Security Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.22 Billion |

| Market Size (2031) | USD 37.82 Billion |

| Growth Rate (2026 - 2031) | 13.34% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

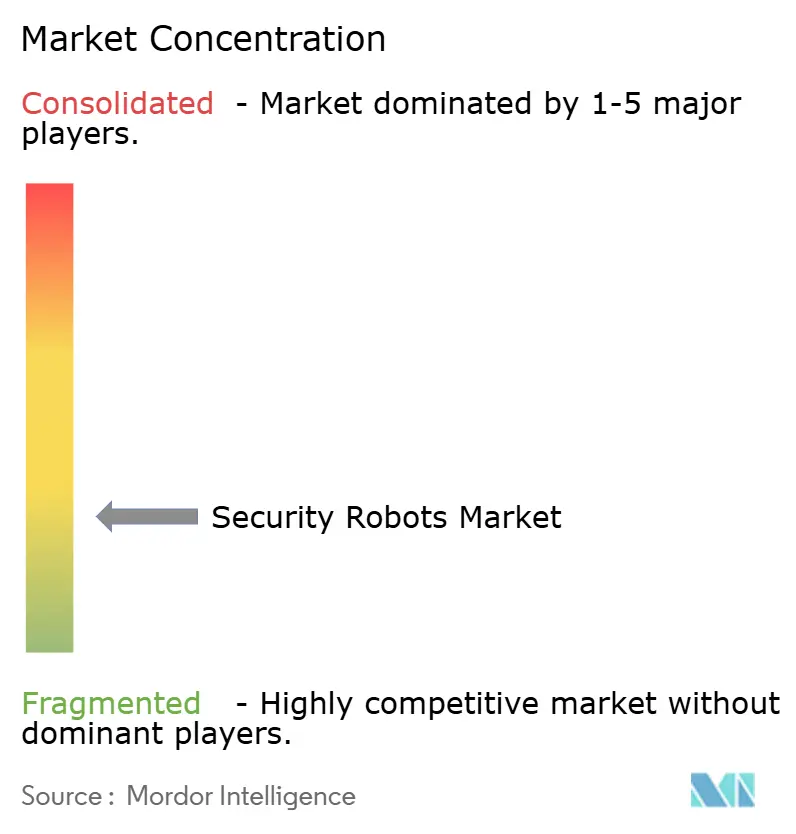

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Robots Market Analysis by Mordor Intelligence

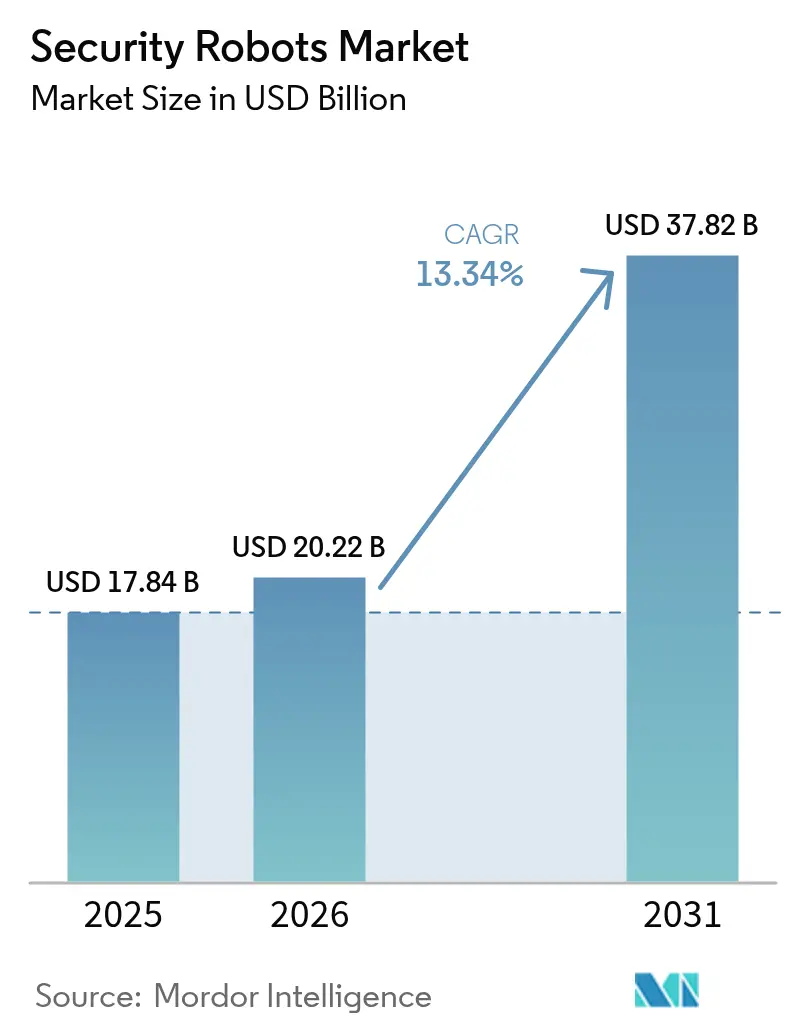

The Security Robots Market size is expected to increase from USD 17.84 billion in 2025 to USD 20.22 billion in 2026 and reach USD 37.82 billion by 2031, growing at a CAGR of 13.34% over 2026-2031. A fundamental shift away from labor-intensive guard patrols toward autonomous, AI-enabled machines is accelerating procurement across defense installations, energy assets, and commercial real estate portfolios. Sharp declines in sensor prices, advances in edge-AI compute, and favorable beyond-visual-line-of-sight (BVLOS) regulations are expanding use cases spanning subsurface intelligence, surveillance, and reconnaissance, indoor retail loss prevention, and offshore energy perimeter monitoring. Vendors are differentiating through perception software that cuts false-alarm rates, while robot-as-a-service (RaaS) contracts lower up-front capital outlays for cost-sensitive commercial operators. Heightened geopolitical tensions, record-high organized retail crime, and infrastructure modernization programs in the Indo-Pacific and Middle East reinforce sustained demand momentum through the forecast horizon.

Key Report Takeaways

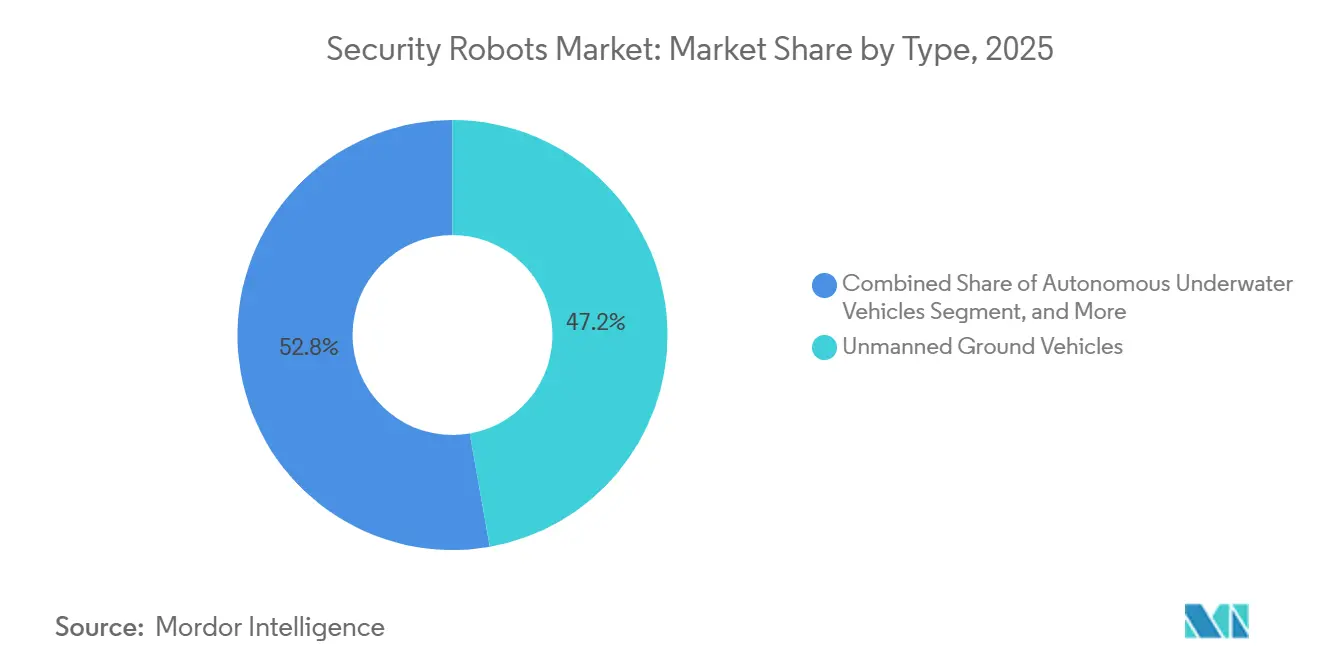

- By type, unmanned ground vehicles led with 47.23% of the security robots market share in 2025, while autonomous underwater vehicles are projected to grow at a 13.96% CAGR through 2031.

- By component, hardware dominated with 64.89% of 2025 sales, whereas the software and AI stack segment posts the highest forecast growth at 13.91% CAGR to 2031.

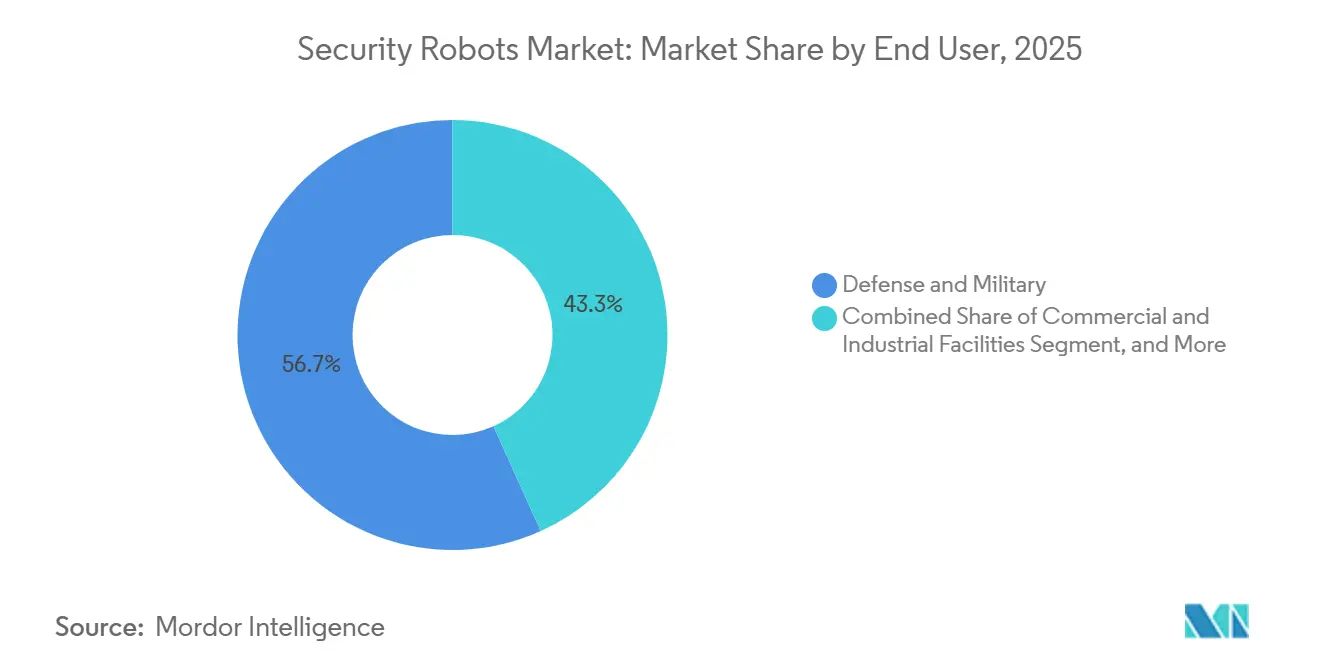

- By end user, defense and military accounted for 56.73% of the security robots market share in 2025, whereas commercial and industrial facilities are set to expand at a 14.16% CAGR over the same period.

- By application, patrolling and surveillance captured 48.91% of 2025 revenue, while spying and reconnaissance are advancing the fastest at a 14.33% CAGR.

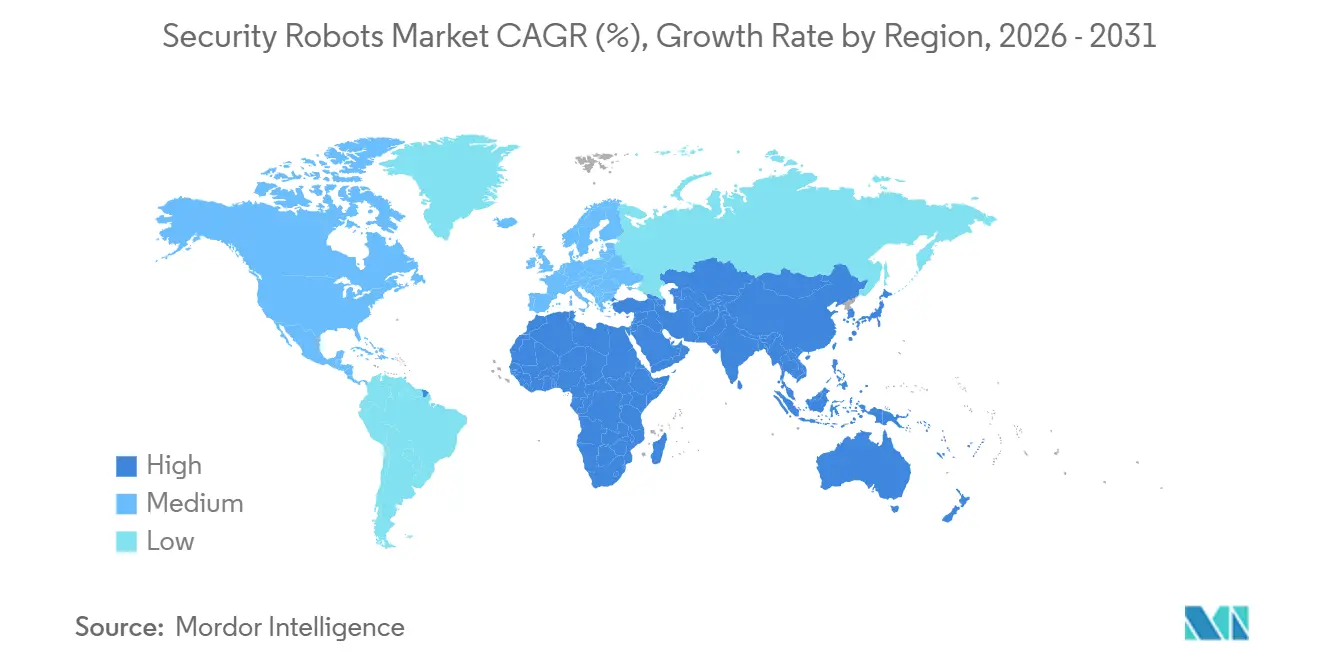

- By geography, North America accounted for 37.83% of 2025 turnover, but the Middle East is expected to log the fastest growth at a 14.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Robots Market Trends and Insights

Drivers Impact AnalysisDrivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deployment of AI-enabled perception stacks lowering false-alarm rates in critical infrastructure | +2.8% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Expansion of civilian BVLOS drone corridors for security patrols | +2.3% | North America, Australia, Middle East | Short term (≤ 2 years) |

| Mandates for perimeter intrusion detection at energy assets | +2.1% | Middle East, North America, Asia Pacific | Medium term (2-4 years) |

| Adoption of robot-as-a-service by commercial real-estate operators | +1.9% | North America, Europe, Asia Pacific urban centers | Short term (≤ 2 years) |

| Accelerated demand for indoor UGVs triggered by retail shrink crisis | +1.7% | North America, Europe | Short term (≤ 2 years) |

| Growing naval budgets for autonomous underwater ISR | +1.5% | United States, Australia, Japan, South Korea, NATO allies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deployment of AI-Enabled Perception Stacks Lowering False-Alarm Rates in Critical Infrastructure

Critical-infrastructure owners are replacing rule-based motion detection with multimodal perception systems that fuse thermal, visible-light, and radar inputs. MOBOTIX field tests at European utility substations cut false positives by 70% in 2024, freeing control-room staff to investigate validated alerts. Edge inference on NVIDIA Jetson modules eliminates cloud latency and supports air-gapped defense sites. Updated 2025 guidelines from the United States Department of Energy mandate AI-verified intrusion detection at Category I nuclear facilities, accelerating purchase cycles.[1]U.S. Department of Energy, “Physical Security Equipment Action Group Guidelines,” energy.gov Insurance carriers now offer premium discounts to facilities that deploy certified AI perception, creating an economic catalyst beyond operational efficiency.

Expansion of Civilian BVLOS Drone Corridors for Security Patrols

The United States Federal Aviation Administration approved routine BVLOS operations in 2024, letting utilities, border agencies, and pipeline operators monitor linear assets without manned chase aircraft.[2]Federal Aviation Administration, “Beyond Visual Line of Sight Operations,” faa.gov Australia’s Civil Aviation Safety Authority enacted a similar BVLOS framework in 2025, widening drone-patrol coverage for remote mining sites and offshore oil platforms. ASTM International’s F3411 remote-identification standard calms public-safety concerns by requiring real-time broadcast of drone ID and telemetry. Shield AI’s V-BAT platform, which won a multi-year United States Army perimeter-surveillance contract in 2025, exemplifies military validation spilling into civilian procurement. The alignment of regulation, standards, and field-proven technology is shrinking adoption timelines across energy, transportation, and defense sectors.

Mandates for Perimeter Intrusion Detection at Energy Assets

Drone incursions at Saudi Aramco sites and ransomware attacks on United States pipelines prompted new security mandates. Saudi Arabia’s National Cybersecurity Authority issued 2025 directives that tie operating licenses for energy facilities to compliance with autonomous-patrol requirements. The United States Transportation Security Administration’s 2024 pipeline guidelines recommend 24/7 perimeter monitoring, pushing operators toward hybrid ground- and aerial-patrol robots. Compliance windows of 18-36 months are driving a near-term backlog for ruggedized platforms that can withstand desert heat, coastal humidity, and corrosive environments.

Adoption of Robot-as-a-Service by Commercial Real-Estate Operators

Commercial landlords are exchanging costly guard contracts for subscription models that bundle hardware, software, and remote monitoring. Knightscope’s K5 leases at roughly USD 7 per hour, beating fully loaded human labor in major United States metros. Cobalt Robotics expanded its RaaS footprint in 2025 via a partnership with HITEK AI, installing indoor patrol robots across data centers and corporate campuses. The vendor-owned approach shields property managers from capex risk and guarantees hardware refresh cycles, aligning with corporate directives to keep security spending off the balance sheet.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented radio-frequency spectrum regulations limiting multi-robot fleets | -1.8% | Global, acute in Europe and Asia Pacific | Medium term (2-4 years) |

| Public backlash against face-recognition patrol bots in municipal deployments | -1.5% | North America, Europe | Short term (≤ 2 years) |

| High total cost of ruggedized all-terrain platforms for petro-chemical sites | -1.2% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Cyber-hardening gaps exposing C2 links to spoofing and jamming | -1.1% | Global, heightened in contested regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Radio-Frequency Spectrum Regulations Limiting Multi-Robot Fleets

Swarm intelligence demands low-latency links, yet radio-frequency allocations vary widely. The International Telecommunication Union’s 2023 conference earmarked 5.9 GHz for vehicle networking in some regions, while others dedicate it to Wi-Fi, forcing security-robot vendors to design multiple radio configurations.[3]International Telecommunication Union, “World Radiocommunication Conference 2023 Final Acts,” itu.int European Union members apply divergent rules to sub-1 GHz industrial bands, inflating certification costs and delaying cross-border rollouts. Until bodies such as ETSI finalize harmonized bands, operators will face greater integration complexity and reduced economies of scale.

Public Backlash Against Face-Recognition Patrol Bots in Municipal Deployments

Local governments and privacy advocates oppose biometric surveillance. San Francisco banned the city's use of facial recognition in 2019, a rule still in force and mirrored by Oakland and Berkeley. The European Union Artificial Intelligence Act, finalized in 2024, classifies real-time biometric ID in public spaces as high-risk, subjecting deployments to rigorous conformity assessments. Retailers and property managers that field face-matching robots risk litigation and reputational harm, prompting a pivot toward anonymized tracking modes that sacrifice forensic value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Subsurface Platforms Gain On Naval Demand

Autonomous underwater vehicles, while only a minority slice today, are expanding at a 13.96% CAGR as navies seek persistent subsurface ISR capabilities. The FY 2026 United States Navy budget earmarked USD 257.5 million for extra-large AUVs, and Australia’s Ghost Shark aims for 60-day endurance by 2027. Unmanned ground vehicles nonetheless accounted for 47.23% of revenue in 2025, reflecting their versatility across indoor patrol, EOD missions, and perimeter sweeps. Boston Dynamics’ Spot won contracts with the New York Police Department and Singapore’s Home Team Science and Technology Agency, underscoring its adaptability to urban and industrial environments. Hybrid amphibious robots, capable of moving between beachheads and shallow waters, serve coastal LNG terminals and offshore wind farms yet face high acquisition costs exceeding USD 600,000.

The security robots market for underwater platforms is projected to grow sharply as allied Indo-Pacific navies expand undersea sensor grids. By contrast, ground-vehicle growth is moderating as installed bases mature, though refresh cycles focused on modular sensor payloads sustain a healthy replacement curve. Over the forecast period, platform interoperability with joint-domain command networks will become a decisive factor in contract awards, nudging vendors to adopt open-architecture standards.

By Component: Software Stack Surges As AI Matures

Hardware accounted for 64.89% of 2025 revenue, but perception, mapping, and fleet-orchestration software are expanding faster at a 13.91% CAGR. NVIDIA Jetson Orin modules now ship with Shield AI, Knightscope, and Anduril robots, providing 200 TOPS of edge AI compute for real-time detection. The security robots market share held by software subscriptions is climbing as customers pay recurring fees for over-the-air upgrades that sharpen accuracy and add functionality. Teledyne FLIR’s infrared modules remain ubiquitous, providing kilometer-scale detection in zero-lux environments.

Services installation, training, and remote monitoring remain a smaller but rising slice. The shift to robot-as-a-service shifts asset risk to vendors, increasing revenue from monthly fees rather than one-time sales. Compliance standards such as ISO 13482 influence service quality expectations, and early adopters reward vendors able to blend autonomous patrols with 24/7 human tele-ops for incident confirmation.

By End User: Commercial Uptake Accelerates Amid Retail Shrink

Defense and military buyers still control 56.73% of 2025 spend, animated by ordnance-disposal modernization and unmanned reconnaissance. Yet commercial and industrial facilities lead growth at 14.16% CAGR, spurred by organized retail crime that cost United States merchants USD 112 billion in 2024. Walmart and Target pilot shelf-scanning robots that double as after-hours patrol units, illustrating multipurpose ROI. Government and law-enforcement agencies occupy the middle tier, balancing security benefits against civil-liberty concerns. Residential estates form an embryonic niche limited by six-figure price tags and bespoke support needs.

As CFOs adopt operating expense models and insurers incentivize the use of autonomous patrols, the market for security robots on corporate campuses is poised for significant growth. While defense budgets remain robust, military procurement schedules are extending. This shift comes as militaries align their requirements with the evolving standards set by NATO, the Five Eyes alliance, and partners in the Indo-Pacific region.

By Application: Reconnaissance Surges On BVLOS Gains

Routine patrolling and surveillance accounted for 48.91% of 2025 revenue, but spying and reconnaissance earned the speed crown with a 14.33% CAGR. FAA BVLOS approval allows drones to monitor border zones and pipeline corridors without human chasers, cutting utilities' hourly costs by more than half. Knightscope’s K5 exceeded 2 million autonomous hours by mid-2025, proving reliability for repetitive rounds. Explosive-detection robots maintain steady defense demand; Northrop Grumman’s new EOD platform shipped to the United States Marine Corps in 2025. Search-and-rescue deployments rose after major disasters in 2024, with Japanese agencies using quadrupeds in quake debris.

Improvements in endurance and fortified encrypted command-and-control systems are pivotal for the market share of reconnaissance platforms in the security robots sector. Vendors are enhancing the investigative value for border forces and critical infrastructure owners by integrating AI-driven change-detection analytics. These analytics flag anomalous activities detected during consecutive drone passes.

Geography Analysis

North America commanded 37.83% of the security robots market share in 2025, supported by mature defense procurement, expanding retail robot-as-a-service rollouts, and the Federal Aviation Administration’s beyond-visual-line-of-sight framework. Regional spending is reinforced by the United States Navy’s multi-year budget for extra-large autonomous underwater vehicles and by Canadian mining operators that use unmanned ground vehicles at remote sites. Mexico is expanding drone surveillance along both borders through bilateral security assistance, broadening the addressable security robotics market across the continent. Competitive pilots at United States utility companies show that aerial robots can cut inspection costs by more than 40%, creating a strong economic case for continued investment. As cyber-hardening standards tighten, North American buyers increasingly favor platforms with encrypted command links and anti-jamming safeguards.

The Middle East is projected to grow at a 14.39% CAGR through 2031, the fastest pace among all regions. Saudi Arabia’s Vision 2030 mandates tie refinery and desalination plant licenses to compliance with autonomous patrol requirements, triggering immediate tenders for rugged hybrid platforms. The United Arab Emirates has field-tested unmanned ground vehicles for crowd management and maritime drones for port security, signaling government endorsement that de-risks private-sector adoption. Israel continues to export reconnaissance drones to neighboring states despite export-control checks, adding specialized payload demand such as loitering munitions for border surveillance.

Europe maintains a mid-tier share, driven by the United Kingdom, Germany, and France, yet growth lags due to stringent biometric-privacy rules under the European Union Artificial Intelligence Act. Germany’s security-technology guidelines require certified encryption for command-and-control links, extending vendor qualification cycles and favoring established defense primes. Asia Pacific shows rapid uptake in China, Japan, South Korea, and India as governments modernize border security and mitigate labor shortages; China alone has deployed thousands of patrol robots across major metro systems. South America and Africa remain nascent but rising, with Brazil’s rainforest monitoring program and South Africa’s private-security pilots illustrating early momentum. Currency constraints and import duties temper immediate volume in these emerging regions, but multilateral financing and falling hardware prices are expected to unlock additional orders over the forecast horizon.

Regulatory Landscape

Regulation for security robots is tightening around two themes: product safety for mobile and consumer-facing machines, and governance of high-risk AI and biometric functions. In the European Union, Regulation (EU) 2023/1230 (Machinery Regulation) and the General Product Safety Regulation (effective December 2024) raise compliance expectations for autonomous systems placed on the market. The EU Artificial Intelligence Act (finalized in 2024) also introduces stricter requirements for real-time biometric identification in public spaces, which affects patrol-robot configurations and deployment approvals. In the United States, oversight is split across federal agencies and state-level AI governance, with the U.S. Consumer Product Safety Commission (CPSC) providing safety-oriented guidance for robotic products and states such as Texas enacting AI governance laws in 2026. This adds to a fragmented compliance environment for vendors operating nationally.

Standards and country-specific security requirements are further shaping market access and platform architectures. ISO 31101:2023 provides a safety management framework for service robots operating in unstructured environments, and ISO 10218-1:2025 updates robotics safety requirements that influence integrators and facility operators. In China, GA/T 1776-2021 sets technical requirements for police robot systems, including mandated use of national cryptographic algorithms (SM2/SM3) for identity authentication and TLS 1.2+ for communications protection. That drives suppliers to engineer jurisdiction-specific cybersecurity stacks alongside physical safety and functional certification.

Value Chain Analysis

The security robots value chain runs from core subsystems (sensors, locomotion and actuators, compute and communications) through software layers (perception, autonomy, mapping, fleet orchestration) and into deployment services, including site assessment, integration with security operations centers, remote monitoring, maintenance, and training. Hardware differentiation is increasingly tied to ruggedization and payload modularity, while recurring value capture shifts toward the software and operations layer that connects heterogeneous fleets (UGVs, drones, and fixed sensors) with existing guard workflows. Robot-as-a-service models reinforce this shift by bundling hardware, software updates, and monitoring into subscriptions, and by aligning procurement requirements in critical infrastructure and defense around documentation, clearance, and lifecycle cyber-hardening.

Upstream dependencies and compliance constraints also affect sourcing and time-to-deploy. Vendors rely on specialist suppliers for thermal imaging modules, edge-AI accelerators, and secure radios, and they face added integration effort from differing spectrum rules, encryption requirements, and safety certification regimes across regions. Recent ecosystem moves point to the services-and-integration layer becoming a coordination point. Certis Group partnered with FieldAI in February 2026 to integrate autonomous robots into security operations (with FieldAI establishing a Singapore office for regional execution), and Asylon and NVIDIA announced a March 2026 collaboration around an AI analytics platform for robotic security using NVIDIA Jetson modules. Together, these announcements highlight how edge compute and managed operations are shaping delivered outcomes.

Competitive Landscape

The security robots arena is moderately concentrated, with the top five suppliers accounting for just under 60% of global revenue. Traditional defense primes Lockheed Martin, Northrop Grumman, BAE Systems, Thales, and Leonardo leverage longstanding command-and-control contracts to bundle autonomous ground, surface, and aerial platforms into integrated security offerings. Their installed base and security clearances provide switching-cost advantages, yet slower software-release cycles leave openings for faster-moving challengers.

Pure-play robotics firms such as Knightscope, Cobalt Robotics, Boston Dynamics, and Shield AI are expanding through flexible subscription pricing and rapid edge-AI updates. Knightscope’s November 2025 agreement with Allied Universal placed K5 patrol robots at 50 United States corporate campuses, demonstrating commercial scalability. Shield AI’s January 2026 follow-on contract for V-BAT drones with the United States Army adds a high-profile reference that resonates with critical infrastructure buyers seeking proven endurance and autonomous takeoff capabilities. Anduril Industries completed sea trials of its Ghost Shark extra-large underwater vehicle in December 2025, positioning the company for future naval tenders that value modular payload bays.

Component specialists also shape competitive dynamics. Teledyne FLIR secured an August 2025 order for thermal modules in unmanned surface vehicles, cementing its role as the infrared-sensor supplier of record for multiple platform builders. NVIDIA’s Jetson Orin chips power perception stacks across several vendors, shifting differentiation toward software algorithms and over-the-air feature unlocks. Emerging white-space niches such as amphibious robots for coastal energy assets and cyber-hardened radios resistant to spoofing are attracting start-ups that can iterate quickly without legacy baggage. As buyers prioritize open architectures and life-cycle encryption updates, suppliers that blend secure hardware with subscription-based AI software are best positioned to expand wallet share through 2031.

Security Robots Industry Leaders

Lockheed Martin Corp.

Northrop Grumman Corp.

Thales SA

BAE Systems plc

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is in the orchestration layer that links robots, drones, sensors, and access control into a unified security operations center workflow. This can reduce false alarms and improve incident response while supporting subscription monetization. The March 2026 Asylon and NVIDIA collaboration to introduce AI-powered analytics for robotic security on edge hardware is one concrete signal of active investment in this direction, and commercial programs that bundle patrol robots with remote monitoring under RaaS contracts further reinforce the use of delivered, managed outcomes. For vendors, this creates space to provide certified integrations such as video management systems, SOC ticketing, and incident reporting tied to measurable results, including reduced false positives and validated alerts in regulated environments.

Another opportunity is compliant, privacy-aware deployment models for public-sector and urban settings, where policy constraints are narrowing routine patrol and biometric surveillance use. In February 2026, the NYPD updated its impact and use policy for tactical robots to comply with Local Law 56 of 2025, explicitly restricting use cases such as routine patrol, crowd control, and biometric surveillance. The policy shift points to demand for governance features (audit logs, mode restrictions, and anonymized analytics) rather than mobility improvements alone. At the federal level in the United States, proposed legislation such as the American Security Robotics Act of 2026 (H.R. 8189 and S. 4235) and related bills focused on communications risk review (for example, H.R. 9129) open procurement channels for suppliers that can show cybersecurity, trusted supply chains, and secure communications for government buyers while allowing commercial adopters to align to comparable security baselines.

Recent Industry Developments

- June 2026: Lockheed Martin demonstrated an intercept of a Group 3 drone target using the Sanctum counter-UAS battle manager with a GRIZZLY containerized launcher. The test points to containerized, rapidly deployable counter-drone robotics and autonomy software being emphasized for deployment around critical infrastructure and expeditionary sites.

- January 2026: Shield AI won a USD 45 million follow-on contract from the United States Army to deploy V-BAT reconnaissance drones across additional forward operating bases in Europe and the Indo-Pacific. The award strengthens military validation for autonomous ISR platforms and supports broader procurement confidence for BVLOS-style perimeter and reconnaissance missions.

- December 2024: MOBOTIX reported field tests at European utility substations in which multimodal perception reduced false positives by 70%. The result reflects how perception software and sensor fusion are becoming decisive procurement criteria for critical infrastructure operators seeking to cut alarm fatigue and reduce monitoring labor.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks revenues generated from robots used to deter, detect, and respond to security threats through patrol, surveillance, inspection, and incident support, across defense, public safety, and commercial sites worldwide.

Scope exclusions: We exclude standard fixed CCTV, non-robotic alarms and access control hardware, and purely manual security guarding labor.

Segmentation Overview

- By Type

- Unmanned Ground Vehicles

- Autonomous Underwater Vehicles

- Hybrid Amphibious Robots

- By Component

- Hardware

- Software and AI Stack

- Services

- By End User

- Defense and Military

- Government and Law-Enforcement

- Commercial and Industrial Facilities

- Residential and Private Estates

- By Application

- Patrolling and Surveillance

- Explosive Detection and Disposal

- Spying and Reconnaissance

- Search and Rescue Disaster Response

- Fire and Hazardous-Environment Response

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to collect anchors that can be checked repeatedly. We referenced public sources such as defense and public safety procurement portals, customs and trade statistics for relevant robotics and sensor categories, and standards and guidance notes from bodies such as ISO and IEEE. We also reviewed robotics publications in peer-reviewed journals. When needed, we checked patents databases to understand which robot form factors were moving from prototypes into productized security use cases.

On the commercial side, we also used company filings, investor presentations, product documentation, and credible press coverage to map typical deployments and pricing patterns, including subscription-style service bundles. Select paid subscriptions were used only for company financials and intelligence, news and financials, and patents lookups, to cross-check timelines and reported revenue direction. These desk research sources are illustrative only, and additional public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how security robots are actually bought and deployed, and what is counted as a security robot program versus adjacent automation. We spoke with a mix of manufacturers, integrators, security service providers, and end users across APAC, EMEA, and the Americas. Follow-up checks then helped confirm unit volumes, typical contract lengths, and attach rates for software and services.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 41% |

| Mid tier: 57% | Functional/Unit leaders: 43% | EMEA: 34% |

| Smaller Players: 15% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing started with a top-down reconstruction of the demand pool, using defense and public safety procurement signals, commercial facility security spending patterns, and observable deployment intensity to translate into robot adoption and replacement cycles. We then corroborated the totals with selective bottom-up approximations, including sampled unit shipments by robot type, typical ASP bands by application, and channel checks on software and service attach rates, before adjusting final numbers.

Key inputs used to keep the model grounded included robot type mix (UGV, AUV, and hybrid amphibious), application mix (patrolling and surveillance, EOD, reconnaissance, and fire or hazardous response), and component split across hardware, software and the AI stack, and services. We also tracked indicators like the share of projects sold as multi-year service bundles, autonomy level expectations, and the pace of new tenders in critical infrastructure and government sites, since these influence recognized revenues year to year.

For forecasting, we used scenario analysis supported by expert consensus on adoption speed by end user and region, then smoothed the curve using time series checks so it does not jump unrealistically. Where bottom-up inputs had gaps, we used conservative ranges for unit volumes and ASP and re-validated through additional primary callbacks when the implied totals moved outside normal procurement or deployment patterns.

Data Validation & Update Cycle

Outputs were triangulated across independent signals, including procurement activity, reported deployments, product pricing logic, and the implied split between hardware and recurring software or services. When variances were large, we reviewed them step by step, rechecking assumptions, re-running currency conversions using consistent timing, and challenging outliers with another layer of analyst review before sign-off.

The report is refreshed annually, and interim updates are made when material events change demand or pricing, such as major policy moves, defense budget shifts, or step changes in commercial adoption. Before delivery, a final pass is completed so clients receive the latest market view with assumptions that still align to current signals.

Mordor Intelligence's Security Robots Market Sizing Compared With Other Published Estimates

Published security robots market estimates can vary widely, even when the topic name looks the same. The gaps usually come from what each study counts as a security robot program, the year used as the anchor, and how recurring software and service revenue is treated.

Non-robotic surveillance infrastructure and routine guarding services sit outside Mordor Intelligence's scope, and that inclusion choice often explains why some published figures land higher even before forecasting assumptions are applied. Differences also show up when sources blend defense-focused platforms with broader mobile robotics, or when currency timing and inflation treatment do not match the contract and delivery calendar that drives recognized revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.22 B (2026) | |

| Global Consultancy A | USD 16.51 B (2025) | Uses an earlier anchor year and appears to apply a different treatment of recurring software and service revenues, which can shift totals when multi-year contracts are common. |

| Industry Publisher B | USD 13.70 B (2025) | Often groups security robots using a narrower demand lens and may undercount defense and government deployments, especially where procurement cycles delay recognition and published unit assumptions stay conservative. |

Across the three figures, most of the spread is explained by scope perimeter and the year used for the stated market value, followed by how service bundles are converted into annual revenues. By tying the total to repeatable signals like tenders, deployment intensity, and realistic pricing bands by robot type and application, the estimate stays traceable and practical to recreate.

Key Questions Answered in the Report

How fast is the security robots market expected to grow between 2026 and 2031?

It is forecast to register a 13.34% CAGR, climbing from USD 20.22 billion in 2026 to USD 37.82 billion by 2031.

Which platform type is growing the quickest?

Autonomous underwater vehicles post the fastest trajectory, advancing at a 13.96% CAGR on the back of expanding naval ISR budgets.

Why are commercial facilities accelerating adoption?

Retail shrink hit USD 112 billion in 2024, pushing merchants toward indoor ground robots that deter theft while robot-as-a-service pricing avoids up-front capex.

What is driving security-robot uptake in the Middle East?

Vision 2030 infrastructure projects and cybersecurity mandates that tie energy-site licenses to autonomous patrol compliance create urgent demand.

How does robot-as-a-service benefit property managers?

RaaS turns hardware ownership into a monthly operating expense, includes software updates, and eliminates technology-obsolescence risk.

Which restraint most hampers urban deployments?

Public backlash against facial recognition in patrol bots has led cities such as San Francisco to ban biometric surveillance on municipal property.

Page last updated on: