Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

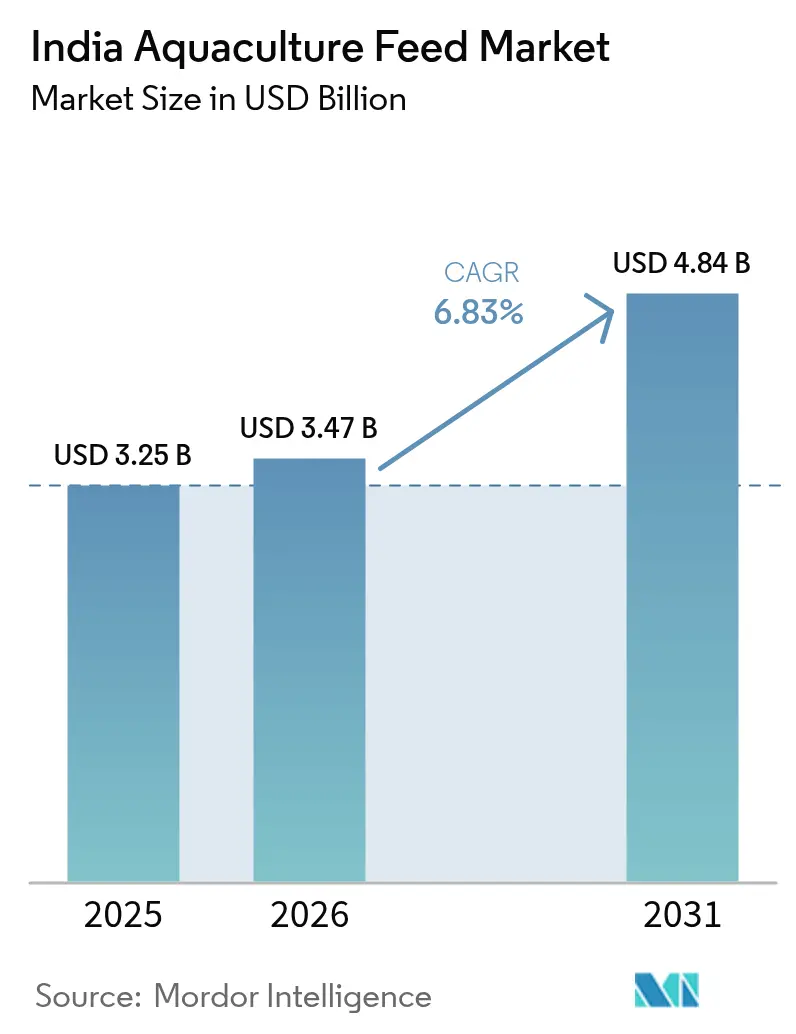

| Base Year Market Size (2025) | USD 3.25 Billion |

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 4.84 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

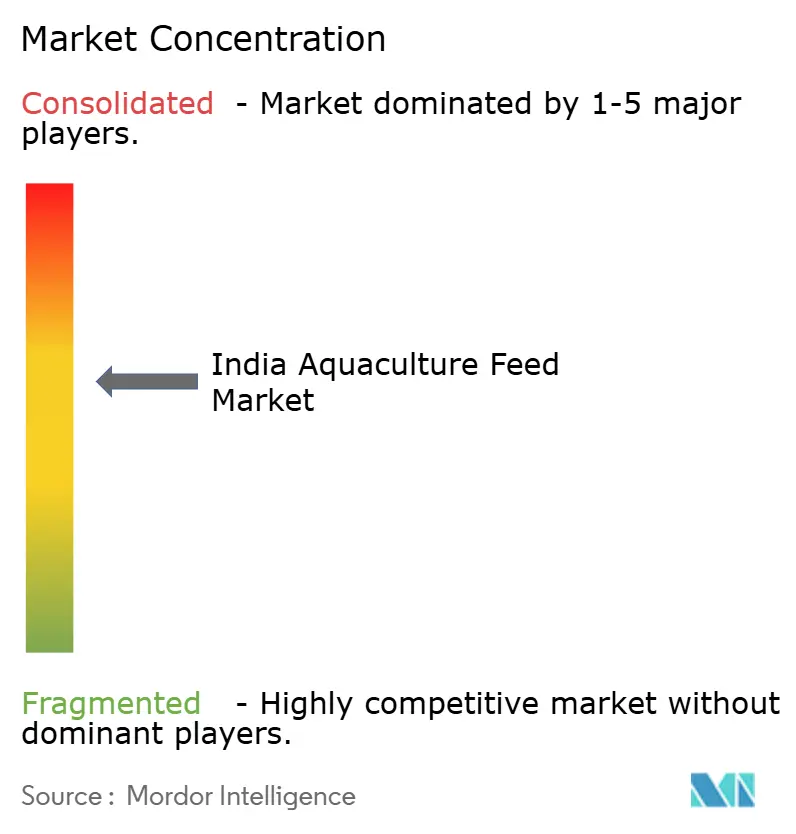

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Aquaculture Feed Market Analysis by Mordor Intelligence

The India aquaculture feed market size was valued at USD 3.25 billion in 2025 and estimated to grow from USD 3.47 billion in 2026 to reach USD 4.84 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031). The market demonstrates resilience in managing supply-chain disruptions while maintaining India's position as a key player in Asia-Pacific aquaculture. The implementation of government initiatives through Blue Revolution 2.0, continued growth in shrimp exports, increasing urban seafood consumption, and enhanced technology adoption create favorable conditions for industry growth in 2024. According to the ICAR-Central Marine Fisheries Research Institute, India's marine fish catch volume reached 3.45 million metric tons in 2024, with Gujarat, Tamil Nadu, and Kerala recording the highest landings[1]Source: ICAR-Central Marine Fisheries Research Institute (CMFRI), "CMFRI Annual Report 2024", cmfri.org.in. Feed manufacturers optimize operations through economies of scale, specialized feed formulations, and digital distribution networks, despite challenges from raw material price fluctuations and disease outbreaks. Coastal states dominate market growth, the expansion of inland aquaculture, and increased e-commerce adoption create new opportunities across the country.

Key Report Takeaways

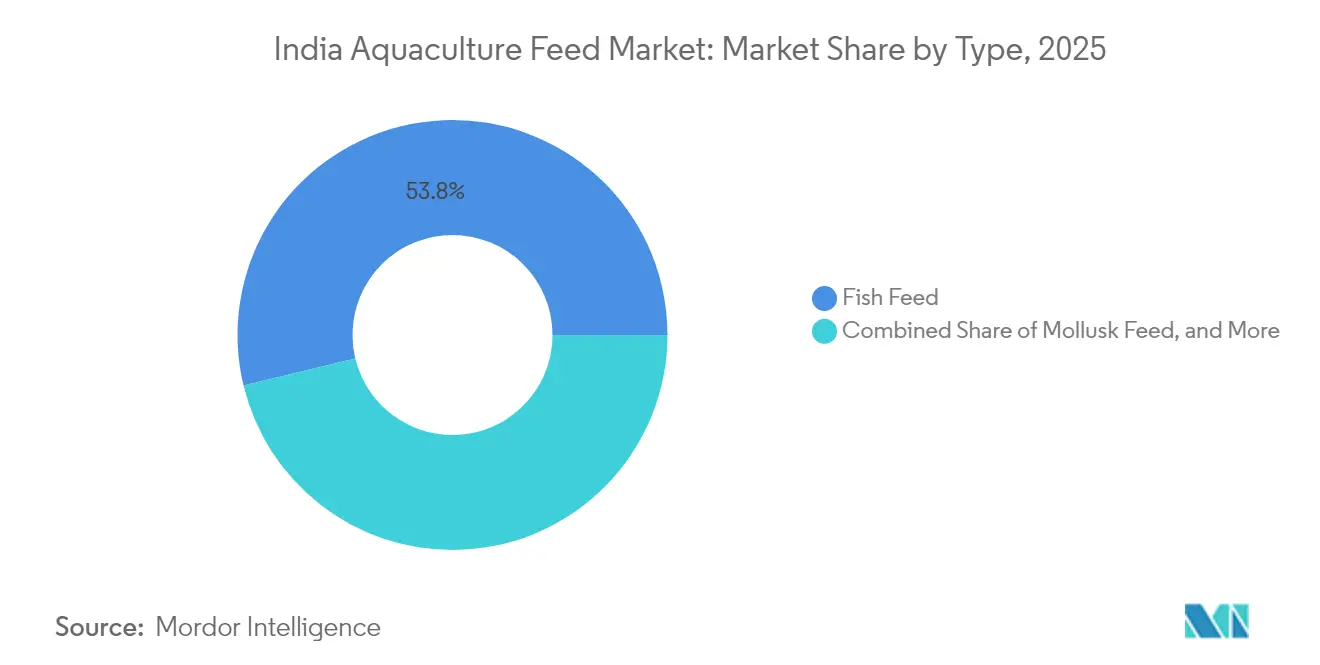

- By type, fish feed accounted for 53.78% of the India aquaculture feed market share in 2025, while shrimp feed is projected to advance at a 9.86% CAGR through 2031.

- By ingredient, soybean meal contributed 34.92% of the India aquaculture feed market size in 2025, whereas corn gluten meal is forecast to grow at a 9.08% CAGR to 2031.

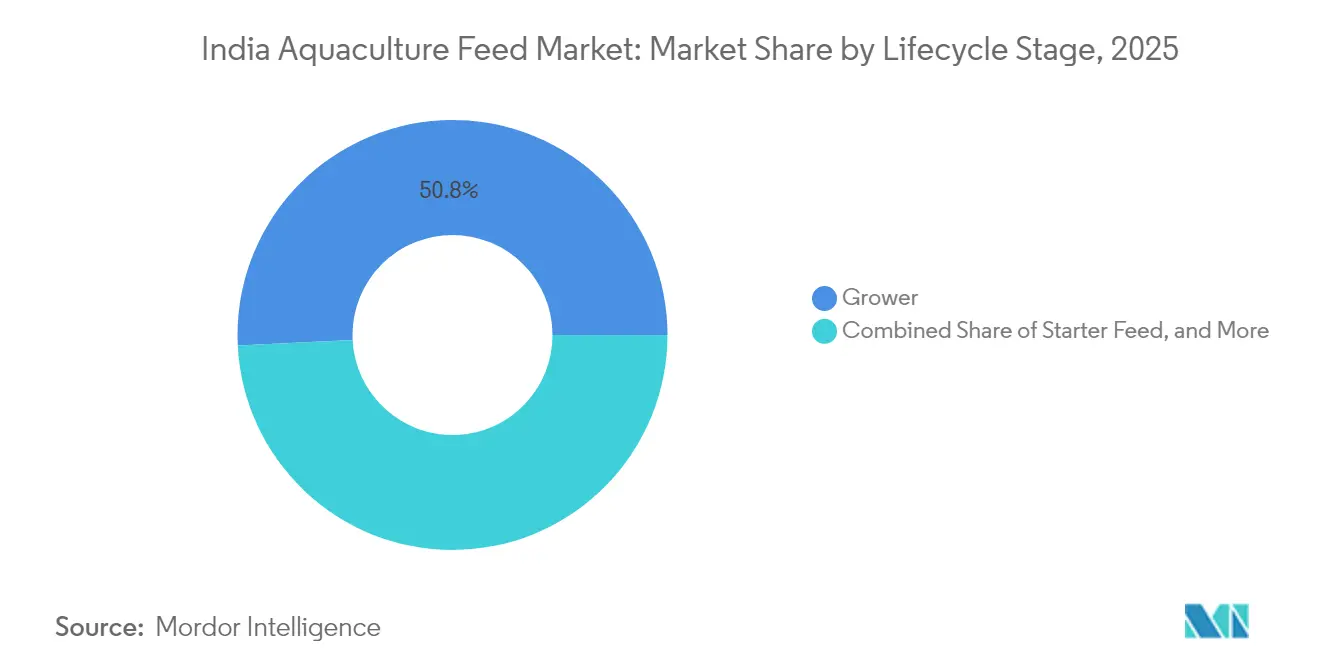

- By lifecycle stage, grower feed captured 50.78% of the India aquaculture feed market size in 2025; starter feed is projected to expand at a 10.35% CAGR through 2031.

- By form, pellets commanded 62.75% of the India aquaculture feed market revenue in 2025, and extruded floating feeds are projected to rise at a 9.42% CAGR through 2031.

- Avanti Feeds Limited, Charoen Pokphand Foods PCL, Growel Feeds Private Limited, IFB Agro Industries Ltd, and Godrej Agrovet Limited together controlled a significant portion of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Aquaculture Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic seafood consumption | +1.2% | Nationwide, strongest in urban centers | Medium term (2-4 years) |

| Expansion of export-oriented aquaculture | +1.8% | South and East coastal belts | Long term (≥ 4 years) |

| Government subsidies and schemes for aquaculture inputs | +0.9% | Nationwide rural clusters | Short term (≤ 2 years) |

| Technical adoption of high-protein formulated feeds | +1.1% | Commercial farms in South and West India | Medium term (2-4 years) |

| Corporate retail chains’ private-label fish demand | +0.7% | Urban markets in North and West India | Medium term (2-4 years) |

| AI-driven pond monitoring improving feed conversion ratios | +0.8% | Tech-enabled farms in South and East India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Seafood Consumption

Per capita fish consumption reached 5.7 kg in 2025, driven by urban consumers shifting toward lean protein sources[2]Source: Food and Agriculture Organization, “India Country Profile – Fisheries and Aquaculture,” fao.org. Organized retail chains reported significant growth in seafood sales, leading farmers to improve feed quality for consistent year-round production. The increasing demand for quality fish products has strengthened the aquafeed market, as farmers prioritize feed conversion efficiency to maintain a reliable supply. Consumer preferences for fresh and safe fish products have increased demand for farmed tilapia and pangasius, supporting the growth of India aquaculture feed market. South Indian households, traditionally incorporating fish in their daily diet, have expanded their consumption to include farmed species, increasing the adoption of commercial feed.

Expansion of Export-Oriented Aquaculture

India's seafood exports reached USD 8.09 billion in 2024, with shrimp contributing 75% of the total value[3]Source: Marine Products Export Development Authority, “Annual Report 2023-24,” mpeda.gov.in. Export-oriented farms consume more feed per hectare compared to domestic-focused operations, due to higher stocking densities and intensive farming practices required to meet international quality standards. The United States remains India's primary seafood export destination, accounting for 35% of total shipments. Recent tariff adjustments have led to market diversification toward Europe and the Middle East. The export focus has increased demand for specialized feeds with enhanced nutritional profiles and improved feed conversion ratios.

Government Subsidies and Schemes for Aquaculture Inputs

The Pradhan Mantri Matsya Sampada Yojana allocated INR 6,000 crore (USD 720 million) for fisheries development in July 2025, with 40% dedicated to feed-related infrastructure[4]Source: Department of Fisheries, “Blue Revolution 2.0 – Pradhan Mantri Matsya Sampada Yojana,” Government of India, dof.gov.in. The extension of Kisan Credit Card coverage to fisheries in 2024 enables farmers to access institutional credit at 7% annual interest rates, reducing financial barriers to feed procurement. State-level subsidies differ across regions, with Andhra Pradesh providing 50% capital subsidies for feed manufacturing units, while West Bengal emphasizes input cost support through cooperative societies. The Fisheries and Aquaculture Infrastructure Development Fund supports cold chain and processing facilities, which increases the demand for quality feeds.

Technical Adoption of High-Protein Formulated Feeds

Protein levels in commercial diets increased to 28-32%, reducing feed conversion ratios to below 1.5:1 on export farms. The use of specialized ingredients, including amino-acid supplements, reduced grow-out time by nearly 20%, enabling higher pond densities and export certifications. Export-oriented shrimp farms show the highest adoption rates, as international buyers include feed quality parameters in sustainability certification requirements. Technology transfer from multinational feed companies has improved the availability of specialized formulations, but their premium pricing restricts adoption among small-scale farmers, resulting in varied adoption rates across the Indian aquafeed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in fishmeal and raw-material prices | −1.5% | Nationwide; coastal manufacturing clusters | Short term (≤ 2 years) |

| Disease outbreaks in aquaculture farming | −1.2% | Intensive farms in South and East India | Medium term (2-4 years) |

| Tighter environmental norms on feed-mill effluent | −0.8% | Industrial hubs in South and West India | Long term (≥ 4 years) |

| Competition from low-cost homemade feeds | −0.9% | Rural ponds across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Fishmeal and Raw Material Prices

Fishmeal prices fluctuated between USD 1,200-1,500 per metric ton in 2024, with quarterly variations of 15-20%[5]Source: United States Department of Agriculture, “Global Agricultural Information Network – India Aquaculture Report,” usda.gov. Soybean meal experienced comparable price volatility, affecting feed production profitability, as raw materials constitute 75% of production costs. Indian feed manufacturers import 60% of their fishmeal requirements from Peru and Chile, making them vulnerable to currency fluctuations and supply chain disruptions. The high proportion of raw material costs in total production expenses makes price stability essential for maintaining export competitiveness.

Disease Outbreaks in Aquaculture Farming

Disease outbreaks significantly impacted aquaculture production in India during 2023-2024. Early Hepatopancreatic Necrosis Syndrome and White Spot Virus reduced shrimp production by 30% in Andhra Pradesh in 2024, decreasing feed consumption and reducing farmer income[6]Source: Central Institute of Brackishwater Aquaculture, “Disease Management in Aquaculture,” ciba.res.in. Disease management protocols require medicated feeds or feeding suspensions, disrupting regular consumption patterns and affecting feed manufacturer revenues. In Tamil Nadu, Tilapia Parvovirus (TiPV) outbreaks in freshwater systems during 2023 resulted in 40-50% mortality rates in severe cases. These recurring disease outbreaks create demand fluctuations that affect production planning and inventory management for feed manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shrimp Feed Drives Premium Growth

Fish feed constituted 53.78% of the India aquaculture feed market share in 2025, driven by the production of carp, tilapia, and catfish for domestic consumption. The extensive carp farming operations in West Bengal and Odisha maintain consistent demand, while tilapia's rapid growth cycle contributes to increased feed consumption. Crustacean feed, despite lower volume, generates higher margins due to its enhanced nutrient requirements and strict export quality standards.

The shrimp feed segment is anticipated to grow at a 9.86% CAGR through 2031, driven by expanding farm areas and increased stocking densities in export-oriented operations. High-protein formulations specifically designed for vannamei shrimp support value growth, complemented by international certifications that emphasize efficient feed conversion and traceability. Major manufacturers' ongoing research and development in functional feed additives improve shrimp gut health and survival rates, establishing this segment as the key revenue generator in the India aquaculture feed market.

By Ingredient: Soybean Meal Dominated the Market

Soybean meal accounts for 34.92% of the India aquaculture feed market size in 2025, supported by domestic production and its balanced amino-acid profile. While fishmeal maintains importance in marine species feeds, its high costs and environmental concerns drive manufacturers to seek protein alternatives. The corn gluten meal segment is projected to grow at a 9.08% CAGR through 2031, driven by increased corn wet-milling capacity and improved cost efficiency.

The market shows increasing adoption of feed additives, including enzymes and probiotics, to improve feed efficiency. While insect meals and single-cell proteins remain in early development stages, they represent potential future ingredients. The industry prioritizes strategies to manage price volatility, reduce dependency on marine ingredients, and improve feed digestibility to maintain a consistent nutrition supply in the India aquaculture feed market.

By Lifecycle Stage: Starter Feed Innovation

Grower feed accounted for 50.78% of India aquaculture feed market share in 2025, due to high consumption during the extended growth phase of aquatic species. The consistent demand across species is supported by farmers' reliance on balanced grower diets to maintain optimal growth rates and survival.

The starter feed segment is anticipated to grow at a 10.35% CAGR, supported by increasing hatchery operations and advancements in micro-pellet technology that improve early-stage survival rates. The use of precision nutrition during larval and fry phases reduces culture cycles and improves pond utilization efficiency. Manufacturers are focusing on micro-encapsulation and particle-size control techniques to enhance nutrient availability, making starter feed a key segment in the India aquaculture feed market. The segment's development includes specialized formulations that address specific nutritional needs, digestive capabilities, and metabolic requirements during different developmental stages. The Coastal Aquaculture Authority's regulations reinforce the need for appropriate feeding protocols in sustainable production practices.

By Form: Extruded (Floating) Technology Upshift

Pellets hold 62.75% of India aquaculture feed market share in 2025, primarily due to their simple production process and widespread acceptance among farmers. Extruded (floating) feeds are growing at a 9.42% CAGR, driven by their higher digestibility and ability to monitor feed consumption. These floating feeds reduce waste, improve water quality, and align with sustainable farming practices. Farmers can observe feeding patterns and adjust feed quantities accordingly, leading to improved growth outcomes.

Powder and liquid concentrate forms cater to specific applications and early growth stages; they remain minor segments. Manufacturers are investing in twin-screw extrusion and density-control technologies to produce feeds with varying buoyancy levels for different aquatic species. Concentrates occupy a small but expanding segment, particularly for nutritional supplements and therapeutic uses where quick absorption is essential. Feed form preferences differ based on species, farming methods, and regional practices, with shrimp farmers preferring sinking pellets and fish farmers opting for floating varieties.

Geography Analysis

South India is driven by Andhra Pradesh's aquaculture output of 1.8 million metric tons and feed manufacturing capacity of over 2 million metric tons annually. Tamil Nadu and Karnataka contribute to growth through integrated brackishwater systems supported by established cold-chain infrastructure. The region maintains its market dominance through technical expertise, suitable climate conditions, and regulatory oversight from the Coastal Aquaculture Authority.

East India's aquaculture sector is expanding through West Bengal's implementation of modern carp farming practices and scientific feeding methods. Odisha's development of brackishwater ponds, supported by Blue Revolution 2.0 grants, contributes to regional growth. The region's adoption of technology from southern states and new feed production facilities under the Pradhan Mantri Matsya Sampada Yojana has increased feed demand along the Bay of Bengal coastline.

North, West, and Central India demonstrate increasing market potential through inland reservoirs and integrated agri-aquaculture systems. Uttar Pradesh and Bihar implement farmer-training programs and subsidized input schemes to increase commercial feed adoption. Maharashtra and Gujarat develop coastal areas for brackishwater aquaculture, and Central Indian states utilize reservoir cages for optimal water resource use, expanding the India aquaculture feed market geographical reach.

Competitive Landscape

The leading producers in the India aquaculture feed market for 2024 include Avanti Feeds Limited, Charoen Pokphand Foods PCL, Growel Feeds Private Limited, IFB Agro Industries Ltd, and Godrej Agrovet Limited. These companies collectively account for a substantial market share, reflecting a moderate level of market concentration. Avanti Feeds Limited maintains market leadership through vertical integration from hatcheries to processing plants. Charoen Pokphand Foods India strengthens its position through global research capabilities and an extensive pan-India dealer network. Growel Feeds Private Limited and Godrej Agrovet Limited complete the market leadership segment, focusing on capacity expansion and specialty product lines.

Market players prioritize capacity expansion, product development, and digital farmer engagement. Avanti's USD 25 million Kovvur plant upgrade in 2024 increases capacity by 200,000 metric tons. Godrej Agrovet introduced ArgoRid in 2025, a fish lice controller developed in collaboration with ICAR-CIFE, to address Argulus infections in aquaculture. The product enhances immunity, healing, and productivity, providing Indian fish farmers with research-based solutions. Companies pursue sustainability certifications, including Best Aquaculture Practices and Aquaculture Stewardship Council, to access export markets and achieve premium pricing.

Environmental compliance requirements and raw material price fluctuations create entry barriers that challenge smaller manufacturers, leading to industry consolidation. Companies increase patent filings for functional additives and precision nutrition, focusing on proprietary feed enzymes and gut-health enhancers. The market increasingly integrates digital advisory platforms, credit-linked sales models, and water-quality solutions as essential service offerings in the India aquaculture feed market.

India Aquaculture Feed Industry Leaders

-

Avanti Feeds Limited

-

Charoen Pokphand Foods PCL

-

Growel Feeds Private Limited

-

IFB Agro Industries Ltd

-

Godrej Agrovet Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: DSM-Firmenich Animal Nutrition & Health (ANH) opened a new feed additive plant in Jadcherla, Hyderabad, India, which includes aquafeed production capabilities. The investment supports the Government's "Make in India" initiative and strengthens ANH's position in India and the Asia-Pacific region. The 11,200-square-meter facility includes a manufacturing line for Mycotoxin Risk Management solutions and a new warehouse.

- June 2025: IFB Agro Industries Ltd. acquired Cargill India's commercial compound shrimp feed and freshwater fish feed business. The acquisition encompasses Cargill India's manufacturing facilities in Vijayawada and Rajahmundry, Andhra Pradesh. The deal includes feed formulations, assets, business contracts, liabilities, licenses, employees, and associated resources.

- July 2025: De Heus opened a new animal feed plant in Rajpura, Punjab, India. The facility produces high-quality feed, including aquafeed, using equipment imported from international suppliers.

India Aquaculture Feed Market Report Scope

Aquaculture feed is any feed containing a balanced mix of essential nutrients such as amino acids, fatty acids, and vitamins administered to aquatic farmed animals as part of aquaculture. The fish feed industry in India is segmented by type (fish feed, mollusk feed, crustacean feed, and other types). Fish feed is sub-segmented into ray-finned fish feed, mackerel feed, ribbon fish feed, cuttlefish feed, catfish feed, and other fish feed. The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Type

| Fish Feed | Carp Feed |

| Salmon Feed | |

| Tilapia Feed | |

| Catfish Feed | |

| Other Fish Feed (Trout Feed, Rohu Feed, etc.) | |

| Mollusk Feed | |

| Crustacean Feed | Shrimp Feed |

| Other Crustacean Feed (Crab Feed, Prawn Feed, Lobstar Feed, etc.) | |

| Other Aquafeed (Turtles, Sea Urchins, Frogs, etc.) |

By Ingredient

| Soybean Meal |

| Fish Meal |

| Corn Gluten Meal |

| Additives (Vitamins, Minerals, Enzymes) |

| Others (Blood meal, Meat and Bone Meal, Groundnut Cake, etc.) |

By Lifecycle Stage

| Starter Feed |

| Grower Feed |

| Finisher Feed |

By Form

| Pellets |

| Extruded (Floating) |

| Powder |

| Liquid Concentrates |

| By Type | Fish Feed | Carp Feed |

| Salmon Feed | ||

| Tilapia Feed | ||

| Catfish Feed | ||

| Other Fish Feed (Trout Feed, Rohu Feed, etc.) | ||

| Mollusk Feed | ||

| Crustacean Feed | Shrimp Feed | |

| Other Crustacean Feed (Crab Feed, Prawn Feed, Lobstar Feed, etc.) | ||

| Other Aquafeed (Turtles, Sea Urchins, Frogs, etc.) | ||

| By Ingredient | Soybean Meal | |

| Fish Meal | ||

| Corn Gluten Meal | ||

| Additives (Vitamins, Minerals, Enzymes) | ||

| Others (Blood meal, Meat and Bone Meal, Groundnut Cake, etc.) | ||

| By Lifecycle Stage | Starter Feed | |

| Grower Feed | ||

| Finisher Feed | ||

| By Form | Pellets | |

| Extruded (Floating) | ||

| Powder | ||

| Liquid Concentrates | ||

Key Questions Answered in the Report

What is the current value of the India aquaculture feed market?

The market is worth USD 3.47 billion in 2026 and is projected to reach USD 4.84 billion by 2031.

Which segment shows the fastest growth within India's aquaculture feed space?

Shrimp feed is projected to expand at a 9.86% CAGR through 2031, driven by export-oriented farming.

Why is soybean meal dominant in India aquaculture feed formulations?

Soybean meal accounts for 34.92% share because it is readily available domestically and offers a balanced amino-acid profile suitable for multiple species.

What regulatory changes affect feed manufacturers most?

Stricter effluent rules introduced in 2024 require zero liquid discharge, prompting investment of USD 50,000-100,000 per plant in treatment systems.

Page last updated on: