Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

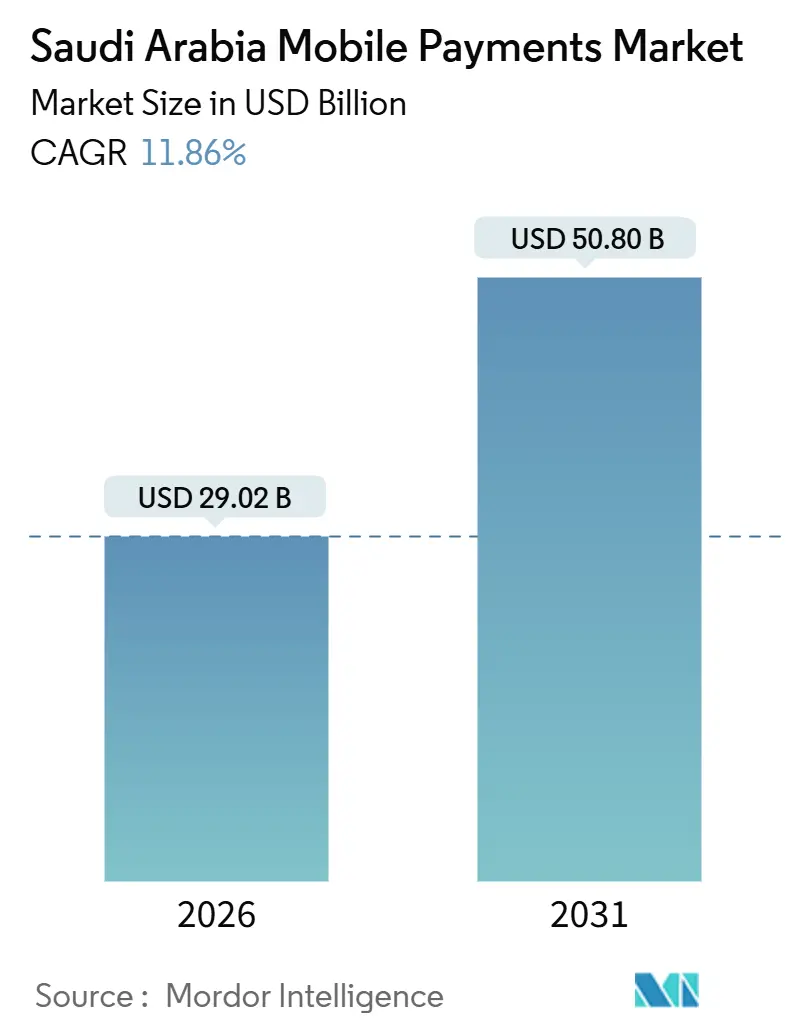

| Market Size (2026) | USD 29.02 Billion |

| Market Size (2031) | USD 50.80 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Mobile Payments Market Analysis by Mordor Intelligence

The Saudi Arabia mobile payments market size was valued at USD 29.02 billion in 2026 to reach USD 50.8 billion by 2031, at a CAGR of 11.86% during the forecast period (2026-2031). This headline growth traces directly to Vision 2030’s cash-lite mandate, which pushed electronic payments to 79% of all retail transactions in 2024. Mandatory integration with SAMA’s Sarie rails, the world-leading 5G coverage that now reaches more than 90% of residents, and a tech-savvy consumer base have combined to propel the Saudi Arabia mobile payments market ahead of most emerging peers. Proximity payments still dominate everyday commerce, yet remote payments are scaling faster as e-commerce volumes climb. Competitive intensity is building rapidly: 224 licensed fintechs were active by mid-2024, and SAMA targets 525 entities by 2030.1Monsha’at, “SME Monitor Q2 2024,” monshaat.gov.sa While fraud concerns and QR-code fragmentation create friction, the medium-term outlook remains strongly positive because regulators, telcos, and payment providers are strategically aligned on a digital-first payment future.

Key Report Takeaways

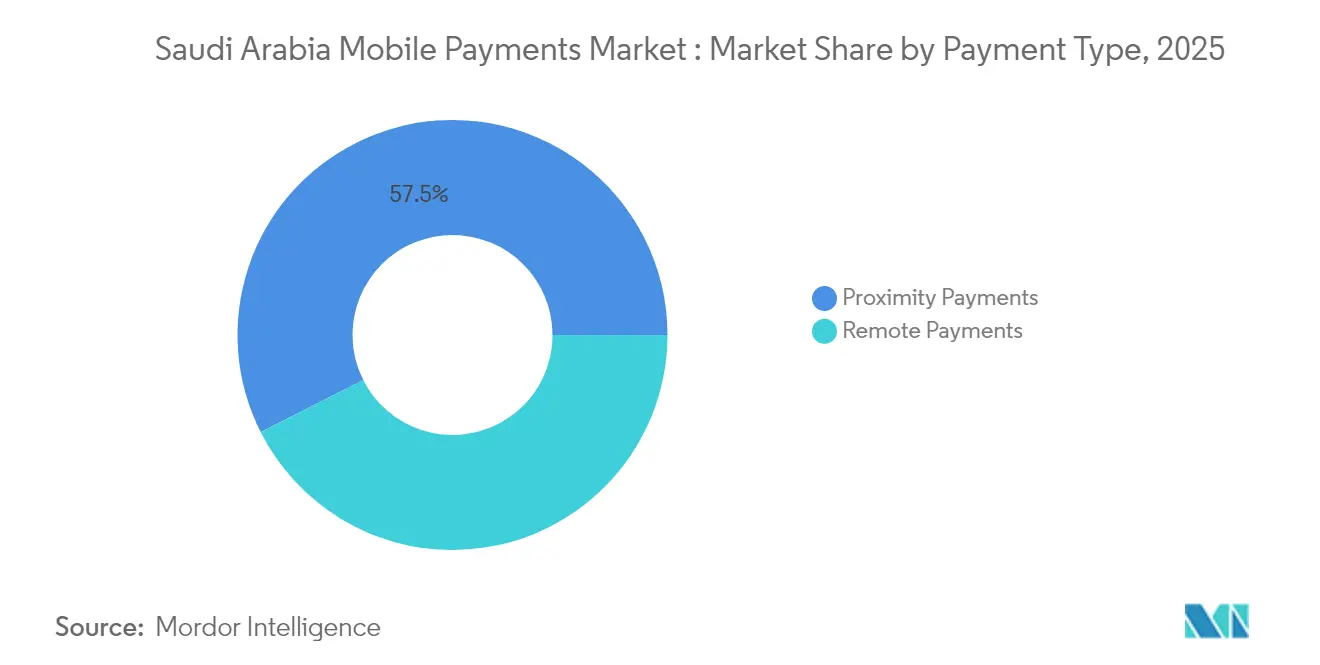

- By payment type: Proximity payments led with 57.45% of Saudi Arabia mobile payments market share in 2025; remote payments are on pace for a 15.05% CAGR through 2031.

- By transaction type: In-store POS maintained 45.30% share of the Saudi Arabia mobile payments market size in 2025, while peer-to-peer transfers post the fastest 15.85% CAGR through 2031.

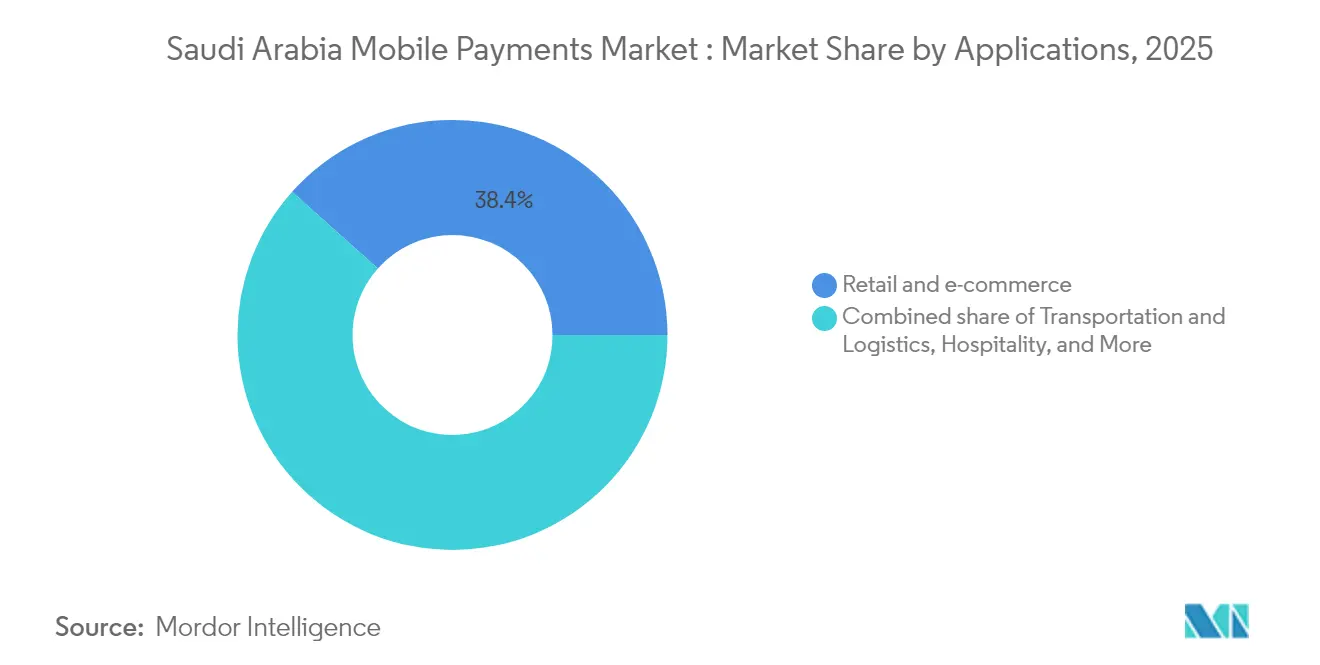

- By application: Retail and e-commerce represented 38.40% of the Saudi Arabia mobile payments market size in 2025; government and public-sector payments are accelerating at a 14.35% CAGR to 2031.

- By end-user: Personal users accounted for 83.25% of the Saudi Arabia mobile payments market share in 2025, yet the business segment is growing at 17.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory adoption of SAMA's Sarie instant-payments rails | + 3.2% | National, with concentration in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| 5G-enabled smartphone ubiquity | +2.8% | National, with early gains in major cities | Short term (≤ 2 years) |

| Vision 2030 cash-lite targets & fiscal incentives | +2.1% | National, government-led initiatives | Long term (≥ 4 years) |

| Pilgrim-service digital wallets (Hajj & Umrah) | +1.9% | Mecca, Medina, with international pilgrim impact | Medium term (2-4 years) |

| Real-time payroll disbursement via WPS mobile channels | +1.6% | National, with SME sector focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Adoption of SAMA’s Sarie Instant-Payments Rails

Sarie processed 10.8 billion real-time transactions in 2024, a 24% annual surge that reset consumer expectations for always-on, sub-second settlement.[2]Central Banking, “Digital payments in Saudi Arabia rise to 70% of retail transactions,” centralbanking.com Settlement fees below SAR 1 encourage merchants to reroute small-ticket sales through Sarie, trimming card costs and freeing liquidity in the banking system. The alias-based address scheme, which lets payers use a mobile number rather than an IBAN, removed the friction that previously deterred unbanked users. Local banks now prioritize Sarie rails for both retail and treasury flows, shrinking dependence on global correspondent networks and giving domestic providers a speed and cost advantage over foreign rivals.

5G-Enabled Smartphone Ubiquity

GCC markets already lead the world in 5G adoption, and Saudi Arabia contributes the bulk of that penetration with 73% of mobile subscriptions expected to be 5G by 2026.[3]Ericsson, “5G Forecast in Gulf Cooperation Council Countries,” ericsson.com Average smartphone traffic exceeded 18 GB per month in 2024, unlocking biometric, augmented-reality, and AI-embedded payment use cases. Apple’s Express Mode roll-out on Riyadh Metro exemplifies frictionless contactless transit and reinforces mass-market familiarity with mobile wallets. Ultralow latency also enables in-app fraud scoring in milliseconds, a prerequisite for Sarie-speed settlement. Collectively, network readiness closes the gap between experimental pilots and mainstream deployment.

Vision 2030 Cash-Lite Targets & Fiscal Incentives

The Financial Sector Development Program stipulates that non-cash instruments must represent 80% of retail volume by 2030, only one point above the 79% already reached in 2024.[4]Ministry of Finance, “Budget Statement Fiscal Year 2024,” mof.gov.sa Ministries now pay suppliers solely through electronic rails, nudging micro-merchants to acquire POS or softPOS solutions or risk losing public contracts. A sandbox regime fast-tracks licensing for novel payment products, compressing time-to-market and crowding the field with agile entrants. Tax offsets for digital receipts and penalties for excess cash use create a financial bias that merchants cannot ignore. As acceptance rises, the Saudi Arabia mobile payments market experiences reinforcing network effects between consumers and merchants.

Pilgrim-Service Digital Wallets (Hajj & Umrah)

Nusuk Wallet, introduced by Saudi National Bank and the Ministry of Hajj, processed pilgrim payments for more than 2 million visitors in its inaugural season. Biometric onboarding sidesteps local KYC constraints for foreign visitors, while AI-powered controls curb fraud in peak weeks. Concentrated seasonal volumes provide a stress-test for scale; success signals to global investors that Saudi payment infrastructure can handle cross-border flows. Regulatory learnings from this niche extend to wider cross-border remittance innovation, anchoring Saudi Arabia’s ambition to become a regional payment hub.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fraud & cyber-security concerns | -1.8% | National, with higher impact in rural areas | Short term (≤ 2 years) |

| Low acceptance by micro-merchants outside tier-1 cities | -1.4% | Secondary cities, rural areas | Medium term (2-4 years) |

| Fragmented QR standards slowing interoperability | -1.1% | National, with concentration in retail sectors | Medium term (2-4 years) |

| Data-localisation hurdles for foreign wallet providers | -0.9% | National, affecting international players | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fraud & Cyber-Security Concerns

A recent user study showed 39% of Saudis dissatisfied with payment security, while 35% remain wary of transaction traceability. SAMA’s Counter-Fraud Framework obliges providers to invest heavily in prevention, detection, and response, stretching the budgets of start-ups that already face intense customer-acquisition costs. AI-based scoring reduces chargebacks but occasionally blocks legitimate transfers, harming user trust. The attack surface expands as payment volumes soar, making continuous security upgrades non-negotiable for providers seeking scale.

Low Acceptance by Micro-Merchants Outside Tier-1 Cities

For merchants in secondary cities, terminal acquisition costs, patchy broadband, and limited digital literacy still deter POS deployment. Customers in rural regions cling to cash due to banking gaps, dampening merchant incentives to invest in acceptance technology. The resulting geographic divide slows inclusive market penetration and leaves untapped volume on the table for ambitious providers that can craft ultra-low-cost, offline-capable solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Remote Surge Challenges Proximity Dominance

Proximity payments accounted for 57.45% of Saudi Arabia mobile payments market share in 2025, supported by more than 1 million POS terminals. Yet remote payments are climbing at a 15.05% CAGR to 2031 as e-commerce sales and government e-service fees migrate online. Contactless readiness is wide-spread—94% of card holders tapped in 2024—signaling comfort with device-based payments. Driven by 5G speed, remote channels integrate AR shopping and voice checkout that play to Saudi consumers’ high mobile data appetite.

In-app government payments via Absher, covering more than 700 services, create recurring remote volumes that deprioritize cash. Apple Pay’s transit launch validates proximity use cases, while the Ministry of Communications authorizes non-banks to embed payments in consumer apps, widening the provider pool. Providers that master omnichannel orchestration will secure mindshare as shoppers blend remote browsing with in-store pickup, gradually shifting wallet share away from plastic cards and towards the Saudi Arabia mobile payments market.

By Transaction Type: P2P Growth Outpaces Traditional Commerce

In-store POS preserved 45.30% of Saudi Arabia mobile payments market size in 2025, reflecting high foot-traffic retail and food-service spending. P2P transfers, however, post a brisk 15.85% CAGR as real-time payroll and remittance flows migrate to wallets. Mada card e-commerce spending hit SAR 197.42 billion (USD 52.6 billion) in 2024, underscoring a sizable person-to-merchant pool. Bill-pay and fee collection segments register steady but less dramatic gains.

Momentum in P2P stems from eight-million-strong STC Pay users sending salaries, allowances, and micro-loans in seconds. International remittances are also digitalizing, eroding money-transfer agents’ share. Diversified use cases hedge providers against cyclical retail spending and distribute profit streams across multiple verticals.

By Application: Government Sector Acceleration Reshapes Market Dynamics

Retail and e-commerce maintained 38.40% of Saudi Arabia mobile payments market size in 2025, fueled by consumer spending and high smartphone engagement. Government applications clock the fastest 14.35% CAGR as Absher completed 430 million e-transactions in 2024. Transportation payments ride Apple Pay’s metro rollout, while hospitality leverages growing tourism demand.

Education payments through SADAD reached SAR 1 billion (USD 267 million) in 2024, a 4.3% uptick on digital tuition settlement. Healthcare remains small but shows promise, with eHealth–Fintech pilots forecasting transaction values of USD 87.14 billion by 2028. Application diversification spreads risk and opens tailored solution lanes, such as pilgrim wallets and sector-specific APIs, across the Saudi Arabia mobile payments market.

By End-User: Business Segment Momentum Signals Enterprise Digitization

Personal wallets still dominate with 83.25% share, but enterprise payments are scaling at 17.05% CAGR. SMEs embrace mobile interfaces to pay suppliers, settle utility bills, and reimburse staff, aligning with Vision 2030’s SME empowerment agenda. The fintech workforce passed 7,000 employees in 2024, supplying domain talent that codes B2B workflows into consumer-grade app designs.

Enterprise adoption rises on the back of Sharia-compliant digital products, Arabic interfaces, and seamless ERP plugins. As firms swap checks for Sarie rails and audit-friendly wallets, the Saudi Arabia mobile payments market shifts from consumer novelty to core corporate infrastructure, presenting white-space for providers skilled in treasury-grade security and complex approvals.

Geography Analysis

Major metropolitan corridors—Riyadh, Jeddah, and Dammam—collectively host more than 95% 5G penetration and the densest POS networks, underpinning 79% national e-payment adoption in 2024. Riyadh anchors fintech headquarters and early Open-Banking pilots, giving capital-region consumers first access to cutting-edge wallet features. The Eastern Province channels industrial B2B payments through Sarie, while the Western Province caters to pilgrim wallets during peak religious seasons.

Mecca and Medina process concentrated seasonal volumes as over 2 million pilgrims transact through the Nusuk Wallet each year, spurring infrastructure investment that can be repurposed for local commerce outside pilgrimage windows. Secondary cities such as Abha and Tabuk lag due to patchy broadband and lower merchant readiness, yet government programs targeting 80% cash-less payments by 2030 incentivize banks to deploy softPOS and QR-code schemes tailored for smaller merchants. Rural areas remain cash-centric, though mobile connectivity expansion gradually widens the addressable user base.

SAMA’s national framework allows regional sandboxes; hence fintechs run geo-targeted pilots—e.g., agriculture wallet trials in Al-Qassim—before scaling nationwide. Cross-border functionality clusters in commercial hubs, but Nusuk’s success suggests broader potential for specialized foreign-exchange wallets. Providers must reconcile a patchwork of urban sophistication and rural constraints as they plot roll-out roadmaps across the Saudi Arabia mobile payments market.

Competitive Landscape

The Saudi Arabia mobile payments market features 224 licensed fintechs plus global brands, yielding a moderately fragmented competitive field. Domestic leader STC Pay enjoys an 8-million-strong customer base, while Mada Pay leverages the national card switch and Al Rajhi Wallet differentiates on Sharia compliance. Apple Pay commands over 20% wallet usage on Saudi web checkouts, the highest share worldwide. Strategic differentiation hinges on regulatory mastery, local partnerships, and vertical specialization.

Players allocate capital toward SAMA’s Counter-Fraud compliance, Open-Banking APIs, and merchant acquisition campaigns. For example, Mastercard’s data-localization project and Amazon Payment Services’ gateway partnership broaden acquirer choice for thousands of merchants. Telr’s alliance with Saudi Awwal Bank adds BNPL, QR, and payment-link features for SMEs, plugging acceptance gaps outside tier-1 cities.

Emerging disruptors deploy AI fraud analytics, blockchain settlement, and biometric authentication to capture niches such as cross-border micro-remittances and healthcare wallets. Incumbent banks counter with ecosystem plays, embedding payments into super-apps that bundle savings, credit, and lifestyle offers. Competitive intensity is poised to heighten as SAMA targets 525 licensed fintechs by 2030, forcing consolidation or strategic alliances to achieve scale within the Saudi Arabia mobile payments market.

Saudi Arabia Mobile Payments Industry Leaders

BayanPay (Bayan Payments Ltd.)

Alinma Pay (Alinma Bank))

Apple Pay (Apple Inc.)

Saudi Digital Payments Co.

Mada Pay (Saudi Payments)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Apple confirmed a SAR 10 billion (USD 2.7 billion) Saudi investment package, including an online store launch and flagship outlets at Diriyah, and extended Express Mode on Riyadh Metro—strategically locking in iOS wallet preference ahead of new merchant roll-outs.

- May 2025: SAMA disclosed that electronic payments reached 79% of 2024 retail volume, validating Vision 2030’s cash-lite trajectory and setting an implicit benchmark for payment providers vying for incremental share.

- April 2025: Telr partnered with Saudi Awwal Bank to extend QR, payment-link, and BNPL rails, aiming to shore up SME acceptance in underserved regions.

- March 2025: Absher logged 430 million e-transactions for 2024, reinforcing government services as a prime catalyst for wallet usage and onboarding.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabia mobile payments market as all value-based transactions initiated through smartphones or tablets that clear over wireless interfaces such as NFC, QR, or in-app token rails, regardless of whether the funding instrument is a bank account, card, or stored value wallet. Transactions executed on feature-phone USSD menus or traditional desktop web checkouts are not counted within this boundary.

Scope exclusion: person-to-business cash-on-delivery settlements are excluded in full.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed executives at domestic wallets, acquirers, and retail chains across Riyadh, Jeddah, and Dammam, while consumer surveys captured frequency and ticket patterns from both citizens and expatriates. These dialogues validated penetration assumptions, fine-tuned average selling price (ASP) curves, and flagged regional seasonality linked to Hajj travel peaks.

Desk Research

We opened the model with macro and usage evidence downloaded from authoritative public sources such as the Saudi Central Bank (SAMA), the Ministry of Communications and Information Technology, Vision 2030 progress scorecards, GSMA Intelligence handset datasets, and peer-reviewed papers indexed on JSTOR. These streams established smartphone stock, average wallet ticket size, real-time payment adoption, and policy milestones. Company filings, IPO prospectuses, and investor presentations were mined for channel throughput hints, then cross-checked against shipment values pulled from the D&B Hoovers paid database. International comparators from the World Bank and the Arab Monetary Fund guided currency and inflation harmonization. The sources listed are illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build began with SAMA-reported electronic retail outlay, from which we isolated the mobile slice through prevalence-to-value ratios derived from survey and GSMA data, which are then corroborated via selective bottom-up wallet volume roll-ups. Key model drivers include smartphone penetration, active wallet ratio, SARIE instant-payment share, average ticket migration, regulatory caps on interchange, and BNPL uptake. Multivariate regression, tested for stationarity, projected each driver through 2030. Scenario analysis shaded downside risk from fee-cap shocks. Gaps in supplier roll-ups were bridged using channel check medians plus weighted ASP variances.

Data Validation & Update Cycle

Outputs pass a two-step peer review where anomalies over three percent trigger a model rerun and, if needed, a follow-up call with prior respondents. Reports refresh annually and are re-opened mid-cycle when material events such as a new mandatory wallet license class occur. Before delivery, an analyst performs a last validation sweep so clients receive our most current view.

Why Mordor's Saudi Arabia Mobile Payments Baseline Rings True

Published numbers seldom align because firms select different transaction pools, funding definitions, or refresh cadences. We acknowledge these divergences upfront and show where they surface most.

Key gap drivers arise when other studies: 1) count only proximity taps or, conversely, fold card and bank transfer spend into a single total; 2) apply global ASP proxies instead of interviewing local merchants about fees; and 3) freeze exchange rates for the forecast horizon while Mordor rolls quarterly averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.94 B (2025) | Mordor Intelligence | - |

| USD 24.70 B (2024) | Global Consultancy A | Limits scope to smartphone NFC and QR, omits in-app remote flows |

| USD 41.30 B (2024) | Regional Consultancy B | Aggregates all card, bank, and mobile channels, inflating base |

| USD 1.03 B (2024) | Industry Association C | Tracks only wallet load value, excludes peer-to-merchant spend |

The comparison shows that once scope and driver selections are harmonized, our balanced, variable-linked baseline offers a dependable anchor for planning decisions.

Key Questions Answered in the Report

What is the current size of the Saudi Arabia mobile payments market?

The market is worth USD 29.02 billion in 2026 and is on track to reach USD 50.8 billion by 2031.

Which segment is growing fastest within the market?

Remote payments and peer-to-peer transfers lead with CAGRs of 15.05% and 15.85% respectively, buoyed by e-commerce and real-time payroll flows.

How significant is government influence on market growth?

Vision 2030’s target of 80% non-cash transactions and mandatory Sarie rail adoption add roughly 3.2 percentage points to market CAGR.

What role do international players such as Apple Pay have?

Apple Pay already captures over 20% of Saudi online wallet checkouts, and new Express Mode transit deployments further entrench its footprint.

What are the main challenges to wider adoption outside major cities?

Fraud concerns and low micro-merchant acceptance due to device costs and patchy connectivity remain key barriers in secondary cities and rural areas.

How competitive is the provider landscape?

The field is moderately concentrated: five leading providers hold slightly more than 60% share, leaving room for niche entrants but also driving consolidation pressure.

Page last updated on: