Saudi Arabia Marketing And Advertising Agency Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

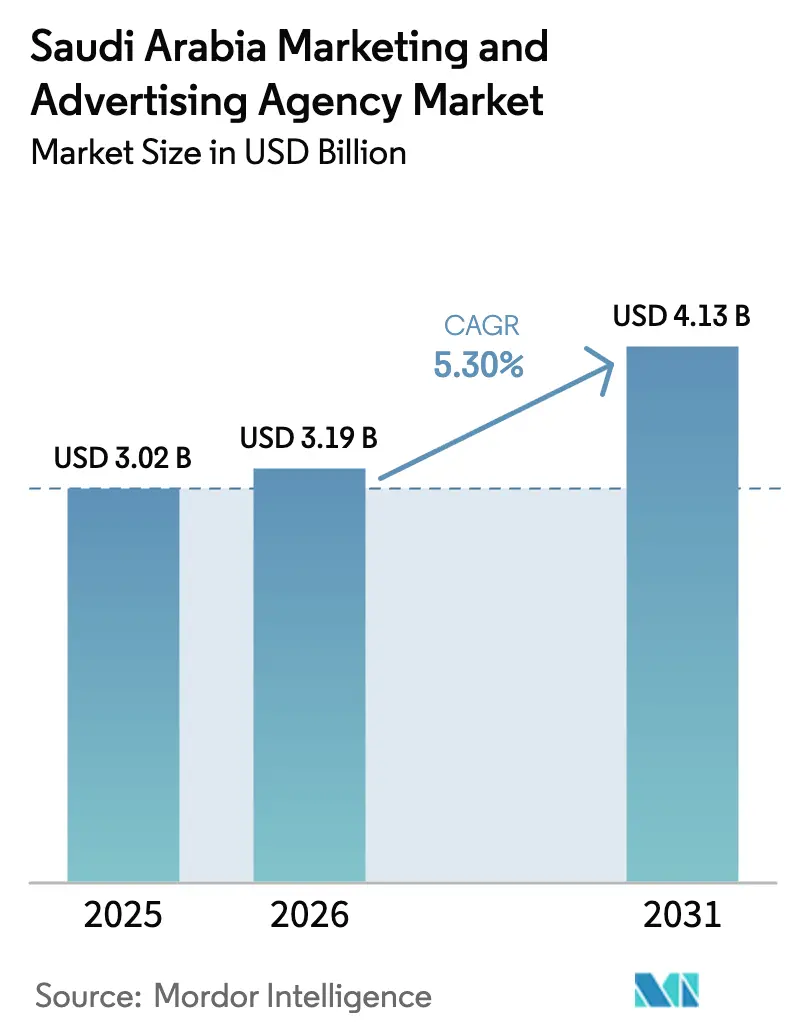

| Base Year Market Size (2025) | USD 3.02 Billion |

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 4.13 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Marketing And Advertising Agency Market Analysis by Mordor Intelligence

The Saudi Arabia marketing and advertising agency market size was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.19 billion in 2026 to reach USD 4.13 billion by 2031, at a CAGR of 5.3% during the forecast period (2026-2031). Vision 2030’s digital transformation agenda, rising e-commerce penetration, and an expanding pipeline of mega-events are driving agency retainers higher and broadening the scope of service requests. Budgets are migrating from broadcast and print to data-led, performance-oriented digital channels as marketers demand clear attribution, lifetime-value modeling, and real-time optimization. Regulatory mandates on influencer licensing and brand-safety compliance are increasing operating complexity, yet they also create competitive moats for agencies that invest in cultural-fit workflows and on-premise data infrastructure. Intensifying competition among global holding companies, consultancies, and home-grown boutiques drives consolidation in one tier and specialist spin-offs in another, reshaping the strategic playbook for both price and capability differentiation.

Key Report Takeaways

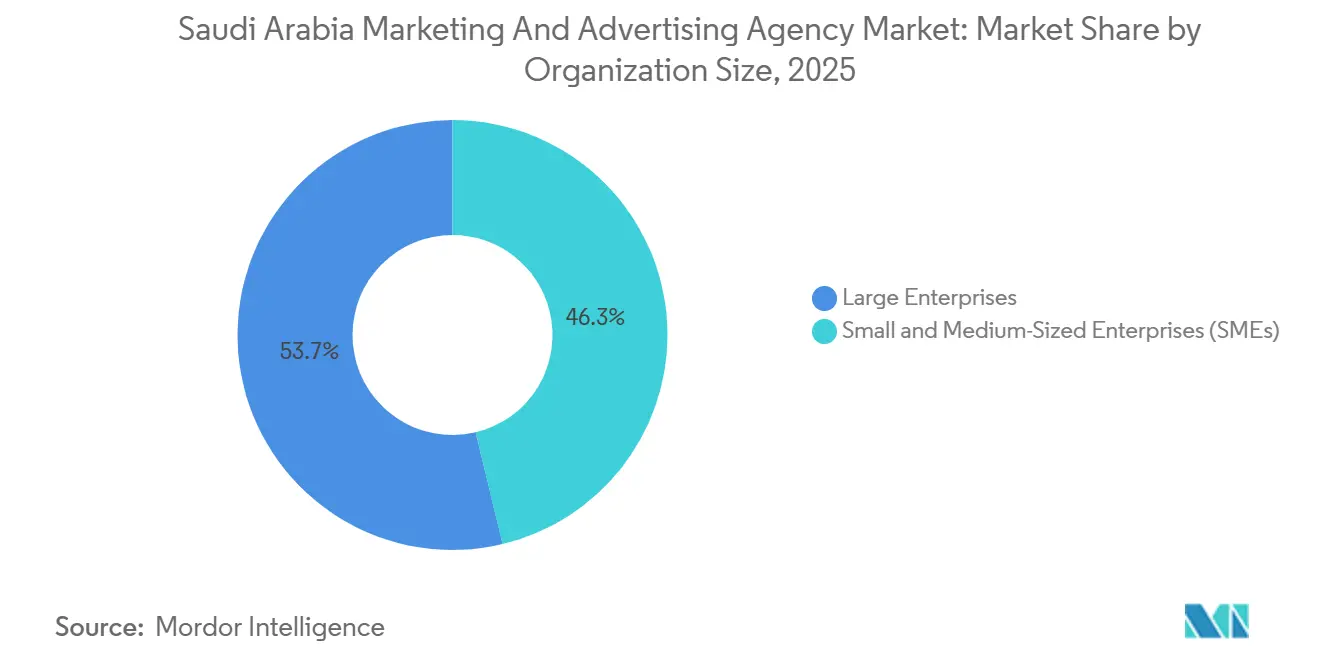

- By organization size, large enterprises led with 53.74% of the Saudi Arabia marketing and advertising agency market share in 2025. Small and medium-sized enterprises are projected to post the fastest growth at a 5.61% CAGR to 2031, propelled by 154,640 new registrations in Q1 2025.

- By service type, digital advertising services accounted for 61.84% of revenue in 2025. Data-and-analytics-led services are expected to expand at a 5.95% CAGR through 2031 as clients prioritize measurement over creative awards.

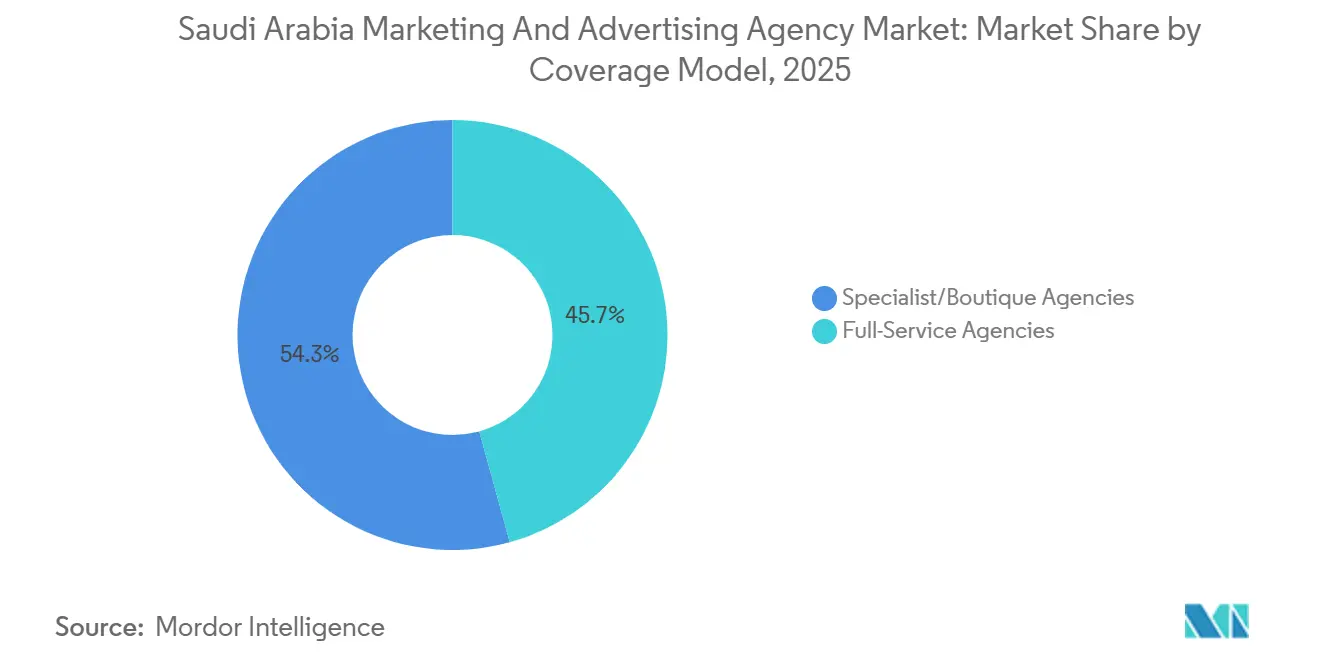

- By coverage model, full-service agencies captured 45.71% share in 2025, while specialist or boutique agencies are advancing at a 6.11% CAGR on the back of demand for programmatic buying and Arabic gaming-influencer expertise.

- By communication channel, social media led with a 40.66% allocation in 2025. Influencer and creator marketing is forecast to grow at a 6.36% CAGR through 2031 as brands seek authentic endorsements that bypass banner blindness.

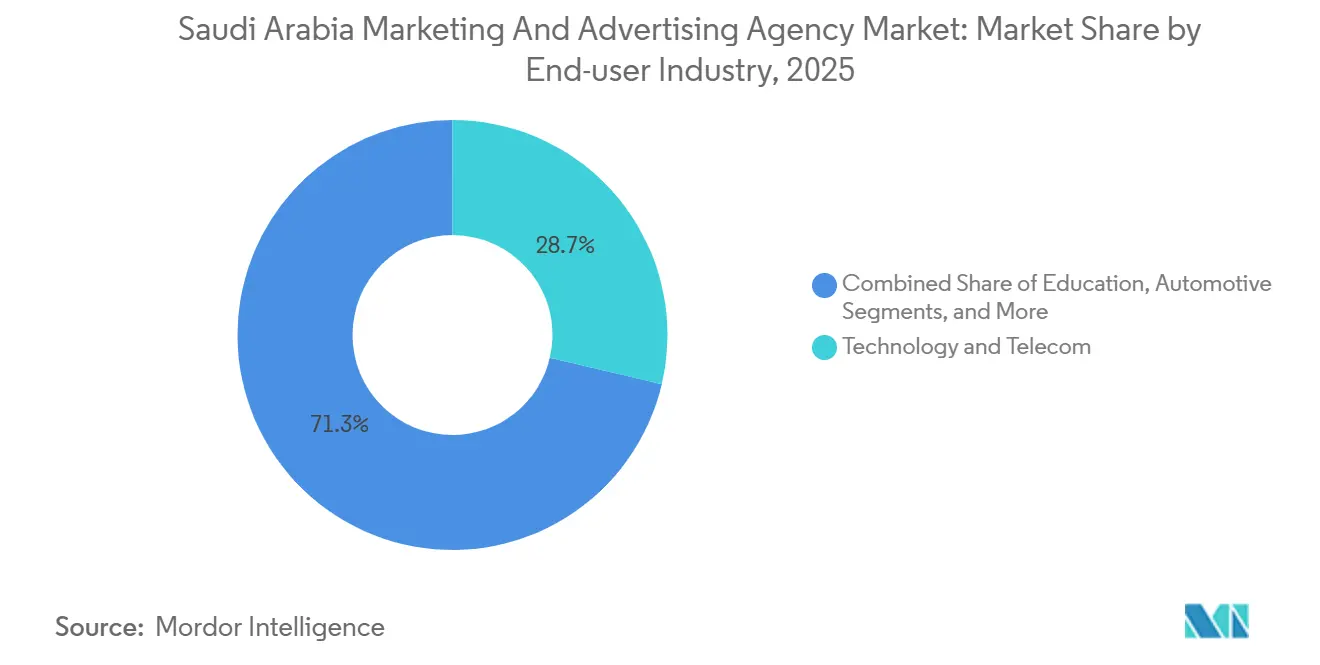

- By end-user industry, technology and telecom accounted for 28.67% of 2025 spend, yet retail and e-commerce is projected to record the highest 6.02% CAGR as online transactions accelerate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Marketing And Advertising Agency Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in digital-ad spend (Vision 2030 push) | +1.8% | National, with concentration in Riyadh and Eastern Province | Long term (≥ 4 years) |

| Accelerated e-commerce and fintech adoption | +1.2% | National, with early gains in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Growing SME sector outsourcing marketing | +0.9% | National, with spillover to smaller provinces | Medium term (2-4 years) |

| Entertainment and sports mega-events pipeline | +0.7% | Riyadh Province and NEOM region primarily | Short term (≤ 2 years) |

| Data-driven hyper-local targeting demand | +0.5% | Major urban centers with 5G coverage | Long term (≥ 4 years) |

| Uptick in Arabic gaming-influencer marketing | +0.4% | National, with youth demographic concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Digital-Advertising Spend Linked to Vision 2030

Government commitment to deliver 80% of services online by 2030 is redirecting public-sector budgets toward omnichannel citizen-awareness campaigns, while PIF portfolio companies such as stc, SEVEN, and Red Sea Global step up brand-building to hit revenue targets. stc alone has allocated SAR 6 billion in digital infrastructure investment for 2025-2027, much of which will be marketed through integrated social, broadcast, and influencer activations.[1]stc Group, “Investor Relations Annual Report 2024,” Stc.com.sa The convergence of sovereign ambition and corporate execution is lengthening contract durations and raising average retainer values for agencies capable of orchestrating multi-platform narratives. These structural tailwinds underpin the positive 1.4-point uplift to forecast CAGR.

Accelerated E-Commerce and Fintech Adoption

E-commerce payments via Mada cards climbed 25.82% year on year to SAR 197.42 billion (USD 52.6 billion) in 2024, lifting online retail’s share of total card spend from 23% to 29%. Fintech penetration followed suit as 261 licensed firms drove digital payments to 70% of all transactions. Buy-now-pay-later leaders Tabby and Tamara onboarded 15 million users by 2025 and redirected fresh capital into search, social, and affiliate bids that prize cost-per-acquisition efficiency over pure creativity.[2]Tabby, “Series D Funding Announcement,” Tabby.ai Agencies that staff data scientists alongside planners enjoy an early-mover edge, adding 1.2 points to market growth momentum.

Growing SME Sector Outsourcing Marketing

The Kingdom registered 154,640 new SMEs in Q1 2025, a 48% increase that indicates a rapidly expanding base of first-time buyers for outsourced marketing services. Vision 2030 aims to lift SME GDP contribution to 35% by decade's end, effectively doubling the addressable market for project-based digital campaigns and social-media management. Monshaat’s Kafalah program disbursed SAR 8.2 billion (USD 2.2 billion) in loan guarantees during 2024, part of which funds brand-building, search advertising, and influencer partnerships. The segment’s dynamism contributes a 0.9-point positive swing to forecast CAGR.

Entertainment and Sports Mega-events Pipeline

Saudi Arabia will host the 2034 FIFA World Cup, the annual Esports World Cup, and the Formula 1 Grand Prix, creating episodic spikes in demand for experiential and broadcast advertising. The 2024 Saudi Arabian Grand Prix alone attracted 2.5 million tourists and delivered SAR 900 million (USD 240 million) in direct spending, prompting automotive, hospitality, and luxury brands to commit multi-season sponsorships. Agencies with event-production and live-content capabilities are poised to capture an additional 0.8-point lift in long-term growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage in advanced mar-tech skills | -0.7% | Riyadh and Jeddah | Short term (≤ 2 years) |

| Brand-safety and cultural-fit compliance costs | -0.5% | National, stricter for foreign entities | Medium term (2-4 years) |

| Rising ad-fraud and viewability concerns | -0.3% | National, heavier in open-web programmatic | Short term (≤ 2 years) |

| Delayed payments from public-sector clients | -0.2% | National, episodic across ministries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage in Advanced Mar-tech Skills

A 20% gap in AI engineers, cloud architects, and data analysts in 2025 forced agencies to pay 30-50% wage premiums or source remote talent from Egypt and Jordan. Mega-projects such as Neom lure scarce specialists with elevated packages, squeezing agency margins on fixed-fee retainers. Although IBM and Waad training initiatives aim to certify 1.1 million Saudis in digital skills by 2026, immediate shortages detract 0.7 points from growth potential.

Brand-Safety and Cultural-Fit Compliance Costs

The General Commission for Audiovisual Media levies fines up to SAR 5 million (USD 1.3 million) for content that violates Islamic values, and each influencer marketing license now costs SAR 15,000 for three years.[3]General Commission for Audiovisual Media, “Influencer Licensing Guidelines 2025,” Gamr.sa Clearance delays compress creative development windows, while ad-verification fees add 5-8% to gross media spend. Compliance overhead drains agility and trims 0.5 points from forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Expand Opportunity Horizon

Small and medium-sized enterprises accounted for USD 1.4 billion of the Saudi Arabia marketing and advertising agency market size in 2025 and are projected to grow at a 5.61% CAGR between 2026 and 2031. Vision 2030’s target of 35% SME GDP contribution incentivizes entrepreneurs to outsource social-media management, search advertising, and micro-influencer campaigns rather than hire full-time marketing staff. The expanding Kafalah loan-guarantee scheme pumps working capital into marketing budgets, making SMEs a reliable pipeline for boutique agencies that offer modular, pay-as-you-go services.

Large enterprises maintained 53.74% of Saudi Arabia marketing and advertising agency market share in 2025, yet their growth pace lags at 4.9% CAGR because many already house in-house creative, production, and media functions. These corporates turn to agencies for specialist tasks such as programmatic bidding or market-mix modeling, sustaining revenue stability but limiting breakout expansion. Multi-year retainers, however, provide predictable cash flows and underpin higher average account values.

By Service Type: Analytics Drives Next Wave of Value

Digital advertising remained the revenue backbone with 61.84% share in 2025, but data-and-analytics-led services are projected to contribute an incremental USD 270 million to Saudi Arabia marketing and advertising agency market size by 2031. Marketers increasingly link budgets to measurable outcomes, prioritizing customer lifetime value and return on ad spend over legacy reach metrics.

Traditional broadcast, print, and radio are in secular decline as 5G and 97% smartphone penetration drive mobile-first content consumption. Integrated marketing solutions, which bundle creative, media, and analytics, appeal to mid-market clients that prize simplicity, yet growth will hinge on embedding AI layers that automate reporting and personalize creative assets in real time. Publicis Groupe’s EUR 300 million AI investment signals an acceleration of this pivot.

By Coverage Model: Specialists Take Share Through Niche Depth

Full-service networks held a 45.71% share in 2025 on the strength of long-standing global relationships, but specialist agencies are forecast to grow at a 6.11% CAGR to 2031 as clients cherry-pick best-of-breed expertise. Boutiques excel in Arabic content localization, gaming-influencer match-making, and programmatic bidding, areas where network agencies face process rigidity.

Networks are responding by spinning out agile sub-brands and acquiring niche players, a tactic underscored by the Omnicom-IPG merger that compressed the big four into three. The consolidation will likely trigger divestments of non-core units and open acquisition paths for boutiques looking to scale without legacy cost structures.

By Communication Channel: Influencers Capture Growth Premium

Social media accounted for 40.66% of budgets in 2025, yet influencer and creator marketing is poised to outpace every other channel at a 6.36% CAGR. Consumers spend an average of three hours six minutes per day on social platforms, and mega creators such as ShongxBong deliver click-through rates that dwarf banner norms.

Search and performance advertising benefits from the surge in online retail, while display and video see margin compression as programmatic auctions standardize inventory pricing. Out-of-home is modernizing through digital screens in Riyadh Metro and highway networks, creating data-rich placements that integrate with mobile retargeting. Broadcast retains a seasonal bump during Ramadan and major sports, yet linear viewership continues to migrate toward streaming.

By End-User Industry: Retail and E-commerce Takes the Growth Mantle

Technology and telecom accounted for 28.67% of 2025 billings, underpinned by stc Group’s USD 18.2 billion revenue base and heavy promotion of digital infrastructure. Retail and e-commerce, however, is poised for the fastest 6.02% CAGR to 2031 as online transactions rise and hypermarkets roll out omnichannel loyalty programs.

Fintech brands use aggressive cost-per-acquisition models that reward agencies able to blend search, affiliate, and influencer tactics. Automotive spending will receive a lift from electric-vehicle launches tied to Public Investment Fund manufacturing targets, though volumes remain modest against retail momentum. Healthcare and education remain highly regulated but hold latent upside as the youth-skewed demographic sustains demand for private clinics and vocational programs.

Geography Analysis

Riyadh, Jeddah, and Dammam together account for an estimated three-quarters of total spending, a concentration explained by headquarters clustering, higher disposable incomes, and superior fiber and 5G coverage. Riyadh houses most government ministries and PIF companies, ensuring a steady stream of public-sector campaigns and prompting global networks such as Monks to relocate regional hubs to the capital in 2024.

Jeddah’s role as the Red Sea gateway fuels tourism, hospitality, and retail advertising, especially during Hajj and Umrah seasons. Dammam anchors the Eastern Province’s petrochemical and logistics sectors, creating industrial B2B marketing opportunities that often flow through specialist agencies with sector knowledge. Tier-2 cities such as Khobar, Taif, and Abha gain incremental spend as nationwide 5G penetration surpasses 78% and enables hyper-local targeting even in secondary markets.

Vision 2030 giga-projects, Qiddiya, and Red Sea Global-are establishing entirely new demand nodes outside legacy corridors. Massive construction footprints require sustained recruitment advertising, destination branding, and foreign-investor outreach. The Visit Saudi campaign aims for 150 million tourists by 2030, a target that drives global media buys, multilingual influencer partnerships, and immersive storytelling designed to translate curiosity into arrivals.

Cross-border integration remains limited. Saudi content guidelines are stricter than those in neighboring UAE and Bahrain, forcing agencies to maintain country-specific compliance modules rather than pan-GCC templates. Nonetheless, Riyadh-based shops occasionally pitch regional mandates when cultural insight and Arabic localization outweigh footprint considerations.

Competitive Landscape

No single agency controls more than 15% of total billings, yielding a moderately fragmented competitive field. WPP, Publicis Groupe, Omnicom-Dentsu, and Havas operate through sub-brands that blend global process with local execution, but their centralized approval layers can delay campaign iteration. The Omnicom-IPG merger intensifies bid competition, encourages AI-enabled automation, and may trigger further M&A as networks off-load non-core assets.

Home-grown players such as Extend Advertising, UBRAND, HyperThink, and Anamel differentiate on Arabic copywriting, local influencer rosters, and rapid compliance sign-off, winning briefs where cultural nuance trumps scale. Consultancies like Accenture Interactive and Publicis Sapient compete on data-science firepower, pitching marketing-mix modeling and CDP integration rather than storyboard originality.

Strategic investments underscore the arms race. Publicis Groupe earmarked EUR 300 million for an AI layer covering media planning, creative versioning, and reporting, while Havas committed EUR 400 million to natural-language processing for Arabic content and computer vision for brand safety. Local investment firm Ignite set aside USD 1.1 billion to build a regional digital-advertising champion via acquisition, a signal that private capital sees value in stitching together fragmented specialists.

Saudi Arabia Marketing And Advertising Agency Industry Leaders

WPP plc

Publicis Groupe SA

Omnicom Group Inc.

The Interpublic Group of Companies, Inc.

Dentsu Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dentsu rolled out a Saudi-hosted clean-room solution that enables privacy-compliant audience activation under the Personal Data Protection Law. The service targets retail and fintech clients seeking first-party data enrichment.

- December 2025: Ignite completed its first acquisition, buying a 55% stake in UBRAND for an undisclosed sum to accelerate programmatic and content-studio scale.

- November 2025: Publicis Groupe activated its AI media-planning layer across seven Saudi accounts, reducing campaign setup time by 40% according to internal benchmarks.

- September 2025: Monks opened a 50-seat content studio in Riyadh, doubling down on vertical short-form video for TikTok and Snapchat after securing a three-year retainer with Noon.

Saudi Arabia Marketing And Advertising Agency Market Report Scope

The Saudi Arabia marketing and advertising agency market is defined based on the revenues generated by marketing and advertising agencies operational in the KSA. The analysis is based on market insights derived from secondary and primary research. The market also covers the major factors impacting its growth, including drivers and restraints.

The Saudi Arabia Marketing and Advertising Agency Market Report is Segmented by Organization Size (Small and Medium-Sized Enterprises and Large Enterprises), Service Type (Digital Advertising Services, Traditional Advertising Services, Integrated Marketing Solutions, and Data-and-Analytics-Led Services), Coverage Model (Full-Service Agencies and Specialist or Boutique Agencies), Communication Channel (Social Media, Search and Performance, Display and Video, Out-of-Home, Broadcast TV and Radio, Influencer and Creator Marketing, and Experiential or Events), End-User Industry (Technology and Telecom, Healthcare, Consumer Goods, Financial Services, Education, Retail and E-commerce, Manufacturing, Media and Entertainment, Government, Automotive, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises |

| Digital Advertising Services |

| Traditional Advertising Services |

| Integrated Marketing Solutions |

| Data- and-Analytics-Led Services |

| Full-Service Agencies |

| Specialist / Boutique Agencies |

| Social Media |

| Search and Performance |

| Display and Video |

| Out-of-Home (OOH) |

| Broadcast TV and Radio |

| Influencer and Creator Marketing |

| Experiential / Events |

| Technology and Telecom |

| Healthcare |

| Consumer Goods |

| Financial Services |

| Education |

| Retail and E-commerce |

| Manufacturing |

| Media and Entertainment |

| Government |

| Automotive |

| Other End-User Industries |

| By Organization Size | Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises | |

| By Service Type | Digital Advertising Services |

| Traditional Advertising Services | |

| Integrated Marketing Solutions | |

| Data- and-Analytics-Led Services | |

| By Coverage Model | Full-Service Agencies |

| Specialist / Boutique Agencies | |

| By Communication Channel | Social Media |

| Search and Performance | |

| Display and Video | |

| Out-of-Home (OOH) | |

| Broadcast TV and Radio | |

| Influencer and Creator Marketing | |

| Experiential / Events | |

| By End-User Industry | Technology and Telecom |

| Healthcare | |

| Consumer Goods | |

| Financial Services | |

| Education | |

| Retail and E-commerce | |

| Manufacturing | |

| Media and Entertainment | |

| Government | |

| Automotive | |

| Other End-User Industries |

Key Questions Answered in the Report

How large will agency spending in Saudi Arabia be by 2031?

The Saudi Arabia marketing and advertising agency market is forecast to reach USD 4.13 billion by 2031, expanding at a 5.3% CAGR from 2026.

Which client segment shows the fastest budget growth?

Small and medium-sized enterprises, boosted by Vision 2030 incentives and new business formation, are projected to grow agency spending at 5.61% CAGR to 2031.

What service line is gaining the most traction with Saudi brands?

Data-and-analytics-led services are the fastest climber, supported by marketers’ shift toward measurable ROI and expected to post a 5.95% CAGR.

How will mega-events influence ad budgets?

The 2034 FIFA World Cup and annual Esports World Cup will create episodic surges in experiential, broadcast, and influencer spending, lifting long-term demand for event-ready agencies.

What is the main operational challenge for agencies today?

Talent shortages in AI engineering and advanced mar-tech skills are inflating salaries and limiting near-term scale, trimming 0.7 percentage points from growth forecasts.

Are compliance requirements affecting campaign timelines?

Yes, brand-safety checks and influencer licensing under GAMR rules add both cost and time, particularly for foreign creators, and agencies must build specialized workflows to stay on schedule.

Page last updated on: