Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

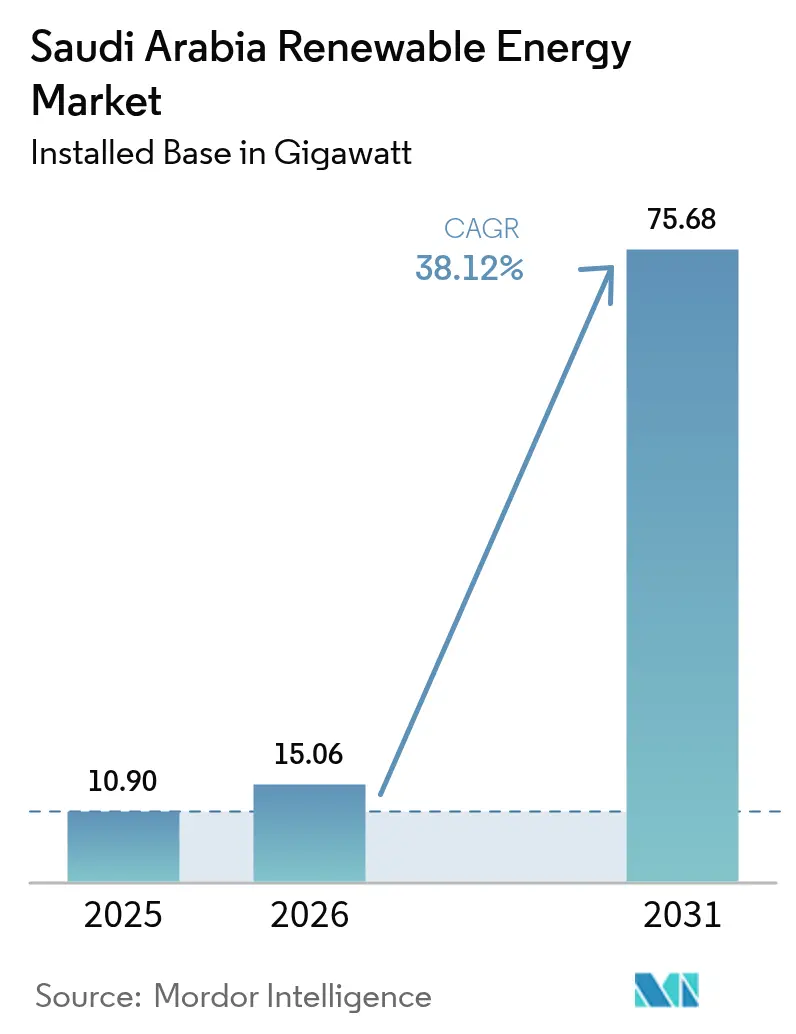

| Base Year Market Size (2025) | 10.90 gigawatt |

| Market Volume (2026) | 15.06 gigawatt |

| Market Volume (2031) | 75.68 gigawatt |

| Growth Rate (2026 - 2031) | 38.12% CAGR |

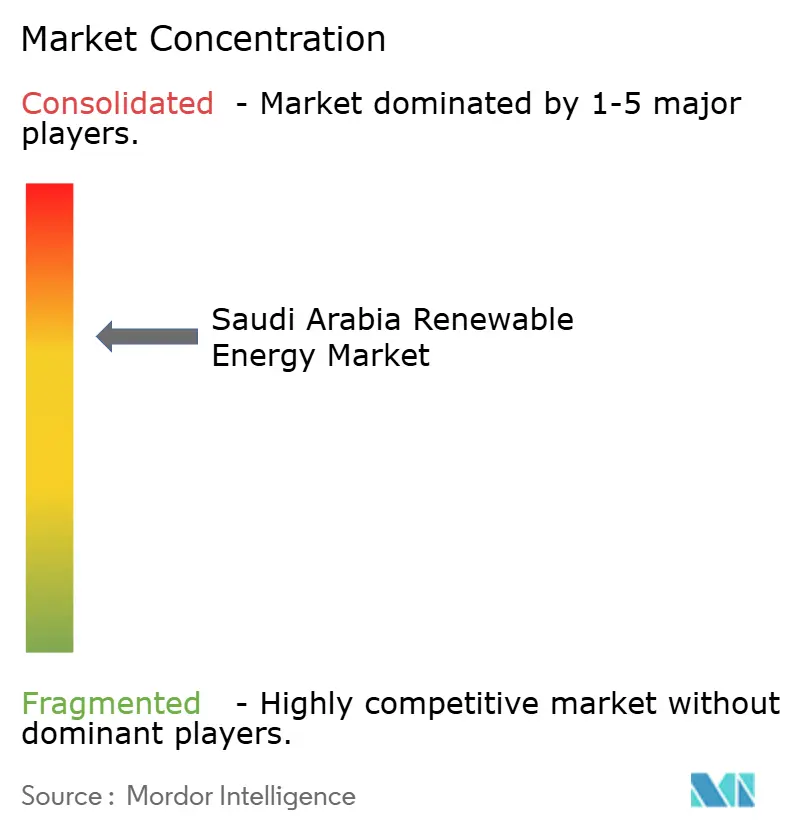

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Renewable Energy Market Analysis by Mordor Intelligence

Saudi Arabia Renewable Energy market size in 2026 is estimated at 15.06 gigawatt, growing from 2025 value of 10.90 gigawatt with 2031 projections showing 75.68 gigawatt, growing at 38.12% CAGR over 2026-2031.

This highlights the Kingdom’s fastest-growing power segment and underscores its Vision 2030 decarbonization goals. Cost-competitive solar tariffs averaging USD 0.018/kWh, giga-project electricity needs, and rapidly growing green-hydrogen demand collectively reinforce long-term growth prospects. The National Renewable Energy Program’s 130 GW procurement pipeline, coupled with ambitious local-content mandates, anchors supply-chain investments and accelerates the localization of manufacturing.[1]Renewable Energy Project Development Office, “National Renewable Energy Program Update,” repdo.gov.sa Rising industrial and commercial power purchases, regulatory support for corporate PPAs, and inland wind resource diversification further broaden the Saudi Arabian renewable energy market opportunity. Meanwhile, operational challenges such as dust-driven PV efficiency losses of 15-20% annually, grid congestion in high-solar regions, and abundant USD 1.25/MMBtu natural-gas supply temper near-term adoption.

Key Report Takeaways

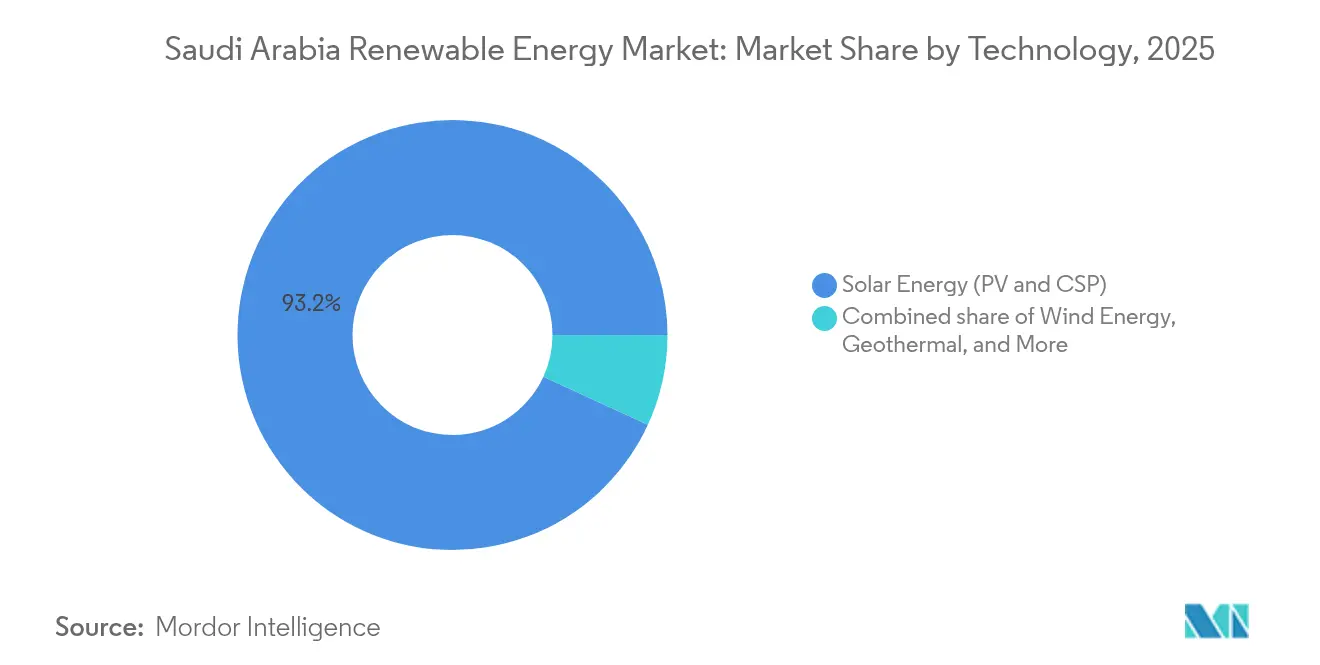

- By technology, solar energy leads the Saudi Arabian renewable energy market with a 93.15% share in 2025, while wind energy is projected to advance at an 81.7% CAGR through 2031.

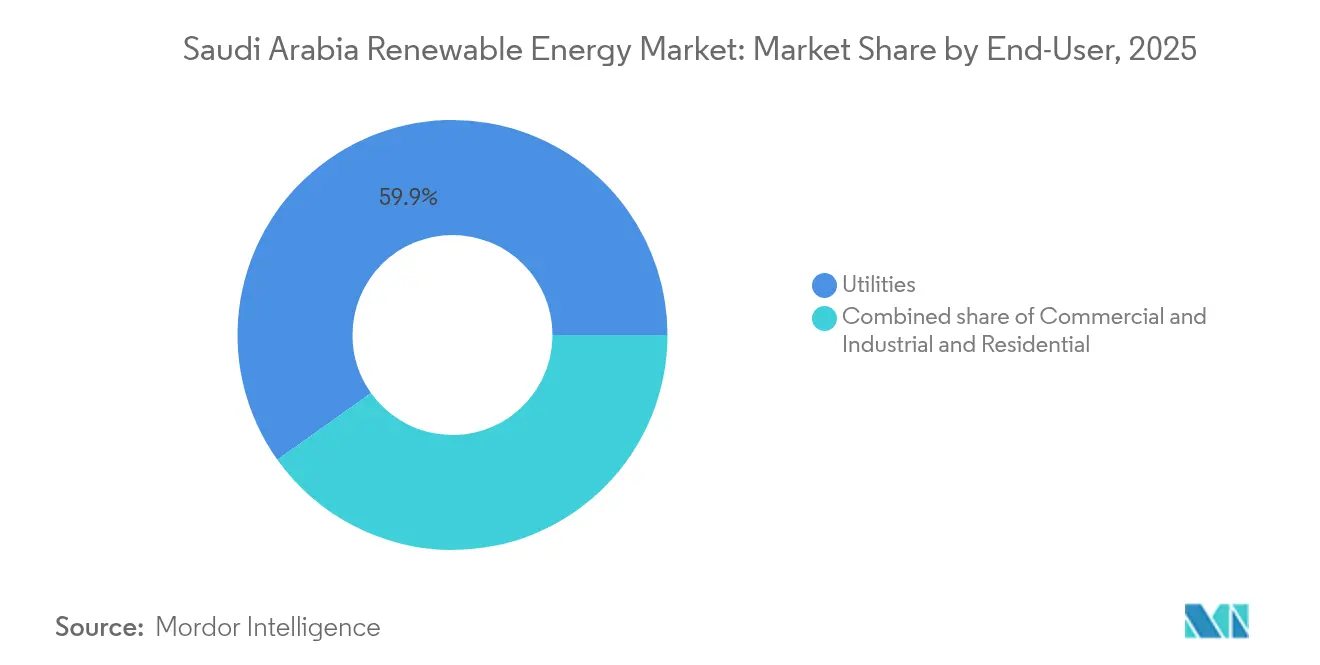

- By end user, utilities held a 59.85% share of the Saudi Arabian renewable energy market size in 2025; commercial and industrial users are expected to expand at a 43.2% CAGR through 2031.

- By company, ACWA Power and Masdar jointly controlled 45% of the awarded capacity in 2024 within the Saudi Arabian renewable energy market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Renewable Energy Program (NREP) 130 GW target by 2030 | 12.50% | National, with concentration in Northern Borders and Tabuk | Long term (≥ 4 years) |

| Declining LCOE for solar PV in KSA | 8.20% | National, strongest in central and northern regions | Medium term (2-4 years) |

| Power demand from giga-projects (NEOM, Red Sea) | 6.80% | Northwestern regions, NEOM and Red Sea Project areas | Medium term (2-4 years) |

| Green-hydrogen export ambitions | 5.40% | Coastal regions with port access, NEOM corridor | Long term (≥ 4 years) |

| Desalination shift to renewables | 3.10% | Eastern and western coastal provinces | Medium term (2-4 years) |

| Corporate PPAs driven by Vision 2030 ESG pledges | 2.70% | Industrial clusters in Riyadh, Eastern Province, Jubail | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

National Renewable Energy Program Drives Unprecedented Capacity Expansion

Round-based auctions under the National Renewable Energy Program issue predictable tenders that underpin the Saudi Arabian renewable energy market, with cumulative allocations expected to reach 17.1 GW by late 2025. Record-low tariffs below USD 0.018/kWh incentivize aggressive bidding and stimulate financing innovation. Local-content thresholds now exceed 35%, catalyzing the production of modules, inverters, and wind turbines inside the Kingdom. Project clustering in the Northern Borders and Tabuk regions exploits superior solar irradiance of 2,400 kWh/m² and 7.5 m/s hub-height winds, mitigating curtailment through geographic diversification. International IEC equipment standards ensure bankability, while streamlined permitting compresses development timelines to 24 months. The resulting visibility fortifies the Saudi Arabia renewable energy market outlook for equipment suppliers and investors alike.

Solar LCOE Competitiveness Reshapes Power-Generation Economics

Utility-scale PV costs breached the USD 0.018/kWh threshold in 2024, achieving parity with gas-fired generation even at subsidized feedstock prices. Scale economies from 1 GW-class projects, sub-4% interest-rate financing, and bifacial modules boost yields by 25-30%. Single-axis tracking maximizes daily output, mitigating dusk-period price cannibalization. Competitive LCOEs spur project oversubscription, with bids overshooting tendered capacity by threefold in Round 6. Nevertheless, USD 0.008-0.012/kWh in grid integration costs partially erode the savings. Integration spending stimulates storage adoption, opening new revenue channels within the Saudi Arabian renewable energy market for battery integrators and EPCs.

Giga-Projects Create Concentrated Renewable Demand Centers

NEOM’s USD 8.4 billion hydrogen project alone requires 4 GW of dedicated solar-wind hybrid capacity, equating to 7% of the 2030 renewables target. The Red Sea tourism development adds 650 MW of demand under a 25-year offtake contract. Their long-dated PPAs de-risk cash flows, enabling non-recourse debt with tenors beyond 20 years. Grid corridors valued at USD 2 billion enhance system resilience and advance inter-regional energy trade. Shared substations, roads, and maintenance bases lower the per-megawatt capital expenditure (capex), underscoring the cluster effect on the Saudi Arabian renewable energy market.

Green-Hydrogen Export Strategy Anchors Long-Term Renewable Demand

Plans to deliver 11 million tpa of green hydrogen by 2030 translate into 120 GW of incremental renewables, dwarfing current installed capacity.[2]Hydrogen Council, “Global Hydrogen Flows,” hydrogencouncil.com A landmark 200,000 tonnes per annum offtake agreement with Germany validates cross-border trade economics. Shipping costs range from USD 1.2 to 1.8/kg, favoring the siting of coastal electrolyzers. Domestic steel and ammonia industries absorb early volumes, smoothing ramp-up risk. Port, storage, and pipeline infrastructure needs USD 15-20 billion, unlocking EPC prospects across the Saudi Arabian renewable energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant low-cost natural gas for power generation | -4.80% | National, strongest in gas-rich Eastern Province | Medium term (2-4 years) |

| Grid congestion & solar curtailment risk | -3.20% | Central and northern high-solar regions | Short term (≤ 2 years) |

| Limited local wind-component supply chain | -2.10% | National, affecting wind project economics | Long term (≥ 4 years) |

| Desert climate-driven O&M degradation | -1.90% | Desert regions, central and northern provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural Gas Price Advantage Creates Adoption Headwinds

Sub-USD 0.03/kWh gas generation costs preserve economic headroom over renewables, particularly during evening peaks. Dispatchable CCGT plants stabilize frequency as renewable penetration climbs, reinforcing gas’s strategic role. Vast 300 TCF proven reserves plus Jafurah basin additions sustain low tariffs until export economics improve. Carbon-neutrality pledges and prospective LNG revenues, however, weaken long-term price caps, gradually tipping the balance in favor of the Saudi Arabian renewable energy market.

Grid Infrastructure Constraints Limit Renewable Integration

Curtailment exceeded 12% in Northern Borders during spring 2025 mid-day peaks, eroding project revenue.[3]International Energy Agency, “Saudi Arabia Energy Policy Review 2025,” iea.org Legacy transmission designed for centralized oil plants lacks dynamic-reactive support as inverter-based resources reach or exceed 30% penetration. Planned USD 8-12 billion in grid upgrades plus 1.1 GW of mandated storage in Round 7 will partially relieve constraints but extend over a 3-5-year rollout. Digital substations and demand-response programs complement hardware solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Dominance Faces Wind Energy Disruption

Solar held 93.15% of the 2025 Saudi Arabia renewable energy market size, benefiting from unmatched irradiance and economies of scale. Massive 1 GW-plus PV blocks near Tabuk drive single-digit USD-cent tariffs while bifacial modules and trackers lift yields across desert terrains. Nonetheless, wind’s 81.7% CAGR projects a swift ascent as Vestas and Siemens Gamesa commission high-capacity turbines optimized for 45% capacity factors. The Dumat Al-Jandal plant validated wind viability at USD 0.0199/kWh, signaling price convergence with PV. Transmission-linked hybrid layouts enhance grid stability, smooth variable output, and reduce curtailment penalties in the Saudi Arabian renewable energy market. Hydropower’s 2.4 GW pumped-storage plans will provide peak shaving, while bioenergy and geothermal remain niche plays.

Solar’s rapid scale-up faces O&M headwinds in sand-laden provinces; wind encounters supply-chain bottlenecks until local nacelle and blade manufacturing matures. Emerging floating PV on desalination reservoirs and agrivoltaic arrays in irrigation districts diversify applications beyond utility-scale deserts. Grid-code updates enable hybrid solar-wind plants to share interconnection points, reducing capital expenditures and expediting permitting. Together, these trends reinforce a balanced generation mix underpinning long-term grid resilience within the Saudi Arabian renewable energy market.

By End User: Commercial Sector Accelerates Corporate Renewable Adoption

Utilities commanded 59.85% of the 2025 Saudi Arabia renewable energy market share, anchored by gigawatt procurements and vertically integrated state off-takers. They retain first-mover advantages in financing, land access, and grid interconnection. Yet commercial and industrial users collectively post a 43.2% CAGR, spurred by net-zero pledges and direct procurement rules that unlock long-tenor PPAs. Ma’aden’s 1.2 GW PPA and SABIC’s multi-site rooftop program illustrate early traction. Distributed PV offsets transmission losses and shields corporates from tariff reforms, while demand-side management and behind-the-meter batteries improve power quality.

Residential uptake stays muted under USD 0.048/kWh subsidized tariffs, although 180% annual growth in rooftop solar applications since 2024 signals rising awareness. The emergent prosumer model will reshape distribution networks, necessitating the use of smart meters, bidirectional transformers, and dynamic pricing. Energy-service companies capitalize on OPEX-driven models that bundle PV, storage, and efficiency retrofits, broadening addressable demand across the Saudi Arabian renewable energy market.

Geography Analysis

Tabuk and Northern Borders provinces dominate the capacity pipelines due to their high solar irradiance, exceeding 2,400 kWh/m², and consistent 7 m/s winds, which host 40% of the planned wind builds and multiple gigawatt PV parks. Land availability and low population density expedite permitting, while proximity to NEOM anchors offtake certainty. Eastern Province industrial hubs generate baseload demand from petrochemical and steel complexes, catalyzing the development of hybrid solar-gas arrangements and future hydrogen consumption. Riyadh’s mature grid and dense commercial load foster distributed generation; rooftop installations surged 180% year over year after net-metering rules took effect, placing the capital at the forefront of prosumer growth within the Saudi Arabian renewable energy market.

Coastal provinces are leveraging renewables to power energy-intensive desalination plants, aligning high solar output with daytime water production peaks and reducing diesel reliance. Western Red Sea sites integrate floating PV with tourism developments, minimizing land conflict. Central agricultural regions such as Qassim explore agrivoltaics to co-optimize water usage, crop yield, and electricity generation. Spatial diversification mitigates weather-related volatility and reduces single-region curtailment risks, thereby reinforcing the national grid’s stability as the Saudi Arabian renewable energy market expands.

Competitive Landscape

Market concentration remains moderate, with ACWA Power and Masdar collectively controlling approximately 45% of the awarded capacity in 2024, leveraging their extensive project finance expertise and in-country networks. New entrants, TotalEnergies, EDF Renewables, and Marubeni, gain ground via joint ventures, bidding aggressively with technology-heavy proposals such as co-located storage and hydrogen-ready designs. Patents for desert-tolerant solar trackers and extended-length wind blades increased to 127 in 2024, reflecting a shift toward localized R&D. EPC contractors bundle predictive-maintenance software and unmanned inspections to reduce OPEX by 15%, enhancing bankability across the Saudi Arabian renewable energy market.

Distributed-generation and storage niches attract specialized developers targeting commercial clients wary of curtailment risk. Equipment manufacturers respond with modular containerized batteries and turnkey microgrids aligned to Vision 2030 localization quotas. Public-sector investment vehicles launch manufacturing funds to secure upstream component supply, aiming for 50% local content by 2028. Collectively, these dynamics suggest a balanced competitive arena in which scale, technological innovation, and local partnerships dictate success trajectories.[5]World Intellectual Property Organization, “Saudi Arabia 2024 Patent Filings,” wipo.int

Saudi Arabia Renewable Energy Industry Leaders

ACWA POWER

Masdar

EDF Renewables

Engie SA

Alfanar Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: NEOM Green Hydrogen Project has reached over 80% completion, moving closer to operation as the world’s largest integrated green hydrogen and ammonia facility. The project features 1.6 GW of wind power from 257 turbines, 2.2 GW of solar PV across a solar farm the size of Manhattan, and a 4 GW dedicated transmission network, enabling the production of up to 1.2 million tonnes of green ammonia annually for global export.

- August 2025: ACWA Power commenced commercial operations of a 2.7 GW solar PV portfolio in Saudi Arabia, comprising the Al Kahfah (1.4 GW), Ar Rass 2 (1 GW of a planned 2 GW), and SAAD 2 (365.7 MW of 1.1 GW) projects, in partnership with Badeel (PIF). The SAR 12.2 billion (US$3.3 billion) projects supply electricity to the Saudi Power Procurement Company under a May 2023 offtake agreement.

- August 2025: Masdar, in collaboration with GD Power and Korea Electric Power, secured USD 1.1 billion in financing from eight banks for the 2 GW Al Sadawi solar PV project in Saudi Arabia, with a target for full operation in 2027.

- July 2025: ACWA Power, Badeel, and SAPCO signed PPAs with SPPC for seven renewable projects in Saudi Arabia, 2 wind farms (3,000 MW) and 5 solar PV plants (12,000 MW), totaling 15,000 MW.

Saudi Arabia Renewable Energy Market Report Scope

Renewable energy is the energy collected from renewable resources such as sunlight, wind, the movement of water, and geothermal heat that are naturally replenished.

Saudi Arabia's renewable energy market is segmented by type. By type, the market is segmented into solar, wind, and other types (hydro, biomass, etc.). For each segment, the market sizing and forecasts are done based on installed capacity (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large is the Saudi Arabia renewable energy market today?

Installed capacity reached 10.90 GW in 2025 and is set to hit 15.06 GW in 2026 on its way to 75.68 GW by 2031.

What is the expected growth rate for renewables in Saudi Arabia?

The sector is forecast to expand at a 38.12% CAGR between 2026 and 2031, driven by Vision 2030 procurement targets.

Which technology dominates new capacity additions?

Solar currently holds 93.15% share, but wind is the fastest-growing segment with an 81.7% CAGR through 2031.

Why are corporates signing power-purchase agreements?

Vision 2030 ESG mandates and cost-competitive solar tariffs encourage industrial and commercial firms to secure fixed-price renewable power.

What challenges could slow renewable deployment?

Low-cost natural gas, grid congestion, supply-chain gaps for wind components, and desert-related O&M issues can dampen near-term adoption.

How will green hydrogen influence future demand?

Plans for 11 million tpa of green hydrogen by 2030 require roughly 120 GW of renewables, ensuring long-term demand for new projects.

Page last updated on: