from what is treated as SLS only, how services are captured, and which year and currency timing are used.

Shipment and pricing signals for industrial SLS systems, along with service bureau utilization checks, are the evidence points that tie Mordor Intelligence to a defined revenue pool of hardware, software, and services rather than a wider additive manufacturing bucket. Other estimates can drift when they blend adjacent powder bed processes, use aggressive adoption scenarios without re-checking utilization, or apply broad average prices that do not reflect the recent mix shift between polymer and metal capable platforms.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.81 B (2025) | |

| Global Consultancy A | USD 5.00 B (2025) | Uses a broader definition that appears to blend some adjacent powder bed fusion revenues into SLS, which can lift the 2025 value even if end-use demand is similar. |

| Industry Publisher B | USD 1.92 B (2024) | Anchors the market at an earlier base year and applies narrower counting that can understate services and software, and it also reflects a slower adoption path in its forecast window. |

The spread in values is mainly explained by scope boundaries, base-year choice, and how services and pricing are handled in the model. By keeping inputs connected to observable system demand, realistic utilization ranges, and clear inclusion rules, we can present a market number that buyers can trace back to repeatable steps.

Key Questions Answered in the Report

How big will selective laser sintering market revenues become by 2031?

The market is projected to reach USD 13.48 billion by 2031, expanding at an 18.69% CAGR from 2026.

Which end-user vertical is growing fastest?

Healthcare shows the highest forecast CAGR at 18.92% because reimbursed patient-specific implants drive premium pricing.

Why are desktop SLS printers gaining traction?

Sub-USD 20 000 price tags, standard electrical requirements, and automated powder-recycling features make in-house production viable for small labs and job shops.

What gap does AI process monitoring close?

Real-time defect detection lowers scrap from 8% to 3%, improves delivery reliability, and strengthens the business case for serial production.

Page last updated on: