Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

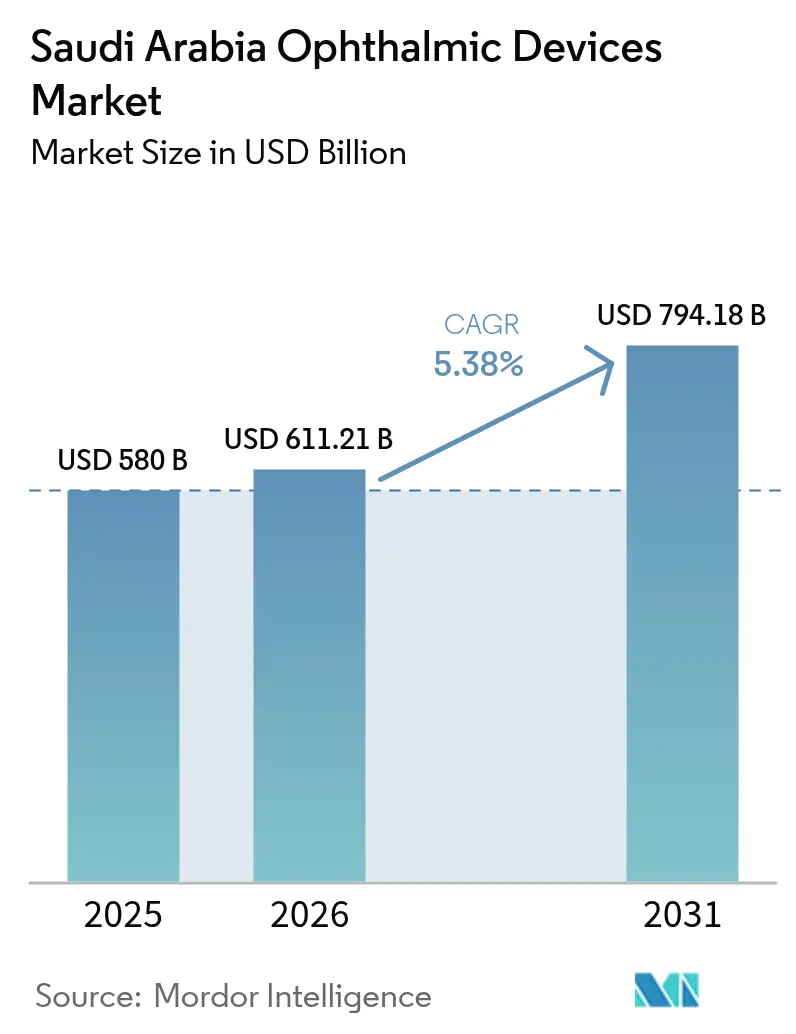

| Base Year Market Size (2025) | USD 580 Billion |

| Market Size (2026) | USD 611.21 Billion |

| Market Size (2031) | USD 794.18 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

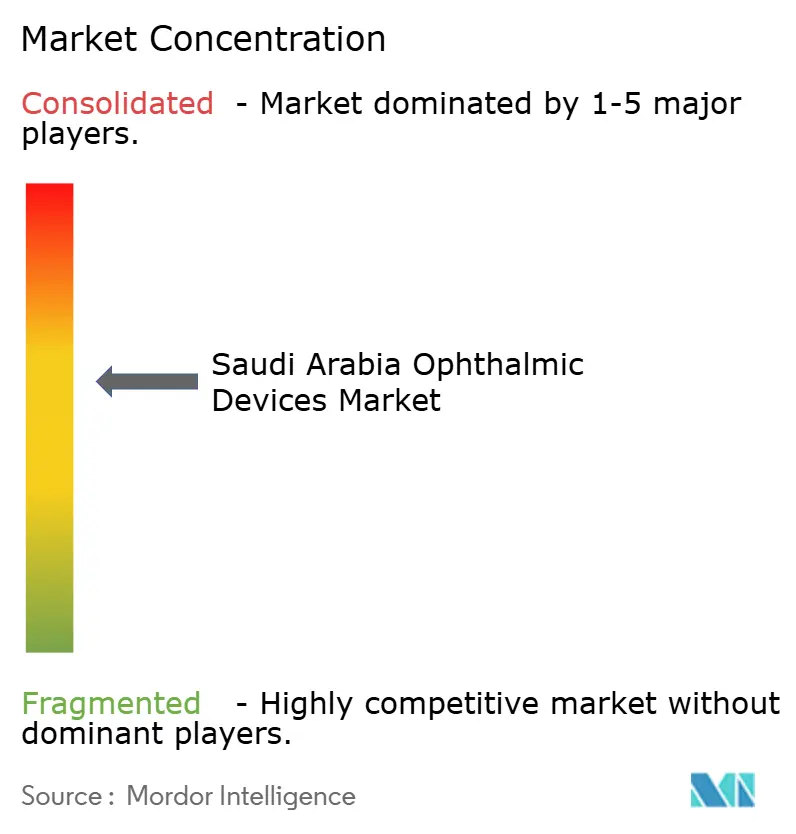

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Ophthalmic Devices Market Analysis by Mordor Intelligence

The Saudi Arabia ophthalmic devices market size is expected to grow from USD 580 million in 2025 to USD 611.21 million in 2026 and is forecast to reach USD 794.18 million by 2031 at 5.38% CAGR over 2026-2031. This advance is anchored in Vision 2030’s USD 65 billion healthcare-modernization plan. Sustained demand arises from a diabetes burden that climbed to 7 million cases in 2021 and is expected to hit 8.4 million by 2030, heightening the need for screening and monitoring technologies. Rapid adoption of artificial-intelligence (AI) diagnostics, growing private investment in ambulatory eye-care centers, and the emergence of Riyadh and Jeddah as medical-tourism hubs further energize the Saudi Arabia ophthalmic devices market. Headwinds persist, however, in the form of import dependency that raises device prices and a shortage of certified technicians, which limits throughput despite equipment availability. Policymakers are therefore refining Saudi Food and Drug Authority (SFDA) procedures and funding training pipelines to ease these constraints.

Key Report Takeaways

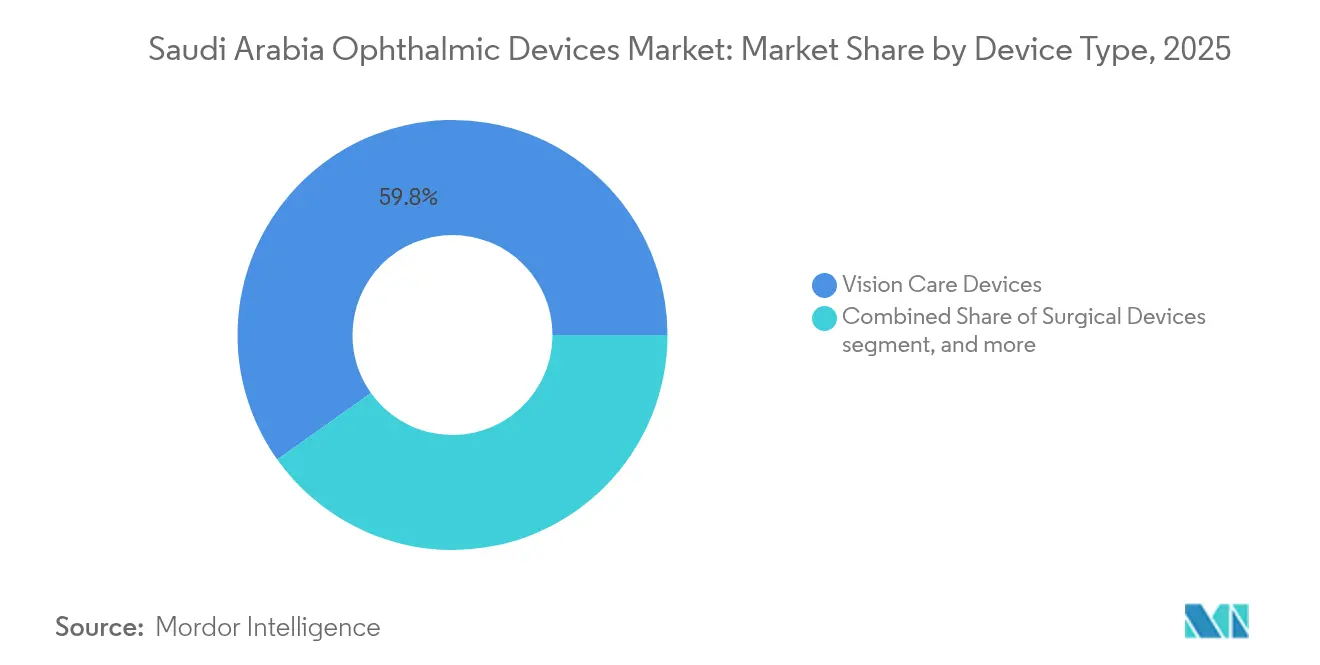

- By device type, vision care devices held 59.83% of the Saudi Arabia ophthalmic devices market share in 2025; Diagnostic & monitoring devices are projected to expand at a 7.42% CAGR through 2031.

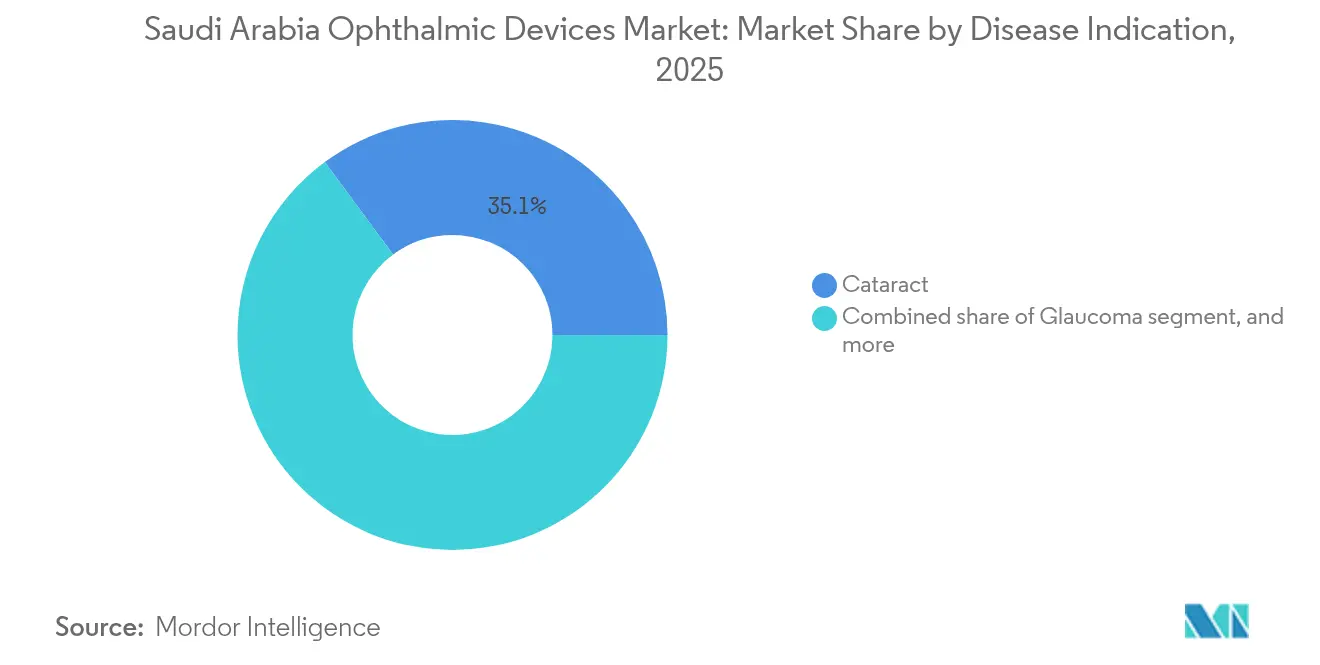

- By disease indication, cataract accounted for 35.12% of the Saudi Arabia ophthalmic devices market size in 2025, while Diabetic retinopathy is set to grow at a 6.74% CAGR to 2031.

- By end-user, hospitals commanded 45.05% revenue share in 2025; Ambulatory surgery centers are expected to post a 6.55% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-funded Vision 2030 ophthalmology infrastructure expansion | +1.8% | Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| High diabetes prevalence driving AI-based diabetic-retinopathy screening uptake | +1.2% | Nationwide; strongest in Western region | Long term (≥ 4 years) |

| Compulsory pre-marital & school eye-health screening programmes | +0.8% | Initially urban, then national | Medium term (2-4 years) |

| Rise of premium elective LASIK & cataract surgeries via medical-tourism hubs (Riyadh, Jeddah) | +0.9% | Riyadh and Jeddah | Short term (≤ 2 years) |

| Emergence of public–private ophthalmic centres of excellence under NHC PPP model | +0.6% | Major metropolitan areas | Medium term (2-4 years) |

| Rapid adoption of cloud-connected OCT & fundus cameras in primary-care polyclinics | +0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Funded Vision 2030 Ophthalmology Infrastructure Expansion

Vision 2030 seeks to raise private-sector participation in healthcare to 68% by 2030 and add about 84,000 beds to reach OECD standards[1]Vision 2030 Program, “SEHA Virtual Hospital Overview,” vision2030.gov.sa. Expansion plans by large hospital groups—such as Dr Sulaiman Al Habib Medical Services, which intends to grow capacity from 1,913 to 3,609 beds by 2028—translate directly into higher purchases of surgical microscopes, optical-coherence-tomography (OCT) scanners, and tele-ophthalmology platforms. The SEHA Virtual Hospital now links more than 150 hospitals, enabling remote retinal assessments and extending specialist reach.

High Diabetes Prevalence Driving AI-Based Diabetic-Retinopathy Screening Uptake

Diabetes affects 31.0% of adults in the Kingdom, and diabetic retinopathy (DR) impacts 46% of diabetics in the Western region. An AI-enabled national tele-retinopathy programme launched in 2024 accelerates screening throughput and accuracy. Early results indicate a 30.0% reduction in unnecessary referrals, spurring demand for AI-ready fundus cameras and cloud-integrated image-management systems. Persistent knowledge gaps—29% of patients report never having had an eye exam—are addressed by payer-funded awareness drives that should boost device utilisation.

Compulsory Premarital & School Eye-Health Screening Programmes

Mandatory premarital genetic screening, in place since 2004, still lacks comprehensive ocular testing despite high hereditary-eye-disease prevalence. Consanguinity accounts for 87.2% of paediatric strabismus cases, highlighting scope for portable autorefractors in primary-care clinics. School screening remains ad-hoc; a Qassim study found a 26.6% vision-test failure rate among preschoolers, signalling strong latent demand for handheld diagnostic kits[2]Naif Almutairi, “Primary Health-Care Eye Services in Saudi Arabia,” sciencedirect.com. Parents show high awareness yet limited follow-through on regular eye checks, suggesting growth potential once national guidelines are enacted.

Rise of Premium Elective LASIK & Cataract Surgeries Via Medical-Tourism Hubs

Riyadh and Jeddah position themselves as regional centers for high-end eye surgery. Magrabi Health alone performs more than 200,000 procedures annually across 40 sites, having pioneered LASIK in the region. Competitive bundled pricing draws Gulf patients, supporting steady demand for femtosecond-laser systems, premium intra-ocular lenses, and advanced diagnostics. Alcon strengthened this premium ecosystem by opening the Middle East’s first Alcon Experience Center in Jeddah in March 2025.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-dependence inflating device prices post-tariff harmonisation (SFDA) | −1.2% | Nationwide; premium segments | Short term (≤ 2 years) |

| Shortage of certified ophthalmic technicians limiting diagnostic throughput | −0.9% | Rural regions most affected | Medium term (2-4 years) |

| Lengthy SFDA device-registration timelines delaying launches | −0.7% | Nationwide | Short term (≤ 2 years) |

| Price-sensitive contact-lens e-commerce dampening uptake of premium vision-care devices | −0.4% | Nationwide; strongest in urban e-commerce channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Import Dependence Inflating Device Prices

The SFDA mandates ISO 13485 certification and local Authorised Representatives, raising import-transaction costs. Beginning January 2025, all medical devices also require SABER platform conformity certificates, which add compliance fees that sellers pass through to buyers. These expenses elevate landed costs—particularly for premium imaging equipment—by an estimated 15%, dampening uptake in smaller clinics.

Shortage of Certified Ophthalmic Technicians Limiting Diagnostic Throughput

Saudi Arabia hosts 2,608 ophthalmologists (81.06 per million people), surpassing WHO guidelines, yet only 38% are nationals and distribution is uneven: Riyadh has 75.6 per million versus 42.8 per million in Jazan[3]Khalid Aldebasi, “Ophthalmologist Distribution in Saudi Regions,” ncbi.nlm.nih.gov. At the technician level, only 0.47% of primary-care centers provide optometry services, so high-value devices such as OCT scanners often sit under-utilised. Government scholarships and fast-track licensing aim to close the skills gap but will take years to yield a balanced workforce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostic Equipment Accelerates Innovation

Vision care devices retained a 59.83% share of the Saudi Arabia ophthalmic devices market in 2025, supported by steady demand for spectacles, contact lenses, and dispensing systems. Diagnostic & Monitoring Devices, however, are set to expand at a 7.42% CAGR through 2031, reflecting hospitals’ shift toward early-stage disease identification. Within this cluster, optical-coherence-tomography scanners should command 24.18% of diagnostic revenue in 2025, benefiting from superior retinal-layer visualisation that aids macular-degeneration and diabetic-retinopathy screening. Ultra-wide-field fundus cameras also post strong orders because clinicians want comprehensive peripheral-retina images to detect lesions missed by 45-degree systems.

The diagnostic up-cycle is reinforced by national tele-health mandates that integrate cloud-based image management and AI grading. As a result, the Saudi Arabia ophthalmic devices market size allocated to diagnostic hardware rises in tandem with digitally linked screening programmes. Surgical-device demand grows at a moderate clip, buoyed by premium intra-ocular-lens adoption in elective cataract and refractive procedures popular in Riyadh and Jeddah. Import tariffs remain a drag on smaller buyers, but multinational suppliers offset duties with leasing options and bundled-service contracts.

By Disease Indication: Diabetic Retinopathy Drives Digital Transformation

Cataract retained 35.12% of revenue in 2025, reflecting an ageing population and high surgery volumes in public hospitals. Diabetic retinopathy now registers the fastest growth trajectory with a 6.74% CAGR forecast for 2026-2031, propelled by a diabetes prevalence that reached 7 million patients in 2021. The Saudi Arabia ophthalmic devices market size tied to diabetic-retinopathy care is therefore climbing quickly as payers subsidise AI-based fundus-camera networks and OCT-angiography units for microvascular mapping.

Glaucoma follows with innovation in micro-invasive implants that lower intra-ocular pressure while reducing recovery time. Cataract solutions continue to benefit from premium multifocal- and toric-lens demand among self-pay and medical-tourism cases. Vendors are introducing disposable vitrectomy packs and dual-platform phaco systems to optimise operating-room turnover in high-volume centres, sustaining overall sales momentum despite price pressures.

By End-User: Ambulatory Surgery Centers Capture Outpatient Shift

Hospitals captured 45.05% of total expenditure in 2025, leveraging integrated care pathways and capital-budget cycles. Yet Ambulatory Surgery Centers (ASCs) are slated for a 6.55% CAGR, mirroring a global pivot toward day-case ophthalmology, especially cataract and LASIK procedures. Government incentives that lift private-sector participation to 68% by 2030 encourage investors to build ASC networks equipped with femtosecond lasers, phaco platforms, and point-of-care diagnostics—all sourced from the Saudi Arabia ophthalmic devices market.

Specialty ophthalmic clinics also scale quickly as regional chains expand footprints beyond Tier-1 cities. These clinics concentrate on refractive and retina-care niches, purchasing compact imaging towers and portable lasers to fit smaller surgical suites. Hospitals still dominate complex ocular-oncology, paediatric, and trauma cases, ensuring baseline demand for high-acuity microscopes and vitrectomy consoles.

Regulatory Landscape

Ophthalmic devices in Saudi Arabia are regulated by the Saudi Food and Drug Authority (SFDA) under its medical devices framework, with market entry centered on obtaining a Medical Device Marketing Authorization (MDMA). Manufacturers, importers, distributors, and Authorized Representatives must operate under an SFDA establishment license, and submissions are routed electronically via the SFDA GHAD portal, alongside a technical file assessment requirement aligned to the device risk profile and classification guidance.

Compliance requirements have expanded in ways that affect ophthalmic device commercialization and lifecycle management. From January 2025, medical devices also require SABER platform conformity certificates, adding a parallel conformity layer that increases administrative burden for import-heavy segments. For device-drug combination offerings relevant to ophthalmology, SFDA issued the Guidance for Combination Products Classification and Registration (Version 2.0) effective March 5, 2026, introducing a Primary Mode of Action (PMOA) approach and a phased plan for ancillary dossier expectations through 2030, which changes dossier planning and sequencing for combination portfolios.

Competitive Landscape

The Saudi Arabia ophthalmic devices market features a moderate concentration. Global OEMs such as Alcon, Carl Zeiss Meditec, Johnson & Johnson Vision, and Bausch + Lomb dominate high-tech segments, leveraging broad portfolios and service networks. Alcon’s Experience Center in Jeddah provides surgeon training and on-site demonstrations, consolidating its influence over premium-device procurement. Multinationals hold a strong foothold in diagnostic imaging and surgical disposables, sectors requiring capital intensity and regulatory experience.

Local and regional chains, including Magrabi Health and Saudi German Hospital Group, compete on service breadth and geographic coverage, often partnering with global suppliers for technology transfers and joint-training initiatives. The rise of AI-based tele-retinopathy platforms creates space for software-driven entrants that differentiate through algorithm accuracy rather than hardware pedigree. Import duties and SFDA timelines, however, favor established distributors that can navigate compliance and finance inventory.

White-space opportunities exist in mobile screening units, low-cost portable fundus cameras, and technician training services. International start-ups offering handheld OCT and smartphone-based anterior-segment imaging may gain traction if they secure authorized-representative partnerships and local technical support. Price-sensitive public tenders still consider value over premium features, positioning mid-tier vendors for share gains once SABER procedures stabilize.

Saudi Arabia Ophthalmic Devices Industry Leaders

Alcon Inc

Bausch Health Companies Inc

Carl Zeiss Meditec AG

Johnson & Johnson Vision Care

EssilorLuxottica SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in scaling diagnostic and monitoring capacity that can operate outside tertiary hospitals. The national tele-retinopathy program launched in 2024 and the SEHA Virtual Hospital network linking more than 150 hospitals have created an operating model for distributed retinal assessment, supporting demand for AI-ready fundus cameras, cloud-connected OCT, and image-management platforms that fit primary-care and polyclinic workflows. With 29% of patients reporting never having had an eye exam, providers and payers have room to expand standardized screening pathways using portable autorefractors, handheld imaging, and service-led deployment (leasing, managed equipment, and on-site training) where technician shortages leave installed equipment underused.

Procurement and localization levers add a further opportunity, especially for suppliers that align to public tenders and local content requirements. Vision 2030 programs and procurement structures, including NUPCO frameworks, reward suppliers that can provide local service coverage, faster turnaround, and localized manufacturing steps such as assembly, packaging, or labeling under SFDA guidance (for example, pathways referenced in MDS-G11). Company moves that deepen local capability, such as Alcon opening its Experience Center in Jeddah in March 2025 for surgeon training and technology education, also point to education-plus-service models as a differentiator alongside hardware sales, particularly in premium cataract and refractive surgery hubs in Riyadh and Jeddah.

Recent Industry Developments

- March 2026: Johnson & Johnson announced U.S. FDA approval of the TECNIS PureSee intraocular lens for cataract surgery. The approval expands the company's surgical vision portfolio that is also commercialized internationally, strengthening competitive positioning in premium IOL categories that are relevant to Saudi Arabia's elective and high-volume cataract centers.

- March 2025: Alcon inaugurated the first Alcon Experience Center in the Middle East and Africa in Jeddah and signed training arrangements with leading hospitals. The facility supports localized surgeon education and product demonstration, which can shorten adoption cycles for advanced cataract and refractive platforms and reinforces after-sales support as a procurement criterion.

- May 2024: Formosa Pharmaceuticals entered an exclusive licensing agreement with Tabuk Pharmaceuticals to commercialize a clobetasol propionate ophthalmic suspension (0.05%) across the Middle East and North Africa. The deal highlights the role of Saudi-based partners in regulatory navigation and commercialization, and it strengthens regional channels that can influence bundled procurement and formulary access alongside ophthalmic procedure device utilization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from ophthalmic devices sold and used in Saudi Arabia for eye diagnosis, vision correction, and eye surgery support, across hospital, clinic, and retail settings, counted at the point of sale to the local customer.

Scope exclusions: We exclude ophthalmic drugs, vision care services, and general hospital equipment that is not primarily intended for eye care use.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- OCT Scanners

- Fundus & Retinal Cameras

- Autorefractors & Keratometers

- Corneal Topography Systems

- Ultrasound Imaging Systems

- Perimeters & Tonometers

- Other Diagnostic & Monitoring Devices

- Surgical Devices

- Cataract Surgical Devices

- Vitreoretinal Surgical Devices

- Refreactive Surgical Devices

- Glaucoma Surgical Devices

- Other Surgical Devices

- Vision Care Devices

- Spectacles Frames & Lenses

- Contact Lenses

- Diagnostic & Monitoring Devices

- By Disease Indication

- Cataract

- Glaucoma

- Diabetic Retinopathy

- Other Disease Indications

- By End-user

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-users

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by pinning down the demand pool and the care setting split, so later assumptions did not drift. We referred to public sources such as the Saudi Ministry of Health statistics releases, the General Authority for Statistics, and World Health Organization country health profiles to understand population, diabetes load, and access signals that shape eye testing and surgery volumes in Saudi Arabia.

To add device and procedure context, we also used materials such as peer-reviewed ophthalmology journals, international diabetes and blindness prevention organizations, and official tender portals where procurement language indicates what is being bought and how frequently. Company annual reports, investor decks, and reputable press were used to sense-check category focus and pricing direction, while paid subscriptions for company financials and intelligence, news and financials, patent databases, and selective tenders tracking helped validate timelines and technology refresh cycles. These desk sources are illustrative and not exhaustive, and we also referred to additional public and paid sources for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what desk sources cannot show clearly, especially current procurement patterns, channel mix, and the practical split between diagnostic equipment and consumables used in Saudi clinic workflows. We spoke with a spread of respondents including distributors, importers, hospital procurement teams, ophthalmologists, and clinic managers across major demand centers in the country, and then used their feedback to close gaps and sanity-check our pricing and volume assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 56% | Functional/Unit leaders: 34% | |

| Smaller Players: 18% | Managers: 54% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up logic, where the starting point was the treated demand pool in Saudi Arabia and how it translates into device usage in eye care settings. For the top-down view, procedure and screening pathways were used to reconstruct demand, and then conversion ratios were applied for device categories tightly linked to care activity.

Key inputs included the diagnosed diabetes population as a proxy for retinal screening needs, cataract and refractive surgery throughput in large hospitals and private centers, installed base replacement cycles for diagnostic devices, average selling price bands for major device groups, and import dependence signals that influence availability and timing. Where needed, selective bottom-up checks were done using distributor channel checks and sampled ASP time-volume calculations, and then totals were adjusted when a local buying pattern suggested a different mix. Gaps were handled by using conservative adoption ranges that were re-tested with interview feedback, rather than forcing a detailed roll-up that cannot be consistently observed.

For forecasting, scenario analysis was used because policy-driven capacity expansions and tender timing can shift annual demand more than a smooth trend line. Assumptions for procedure growth, replacement cadence, and pricing were moved forward using expert consensus from interviews and a review of recent hospital and private sector investment signals.

Data Validation & Update Cycle

Validation was done in layers so the final totals stayed aligned with real-world activity, rather than only matching a single reference number. We compared model outputs against independent signals such as procedure direction, procurement visibility, and category-level pricing, and then reworked any large variance that could not be explained by a clear market driver.

Before sign-off, another analyst reviews the full chain of assumptions, recalculations are performed for outliers, and follow-up calls are triggered when a device category shows an unusual jump or drop. Reports are refreshed annually, and interim adjustments are made if a material policy, reimbursement, or procurement event changes demand. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Saudi Arabia Ophthalmic Devices Market Size Compared Against Other Published Estimates

Published numbers for this market can look far apart because the boundaries around what counts as an ophthalmic device are not always consistent, and the year used as the starting point can shift the whole curve. Differences also come from how pricing is treated (list price versus realized price) and whether import timing is blended into the year of use or the year of purchase.

By checking procedure-linked demand drivers and refreshing price and replacement assumptions with local interviews, Mordor Intelligence keeps the Saudi Arabia total tied to device usage in eye clinics and hospital ophthalmology departments, instead of blending in adjacent optical retail value like spectacle lenses that is often counted differently.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 611.21 M (2026) | |

| Global Consultancy A | USD 515.30 M (2025) | Uses a different base year and applies a faster growth curve into the outlook, which can shift totals if replacement cycles and realized pricing are not re-validated for local procurement patterns. |

| Regional Consultancy B | USD 425.63 M (2024) | Anchors on an earlier base year and a study window that can understate near-term step-ups when hospital capacity additions and tender-driven purchases land unevenly across years. |

The table shows that timing choices and the way pricing and replacement are carried forward can explain much of the spread. Our approach stays repeatable because it is built from visible demand signals, then cross-checked with channel and buyer feedback before finalizing the yearly totals.

Key Questions Answered in the Report

What is the current value of the Saudi Arabia ophthalmic devices market?

The market is valued at USD 611.21 million in 2026 and is projected to rise to USD 794.18 million by 2031.

Which device category is expanding the fastest?

Diagnostic & Monitoring Devices are forecast to grow at a 7.42% CAGR between 2026 and 2031, driven by AI-enabled imaging adoption.

How significant is diabetic retinopathy in driving demand?

Diabetic retinopathy affects 31% of diabetics, spurring rapid uptake of AI-based screening and making it the fastest-growing disease segment at a 6.74% CAGR.

Why are Ambulatory Surgery Centers gaining traction?

ASCs benefit from cost efficiencies and Vision 2030’s privatization push, resulting in an expected 6.55% CAGR through 2031 for ophthalmic procedures.

What regulations influence import pricing?

SFDA registration, ISO 13485 compliance, and the SABER platform add to import costs, increasing prices by around 15% for high-end devices.

Where are premium elective surgeries concentrated?

Riyadh and Jeddah host most premium LASIK and cataract procedures, supported by centers such as Magrabi Health and new facilities like Alcon’s Experience Center.

Page last updated on: