Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

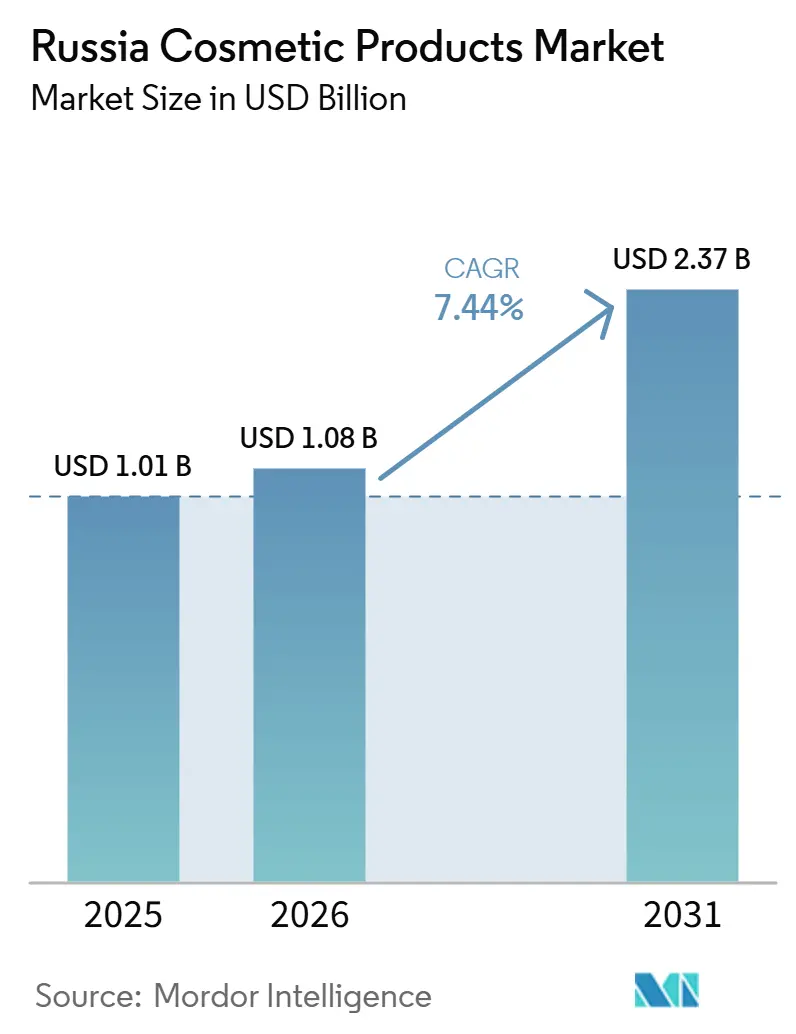

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 2.37 Billion |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Cosmetics Products Market Analysis by Mordor Intelligence

The Russia cosmetics products market size is projected to expand from USD 1.01 billion in 2025 to USD 1.08 billion in 2026 and to USD 2.37 billion by 2031, registering a CAGR of 7.44% between 2026 and 2031. The Russia cosmetics products market is moving through a post-exit reset in which domestic brands are no longer filling shelf gaps alone and are now competing on formulation, brand recall, and channel control. Domestic manufacturer revenues exceeded RUB 1.16 trillion in 2026, reporting on 2025 performance, which shows that local production has become a central part of the Russia cosmetics products market rather than a temporary response to disruption RG.RU. Premium demand, science-backed natural positioning, and faster online beauty purchasing are all supporting the expansion path of the Russian cosmetics products market. Digital commerce is also reshaping competitive power, as Wildberries moved into specialty beauty through the Rive Gauche deal and Ozon expanded its private label activity in beauty, which increases pressure on brands that depend only on wholesale distribution. The main constraint for the Russia cosmetics products market remains its reliance on imported specialty materials and the added operating burden created by mandatory product labeling and updated product safety rules

Key Report Takeaways

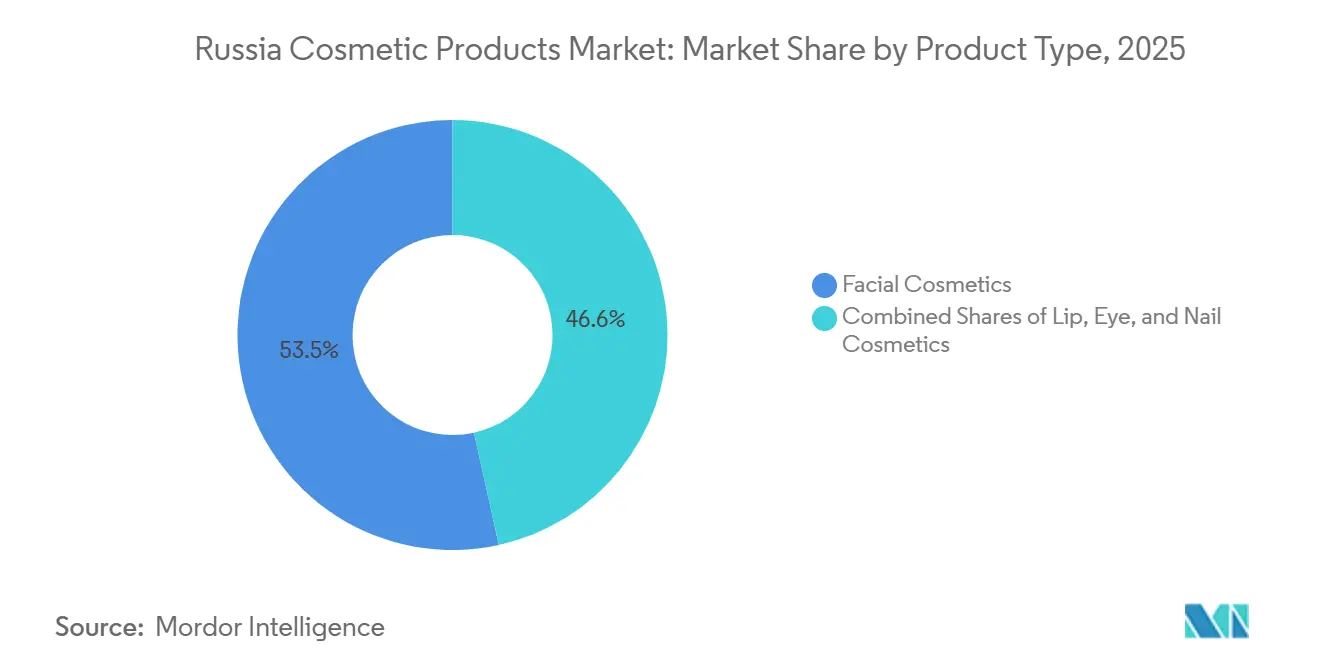

- By product type, facial cosmetics led with a 53.45% revenue share in 2025, while eye cosmetics are forecast to expand at an 8.66% CAGR through 2031.

- By category, mass products held 72.32% of the Russia cosmetics products market share in 2025, while premium products recorded the highest projected CAGR at 8.26% through 2031.

- By ingredient type, conventional and synthetic formulations accounted for 65.21% of the Russia cosmetics products market size in 2025, while natural and organic formulations are advancing at an 8.03% CAGR through 2031.

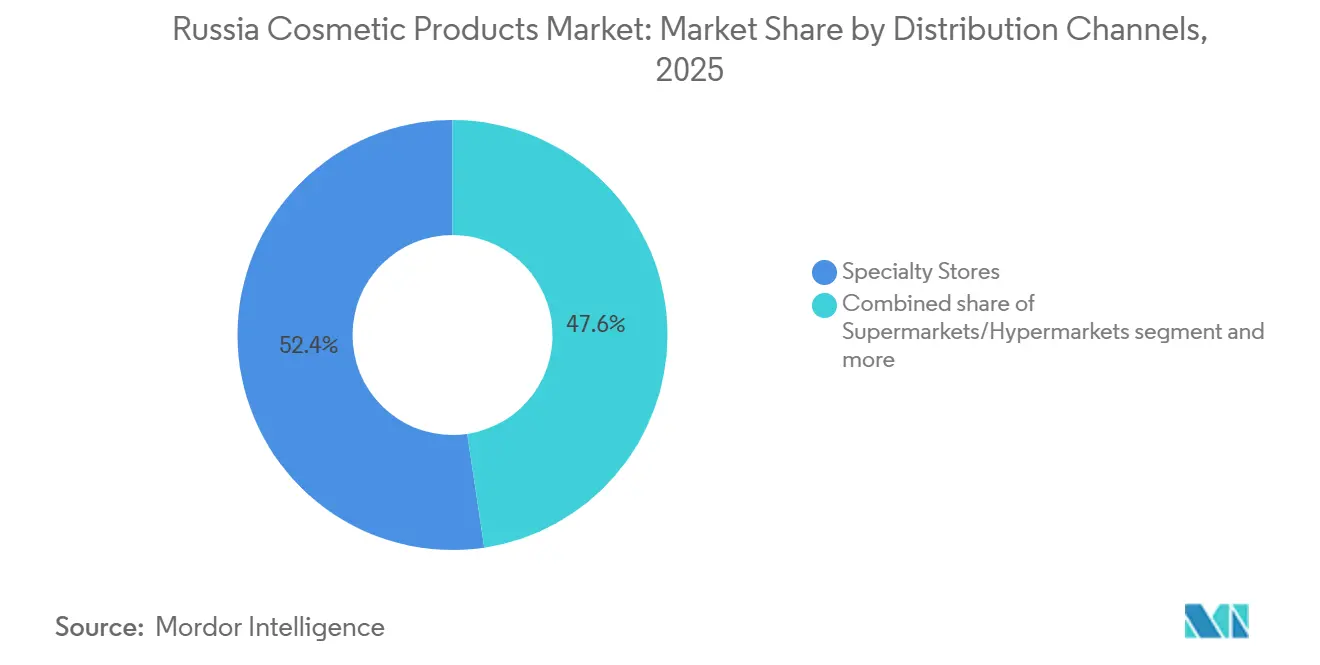

- By distribution channel, specialty stores accounted for 52.36% of the Russia cosmetics products market size in 2025, while online retail stores are forecast to grow at a 7.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Premium Makeup and Color Cosmetics | +2.0% | Moscow, St. Petersburg, Tier 1 urban centers | Medium term (2-4 years) |

| Preference for Long Lasting and Multifunctional Products | +1.2% | National, with early gains in Tier 1 cities | Short term (≤ 2 years) |

| Demand for Natural, Vegan, and Cruelty Free Cosmetics | +1.5% | National, concentrated in urban millennial demand clusters | Medium term (2-4 years) |

| Expansion of Domestic Brands Through Import Substitution | +1.8% | National, with production hubs in Moscow Oblast | Medium term (2-4 years) |

| Influence of Social Media and Makeup Tutorials | +1.0% | National, especially among digital first consumers aged 18 to 35 | Short term (≤ 2 years) |

| Adoption of E-commerce and Online Beauty Marketplaces | +1.3% | National, with stronger momentum in Tier 2 and Tier 3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium Makeup and Color Cosmetics

Russia’s premium cosmetics products space kept expanding even while interest rates and consumer caution remained elevated. Zolotoye Yabloko reported a near-doubling in net profit to RUB 7.40 billion and a one-third rise in revenue to RUB 205 billion in 2025, which shows that premium beauty demand remained firm among higher-spending shoppers[1]Source: Kommersant, “Onlain Navodit Krasotu,” Kommersant, kommersant.ru. That pattern suggests that part of the Russia cosmetics products market is moving toward fewer but higher value purchases rather than broad basket expansion. It also leaves the mid-price layer under more pressure, because it competes with premium aspiration on one side and mass affordability on the other. The same retailer’s online share moved above 60% in 2025, which shows that premium product discovery, replenishment, and brand loyalty are increasingly forming online rather than only inside stores.

Increasing Demand for Natural, Vegan, and Cruelty-Free Cosmetics

Natural positioning is becoming more credible in the Russia cosmetics products market because larger players are pairing marketing claims with research and certified production. Natura Siberica expanded its cooperation with Lomonosov Moscow State University and I.M. Sechenov First Moscow State Medical University to work on nanoliposome and fermentation-based developments, which gives science-backed support to its product positioning. The company also certified production sites in Kamchatka and Sakhalin to Russian organic standards, which raises the compliance bar for smaller brands trying to make similar claims[2]Source: AKM, “AFK Sistema Razvivaet Rynok Organicheskoy Produktsii,” AKM, akm.ru. This matters because natural products are gaining attention not only for ingredient choice but also for traceability and proof of origin. In the Russian cosmetics products market, that combination of science, sourcing, and compliance is helping natural and organic lines compete for premium shelf space and repeat online demand.

Expansion of Domestic Cosmetic Brands Through Import Substitution

The Russia cosmetics products market has moved from urgent replacement of departed brands into a phase where domestic manufacturers need scale, product performance, and broader portfolios. Rossiyskaya Gazeta reported that Russian cosmetics producers captured up to 80% of market turnover, which confirms how far local manufacturing has advanced in a short period. Even so, decorative categories remain harder to localize because high-performance pigments, filters, and other specialty materials are still tied to external supply chains. ARAVIA’s second phase at Protvino is scheduled to add 10,000 sq.m. and lift annual output by 40%, which shows that stronger domestic brands are now investing for the next stage of competition rather than for short-term replacement alone[3]Source: Interfax Russia, “Araviya Zapustit Letom Novyy Proizvodstvenno Skladskoy Kompleks V Protvino,” Interfax Russia, interfax-russia.ru. As the Russia cosmetics products market becomes more crowded, companies with manufacturing depth and export reach are likely to gain an advantage because they can spread development costs across larger volumes.

Growing Influence of Social Media, Beauty Influencers, and Makeup Tutorials

Digital beauty discovery is now a central demand shaper in the Russia cosmetics products market, especially among younger buyers in large cities. Product selection is increasingly influenced by short-format demonstrations, creator recommendations, and beauty communities that can push immediate trial for new formats and shades. This helps eye products and experimentation-led categories because tutorials reduce hesitation and make more complex looks easier to copy. It also supports direct-to-consumer brand building, since online-first labels can build visibility before they secure broad offline placement. The same shift is reinforced by rising e-commerce beauty sales and stronger online contribution from specialty retail chains, which means that content exposure and purchase conversion are now happening much closer together.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Imported Ingredients and Pigments | -1.5% | National, most acute for decorative cosmetics producers | Long term (≥ 4 years) |

| Counterfeit and Grey Market Products | -0.8% | National, concentrated in online channels and informal markets | Short term (≤ 2 years) |

| Economic Uncertainty in Premium Purchasing | -1.2% | National, with stronger pressure on mid price consumers | Medium term (2-4 years) |

| Raw Material Supply Chain Disruptions | -0.9% | National, linked to exposure across China, India, and Turkey | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Cosmetic Ingredients and Pigments

The Russia cosmetics products market still depends on imported specialty inputs in several high-performance product areas. Decorative formulations need pigments, filters, waxes, and film formers that are not yet fully supported by a domestic industrial base at the same quality and scale. This limits how quickly local brands can close performance gaps in long wear and color precision categories. Regulatory compliance adds another layer, because amendments to TR TS 009/2011 came into force on December 24, 2025 and extended the rules that companies need to meet when placing relevant products on the market. In the Russia cosmetics products market, any disruption in imported input availability can therefore affect both formulation planning and speed to shelf.

High Competition from Counterfeit and Grey-Market Cosmetic Products

Counterfeit and gray market products remain a commercial and trust problem in the Russia cosmetics products market, especially in price-sensitive and fast-moving decorative categories. The issue matters because fake or non-compliant goods can distort pricing, weaken brand confidence, and increase safety concerns for buyers. Russia introduced mandatory digital labeling for cosmetics under Government Decree No. 1681, and the system became operative from March 1, 2025, as a legal condition for sale. That move improves traceability and should help larger organized players defend legitimate sales channels over time. Even so, compliance costs are easier for bigger operators to absorb, which means the Russia cosmetics products market may become tougher for smaller brands that already face funding and distribution limits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Cosmetics Anchor the Market While Eye Category Accelerates

Facial cosmetics held 53.45% of the Russia cosmetics products market share in 2025, which kept this category at the center of value creation across both mass and premium tiers. The category benefits from steady demand for foundations, concealers, primers, and blushers, because complexion products are often treated as core routine purchases rather than discretionary extras. The Russia cosmetics products market also shows resilience in facial products because consumers can switch brands inside the category without exiting the category itself. That has helped domestic alternatives and Korean imports retain demand after the withdrawal of many Western labels.

Eye cosmetics are expected to grow at an 8.66% CAGR through 2031, which makes them the fastest-expanding product group in the Russia cosmetics products market. This pace reflects strong engagement with tutorial-led usage, especially in digital channels where liner work, bold shadows, and defined looks are easier to demonstrate than complexion matching. Eye products also benefit from faster trend cycles, which support repeat purchase and shade expansion. The growth outlook is positive, but the category remains exposed to imported raw material needs because wear performance and pigment intensity depend heavily on specialty inputs. Lip and nail products remain an important third pillar, though competition is tighter there because price comparison is simpler and product duplication is more common.

By Category: Mass Segment Leads as Premium Outpaces on Growth Rate

Mass products accounted for 72.32% of the Russia cosmetics products market size in 2025, which reflects the broad reach of accessible price points and the strong presence of domestic brands in everyday purchase categories. This segment remains the volume engine of the Russia cosmetics products market because it covers the widest shopper base and is better aligned with inflation-sensitive spending behavior. Supermarkets, hypermarkets, and marketplaces all support mass segment visibility, which helps sustain turnover even in a cautious consumption setting. The segment also benefits from quick replenishment cycles and simpler consumer comparison across brands.

Premium products are forecast to expand at an 8.26% CAGR through 2031, which places them ahead of the broader category on growth rate. Zolotoye Yabloko’s 2025 revenue and profit results show that premium beauty buyers continued to spend, and that specialty retail can still grow when assortment and digital execution remain strong. This supports a two-speed structure in the Russia cosmetics products market, where consumers either stay in value-oriented mass options or move toward quality-focused premium items. That leaves the mid-price layer with less room to defend its position. The premium segment could face stronger rivalry later in the forecast period if multinational names rebuild legal and brand groundwork for fuller participation.

By Ingredient Type: Synthetic Formulations Lead but Organic Competes on Science

Conventional and synthetic formulations represented 65.21% of the Russia cosmetics products market size in 2025, which confirms that scale, affordability, and established production methods still shape most supply. These formulations remain dominant because they are easier to produce consistently across broad assortments and mass price bands. Large domestic capacity expansion also supports their continued role in the Russia cosmetics products market. For many shoppers, performance and availability still outweigh ingredient philosophy in core decorative purchases.

Natural and organic formulations are projected to grow at an 8.03% CAGR through 2031, which shows that the premium end of ingredient demand is gaining depth. The segment is benefiting from stronger consumer focus on sourcing, safety language, and visible proof of compliance. Natura Siberica’s certified sites and expanded research partnerships have raised the credibility threshold for brands that want to compete in this area. That matters because it shifts competition away from simple packaging claims and toward documented standards, technical evidence, and product consistency. In the Russia cosmetics products market, the natural segment is therefore competing on proof rather than only on image.

By Distribution Channel: Specialty Stores Lead but Marketplace Integration Reshapes the Landscape

Specialty stores captured 52.36% of the Russia cosmetics products market size in 2025, which kept them as the leading route for curated beauty sales and premium brand presentation. Chains such as Zolotoye Yabloko, L’Etoile, and Ile de Beauté still matter because they offer sampling, advice, and stronger merchandising than general retail formats. Their role is especially important in categories where shade selection and product trial influence conversion. The Russia cosmetics products market still relies on specialty stores for premium visibility and brand building.

Online retail stores are forecast to grow at a 7.85% CAGR through 2031, and actual momentum already strengthened in early 2026. Beauty and health product sales online grew 16.50% year on year to RUB 91.30 billion in January to February 2026, which shows that the Russia cosmetics products market is seeing faster digital transaction growth than in the prior year. Wildberries and Ozon are central to this shift because they combine reach, logistics, and rapid assortment turnover. Ozon’s beauty category rose 65.60% year-on-year to RUB 107.16 billion through October 2025, while domestic brands sold strongly on Wildberries, which confirms that marketplaces are now core commercial infrastructure rather than a secondary channel.

Geography Analysis

The Russia cosmetics products market remains a single-country study, but demand and supply are not evenly distributed across the country. Moscow and St. Petersburg continue to dominate premium sales, specialty retail concentration, and early adoption of new beauty formats. These two cities also lead online penetration within organized beauty retail, with Zolotoye Yabloko’s online share exceeding 60% in 2025 and L’Etoile’s reaching 33% from 29% in 2024. Their importance to the Russia cosmetics products market goes beyond store density because they set trend direction for product mix, price tolerance, and premium acceptance. In practical terms, they remain the first testing ground for brands that want to scale nationally.

Moscow Oblast stands out as the main production corridor of the Russia cosmetics products market. ARAVIA’s Protvino complex is expanding in 2026, and Faberlic’s Chekhov plant already adds large-scale annual capacity inside the same broader area. This creates a geographic link between manufacturing scale, logistics access, and proximity to the country’s strongest beauty demand centers. It also gives domestic producers in the region a speed advantage when they need to refresh assortment or support marketplace fulfillment.

Tier 2 and Tier 3 cities are becoming more important to the Russia cosmetics products market because online logistics can reach them more efficiently than specialty store expansion can. The average online beauty purchase ticket rose 16.10% to RUB 3,600 by early 2026, which suggests that regional consumers are not only buying more often online but also spending more per transaction. This benefits brands that were built for marketplace visibility and broad price accessibility. It also reduces the historical advantage of multinational brands that relied more heavily on Tier 1 specialty shelf presence. Export activity to CIS countries and newer destinations such as Saudi Arabia and Vietnam adds another layer to the geographic picture, because it lets Russian manufacturers use domestic scale more efficiently without reducing local supply

Competitive Landscape

The Russia cosmetics products market is fragmented, with a large field of domestic manufacturers competing alongside a smaller set of multinational names that are preserving future options. The competitive focus has changed since the first replacement wave, and scale alone is no longer enough to protect position. In 2026, the strongest players are building advantage through formulation depth, manufacturing investment, and stronger control over digital channels. This has made the Russia cosmetics products market more demanding for smaller brands that lack capital for compliance, marketing, and capacity expansion. It also means that brand identity and execution now matter more than simple product availability.

Faberlic and ARAVIA are good examples of how leading local companies are responding. Faberlic officially opened its second plant in Chekhov in 2025, a 14,000 sq.m. facility with annual capacity above 60 million units and investment above RUB 1.50 billion. ARAVIA is adding a second phase to its Protvino complex in July 2026, which will raise output by 40% and support a wider launch pipeline. Natura Siberica is pursuing a different route by linking natural product claims to formal scientific partnerships and certified production, which raises the credibility threshold inside that niche.

Multinational brands have not disappeared from the competitive picture. L’Oréal registered 6 cosmetics trademarks in Russia in February 2026, including Maybelline, Lancôme, Pureology, Alien, and Essie, which shows that it is maintaining legal infrastructure for possible future activity. Marketplace groups are also emerging as a new competitor type, because Wildberries strengthened its premium beauty reach through Rive Gauche and Ozon developed private label beauty offerings through Ozon Select. This puts direct pressure on undifferentiated mass products, since the platform can influence both visibility and pricing. Compliance rules reinforce this shift, because mandatory labeling under the Chestny ZNAK system and updated technical rules favor operators that can absorb system costs and manage more complex supply chains

Russia Cosmetics Products Industry Leaders

The Procter & Gamble Company

Beiersdorf AG

L'Oréal S.A.

Shiseido Company, Limited

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rospatent confirmed L’Oréal’s registration of 6 cosmetics trademarks in Russia, covering Alien, Maybelline, Pureology Professional Color Care, Lancôme, and Essie, with exclusive rights running to 2035.

- October 2025: Wildberries acquired the specialty cosmetics chain Rive Gauche, adding a major premium beauty retail network to its broader marketplace system and strengthening its position in the beauty and personal care retail space.

Russia Cosmetics Products Market Report Scope

Cosmetics and personal care is an art field that addresses the looks and health of one's hair, nails, and skin.

Russia's cosmetics and personal care products market is segmented by product type, category, ingredient type and distribution channel. By product type, the market is segmented into personal care products and cosmetics/make-up products. The personal care products segment is further segmented into hair care products, skincare products, bath and shower products, oral care products, men's grooming products, deodorants and antiperspirants & perfumes and fragrances. The cosmetics/make-up products segment is further segmented into facial cosmetics, eye cosmetics, and lip and nail make-up products. By category, the market studied is segmented into premium and mass products. By ingredient type, the mrket is segmented into natural & organic and conventional/synthetic. By distribution channel, the market studied is segmented into specialty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels.

The market sizing has been done in value terms in USD for all the abovementioned segments.

Product Type

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Make-up Products |

By Category

| Premium Products |

| Mass Products |

By Ingredient Type

| Natural and Organic |

| Conventional/Synthetic |

By Distribution Channel

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| Product Type | Facial Cosmetics |

| Eye Cosmetics | |

| Lip and Nail Make-up Products | |

| By Category | Premium Products |

| Mass Products | |

| By Ingredient Type | Natural and Organic |

| Conventional/Synthetic | |

| By Distribution Channel | Specialty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Channels |

Key Questions Answered in the Report

How large will Russia cosmetics sales be by 2031?

The report projects the Russia cosmetics market size to reach USD 2.37 billion by 2031 from USD 1.08 billion in 2026, at a 7.44% CAGR.

Which product group leads current demand in Russia?

Facial cosmetics lead with 53.45% of 2025 revenue, supported by steady demand across both mass and premium price points.

Which category is growing the fastest through 2031?

Eye cosmetics are forecast to post the fastest product growth at an 8.66% CAGR through 2031.

Are premium beauty products still expanding in Russia?

Yes. Premium products are projected to grow at an 8.26% CAGR, and Zolotoye Yabloko reported strong revenue and profit growth in 2025.

Page last updated on: