Seaweed-Based Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

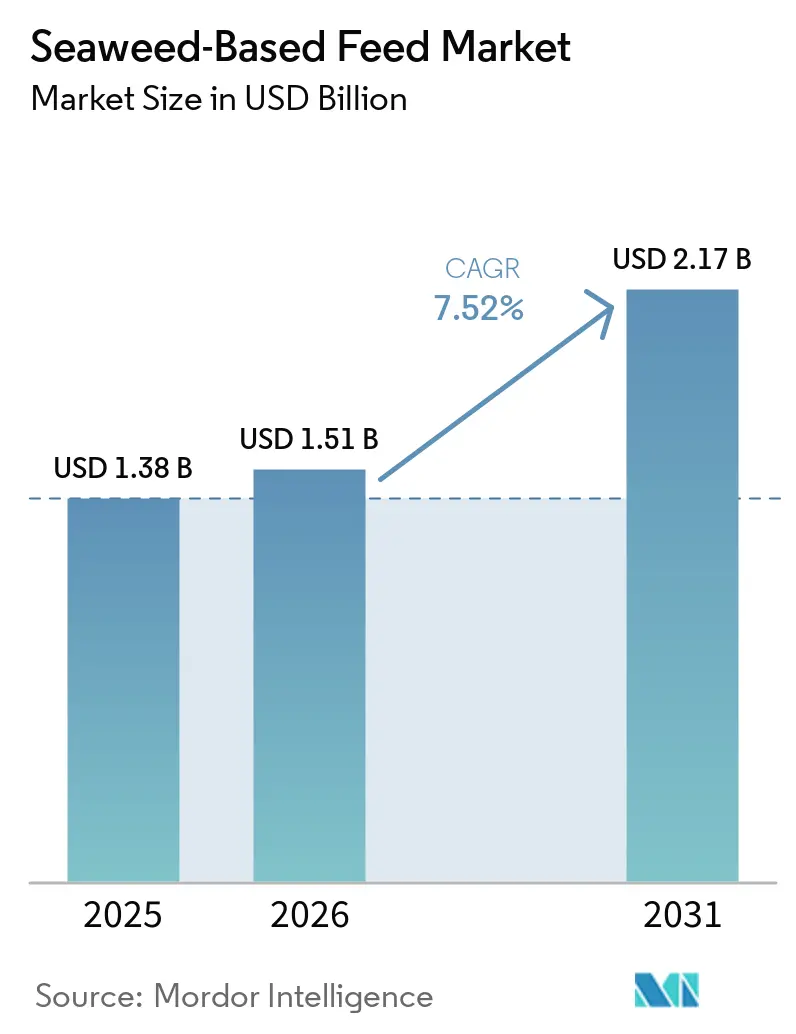

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seaweed-Based Feed Market Analysis by Mordor Intelligence

The seaweed-based feed market was valued at USD 1.38 billion in 2025 and is projected to grow from USD 1.51 billion in 2026 to USD 2.17 billion by 2031, registering a CAGR of 7.52% during the forecast period (2026-2031). Marine macroalgae are increasingly recognized for their potential to reduce greenhouse gas emissions and serve as a source of trace minerals. These algae are gaining attention due to their ability to improve livestock health and productivity while addressing environmental concerns. In countries such as Norway, Chile, and Japan, brown seaweed extracts rich in fucoidan and laminarin are being used as alternatives to antibiotic growth promoters in aquafeeds, contributing to sustainable aquaculture practices. Procurement in this market is primarily driven by direct business-to-business contracts, underscoring the importance of traceable supply chains to ensure quality and regulatory compliance.

Key Report Takeaways

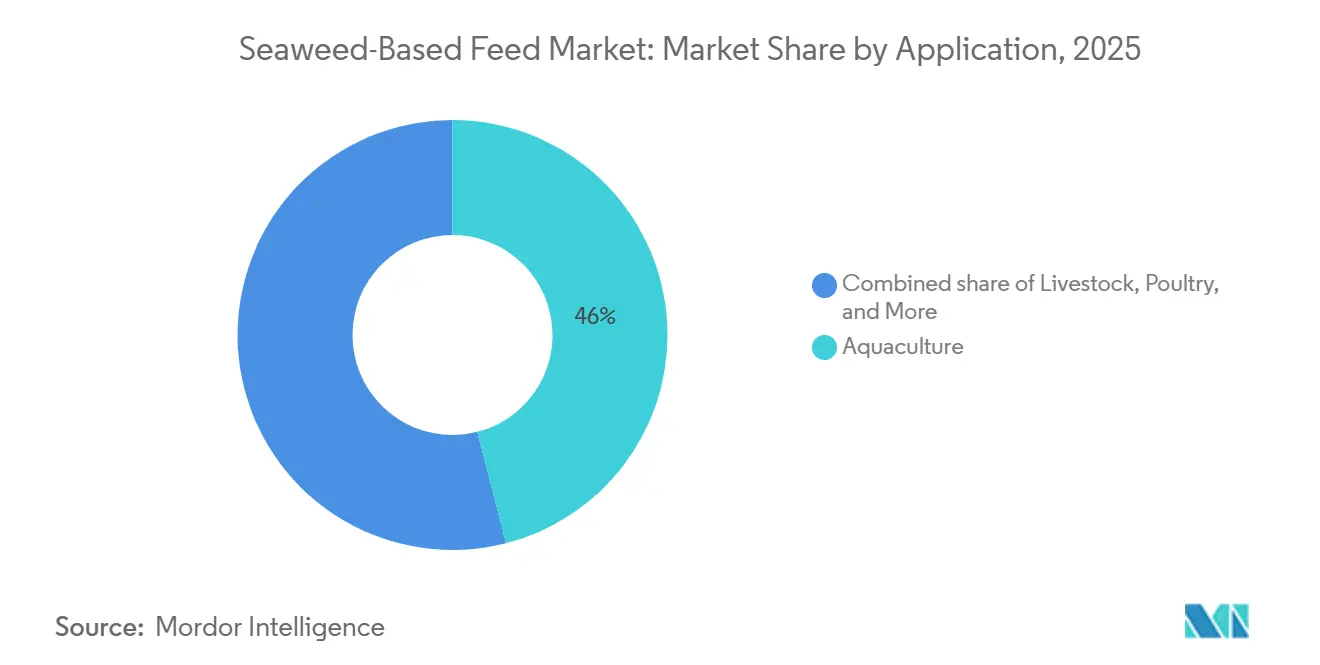

- By application, aquaculture held the largest share, accounting for 46% of seaweed-based feed market size in 2025, while livestock is projected to expand at a fastest 12.3% CAGR between 2026-2031.

- By species, brown seaweed commanded largest 42% share of seaweed-based feed market size in 2025, whereas red seaweed is forecast to register the fastest 13.1% CAGR through 2026-2031.

- By form, powder dominated with largest 51% share of seaweed-based feed market size in 2025, whereas liquid extract is set to rise at the fastest 13.9% CAGR over 2026-2031.

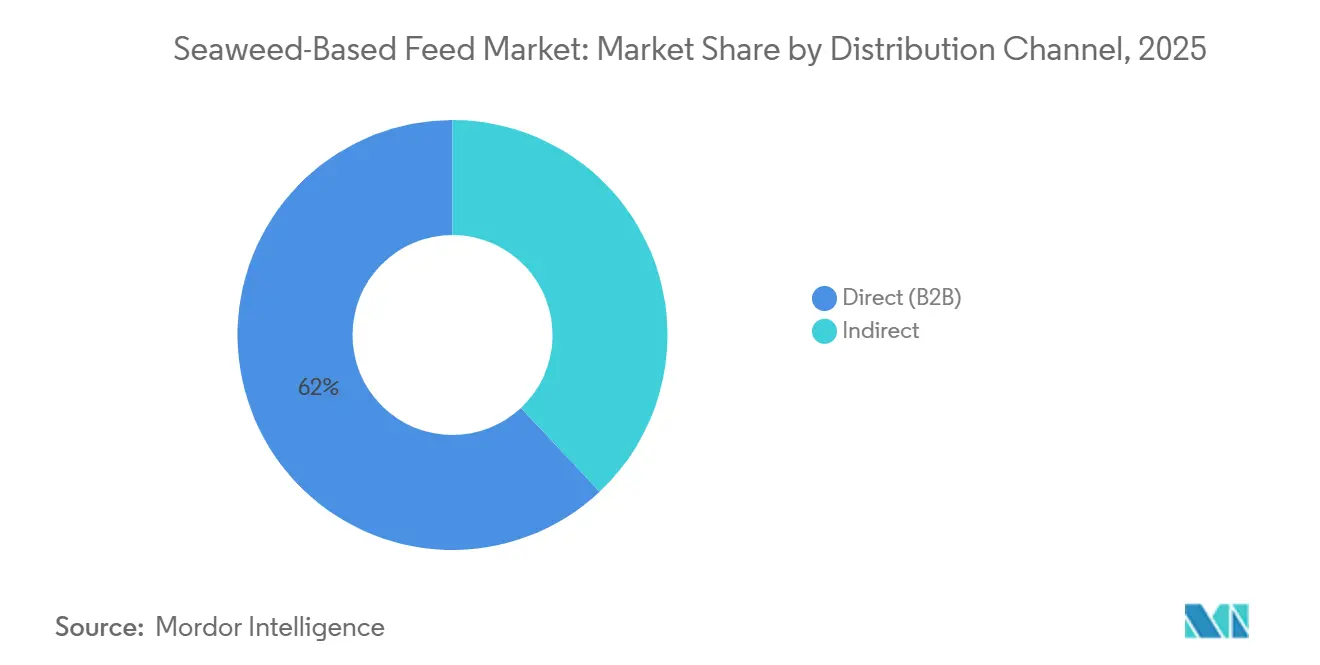

- By distribution channel, direct (B2B) held the largest share, accounting for 62% of the seaweed-based feed market share in 2025 and is projected to expand at an 11.4% CAGR through 2026-2031.

- By geography, Asia-Pacific captured largest 45% share of seaweed-based feed market size in 2025, whereas South America is advancing at the fastest 10.5% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Seaweed-Based Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable aquaculture feed | +2.1% | High in Asia-Pacific and Europe | Medium term (2-4 years) |

| Regulatory curbs on antibiotic growth promoters | +1.8% | North America and Europe, spillover to Latin America | Short term (≤ 2 years) |

| Functional benefits of seaweed bio-actives | +1.5% | Premium aquaculture markets worldwide | Medium term (2-4 years) |

| Expansion of commercial ocean farming capacity | +1.4% | Core Asia-Pacific, emerging Australia and South America | Long term (≥ 4 years) |

| Methane-reducing cattle feed trials gain traction | +1.3% | North America, Europe, Oceania and South America | Medium term (2-4 years) |

| Blue-carbon ESG credit monetization | +0.9% | Global voluntary carbon markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Aquaculture Feed

Farmed fish and shrimp producers are replacing fishmeal and soy concentrate with seaweed-based ingredients to meet sustainability goals and improve feed-conversion ratios. In 2026, BioMar Group A/S launched functional aquafeed for hatcheries, highlighting seaweed derivatives as sustainable solutions. India’s seaweed production tripled to 74,083 metric tons in 2024 under the Pradhan Mantri Matsya Sampada Yojana, reducing costs and strengthening Asia-Pacific’s role in kelp-based feed supply[1]Source: Ministry of Fisheries India, “PMMSY Seaweed Expansion,” pib.gov.in. Scientific validation, product innovation, and increased supply are driving seaweed’s role in sustainable aquaculture nutrition.

Regulatory Curbs on Antibiotic Growth Promoters

The European Union's ban on prophylactic antibiotics and the United States Food and Drug Administration's guidance have compelled feed mills to adopt natural immunity enhancers as part of their production processes. In response to these regulatory changes, Cargill has incorporated Ascophyllum nodosum, a type of seaweed, into broiler starter feeds to comply with antibiotic-free labeling requirements and support animal health. In 2024, Canada approved the use of algal omega-3 oil in aquafeeds, marking a significant step toward the acceptance of marine bioactives in animal nutrition. This approval reflects a growing openness among regulatory agencies to innovative, sustainable feed ingredients. Additionally, traceability standards under the International Organization for Standardization (ISO) 22,000 now favor vertically integrated ocean farming operations, promoting enhanced transparency and accountability in the supply chain.

Functional Benefits of Seaweed Bio-actives

Seaweed polysaccharides such as fucoidan, laminarin, and alginate are increasingly valued for enhancing immunity and gut integrity in livestock and aquaculture. Alltech priced its Integral A-plus blend at USD 19.50 per kilogram in 2026, citing dairy producers using 0.1% Ascophyllum nodosum meal reporting significant reductions in somatic cell counts. In 2025, Cargill, Incorporated demonstrated improved vaccine responses and reduced mortality in United States broilers using proprietary kelp premixes, leading to a nationwide rollout of seaweed-fortified starter feeds. Marinova Pty Ltd. tripled its fucoidan extraction capacity at its Tasmania facility in 2024 to meet the demand of aquafeed clients for compliance with European antibiotic-free requirements. BioMar Group A/S added refined laminarin fractions to its POWER H2O salmon feed in 2025, achieving a 15% reduction in post-transfer mortality at Norwegian recirculating farms. These outcomes confirm the role of functional bioactives in boosting producer performance and solidify seaweed's importance in the feed market.

Expansion of Commercial Ocean Farming Capacity

Rope-grown kelp yields up to 40 metric tons of wet biomass per hectare annually, cutting input costs. New South Wales projected a USD 597 million to USD 1.5 billion seaweed opportunity by 2030, enough dry Asparagopsis to meet up to 97% of global needs[2]Source: New South Wales Department of Primary Industries, “Seaweed Industry Prospectus,” dpi.nsw.gov.au. Sea Forest raised USD 13.6 million in 2025 to build a 7,000 metric-ton Asparagopsis facility in Tasmania. Symbrosia is constructing a solar-powered 15-acre refinery in Hawaii, targeting 3,385 metric tons of dry biomass by 2027. The Philippines committed USD 18.5 million in 2025 for nurseries, dryers, and bioreactors to stabilize carrageenan supply[3]Source: Philippine Department of Agriculture, “Official Website,” Department of Agriculture, da.gov.ph .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High processing cost versus conventional additives | –1.2% | Price-sensitive markets worldwide | Short term (≤ 2 years) |

| Supply variability due to seasonal harvests | –0.9% | Southern Hemisphere Asparagopsis zones | Medium term (2-4 years) |

| Heavy-metal contamination compliance risks | –0.7% | Europe and North America | Short term (≤ 2 years) |

| Sparse multi-species digestibility datasets | –0.5% | Global regulatory territories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Processing Cost Versus Conventional Additives

Freeze-drying Asparagopsis costs USD 8-12 per kilogram, far higher than USD 0.50-1.50 for standard mineral premixes, creating a price premium of at least 600%. Cascadia Seaweed raised USD 2.96 million in 2024 for a British Columbia biorefinery but requires over 10,000 metric tons of annual output to match soy-protein concentrate costs. Fremantle Seaweed an aquaculture farm based in western Australia secured USD 1.44 million in 2025 for a 3,000-hectare Asparagopsis farm, but its product remains less cost-effective than 3-nitrooxypropanol inhibitors, limiting adoption among cost-sensitive beef producers. In Brazil and Argentina, sun-drying necessitated by the lack of energy subsidies degrades heat-sensitive polysaccharides by up to 40%, reducing functional value and forcing price discounts. These cost barriers keep seaweed additives classified as niche, premium inputs, slowing the growth of the seaweed-based feed market.

Supply Variability Due to Seasonal Harvests

Asparagopsis production peaks during austral winters, resulting in supply gaps for half the year. This seasonal limitation poses challenges for consistent supply chains and requires strategic planning to mitigate disruptions. Sea Forest reported revenue of USD 528,000 in early 2026, reflecting significant growth. However, the company faces the challenge of financing cold storage facilities to ensure year-round availability and meet the demands of 12-month beef contracts. In 2023, 97% of Chile's Gracilaria production, totaling 14,426 metric tons, was wild-harvested. This reliance on wild harvesting exposes buyers to risks from El Niño-related storm damage, highlighting the need for more resilient sourcing methods. Hatch Blue's 2025 fieldwork revealed that Saint Lucia outperforms Brazil in production consistency, emphasizing the variability in regional performance and the importance of localized strategies. Meanwhile, India's 47,245 seaweed rafts approved under the Pradhan Mantri Matsya Sampada Yojana (PMMSY) initiative as of 2025 continue to face delays due to cyclone-related disruptions in nurseries, underscoring the impact of extreme weather events on aquaculture operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Livestock Adoption Accelerates Under Methane Mandates

Aquaculture accounted for 46% of the seaweed-based feed market share in 2025, reflecting decades of established inclusion in the diets of salmon, trout, and shrimp. Livestock is anticipated to capture a larger share of the seaweed-based feed market, driven by 12.3% CAGR growth during 2026-2031, as dairy and beef operators adopt red seaweed extracts to meet climate levies. Poultry and swine remain minor users because regulators require more digestibility data, although small-scale trials show immune benefits. Pet food formulators are beginning to blend algal omega-3 oils to differentiate premium lines launched in 2026. Recirculating aquaculture system operators in Europe report improved pellet water stability when 1% kelp meal is added.

Rapid livestock uptake rests on secured offtake deals. Sea Forest signed agreements covering 123,000 cattle in 2025 and partnered with Orffa for European Union dairy channels. Symbrosia expects its Hawaii refinery to service 1.4 million head annually from 2027. Aquaculture trials have expanded to Pacific white shrimp, showing 30% growth gains at 2% Asparagopsis inclusion. Pet brands test microalgae blends for coat shine and joint health yet must formulate around iodine ceilings. Poultry integrators could unlock volume once multi-site studies validate 0.5-1% kelp inclusion across broiler breeds.

By Species: Red Seaweed Rises on Proven Methane Mitigation

Brown seaweed retained 42% of revenue in 2025 because Laminaria supply chains in China and Japan already feed regional mills. Red seaweed is the fastest-growing segment, with a 13.1% CAGR through 2031, and is forecast to sharply expand the seaweed-based feed market once Asparagopsis volumes scale. Green seaweed holds a smaller slice but brings high protein concentrations that appeal to land-based aquaculture. Micro-algae blends attract premium niches in pet food and specialty fish diets at above USD 15 per kilogram.

Efficacy data underpins red seaweed momentum. Mexico’s 2025 authorization of Brominata established a regulatory beachhead. CH4 Global’s EcoPark came online in 2025 to serve tens of thousands of cattle daily. Brown seaweed maintains its aquaculture dominance through BioMar’s POWER H2O feed launched in 2025. Marinova’s 2024 expansion tripled fucoidan output to meet rising demand for immunomodulators. Green Ulva inclusion continued to improve quail feed conversion in 2024 trials, hinting at broader monogastric applications.

By Form: Liquid Extract Gains on Precision On-Farm Dosing

Powder led the seaweed-based feed market with 51% share in 2025 because spray-drying integrates easily into mill processes. Liquid extract is forecast to be the fastest format, with a 13.9% CAGR from 2026-2031, aligning with on-farm injection systems that safeguard volatile bioactives. Pellets maintain relevance in aquaculture, providing water stability and nutrient retention. Flakes occupy a niche in pet treats and direct-fed supplements where visual cues of natural ingredients influence buyers.

Liquid extract adoption mirrors methane-reduction deployments. Symbrosia’s SeaGraze liquid targets total mixed ration systems for cattle. Sea Forest dispatches liquid Asparagopsis to dairies in Australia and Europe. Powder players such as Cascadia Seaweed invested in a British Columbia dryer in 2024 to pursue economies of scale. BioMar binds kelp meal into high-durability pellets that resist leaching in recirculating systems. Flake providers Acadian Seaplants and Ocean Harvest Technology market visible Ascophyllum pieces to pet-food brands focused on natural positioning.

By Distribution Channel: Direct B2B Channels Accelerate as Traceability Becomes Non-Negotiable

Direct business-to-business (B2B) channels accounted for 62% of the market in 2025 and are expanding at the fastest 11.4% CAGR over 2026-2031. This leadership reflects how feed mills and livestock integrators sign multi-year contracts with seaweed processors to lock in pricing, verify batch-level traceability, and satisfy retailer sustainability scorecards. Cargill, Olmix, and BioMar exemplify this shift by embedding seaweed ingredients directly into compound feeds for poultry, swine, and salmon rather than purchasing through distributors. The rise of blockchain systems that record harvest date, heavy-metal results, and carbon intensity further cements direct B2B as the preferred route for methane-reduction additives where dosing precision is critical.

Indirect channels accounted for the remaining share of distribution in 2025 and are growing at a solid CAGR through 2031 as they cater to smaller mills, on-farm mixers, and niche pet-food brands that favor flexible order sizes. Distributors and e-commerce platforms such as Amazon and Chewy help boutique companies reach customers without maintaining large inventories. Acadian Seaplants widened its geographic footprint by partnering with BASF in 2024, while DSM-Firmenich markets its 2026 Veramaris O3 Max Pure through both direct deals with major pet-food manufacturers and distributor networks that target premium natural formulas. Although indirect sales expand steadily, their growth remains tied to broader adoption among small buyers who value convenience over full supply-chain control.

Geography Analysis

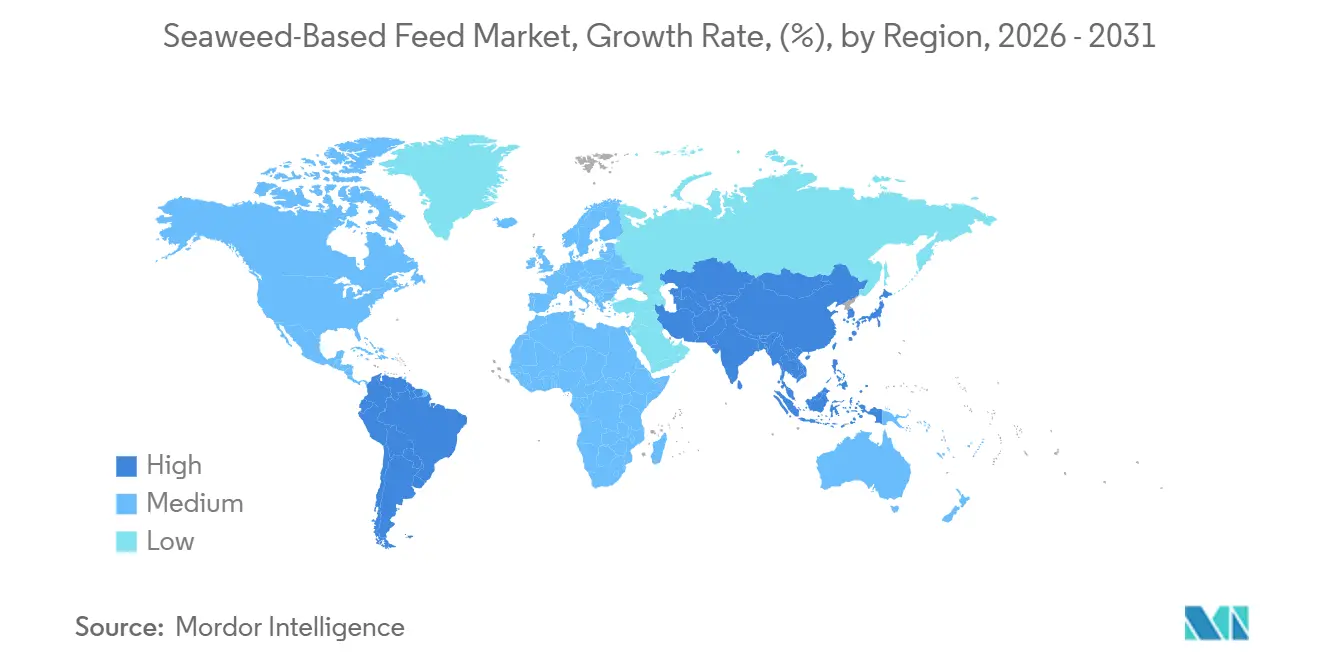

Asia-Pacific retained the largest 45% market share in 2025, reflecting deep Laminaria supply chains in China and expanding kelp farms in India. Producers in Japan and South Korea leverage vertically integrated models that cut logistics costs and speed batch-level traceability. South America is the fastest region, advancing at a 10.5% CAGR over 2026-2031 as Chilean salmon companies adopt integrated macroalgae systems and Brazilian beef exporters monetize blue-carbon credits. These quantitative trends show that the leading, fastest territories drive overall market growth momentum.

Europe maintains robust demand as Norwegian brown-seaweed biorefineries reach commercial scale and European Union regulations favor natural feed additives over antibiotics. North America benefits from Ascophyllum harvests in the North Atlantic and early adoption of Asparagopsis supplements by large dairy integrators. The Middle East shows steady uptake through imported powders blended into poultry rations, while Africa relies on Asian extracts but explores coastal farming pilots. Although these areas trail the leaders in absolute revenue, technology transfer and regulatory alignment continue to widen their addressable opportunity.

Regional investments are anticipated to broaden the seaweed-based feed market size through 2031. Asia-Pacific governments fund nurseries, dryers and bioreactors that lower entry barriers for new growers, while Australian hubs scale rope-grown Asparagopsis for methane reduction. Chile, Norway and Canada refine biorefinery designs that squeeze more value from each kilogram of biomass, improving cost competitiveness. As traceable supply networks mature, all regions are positioned to raise inclusion rates across aquaculture, livestock and pet-food applications, reinforcing the long-term growth trajectory.

Competitive Landscape

The seaweed-based feed market is moderately concentrated. The top 5 major players, Cargill, Incorporated, Olmix SA, BioMar Group A/S, Acadian Seaplants Limited, and Alltech, Inc., account for a significant share of worldwide revenue, conferring procurement leverage yet leaving space for regional challengers. Cargill, Incorporated utilizes its expertise in global kelp procurement and multi-species formulation to support major accounts in poultry, swine, and salmon. The company’s extensive supply chain and research capabilities enable it to meet the diverse needs of its clients while maintaining consistent quality. Olmix SA focuses on proprietary Ulvan extraction and provides customized blends to European and Asian mills seeking natural immunity enhancers. By leveraging advanced extraction techniques and a deep understanding of market requirements, Olmix SA ensures its products align with customer demands for sustainable and effective solutions. These two companies play a key role in setting pricing benchmarks and shaping technical standards for traceable seaweed inclusion, influencing the broader adoption of seaweed-based products in the feed industry.

BioMar Group A/S strengthens its salmon portfolio with brown-kelp derivatives, highlighted by the 2025 launch of POWER H2O feed for recirculating systems. Acadian Seaplants Limited integrates North Atlantic Ascophyllum harvests with ISO 22000 traceability, widening reach through a 2024 BASF distribution pact. Alltech, Inc. positions its Integral line as a premium immunomodulator that commands higher margins in dairy and beef rations. Venture-backed entrants such as Blue Ocean Barns, CH4 Global, Symbrosia and Sea Forest intensify rivalry by securing early regulatory approvals for Asparagopsis additives.

Companies are scaling capacity, advancing digital traceability and pursuing carbon-credit monetization to expand the market through 2031. DSM-Firmenich’s 2026 divestiture of feed enzymes frees capital for algal oil specialties that complement seaweed bioactives. Marinova’s 2024 fucoidan expansion and Alginor’s PROTEUS full-biomass biorefinery lower unit costs and improve sustainability metrics. With vertically integrated farms, blockchain records and blue-carbon credits, incumbents and newcomers alike are poised to increase seaweed inclusion across livestock, aquaculture and pet nutrition.

Seaweed-Based Feed Industry Leaders

Cargill, Incorporated

Olmix SA

BioMar Group A/S

Acadian Seaplants Limited

Alltech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Hatch Blue unveiled the Seaweed Insights platform covering six Latin American countries. The centralized dataset helps financiers and processors identify reliable farming zones, speeding investment decisions and expanding raw-material flows that feed regional growth in seaweed-based feed additives.

- January 2026: SeaForester and Seaweed Solutions merged, raising USD 1.9 million for ocean reforestation. The larger entity aims to restore and cultivate 10,000 hectares of kelp forests, adding biomass that can be refined into functional feed ingredients and expanding long-term market capacity.

- December 2025: Symbrosia secured USD 5.8 million in Series A-1 funding to scale SeaGraze and pursue United States Food and Drug Administration clearance. The new capital and anticipated regulatory pathway accelerate the commercial rollout, driving faster adoption of methane-reducing seaweed extracts and boosting overall demand in the feed market.

Global Seaweed-Based Feed Market Report Scope

Seaweed-based feed is a sustainable and nutritious animal feed ingredient derived from marine macroalgae. It serves as a natural, mineral-rich additive that improves gut health and provides nutritional benefits for livestock and aquaculture. Seaweed is commonly processed into meal, powder, or extracts. The seaweed-based feed market report is segmented by application (aquaculture, livestock, poultry, and pet food), by species (brown seaweed, red seaweed, green seaweed, and micro-algae blends), by form (powder, pellets, liquid extract, and flakes), by distribution channel (direct (b2b), and indirect), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Aquaculture |

| Livestock |

| Poultry |

| Pet Food |

| Brown seaweed |

| Red seaweed |

| Green seaweed |

| Micro-algae blends |

| Powder |

| Pellets |

| Liquid extract |

| Flakes |

| Direct (B2B) |

| Indirect |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| Application | Aquaculture | |

| Livestock | ||

| Poultry | ||

| Pet Food | ||

| Species | Brown seaweed | |

| Red seaweed | ||

| Green seaweed | ||

| Micro-algae blends | ||

| Form | Powder | |

| Pellets | ||

| Liquid extract | ||

| Flakes | ||

| Distribution Channel | Direct (B2B) | |

| Indirect | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the seaweed-based feed market in 2031?

The seaweed-based feed market is forecast to reach USD 2.17 billion by 2031.

Which region holds the largest share in seaweed-derived feed ingredients?

Asia-Pacific led with 45% revenue in 2025 due to China's extensive Laminaria cultivation and supportive policies in India and Japan.

Which application is growing the fastest within this market?

Livestock feed is the fastest segment, advancing at a 12.3% CAGR during 2026-2031 as red seaweed extracts gain regulatory clearance for methane mitigation.

How are new entrants influencing competition?

Startups such as Blue Ocean Barns and Symbrosia secure first-mover regulatory approvals for Asparagopsis additives, challenging incumbents through methane-reduction efficacy and carbon-credit monetization.

What regulatory factors support adoption of seaweed in animal diets?

The European Union ban on prophylactic antibiotics and United States Food and Drug Administration guidance limiting antibiotic growth promoters push feed mills toward natural bioactive alternatives like kelp extracts.

Page last updated on: