Europe Cloud CRM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.49 Billion |

| Market Size (2026) | USD 14.23 Billion |

| Market Size (2031) | USD 18.36 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

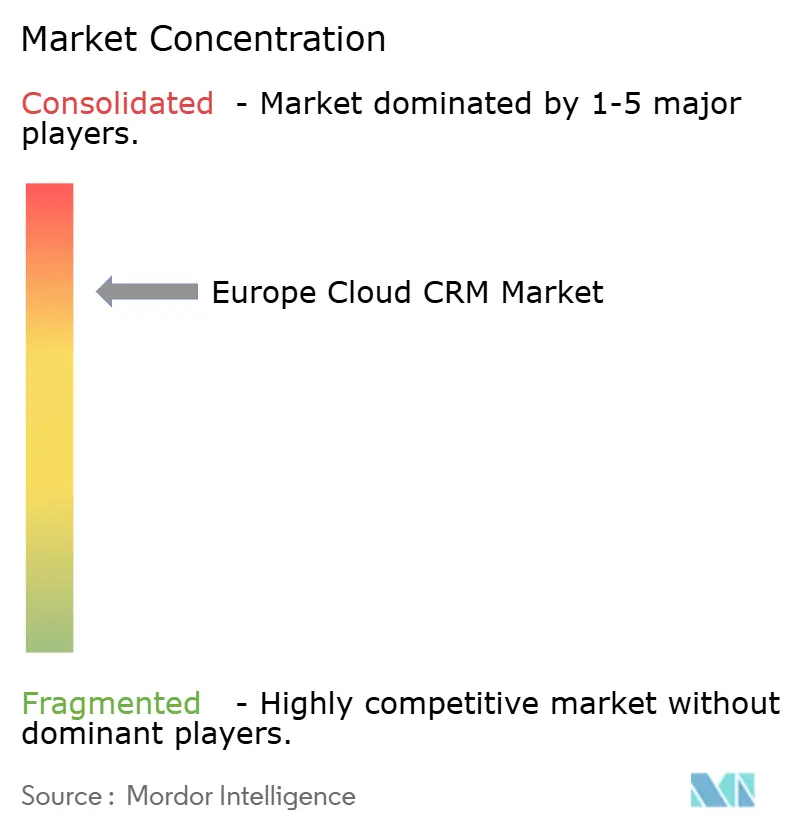

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cloud CRM Market Analysis by Mordor Intelligence

The Europe Cloud CRM Market size is expected to grow from USD 13.49 billion in 2025 to USD 14.23 billion in 2026 and is forecast to reach USD 18.36 billion by 2031 at 5.23% CAGR over 2026-2031.

A switch from on-premises tools to cloud-native platforms, sovereign-AI infrastructure rollouts, and SME voucher schemes are steering steady mid-single-digit expansion. Public cloud continues to dominate initial deployments, but hybrid models gain ground as financial-services and healthcare firms retain sensitive records on-premises. Spain’s voucher-led surge, agentic AI that trims sales-cycle time, and looming portability mandates further recalibrate competitive tactics across the Europe cloud CRM market. Vendors now differentiate on language support, privacy guarantees, and integration breadth rather than database scale alone.

Key Report Takeaways

- By deployment type, public cloud held 69.17% revenue share in 2025 while hybrid cloud is on track to post a 6.80% CAGR through 2031.

- By enterprise size, large enterprises accounted for 57.06% of the Europe cloud CRM market share in 2025, whereas SMEs are expanding at a 6.10% CAGR to 2031.

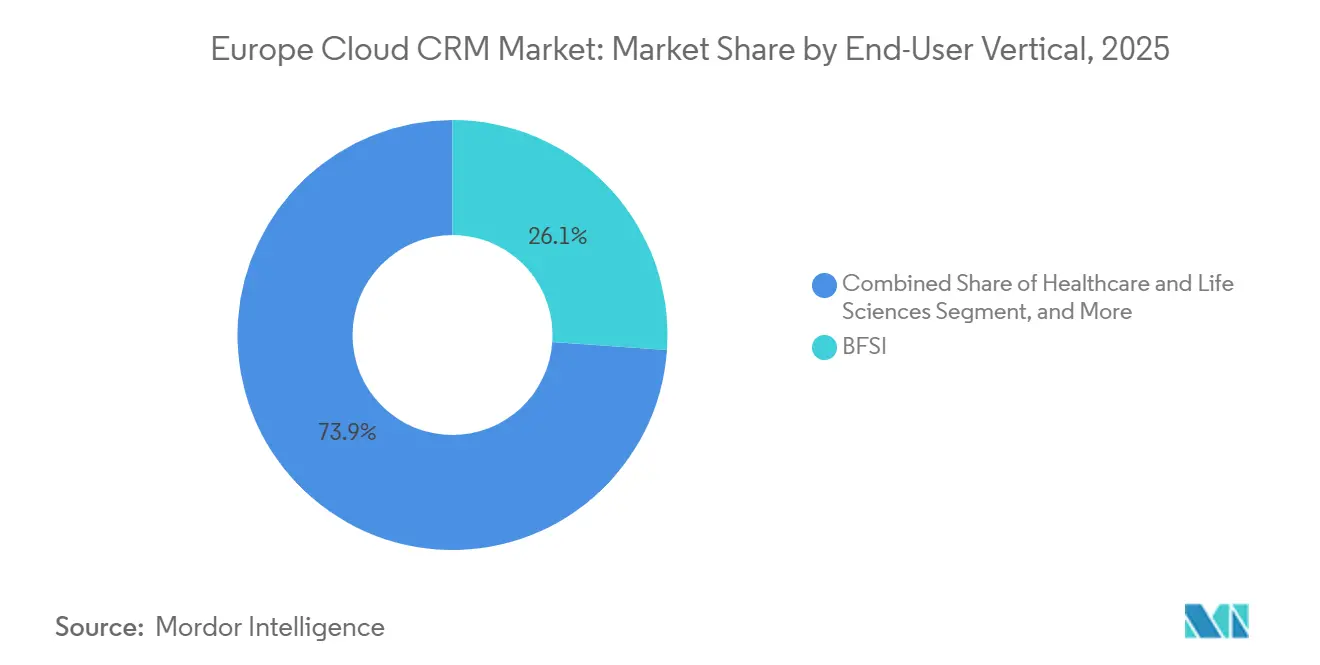

- By end-user vertical, banking and financial services captured 26.11% share in 2025, while healthcare and life sciences is forecast to record the fastest growth at a 5.95% CAGR.

- By geography, the United Kingdom led with 23.91% revenue share in 2025; Spain is forecast to log a 6.60% CAGR across the same horizon.

- By CRM function, sales automation contributed 41.24% revenue in 2025, yet marketing automation is projected to accelerate at a 6.23% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Cloud CRM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital Transformation Across European Enterprises | +1.20% | Global, with concentration in Germany, France, United Kingdom | Medium term (2-4 years) |

| Rising Demand for Omnichannel Customer Engagement | +0.90% | Global, led by retail and BFSI sectors | Short term (≤ 2 years) |

| Cost-Efficiency and Scalability of Public Cloud Deployments | +0.80% | Global, particularly SME-heavy markets in Spain, Italy | Medium term (2-4 years) |

| Emergence of Sovereign-AI Compute for Compliant CRM AI Features | +0.60% | EU core (Germany, France, Netherlands), spillover to Nordics | Long term (≥ 4 years) |

| SME Voucher and Tax-Credit Schemes Fueling Cloud Uptake | +0.50% | Spain, Germany, France, Greece, Ireland | Medium term (2-4 years) |

| Adoption of Agentic AI Assistants Automating CRM Workflows | +0.70% | Global, early traction in IT, telecom, professional services | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital Transformation Across European Enterprises

Stimulus programs and post-pandemic work models have embedded remote selling, making legacy Siebel or SAP on-premises deployments costly and inflexible. Germany’s Digital Jetzt grants of EUR 50,000-100,000 (USD 55,000-110,000) per applicant cover software and consulting, nudging manufacturers toward hybrid cloud.[1]KfW, “Digital Jetzt Funding Programme,” kfw.de The European Commission’s Digital Decade agenda targets 75% enterprise cloud uptake by 2030, sharpening compliance pressure on lagging sectors. SAP will sunset ECC 6.0 support in 2027, forcing more than 20,000 European clients to re-platform and often reassess incumbent CRM modules.[2]SAP SE, “S/4HANA Cloud,” sap.com Banks simultaneously embed CRM analytics into Basel III liquidity models, elevating customer-engagement data to a regulatory asset. Together, these forces sustain momentum across the European cloud CRM market, even as macro headwinds moderate overall IT budgets.

Rising Demand for Omnichannel Customer Engagement

Shoppers consult an average of 4.2 touchpoints before purchase, exposing single-channel CRM architectures. SAP Emarsys already orchestrates 1.5 billion interactions daily across email, SMS, push, and in-app alerts. Adobe has linked Marketo Engage with its experience stack, so retailers like Inditex trigger store-level promotions once mobile presence is detected.[3]Adobe Inc., “Experience Cloud Overview,” adobe.com Forthcoming ePrivacy rules will squeeze cookie-based tracking, making first-party data held in CRM systems indispensable. Telecom carriers’ layer conversational AI on these databases; Vodafone now resolves 40% of tier-one inquiries via WhatsApp Business APIs. Heightened buyer expectations, therefore, intensify price competition yet enlarge the total addressable base for the European cloud CRM market.

Cost-Efficiency and Scalability of Public Cloud Deployments

Subscription models convert fixed server outlays into flexible operating costs. A 50-seat Zoho rollout costs under EUR 2,500 (USD 2,750) a month, far below the six-figure implementation once required for Siebel. HubSpot’s 216,000-strong customer base, 60% of whom are SMEs, signals democratized access. Seasonal operators can expand compute during tourism peaks and scale back off-season, an elasticity absent in on-premises suites. Hidden charges remain: Google Cloud still imposes a 60-day exit limit, and Azure passes through at-cost data-transfer fees, but the EU Data Act will mandate standardized export within 30 days by 2027, loosening historical lock-in. Cost and scale advantages should therefore continue to lift the Europe cloud CRM market.

Emergence of Sovereign-AI Compute for Compliant CRM AI Features

The EU AI Act classifies certain CRM use cases, such as automated credit scoring, as high-risk, demanding strict localization. Oracle, Microsoft, and SAP now operate sovereign regions across Spain, Germany, and France so inference never exits the bloc. Microsoft’s EU Data Boundary further encrypts data such that non-EU staff cannot access records. Although sovereign nodes add about 10-15% to infrastructure cost, they unlock public-sector tenders off-limits to generic public cloud. As generative AI drafts emails, summarizes calls, and predicts churn, onshore compute evolves from a compliance box into a competitive differentiator that may lift premium pricing in the Europe cloud CRM market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Data-Residency and Compliance Complexity | -0.80% | EU-wide, acute in Germany, France, Netherlands | Short term (≤ 2 years) |

| Vendor Lock-in Due to Egress Fees and Limited Portability | -0.60% | Global, disproportionate impact on SMEs | Medium term (2-4 years) |

| Fragmented Late-Stage Funding for EU CRM Scale-ups | -0.40% | EU-based startups, particularly Series C and beyond | Long term (≥ 4 years) |

| Skills Gap in CRM-Centric AI and Data Talent | -0.50% | EU-wide, severe in Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Data-Residency and Compliance Complexity

Penalties that rise to 4% of global turnover compel meticulous data governance. Supplementary safeguards, including encryption, pseudonymization, and customer-managed keys, lift infrastructure cost by roughly one-quarter. Divergent interpretations across CNIL, BfDI, and other authorities force vendors to keep country-specific templates, delaying feature releases. SMEs rarely possess in-house counsel, creating a reliance on external audits or codes of conduct that add onboarding friction. Combined, these burdens shave growth from the Europe cloud CRM market until common certification schemes scale.

Vendor Lock-in Due to Egress Fees and Limited Portability

Even after AWS abolished outbound charges in 2024, competitors still restrict bulk exports or charge at-cost transfer rates that equal up to 2% of annual spend. Proprietary objects and workflow code make one-for-one migration from Salesforce to Dynamics costly, dampening switching despite price gaps. The Data Act bans punitive exit clauses by 2027, but technical schemas remain unsettled, leaving enforcement ambiguous. Such frictions temper vendor churn and consequently restrain the Europe cloud CRM market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Models Bridge Compliance and Flexibility

Hybrid architectures are expanding at a 6.80% CAGR, a pace faster than the Europe cloud CRM market itself. Public cloud still accounted for 69.17% revenue in 2025, boosted by low-touch SaaS favoured by SMEs. Private cloud persists among tier-one banks that must retain anti-money-laundering logs on-premises per European Central Bank oversight. Nutanix reports 65% of large European enterprises now prefer two-tier deployments so special-category data under GDPR Article 9 never leaves sovereign datacenters. Azure Arc, AWS Outposts, and Google Anthos extend hyperscaler control planes into customer facilities, letting firms keep ledgers in-house while exposing a customer-friendly web interface in the cloud.

Hybrid strategies also hedge against vendor lock-in, a growing worry ahead of the Data Act’s portability rules. Insurance carriers experiment with agentic AI in public cloud sandboxes, then redeploy inference to on-prem nodes once models stabilize. The Europe cloud CRM market size for hybrid-enabled projects is poised to widen as defense agencies, public hospitals, and manufacturing groups pilot sovereign-AI workloads. Over the forecast horizon, declining orchestration complexity and maturing multi-cloud standards should further narrow cost gaps with pure SaaS, anchoring hybrid models as the mainstream choice for regulated sectors.

By Enterprise Size: Voucher-Backed SME Adoption Accelerates

Large enterprises delivered 57.06% revenue in 2025, yet small and medium firms grow at a faster 6.10% CAGR, reflecting a freemium wave that trims onboarding cost. HubSpot’s freemium tier, priced at EUR 45 (USD 49.5) per month, offers email tracking and basic automation previously possible only in enterprise bundles. Spain’s Kit Digital issues EUR 6,000-12,000 (USD 6,600-13,200) vouchers, fully offsetting a three-year subscription for a 10-seat sales team. Germany’s KfW grants reimburse up to EUR 100,000 (USD 110,000), catalysing upgrades among Mittelstand manufacturers.

Platform design has evolved in lockstep. Pipedrive’s pipeline view targets five-to-50-user teams that lack IT administrators, while monday.com bundles CRM with simple no-code workflow builders. The Europe cloud CRM market size tied to SMEs is projected to keep outpacing overall growth as voucher programs prove ROI and encourage cash-strapped owners to renew beyond subsidy windows. Conversely, large-enterprise renewals may moderate given cost audits and procurement delays, yet their high seat counts will preserve revenue dominance.

By End-User Vertical: Healthcare Gains Momentum as APIs Normalize

Banking, financial services and insurance retained 26.11% share in 2025, leveraging open-banking APIs to embed personalized financial advice into CRM dashboards. Healthcare and life sciences, however, post the briskest 5.95% CAGR through 2031. Oracle Health integrated its patient-record suite with CRM across more than 70 NHS trusts, closing data gaps between appointment scheduling and follow-up care. Salesforce Health Cloud 2.0 now ships with FHIR-ready data lakes and HIPAA controls, allowing pharma firms to link educational outreach directly to physician-level engagement.

Retail adoption climbs as omnichannel loyalty schemes demand unified profiles; Inditex connects web browsing with in-store inventory to push real-time offers. Manufacturers embed sensor data into CRM for predictive maintenance; Siemens routes machine alerts through SAP Customer Experience, scheduling parts before downtime occurs. Government agencies embrace citizen portals tied to national identity registries such as Estonia’s X-Road, opening one-click access to public services. Each vertical’s maturation widens the Europe cloud CRM market by converting line-of-business use cases into enterprise-wide platforms.

By CRM Function: AI-Infused Marketing Leads Budget Re-Allocation

Sales automation still commanded 41.24% revenue in 2025, but marketing automation is growing at 6.23% CAGR as generative tools simplify content production. HubSpot’s AI assistant drafts email sequences in seconds, halving campaign lead times. SAP Emarsys applies real-time propensity scoring across 30 channels, driving cross-sell at scale. Adobe Marketo Engage dynamically adjusts ad spend based on live CRM opportunity stages.

Customer-service modules integrate conversational AI; Zendesk Answer Bot now resolves up to one-third of tier-one tickets. Analytics features, once premium, ship as standard; Einstein Analytics, Power BI plug-ins, and Zoho Analytics embed churn prediction inside core licenses. The EU AI Act requires disclosure when content is AI-generated, which might temporarily curb adoption in consumer-facing workflows; nonetheless, first-party data urgency ahead of cookie deprecation keeps momentum intact. As a result, marketing automation will keep reshaping budget priorities within the Europe cloud CRM market.

Geography Analysis

The United Kingdom retained 23.91% revenue share in 2025 after the data-adequacy renewal that now covers immigration records, safeguarding seamless transfers for multinational deployments. London’s dense financial-services cluster fuels demand for Salesforce Financial Services Cloud and Oracle CX, complemented by local sovereign cloud launches that placate post-Brexit privacy concerns. Germany follows closely, where KfW grants catalyse large hybrid migrations among Mittelstand manufacturers, and SAP leverages domestic trust plus T-Systems hosting to retain accounts.

Spain tops the growth chart at 6.60% CAGR, energized by the Digital Spain 2026 kit that issues EUR 6,000-12,000 (USD 6,600-13,200) vouchers to over 200,000 SMEs. Tourism operators adopt cloud CRM to personalize guest journeys as travel rebounds, and banks such as BBVA modernize CRM to fend off challenger brands. France advances on a sovereignty wave backed by Thales and OVHcloud, while Brevo’s EUR 500 million (USD 550 million) secondary transaction underscores rising domestic scale-ups.

The Nordics boast the highest digital-service penetration in Europe, and local vendor SuperOffice wins on language-specific workflows. Benelux expansion accelerates on the back of Efficy and Odoo valuations, whereas Italy remains slower due to SME hesitancy despite NextGenerationEU funds routed through Telecom Italia partnerships. Collectively, these dynamics validate the Europe cloud CRM market’s resilience and highlight considerable whitespace in southern and eastern regions.

Regulatory Landscape

GDPR remains the baseline compliance regime shaping cloud CRM data handling across the EU, with supervisory authorities such as CNIL (France) and BfDI (Germany) influencing vendor templates for consent, retention, and cross-border transfers. Over 2024-2026, the regulatory push extends from privacy into operational resilience and contracting: Delegated Regulation (EU) 2024/1773 set technical standards for ICT service contractual arrangements supporting critical functions, reinforcing expectations that regulated buyers (notably BFSI and healthcare) tighten CRM outsourcing terms.

A second layer of EU-wide cloud market rules is tightening portability and sovereignty requirements. The EU Data Act (Regulation (EU) 2023/2854) starts applying from September 2025 and introduces obligations around cloud switching, interoperability, and data access, aligning with the report theme of reducing lock-in and standardizing export. In October 2025, the European Commission introduced Cloud Sovereignty Framework guidance in connection with the Cloud III Dynamic Purchasing System tender, creating clearer criteria that vendors must meet for public-sector cloud bids. In June 2026, the Commission advanced a Cloud and AI Development Act proposal that includes a multi-level sovereignty framework and a capacity agenda for EU data centers, reinforcing localization-linked product, hosting, and audit requirements for cloud CRM deployments.

Competitive Landscape

North American hyperscalers Salesforce, Microsoft, Oracle, collectively command about 55-60% of European revenue, yet local challengers steadily fortify their positions. Salesforce leverages a 7,000-strong AppExchange ecosystem but faces margin pressure as SMEs pivot to HubSpot, Zoho, and Pipedrive’s lower cost tiers. Microsoft bundles Dynamics 365 with Office subscriptions, using pricing advantage and EU Data Boundary assurances to deepen footprint. SAP’s decision to retire ECC drives existing clients to review CRM alternatives, enabling Oracle CX and niche AI-native entrants to vie for share.

European startups concentrate on AI-first or industry-specific propositions. Attio pulls contact data straight from email and calendar feeds, removing manual entry for venture-backed clients. Modjo layers conversational analytics onto sales calls, feeding insights back into any connected CRM. Procore shows the power of vertical specialization in construction, while Veeva sets the example in life sciences. The EU Data Act’s ban on switching fees from 2027 is expected to erode historical lock-in moats, redirecting rivalry toward feature velocity and AI accuracy. Patent filings in conversational AI and knowledge-graph CRM rose sharply, led by Salesforce’s 1,200 AI-related patents during 2024.

Late-stage funding became selective in 2025: Brevo reached unicorn status via a EUR 500 million (USD 550 million) secondary round, whereas smaller Series C hopefuls struggled as investors grew risk-averse. Capital scarcity might trigger consolidation among niche vendors unless portability rules level the field. Overall, the Europe cloud CRM market skews moderately concentrated yet remains contestable, particularly in vertical micro-segments where localized compliance and language support trump scale.

Europe Cloud CRM Industry Leaders

Zendesk Inc.

Salesforce.com, inc.

Zoho Corporation Pvt. Ltd.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulated and public-sector-aligned deployments are a concrete whitespace where vendors can win by packaging cloud CRM with sovereignty controls, standardized exit tooling, and auditable AI workflows. The EU Data Act application from September 2025 moves switching and portability from a buyer negotiation topic to a compliance deliverable, which increases demand for migration accelerators, schema mapping, and multi-CRM interoperability layers that reduce egress and re-platforming friction.

Hybrid adoption dynamics in Europe also create a commercialization lane. Offerings that bridge sovereign regions with on-premises data stores (for GDPR Article 9 and sector rules) can be positioned as a governance-first alternative to pure SaaS for BFSI and healthcare buyers. AI enablement is being localized through vendor investments and partner ecosystem building as much as through feature releases: Salesforce disclosed multi-year commitments across major European countries, including EUR-scale investments in the United Kingdom (September 2025) and new 2026 announcements tied to AI readiness and regional hubs. This reinforces demand for partner-led implementation, training, and industry templates around agentic automation in sales, marketing, and service workflows. On the vendor side, European scale-ups such as Brevo earmarked proceeds from its December 2025 secondary transaction to accelerate AI roadmap work, supporting a broader shift toward embedded consent management, first-party data capture, and multilingual AI assistants as core CRM buying criteria across Europe.

Recent Industry Developments

- July 2026: Salesforce announced a USD 1 billion investment in Switzerland over five years to support agentic AI adoption. The investment strengthens local capacity for AI delivery and partner enablement, aligning CRM roadmaps with Europe-specific data handling and enterprise architecture needs.

- September 2025: Salesforce announced a USD 6 billion investment in the United Kingdom over five years focused on transforming organizations into Agentic Enterprises. This expanded regional commitment supports customer adoption programs and services capacity that can accelerate large-scale CRM modernization and AI workflow rollout in the UK.

- October 2024: Salesforce rolled out Health Cloud 2.0 with FHIR-ready capabilities and HIPAA-aligned controls, supporting more standardized integration with healthcare data systems. The release broadens addressable healthcare use cases for cloud CRM in Europe where interoperability and compliance requirements drive purchasing decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks spending in Europe on cloud-delivered CRM software that supports sales, marketing, customer service, and related analytics features, when it is consumed through subscription or hosted delivery models.

Scope exclusions: We do not count on-premise CRM licenses, general IT services that are not CRM-specific, or adjacent customer experience tools that sit outside a CRM workflow.

Segmentation Overview

- By Deployment Type

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Vertical

- BFSI

- IT and Telecommunication

- Retail and E-Commerce

- Government and Public Sector

- Manufacturing

- Healthcare and Life Sciences

- By CRM Function

- Sales Automation

- Marketing Automation

- Customer Service and Support

- Analytics and AI-Driven Insights

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Netherlands

- Nordics

- Benelux

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market frame and anchor the model to observable demand signals. We relied on public sources such as Eurostat for enterprise ICT and cloud adoption indicators, the European Commission for digital policy and compliance cues, OECD digital economy datasets, and national statistics offices that publish business demography and IT spending context.

To translate context into sizing inputs, we also reviewed CRM and SaaS adoption commentary from industry associations and standards bodies, then cross-checked trends using company annual reports, investor presentations, and earnings call notes. For pricing and offering structure, we used public product documentation and reputable press coverage, and then we complemented this with paid subscriptions for company financials and intelligence, news and financials, and broad patent databases to track feature direction (for example, AI-enabled CRM functions). The sources listed are illustrative only, and we used additional public and paid references to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test what desk research could not show clearly, especially how CRM demand is split by enterprise size, deployment choice, and function mix across Europe. We spoke with a balanced set of respondents across vendors, channel partners, system integrators, and end-user buyers to confirm how pricing moves in practice, how renewals behave, and when migrations tend to occur before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | |

| Mid tier: 52% | Functional/Unit leaders: 34% | |

| Smaller Players: 17% | Managers: 54% |

Market-Sizing & Forecasting

For the core sizing, a top-down approach was used where Europe-level cloud software demand is reconstructed from enterprise adoption signals and CRM spend intensity, and then distributed across major countries and buyer types. To keep the totals realistic, we then sanity-checked outputs with selective bottom-up approximations, such as sampled subscription price points multiplied by estimated seats for typical buyer cohorts, plus channel checks on deal sizes and renewal shares.

Key inputs that shaped the model included enterprise cloud adoption levels, CRM penetration by industry, average seats per customer for SMEs versus large enterprises, public versus private versus hybrid cloud mix, and the shifting share of spend across sales automation, marketing automation, customer service, and analytics and AI-driven insights. Where direct data was thin, gaps were handled through clearly stated proxy rules, such as using employment bands to estimate seat ranges, followed by interview validation.

Forecasting was done using scenario analysis supported by consensus ranges from primary discussions, since regulatory pressure, migration cycles, and AI feature packaging can change buying pace. The final forecast reflects expected subscription expansion, replacement of legacy systems, and price progression patterns that were validated across multiple respondent groups.

Data Validation & Update Cycle

Outputs were validated in steps so obvious distortions were caught early. We compared results against independent signals like regional cloud adoption trends, reported software revenue direction, and typical CRM renewal patterns, then investigated variances that fell outside expected ranges.

Before sign-off, the model and assumptions go through an internal review pass, and follow-up questions are triggered when interview feedback conflicts with desk indicators. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, sharp pricing shifts, or step changes in enterprise migration behavior. Right before delivery, a final analyst check is completed so clients receive an up-to-date view.

Mordor Intelligence's Europe Cloud Crm Market Size Versus Other Published Estimates

Published market sizes for Europe cloud CRM often differ because each publisher draws the line around what counts as CRM spend, how they treat deployment types, and how they convert subscriptions into annual value. Differences also come from whether forecasts assume steady renewal-led growth or a faster AI-led upgrade cycle.

Some estimates bundle wider customer experience software and related services, and that inflates the total even if the region and years look similar. In contrast, Mordor Intelligence counts only cloud CRM spending tied to core CRM functions and separates public, private, and hybrid deployments so adjacent tools and non-CRM services are not blended into the number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.49 B (2025) | |

| Industry Report A | USD 8.50 B (2024) | Uses an earlier base year and appears to apply a narrower revenue capture approach, which can undercount renewals and expansion seats when cloud CRM is sold as bundled subscriptions. |

| Press Release B | USD 12.00 B (2024) | Relies on an older pricing and adoption picture and may focus mainly on public cloud CRM, which can miss private and hybrid deployments used by regulated and government-heavy buyers in Europe. |

Taken together, the spread is mostly explained by time period alignment and what is included around CRM functions and deployment types. By tying the total to specific adoption indicators, seat and pricing checks, and a clear inclusion list, we keep the estimate traceable and easier to replicate when assumptions are updated.

Key Questions Answered in the Report

How large is the Europe cloud CRM market in 2026 and what growth is expected?

The Europe cloud CRM market size reached USD 14.23 billion in 2026 and is forecast to rise to USD 18.36 billion by 2031 at a 5.23% CAGR.

Which deployment model dominates European CRM spending?

Public cloud leads with 69.17% revenue share in 2025, but hybrid cloud shows the fastest momentum, expanding at a 6.80% CAGR as compliance rules tighten.

What vertical segment is growing quickest in CRM adoption?

Healthcare and life sciences is the fastest riser, projected to advance at a 5.95% CAGR because FHIR standards now allow easy data exchange with clinical systems.

Why are SMEs accelerating CRM uptake?

Voucher programs in Spain, Germany, and other countries subsidize subscription fees, while freemium pricing from vendors like HubSpot and Zoho lowers upfront cost.

How will the EU Data Act affect vendor lock-in?

From January 2027, switching fees are banned and providers must furnish exportable data within 30 days, reducing barriers to change and intensifying competition.

What role does sovereign-AI infrastructure play in market dynamics?

Sovereign nodes in Germany, France, and Spain let vendors localize AI processing, opening high-compliance verticals and differentiating offerings beyond generic SaaS.

Page last updated on: