Direct Metal Laser Sintering 3D Printing Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

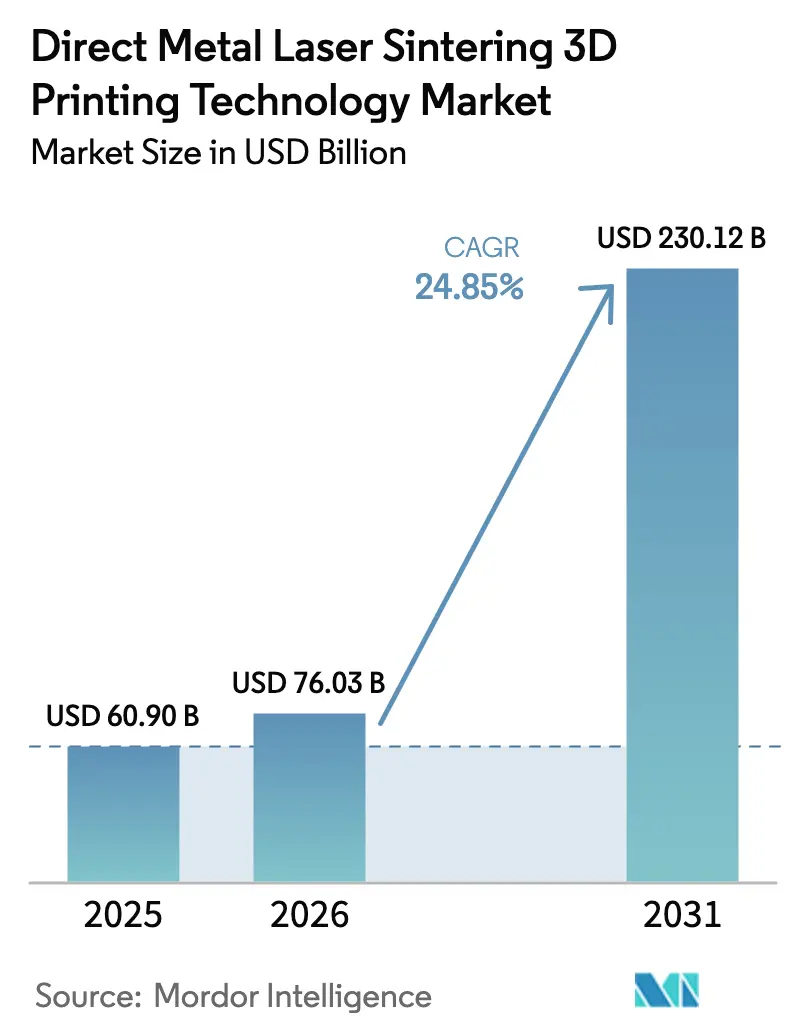

| Market Size (2026) | USD 76.03 Billion |

| Market Size (2031) | USD 230.12 Billion |

| Growth Rate (2026 - 2031) | 24.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct Metal Laser Sintering 3D Printing Technology Market Analysis by Mordor Intelligence

The direct metal laser sintering (DMLS) 3D printing technology market size was valued at USD 60.9 billion in 2025 and estimated to grow from USD 76.03 billion in 2026 to reach USD 230.12 billion by 2031, at a CAGR of 24.85% during the forecast period (2026-2031). Multi-laser architectures are enabling a step-change in productivity that is pushing DMLS from prototyping into mainstream serial production. Europe’s aerospace-focused manufacturing base is driving early adoption, while new build-volume classes and advanced monitoring systems are lifting part-quality confidence and widening the addressable application pool. Favorable industrial subsidies in Nordic countries are accelerating capital investment, whereas Asian manufacturers are matching pace through large-scale capacity additions and precision engineering capabilities. Meanwhile, titanium’s established performance credentials continue to anchor the materials mix, yet aluminum alloys are gaining share as electric-vehicle (EV) thermal-management designs migrate into serial output.

Key Report Takeaways

- By component, Systems captured 56.70% of the direct metal laser sintering (DMLS) 3D printing technology market share in 2025; Services are projected to expand at a 26.05% CAGR through 2031.

- By material type, titanium and titanium alloys led with 33.60% revenue share in 2025, while aluminum and aluminum alloys are forecast to grow at a 27.66% CAGR to 2031.

- By laser configuration, multi-laser systems held 47.60% of the direct metal laser sintering (DMLS) 3D printing technology market size in 2025; high-productivity systems (>4 lasers) are advancing at a 31.02% CAGR through 2031.

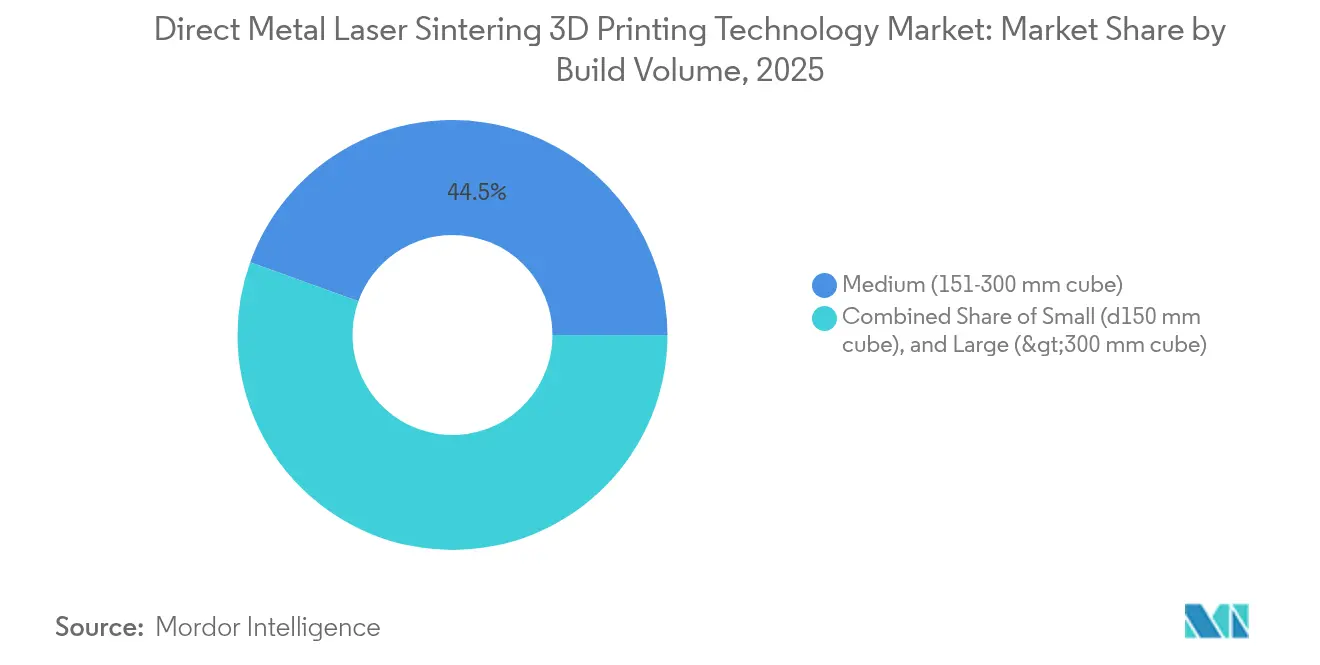

- By build volume, medium chambers (151–300 mm cube) held 44.50% of the direct metal laser sintering (DMLS) 3D printing technology market share in 2025, while large-format systems (>300 mm cube) accounted for 26.45%.

- By end-use industry, aerospace and defense commanded 38.30% share of the direct metal laser sintering (DMLS) 3D printing technology market size in 2025, whereas medical and dental applications are accelerating at a 26.02% CAGR.

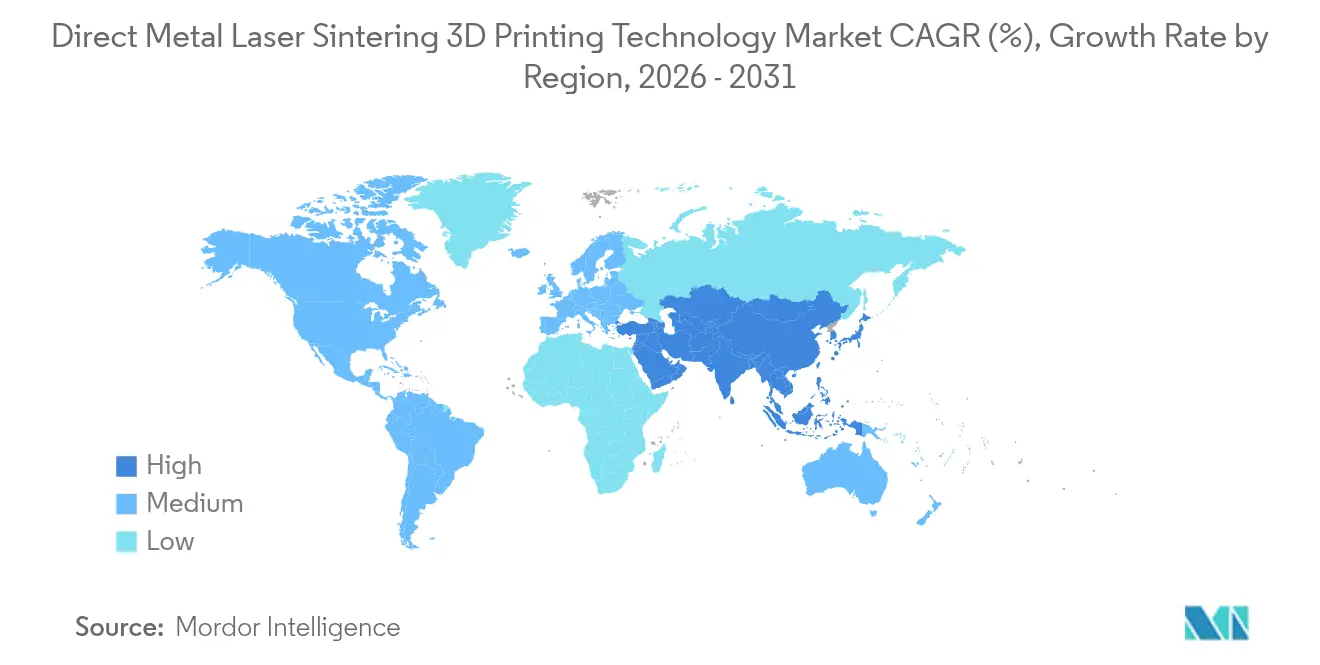

- By geography, Europe led with 34.70% revenue share in 2025, and Asia is positioned to record the fastest CAGR at 28.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Direct Metal Laser Sintering 3D Printing Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for lightweight aerospace parts | 6.30% | North America and Europe | Medium term (2-4 years) |

| Rising adoption in patient-specific implants | 5.10% | Asia; spillover to Europe | Medium term (2-4 years) |

| EV power-train momentum for Al and Cu components | 4.60% | Europe, North America, China | Long term (≥ 4 years) |

| Shift toward multi-laser large-format systems | 3.80% | Global; early in Europe and North America | Short term (≤ 2 years) |

| Government industrial 3D-printing subsidies | 3.00% | Middle East, Nordics, SE Asia | Medium term (2-4 years) |

| Post-COVID supply-chain resilience goals | 2.50% | Global; focus in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Lightweight Complex Metal Parts in Aerospace and Defense

Aerospace programmes are adopting DMLS to realise lattice structures and conformal cooling channels that remove up to 25% of component weight without compromising strength. SpaceX’s investment in DMLS for its Raptor 3 engine underlines the economic and performance upside of on-site additive production. Defence primes mirror this trajectory, deploying the technology for rapid prototyping and in-theatre spares, thereby shortening development cycles and logistics lead times.

Rising Adoption in Medical and Dental Implants Requiring Patient-Specific Titanium Structures

Healthcare providers in Asia are scaling DMLS capacity to address the growing need for customised implants, a trend supported by clinical evidence that laser-built Ti6Al4V shows superior porosity and osseointegration [1]Wei Long, Jia An & Chee Kai Chua, “Process, Material, and Regulatory Considerations for 3D-Printed Medical Devices and Tissue Constructs,” Engineering, doi.org. Regulatory bodies in Japan and South Korea have streamlined approval pathways for additively manufactured implants, encouraging local suppliers to expand production capability.

Momentum of Electric-Vehicle Power-train Development Accelerating Aluminum and Copper DMLS Components

EV OEMs exploit aluminum’s high thermal conductivity to design battery housings and e-motor cooling jackets. Pilot lines at European automotive plants demonstrate 30% part-count reduction and measurable range gains when generative design and DMLS convergence are applied. Component road-maps now earmark high-performance copper alloys for in-situ printed busbars.

Shift Toward Multi-Laser Large-Format Systems Enabling Cost-Effective Serial Production

Multi-laser configurations allow simultaneous exposure of larger powder-bed zones, cutting build time by 90%. Eplus3D’s 64-laser EP-M2050 sets the throughput benchmark and illustrates a capital-productivity equation that finally competes with CNC machining for medium-volume runs. Early adopters in aerospace are extending the machine’s availability to cross-functional production cells.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure and skilled-labour gap | −3.8% | Global; higher in emerging markets | Medium term (2-4 years) |

| Stringent powder-safety regulations in EU | −2.5% | European Union; global spillover | Short term (≤ 2 years) |

| Surface-finish and post-processing complexity | −2.0% | Global; automotive hubs | Medium term (2-4 years) |

| Volatility in spherical metal-powder prices | −1.3% | Global; regions without atomisers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Skilled-Labour Gap for Operating Metal Powder-Bed Fusion Lines

Industrial DMLS machines range from USD 100,000 to USD 1 million, excluding ancillary safety infrastructure. Training pipelines remain thin; three-quarters of surveyed manufacturers highlight a shortage of process engineers proficient in parameter optimisation. SMEs therefore outsource builds or defer adoption, slowing penetration outside Tier 1 supply chains.

Stringent Powder-Safety Regulations Elevating Compliance Costs

EU directives on metal-powder handling mandate explosion-proof ventilation and continuous dust monitoring, pushing compliance costs above capital expenditure for smaller shops. Post-processing vendors displayed enclosed depowdering and finishing cells at TCT 2025, signalling a commercial response yet adding an incremental investment layer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Hardware Growth

Services captured attention by scaling at a 26.05% CAGR, even as Systems retained 56.70% revenue in 2025. Uptake of design-for-additive consulting, parameter development and specialised post-processing reflects customers’ preference to contract expertise rather than commit to full plant investment. Global service bureaux now operate mixed fleets of single- and multi-laser units, enabling low-risk entry for new adopters while deepening recurring revenue for machine OEMs.

A maturing ecosystem of powder recyclers, software integrators and workflow-automation vendors supports broader market participation. The direct metal laser sintering (DMLS) 3D printing technology market size for Services is expected to close much of the present gap with hardware by 2031 as serial production programmes outsource overflow capacity. SMEs find service models particularly attractive, side-stepping high fixed costs until volumes justify captive lines.

By Material Type: Aluminum Alloys Challenge Titanium’s Dominance

Titanium and titanium alloys held a 33.60% share in 2025, underscoring their status as the default aerospace and medical materials. Surgeons favour titanium’s biocompatibility, while airframe builders leverage its strength-to-weight advantages for structural brackets. However, aluminum alloys are the fastest-moving category, projected to reach a 27.66% CAGR as EV power-train components migrate to additive routes. Thermal-management assemblies show weight savings and simplified part architectures, winning adoption across battery producers and e-motor suppliers.

The direct metal laser sintering (DMLS) 3D printing technology market share linked to aluminum will rise as large-format chambers accommodate bigger casings. Powder producers are scaling atomisation lines to stabilise input costs, and machine vendors have unlocked parameter sets that mitigate reflectivity issues. Concurrently, nickel superalloys, stainless steels and cobalt-chrome maintain niche relevance for high-temperature or wear-critical use cases, broadening material optionality for design engineers.

By Laser Configuration: High-Productivity Systems Transform Economics

Multi-laser systems accounted for 47.60% of 2025 shipments, reflecting industry consensus that throughput is key to cost parity with conventional machining. Early adapters confirm 30% cost-per-part reductions once four-laser or greater platforms enter production lines. The direct metal laser sintering (DMLS) 3D printing technology market size allocated to >4-laser configurations is forecast to expand at a 31.02% CAGR, reshaping ROI calculations for green-field factories.

Software partnerships now focus on synchronising beam overlap, real-time calibration and advanced tool-path strategies. As productivity rises, customers re-evaluate equipment footprints, integrating powder handling and depowdering within closed cells to raise utilisation. Single-laser machines retain footholds in RandD and boutique jewellery segments but cede share in mainstream industrial programmes.

By Build Volume: Large-Format Systems Enable New Applications

Medium build chambers (151–300 mm cube) captured 44.50% of 2025 revenue, offering a balanced proposition of cost and throughput, whereas large-format systems (>300 mm cube) represented 26.45% and are unlocking new aerospace and energy use cases such as turbine cases and satellite structures. Nonetheless, large-format systems exceeding 300 mm cube are unlocking new aerospace and energy use cases such as turbine cases and satellite components. Eplus3D’s EP-M2050 headline specification illustrates the productivity leap coupled with expanded part envelopes.

Demand for large parts drives material throughput, prompting powder suppliers to invest in bulk recycling and closed-loop handling. Small-volume printers remain vital for dental crowns and boutique medical devices, where precision and surface finish trump size. Across all volumes, workflow automation-from-powder-to-part is the differentiator, evidenced by integrated sieving and quality-assurance cameras that cut operator intervention.

By End-Use Industry: Medical Applications Challenge Aerospace Dominance

Aerospace and defense remained the largest user segment at 38.30% share in 2025, propelled by weight-saving imperatives and supply-chain localisation. Regulatory clearance for flight-critical DMLS parts accelerates as OEMs document repeatability across multi-laser platforms. Simultaneously, medical and dental applications chart the steepest growth curve at 26.02% CAGR, benefiting from titanium lattice structures that match patient anatomy and promote osseointegration.

Automotive stakeholders increasingly deploy DMLS for lightweight brackets, e-pump housings and tooling inserts with conformal channels. In the oil and gas sector, on-demand production of legacy spare parts cuts lead times by 50%. Academic consortia expand materials libraries and process maps, reducing time-to-qualification for new alloys and reinforcing the talent pipeline that the broader market relies upon.

Geography Analysis

Europe commanded 34.70% of global demand in 2025. Aerospace primes in Germany, France and the United Kingdom validate multi-laser workflows for structural parts, while Nordic incentive schemes co-fund capital acquisitions, creating a critical mass of equipment suppliers and service bureaux. Medical device clusters in Switzerland and the Benelux employ laser powder-bed fusion for patient-matched implants, leveraging proximity to regulatory authorities to accelerate product launches. Corporate sustainability agendas add momentum; Rolls-Royce now recycles retired Tornado components back into powder feedstock, closing the materials loop and reducing Scope 3 emissions.

Asia records the fastest regional CAGR at 28.32% through 2031. China scales domestic machine brands such as BLT and Eplus3D, aligning additive capacity with national aerospace programmes and EV supply chains. Japanese firms leverage precision-machining heritage to refine post-processing protocols, particularly in orthopaedics. India’s Ministry of MSME funds Technology Centres that introduce SMEs to DMLS workflows, broadening the adoption base . The direct metal laser sintering (DMLS) 3D printing technology market size attributable to Asia will therefore compound rapidly as localised powder production stabilises input costs.

North America maintains an innovation edge, supported by strong defence budgets and space-launch activity. Incodema3D expanded its fleet to 28 metal machines to meet aerospace and energy backlogs. Nikon’s Advanced Manufacturing Technology Centres in the United States provide application engineering for both powder-bed and directed-energy processes. The Middle East builds green-field aerospace clusters with state support, and selected African markets pilot additive repair cells for mining equipment, illustrating a gradual but broadening geographic participation.

Competitive Landscape

ompetitive intensity is moderate, with global machine OEMs, specialist material suppliers and software innovators converging on seamless end-to-end solutions. EOS, 3D Systems and Nikon SLM Solutions lead multi-laser hardware development and maintain direct sales channels into regulated industries. Challengers such as Velo3D differentiate via support-free build strategies, while Desktop Metal targets cost-per-part reductions through binder-jet hybrids. Corporate strategy increasingly revolves around ecosystem partnerships: Dyndrite’s collaboration with Nikon SLM Solutions embeds advanced tool-path generation that boosts volumetric build rates and time-to-validation.

Materials differentiation is another competitive lever. EOS expanded its superalloy range with IN738 and K500 to meet turbine and marine requirements[3]EOS, “EOS M 400 – 3D Printing for Industrial Production,” eos.info. Powder specialists are co-locating atomisation plants within machine-assembly facilities to guarantee feedstock quality, a vertical-integration trend mirrored by powder recycling companies that install within customer premises. Service bureaux invest in robotic depowdering and AI-enabled inspection to raise utilisation and capture premium aerospace contracts.

M&A momentum illustrates ongoing consolidation. Nano Dimension’s 2025 acquisitions of Desktop Metal and Markforged create a multi-modality additive conglomerate capable of cross-selling metal and polymer technologies, signalling a play for platform breadth and synergies in procurement, software and customer support. Strategic stakes in start-ups with process-monitoring IP aim to close the feedback loop between melt-pool analytics and closed-loop control, thereby lifting first-time-right yields.

Direct Metal Laser Sintering 3D Printing Technology Industry Leaders

EOS GmbH

3D Systems Corporation

General Electric (GE Additive/Concept Laser)

Trumpf GmbH + Co. KG

SLM Solutions Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AM Solutions showcased enclosed depowdering and finishing cells at TCT 2025, addressing surface finish hurdles for high-volume applications.

- March 2025: Nikon opened Advanced Manufacturing Technology Centres in the United States and Japan to deepen application engineering for powder-bed fusion and DED technologies.

- January 2025: EOS and AMEXCI entered a collaboration with Saab to advance metal additive manufacturing of defence components in Finland.

- January 2025: EOS installed its 5,000th industrial 3D printer at Keselowski Advanced Manufacturing in North Carolina, marking scale-up of production-grade powder-bed fusion lines.

Global Direct Metal Laser Sintering 3D Printing Technology Market Report Scope

Direct Metal Laser Sintering (DMLS) is a state-of-the-art 3D printing technology that produces metal parts through an additive manufacturing process. As a type of Selective Laser Melting (SLM), DMLS utilizes a high-powered laser to fuse fine metal powder particles layer by layer, creating a solid object.

The study tracks the revenue accrued through the sale of the direct metal laser sintering 3D printing technology market by various players across the globe. it also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The direct metal laser sintering 3D printing technology market is segmented by material type (titanium, aluminium, nickel, stainless steel, cobalt, and others), application (aerospace, medical, automotive, and other end users), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Systems |

| Materials (Metal Powders) |

| Services (Printing, Design, Post-Processing) |

| Titanium and Titanium Alloys |

| Aluminum and Aluminum Alloys |

| Nickel and Nickel Alloys |

| Stainless Steel |

| Cobalt-Chrome |

| Precious Metals |

| Tool Steels |

| Others |

| Single-Laser Systems |

| Multi-Laser Systems (2-4 Lasers) |

| High-Productivity Systems (>4 Lasers) |

| Small (<150 mm cube) |

| Medium (151-300 mm cube) |

| Large (>300 mm cube) |

| Aerospace and Defense |

| Medical and Dental |

| Automotive and Transportation |

| Industrial and Tooling |

| Oil and Gas and Energy |

| Jewelry and Art |

| Academic and Research Institutions |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific |

| By Component | Systems | |

| Materials (Metal Powders) | ||

| Services (Printing, Design, Post-Processing) | ||

| Titanium and Titanium Alloys | ||

| By Material Type | Aluminum and Aluminum Alloys | |

| Nickel and Nickel Alloys | ||

| Stainless Steel | ||

| Cobalt-Chrome | ||

| Precious Metals | ||

| Tool Steels | ||

| Others | ||

| Single-Laser Systems | ||

| By Laser Configuration | Multi-Laser Systems (2-4 Lasers) | |

| High-Productivity Systems (>4 Lasers) | ||

| By Build Volume | Small (<150 mm cube) | |

| Medium (151-300 mm cube) | ||

| Large (>300 mm cube) | ||

| By End-Use Industry | Aerospace and Defense | |

| Medical and Dental | ||

| Automotive and Transportation | ||

| Industrial and Tooling | ||

| Oil and Gas and Energy | ||

| Jewelry and Art | ||

| Academic and Research Institutions | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

Key Questions Answered in the Report

What is driving the rapid growth of the direct metal laser sintering (DMLS) 3D printing technology market?

Growth is propelled by multi-laser productivity gains, aerospace demand for lightweight parts, rising medical implant customisation, and supportive government subsidies, resulting in a 24.85% CAGR through 2031 (2026-2031).

Which region currently leads the market and which is growing fastest?

Europe holds 34.70% of global revenue, while Asia is the fastest-expanding region with a projected 28.32% CAGR as China and Japan scale capacity (2026-2031).

How are multi-laser systems changing the economics of metal additive manufacturing?

Platforms with four or more lasers reduce build times by up to 90%, lowering cost-per-part by roughly 30% and enabling economically viable serial production.

Why are aluminum alloys gaining traction against titanium in DMLS applications?

Aluminum offers superior thermal conductivity and lower mass, making it ideal for electric-vehicle power-train components; this segment is set to grow at a 27.66% CAGR to 2031 (2026-2031).

Page last updated on: