Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

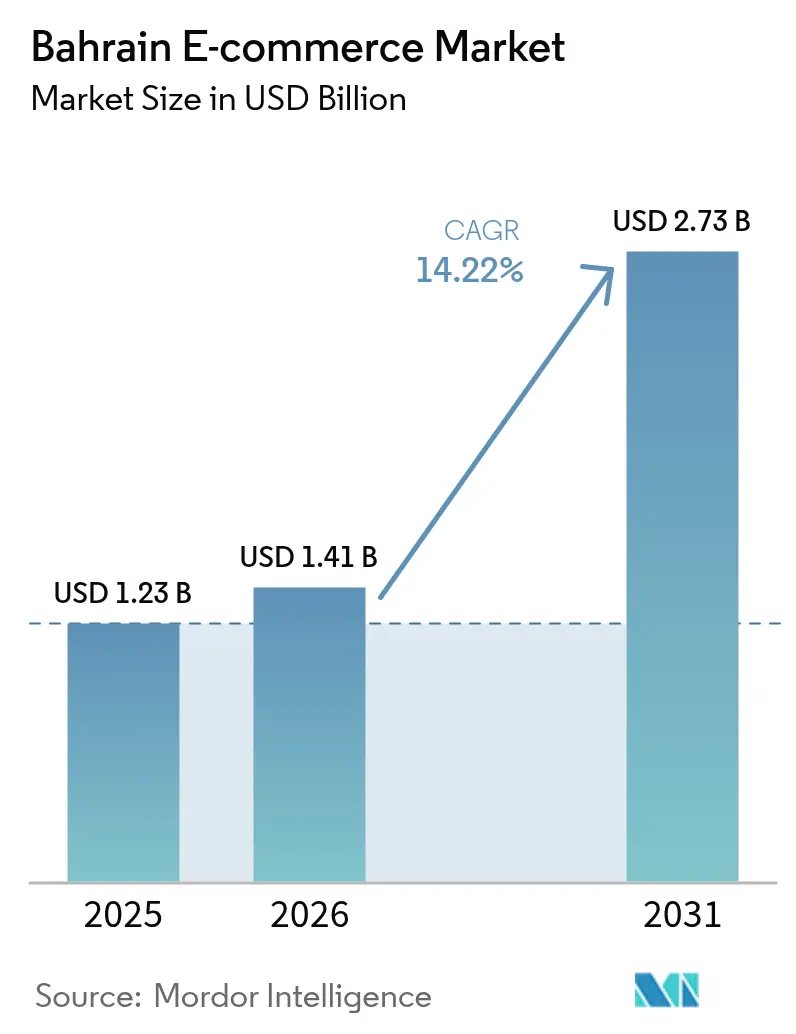

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 2.73 Billion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

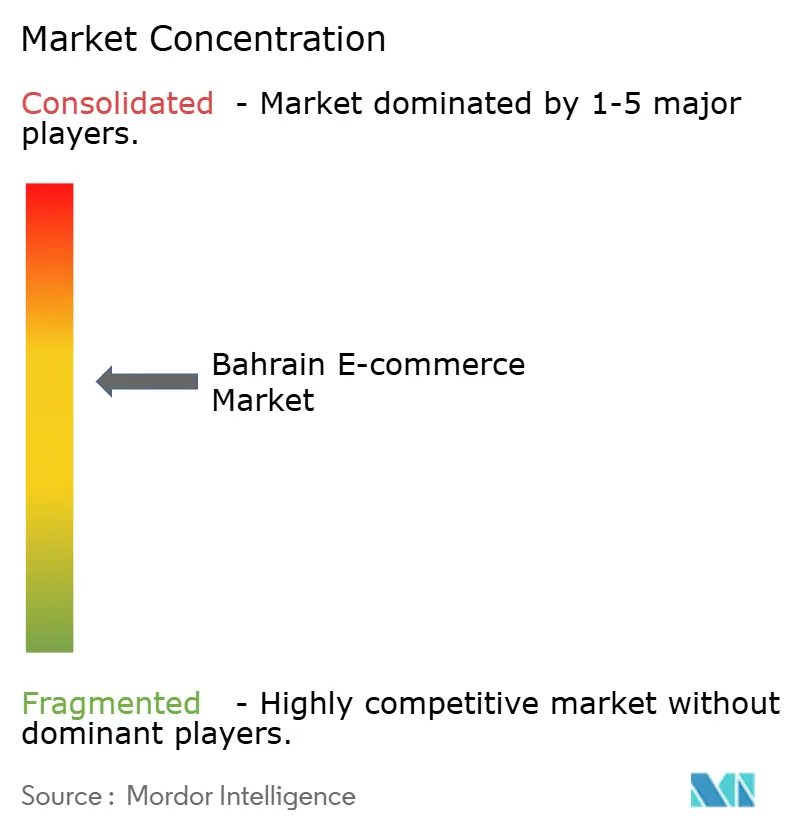

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain E-commerce Market Analysis by Mordor Intelligence

The Bahrain e-commerce market size is expected to grow from USD 1.23 billion in 2025 to USD 1.41 billion in 2026 and is forecast to reach USD 2.73 billion by 2031 at 14.22% CAGR over 2026-2031. Rising smartphone penetration, cloud-first policies, and supportive fintech rules are accelerating digital buying, while the kingdom’s proximity to Saudi Arabia boosts cross-border trade. Mobile checkouts already account for two-thirds of transactions, and the mainstream use of digital wallets plus Buy-Now-Pay-Later (BNPL) is reducing cash friction. Same-day delivery networks are scaling quickly on the back of airport and port upgrades, and young shoppers are driving strong demand for fashion, beauty, and food delivery services. Cyber-fraud and last-mile costs remain hurdles, yet continued public-private investment in security, logistics, and talent is expected to sustain double-digit growth for the Bahrain e-commerce market.[1]Bahrain News Agency, “Digital Platforms Boost Online Services,” bna.bh

Key Report Takeaways

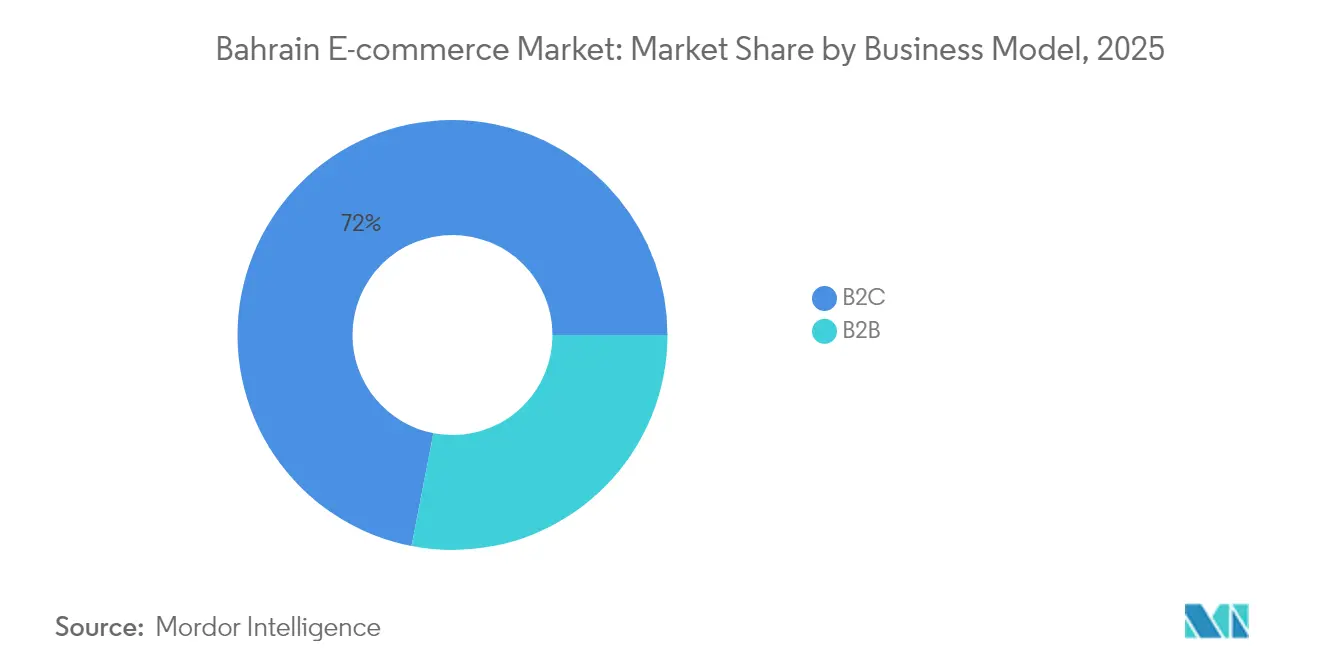

- By business model, B2C captured 71.95% of Bahrain e-commerce market share in 2025, while B2B is projected to expand at 16.05% CAGR through 2031.

- By device type, smartphones commanded 67.98% of Bahrain e-commerce market share in 2025 and are forecast to post 15.22% CAGR to 2031.

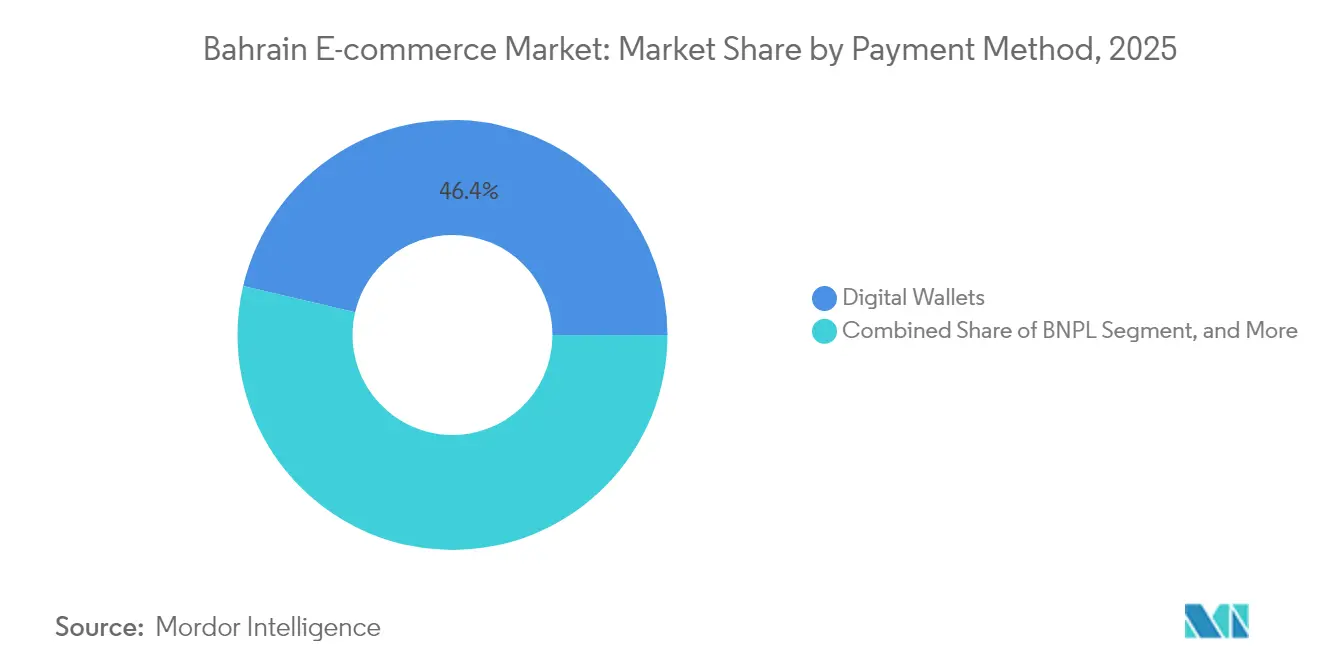

- By payment method, digital wallets led with a 46.35% share of the Bahrain e-commerce market size in 2025, whereas BNPL is set to grow at 14.98% CAGR to 2031.

- By product category, fashion and apparel held 28.15% of Bahrain e-commerce market share in 2025, and food & beverages is advancing at 14.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile-commerce transactions | +3.2% | National, Manama and Muharraq focus | Short term (≤ 2 years) |

| Rapid expansion of same-day delivery infrastructure | +2.8% | National, spreading from urban centers | Medium term (2-4 years) |

| Growing fashion and beauty demand among Gen-Z | +2.1% | National with regional spillover | Medium term (2-4 years) |

| Government “Bahrain Digital Economy” initiatives | +1.9% | National, GCC integration | Long term (≥ 4 years) |

| Mainstream adoption of digital wallets and BNPL | +2.4% | National, cross-border use | Short term (≤ 2 years) |

| Regional cross-border marketplaces boosting SKU variety | +1.8% | GCC-wide, Bahrain logistics hub | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile-Commerce Transactions

Smartphone orders represented 68.52% of B2C sales in 2024 and are rising at 15.63% CAGR, backed by 156.6% mobile line density and median speeds of 119.04 Mbps. Two-thirds of residents use mobile payments, and the eKey 2.0 biometric system now processes more than 2 million verifications each month, which lowers checkout drop-off. Instagram reaches 73.7% of the population and TikTok captures 79.5% of internet users, turning social feeds into direct sales lanes. Secure authentication, fast networks, and shoppable content therefore anchor mobile as the chief growth engine for the Bahrain e-commerce market. Platforms that optimize pages for quick mobile loading see reduced cart-abandon rates and higher repeat purchase frequency.

Rapid Expansion of Same-Day Delivery Infrastructure

Same-day fulfillment has shifted from novelty to norm thanks to Bahrain’s compact geography and heavy logistics investment. Kulsha Logistics now runs more than 100 vehicles, including temperature-controlled vans, while Parcel has completed 1.5 million deliveries and expanded into Riyadh. The USD 1.1 billion airport upgrade added a 25,000 m² cargo village with capacity for 1.3 million t, and Khalifa Bin Salman Port clears containers in under three hours. These gains pushed Bahrain to 34th on the World Bank Logistics Performance Index, second in the GCC. Retailers leverage this network to promise same-day shipping nationwide, raising service expectations and fueling order volumes for the Bahrain e-commerce market. Businesses that fail to match this speed risk churn, especially in high-velocity categories such as groceries and electronics.

Growing Fashion and Beauty Demand Among Gen-Z Consumers

Gen-Z already represents 22% of GCC residents and favors digital discovery blended with offline trial. Skincare alone formed a USD 300 million GCC niche growing 30% year-over-year in 2023.[2]Chalhoub Group, “Beauty Report 2024,” chalhoubgroup.com In Bahrain, 91% of female Gen-Z shoppers tap Instagram during the buying journey, while click-and-collect bridges online and physical experiences. Personal-care spending by under-30 shoppers is projected to grow 1.3–1.6× from 2022 levels by 2030, driving higher average order values. Global labels such as Tommy Hilfiger and Calvin Klein expanded through 19 new stores at The Avenues mall, creating omnichannel touchpoints that feed web conversion. To serve these trend-seekers, e-tailers refresh assortments rapidly and test subscription boxes, reinforcing repeat spend within the Bahrain e-commerce market.

Government “Bahrain Digital Economy” Initiatives

The Information and eGovernment Authority digitized 89% of public services during H1 2024, cutting transaction times by 68% and trimming costs by 75%. Cloud-first rules shifted more than 100 state servers to AWS, which now runs a regional data-center cluster in Manama. The national eKYC framework under Central Bank supervision enables secure onboarding for banks, fintechs, and marketplaces, while the Sijilat portal automates commercial licensing. Gateway Gulf 2024 unlocked USD 12 billion in new digital deals, including J.P. Morgan’s tech hub announcement. These cohesive policies give online merchants low-cost hosting, quick registration, and robust ID checks, strengthening the Bahrain e-commerce market over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile costs for low-density areas | –1.8% | National, outer regions | Medium term (2-4 years) |

| Persistent cash-on-delivery preference inflating returns | –1.2% | National, generational skew | Short term (≤ 2 years) |

| Limited cold-chain capacity for online grocery | –0.9% | National, perishables | Medium term (2-4 years) |

| Rising cyber-fraud incidents eroding shopper trust | –1.5% | National, cross-border links | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Costs for Low-Density Areas

Delivery expenses escalate outside the Manama-Muharraq belt, where population clusters thin out and route density falls. Couriers often set minimum order thresholds, which deters small-ticket purchases in towns such as Sitra and Hamad. Low-value baskets then migrate to store pickup, hurting convenience metrics. Shared locker networks and pickup-drop points are being tested, yet capital outlays remain heavy for smaller fleets. Until density-based pricing, shared routes, or alternative handover models scale, margins in the Bahrain e-commerce market will stay compressed for rural dispatches.

Rising Cyber-Fraud Incidents Eroding Shopper Trust

Although 97% of residents adopt security steps, 52% have still suffered scams and 62% report fake money-transfer requests. False payment declines impact 23% of buyers, and a single failure leads one-third of shoppers to switch sites. The National Cybersecurity Centre and a new Personal Data Protection Law give legal cover, but only 20% of organizations believe they are breach-ready. Payment platforms therefore invest in tokenization, two-factor logins, and AI fraud filters to maintain loyalty within the Bahrain e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Consumer Strength with Enterprise Upside

B2C transactions commanded 71.95% of Bahrain e-commerce market share in 2025 on the strength of broad digital wallet uptake and 720 government e-services that normalize online payments. Business buyers lagged but are accelerating at 16.05% CAGR as firms adopt cloud invoicing and integrate with Sijilat licensing tools. The Bahrain e-commerce market size for B2B orders is projected to close much of the gap by 2031 through marketplace catalogs that sync with ERP workflows. Enterprise demand is underpinned by USD 12 billion in tech pledges secured at Gateway Gulf 2024, which will add AI, cloud, and fintech capacity. As product data, credit terms, and regulatory compliance harmonize, the lines between procurement and retail experiences blur. Platforms that embed procurement analytics and one-click reordering should capture sticky enterprise spend, lifting overall order values across the Bahrain e-commerce industry.

Rapid B2B adoption also raises the need for shared logistics hubs and neutral payment rails. Open-banking mandates allow suppliers to initiate instant settlements, cutting Days-Sales-Outstanding. While consumer traffic fuels scale, enterprise workflows supply margin stability, positioning omni-model operators to overtake pure-play peers within the Bahrain e-commerce market.

By Device Type: Smartphones Dominate Digital Buying

Smartphones contributed 67.98% of Bahrain e-commerce transactions in 2025 yet still clock the highest 15.22% CAGR, confirming a mobile-first paradigm. High 5G penetration plus biometric eKey authentication trims page loads and login steps, lifting conversion to above global averages. Desktops retain relevance for higher-ticket carts and B2B quotes, but their share slips yearly as social commerce funnels shoppers directly to mobile checkout. Tablets and emerging devices such as smart TVs occupy niche slots, often as discovery screens feeding later phone purchases.

The Bahrain e-commerce market size tied to mobile orders is forecast to double by 2031 as shoppable video, augmented reality try-ons, and voice search mature. Retailers re-design storefronts with compressed image files and one-handed navigation, while logistics apps push driver updates to consumers in real time. Transaction alerts via BenefitPay reinforce trust and reduce disputes. The dominance of the handheld screen makes responsive design and app loyalty programs critical differentiators in the Bahrain e-commerce industry.

By Payment Method: Wallet First, BNPL Rising

Digital wallets led all methods with 46.35% of the Bahrain e-commerce market size in 2025, buoyed by the BENEFIT network’s instant bank-linked transfers. Cards still enjoy wide acceptance due to global schemes, yet the share trend favors wallets because they support stored credentials and loyalty hooks. BNPL, though only a small base, is the fastest segment at 14.98% CAGR. Services such as Tabby’s Pay-in-4 hosted on EazyPay terminals directly address affordability and boost average basket values.

As BNPL matures, regulators mandate clear fee disclosures, keeping default risk low. Cash-on-delivery has fallen below 10% across the GCC and is forecast to shrink further as fraud coverage and instant refunds enhance digital trust. For the Bahrain e-commerce market, payment orchestration layers that auto-route transactions to the cheapest rail while offering installments will become standard. Platforms balancing cost, approval speed, and shopper preference will reduce cart abandonment.

By Product Category: Fashion Leads, Food Expands

Fashion and apparel held 28.15% Bahrain e-commerce market share in 2025, supported by in-store pickups at global brands like Calvin Klein and Skechers. Cross-border assortment from neighboring GCC warehouses keeps styles current and shipping swift. Beauty follows closely, fueled by GCC skincare spend rising 30% in 2023. Electronics remain a solid performer after the 2024 Apple Store launch at Seef Mall embedded omnichannel repair and click-and-collect services.

Food and beverages is the fastest mover at 14.62% CAGR on the back of a USD 361.1 million delivery app sector that already touches 43.8% of residents. Grocery, pharmacy, and flower deliveries converge onto unified apps like Talabat, creating bundled demand spikes. Cold-chain gaps persist but are closing with new chilled hubs at the airport cargo village. Subscription meal kits and hyperlocal restaurant pop-ups should further grow the Bahrain e-commerce market through higher order frequency.

Geography Analysis

Bahrain’s 765 km² landmass allows national same-day delivery, yet the kingdom also acts as a launchpad into a GCC market projected to reach USD 63 billion by 2027. Via the King Fahad Causeway, sellers can access 75% of Saudi economic activity within hours, translating to USD 9.06 billion in annual two-way trade. Container clearance below three hours at Khalifa Bin Salman Port and 25,000 m² of new air cargo space cut dwell times, giving Bahraini hubs a time-to-market edge.

Free-zone incentives remove import VAT for transit goods, and generous de-minimis thresholds lower B2C customs costs, attracting foreign merchants to base GCC operations in Manama. AWS regional data centers slash latency for shoppers in Kuwait, Qatar, and the UAE, ensuring page speed parity. These factors position the Bahrain e-commerce market as both a domestic growth story and a regional distribution node.

While dense urban cores drive volume, outer towns provide incremental upside if last-mile pooling and parcel lockers gain traction. Government road-widening plans and shared delivery corridors under Tamkeen’s logistics roadmap aim to boost rural service density. As infrastructure spreads, geography should become less of a constraint and more of a catalyst for the Bahrain e-commerce industry.

Competitive Landscape

The Bahrain e-commerce market is moderately fragmented with global, regional, and local players jostling for share. Amazon benefits from scale and AWS integration, Noon leverages GCC-wide fulfillment, and Talabat dominates food delivery. Homegrown sites such as Dukakeen and social gifting newcomer OlaHub compete on local curation and Arabic UX. Apparel Group’s mall expansion brings 19 international fashion labels under one omnichannel umbrella, raising brand expectations.

Payment specialists are central to differentiation. EazyPay added BNPL through Tabby, while BenefitPay scales wallet rail adoption. Logistics startups like Parcel pivot into Saudi routes, showcasing a “Bahrain-built, region-served” playbook. AI analytics firm Intelligence Lens set up its headquarters in Manama to supply real-time commerce dashboards, indicating a data-led arms race.

The Central Bank’s sandbox hosts over 30 fintech pilots from 15+ jurisdictions, encouraging product variety but also increasing regulatory oversight. Over the forecast period, alliances between last-mile firms and payment gateways are likely as firms seek full-stack offerings. Consolidation around omni-category platforms may emerge, yet niche verticals such as ethical fashion or halal beauty remain open fields within the Bahrain e-commerce market.

Bahrain E-commerce Industry Leaders

Amazon.com, Inc.

H & M Hennes & Mauritz AB

AliExpress

Namshi General Trading L.L.C

Talabat Middle East Internet Services Company W.L.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Apparel Group opened 19 stores at The Avenues Phase 2, adding Tommy Hilfiger and Calvin Klein and linking online loyalty with in-store pickup.

- March 2025: The government launched My Gov and eKey 2.0, combining 41 digital public services with biometric login for more than 2 million monthly verifications.

- February 2025: Delivery startup Parcel entered Riyadh after 1.5 million local drops, exporting Bahrain’s last-mile tech know-how.

- January 2025: Tamkeen and AWS began a national AI skills program to feed e-commerce talent pipelines.

Bahrain E-commerce Market Report Scope

The Bahrain e-commerce market is segmented into B2B E-commerce and B2C E-commerce. By B2C E-commerce, the market studied is further subdivided into beauty and personal care, consumer electronics, fashion and apparel, food and beverage, and furniture and home. The report studies the impact of COVID-19 on the studied market. The market studied briefs about the ongoing trends and challenges of the e-commerce market in Bahrain.

By Business Model

| B2B |

| B2C |

By Device Type for B2C E-commerce

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method for B2C E-commerce

| Credit / Debit Cards |

| Digital Wallets |

| Buy-Now-Pay-Later (BNPL) |

| Other Payment Methods |

By Product Category for B2C E-commerce

| Beauty and Personal Care | Hair Care |

| Skin Care | |

| Cosmetics and Beauty Tools | |

| Other Types | |

| Consumer Electronics | Mobile Phones |

| PCs and Laptops | |

| Audio Devices | |

| Gaming Devices | |

| Other Types | |

| Fashion and Apparel | Clothing |

| Footwear | |

| Fashion Accessories | |

| Other Types | |

| Food and Beverages | Packaged Food |

| Bakery and Confectionery | |

| Meat, Poultry and Seafood | |

| Other Types | |

| Furniture and Home | Home Furniture |

| Office Furniture | |

| Outdoor Furniture | |

| Other Types | |

| Other Product Categories |

| By Business Model | B2B | |

| B2C | ||

| By Device Type for B2C E-commerce | Smartphone / Mobile | |

| Desktop and Laptop | ||

| Other Device Types | ||

| By Payment Method for B2C E-commerce | Credit / Debit Cards | |

| Digital Wallets | ||

| Buy-Now-Pay-Later (BNPL) | ||

| Other Payment Methods | ||

| By Product Category for B2C E-commerce | Beauty and Personal Care | Hair Care |

| Skin Care | ||

| Cosmetics and Beauty Tools | ||

| Other Types | ||

| Consumer Electronics | Mobile Phones | |

| PCs and Laptops | ||

| Audio Devices | ||

| Gaming Devices | ||

| Other Types | ||

| Fashion and Apparel | Clothing | |

| Footwear | ||

| Fashion Accessories | ||

| Other Types | ||

| Food and Beverages | Packaged Food | |

| Bakery and Confectionery | ||

| Meat, Poultry and Seafood | ||

| Other Types | ||

| Furniture and Home | Home Furniture | |

| Office Furniture | ||

| Outdoor Furniture | ||

| Other Types | ||

| Other Product Categories | ||

Key Questions Answered in the Report

How large will online sales in Bahrain be by 2031?

The Bahrain e-commerce market size is forecast to reach USD 2.73 billion by 2031, growing at 14.22% CAGR.

Which device drives most online purchases in Bahrain?

Smartphones generate 67.98% of transactions and are expanding at 15.22% CAGR, reflecting a clear mobile-first pattern.

What payment method is most popular among Bahraini online shoppers?

Digital wallets lead with 46.35% share, while BNPL is the fastest-growing option at 14.98% CAGR.

Which product line sells the most online?

Fashion and apparel hold the highest share at 28.15%, supported by a robust omnichannel presence of global brands.

What hampers e-commerce expansion in Bahrain?

Key constraints include high last-mile costs in low-density areas and rising cyber-fraud incidents that undermine buyer confidence.

Page last updated on: