Search And Rescue (SAR) Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

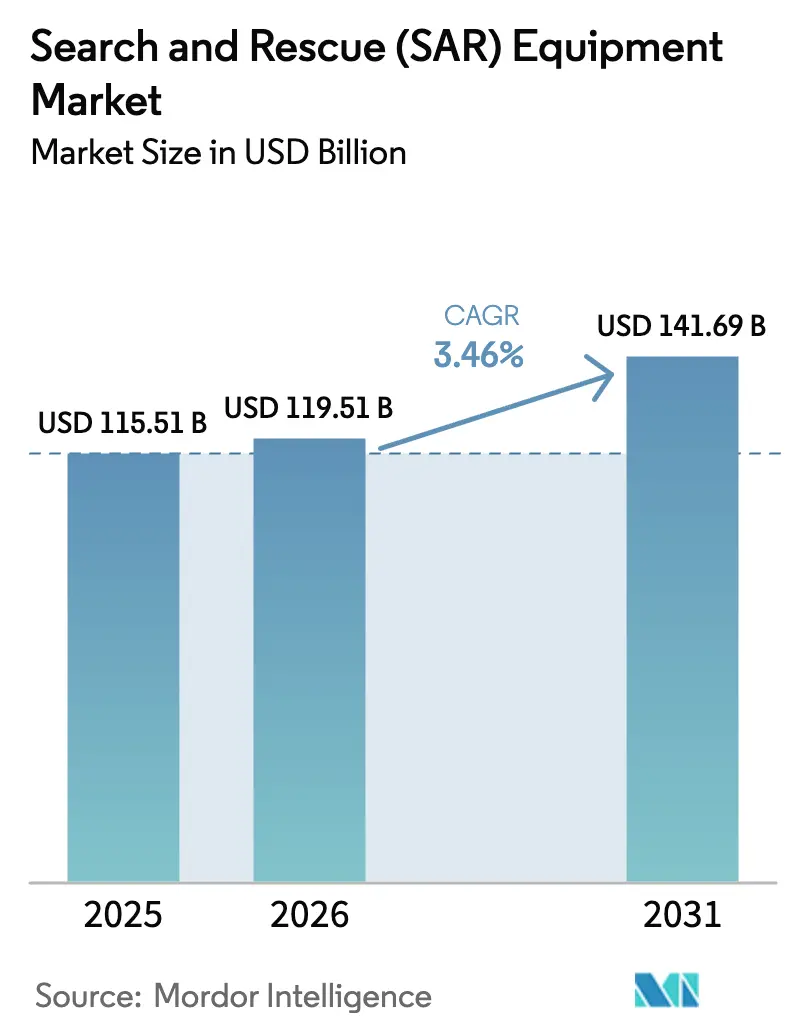

| Market Size (2026) | USD 119.51 Billion |

| Market Size (2031) | USD 141.69 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

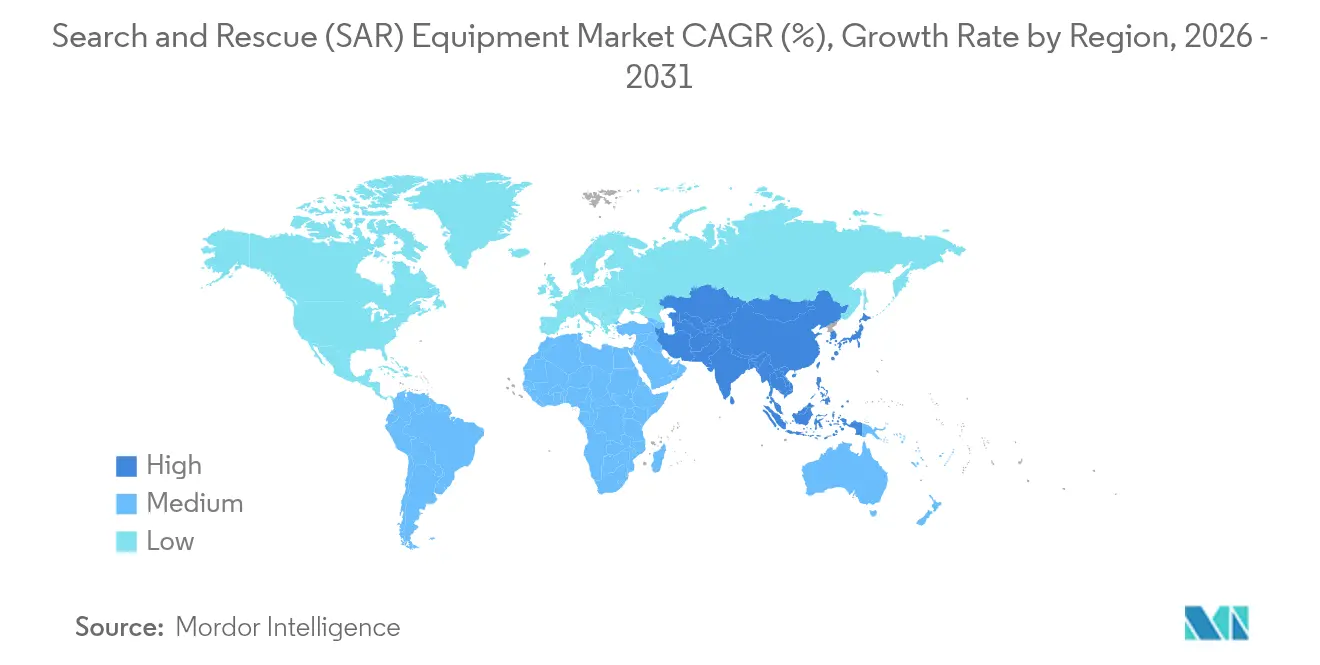

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Search And Rescue (SAR) Equipment Market Analysis by Mordor Intelligence

The search and rescue equipment market size was valued at USD 115.51 billion in 2025 and estimated to grow from USD 119.51 billion in 2026 to reach USD 141.69 billion by 2031, at a CAGR of 3.46% during the forecast period (2026-2031). Escalating climate-driven disasters, the switch to next-generation Cospas-Sarsat beacons, and steady modernization cycles across defense and civilian fleets continue to underpin demand. Autonomous air, surface, and ground platforms linked to LEO-satellite networks are improving mission reach. At the same time, government stimulus, such as Canada’s wildfire-management outlay and the European Union’s rescEU fleet, keeps procurement pipelines active. At the same time, interoperability gaps between analog radios and emerging digital systems pose execution risk, and tighter post-pandemic budgets could slow capital programs in several high-debt economies.

Key Report Takeaways

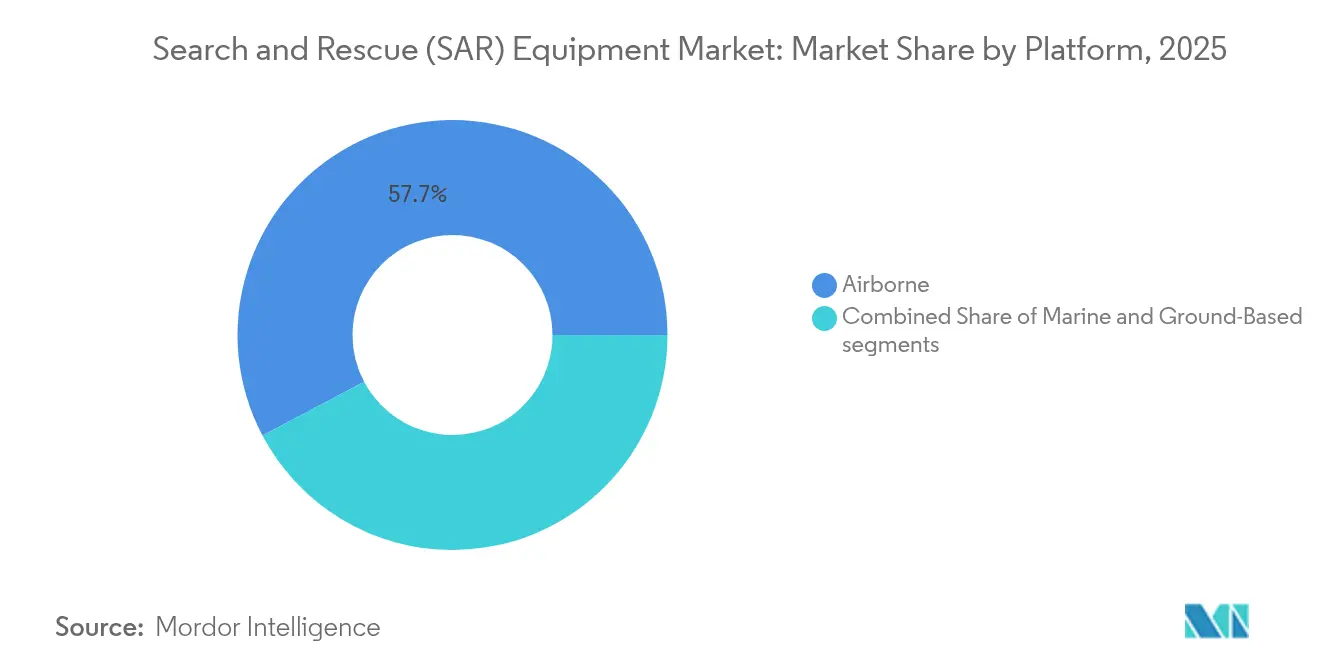

- By platform, airborne systems held 57.74% of the search and rescue equipment market share in 2025, while ground-based systems posted the fastest growth at a 6.05% CAGR through 2031.

- By equipment, communication systems commanded the highest growth profile at 7.12% CAGR, whereas rescue equipment retained 32.10% of the search and rescue equipment market size in 2025.

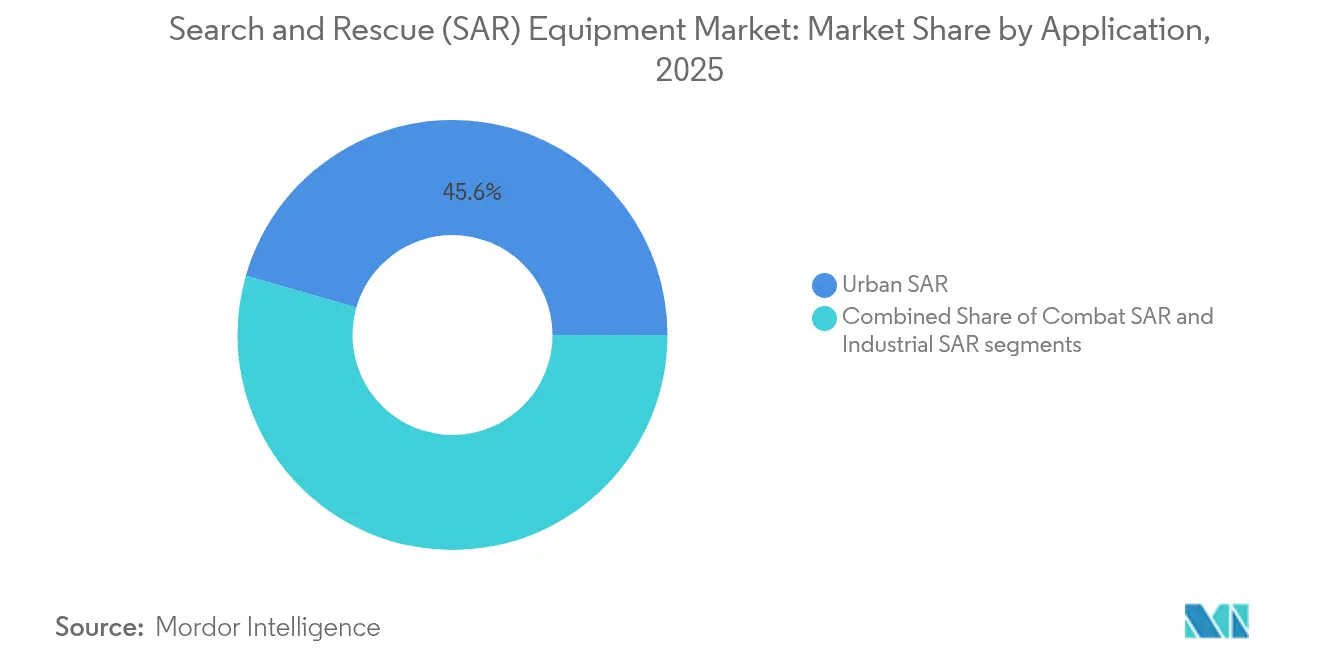

- By application, urban SAR accounted for a 45.55% share in 2025; industrial SAR is projected to expand at a 5.62% CAGR to 2031.

- By end-user, defense and military agencies led with 51.00% revenue share in 2025, while industrial operators are expected to register a 5.66% CAGR through 2031.

- By geography, North America contributed 38.12% of 2025 revenue; Asia-Pacific is set to grow at a 5.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Search And Rescue (SAR) Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency and severity of climate-driven disasters boosting multi-domain SAR procurement | +0.8% | Global, concentrated in North America, Europe, Asia-Pacific coastal regions | Medium term (2-4 years) |

| Proliferation of UAVs and autonomous platforms for wide-area imaging | +0.6% | Global, early adoption in North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| LEO-satellite and IoT convergence enabling real-time situational awareness | +0.5% | Global coverage with priority deployment in remote and maritime areas | Medium term (2-4 years) |

| Expansion of offshore energy, remote mining and polar logistics hubs | +0.4% | Arctic routes, offshore energy corridors, remote mining locations worldwide | Long term (≥ 4 years) |

| Mandatory migration to 2nd-generation Cospas-Sarsat MEOSAR beacons | +0.3% | Global maritime and aviation sectors | Short term (≤ 2 years) |

| Global replacement cycle of aging SAR rotorcraft and fixed-wing fleets | +0.4% | North America and Europe primarily, spillover to developed Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising frequency and severity of climate-driven disasters boosting multi-domain SAR procurement

Severe weather caused USD 380 billion in global economic losses during 2024, leaving a 69% protection gap in insurance coverage. Governments are responding by shifting funding from post-event relief to proactive capability build-outs. Natural Resources Canada earmarked USD 346.1 million for wildfire equipment and training, and similar commitments appear in FEMA’s USD 33.1 billion FY 2025 budget. More billion-dollar storms heighten the need for multi-domain assets that can deploy rapidly across forests, coasts, and urban centers, moving the search and rescue equipment market toward fleet renewals and higher-technology payloads.

Proliferation of UAVs and autonomous platforms for wide-area imaging

Thermal-equipped drones now deliver 95% precision in human-detection trials, and YOLOv8 inference models allow real-time target confirmation. As defense drone spending scales, cost curves favor civilian SAR agencies adopting “drone-as-a-service” contracting. Mixed fleets, such as the Queensland Police’s Bell 429 helicopters and rotary-wing UAS, illustrate operational optimisation in dense urban terrain.

LEO-satellite and IoT convergence enabling real-time situational awareness

Galileo SAR services achieve 100% detection probability with 99.8% location accuracy within 5 km.[1]Source: International Civil Aviation Organization, “Search and Rescue Workshop Presentation,” icao.int Global GNSS revenue is on track to more than double by 2033, and the Return Link Service now offers distress signal confirmation to survivors. Coupled with Earth observation feeds, responders gain continuous weather, thermal, and traffic updates. Consumer devices such as smartphones and satellite SOS further extend redundancy when terrestrial grids fail.

Expansion of offshore energy, remote mining and polar logistics hubs

New Arctic shipping corridors and offshore rigs are spurring purpose-built capacity. Equinor’s five-year lease of AW 139 helicopters, agent-based SAR time-motion models for the Barents Sea, and national workshop findings on North Atlantic crisis response indicate demand for season-adaptive equipment, polar-rated communications, and multinational coordination protocols.[2]Source: Offshore Magazine, “Equinor Boosts North Sea Search and Rescue Helicopter Fleet,” offshore-mag.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-agency certification (Cospas-Sarsat, IMO, FAA, EASA) | –0.4% | Global, heightened complexity in international operations | Medium term (2-4 years) |

| Scarcity of Certified Training for Urban Robotics SAR Crews | –0.3% | Urban centers worldwide, acute shortages in developing regions | Long term (≥ 4 years) |

| Post-pandemic fiscal tightening delaying capital procurements | –0.2% | Developed economies with high debt-to-GDP ratios | Short term (≤ 2 years) |

| Interoperability gaps between legacy analog radios and next-gen digital/AI systems | –0.3% | Global, with legacy system concentration in established markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent multi-agency certification requirements

Complying with IMO, FAA, EASA, and Cospas-Sarsat mandates extends product cycles and raises testing costs, particularly for dual-use payloads needing separate military and civilian approvals. The IAMSAR Manual amendments add equipment tracking obligations, and FCC rule changes in 70/80/90 GHz bands require coordination across maritime and aviation domains, reinforcing the barrier for small entrants.

Scarcity of certified training for urban robotics SAR crews

FEMA backs only 28 Type 1 urban search and rescue task forces nationally, while SkillsUSA competitions highlight a global shortfall in technicians able to run drones, ground robots, and AI-enabled sensors. Community-level CERT programs cover basic first aid, but scaling an advanced curriculum to meet next-gen platform complexity remains a long-term challenge to full equipment utilization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Airborne systems anchor the revenue base

Airborne assets generated 57.74% of 2025 revenue, underscoring the search and rescue equipment market’s reliance on helicopters, fixed-wing aircraft, and UAS. Airbus’s RACER demonstrator delivers 400 km/h cruise and 20% fuel-burn gains, widening the mission envelope for high-speed extractions. Fixed-wing models augment range for open-ocean operations, while long-endurance UAS equipped with synthetic-aperture radar fill detection gaps over rough seas. Blended manned-unmanned tasking reduces sortie cycles and directs crewed platforms to confirmed survivor sites.

Ground-based platforms, however, hold the fastest CAGR at 6.05% as urbanisation and industrial corridors demand all-terrain vehicles, robotic crawlers, and wearable exoskeletons for confined-space rescues. Integration with 5G and edge-computing nodes allows near-instant video offload to command posts. The search and rescue equipment market size for ground solutions is expected to climb steadily as cities harden critical infrastructure and private operators mandate on-site response fleets.

By Equipment: Communication systems accelerate digital transition

Migration from VHF analog radios to software-defined, multi-band devices drives a 7.12% CAGR for communication equipment. FCC approval for high-frequency air-to-surface links unlocks gigabit channels for sensor fusion, while MEOSAR readiness deadlines push beacon refresh cycles. In 2025, rescue equipment still led overall revenue at 32.10%, covering stretchers, power cutters, and evacuation kits. Yet, as agencies prioritise real-time data exchange, the market share for communication suites will witness faster growth.

Search sensors benefit from improved uncooled IR arrays, and rescue radars adopt phased-array steering for clutter rejection. Technical equipment—planning, analytics, and 3D mapping software—leverages AI to automate crew-task pairing and stock-level alerts. Other categories capture emerging IoT beacons and autonomous tenders aimed at hazardous-material scenarios, diversifying supplier opportunities within the broader search and rescue equipment industry.

By Application: Industrial settings outpace broader growth

Urban SAR maintained leadership with 45.55% revenue in 2025, yet industrial SAR posts a 5.62% CAGR as offshore wind, deep-water hydrocarbons, and remote mineral assets demand dedicated coverage. Operators increasingly fund self-contained platforms, citing regulator pressure to shorten response times where government assets are distant. Therefore, the search and rescue equipment market size for industrial use is forecasted to expand more quickly than the combat or maritime public-safety segments.

Combat SAR remains strategically important for defense ministries upgrading night vision, counter-UAS, and electronic warfare suites. Urban environments gravitate toward robotics, thermal imaging, and multiband comms to manage high-rise extractions and tunnel incidents. Each application vertical feeds specialised payload road maps inside the overarching search and rescue equipment market.

By End-User: Industrial operators step up procurement

Defense and military agencies accounted for 51.00% of 2025 sales, but industrial operators—oil, gas, mining, and offshore wind—are on a 5.66% CAGR trajectory as they invest in self-reliant fleets. Dual-use supply chains allow contractors to repurpose military-grade avionics for civilian rigs, aligning with sustainability mandates and insurer expectations. Public-safety departments continue to benefit from FEMA grants and regional cost-share schemes, though capital pacing may soften under fiscal tightening.

Cross-sector convergence is rising: defense prime RTX Corporation fields hyperspectral sensors adaptable for commercial pipeline monitoring, while private energy majors lease spare rotorcraft time to coastal guard units during low-demand windows. Such partnerships expand addressable revenue without overextending public budgets, strengthening resilience across the search and rescue equipment market.

Geography Analysis

North America controlled 38.12% of 2025 turnover, anchored by FEMA’s USD 33.1 billion fiscal-year budget and sustained Coast Guard, Air Force, and state wildfire outlays. The region’s integrated aerospace-industrial base accelerates the fielding of hybrid-electric propulsion, polar hardening kits, and cloud-based command software, keeping the search and rescue equipment market ahead in capability.

Europe maintains a sizable share through rescEU pooled assets and Galileo’s mature SAR payload. Joint procurement drives volume discounts, while Arctic member states channel funds into ice-class hulls and long-range drones. Europe’s regulatory emphasis on green aviation also nudges suppliers to develop biofuel-compatible engines and recyclable composite structures.

Asia-Pacific is the fastest-growing theatre at 5.57% CAGR. Rapid coastal urbanisation, frequent typhoons, and seismic hazards force governments to upscale inventories—from Japan’s satellite-enabled command upgrade to Australia’s Disaster Ready Fund. Industrial SAR revenues grow as LNG carriers, offshore rigs, and mountain mining sites purchase bespoke kits. Cross-border disaster-relief exercises foster doctrine convergence and shore up regional demand for interoperable systems.

Competitive Landscape

The market shows moderate concentration: top defense conglomerates combine airframes, sensors, and networking software into turnkey packages, yet category fragmentation leaves room for niche innovators. RTX Corporation’s USD 218 billion backlog and USD 10.3 billion annual R&D spend exemplify scale advantages. Airbus leverages rotorcraft speed records to secure high-altitude, long-range tenders, whereas Leonardo fields AW 139 variants tailored for offshore leases like Equinor’s North Sea program.

Technology trends emphasise open-architecture avionics, AI-assisted mission planning, and modular payload bays. Established players partner with software start-ups for computer-vision triage tools or sat-com operators for resilient L-band connectivity. New entrants focus on swarm-capable micro-UAS, low-SWaP sensors, and cloud-native command dashboards, gradually eroding incumbent share in subsystem niches.

Industrial operators increasingly procure directly, squeezing margins for intermediaries but providing specialist vendors a foothold. Meanwhile, governments push domestic content rules, which could reshape sourcing for foreign primes and invite joint-venture assembly lines. Over time, strategic manoeuvring will hinge on accelerating certification cycles and bundling training solutions to close skill gaps.

Search And Rescue (SAR) Equipment Industry Leaders

RTX Corporation

Thales Group

Honeywell International, Inc.

Leonardo S.p.A.

Textron Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Fluid Watercraft unveiled new Search and Rescue (SAR) boats. The rigid inflatable boats (RIBs) incorporate technology to support first responder marine operations.

- January 2024: Equinor ASA awarded Lufttransport a five-year contract for two Leonardo AW 139 SAR helicopters in the North Sea Troll and Oseberg areas.

- June 2023: Subject to final approvals, Bristow Ireland Limited stands to secure a potential USD 714 million contract from the Irish government for Coast Guard Search and Rescue (SAR) operations. This contract is set to ensure round-the-clock operations at four helicopter bases located in Sligo, Shannon, Waterford, and Dublin, and includes provisions for a fixed-wing aircraft component.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the search & rescue (SAR) equipment market as the global sale of purpose-built hardware and associated kits deployed on airborne, marine, and ground platforms to locate, stabilize, and evacuate people in life-threatening situations. Equipment ranges from personal locator beacons, infrared and radar search sensors, satellite or software-defined radios, stretchers, and power rescue tools to entire missionized craft and UAV payloads.

Scope Exclusion: routine firefighting hoses, standard ambulances, and generic first-aid consumables that are not certified for SAR missions remain outside this frame.

Segmentation Overview

- By Platform

- Airborne

- Helicopters

- Fixed-Wing Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Marine

- Ground-Based

- Airborne

- By Equipment

- Rescue Equipment

- Power Rescue Tools

- Medical and Evacuation Kits

- Search Equipment

- Thermal / IR Sensors

- Rescue Radars

- Communication Equipment

- SATCOM Terminals

- Software-Defined Radios

- Technical Equipment

- Planning and Command Systems

- Other Equipment

- Rescue Equipment

- By Application

- Combat SAR

- Urban SAR

- Industrial SAR

- By End-User

- Defense and Military Agencies

- Public Safety and Law-Enforcement

- Industrial Operators

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed coast-guard logistics heads, civil defense buyers, SAR squadron commanders, and product managers across North America, Europe, Asia-Pacific, and the Middle East. Their inputs clarified real-world adoption lags, average selling prices, and upgrade triggers, allowing us to reconcile secondary totals and assumptions.

Desk Research

We start with open-source pillars such as International Maritime Organization carriage mandates, International Civil Aviation Organization Annex 12 records, United Nations OCHA disaster event charts, National Fire Protection Association rescue standards, and U.S. Federal Procurement Data System contract releases. Company 10-Ks, coast-guard budget bills, and reputable trade journals complement these baselines. Paid dashboards, including D&B Hoovers for supplier financials and Aviation Week fleet logs, let us sanity-check unit deliveries and retrofit cycles. The sources cited illustrate the evidence pool only; analysts referred to many others while building and validating the dataset.

Market-Sizing & Forecasting

A top-down construct begins with platform inventories and disaster incidence statistics, which are then matched with equipment fit rates and replacement windows. Select bottom-up checks, supplier shipment rollups and sampled ASP × volume for beacons, stretchers, and rescue winches, tighten each region's spend curve. Key variables shaping the model include: 1) mandated EPIRB carriage per SOLAS vessel, 2) annual helicopter procurement budgets, 3) average disaster response hours logged per country, 4) UAV penetration in SAR sorties, and 5) inflation-adjusted defense outlays. A multivariate regression blends these indicators to project demand through 2030, while scenario buffers cover extreme disaster years and currency swings.

Data Validation & Update Cycle

Outputs undergo variance checks against import data (Volza), media-reported contract values (Dow Jones Factiva), and prior-year actuals. Senior reviewers clear anomalies before sign-off. Reports refresh annually, with mid-cycle revisions triggered by large-ticket procurements or regulatory shifts; a last-minute analyst sweep ensures clients receive the latest view.

Why Our Search and Rescue Equipment Baseline Proves Dependable

Estimates published across the industry often diverge because firms pick different cut-off years, include or omit multi-mission craft, or overlook currency effects. According to Mordor Intelligence, clarity on scope and recurring data hygiene keeps our baseline firmly grounded.

Key gap drivers arise when others fold in training services, drop marine-only assets, or forecast off legacy growth curves that ignore UAV uptake and MEOSAR beacon upgrades. Divergent refresh cadences and inconsistent exchange rates widen spreads further.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 115.51 B (2025) | Mordor Intelligence | |

| USD 128.60 B (2024) | Global Consultancy A | Includes SAR vehicles and support contracts; relies on single top-down macro factor |

| USD 93.72 B (2025) | Trade Journal B | Excludes marine communication suites; uses constant 2023 currency, no inflation pass-through |

| USD 2.35 B (2024) | Regional Consultancy C | Tracks only handheld devices and PPE; narrow geographic coverage |

Taken together, the comparison shows that when the right scope, variables, and yearly updates align, as they do in Mordor's approach, decision-makers receive a balanced, transparent starting point that they can readily audit and replicate.

Key Questions Answered in the Report

What is the current value of the search and rescue equipment market?

The market is valued at USD 119.51 billion in 2026 and is forecasted to grow to USD 141.69 billion by 2031 at a 3.46% CAGR.

Which platform segment leads the market?

Airborne systems dominated with 57.74% revenue share in 2025, reflecting the mission flexibility of helicopters, fixed-wing aircraft and UAS.

Why are communication systems the fastest-growing equipment category?

Agencies are replacing analog radios with multi-band, software-defined devices to support AI and satellite data streams, giving the segment a 7.12% CAGR.

Which region is expanding quickest?

Asia-Pacific posts the fastest regional growth as coastal development, frequent natural disasters and defense upgrades drive procurement.

How are industrial operators influencing demand?

Offshore energy, mining and polar logistics companies are investing in self-contained fleets, making industrial operators the fastest-growing end-user group.

What is the biggest restraint on market growth?

Complex, multi-agency certification processes lengthen development timelines and raise costs, particularly for new entrants making dual-use equipment.

Page last updated on: