Rotator Cuff Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

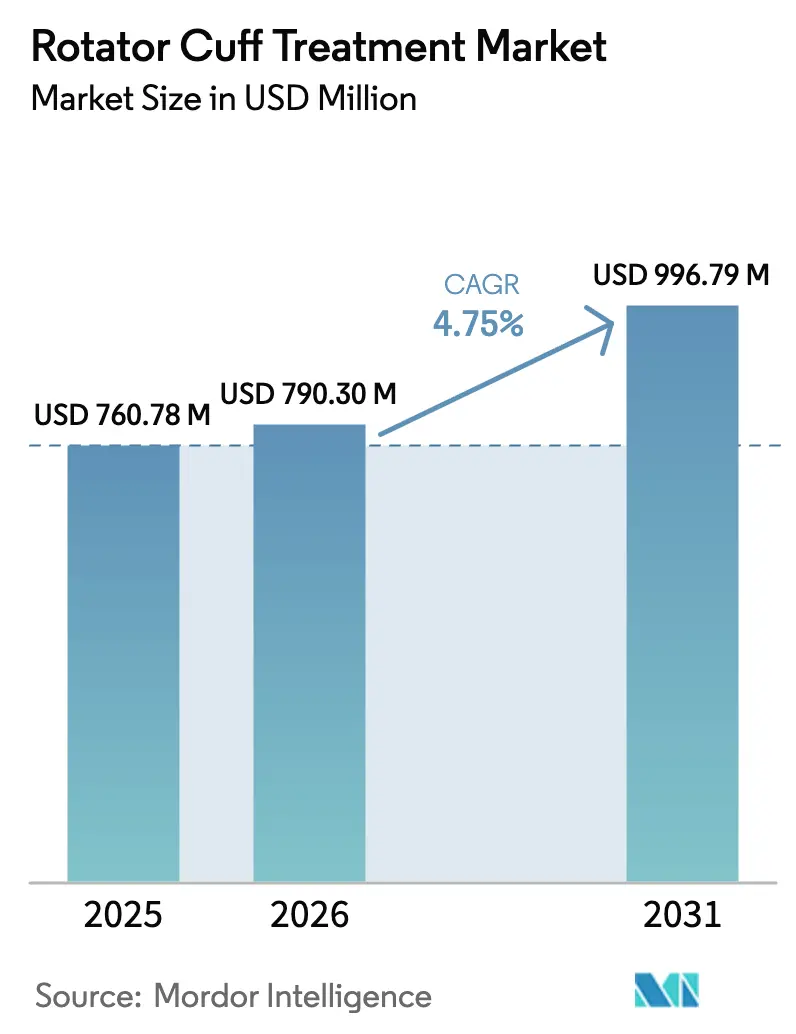

| Market Size (2026) | USD 790.30 Million |

| Market Size (2031) | USD 996.79 Million |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

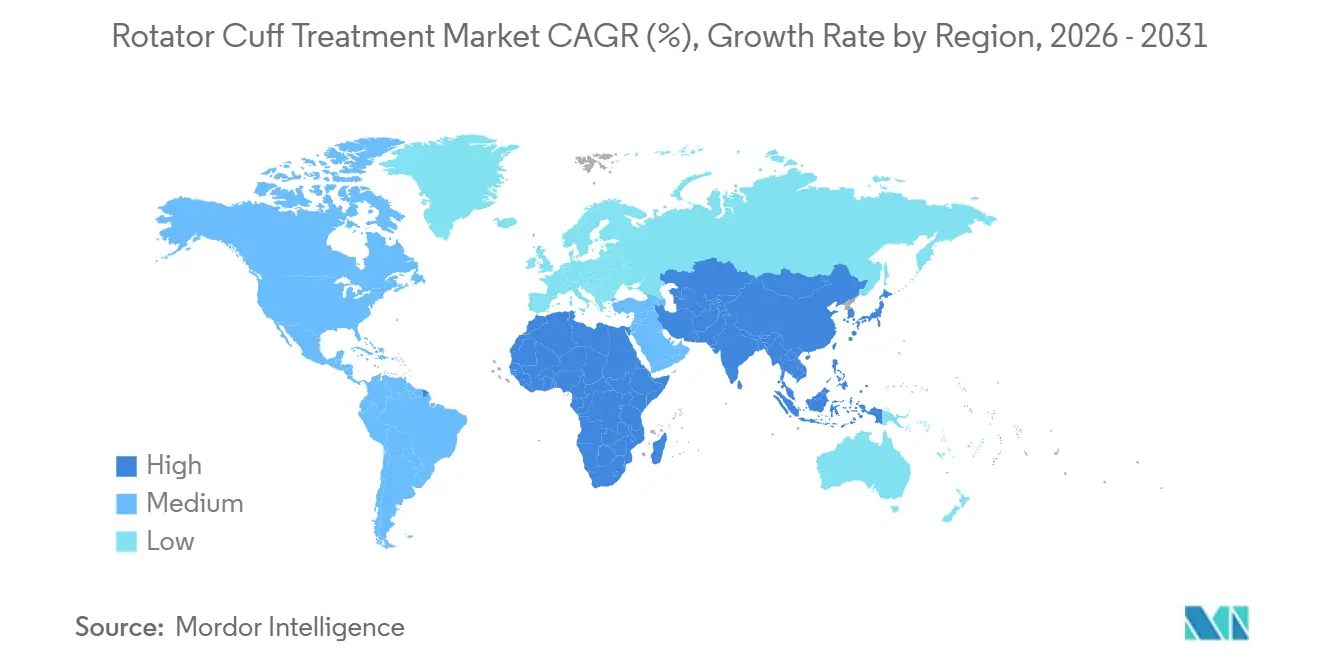

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rotator Cuff Treatment Market Analysis by Mordor Intelligence

The Rotator Cuff Treatment Market size is expected to grow from USD 760.78 million in 2025 to USD 790.30 million in 2026 and is forecast to reach USD 996.79 million by 2031 at 4.75% CAGR over 2026-2031.

Robust procedure volumes, accelerating adoption of orthobiologics, and the payer-led shift toward outpatient delivery underpin this steady expansion. Orthopedic majors are bundling anchors, biologics, and navigation systems to defend share, while venture-backed specialists chase anchorless repair techniques that promise lower implant costs and faster healing. Medicare’s 2025 payment update lifted ambulatory-surgery-center (ASC) rates for arthroscopic cuff repair by 3.2%, widening the economic appeal of same-day discharge models and compressing hospital-based volumes. At the same time, the U.S. Food and Drug Administration cleared 14 new suture-anchor and biologic-patch devices in 2024, signaling regulatory confidence in knotless fixation and allogenic augmentation technologies that shorten operative time and bolster repair integrity.[1] U.S. Food and Drug Administration, “FDA 510(k) Clearances for Orthopedic Devices, 2024,” fda.gov

Key Report Takeaways

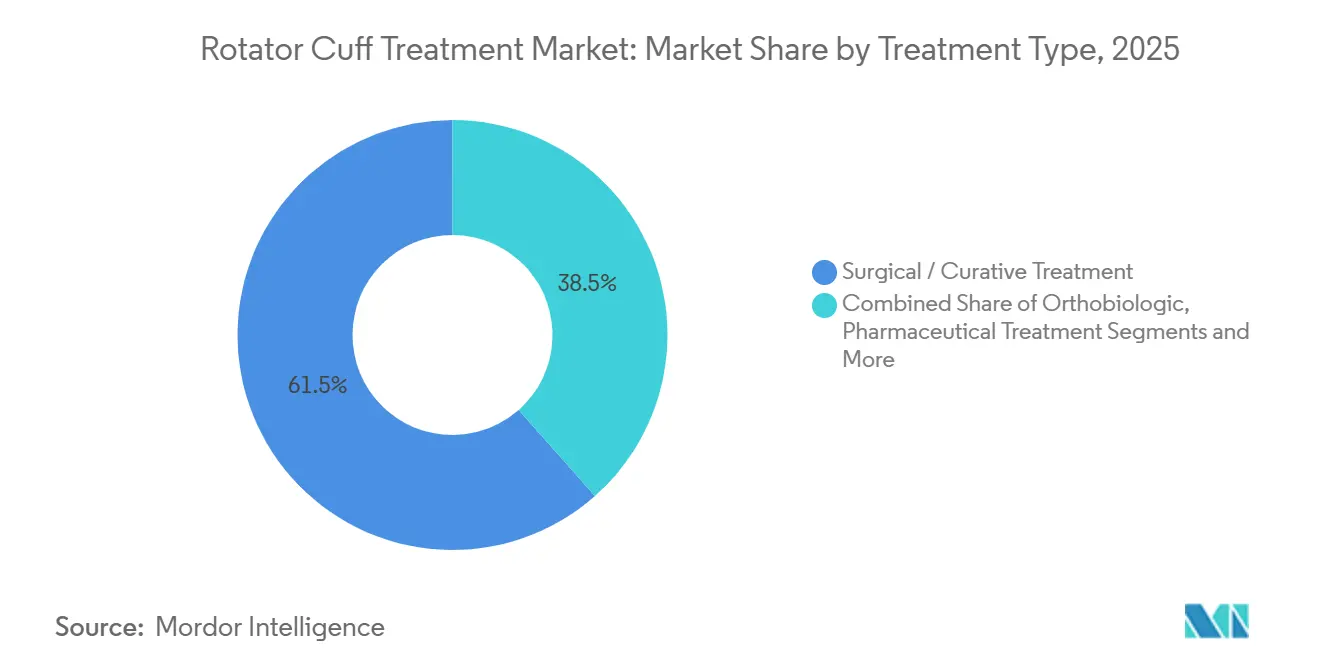

- By treatment type, Surgical and curative solutions held 61.53% of the rotator cuff treatment market share in 2025, while orthobiologics are projected to grow at an 8.36% CAGR through 2031.

- By product type, Implants and fixation devices accounted for 39.46% of the rotator cuff treatment market size in 2025, whereas biologic patches and meshes represent the fastest-growing product class at a 9.24% CAGR to 2031.

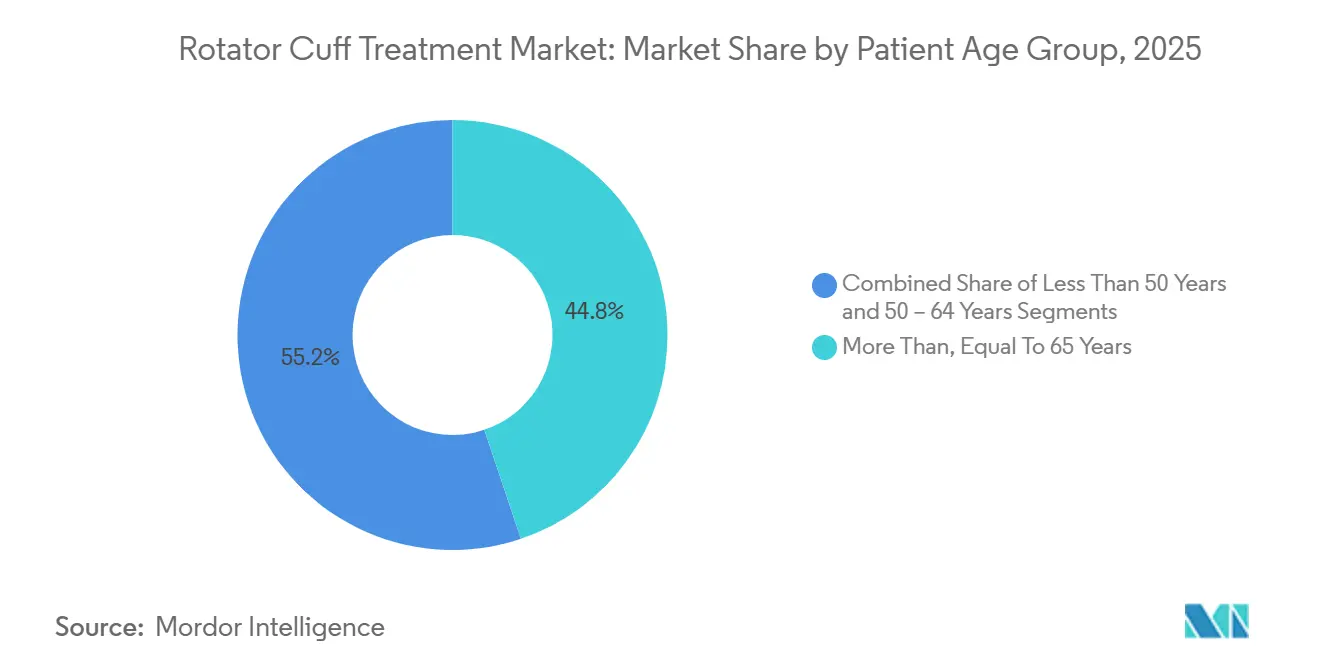

- By patient age group, Patients aged 65 years and older commanded 44.84% of 2025 procedures, yet the under-50 group is expanding most rapidly at a 7.35% CAGR through 2031.

- By indication, age-related degeneration represented 46.24% of revenue in 2025, while sports injuries are forecast to advance at a 6.24% CAGR over 2026-2031.

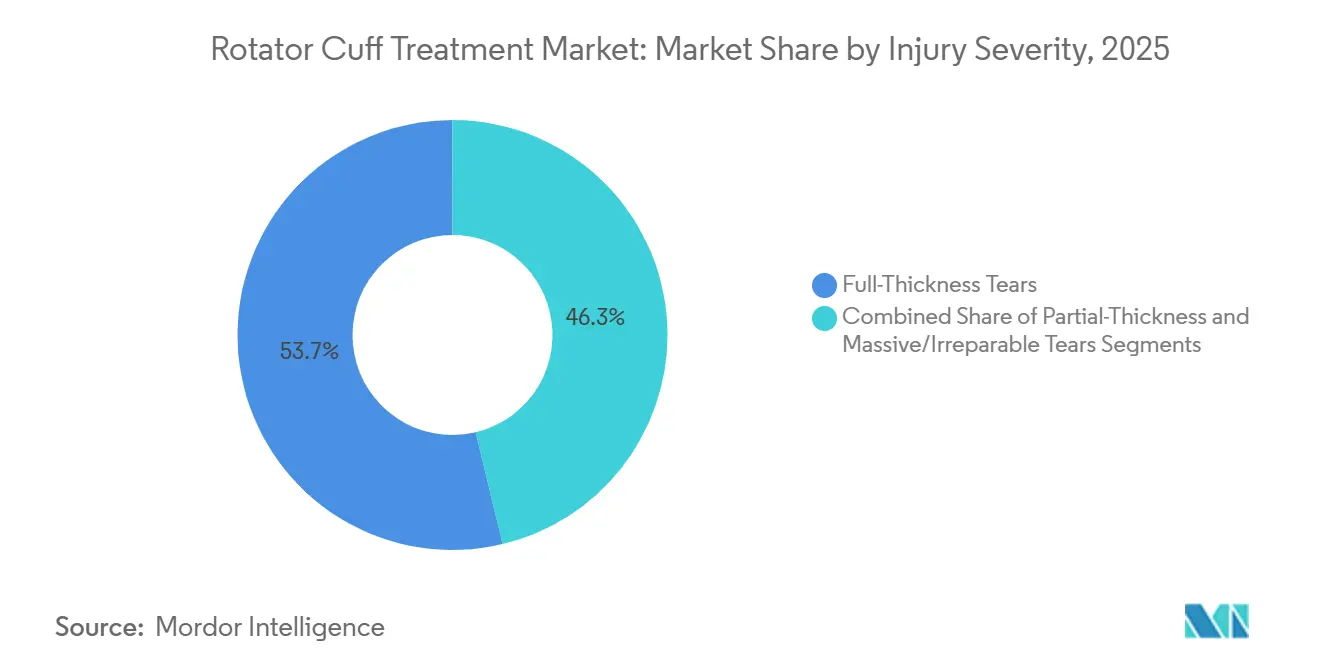

- By Injury Severity, Full-thickness tears captured 53.73% of cases in 2025, but massive and irreparable tears are set to rise at an 8.43% CAGR, reshaping device demand toward reverse shoulder arthroplasty and biologic augmentation.

- By end user, Hospitals generated 63.62% of end-user revenue in 2025; ambulatory surgical centers form the fastest-growing channel at a 6.61% CAGR through 2031 as payers steer volume to lower-cost outpatient settings.

- By geography, North America led with a 39.54% share in 2025, whereas Asia-Pacific is poised for the quickest regional expansion, climbing at a 6.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rotator Cuff Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Sports & Work-Related Shoulder Injuries | +1.2% | Global, highest in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Aging Population Driving Degenerative Tears | +1.5% | North America, Europe, Japan, China | Long term (≥ 4 years) |

| Technological Advances in Minimally Invasive & Robotic Surgery | +0.9% | North America, Europe; spillover Asia-Pacific | Short term (≤ 2 years) |

| Growing Adoption of Orthobiologics & Regenerative Therapies | +1.3% | North America, Europe; emerging Asia-Pacific | Medium term (2-4 years) |

| Ambulatory-Surgery-Center Shift Boosting Procedure Volumes | +0.8% | North America dominant; early Europe, GCC | Short term (≤ 2 years) |

| Reimbursement Updates Favoring Outpatient Cuff Repairs | +0.7% | North America; selective European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Sports & Work-Related Shoulder Injuries

Participation in overhead sports and manual-labor occupations is elevating rotator cuff injury rates among working-age adults, reversing the perception that tears are confined to older cohorts. The U.S. Bureau of Labor Statistics logged 142,000 shoulder-related workers’-comp claims in 2024, a 9% jump from 2023, with construction, warehousing, and healthcare accounting for 61% of cases.[2]U.S. Bureau of Labor Statistics, “Occupational Shoulder Injuries, 2024,” bls.gov Recreational athletes aged 35-50 are presenting with partial-thickness tears 23% more frequently than a decade ago, driven by CrossFit, pickleball, and obstacle-course racing.[3]S. Martinez, “Epidemiology of Sports-Related Rotator Cuff Tears, 2019-2024,” American Journal of Sports Medicine, journals.sagepub.com Early surgical intervention preserves productivity and athletic performance, compressing the diagnostic-to-repair timeline and enlarging the pool of candidates for minimally invasive repair. Employer prevention efforts lag the pace of injuries, ensuring sustained procedure volumes despite declining per-case reimbursement.

Aging Population Driving Degenerative Tears

Global aging is the most durable structural tailwind. Individuals over 65 already represent 44.84% of procedures, and United Nations projections show that cohort doubling to 1.6 billion by 2050. Degenerative tears often progress silently until weakness forces clinical evaluation, generating a backlog of latent cases poised to convert as imaging access broadens. Japan reported a 12% rise in shoulder arthroscopies in patients over 70 during 2025, an outcome of expanded outpatient coverage and seniors’ desire to maintain independence. Reverse shoulder arthroplasty has become the default salvage option for massive irreparable tears, overtaking hemiarthroplasty due to superior functional scores.

Technological Advances in Minimally Invasive & Robotic Surgery

Robotic-assisted platforms are standardizing anchor placement, shrinking learning curves, and shortening OR time. Stryker’s Mako system won FDA clearance for shoulder arthroscopy in 2024. A multicenter 2025 trial recorded a 14-minute reduction in mean operative time and a 38% drop in fluoroscopy exposure with robotic assistance compared with conventional techniques. Anchorless repair devices and augmented-reality navigation appeal to price-sensitive regions by eliminating metal implants and lowering radiation exposure, respectively, broadening access to advanced repair outside tertiary centers.

Growing Adoption of Orthobiologics & Regenerative Therapies

Platelet-rich plasma, stem-cell concentrates, and acellular dermal matrices are moving from experimental status to routine adjuncts for large and massive tears. A 2024 Lancet randomized trial showed a 42% reduction in re-tear incidence at 24 months when repairs were augmented with acellular dermal matrix. Medicare’s January 2025 add-on code reimburses an extra USD 850 per biologic-augmented case, legitimizing adoption in ASC settings. Allogenic PRP products further trim OR time by removing centrifugation, appealing to high-volume centers grappling with tight schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Implants & Biologics | -0.8% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Re-Tear Risk and Variable Surgical Outcomes | -0.6% | Global; pronounced in massive tears | Medium term (2-4 years) |

| Strict EU-MDR / FDA Pathways for Novel Biologics | -0.5% | Europe, North America | Long term (≥ 4 years) |

| Surgeon-Skill Gaps in Emerging Markets | -0.4% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Implants & Biologics

Acellular dermal matrices cost USD 2,500-4,500, while PRP kits add USD 800-1,200 per case, outstripping the USD 850 Medicare add-on, particularly in price-sensitive markets. Chinese and Indian patients, who pay 40-60% of orthopedic bills out of pocket, often delay surgery or choose suture-only options. U.S. value-based contracts intensify scrutiny; 68% of surgeons report pressure to justify biologic use with outcomes data.

Re-Tear Risk and Variable Surgical Outcomes

Meta-analysis places re-tear rates at 11% for small tears and up to 40% for massive lesions. Revision doubles total episode cost under bundled payments, prompting insurers like Cigna to exclude providers with outlier re-tear statistics. Biologic augmentation narrows variability but has yet to eliminate high-risk failures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Biologics Reshape Surgical Standards

Orthobiologics are expanding at an 8.36% CAGR through 2031. Surgical repairs still represented 61.53% of 2025 revenue, yet the rotator cuff treatment market size tied to platelet-rich plasma, stem-cell scaffolds, and acellular dermal matrices is rising steadily. Surgeons now integrate biologic augmentation into repairs of large and massive tears to lower re-tear risk, compressing anchor-only margins and spurring incumbent vendors to diversify into tissue engineering. Physiotherapy and palliative regimens remain first-line for partial tears and low-demand elders, while repeated corticosteroid injections face curbs due to documented tendon degeneration and elevated failure rates.

Biologic adoption coexists with a robust pipeline of stemless reverse arthroplasty implants aimed at massive irreparable pathology. The American Shoulder and Elbow Surgeons registry cites a 19% annual increase in reverse procedures across 2024-2025. Preventive programs and eccentric strengthening slow early degeneration but rarely avert surgery once functional decline sets in. Consequently, the rotator cuff treatment market maintains a dual trajectory: elective arthroscopy fortified by biologics for reparable tears and arthroplasty for salvage cases.

By Product Type: Biologic Patches Outpace Legacy Anchors

Biologic patches and meshes are advancing at a 9.24% CAGR, the fastest product category pace. In contrast, implants and fixation devices commanded 39.46% of 2025 revenue but are maturing as bundled-payment pressures curb anchor counts. Knotless systems fetch USD 450-650 each—higher than conventional anchors—yet ASCs absorb the premium in exchange for quicker OR turnover. Imaging and navigation platforms, such as Stryker’s 2024 augmented-reality arthroscopy suite, reduce anchor misplacement by 22% and support premium pricing.

The American Academy of Orthopaedic Surgeons downgraded corticosteroid injections for surgical candidates in 2025. This guidance shrinks the drugs subsegment and redirects capital toward regenerative scaffolds. Minimal-processing allografts retain 68% of native growth factors versus 12% for heavily cross-linked alternatives, accelerating tendon integration. As payers demand outcome data, vendors emphasize biomechanical strength and healing profiles to justify premium price points.

By Patient Age Group: Younger Cohorts Drive Volume Growth

Patients under 50 are expanding at a 7.35% CAGR through 2031, energizing demand for advanced biologics and rapid-rehab pathways. Seniors over 65 still hold 44.84% share, yet growth moderates as reverse arthroplasty replaces multiple repair attempts. Healing success among 55-64-year-olds matches younger cohorts when augmented with acellular dermal matrix. Younger patients show a higher propensity to self-pay for biologic upgrades, nudging manufacturers toward premium tiering strategies.

Generational preferences steer technology mix: younger athletes insist on minimally invasive approaches and same-day discharge, while older adults value pain relief and independence. Surgeons tailor implant density, rehab intensity, and biologic usage accordingly, reinforcing age-driven segmentation across the rotator cuff treatment market.

By Indication: Sports Injuries Gain Share

Sports injuries are climbing at a 6.24% CAGR, eating into the 46.24% dominance of age-related degeneration. Pickleball, CrossFit, and obstacle-course racing fueled a 34% jump in sports-related tears from 2019-2024. These patients tolerate aggressive rehab and favor biologic augmentation, with 58% of sports-related repairs in under-50s receiving PRP or dermal matrix versus 31% among degenerative cases. Traumatic tears remain smaller in volume yet drive complex reconstructions that bundle implants, biologics, and navigation.

Age-related cases progress through staged care: therapy, injections, then surgery. By contrast, sports injuries move swiftly to arthroscopy, sustaining high device utilization. Device makers therefore differentiate evidence packs and marketing narratives by indication, further fragmenting the rotator cuff treatment market share landscape.

By Injury Severity: Massive Tears Command Premium Solutions

Massive and irreparable tears are growing at 8.43% annually. Finite-element analysis shows stress concentrations beyond conventional anchor thresholds once tears exceed 4 cm, prompting biologic augmentation or conversion to reverse arthroplasty. Full-thickness tears remain the volume engine, capturing 53.73% share in 2025. Partial-thickness tears are managed more conservatively, reducing surgical volumes.

Stemless reverse systems, such as Exactech’s Equinoxe, reached 14% U.S. market penetration by Q1 2024, preserving bone stock for future revisions. Superior capsule reconstruction using fascia lata autograft is emerging as a bridge for younger patients with irreparable tendons, further enlarging the premium biologics niche.

By End User: Ambulatory Centers Capture Outpatient Shift

ASCs are climbing at a 6.61% CAGR. Although hospitals still represented 63.62% of 2025 revenue, Medicare pays USD 4,820 for CPT 29827 in ASCs versus USD 7,340 in hospital outpatient departments, a 34% spread encouraging migration. Anthem’s penalty policy alone redirected 12,000 California cases to ASCs in 2024.

Physician-owned clinics invest in point-of-care MRI to secure imaging revenue, while home-care companies bundle wearable sensors and tele-rehab to manage post-acute recovery. Manufacturers respond with channel-specific sales teams and pricing models, reinforcing fragmentation in the rotator cuff treatment market.

Geography Analysis

North America generated 39.54% of 2025 revenue, anchored by roughly 450,000 annual cuff repairs and payer policies that reward outpatient biologic-augmented arthroscopy. Canada’s single-payer constraints prolong waitlists, but cross-border travel to U.S. centers and rising supplemental insurance temper leakage. Mexican providers lure U.S. self-pay patients with 40-60% lower package prices, yet inconsistent follow-up deters broad adoption.

Asia-Pacific is the fastest-growing region at a 6.22% CAGR. China logged a 17% rise in shoulder arthroscopies in 2025. Indian surgeons cite device cost as the top barrier, spurring domestic anchor systems priced at USD 80-120. Japan’s stringent PMDA reviews delay high-tech launches 18-24 months, favoring entrenched suppliers. South Korea and Thailand capture medical-tourism flows, with Bangkok’s Bumrungrad Hospital posting a 22% rise in shoulder cases from Middle Eastern and Australian patients in 2024.

Europe faces MDR friction that stretches CE marking for novel biologics by up to 18 months. Germany, France, and the United Kingdom account for 55% of regional revenue. NHS waitlists topping 12-18 months catalyzed a 19% uptick in private shoulder procedures in 2024. Southern Europe lags on per-capita volume but leverages medical tourism to mitigate domestic shortfalls. GCC countries lead Middle East adoption thanks to high incomes and Western-trained surgeons, whereas South America remains hampered by macroeconomic volatility despite niche growth in Brazil and Argentina.

Competitive Landscape

The key suppliers includes Arthrex, Stryker, Smith & Nephew, Zimmer Biomet, and Johnson and Johnson, indicating moderate concentration. Defensive integration strategies bundle anchors, biologics, instruments, and navigation to secure single-vendor contracts with ASCs. Stryker’s 2024 acquisition of SERF added proprietary knotless anchors and RF devices that challenge Arthrex’s FiberTak suite. Smith & Nephew gained Integrity Orthopaedics’ RCR system for USD 225 million in January 2026, reinforcing its biologic graft franchise.

Disruptors target white spaces: Embody raised USD 45 million in 2024 to commercialize a resorbable collagen scaffold. Parcus Medical secured FDA clearance for a knotless anchor that undercuts incumbent pricing by 30% while matching pullout strength. Patent filings cluster around tissue decellularization and growth-factor retention, with Organogenesis, Integra LifeSciences, and Anika Therapeutics defending IP moats that dictate mechanical strength and healing velocity.

Regulatory agility is an edge; incumbents exploit established 510(k) pathways to refresh product lines quickly, while nascent cell-based therapies face prolonged review cycles. As outcome-based purchasing gains traction, data on re-tear-free survival and functional recovery eclipse incremental implant features as the primary basis for differentiation across the rotator cuff treatment market.

Rotator Cuff Treatment Industry Leaders

Arthrex, Inc.

Smith & Nephew plc

Johnson & Johnson (DePuy Mitek)

Stryker

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Arcuro Medical completed first cases of its SuperBall-RC system and released supportive white papers.

- February 2026: JUST Medical Devices received China NMPA approval for the Ossenhan Reverse Shoulder System, expanding the company’s high-end implant line.

- January 2026: Smith & Nephew agreed to acquire Integrity Orthopaedics for USD 225 million, adding an RCR platform designed to cut re-tear rates.

Global Rotator Cuff Treatment Market Report Scope

As per the scope of the report, the rotator cuff comprises muscles and tendons that keep the ball (head) of the upper arm bone (humerus) in the shoulder socket. The common rotator cuff injuries are rotator cuff tears, tendinitis, bursitis, and degenerative injuries.

The Rotator Cuff Treatment Market Report is segmented by Treatment Type, Product Type, Patient Age, Indication, Injury Severity, End User, and Geography. By Treatment Type, the market is segmented into Surgical, Physiotherapy, Preventive, Orthobiologics, and Pharmaceutical treatments. By Product Type, the market is segmented into Implants, Instruments, Rehabilitation Equipment, Imaging Systems, and Drugs. By Patient Age, the market is segmented into <50 Years, 50–64 Years, and ≥65 Years. By Indication, the market is segmented into Sports, Age‑Related, and Traumatic injuries. By Injury Severity, the market is segmented into Partial Tears, Full Tears, and Massive Tears. By End User, the market is segmented into Hospitals, ASCs, Clinics, and Home Care. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Surgical / Curative Treatment | Arthroscopic Repair | |

| Open Repair | ||

| Mini-open Repair | ||

| Shoulder Arthroplasty | Reverse Shoulder Arthroplasty | |

| Stemless Shoulder Arthroplasty | ||

| Physiotherapy / Palliative Treatment | ||

| Preventive / Conservative Management | ||

| Orthobiologics | PRP & Growth-Factor Therapy | |

| Stem-cell Therapy | ||

| Biological Meshes & Patches | ||

| Pharmaceutical Treatment | NSAIDs | |

| Corticosteroid Injections | ||

| Implants & Fixation Devices | Suture Anchors |

| Knot-less Fixation Systems | |

| Biologic Patches & Meshes | |

| Tendon Grafts & Scaffolds | |

| Surgical Instruments & Power Systems | |

| Rehabilitation Equipment | Physical-Therapy Devices |

| Braces & Supports | |

| Imaging & Navigation Systems | |

| Drugs | |

| Others |

| < 50 Years |

| 50 – 64 Years |

| ≥ 65 Years |

| Sports-Related Injuries |

| Age-Related Degeneration |

| Traumatic Injuries |

| Partial-Thickness Tears |

| Full-Thickness Tears |

| Massive / Irreparable Tears |

| Hospitals |

| Ambulatory Surgical Centers |

| Orthopedic Clinics & Physician Offices |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Surgical / Curative Treatment | Arthroscopic Repair | |

| Open Repair | |||

| Mini-open Repair | |||

| Shoulder Arthroplasty | Reverse Shoulder Arthroplasty | ||

| Stemless Shoulder Arthroplasty | |||

| Physiotherapy / Palliative Treatment | |||

| Preventive / Conservative Management | |||

| Orthobiologics | PRP & Growth-Factor Therapy | ||

| Stem-cell Therapy | |||

| Biological Meshes & Patches | |||

| Pharmaceutical Treatment | NSAIDs | ||

| Corticosteroid Injections | |||

| By Product Type | Implants & Fixation Devices | Suture Anchors | |

| Knot-less Fixation Systems | |||

| Biologic Patches & Meshes | |||

| Tendon Grafts & Scaffolds | |||

| Surgical Instruments & Power Systems | |||

| Rehabilitation Equipment | Physical-Therapy Devices | ||

| Braces & Supports | |||

| Imaging & Navigation Systems | |||

| Drugs | |||

| Others | |||

| By Patient Age Group | < 50 Years | ||

| 50 – 64 Years | |||

| ≥ 65 Years | |||

| By Indication | Sports-Related Injuries | ||

| Age-Related Degeneration | |||

| Traumatic Injuries | |||

| By Injury Severity | Partial-Thickness Tears | ||

| Full-Thickness Tears | |||

| Massive / Irreparable Tears | |||

| By End User | Hospitals | ||

| Ambulatory Surgical Centers | |||

| Orthopedic Clinics & Physician Offices | |||

| Home-Care Settings | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the expected value of the rotator cuff treatment market by 2031?

It is projected to reach USD 996.79 million by 2031 at a 4.75% CAGR over 2026-2031.

Which region is growing fastest in rotator cuff procedures?

Asia-Pacific leads with a 6.22% CAGR driven by China and India’s rising volumes.

How are ambulatory surgical centers affecting procedure economics?

ASCs capture rising volumes due to 3.2% higher Medicare rates and lower facility fees than hospitals, trimming total episode costs.

Why are orthobiologics gaining traction?

Level I evidence shows acellular dermal matrices cut re-tear risk by 42%, and Medicare reimburses an extra USD 850 per augmented case.

What challenges hinder biologic patch commercialization in Europe?

EU MDR reclassification to Class III adds 14-18 months and multi-million-euro compliance costs, delaying launches.

Which patient group drives the highest growth?

Patients under 50 expand at 7.35% annually thanks to sports injuries and willingness to adopt premium biologics.

Page last updated on: