Middle East Marketing And Advertising Agency Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

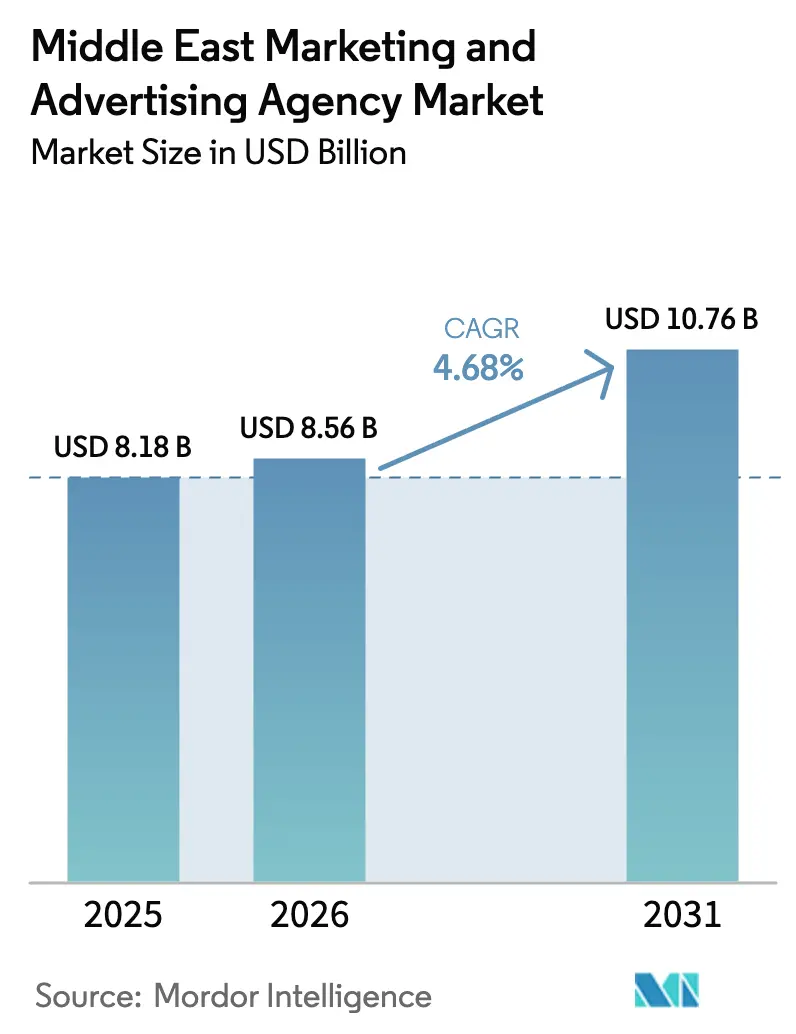

| Base Year Market Size (2025) | USD 8.18 Billion |

| Market Size (2026) | USD 8.56 Billion |

| Market Size (2031) | USD 10.76 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Marketing And Advertising Agency Market Analysis by Mordor Intelligence

The Middle East Marketing and Advertising Agency Market size was valued at USD 8.18 billion in 2025 and is estimated to grow from USD 8.56 billion in 2026 to reach USD 10.76 billion by 2031, at a CAGR of 4.68% during the forecast period (2026-2031). Robust government diversification agendas, headlined by Saudi Vision 2030 and UAE Vision 2030, are steering budgets away from hydrocarbons and toward tourism, fintech, gaming, and cultural mega-projects. Surging mobile and social-media adoption, now exceeding 95% household penetration across the Gulf, is shifting spend toward performance-based digital formats and influencer marketing. Agencies that overlay data science onto Arabic-language creative are capitalizing on this pivot, while full-service retainers are being unbundled in favor of niche mandates spanning programmatic buying, crisis communications, and content localization. Growing in-house capabilities at multinationals are compressing margins for commoditized media services, propelling agencies to differentiate through technology integration and regulatory fluency.

Key Report Takeaways

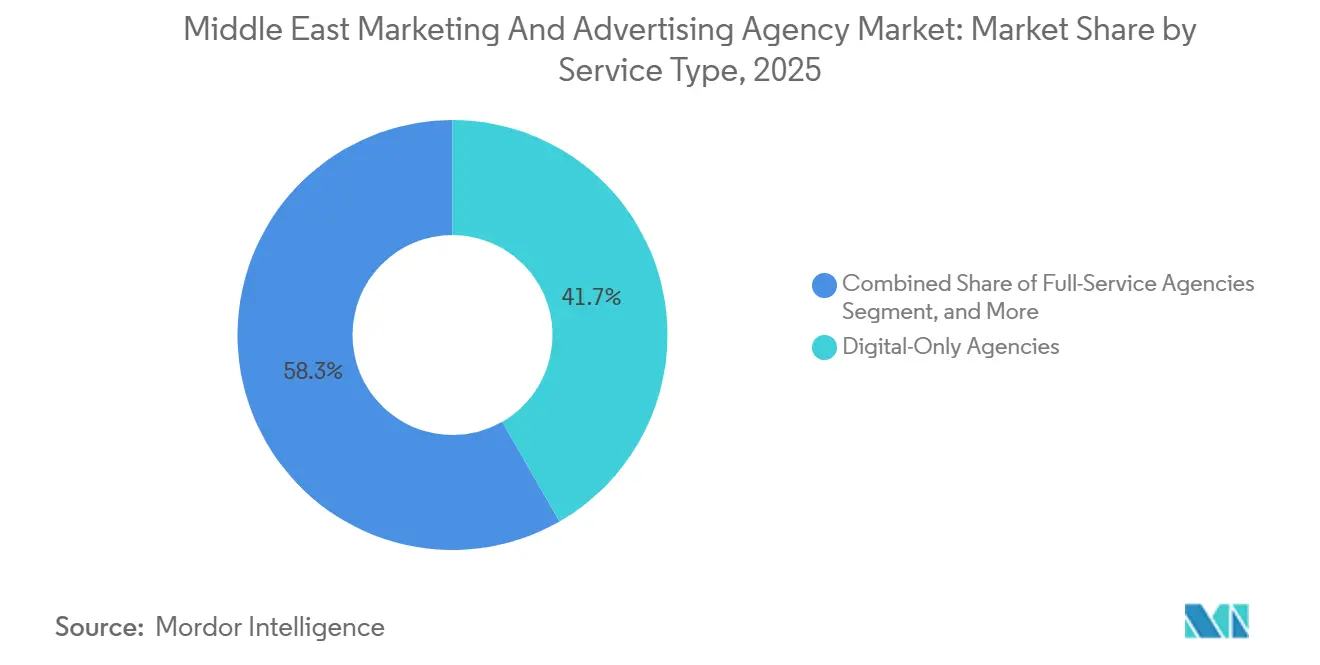

- By service type, digital-only specialists led with 41.72% of Middle East marketing and advertising agency market share in 2025, while public-relations and reputation management is set to advance at a 5.93% CAGR to 2031.

- By organization size, large enterprises accounted for 58.63% share of the Middle East marketing and advertising agency market size in 2025, whereas the SME segment is projected to expand at 5.12% CAGR to 2031.

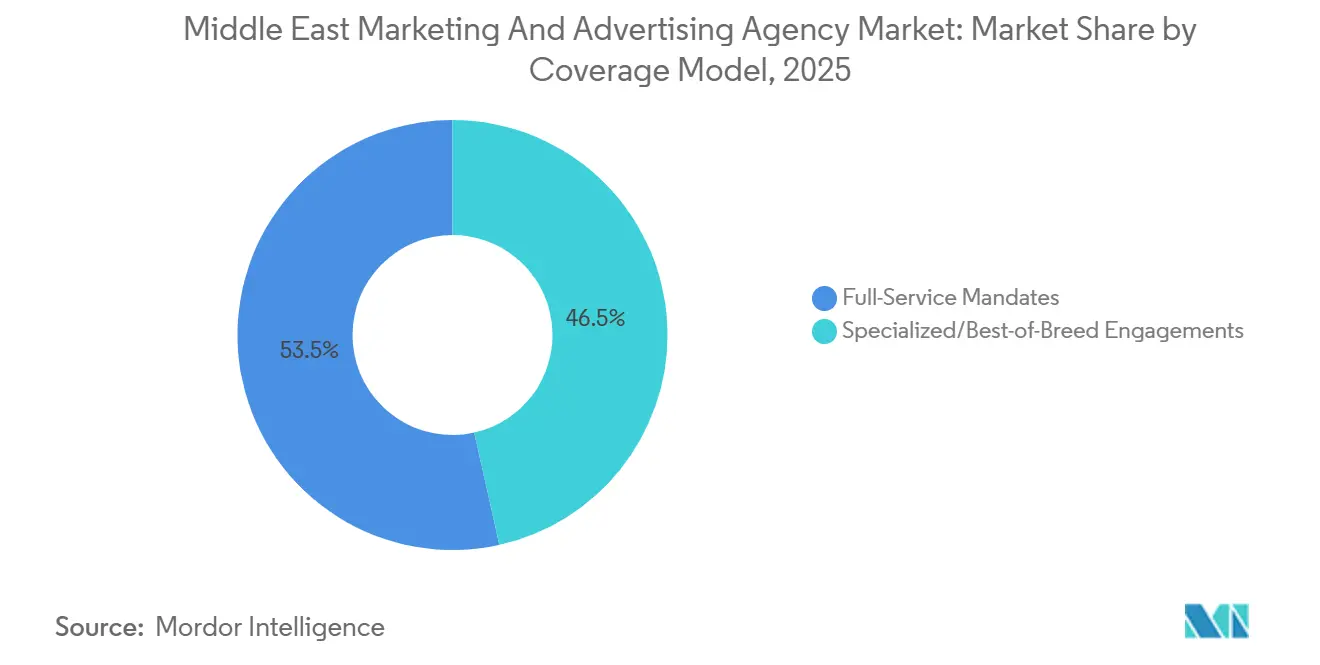

- By coverage model, specialized or best-of-breed mandates captured 46.51% share of the Middle East marketing and advertising agency market size in 2025 and are climbing at 5.82% CAGR through 2031.

- By end-user sector, private enterprises generated 62.38% of 2025 revenue, but public and institutional clients exhibit the strongest outlook at a 5.92% CAGR to 2031.

- By country, Saudi Arabia commanded 36.63% of 2025 revenue, while Qatar is forecast to post the fastest 5.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Marketing And Advertising Agency Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital-Ad Spend Among GCC Corporates | +1.2% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Government Diversification, Saudi and UAE Visions 2030 | +1.5% | Saudi Arabia, UAE, Bahrain, Oman | Long term (≥ 4 years) |

| Social-Media and Mobile Penetration Surge | +0.9% | GCC-wide, strongest in UAE and Saudi Arabia | Short term (≤ 2 years) |

| E-Commerce Performance-Marketing Boom | +1.0% | Saudi Arabia, UAE, Kuwait, Qatar | Medium term (2-4 years) |

| Esports and Gaming Sponsorship Uptake | +0.7% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Mega-Events Tourism, Neom, Expo 2030 | +0.8% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Diversification, Saudi and UAE Visions 2030

Massive public-sector investment is transforming ministries and sovereign funds into prolific advertisers. Saudi Arabia’s USD 38 billion gaming program and the USD 500 billion Neom project each require multi-year, multi-channel campaigns that few agencies can execute at scale.[1]Public Investment Fund, “Gaming and Esports Strategy,” pif.gov.sa Parallel UAE bets on fintech, renewables, and space exploration broaden the brief beyond consumer work toward B2B positioning. Compliance with strict cultural guidelines adds execution complexity that favors shops staffed by bilingual strategists and regulatory experts. These mandates deliver high-value retainers, anchoring predictable revenue even as private-sector billing turns project-based.

Rising Digital-Ad Spend Among GCC Corporates

Corporate treasuries are reallocating budgets from print and outdoor to performance-driven social and programmatic formats. Year-over-year in-app purchase revenue jumped 20% in 2025, proving the conversion upside of mobile-first outreach. Agencies with martech stacks that fuse sentiment analysis and automated creative optimization secure preferred-supplier status. Conversely, creative boutiques lacking data engineers struggle to defend pricing. The shift is accelerating consolidation among digital specialists that can bundle analytics, content, and media in one sprint-style workflow.

Social-Media and Mobile Penetration Surge

Smartphones serve as the dominant commerce gateway, flattening the path from discovery to checkout on TikTok and Instagram. Saudi Arabia’s 48% female gamer cohort highlights the depth of high-engagement micro-segments now reachable through influencers rather than celebrity endorsements. Brands are crowdsourcing creative concepts in real time, forcing agencies to manage always-on creator communities instead of periodic TV bursts. Those without proprietary influencer-management tools face bypass risk as advertisers contract creators directly through platform marketplaces.

E-Commerce Performance-Marketing Boom

Regional e-commerce scaled to USD 50 billion in 2025, creating a fertile ground for cost-per-acquisition billing. Direct-to-consumer labels, operating on slim net margins, only fund campaigns that link ads to cart checkouts. This reality is pushing agencies to embed conversion-rate-optimization specialists and integrate with client CRM stacks. Creative storytelling remains valuable, but only when mapped to attributable funnel milestones, prompting a fusion of art direction and data engineering inside account teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SME Budget Constraints | -0.6% | GCC-wide, acute in Kuwait, Bahrain, Oman | Short term (≤ 2 years) |

| In-Housing of Marketing Functions | -0.9% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Bilingual Data-Driven-Creative Talent Gap | -0.5% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Strict Cultural-Content Regulations | -0.4% | Saudi Arabia, UAE, Kuwait, Bahrain, Oman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

In-Housing of Marketing Functions

Two-thirds of multinationals now operate internal agencies, erasing lucrative media-planning fees that once cross-subsidized creative development.[2]World Federation of Advertisers, “In-Housing Survey 2025,” wfanet.org Cost savings and faster turnaround motivate the shift, with many corporations piloting three-person programmatic desks that handle 20-country portfolios. Agencies are repositioning toward harder-to-replicate services such as Arabic localization and crisis communications, yet the revenue gap from surrendered media billings remains material. This squeeze is catalyzing M&A as holding companies acquire tech consultancies to regain boardroom relevance.

SME Budget Constraints

Although small and medium businesses comprise more than 90% of registered Gulf companies, inflation and high interest burdens limit their discretionary spend. The segment gravitates to self-serve dashboards from Meta and Google, leaving agencies to compete on razor-thin project scopes. Elevated churn raises client-acquisition costs, undermining profitability unless workflow automation offsets low average revenue per account. Consequently, many agencies prioritize a barbell portfolio of large enterprises and sovereign projects, accepting limited SME exposure despite the headline population of accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Specialists Dominate, PR Surges

Digital-only agencies held 41.72% of 2025 revenue, reflecting the demand for measurable conversion paths across search, social, and programmatic display. That share underscores how the Middle East marketing and advertising agency market rewards data-rich execution over traditional reach metrics. Public-relations and reputation management will post the quickest 5.93% CAGR as Gulf governments and corporates seek narrative steering amid geopolitical scrutiny. AI-driven sentiment analysis now anchors campaign war rooms, a discipline that smaller creative boutiques cannot easily replicate. Media-buying desks leverage automated bidding to lower effective CPMs, while bilingual copywriting remains a scarce craft.

Specialists are embedding tech platforms to defend margins. Seventy-seven percent of regional PR executives reported daily AI usage in 2025, enabling near-real-time issue mapping. Creative shops win mandates when they fuse cultural nuance with shoppable ad units, ensuring each execution feeds the attribution models underpinning performance contracts. Meanwhile, full-service networks are buying or incubating niche outfits to plug capability gaps, though integration lag often delays client-visible impact.

By Organization Size: Enterprises Lead, SMEs Accelerate

Large enterprises generated 58.63% of 2025 billings, supplying the account stability that lets agencies invest in proprietary tools. Those accounts also demand omnichannel orchestration and 24-hour multilingual support, heightening staffing and platform costs for providers. Nevertheless, SME clients will expand at a brisk 5.12% CAGR, buoyed by the falling cost of cloud commerce suites and social-media ad inventory. Their value to the Middle East marketing and advertising agency market rests on volume rather than ticket size, pushing agencies to automate briefing, creative versioning, and reporting.

Enterprises’ pivot to in-house media buying is shrinking the work scope that agencies historically controlled. To offset, shops bundle analytics dashboards, CRM integrations, and localized copy into outcome-based statements of work. SMEs favor modular retainers or project bursts, frequently benchmarking agency pricing against do-it-yourself ad platforms. Thus, profitability depends on segment-specific operating models rather than uniform resource allocation.

By Coverage Model: Specialized Mandates Gain Traction

Specialized or best-of-breed engagements captured 46.51% of 2025 spend and are climbing at a 5.82% CAGR, evidencing client appetite for pick-and-choose partner ecosystems. Brands now unbundle creative ideation, media trades, and analytics to minimize overhead and tap deep expertise. The Middle East marketing and advertising agency market size attributable to full-service retainers is consequently flattening, pushing network agencies to spin up micro-units focused on programmatic, esports, or Arabic voice search.

Performance-tied contracts amplify this shift. Niche players that can connect ad impressions to bottom-line sales win procurement contests because risk is shared. Others lean on regulatory mastery, navigating alcohol, modesty, and religious-image restrictions that can derail regional rollouts. Best-of-breed players also ride on SaaS subscription income from proprietary dashboards, improving revenue visibility beyond classic fee billing.

By End-User Sector: Private Dominates, Public Accelerates

Private enterprises contributed 62.38% of revenue in 2025, led by retail, telecom, finance, and direct-to-consumer categories. Public and institutional clients show the fastest 5.92% CAGR as sovereign funds market mega-projects such as Neom and Saudi gaming initiatives. Campaigns must pass cultural-content screens enforced by Saudi and UAE regulators,[3]UAE National Media Council, “Advertising Content Guidelines,” nmc.gov.ae giving an edge to agencies with bilingual compliance officers.

Private clients continue to compress fees, enforcing cost-per-acquisition or return-on-ad-spend clauses. Agencies respond with dashboards that map creative lift to cart value, safeguarding margins through demonstrable impact. Public entities, while budget-richer, impose longer approval cycles and stricter content audits. Winning shops balance the agility prized by consumer brands with the procedural rigor expected by ministries and investment authorities.

Segment Analysis: By Coverage

Saudi Arabia retained 36.63% share of 2025 billings, with Riyadh anchoring sovereign campaigns tied to entertainment, tourism, and fintech diversification. Mega-projects such as Neom and the Red Sea Development require persistent cross-border media buys and Arabic localization, ensuring multi-year revenue visibility. Jeddah complements this with private-sector assignments centered on its port and aviation hubs, while Dammam supplies petrochemical briefs that often span Saudi-Bahraini borders.

The United Arab Emirates acts as the service hub for multinational mandates across the wider Middle East and North Africa. Dubai Media City’s licensing flexibility and 100% foreign ownership privileges encourage agency startups and global network satellites alike. Abu Dhabi’s sovereign funds finance advanced industry campaigns in space, renewable energy, and biotech, each demanding B2B storytelling that projects regional innovation leadership. Compliance with National Media Council content codes necessitates in-house Arabic copywriters versed in dialect nuances.

Qatar will expand at a 5.83% CAGR through 2031, riding a tourism uplift that keeps World-Cup-era hotels, metros, and airports at peak utilization. High-profile events, from the AFC Asian Cup to the Formula 1 Grand Prix, create recurring sponsorship inventory. Although Kuwait, Bahrain, and Oman together account for under one-fifth of regional spend, each offers specialization niches, Kuwait’s e-government rollouts, Bahrain’s finance branding, and Oman’s culture-led destination work. Agencies able to scale talent fluidly across these micro-markets capture incremental revenue without fixed-cost drag.

Competitive Landscape

Top Companies in Middle East Marketing and Advertising Agency Market

No single agency controls more than a low-double-digit percentage of regional billings, keeping the Middle East marketing and advertising agency market structurally fragmented. Global holding groups such as WPP, Publicis, Omnicom, and Dentsu maintain Gulf hubs that manage multinational accounts, whereas independents like FP7 McCann, Memac Ogilvy, and TBWA\RAAD carve out market share through cultural fluency and price agility. Strategy consultancies, notably Accenture Song and Deloitte Digital, challenge incumbents by bundling tech transformation with creative services, a proposition resonating with C-suite buyers.

In-housing compounds fragmentation. As 66% of multinationals now self-manage media buying, agencies respond by doubling down on services that resist commoditization: Arabic localization, real-time crisis counsel, and influencer network curation. Talent scarcity, especially bilingual data-literate creatives, inflates salaries and sparks acquisition races for boutique shops owning such capabilities. Several networks launched academies in 2026 to pipeline junior Arabic copywriters, though time-to-productivity remains a headwind.

Commercial models are also shifting. Outcome-based retainers, still a minority of contracts, are favored by digitally native advertisers seeking cost certainty. Agencies willing to underwrite performance gain wallet share yet juggle higher financial risk. Meanwhile, regional award shows, including a record 32 Lions won at Cannes 2025, act as visibility multipliers for creative boutiques, helping them court multinational RFPs despite lean headcounts.

Middle East Marketing And Advertising Agency Industry Leaders

WPP plc

Publicis Groupe SA

Omnicom Group Inc.

Accenture Song

Dentsu Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Riyadh unveiled the Esports World Cup prize pool exceeding SAR 262 million (USD 70 million), creating major sponsorship inventory for agencies positioned in gaming activation.

- September 2025: Kijamii rebranded around an AI-driven influencer-matching engine, signaling maturation of social-commerce enablement tools.

- August 2025: Agencies from the Middle East and North Africa secured 32 Lions at Cannes, spotlighting regional creative competitiveness.

- July 2025: OMD completed a global refresh under “We Create What’s Next,” integrating AI optimization across its Gulf media desks.

Middle East Marketing And Advertising Agency Market Report Scope

Advertising agencies are specialized in the field of communication, including advertising and indirect marketing. In order to assist with the development of a marketing strategy, marketing agents offer a broader and consultative approach. Depending on their own resources, some of them also make recommendations for marketing techniques and offer communication services.

The Middle East Marketing and Advertising Agency Market Report is Segmented by Service Type (Full-Service Agencies, Digital-Only Agencies, Media Buying and Planning, Creative and Branding Boutiques, PR and Reputation Management), Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), Coverage Model (Full-Service Mandates, Specialized Engagements), End-User Sector (Public and Institutional, Private Enterprises), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

| Full-Service Agencies |

| Digital-Only Agencies |

| Media Buying and Planning |

| Creative and Branding Boutiques |

| PR and Reputation Management |

| Small and Medium-Sized Enterprises (?250 Employees) |

| Large Enterprises (>250 Employees) |

| Full-Service Mandates |

| Specialized/Best-of-Breed Engagements |

| Public and Institutional |

| Private Enterprises |

| Saudi Arabia | Riyadh |

| Jeddah | |

| Dammam | |

| United Arab Emirates | Dubai |

| Abu Dhabi | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Rest of Middle East |

| By Service Type | Full-Service Agencies | |

| Digital-Only Agencies | ||

| Media Buying and Planning | ||

| Creative and Branding Boutiques | ||

| PR and Reputation Management | ||

| By Organization Size | Small and Medium-Sized Enterprises (?250 Employees) | |

| Large Enterprises (>250 Employees) | ||

| By Coverage Model | Full-Service Mandates | |

| Specialized/Best-of-Breed Engagements | ||

| By End-User Sector | Public and Institutional | |

| Private Enterprises | ||

| By Country | Saudi Arabia | Riyadh |

| Jeddah | ||

| Dammam | ||

| United Arab Emirates | Dubai | |

| Abu Dhabi | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Oman | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the 2026 value of the Middle East marketing and advertising agency market?

It stands at USD 8.56 billion, on track to reach USD 10.76 billion by 2031.

Which service type is growing fastest in Gulf agency spend?

Public-relations and reputation management leads with a 5.93% CAGR through 2031.

Why is Qatar the quickest-growing geography?

Post-World-Cup infrastructure and year-round tourism pushes are driving a projected 5.83% CAGR to 2031.

How are agencies responding to in-housing by multinationals?

They are pivoting toward specialized offerings such as Arabic localization, crisis counsel, and performance-tied contracts.

What segment commands the largest share of 2025 revenue?

Digital-only specialists lead with 41.72% of market share.

Which restraint has the greatest negative CAGR impact?

The in-housing of marketing functions, reducing forecast growth by 0.9%.

Page last updated on: