3D Printing Materials And Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

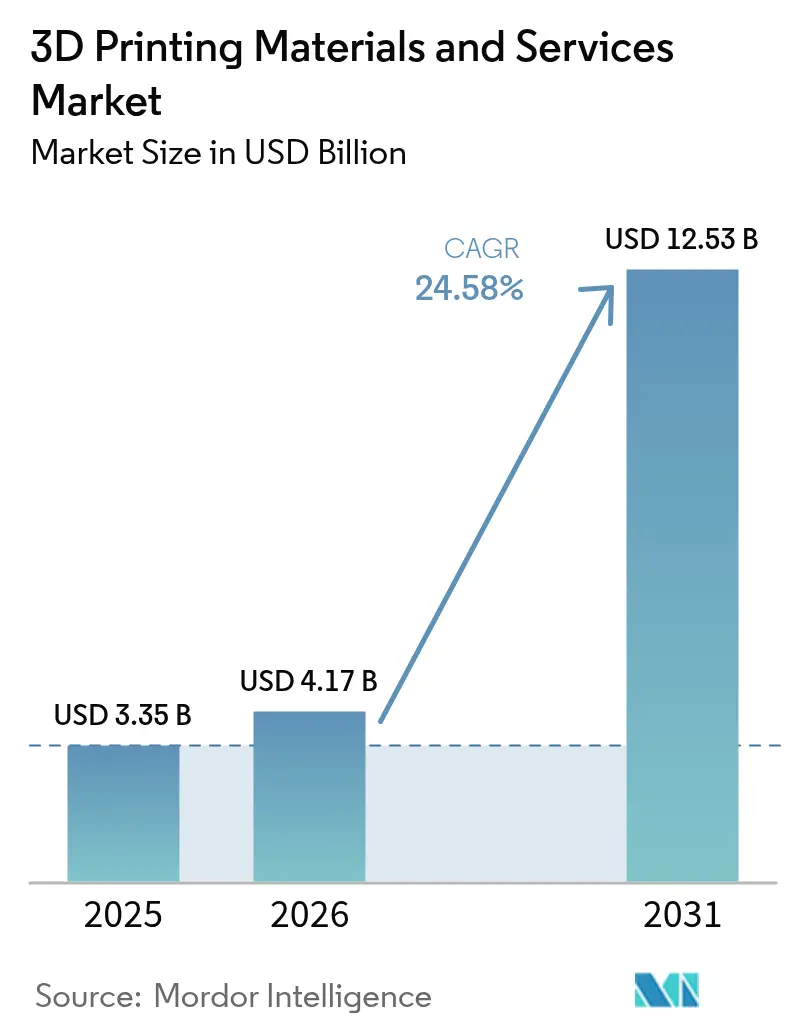

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 12.53 Billion |

| Growth Rate (2026 - 2031) | 24.58% CAGR |

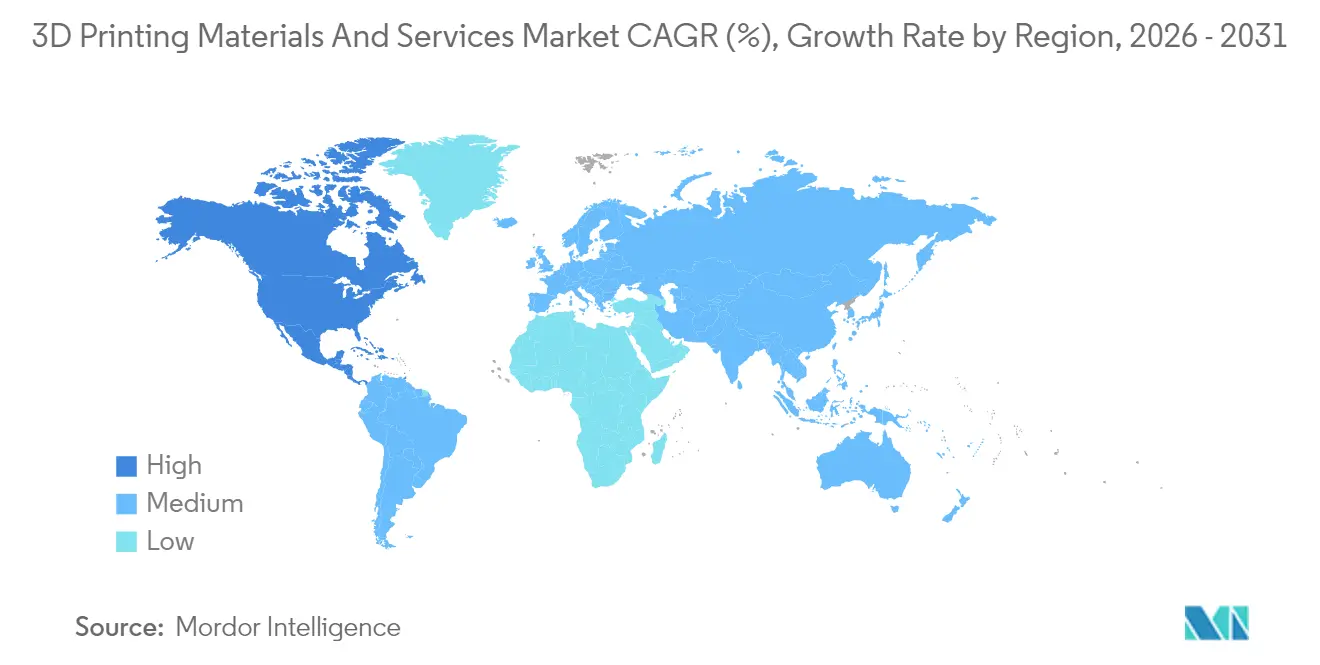

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printing Materials And Services Market Analysis by Mordor Intelligence

The 3D Printing Materials And Services Market size market is expected to grow from USD 3.35 billion in 2025 to USD 4.17 billion in 2026 and is forecast to reach USD 12.53 billion by 2031 at 24.58% CAGR over 2026-2031.

This growth reflects the steady shift from rapid prototyping to certified, production-grade uses in aerospace, healthcare and e-mobility. Demand is amplified by Print-as-a-Service subscriptions that let small and medium enterprises avoid large capital outlays, as well as by regulatory acceptance of metal additive manufacturing (AM) in flight-critical parts. Hybrid extrusion, bio-compatible polymers and recyclable filaments are widening the material palette, while cost-down pressures push manufacturers toward distributed, on-demand builds.

Momentum is supported by North American defense funding, EU Green Deal incentives and Asia Pacific’s digital manufacturing push. Services hold leadership with 58% revenue share in 2024 and also post the fastest 14% CAGR to 2030. FDM/FFF keeps the largest installed base, yet Multi Jet Fusion (MJF) and Binder Jetting are scaling 15% annually as their throughput and isotropic properties suit low-to-mid-volume production. Filament remains the dominant format, but powder usage is advancing 14% per year on the back of titanium and aluminum alloy adoption. Prototyping still commands 42% of revenue, though functional parts are increasing at 15% CAGR, particularly in aerospace where lightweight, consolidated structures shorten supply chains. Overall, the 3D printing materials and services market is entering a phase where certified production, sustainability and service models intersect to unlock new profit pools across industrial verticals.

Key Report Takeaways

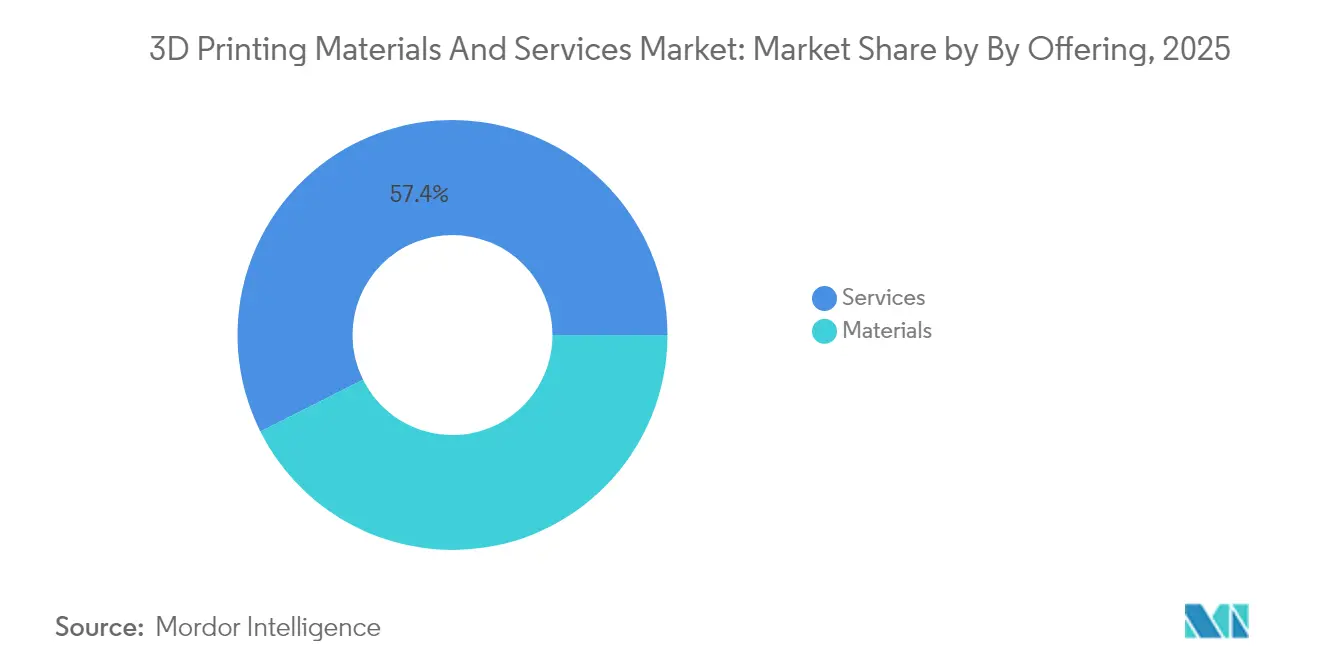

- By offering services, thecompanys captured 57.40% of the 3D printing materials and services market share in 2025; the segment is growing at a 13.55% CAGR through 2031.

- By technology, FDM/FFF led with 37.20% revenue share in 2025, while MJF and Binder Jetting are forecast to advance at a 13.20% CAGR between 2026-2031.

- By material form, filament commanded 47.10% of the 3D printing materials and services market size in 2025; powder formats are set to expand at a 12.90% CAGR to 2031.

- By application, prototyping held 41.30% revenue share in 2025; functional parts are the fastest-growing use at 13.40% CAGR through 2031.

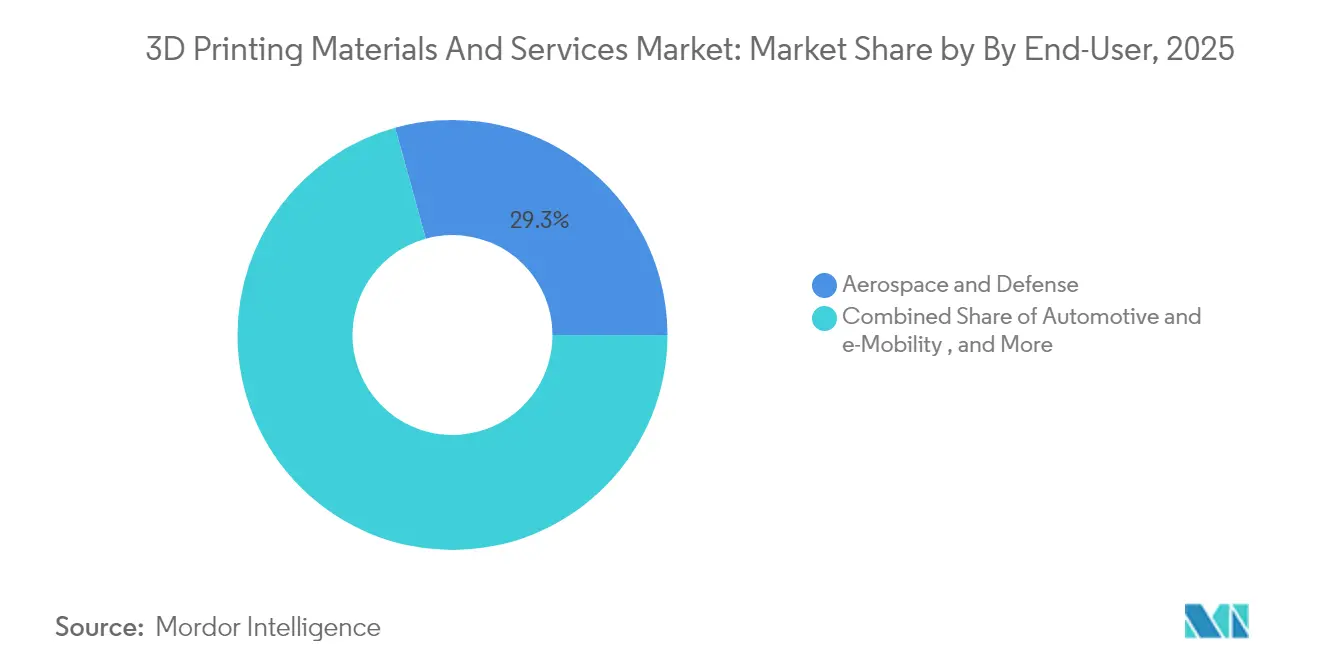

- By end-user, aerospace and defense represented 29.30% revenue share in 2025; healthcare is projected to grow at 13.30% CAGR from 2026-2031.

- Geographically, North America led with 39.20% revenue in 2025, while Asia Pacific is on track for a 14.45% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Printing Materials And Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of metal AM in aerospace | +7.20% | North America, Europe | Medium term (2-4 years) |

| Cost-down pressure fueling on-demand services | +5.80% | North America, Europe | Short term (≤ 2 years) |

| Bio-compatible polymers for point-of-care | +4.50% | Asia Pacific, North America | Medium term (2-4 years) |

| Hybrid extrusion for lightweight e-mobility | +3.10% | Europe, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of metal AM in aerospace

Regulators now accept certified metal AM parts for flight use. Materialise obtained EN 9100 accreditation in 2025, unlocking the supply of structural titanium and aluminum components that meet aerospace quality standards. Parallel U.S. defense programs with America Makes are standardizing qualification pathways, and 3D Systems has already delivered over 2,000 mission-critical titanium or aluminum components for space missions.[2]3D Systems Corporation, “3D Systems Produces Over 2,000 Flight Components,” 3dsystems.comThese milestones validate AM for safety-critical parts, accelerating procurement away from legacy castings.

Cost-down pressure fueling on-demand services

Inventory inflation and tooling costs have led manufacturers to outsource builds to distributed service bureaus. MX3D raised EUR 7 million in 2025 to scale Wire Arc AM on a Print-on-Demand model that cuts raw-material waste by up to 90%. Protolabs reported USD 83 million in 2024 3D-printing revenue, illustrating commercial traction for service-first models that compress lead time and free cash flow.

Bio-compatible polymers for point-of-care

Hospitals in Asia now print surgical guides and implants on site using validated resins and PEEK blends. Stratasys offers BoneMatrix and GelMatrix on its J850 platform to fabricate realistic anatomical models that reduce operating-room time. The healthcare segment is forecast to expand 17.5% annually, reflecting rising acceptance of patient-specific AM solutions across orthopedics and dentistry.

Hybrid extrusion for lightweight e-mobility

Combining carbon fiber PA with elastomers in a single build yields brackets and battery housings with higher stiffness-to-weight ratios. BMW produced 300,000 printed parts in 2023, including grippers that are 25% lighter, which lowered cycle times and CO₂ output. Such multi-material deposition supports drivetrain and interior applications where mass reduction translates directly to extended vehicle range.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of high-purity metal powder prices | -3.20% | Global, higher in Europe and North America | Medium term (2-4 years) |

| Limited qualification standards for critical parts | -2.80% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility of high-purity metal powder prices

Prices for titanium and copper powders swing with ore shortages and regulatory curbs, inflating bill-of-material costs for aerospace and medical builds. The titanium AM market is expected to reach USD 1.4 billion by 2032, yet supply instability forces OEMs to stockpile feedstock and recycle scrap to maintain margins, especially in Europe, where energy tariffs are high.

Energy-intensive post-processing inflating TCO

Support removal, heat treatment and surface finishing can account for one-third of energy use. Studies note that optimizing FFF parameters can cut consumption by up to 72%, but small firms often lack the capital for closed-loop systems, restraining wider adoption of the technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Sustain Dual Leadership

Services generated 57.40% of 2025 revenue and are expanding at a 13.55% CAGR as enterprises outsource design validation and low-volume production. The 3D printing materials and services market size for services stood at USD 1.92 billion in 2025 and is forecast to exceed USD 4.12 billion by 2031. Subscription packages from providers like 3Dock lower entry barriers for intermittent users. Materials, while smaller, fuel service innovation through higher-margin specialty powders and bio-polymers. The materials segment is growing 11.40% per year, propelled by powders for powder-bed fusion. Filament held the largest 47.10% share in 2025. HP’s halogen-free PA 12 FR illustrates how engineered polymers trim operating costs by 20% while meeting strict flame-retardancy norms. Advancements in recycled filament and composite pellets appeal to customers seeking lower environmental impact, reinforcing material-driven differentiation within service offerings.

By Technology: Emerging Methods Challenge FDM

FDM/FFF retained a 37.20% revenue share in 2025 through its vast installed base and accessible price point. The segment still registers 10.40% growth, but MJF and Binder Jetting are outpacing it at a 13.20% CAGR. These powder-based technologies deliver near-isotropic properties that suit jigs, fixtures, and low-to-mid-volume production runs. HP and INDO-MIM’s binder-jet partnership is scaling metal parts that pass aerospace validation, indicating readiness for serial output.

SLA, DLP, and SLS retain relevance for precision dental models and medical devices. EOS systems fabricate patient-specific cranial implants within days, enhancing hospital throughput. Wire Arc AM, currently niche, is gaining traction for large titanium structures in energy and maritime sectors, as demonstrated by MX3D’s funded expansion.

By Form (Materials): Powder Ascends

Filament dominated with 47.10% share in 2025, but powder formats are advancing 12.90% annually, reaching 33.20% share by 2031. The 3D printing materials and services market size for powders is projected to cross USD 3.55 billion by 2031 on the back of turbine blades, orthopedic implants and lightweight lattices produced via powder-bed fusion. Resin adoption is accelerating in dental and audiology niches, aided by bio-compatible, sterilizable chemistries that comply with ISO 10993. Resin system suppliers are also formulating plant-based feedstocks that answer EU directives on recyclability, demonstrating how sustainability imperatives steer material R&D.

By Application: Functional Parts Close the Gap

Prototyping preserved 41.30% of revenue in 2025, but functional parts printed in production-grade polymers and metals are rising at 13.40% CAGR. The 3D printing materials and services market share linked to functional parts is expected to reach 39.10% by 2031. Heat exchangers, satellite brackets and surgical implants illustrate the migration to end-use output. Tooling follows, with conformal-cooled injection molds and robot grippers saving lead time and weight. BMW cut 25% mass from grippers, lowering CO₂ per cycle and validating the ROI of printed tooling . Dental aligners and orthopedic inserts form another fast-growing niche, benefiting from rapid patient-specific design iterations.

By End-User: Healthcare Gains Momentum

Aerospace and defense led with 29.30% revenue in 2025, supported by GE Aerospace and Airbus investments. Certified metal AM shortens spare-part lead time and cuts buy-to-fly ratios. Healthcare, however, exhibits the quickest 13.30% CAGR as hospitals embrace point-of-care printing for anatomical models and implants. The 3D printing materials and services market size allocated to healthcare is set to climb from USD 0.46 billion in 2025 to USD 1.24 billion by 2031. Automotive and e-mobility customers leverage hybrid extrusion and MJF for brackets, housings and interior personalization. Consumer products, industrial equipment and construction represent smaller shares but are scaling as retailers test mass customization and builders deploy printed formwork for complex concrete pours.

Geography Analysis

North America accounted for 39.20% of 2025 revenue. Defense programs accelerate metal AM qualification, and GE Aerospace’s USD 1 billion capacity expansion will strengthen domestic AM supply chains. Hospitals adopt printed anatomical models that cut surgical time by up to 30%, adding healthcare pull. Europe holds the second-largest position, bolstered by Germany’s installed base and EU incentives for recyclable materials. Fraunhofer’s project that converts polypropylene waste to filament illustrates policy-driven innovation. Spain’s designation as Formnext 2025 partner country underscores the region’s manufacturing renaissance and export orientation. Asia Pacific is the fastest-growing region at 14.45% CAGR. China deploys AM for automotive, electronics, and hip implants, while Japan emphasizes precision tooling. Government grants, a deep manufacturing ecosystem, and rising healthcare spending underpin demand. Emerging markets in South America and the Middle East use AM for oil-and-gas spares and aerospace parts, providing additional, though smaller, growth nodes.

Regulatory Landscape

Regulation for 3D printing materials and services is anchored in application-specific frameworks, with medical devices and aerospace parts subject to established quality systems rather than standalone AM-only rules. For healthcare, the US FDA maintains device-focused guidance for 3D-printed medical devices, while authorities such as Singapore's Health Sciences Authority (HSA) and Swissmedic provide dedicated guidance covering design controls, validation, and traceability for 3D-printed devices. In pharmaceuticals, the European Medicines Agency (EMA) sets expectations that 3D printing equipment used for solid oral dosage forms is qualified and validated under EU GMP (including Annexes 11 and 15), reinforcing documentation and process-control requirements for AM-enabled manufacturing.

Standards continue to formalize digital-thread and qualification expectations across industrial AM workflows. ISO/ASTM 52959:2026 (published February 2026) defines requirements for compression validation specimens for additively manufactured metallic lattice designs, supporting more consistent mechanical validation approaches. ISO/ASTM 52951 (finalized June 2026) addresses data-package methods and parameter sets spanning design through acceptance, strengthening interoperability and auditability for qualified production. Sustainability-linked compliance also tightens for polymer feedstocks in Europe: EU Regulation 2025/2365 (November 12, 2025) introduces supply-chain requirements to prevent plastic pellet loss, with large operators (handling 1,500+ tonnes) required to demonstrate compliance to a certifier by December 17, 2027, adding operational controls relevant to pellet-based and converted polymer material streams used by AM suppliers and service bureaus.

Value Chain Analysis

The value chain spans feedstock production (polymers, resins, and metal powders), material conditioning and qualification, printing hardware and software ecosystems, service bureaus and OEM production cells, and downstream post-processing and inspection. Materials suppliers and powder producers depend on upstream mining and atomization for metals, and on polymer conversion for filaments and pellets, while industrial users increasingly consider resilience and local sourcing as part of supplier selection. In aerospace-grade titanium structures, qualification partnerships show how upstream process maturity and downstream certification connect, as in the June 2026 Cooperation and Research Agreement between Norsk Titanium and Airbus to mature Rapid Plasma Deposition for fatigue-critical structural titanium parts.

Midstream, printing platforms and software manage build preparation, parameter control, and traceability, then hand off parts to secondary operations such as support removal, heat treatment, surface finishing, and inspection. Post-processing remains a structural bottleneck for serial production because it is energy and labor intensive and often fragmented across equipment and vendors, limiting end-to-end workflow integration between printers, materials, and finishing. Material-portfolio expansion agreements also influence availability and qualification pathways, such as EOS partnering with Constellium (July 2026) to incorporate advanced aluminum alloys (including Aheadd CP1) into EOS materials, which supports broader industrial adoption where alloy availability, repeatable properties, and validated parameters are prerequisites.

Competitive Landscape

The field remains moderately fragmented. Top platforms include HP, Stratasys, 3D Systems, EOS, and Desktop Metal, yet consolidation is evident. Nano Dimension’s acquisition of Desktop Metal and Markforged combines complementary printer portfolios and material science competencies, signaling a pivot toward scale and standardization.

Differentiation depends on proprietary powders, recyclable polymers, and AI-driven print-parameter optimization. HP’s PA 12 FR exhibits 60% powder reusability and 20% lower TCO, reflecting the dual push for cost savings and sustainability. Service bureaus invest in simulation and automated post-processing to cut labor and guarantee repeatability. Start-ups focus on niche applications such as silicone bio-printing and large-format continuous-fiber composites, challenging incumbents on agility and domain expertise.

Innovation pipelines increasingly integrate sensor-based monitoring and machine-learning algorithms that predict part quality in real time. Vendors that combine hardware, qualified materials, software, and service ecosystems are best placed to capture subscription revenue across verticals.

3D Printing Materials And Services Industry Leaders

Ultimaker BV

3D Systems, Inc.

Höganäs AB

Arkema SA

Royal DSM (Covestro)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A prominent opportunity is scaling domestic, qualified metal powder and production capacity for defense and aerospace programs, where traceability and supply assurance factor into procurement. In the United States, America Makes and Department of Defense-backed initiatives support qualification pathways and broader program funding, while investments expand physical capacity across the ecosystem. In 2026, 6K Additive began expanding its Burgettstown, Pennsylvania campus to increase powder production capacity (from 200 to 1,000 metric tons), and Divergent Technologies announced a new 430,000 sq.ft. factory in Long Beach, California alongside its Monolith One metal 3D printer. Together, these moves broaden the industrial base for production-grade AM and related service demand.

Another whitespace is end-to-end production integration that reduces the post-processing and quality-assurance burden for repeatable serial manufacturing, particularly for regulated or safety-critical use cases. Factory software, digital-thread data packaging, and automated monitoring align with new ISO/ASTM activity, including ISO/ASTM 52951 finalized in June 2026, which formalizes data-package methods from design through acceptance and supports audit-ready workflows across distributed production networks. In healthcare, point-of-care printing remains constrained by validation and material biocompatibility requirements, creating room for suppliers offering validated resin and polymer systems that align with regulator expectations (FDA, HSA, Swissmedic) and ISO 10993, alongside service models that help hospitals and dental labs implement consistent process controls without building full in-house expertise.

Recent Industry Developments

- May 2026: UltiMaker launched the Factor 4 Plus industrial 3D printer aimed at continuous manufacturing and defense-oriented production use cases. The launch strengthens its position in higher-duty-cycle environments where repeatability, uptime, and controlled workflows influence printer selection and accompanying material sales.

- April 2026: 3D Systems introduced AddiTrak, an on-premises software platform for monitoring fleets and controlling processes in additive manufacturing operations. The release supports factory-scale deployment by improving traceability and process control across distributed printers, which is important for regulated and mission-critical production.

- May 2025: MX3D raised EUR 7 million to scale Wire Arc Additive Manufacturing (WAAM) capacity. The funding accelerates expansion of print-on-demand, large-part metal printing capabilities, broadening the addressable service market for industrial components where subtractive waste and lead times are key constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from 3D printing materials and 3D printing services used to make parts through additive manufacturing, across major end-user industries and regions. It includes commonly used printing materials and outsourced or in-house service revenues tied to printing activity.

Scope exclusions: It does not count 3D printer hardware sales or standalone software licenses unless they are bundled within a priced service engagement.

Segmentation Overview

- By Offering

- Materials

- Plastics (PLA, ABS/ASA, PETG, Photopolymers)

- Metals (Ti-6Al-4V, Inconel, AlSi10Mg, SS 316L)

- Ceramics (Alumina, Zirconia, Silicon Nitride)

- CompositesandOthers (Carbon-Fiber, Bio-Polymers)

- Services

- Rapid Prototyping

- ToolingandFixtures

- Production / Bridge Manufacturing

- DesignandEngineering Services

- Materials

- By Technology

- FDM / FFF

- SLS / SLA / DLP

- MJFandBinder Jetting

- DMLS / EBM / L-PBF

- Other Emerging (LCD, CLIP, WAAM)

- By Form (Materials)

- Filament

- Powder

- Liquid / Resin

- By Application

- Prototyping

- Functional Parts

- ToolingandMolds

- DentalandOrthopedic Implants

- By End-user

- AerospaceandDefense

- Automotiveande-Mobility

- HealthcareandLife Sciences

- Industrial Machinery

- Consumer ProductsandElectronics

- ConstructionandArchitecture

- By Geography

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- Rest of Asia Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with pinning down what is being counted as materials and what is being counted as services, and then mapping that to reported revenue pools and usage signals. For this market, we mainly used public sources that help anchor demand by industry activity and trade flows, such as US Census Bureau trade statistics, Eurostat manufacturing and trade tables, UN Comtrade, World Bank macro indicators, and OECD industrial production series.

We also reviewed annual reports and investor presentations of relevant suppliers and service providers, along with association websites, peer-reviewed journals covering additive manufacturing adoption, and reputable press releases on capacity expansions or new material qualifications. When company splits were not clear, we used a paid subscription for company financials and a paid patent database selectively, to cross-check business mix and innovation focus. These desk research sources are illustrative and not exhaustive, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test the pricing and volume assumptions that desk sources cannot fully explain, especially by technology and material family. We spoke with a mix of material suppliers, service bureaus, equipment ecosystem participants, and end-user procurement or engineering teams across APAC, EMEA, and the Americas. This helped ensure adoption timing and qualification cycles were reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 47% |

| Mid tier: 61% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 14% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach where additive manufacturing activity by end-use industry and region is reconstructed from manufacturing output signals, trade and production direction, and the practical penetration of 3D printing into prototyping and production use cases. Once the demand pool was formed, it was translated into revenues using a set of price and mix assumptions for key material families and common service types.

To keep the totals realistic, we then corroborated outputs using selective bottom-up checks, such as sampling material ASPs by form factor and application, rolling up service bureau revenue ranges where disclosed, and running channel checks on utilization and order patterns. Variables used as model inputs included the share of service revenue versus material revenue, the mix of metal versus polymer usage, technology adoption by major processes (such as FDM, SLS, SLA, DLP, and EBM), qualification lead times in regulated end uses, and regional manufacturing growth that drives part demand. Where bottom-up fragments had gaps, those areas were filled using conservative proxy ratios validated in interviews, followed by rebalancing to avoid over-counting between materials consumed and services billed.

Forecasts were produced using scenario analysis supported by expert consensus on adoption speed, material price progression (especially for metal powders and performance polymers), and the shift from prototyping toward low-volume production. Assumptions were stress-tested so that growth does not rely on one single end-use sector or one single technology trend.

Data Validation & Update Cycle

Triangulation was done by checking whether implied consumption and service revenue trends matched independent signals like industrial output direction, trade movement for relevant materials, and observed adoption changes shared by interviewees. When an output looked too high or too low for a region or technology, it was reviewed again, the driver assumptions were inspected, and follow-up outreach was triggered to confirm what changed.

Before sign-off, the model and written outputs go through a multi-step review so any variance against known market signals is explained and resolved. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp pricing shifts, regulation changes affecting qualification, or major capacity moves. Right before delivery, a final pass is completed so clients receive the most current view supported by the same repeatable steps.

Mordor Intelligence's 3d Printing Materials and Services Market Size Compared With Other Published Estimates

Published market numbers for this space can look far apart because the line between materials and services is not drawn the same way, and because some publishers widen the scope into adjacent revenue pools. Year labeling also matters, since some figures are calendar-year totals while others align to a base year used for modeling.

The main gap comes from whether printer hardware and standalone software are folded into the total. Mordor Intelligence counts only materials and service revenues tied directly to printing activity, and then checks the split using technology mix and service share indicators before finalizing totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.17 B (2026) | |

| Industry Research Publisher A | USD 23.41 B (2025) | Uses a wider definition that includes software and a broader ecosystem view, and it also cites a different base year, which lifts the headline value versus a materials-and-services-only total. |

| Trade Journal B | USD 15.90 B (2024) | Represents the total 3D printing market including printers along with materials and services, and the calendar-year framing can further shift comparisons versus a component-only market view. |

The table shows that most of the spread is explained by what gets included and how the year is set, rather than a simple disagreement on growth direction. By keeping the scope limited to materials plus services, and by tying assumptions to visible signals like service share, material mix, and technology adoption, the estimate stays easier to replicate and easier to audit across regions.

Key Questions Answered in the Report

What is the current value of the 3D printing materials and services market?

The market stands at USD 4.17 billion in 2026 and is forecast to reach USD 12.53 billion by 2031.

Which segment grows fastest within the market?

Services expand at 13.55% CAGR because Print-as-a-Service models remove large upfront equipment costs.

Why are MJF and Binder Jetting gaining share?

They deliver higher throughput and near-isotropic properties, supporting serialized production in automotive and consumer goods.

How are healthcare providers using 3D printing?

Hospitals use bio-compatible polymers to print patient-specific implants and anatomical models that can cut operating-room time by up to 30%.

What restrains wider AM adoption among small firms

High-purity metal powder price swings and the energy intensity of post-processing inflate total cost of ownership.

Page last updated on: