Automatic Weapons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

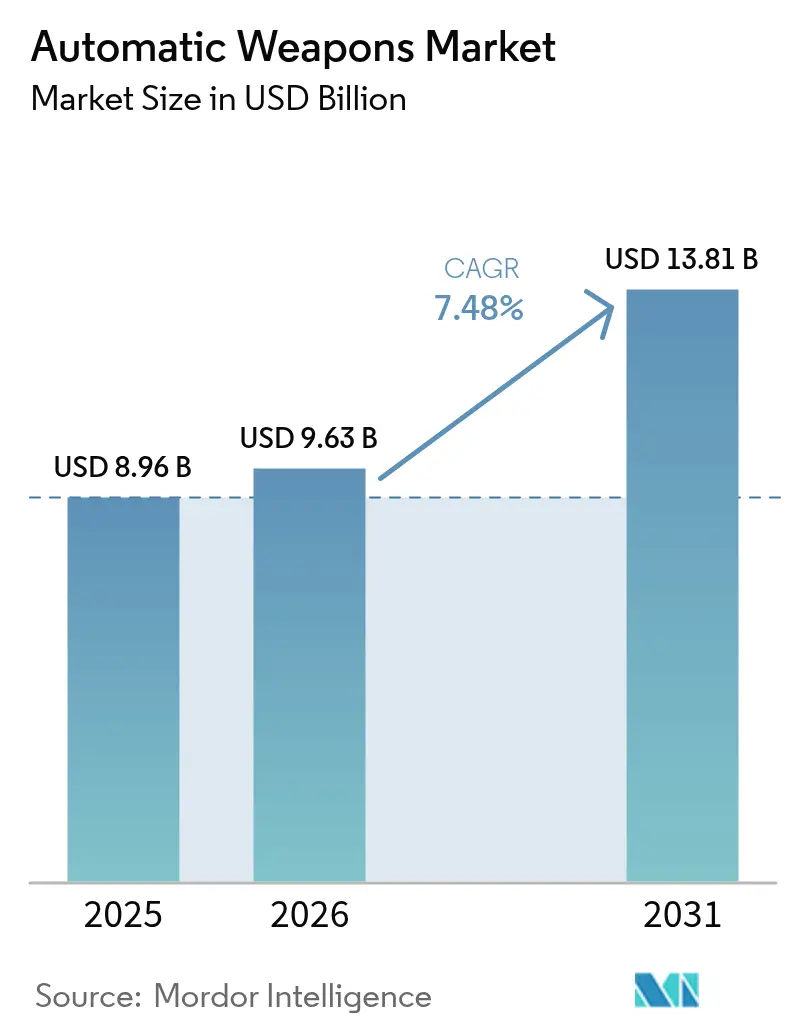

| Market Size (2026) | USD 9.63 Billion |

| Market Size (2031) | USD 13.81 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Weapons Market Analysis by Mordor Intelligence

The automatic weapons market size is expected to grow from USD 8.96 billion in 2025 to USD 9.63 billion in 2026 and is forecast to reach USD 13.81 billion by 2031 at 7.48% CAGR over 2026-2031. Heightened defense spending, persistent geopolitical flashpoints, and the urgency to retire aging Cold War inventories underpin demand for digitally networked, AI-ready small-caliber and medium-caliber systems. Military planners are opting for weapons that plug into broader sensor grids, enabling faster target recognition and data exchange. Procurement is further stimulated by modular designs that allow quick caliber swaps, by the spread of remote weapon stations on land vehicles and patrol craft, and by nationwide initiatives to harden forces against drone swarms. Supply-chain risk around rare-earth magnets, barrel steel, and specialized propellants poses near-term headwinds yet also prompts domestic sourcing initiatives in the United States, Europe, and Asia-Pacific.

Key Report Takeaways

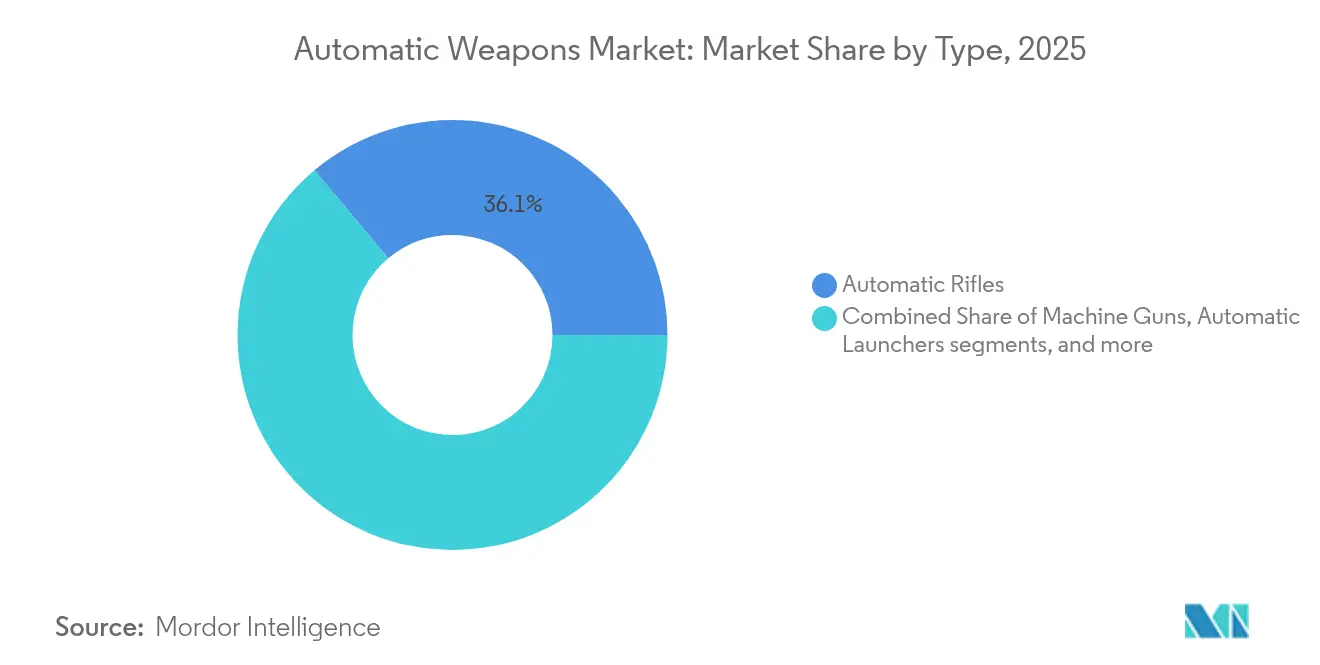

- By type, automatic rifles led the automatic weapons market share at 36.10% in 2025, while automatic cannons are expanding at an 8.32% CAGR to 2031.

- By platform, land platforms held 58.55% of the automatic weapons market in 2025; naval platforms exhibit the fastest 9.05% CAGR through 2031.

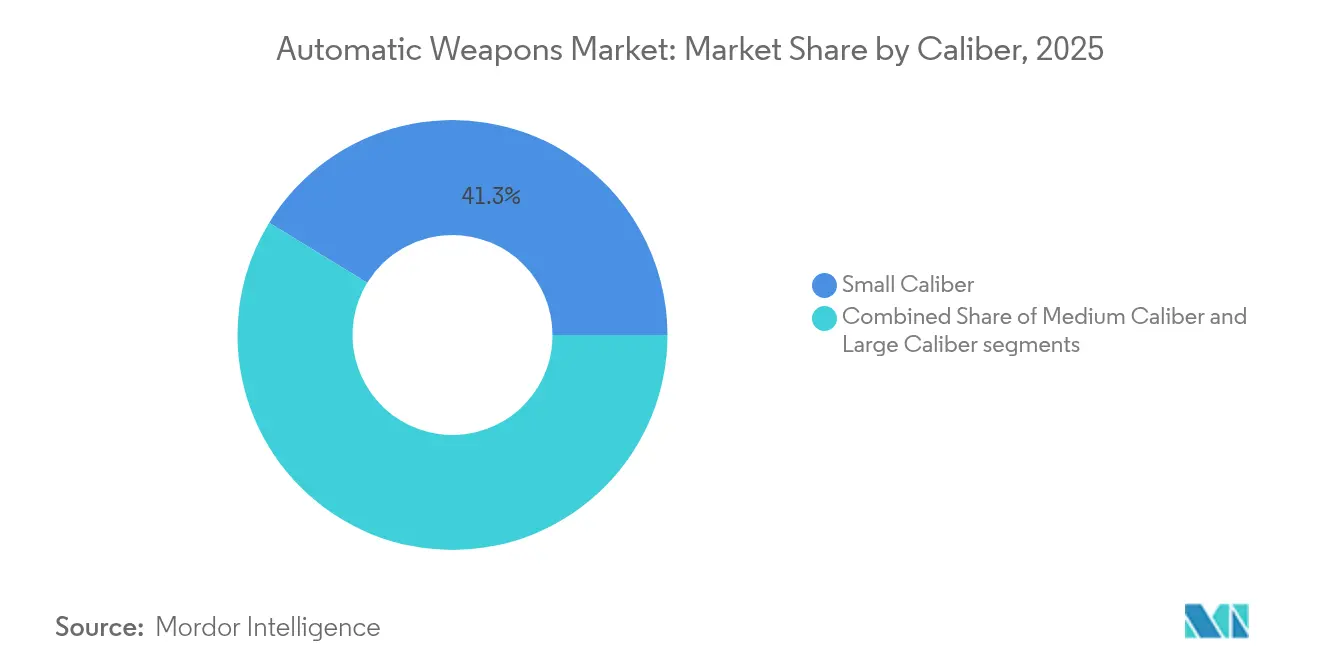

- By caliber, small caliber systems accounted for 41.25% share of the automatic weapons market size in 2025, whereas large caliber weapons are growing at an 8.11% CAGR to 2031.

- By end-user, the defense segment commanded 78.80% of 2025 revenue, while special operations forces recorded a 9.62% CAGR to 2031.

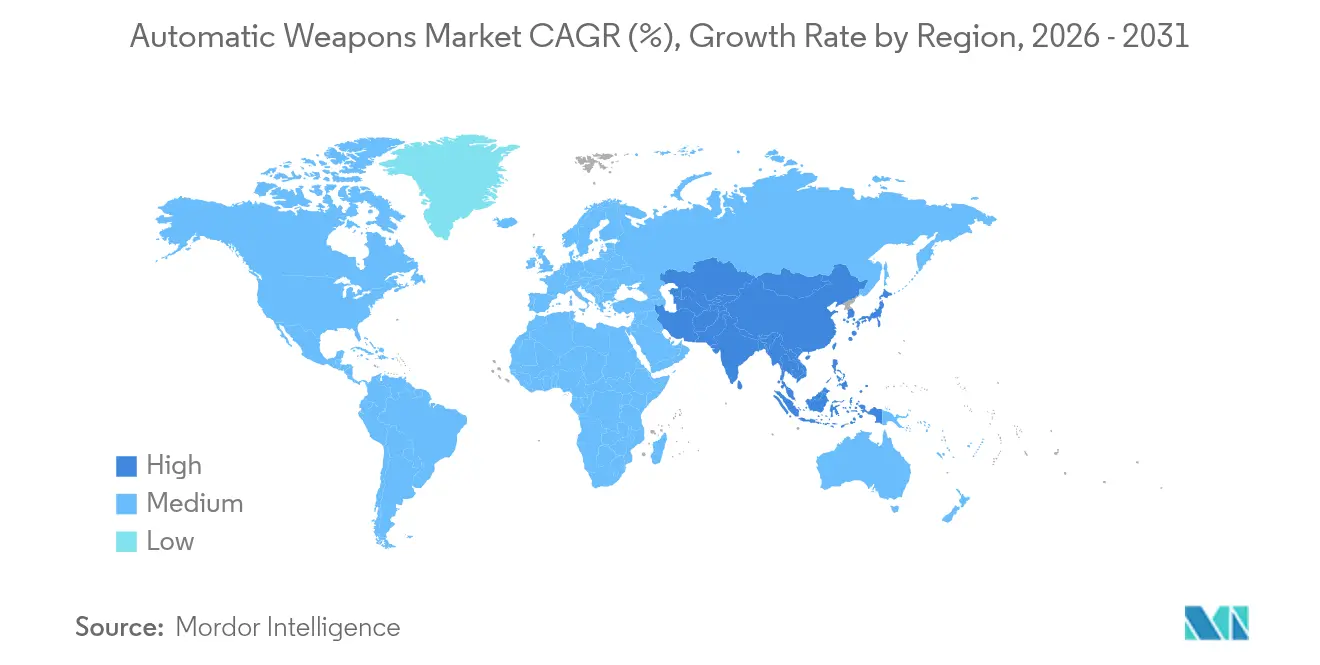

- By geography, North America retained a 38.20% share in 2025, yet Asia-Pacific registered the quickest 8.74% CAGR due to mounting regional modernization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automatic Weapons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating geopolitical tensions and multi-domain doctrine | +2.1% | Global (focus on Eastern Europe, Indo-Pacific) | Medium term (2-4 years) |

| Replacement of legacy small-arms with modular platforms | +1.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Asymmetric warfare demand for lightweight, high-mobility weapons | +1.4% | Global, early adoption in conflict zones | Short term (≤ 2 years) |

| Integration of AI-enabled fire-control electronics | +1.6% | North America, EU, advanced APAC markets | Medium term (2-4 years) |

| Proliferation of unmanned and remotely-operated weapon stations | +1.3% | Global, emphasis on naval and land vehicles | Medium term (2-4 years) |

| Shift to polymer-cased and caseless ammunition | +1.1% | North America, EU; gradual adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Geopolitical Tensions and Multi-Domain Operations Doctrine

Multi-domain doctrine obliges armies to field automatic weapons able to exchange targeting data across land, sea, and air networks in near real time. Ukraine’s Sky Sentinel turrets, which employed .50-caliber M2 Browning guns to down six Shahed drones, illustrate the new fusion of legacy firepower with AI sensors. Allied forces, noting similar threats, are integrating smart optics such as the USD 13 million SMASH 2000L scopes that auto-track drones, now fielded by the US Army. Procurement officers now prioritize connectivity protocols and low-latency data links when drafting requirements. In parallel, fleet commanders retrofit remote weapon stations on patrol craft to guard chokepoints against low-cost loitering munitions. Collectively, these measures move the automatic weapons market from stand-alone small arms toward networked effectors embedded in command-and-control webs.

Ongoing Replacement Cycle of Legacy Small-Arms Inventories

NATO members are fast-tracking replacements for aging M16- and AK-family rifles. Sweden rushed a USD 64 million order for 15,000 Colt M4s to bolster reserves amid regional tension. The US Army allotted USD 367.3 million in FY 2025 for Next Generation Squad Weapons that pair 6.8 mm rounds with advanced optics, marking the biggest US small-arms shift in six decades. Singapore chose Colt’s IAR6940E-SG to replace the four-decade-old Ultimax 100, showing even tech-savvy nations sometimes import rather than develop locally. Beyond rifles, Israel Weapon Industries (IWI) rolled out the Arbel computerized system, hitting 90% of moving targets during trials, demonstrating how digital fire-control is redefining accuracy benchmarks.

Rise in Asymmetric Warfare Requirements

Urban combat and counter-insurgency prompt demand for low-weight weapons with precision aids. US Marines trialed the ZeroMark system: a motorized buttstock that corrects aim with machine vision and LiDAR, cutting engagement time against drones. Ukrainian units fielded armed ground robots bearing rifles and grenade launchers to clear trenches while limiting soldier exposure. SOCOM’s push for sub-24-pound .338 Norma machine guns that reach 2,000 m further shows that mobility now outweighs sheer rate of fire. Such requirements channel R&D toward polymer ammunition, suppressors, and lightweight alloys, stimulating diverse entrants and intensifying competition.

Advanced Fire-Control Electronics and AI Integration

Firearms are transitioning from mechanical devices to sensor-rich edge nodes. China’s prototype coil gun, powered by lithium-ion batteries and firing at 3,000 rpm, hints at future electromagnetic weapons. India unveiled the Ten AI Weapon System, a 7.62 mm medium machine gun that auto-tracks targets via onboard AI, during Aero India 2025. Kalashnikov demonstrated a station that autonomously identifies and engages threats, merging traditional gunmaking with AI analytics. These advances cut operator workload, shorten sensor-to-shooter loops, and create demand for software update pipelines similar to those in the aerospace domain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration cost of advanced electro-optical sensors and digital fire-control units | -1.2% | Global, acute in cost-sensitive markets | Short term (≤ 2 years) |

| Supply-chain volatility for barrel-steel alloys, rare-earth magnets, and energetic chemicals | -0.9% | Global, severe impact on Western manufacturers | Medium term (2-4 years) |

| Stringent international arms-transfer rules and complex end-user certificate requirements | -0.8% | Global, particularly cross-border transactions | Long term (≥ 4 years) |

| Duplicate integration-cost pressure on procurement cycles | -0.7% | Emerging markets and budget-limited militaries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Costs of Advanced Sensor Systems

Next-generation optics elevate unit prices far above legacy equivalents. The SMASH 2000L, now standard on some US rifles, demands significant training and lifecycle support, straining the budgets of smaller militaries. Early lots of NGSW weapons cost nearly USD 9,000 each, four times the cost of legacy carbines. Manufacturers seek weight savings to offset price hikes; Sig Sauer’s Pitbull remote station dropped from 500 lb to 205 lb, making it feasible for light vehicles. Still, defense ministries with tight budgets defer upgrades, moderating near-term adoption rates.

Supply-Chain Volatility for Critical Materials

China processes over 90% of global rare-earths, and its 2024 export curbs on gallium and germanium disrupted Western missile and optics lines. The US strategic stockpiles have fallen from USD 42 billion in the 1950s to USD 888 million, limiting surge capacity. Bottlenecks in machine tools slow artillery and small-caliber barrel output, a reality highlighted during replenishment for Ukraine aid shipments. Governments fund domestic processing and alloy plants, but timelines stretch several years, inserting cost and schedule risk into major procurement programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Automatic Cannons Drive Innovation

Automatic rifles held the largest share at 36.10% in 2025, underscoring their role as the infantry’s backbone. The automatic weapons market size for rifles is projected to grow steadily as armies standardize on modular, suppressor-ready designs. Automatic cannons post the fastest 8.32% CAGR thanks to naval and air-defense applications that demand higher-energy projectiles to defeat drones and light armor.

Growth in cannons is propelled by 30 mm turrets ordered for US Marine ACVs and by European programs adding 35 mm systems with air-burst ammunition. Machine guns enjoy replacement demand but less dramatic growth, while Automatic Launchers gain relevance for counter-UAS tasks in urban environments. Gatling designs, niche yet indispensable for close-in weapon systems, receive electronics upgrades to link with ship radar feeds, ensuring continued production runs through 2030.

By Platform: Naval Acceleration Outpaces Land Dominance

Land systems commanded 58.55% of 2025 revenue, reflecting armored vehicle retrofits and dismounted modernization. Yet naval installations will clock a 9.05% CAGR, outpacing the broader automatic weapons market as fleets install remote stations that can lock onto fast, low-flying threats. The automatic weapons market share for land systems is secure, but growth moderates as inventories mature.

Crucially, maritime uptake is widening beyond blue-water navies; Taiwan’s patrol frigates will mount 20 mm XTR-102A2 systems to deter incursions in the Taiwan Strait. Airborne mounts concentrate on rotary platforms where door guns remain essential for convoy escort and medical evacuation. Uncrewed surface and ground vehicles open additional hulls and chassis for small, stabilized turrets, expanding the addressable platform base.

By Caliber: Large Caliber Systems Gain Momentum

Small caliber systems dominated at 41.25% in 2025, reflecting broad infantry deployment. Polymer-cased rounds that are 37% lighter than brass versions unlock further efficiency. However, large-caliber weapons show an 8.11% CAGR as forces seek longer reach and improved armor penetration. The automatic weapons market size for large-caliber cannon is expected to widen when 50–60 mm programmable ammunition enters serial production.

Medium caliber remains relevant on armored vehicles and naval mounts, especially where 30 mm and 35 mm compromise weight and effect. Technology spill-overs, such as air-burst fuzing, make each round more effective, encouraging adoption without linearly scaling ammunition demand. Logistics planners now evaluate unit lethality per kilogram rather than raw rate of fire, a metric favoring advanced calibers with smart munitions.

By End-User: Special Operations Drive Innovation

Defense ministries held 78.80% of 2025 spending, yet Special Operations Forces will record a 9.62% CAGR through 2031. The automatic weapons market continues to treat SOF as early adopters, fielding lightweight .338 Norma machine guns that bridge the gap between 7.62 mm and .50 cal heavy guns.

Though smaller in volume, law-enforcement agencies acquire suppressor-ready carbines and compact remote stations for critical‐infrastructure protection. Dual-use designs that comply with military and police standards shorten development cycles and stabilize production lines. Over time, SOF feedback on ergonomics, recoil mitigation, and sensor integration migrates into general-purpose infantry weapons, lifting the baseline capability across regular forces.

Geography Analysis

North America commanded 38.20% of global revenue in 2025, anchored by the United States, which accounts for nearly 40% of worldwide arms exports. Ongoing multi-year contracts for NGSW rifles and remote turrets sustain domestic output, while Canada’s NATO commitments and Mexico’s internal security procurements add incremental volume. Regional suppliers benefit from short feedback loops with end-users, allowing rapid spiral upgrades and fostering iterative product development that keeps the automatic weapons market competitive.

Asia-Pacific posts the fastest 8.74% CAGR, driven by China’s USD 314 billion defense budget and rising outlays by India, Japan, and South Korea. Japan lifted defense spending 21% to USD 55.3 billion, emphasizing long-range fires and hardened base defense. India, the world’s top arms importer, promotes local build partnerships that include small arms lines with technology transfer clauses. Taiwan’s incremental 1.8% budget hike channels funds into naval remote stations and counter-drone rifles, underscoring the region’s seaborne threat focus. Collectively, modernization across diverse operational doctrines creates varied specifications, broadening sales opportunities for global suppliers.

Europe is accelerating procurement after Russia’s 2022 invasion of Ukraine, with regional imports rising 47% between 2019 and 2024. EU initiatives to boost joint ammunition production complement bilateral deals such as Lithuania’s USD 36 million Minimi machine-gun purchase. Israel’s record USD 14.7 billion defense exports in 2024, a large portion to Europe, highlight the region’s tilt toward proven off-the-shelf solutions. Simultaneously, European states channel funds into domestic plants to reduce external dependency, stimulating R&D in smart munitions and AI-assisted fire-control tailored for NATO interoperability.

Competitive Landscape

The automatic weapons market is moderately consolidated. Legacy primes—General Dynamics Corporation, Northrop Grumman, Rheinmetall AG—retain scale advantages in medium-caliber guns and ammunition backlogs, yet face agile competition from firms specializing in software-defined sights and unmanned turrets. Northrop Grumman, for example, leads global medium-caliber sales with its Bushmaster line and maintains in-house ammunition lines, ensuring bundled offers that suit fixed-price contracts.[2]Northrop Grumman, “Armament Systems and Ammunition,” northropgrumman.com

Mergers and Acquisitions remain brisk as companies seek vertical integration. Colt CZ Group acquired Mk 47 grenade-launcher technology and later purchased Valley Steel Stamp to secure a US parts foothold.[3]Colt CZ Group, “Colt CZ Group Acquires Mk 47 Automatic Grenade Launcher Technology,” coltczgroup.com The same group closed a USD 2.225 billion buyout of The Kinetic Group, consolidating ammunition production under one roof. Rheinmetall’s USD 950 million purchase of Loc Performance boosts its US vehicle integration capacity, enabling bundled turret-vehicle offerings attractive to the Army’s Optionally Manned Fighting Vehicle program.

Tech startups exploit white-space niches in AI models for automatic target detection and in ultra-light composite receivers. Patent filings in automated threat detection and non-lethal vehicle-launched weapons rose sharply in 2024. To outpace rivals, incumbents sign data-sharing pacts with optics companies, ensuring software roadmaps align with platform refresh cycles. Supply-chain stress, especially for rare-earth magnets, has triggered joint ventures aimed at domestic processing, further reshaping partner networks. Market winners will be those blending mechanical pedigree with updatable software stacks that keep pace with evolving engagement rules.

Automatic Weapons Industry Leaders

Rheinmetall AG

BAE Systems plc

General Dynamics Corporation

SIG SAUER, Inc.

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Brazilian Army announced its plans to acquire Turkish-manufactured M2HB heavy machine guns as part of its military modernization program.

- September 2024: The US Army awarded US Ordnance a USD 15 million contract for 7.62x51 mm M60E6 and M60E4 machine guns, conversion kits for existing M60s, supporting equipment, and training.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the automatic weapons market as all fully-automatic firearms and crew-served guns, including automatic rifles, machine guns, automatic launchers, automatic cannons, and Gatling-type systems, fielded on land, naval, and airborne platforms. These weapons discharge multiple rounds per trigger pull and are procured primarily by defense ministries and law-enforcement agencies.

Scope exclusion: Civilian sporting and hunting semi-automatic firearms lie outside this assessment.

Segmentation Overview

- By Type

- Automatic Rifles

- Machine Guns

- Automatic Launchers

- Automatic Cannons

- Gatling Gun

- By Platform

- Land

- Airborne

- Naval

- By Caliber

- Small Caliber

- Medium Caliber

- Large Caliber

- By End-User

- Defense

- Army

- Navy

- Air Force

- Special Operations Forces

- Law Enforcement

- Defense

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with program managers, ordnance officers, procurement officials, and maintenance commanders across North America, Europe, Asia-Pacific, and the Middle East helped us verify platform inventories, average selling prices, and replacement cycles. Follow-up surveys with integrators and depot engineers clarified caliber mix shifts and remote-weapon-station penetration, allowing Mordor to adjust preliminary totals.

Desk Research

Mordor analysts began with open data from sources such as SIPRI defense-spending tables, UN Comtrade shipment records, U.S. Federal Procurement Data System, and patents indexed in Questel. We blended these with fleet statistics from Jane's Defense, inventory updates published by NATO and the Stockholm International Peace Research Institute, and production disclosures in SEC 10-Ks and EDA filings. Subscription databases, D&B Hoovers for company revenue splits and Dow Jones Factiva for contract news, filled historic gaps and cross-checked regional shipments.

Trade association yearbooks (e.g., National Defense Industrial Association), parliamentary defense committee minutes, and reputable press briefings added narrative context on modernization programs and budget enactment. The sources listed above illustrate our evidence base; many additional public and paid references supported data validation.

Market-Sizing & Forecasting

We anchor the baseline through a top-down defense-budget apportion model that allocates combat-system spend, then validate it with selected bottom-up checks, including supplier shipment roll-ups and sampled average selling price multiplied by volume from disclosed contracts. Key variables include active force size, planned infantry modernization lots, platform service-life extension schedules, and average unit costs by caliber class, along with import-export trends and exchange-rate movements. Forecasts apply multivariate regression and scenario analysis, capturing correlations between procurement outlays, geopolitical tension indices, and barrel-wear replacement ratios. Volume gaps in nations with opaque data were bridged using proxy indicators such as infantry-to-population ratios and historic spend elasticity agreed upon by expert respondents.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance checks against independent shipment and budget trackers, and automated outlier flags. Reports refresh each year, with interim updates triggered by material contract awards or policy shifts. Before release, an analyst re-runs the model so clients receive the latest view.

Why Mordor's Automatic Weapons Baseline Earns Trusted Reliance

Published estimates often diverge because firms choose different platform scopes, pricing ladders, and refresh cadences.

Key gap drivers include whether semi-automatic inventories are mixed with fully-automatic totals, how research converts multiyear contract values into annualized revenue, and the cadence at which currency swings are rebased. Mordor updates annually and excludes civilian channels, whereas several publishers roll five-year contract obligations straight into one figure or lump civilian rifles with military buys, inflating their headline values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.96 B | Mordor Intelligence | - |

| USD 10.60 B | Global Consultancy A | Includes semi-automatic civilian sales and uses list prices without delivery schedules |

| USD 9.99 B | Industry Publisher B | Allocates entire multiyear contract value to first year and converts at fixed 2022 FX rates |

| USD 9.39 B | Regional Consultancy C | Mixes police side-arm upgrades and lacks remote-weapon-station platform split |

In sum, our disciplined scope, annual currency rebasing, and dual-path validation deliver a balanced, transparent baseline clients can replicate and trust for strategic planning.

Key Questions Answered in the Report

What is the current size of the automatic weapons market?

The automatic weapons market stands at USD 9.63 billion in 2026 and is projected to reach USD 13.81 billion by 2031.

Which region is growing fastest in automatic weapons procurement?

Asia-Pacific shows the highest growth with a 8.74% CAGR, driven by modernization across China, India, Japan, and South Korea.

Why are Automatic Cannons the fastest-growing weapon type?

Naval and air-defense programs favor 30–40 mm cannons with air-burst munitions that counter drones and light armor, producing an 8.32% CAGR.

How are supply-chain risks affecting manufacturers?

Reliance on Chinese rare-earth processing and limited barrel-steel capacity adds cost and schedule risk, prompting governments to re-shore production.

What role do Special Operations Forces play in innovation?

SOF units adopt lightweight, high-caliber systems early, validating new materials and AI sights that later trickle down to conventional infantry.

Are AI-enabled optics becoming standard?

Yes. Contracts like the SMASH 2000L scope for the US Army show that smart sights able to auto-track drones are moving from prototypes to field issue.

Page last updated on: