Naval Radar Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.98 Billion |

| Market Size (2031) | USD 12.57 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

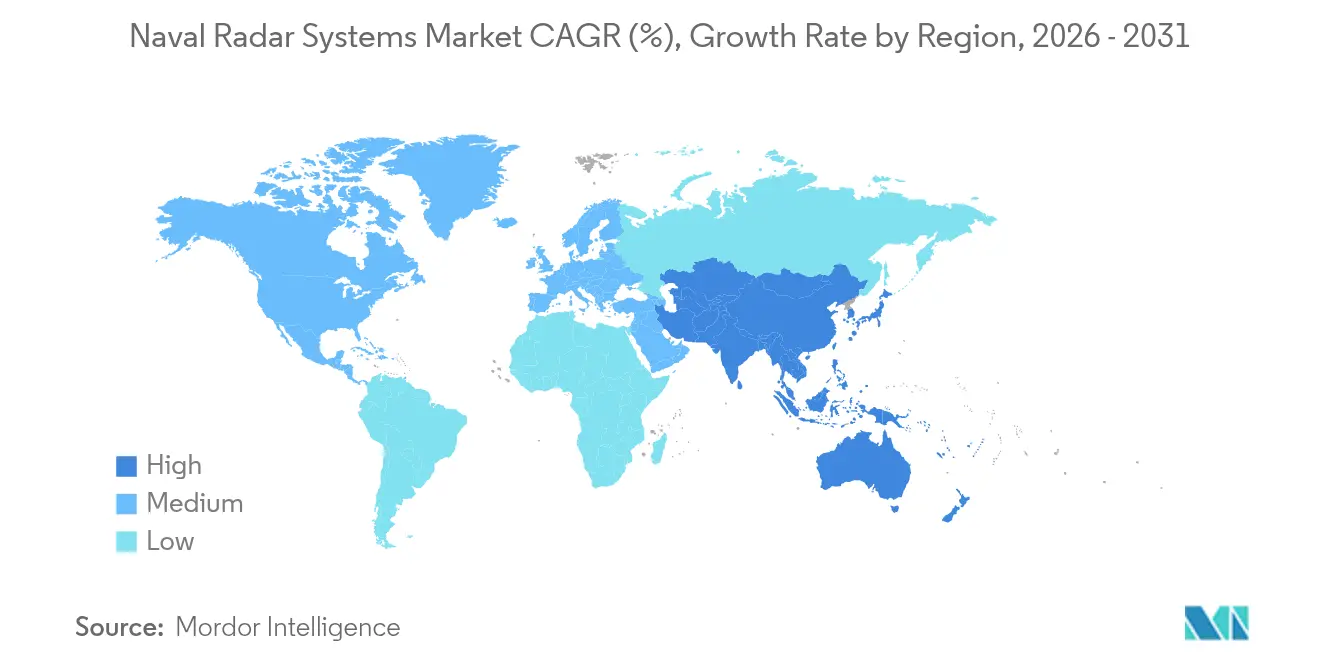

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Naval Radar Systems Market Analysis by Mordor Intelligence

The naval radar systems market size is expected to grow from USD 9.53 billion in 2025 to USD 9.98 billion in 2026 and is forecast to reach USD 12.57 billion by 2031 at 4.72% CAGR over 2026-2031. Sustained demand springs from multi-domain missile threats, a transition from legacy 2-D sensors, and the need for radar electronic warfare (EW) fusion that shortens kill-chain timelines. Falling GaN cost curves, now below USD 4 per watt, enable affordable power-dense transmit-receive modules, helping suppliers preserve margins despite aggressive price negotiations. Modernization funding remains anchored in North America and Europe. Yet, Indo-Pacific surface-fleet growth tilts future volume toward Asia-Pacific, keeping the naval radar systems market on a resilient, mid-single-digit trajectory. Competitive dynamics intensify as primes consolidate RF component supply chains to hedge against gallium export controls while smaller firms use AI-enabled architectures to penetrate emerging unmanned segments.

Key Report Takeaways

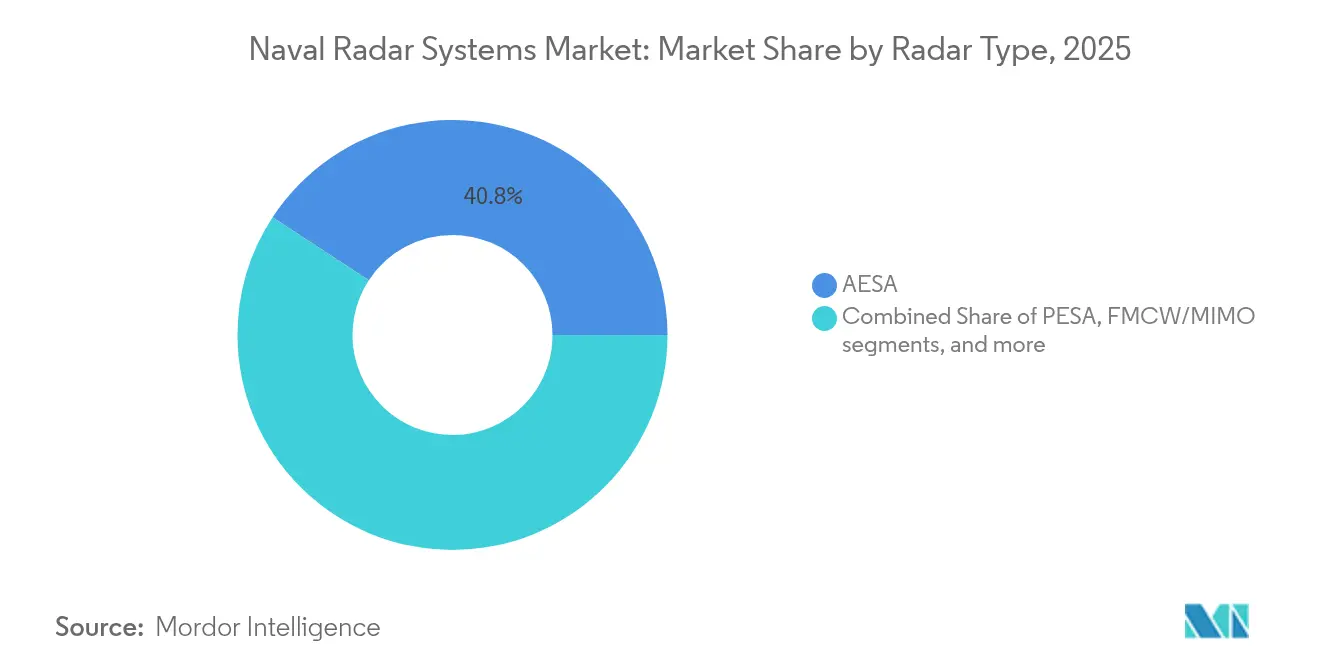

- By radar type, AESA accounted for 40.78% of the naval radar systems market share in 2025, whereas FMCW/MIMO is poised for the fastest 6.55% CAGR through 2031.

- By platform, destroyers and cruisers commanded a 38.74% share of the naval radar systems market in 2025, while unmanned surface and AUV platforms are projected to expand at an 8.12% CAGR.

- By application, surveillance and early-warning held 31.92% share of the naval radar systems market size in 2025; electronic-warfare support is forecasted to grow at 5.62% CAGR.

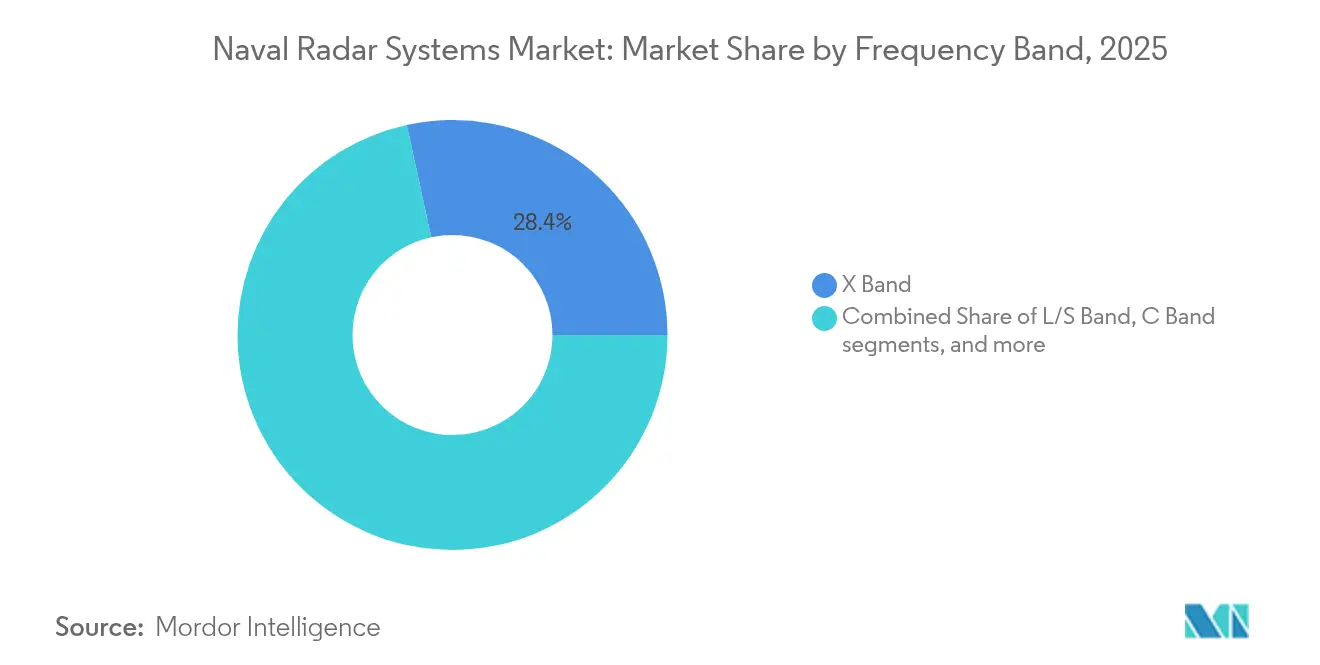

- By frequency band, the X-band remained dominant with a 28.41% share, yet Ku/Ka-band solutions are on track for a 6.52% CAGR.

- By component, antenna and array panels captured a 35.62% share, and transmitters/power amplifiers are set for the quickest 4.65% CAGR.

- By range, short-range systems (less than 50 km) secured a 40.86% share, whereas long-range systems (greater than 200 km) should rise at a 7.42% CAGR.

- By geography, North America retained a 37.21% share of the naval radar systems market in 2025; Asia-Pacific is advancing at an 8.31% regional CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Naval Radar Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating multi-domain missile threats | +1.2% | Indo-Pacific and Middle East | Medium term (2-4 years) |

| Modernization cycles from 2-D to AESA | +0.8% | North America and Europe | Long term (≥4 years) |

| Indo-Pacific naval build-up and frigate programs | +0.7% | Asia-Pacific | Medium term (2-4 years) |

| Mandatory radar cross-section management | +0.4% | Global | Long term (≥4 years) |

| GaN cost curve less than USD 4/W | +0.6% | Global | Short term (≤2 years) |

| Integration of radar-EW fusion chips | +0.5% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Multi-Domain Missile Threats

Shipborne radar requirements changed after sea-skimming, and hypersonic missiles showcased harsh lessons in the Red Sea and overwhelming legacy sensors during saturation raids. The US Navy accelerated SPY-6 back-fit packages beginning in 2026 with a USD 536 million budget to bolster detection windows.[1]Company Release, “SPY-6 Back-Fit Program Accelerated,” Naval News, navalnews.com China’s push toward near-light-speed radar that reveals submarines hundreds of meters below the surface widens the technology gap and presses allies to field agile multi-function arrays. As a result, suppliers are designing software-defined waveforms that concurrently track ballistic, hypersonic, and sea-skimming profiles without mode-switch latency. These converging threats underpin a steady spending cadence inside the naval radar systems market.

Modernization Cycles of Aged 2-D Radars to AESA

Frigates and destroyers commissioned before 2005 are near obsolescence, triggering large-scale AESA retrofits such as Germany’s EUR 200 million (USD 232.42 million) F124 upgrade awarded to Hensoldt and IAI. The Netherlands followed with four air-defense frigates worth EUR 3.5 billion (USD 4.07 billion), embedding active-phased-array suites at the build stage rather than mid-life. South Korea’s Hanwha Systems prototype can concurrently track 4,000 targets, illustrating sovereign technology responses to export limits. Replacement programs increasingly value firmware-driven enhancements that avoid dry-dock structural changes. These dynamics lock in a predictable upgrade backlog supporting the naval radar systems market expansion through 2030.

Indo-Pacific Naval Build-Up and Frigate Programs

Australia committed AUD 50 billion (USD 32.47 billion) to double its surface fleet, lining up multi-year radar procurement arcs that uplift regional demand. Japan’s first SPY-7(V)1 for its Aegis-equipped vessels delivers S-band GaN power with 4,828 km terrestrial reach. The Philippines fielded Mitsubishi Electric FPS-3ME units valued at PHP 5.5 billion (USD 96.76 million) to strengthen maritime domain awareness. Taiwan’s sole-source Raytheon contract further tightens schedules amid rising cross-strait tension. These programs underpin the fastest regional CAGR in the naval radar systems market.

Mandatory Radar Cross-Section Management

Stealth-centric navies now mandate integrated masts and flush sensor mounting, yielding up to 46.46 dBsm arithmetic mean signature reduction versus conventional layouts. Early design involvement between shipyards and radar OEMs uses a shooting-and-bouncing-rays simulation to optimize antenna placement across multi-band threats. The collaboration aligns survivability, sensor performance, and electromagnetic compatibility without retrofit penalties. Consequently, low-observable requirements move from “nice-to-have” to baseline contract specification, sustaining premium pricing power for compliant solutions.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control limits on GaN MMICs | -0.9% | Global | Medium term (2-4 years) |

| Cost overruns driving radar de-scoping | -0.6% | North America and Europe | Short term (≤2 years) |

| Littoral S/X-band spectrum congestion | -0.4% | Coastal regions | Long term (≥4 years) |

| Hull-top weight and power constraints | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-Control Limits on GaN MMICs

China controls 85% of the primary gallium supply, and recent export curbs elevate procurement risk for Western radars using GaN modules. US export listings further restrict 40–230 GHz devices, complicating co-development with allies.[2]Bureau Release, “Commerce Control List—Category 6,” Bureau of Industry and Security, bis.doc.gov Washington and Brussels sponsor domestic gallium refineries, yet multi-year timelines keep dependency high, inserting delivery uncertainty into several naval radar systems market contracts.

Cost Overruns Driving Radar De-Scoping

The US Navy swapped its Dual Band Radar for Enterprise Air Surveillance Radar on CVN-79, cutting USD 180 million but lowering performance.[3]Sam LaGrone, “Cost-Driven Radar Swap on CVN-79,” USNI News, news.usni.org GAO highlights AN/SPY-6 schedule slips rooted in underestimated software complexity, echoing across allied budgets. Fiscal ceilings force capability trade-offs that dampen near-term revenue for high-end sensors inside the naval radar systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Radar Type: AESA Dominance Drives Modernization

AESA systems held the largest 40.78% naval radar systems market share in 2025, thanks to robust multi-target tracking and jam-resistant digital beamforming. The naval radar systems market size for FMCW/MIMO radars is projected to expand at 6.55% CAGR through 2031, propelled by demand for software-defined multifunctionality that supports concurrent communications links. Traditional passive electronically scanned arrays (PESA) linger in cost-sensitive upgrades, while quantum and photonic concepts occupy the “Others” category as long-range R&D bets.

Lockheed Martin’s SPY-7 demonstrated persistent tracking for Spain’s F-110 frigate program, with delivery in 2026 and commissioning in 2028. Meanwhile, FMCW solutions migrating from automotive supply chains show favorable volume economics, compressing entry barriers for new vendors. Cross-domain algorithm sharing reduces development cycles, giving navies affordable pathways to plug-and-play waveform libraries that future-proof their fleet sensors.

By Platform: Unmanned Systems Reshape Naval Operations

Destroyers and cruisers accounted for 38.74% of the overall naval radar systems market size in 2025 because fleet air-defense doctrines still center on large combatants. However, unmanned surface and AUV platforms head the growth table with an 8.12% CAGR, reflecting distributed lethality strategies that call for low-signature scouts.

Miniaturized GaN power amplifiers and conformal antennas now satisfy the size, weight, and power (SWaP) envelopes of unmanned hulls, unlocking new procurement layers. Submarine mast radars also advance, enabling periscope-depth situational awareness with minimal exposure. Modular “payload bay” concepts allow common sensor cores to slide between unmanned and manned vessels, lowering integration costs and stoking cross-platform fleet standardization.

By Application: Electronic Warfare Integration Accelerates

Surveillance and early warning maintained a 31.92% share of the naval radar systems market in 2025, remaining indispensable for blue-water command decisions. The naval radar systems market size for electronic-warfare support is on track for a 5.62% CAGR as adversaries flood the spectrum with agile jamming, forcing navies to embed EW receivers within primary radar tiles.

Collins Aerospace’s USD 904 million Cooperative Engagement Capability upgrade stitches AESA radar tracks into secure datalinks, fusing threat libraries across distributed vessels. AI-based classifiers now auto-label emitter fingerprints, cutting operator reaction time. Surveillance, fire-control, and EW codebases converge onto a single back-plane, promising lifecycle cost drops as navies update mission packages via secure patches instead of hull visits.

By Frequency Band: X-Band Leadership Faces Ku/Ka Challenge

X-band radars retained a 28.41% share in 2025 owing to optimal sea-state clutter rejection and mature fire-control algorithms. The naval radar systems market size for Ku/Ka-band systems is projected to broaden at a 6.52% CAGR because high-resolution imaging and SATCOM coexistence drive dual-band procurement.

Dynamic spectrum-sharing research indicates S-band radars can cohabitate with LTE at greater than 50 km separation, but regulatory adoption remains slow. Cognitive radar prototypes using reinforcement learning alter pulse patterns in real time, minimizing mutual interference. Software-defined architectures allow quick band reconfiguration, empowering navies to match emission profiles with mission threat envelopes and sovereign spectrum rules.

By Component: Antenna Innovation Drives Performance

Antenna and array panels cornered 35.62% of 2025 revenue, defining system gain and beam agility. Transmitters and power amplifiers are heading for the highest 4.65% CAGR as GaN parts deliver triple the power density of legacy gallium-arsenide devices.

Modular tile arrays let maintainers swap failed modules dockside, avoiding lengthy depot visits. Photonic front-ends promise wider instantaneous bandwidth yet remain mostly in laboratory validation. Meanwhile, AI-tuned cooling loops lower array junction temperatures by 8 °C, extending mean-time-between-failure and sharpening radar availability metrics across the naval radar systems market.

By Range: Long-Range Systems Lead Growth

Short-range radars under 50 km captured 40.86% of the 2025 demand for navigation, harbor defense, and close-in gun support. Long-range systems over 200 km should advance at 7.42% CAGR as ballistic missile defense (BMD) fleets roll out persistent discrimination radars capable of 360° volumetric tracking.

Distributed power architectures reduce cabling mass in multi-antenna airborne platforms, concepts now migrating to naval topside arrays. Short-range FMCW modes embed inside larger AESA packages, giving commanders a digital “zoom lens” that flexes between local force-protection and theater-wide cueing without hardware swaps.

Geography Analysis

North America led with 37.21% of the naval radar systems market share in 2025, underpinned by the US Navy’s plan to install SPY-6 on 65 surface combatants and to field Enterprise Air Surveillance Radar aboard future carriers. Canada’s selection of SPY-7 for River-class destroyers adds cross-border industrial synergy, while Mexico’s incremental coastal surveillance upgrades leave room for follow-on orders. Robust defense budgets exceeding USD 800 billion provided multiyear funding visibility, enabling OEMs to lock in scale pricing for GaN devices.

Asia-Pacific represents the fastest-growing cluster, expanding at 8.31% CAGR to 2031 as China’s submarine-tracking radar tests accelerate regional procurement urgency. Japan’s USD 41 million indigenous long-range radar program and South Korea’s KDX-II destroyer refits, worth USD 300 million, evidence a strategic tilt toward sovereign sensor ecosystems. Australia’s AUD 50 billion (USD 32.47 billion) fleet expansion and the Philippines’ PHP 5.5 billion (USD 96.76 million) radar import package underscore the region’s broad spending front, cushioning suppliers against order volatility elsewhere.

Europe posts steady gains as NATO cohesion intensifies. Germany’s EUR 200 million (USD 232.42 million) ( F124 upgrade and the Netherlands’ EUR 3.5 billion (USD 4.07 billion) frigate build ensure a rolling backlog. Spain integrates SPY-7 into F-110 hulls, while the Franco-Italian Horizon mid-life overhaul, worth EUR 1.5 billion (USD 1.74 billion), pushes common standards across multiple navies. Eastern Mediterranean tensions nudge Greece toward new air-defense frigates, and Norway eyes enhanced coastal sensors, suggesting a secure medium-term growth lane despite fiscal scrutiny.

Regulatory Landscape

Naval radar equipment must align with international maritime safety and performance baselines where applicable, anchored by IMO Resolution MSC.192(79) for shipborne radar. Beyond IMO, market access and certification are shaped by country and region-specific radio equipment and spectrum rules, including ISED RSS-238 in Canada for shipborne radar operating in the 2,900-3,100 MHz and 9,225-9,500 MHz bands.

Defense electronics supply and collaboration are also influenced by export control frameworks and periodic rulemaking. The US Department of Commerce, Bureau of Industry and Security (BIS) issued export control updates in October 2024 and January 2026 that eased certain licensing requirements for specific technologies to close allies (notably Australia, Canada, and the United Kingdom), supporting cross-border industrial teaming and supply chain planning. China also refreshed its national standard ecosystem for marine radar, including GB/T 9391-2025, with an effective date of May 1, 2026, creating an additional compliance touchpoint for OEMs and integrators selling into or sourcing from China.

Value Chain Analysis

The naval radar systems value chain starts with upstream raw materials and microelectronics, where gallium and GaN device availability shapes cost, lead times, and exportability. This flows into GaN foundry services and packaging, followed by transmit/receive module assembly, antenna and array panel integration, and high performance digital processing hardware. Primes and key subsystem suppliers then build waveform and signal processing software, deliver system integration (including combat system and EW interfaces), and provide shipboard installation support, either through direct naval procurement channels or via Foreign Military Sales pathways.

Downstream activities include acceptance testing, sea trials, and configuration management for mission updates. Modular open system approaches and software-defined radar work reduce the need for hardware redesign cycles. Program activity also shows the chain's service and upgrade intensity, with ManTech receiving a five year USD 197 million contract in July 2026 to support RDT&E services to modernize ship surface radar systems, and Indra contracting with Kongsberg Defence and Aerospace in April 2026 to supply EW and radar systems for six Type 212CD submarines for Germany and Norway. Together, these moves highlight the role of integration houses, test infrastructure, and long tail engineering support alongside hardware manufacturing capacity.

Competitive Landscape

The naval radar systems market is moderately concentrated. RTX Corporation, Lockheed Martin Corporation, Thales Group, and Northrop Grumman Corporation collectively account for major revenue, each leveraging vertically integrated semiconductor lines, ship-set integration teams, and in-house signal-processing IP. Their scale affords early access to scarce gallium supplies and the capital required for 200 kW-class GaN amplifier development.

Disruption nevertheless brews at the edges. Echodyne’s metamaterial apertures furnish high-gain dishes at a fraction of legacy cost, enabling small patrol craft to host precision sensors for the first time. Anduril’s 2025 acquisition of Numerica folded Spyglass radar into its AI-centric Lattice platform, showcasing how software-first entrants swallow RF specialists to present turnkey solutions. Meanwhile, Ultra Maritime’s USD 421 million surface-search radar award shows that second-tier players can secure marquee contracts by emphasizing open-architecture compliance.

Strategic themes revolve around control of GaN wafer capacity, sensor-EW convergence, and autonomy-ready designs. Primes cultivate sovereign fabs to alleviate embargo risk. European mid-caps partner on shared aperture demonstrators to win export licenses barred to US ITAR-laden gear. Joint ventures and co-development memoranda of understanding aim to bundle training, digital twin, and lifecycle support, tilting competition toward service-based revenue streams that grow faster than hardware alone within the naval radar systems market.

Naval Radar Systems Industry Leaders

RTX Corporation

Thales Group

Northrop Grumman Corporation

HENSOLDT AG

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Modernization and backfit programs on legacy hulls remain a visible whitespace, with navies seeking improved detection windows against sea skimming and complex raid profiles without incurring major structural changes. The US Navy budgeted USD 536 million beginning in 2026 to accelerate SPY-6 backfit packages, and the June 2026 USD 515 million US Navy contract for the SPY-6 family (including upgrades for Flight IIA destroyers) reinforces a broad installed base that supports recurring opportunities in integration, testing, and configuration updates around a common radar family.

Software defined and modular radar architectures create a second opportunity lane, particularly for radar-EW fusion and rapid waveform updates delivered as capability increments. In May 2026, the Office of Naval Research awarded RTX (Raytheon) a contract to advance next generation software defined radar capability, indicating demand for independently operable building blocks and faster mission adaptation. International programs also expand addressable demand for shipset radars through standardized combat system ecosystems, including the April 2026 US approval of an AEGIS and AN/SPY-6(V)1 package for Germanys F127 frigates, which increases interoperability driven procurement and associated supply chain scaling requirements.

Recent Industry Developments

- June 2026: RTX (Raytheon) received a USD 515 million US Navy contract for the SPY-6 family of radars, covering continued integration, test, and production support, including upgrades for Flight IIA destroyers and support tied to Germanys F127 program. The award reinforces the SPY-6 centered roadmap across multiple ship classes and sustains demand for GaN arrays, integration labor, and qualification throughput. It also increases program scale that can pull allied requirements into a more common radar and combat system ecosystem.

- October 2025: RTX announced Germanys selection of the SPY-6(V)1 radar for its future F127 frigates. The decision strengthens the Foreign Military Sales channel for high-end naval AESA radars and links European fleet modernization to US origin radar architectures. It also raises the importance of exportable configurations, long lead microelectronics planning, and interoperability driven integration services.

- September 2024: The US Department of Commerce, Bureau of Industry and Security (BIS) published an export control rule update affecting licensing for certain advanced technologies and allied destinations. Export control clarity influences how radar OEMs structure international teaming, component sourcing, and downstream re export permissions for naval radar subsystems. The update also factors into supplier strategies to localize sensitive microelectronics steps and reduce schedule risk tied to controlled items.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the naval radar systems market covers radar equipment and embedded software installed on naval platforms to detect, track, and support navigation and fire control. It includes new-build fitment sold with ship construction, and it also includes upgrade kits sold into fleet modernization programs.

Scope exclusions: Shore-based coastal surveillance radars, civil marine radars used on merchant vessels, and post-warranty maintenance revenue are excluded.

Segmentation Overview

- By Radar Type

- AESA

- PESA

- FMCW/MIMO

- Others

- By Platform

- Destroyers and Cruisers

- Frigates

- Corvettes and OPVs

- Aircraft Carriers and Amphibious Ships

- Submarines (mast-mounted)

- Unmanned Surface/AUV Platforms

- By Application

- Surveillance and Early Warning

- Missile Guidance/Fire Control

- Navigation and Collision-Avoidance

- Surface Search and Target Tracking

- Weather and Environmental Monitoring

- Electronic Warfare Support

- By Frequency Band

- L/S Band

- C Band

- X Band

- Ku/Ka Band

- By Component

- Transmitter/Power Amplifier

- Receiver/Down-converter

- Antenna/Array Panels

- Other Components

- By Range

- Short (Less than 50 km)

- Medium (50–200 km)

- Long (Greater than 200 km)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Taiwan

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Turkey

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pinning down the demand pool, which is the active fleet, the new ships and submarines entering service, and the upgrade timing for legacy platforms. We reference public defense budget documents, national procurement portals, and audit publications (such as GAO-style reports) to understand program timing and funding flow. To keep platform counts and deliveries grounded, sources such as IISS Military Balance summaries, UNROCA disclosures, and government ship registries are reviewed where available.

We also use open sources such as customs and trade statistics (where radar-related codes are meaningful), patent databases for radar and AESA-related filings, and peer-reviewed journals that discuss naval sensor performance trends and integration constraints. Company filings, investor presentations, and credible defense press are used to map contract wins to system classes and upgrade cycles. Paid subscriptions are applied selectively for company financials and intelligence, defense contracts and tenders, and aircraft and ship program databases that help cross-check timelines. The sources listed here are illustrative, and many other public documents were read to fill gaps and validate assumptions.

Primary Interviews and Surveys

Primary work is used to test what desk signals cannot confirm cleanly, including typical radar shipset quantities, upgrade content by class, and how pricing changes when new transmit-receive modules and software-defined processing are introduced. We spoke with a mix of OEM-side roles, naval procurement and program stakeholders, and integrators across major shipbuilding and operating regions, so the assumptions reflect delivery patterns rather than announced intent only.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 48% |

| Mid tier: 52% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 18% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built with a top-down approach where fleet and shipbuilding data are reconstructed into an annual installation and upgrade opportunity, which is then converted into revenue using typical system values by platform class. The model is anchored on indicators such as active surface combatant and submarine counts, new-build deliveries, mid-life upgrade cadence, radar fit per platform, and the mix shift toward AESA and multi-function radar suites. When budgets and programs are visible, planned spend is filtered through delivery schedules so the timing matches procurement reality.

Selective bottom-up approximations are used to keep totals realistic, including a roll-up of publicly disclosed contracts, sampled pricing checks from tenders, and sanity checks using supplier revenue exposure to naval sensors. Where contract detail is missing, gaps are handled with class-based proxies (for example, applying a typical upgrade package value to a known set of hulls scheduled for refit). Forecasting is done using scenario analysis supported by expert inputs on shipbuilding throughput, defense funding direction, and expected adoption pace of modern arrays and processing upgrades.

Data Validation & Update Cycle

Validation is done in steps so outliers are caught early and explained before sign-off. We compare model outputs against independent signals such as major naval procurement announcements, shipyard delivery capacity, and visible tender volume, then we recheck any sharp year-to-year jumps that do not match program timing. A second analyst review is used to challenge key assumptions like upgrade intervals and average system values, and follow-up outreach is triggered if a variance remains unexplained.

Reports are refreshed annually, and interim updates are made when material events occur, such as a major new radar award, a program delay, or a budget rebaseline. Before delivery, a final review pass is performed so clients receive the latest version of numbers and assumptions.

Mordor Intelligence's Naval Radar Systems Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for naval radar systems, because publishers do not always count the same revenue streams or align the same years and exchange-rate timing. We keep the sizing logic traceable to platform demand and procurement cadence, so the estimate can be checked back to real fleet and program signals.

After-sales maintenance contracts and long-term support are a common add-on in some publications, and that single inclusion can move totals upward because sustainment spans many years per ship. In Mordor Intelligence's scope, post-warranty maintenance revenue sits outside the market value, so the number stays focused on new installations and modernization kits that are directly tied to procurement cycles. Differences also come from whether coastal surveillance radars are folded in, how upgrade packages are priced as software content rises, and how often the model is refreshed after program delays.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.98 B (2026) | |

| Trade Journal A | USD 4.52 B (2025) | Uses a narrower revenue pool that is closer to surveillance radar only, and it appears to exclude several multi-function shipboard suites and larger combatant upgrade packages. |

| Industry Publisher B | USD 4.80 B (2026) | Counts a tighter set of naval radar deliveries and may omit some submarine and high-end surface combatant fire-control radar content, which pushes the total below a full shipboard system view. |

The spread across the three figures is mostly explained by what is counted as a naval radar system, and which adjacent radar uses are left in or out. When the scope is tied back to platform installs, upgrade timing, and contract visibility, the resulting total stays balanced and can be repeated with clear inputs rather than hidden add-ons.

Key Questions Answered in the Report

What is the current size of the naval radar systems market?

The naval radar systems market generated USD 9.98 billion in 2026 and is projected to reach USD 12.57 billion by 2031, advancing at a 4.72% CAGR.

Which radar type leads adoption today?

AESA radars hold the largest 40.78% share, reflecting their superior multi-target and EW resilience capabilities.

Which region is growing fastest for naval radar procurements?

Asia-Pacific is expanding at 8.31% CAGR, spurred by Indo-Pacific surface-fleet expansion and frigate modernization programs.

How are export controls affecting suppliers?

Restrictions on GaN MMIC exports and China’s dominance in gallium supply introduce schedule risk and spur investment in domestic semiconductor capacity.

What platform segment shows the highest growth potential?

Unmanned surface and autonomous underwater vehicles are forecast to grow at 8.12% CAGR as navies adopt distributed sensor architectures.

Who are the major players in this industry?

RTX Corporation, Lockheed Martin Corporation, Thales Group, and Northrop Grumman Corporation collectively hold a major market share, with emerging competition from firms like Echodyne and Anduril.

Page last updated on: