Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

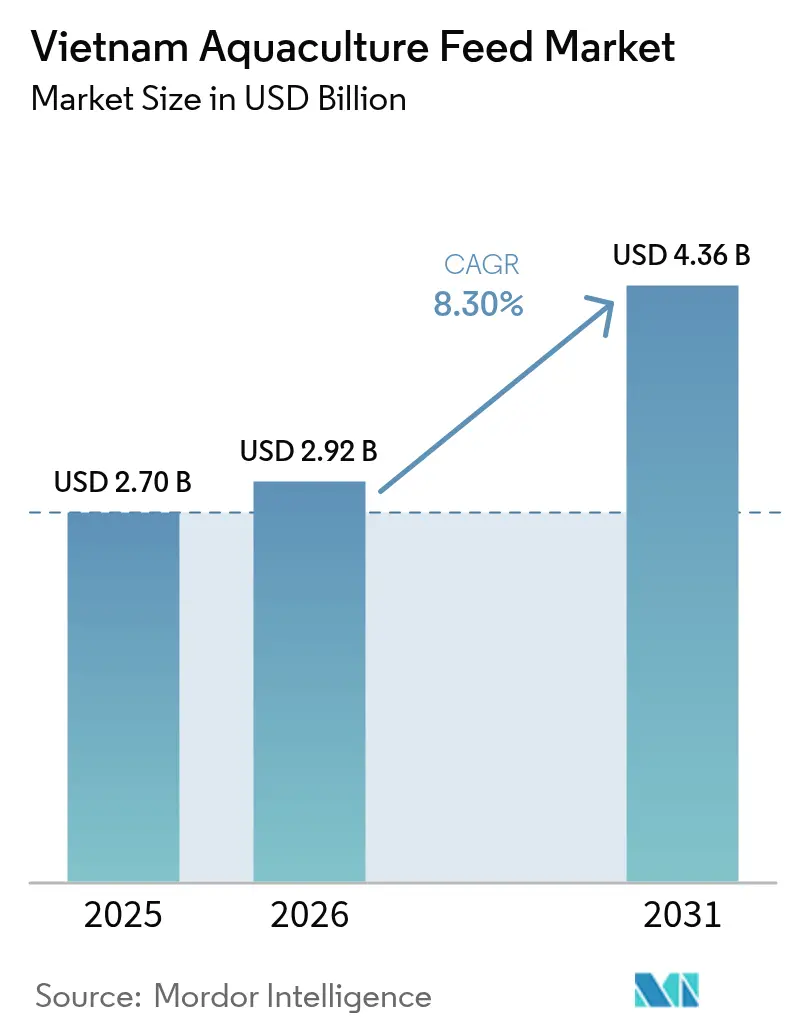

| Base Year Market Size (2025) | USD 2.70 Billion |

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 4.36 Billion |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Aquaculture Feed Market Analysis by Mordor Intelligence

The Vietnam aquaculture feed market size was valued at USD 2.70 billion in 2025 and estimated to grow from USD 2.92 billion in 2026 to reach USD 4.36 billion by 2031, at a CAGR of 8.30% during the forecast period (2026-2031). Strong export demand for shrimp and pangasius, increased uptake of functional formulations, and rising investments in Recirculating Aquaculture Systems (RAS) are driving the Vietnam aquaculture feed market on an expansive trajectory. Extruded diets retain dominance because their buoyancy and water stability curb feed waste, while micro feeds are rapidly scaling across hatcheries. Algal and insect proteins are gaining traction as feed producers seek to insulate margins from volatile fish-meal prices. Regional tax incentives in the Shrimp-specific feed subsidies in the Mekong Delta and Central Coast are accelerating premium-feed adoption, and AI-enabled precision-feeding platforms are beginning to compress feed conversion ratios, lifting farm profitability.

Key Report Takeaways

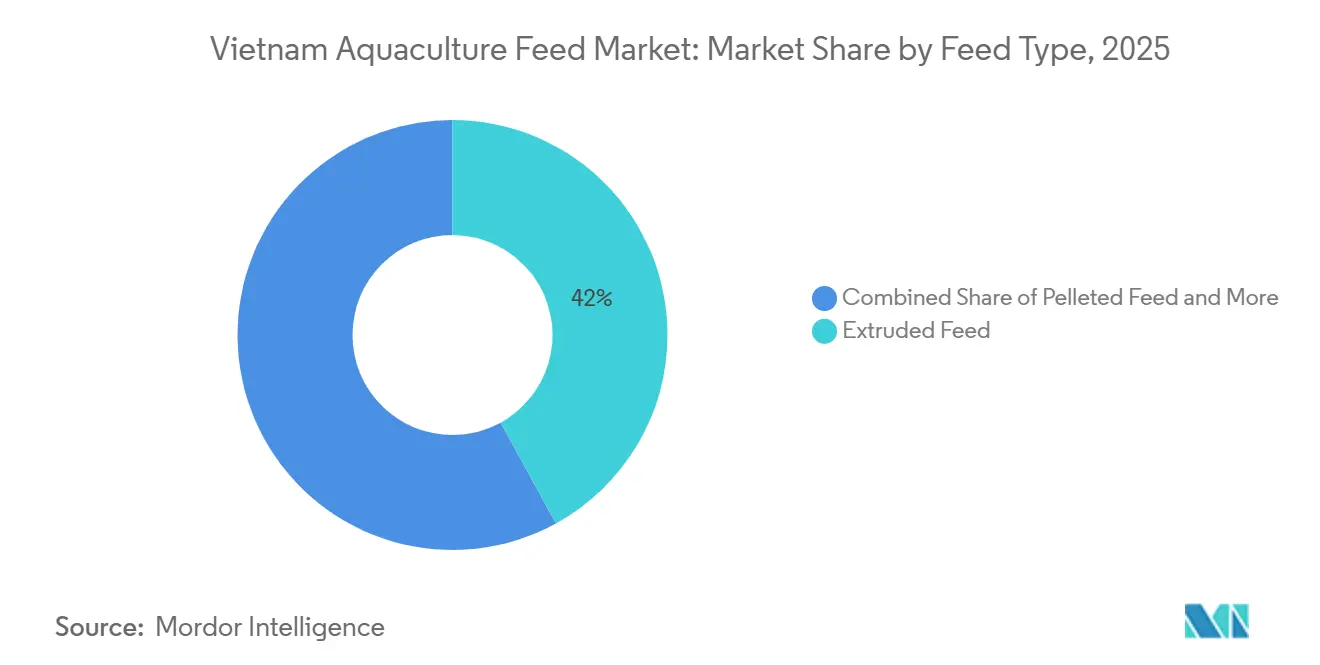

- By feed type, extruded diets were the largest segment, accounting for 42.0% of the Vietnam aquaculture feed market share in 2025, whereas micro feeds are the fastest-growing segment, advancing at an 11.5% CAGR through 2031.

- By ingredient source, fish meal and fish oil were the largest segment, commanding 38.0% of the Vietnam aquaculture feed market in 2025, while algal and alternative proteins are the fastest-growing segment, projected to grow at a 14.2% CAGR to 2031.

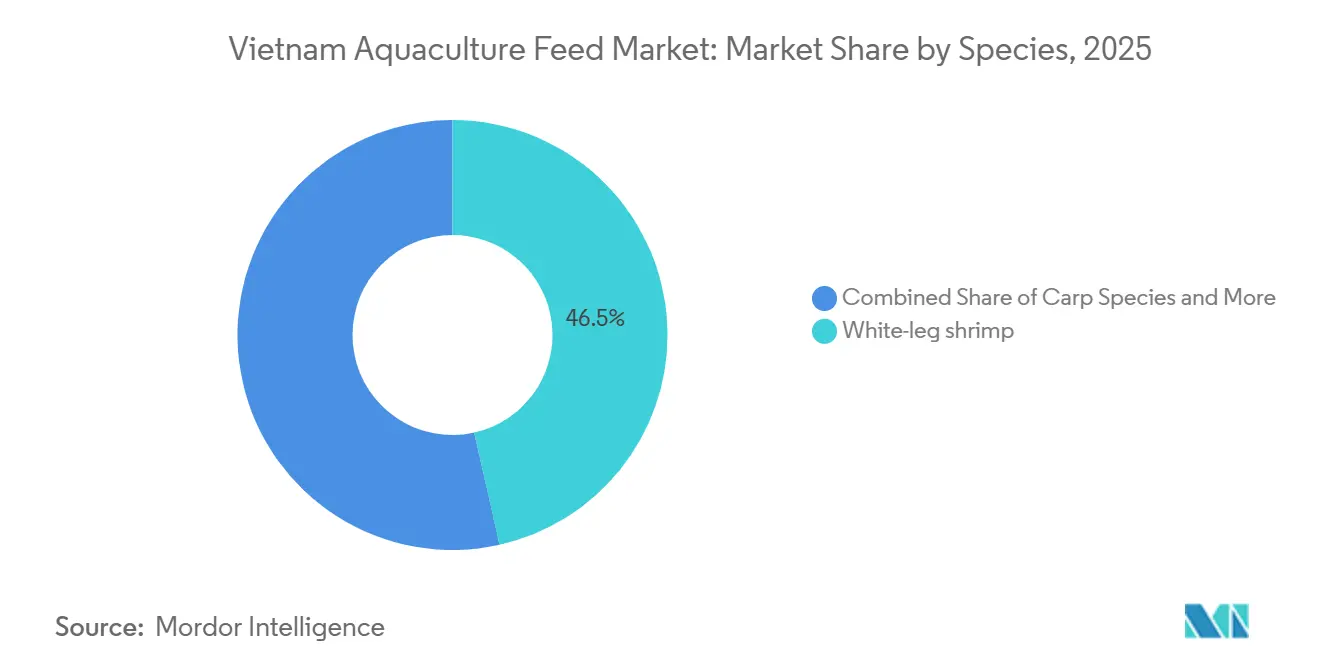

- By species, white-leg shrimp were the largest segment, holding 46.5% of the Vietnam aquaculture feed market size in 2025. Tilapia is the fastest-growing segment, forecast to expand at a 10.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Aquaculture Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust expansion of domestic Recirculating Aquaculture Systems facilities | +1.8% | National, with a concentration in the Mekong Delta, Southeast Region, and Red River Delta | Medium term (2-4 years) |

| Mainstream growth of functional feeds | +1.5% | National, the strongest uptake in the Mekong Delta and the Southeast Region for shrimp applications | Short term (≤ 2 years) |

| Rising consumer demand for antibiotic-free seafood | +1.3% | Global export markets (European Union, North America, and Japan), driving Vietnam-wide compliance | Medium term (2-4 years) |

| Integration of AI-driven precision-feeding platforms | +1.2% | Early adoption in the Mekong Delta and the Southeast Region, and expanding to the Red River Delta | Medium term (2-4 years) |

| Scale-up of single-cell protein production from biogas effluent | +0.9% | Pilot projects in the Mekong Delta and the Southeast Region, with limited national rollout | Long term (≥ 4 years) |

| Shrimp-specific feed subsidies in the Mekong Delta | +0.7% | Mekong Delta provinces (Ben Tre, Tra Vinh, Soc Trang, and Ca Mau) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Expansion of Domestic Recirculating Aquaculture Systems Facilities

The rapid expansion of Recirculating Aquaculture Systems (RAS) in Vietnam is significantly improving production efficiency and biosecurity in high-value species farming. RAS facilitates controlled water quality, reduces disease outbreaks, and enhances stocking density, particularly in shrimp and pangasius farming. For instance, intensive shrimp farms in the Mekong Delta are increasingly adopting RAS technology to minimize water exchange and mitigate disease risks such as Early Mortality Syndrome (EMS). This technology-driven approach supports higher output per hectare and stabilizes year-round production, directly contributing to overall aquaculture growth.

Mainstream Growth of Functional Feeds

The growing adoption of functional feeds fortified with probiotics, enzymes, and immunostimulants is improving feed conversion ratios and survival rates in shrimp and fish farming. As disease management becomes increasingly critical, farmers are transitioning from traditional feed to specialized formulations that enhance gut health and immunity. For instance, shrimp farms in Soc Trang and Bac Lieu provinces are using probiotic-enhanced feeds to reduce reliance on antibiotics while maintaining export-grade quality. This shift increases feed value per metric ton and enhances farm productivity, thereby driving sectoral growth. GreenFeed secured Aquaculture Stewardship Council certification in October 2025 for its probiotic shrimp diet, delivering improved feed conversion and cost savings for farmers[1]Source: General Statistics Office of Vietnam, “Agriculture, Forestry and Fishing Statistics,” gso.gov.vn.

Rising Consumer Demand for Antibiotic-Free Seafood

Rising demand from export markets such as the European Union, North America, and Japan for antibiotic-free and traceable seafood is prompting Vietnamese producers to upgrade farming practices. Compliance with international standards, such as Best Aquacultural Practices (BAP) certifications, is encouraging investments in improved water management, feed quality, and traceability systems. For instance, pangasius exporters in the Mekong Delta are increasingly adopting antibiotic-free production protocols to maintain access to premium markets. This export-driven compliance enhances Vietnam’s global competitiveness and fosters value-added growth in aquaculture.

Integration of AI-Driven Precision-Feeding Platforms

The adoption of AI-based feeding systems and smart monitoring platforms is optimizing feed utilization and reducing waste. These technologies leverage sensors and real-time data analytics to adjust feed distribution based on shrimp or fish behavior and environmental conditions. For instance, large-scale shrimp farms are implementing automated feeders that monitor consumption patterns, reducing feed wastage, improving feed conversion ratios, and lowering production costs. This technological integration boosts operational efficiency and profitability, supporting sustainable market growth. These digital tools cut input costs, elevate water quality, and will increasingly differentiate suppliers in the Vietnam aquaculture feed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fishmeal and fish oil prices | -1.4% | Global, with an acute impact on Vietnam due to high import dependence | Short term (≤ 2 years) |

| Stringent effluent-discharge rules from the Ministry of Natural Resources and Environment | -0.9% | National, with stricter enforcement in the Mekong Delta and the Southeast Region | Medium term (2-4 years) |

| Supply-chain bottlenecks for specialty additives | -0.6% | National, affecting imports of probiotics, enzymes, and immunostimulants | Short term (≤ 2 years) |

| Farmer hesitancy toward genetically engineered protein inputs | -0.5% | National, particularly among smallholder farms in the Mekong Delta and the Red River Delta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Fish-Meal and Fish-Oil Prices

Vietnam relies heavily on imported fishmeal and fish oil for aquafeed production, making the industry susceptible to global price fluctuations. Increases in global fishmeal prices, often driven by supply constraints in Peru, directly raise feed production costs. This impacts shrimp farmers, leading to margin compression. As a result, some small-scale operators are compelled to reduce stocking densities or delay production cycles. The export price of fish oil from Vietnam has fluctuated significantly over the past two years. In 2024, prices ranged from 0.83 USD per kg to 2.96 USD per kg. In 2025, prices continued to vary, ranging from 0.97 USD per kg to 2.48 USD per kg[2]Source: Vietnam Directorate of Fisheries, “Aquaculture Feed Price Monitoring Report 2025,” tongcucthuysan.gov.vn.

Stringent Effluent-Discharge Rules

In February 2026, stricter environmental regulations introduced by the Ministry of Natural Resources and Environment have increased compliance costs for aquaculture farms. Farmers are required to invest in wastewater treatment systems and sedimentation ponds to meet discharge standards, particularly in the Mekong Delta. For instance, shrimp farms adopting high-density production must allocate additional capital to effluent management infrastructure, resulting in higher upfront investment costs. While these regulations are environmentally beneficial, they have slowed expansion among small and medium-scale farmers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Type: Extruded Diets Dominate as Micro Feeds Surge

Extruded diets were the largest segment, accounting for 42.0% of the Vietnam aquaculture feed market share in 2025, reflecting their buoyancy advantage, which reduces waste and improves feed conversion. Pelleted diets held a significant share yet are losing ground to extruded formats as intensive shrimp farmers shift toward higher efficiency. Pelleted manufacturers are retrofitting steam conditioners to raise pellet durability, but their inherent density mismatch with shrimp feeding habits restricts uptake.

Micro feeds are the fastest-growing segment, advancing at a 11.5% CAGR through 2031, as hatcheries invest in controlled-release technology to drive gains in larval survival. Moist feeds remain a niche for eel and ornamental species because their short shelf life increases labor costs and limits their commercial potential in the Vietnamese aquaculture feed market. Thang Long Group inaugurated a new feed mill in Hai Duong province in May 2024, increasing its annual capacity to 700,000 metric tons. The facility focuses on producing extruded shrimp diets to target the premium segment and enhance profit margins[3]Source: Thang Long Group, “New Feed Mill in Hai Duong Province,” thanglongfeed.com.

By Ingredient Source: Marine Proteins Face Substitution Pressure

Fish meal and fish oil were the largest segment, commanding 38.0% of the Vietnam aquaculture feed market in 2025, owing to stable local supply and cost parity, though anti-nutritional factors cap inclusion rates in high-value shrimp diets. Fish oil continues to be a critical source of highly unsaturated fatty acids in marine finfish diets, although enzyme supplementation allows for partial replacement. Animal by-products, such as poultry meal, are commonly used in cost-effective pangasius feed formulations but are subject to increasing traceability requirements from export buyers. Government incentives are driving the domestic production of alternative proteins, enabling feed mills to mitigate risks associated with global commodity price fluctuations.

Algal and alternative proteins are the fastest-growing segment, projected to grow at a 14.2% CAGR to 2031. Plant proteins, primarily soy and wheat gluten, were the second-largest segment, driven by stable local supply and cost parity, though anti-nutritional factors cap inclusion rates in high-value shrimp diets. Algal proteins, sourced from Spirulina and Chlorella, provide omega-3 fatty acids without the risk of heavy-metal contamination associated with fish oil, making them a reliable alternative to mitigate marine-ingredient volatility. Regulatory uncertainties and limited farmer confidence continue to pose challenges.

By Species: Shrimp Feeds Lead While Tilapia Accelerates

White-leg shrimp were the largest segment, holding 46.5% of the Vietnam aquaculture feed market size in 2025, mirroring Vietnam’s third-place global rank in shrimp exports. White-leg shrimp production is growing, driven by the adoption of intensive farming practices, premium export pricing, and technological advancements, such as Recirculating Aquaculture Systems (RAS) and precision feeding, which require specialized, high-performance feeds.

Tilapia is the fastest-growing segment, forecast to expand at a 10.9% CAGR through 2031, as cage systems expand across Northern reservoirs. Giant tiger prawn diets grow slowly because of longer culture cycles and higher disease risk. The rapid growth of tilapia production is drawing investment from multinational feed suppliers. For instance, in 2023, Aller Aqua Vietnam has developed a floating extruded feed specifically designed for cage systems, which minimizes feed waste compared to sinking pellets. Carp and catfish, traditional freshwater species, constitute a substantial portion of feed consumption. This is primarily concentrated in the Northern Midlands and Mountains region, where smallholder polyculture systems are prevalent. Other species, such as eel, grouper, and ornamental fish, occupy niche segments characterized by specialized nutritional needs and premium pricing.

Geography Analysis

Mekong Delta provinces, including Can Tho, Soc Trang, and Ca Mau, contribute over half of Vietnam's aquaculture production, driving regional feed consumption and manufacturing. Companies such as De Heus, Skretting, and CP Foods strategically position their mills near these areas to reduce freight costs and ensure timely deliveries. Additionally, Southeast coastal provinces support marine-cage culture, which increases demand for oil-rich extruded pellets, further boosting growth in feed consumption.

The geographic distribution of aquaculture activities results in varied patterns of feed demand. The Mekong Delta requires significant quantities of cost-effective pelleted feeds for pangasius and extensive shrimp farming systems. In contrast, coastal regions demand high-quality extruded feeds for intensive marine aquaculture. Central provinces, such as Nghe An and Dong Nai, have implemented updated aquaculture regulations that influence feed usage and traceability. These regulations include specific procedures for disease reporting and environmental compliance, which impact feed distribution and emergency response strategies.

While regional concentration offers economies of scale, it also increases vulnerability to flooding and disease outbreaks. As a result, manufacturers prioritize contingency stockpiles and diversified transport routes to mitigate risks. This geographic concentration provides competitive advantages for integrated operations that combine feed production, farming, and processing within regional clusters. However, it also exposes supply chains to disruptions caused by extreme weather events or disease outbreaks affecting multiple provinces simultaneously.

Competitive Landscape

The Vietnam aquaculture feed market demonstrates moderate concentration with players including Skretting Vietnam (Nutreco N.V.), Cargill Inc., De Heus Animal Nutrition B.V., Charoen Pokphand Group, and Archer-Daniels-Midland Company accounting for significant revenue in 2025. The market features a mix of multinational corporations and agile domestic firms. Companies such as Cargill Inc., De Heus Animal Nutrition B.V., Charoen Pokphand Group, leverage global research and development capabilities and financial resources to secure a substantial share of premium feed sales. Meanwhile, domestic players like GreenFeed, Tongwei, and Olam Agri focus on localized formulations and farmer financing.

Domestic companies, including GreenFeed, Tongwei, and newer entrants such as Olam Agri Vietnam, adopt differentiation strategies through regional specialization, species-specific formulations, and integrated value-chain approaches that combine feed production with farming and processing. The competitive landscape fosters continuous innovation, with firms investing in alternative protein sources, precision feeding technologies, and sustainability certifications. These efforts aim to capture premium market segments and meet the demands of export-oriented customers requiring traceability and environmental compliance.

Alternative-protein alliances are budding, Entobel’s insect-meal project and methanotroph trials by Hanoi’s Institute of Biotechnology seek to dilute fish-meal exposure. Yet regulatory lag and farmer skepticism prolong marine-ingredient dominance. Competition will intensify as buyers demand empirical on-farm trial data before switching suppliers, likely squeezing manufacturers that cannot prove measurable performance gains.

Vietnam Aquaculture Feed Industry Leaders

Skretting Vietnam (Nutreco N.V.)

Cargill Inc.

De Heus Animal Nutrition B.V.

Charoen Pokphand Group

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: De Heus opened a new shrimp feed mill in the Co Chien Industrial Zone, Vinh Long province, representing a significant expansion of international feed manufacturing capacity in Vietnam's key aquaculture region.

- May 2024: Vietnam's government issued Decree 38/2024 establishing comprehensive administrative penalties for aquafeed violations, including fines up to VND 50 million for unauthorized ingredients and mandatory product recalls for non-compliant formulations.

- March 2024: Vietnam and Indonesia agreed to expand bilateral cooperation in aquaculture, including lobster seed production and export to Vietnam, tuna farming cooperation mechanisms, and seaweed cultivation technology transfer, creating opportunities for specialized aquafeed development.

Vietnam Aquaculture Feed Market Report Scope

Aquafeed is a formulated feed specifically designed for farmed aquatic species such as fish, shrimp, and other marine organisms. It consists of a balanced mixture of ingredients, including proteins, lipids, carbohydrates, vitamins, minerals, and functional additives to support optimal growth, health, and feed conversion efficiency in aquaculture systems.

The report on the Vietnam aquaculture feed market provides a detailed analysis across feed type, ingredient source, and species. It evaluates feed categories including extruded feed, pelleted feed, moist feed, and micro feed; examines ingredient sources such as fish meal and fish oil, plant protein, animal by-products, and algal and alternative proteins; and covers key farmed species including white-leg shrimp, giant tiger prawn, pangasius, carp, catfish, tilapia, and other species. All market estimates and forecasts are presented in USD value terms.

By Feed Type

| Extruded Feed |

| Pelleted Feed |

| Moist Feed |

| Micro Feed |

By Ingredient Source

| Fish Meal and Fish Oil |

| Plant Protein |

| Animal By-products |

| Algal and Alternative Proteins |

By Species

| White-leg Shrimp (Litopenaeus vannamei) |

| Giant Tiger Prawn (Penaeus monodon) |

| Pangasius |

| Carp |

| Catfish |

| Tilapia |

| Other Species |

| By Feed Type | Extruded Feed |

| Pelleted Feed | |

| Moist Feed | |

| Micro Feed | |

| By Ingredient Source | Fish Meal and Fish Oil |

| Plant Protein | |

| Animal By-products | |

| Algal and Alternative Proteins | |

| By Species | White-leg Shrimp (Litopenaeus vannamei) |

| Giant Tiger Prawn (Penaeus monodon) | |

| Pangasius | |

| Carp | |

| Catfish | |

| Tilapia | |

| Other Species |

Key Questions Answered in the Report

What is the current value of the Vietnam aquaculture feed market?

The Vietnam aquaculture feed market was valued at USD 2.70 billion in 2025 and is projected to grow from USD 2.92 billion in 2026 to USD 4.36 billion by 2031, registering a CAGR of 8.30% during the forecast period (2026-2031).

Which species uses the most commercial feed in Vietnam?

White-leg shrimp commands 46.5% value share of the market in 2025, owing to Vietnam's dominant shrimp export sector.

Why are Recirculating Aquaculture Systems important to feed suppliers?

Recirculating Aquaculture Systems units are projected to expand and require high-energy extruded diets, thereby creating a premium market segment for feed suppliers.

How are volatile fish-meal prices affecting manufacturers?

An increasing spike in early 2025 compressed feed-mill margins by up to 5% points and accelerated trials of algal and insect proteins.

Page last updated on: