Blood Pressure Cuffs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

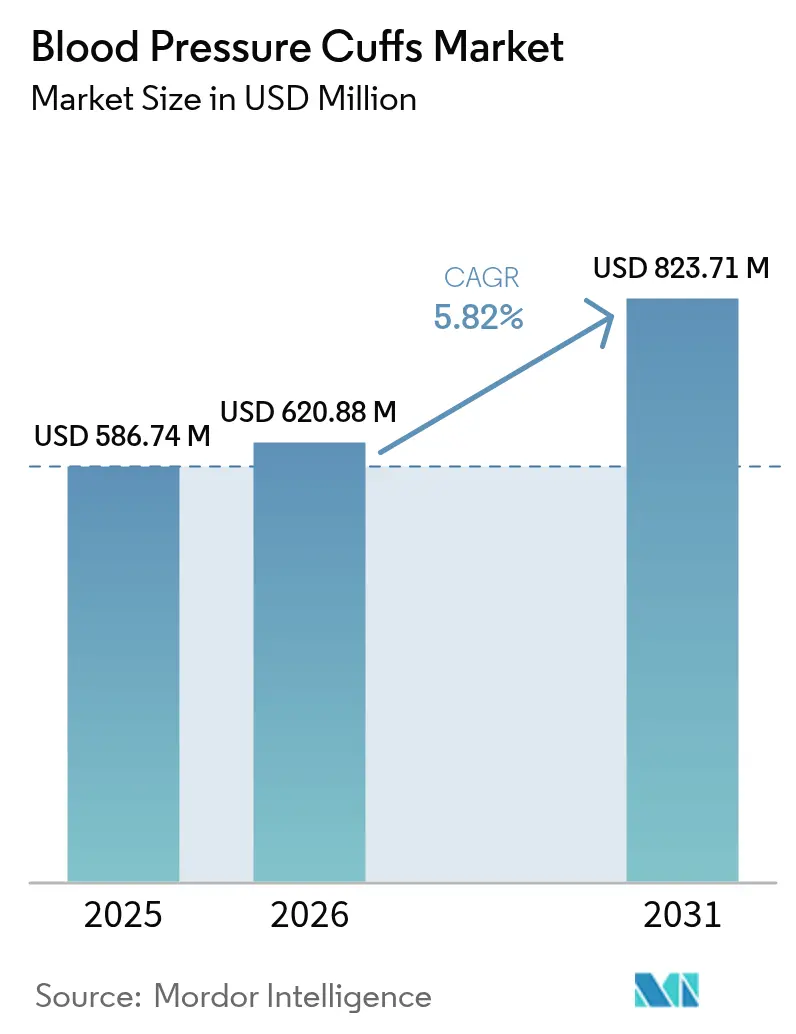

| Market Size (2026) | USD 620.88 Million |

| Market Size (2031) | USD 823.71 Million |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

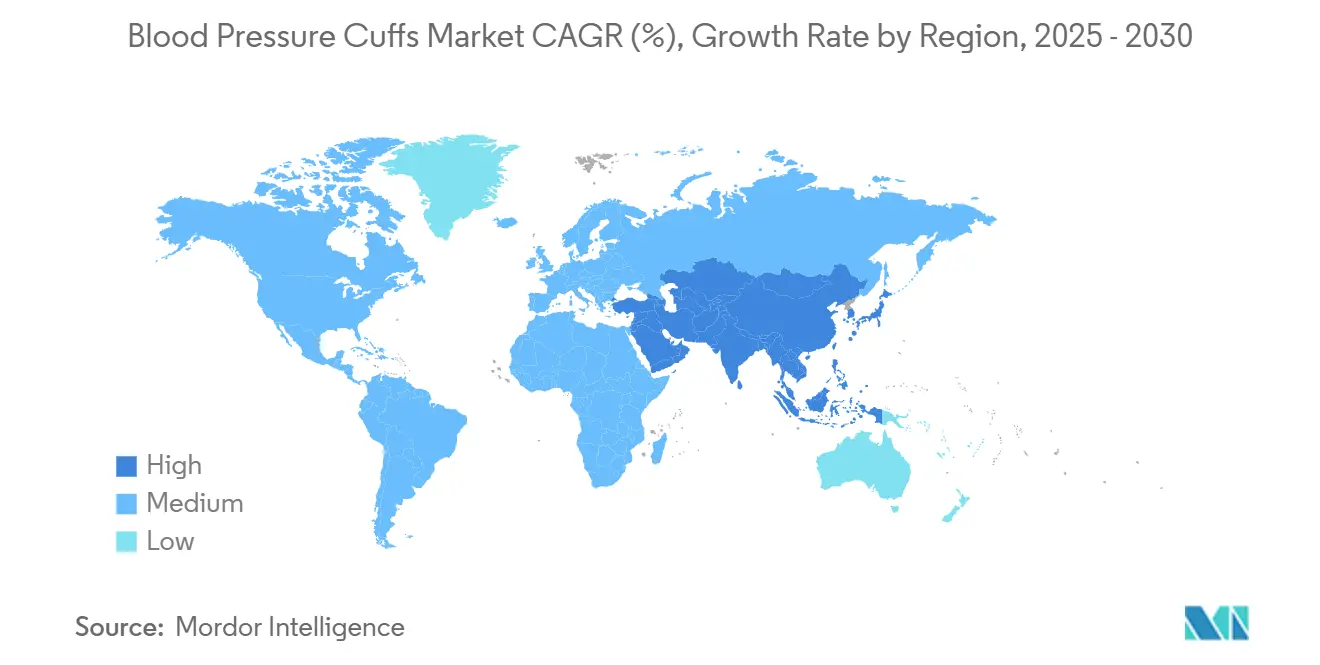

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

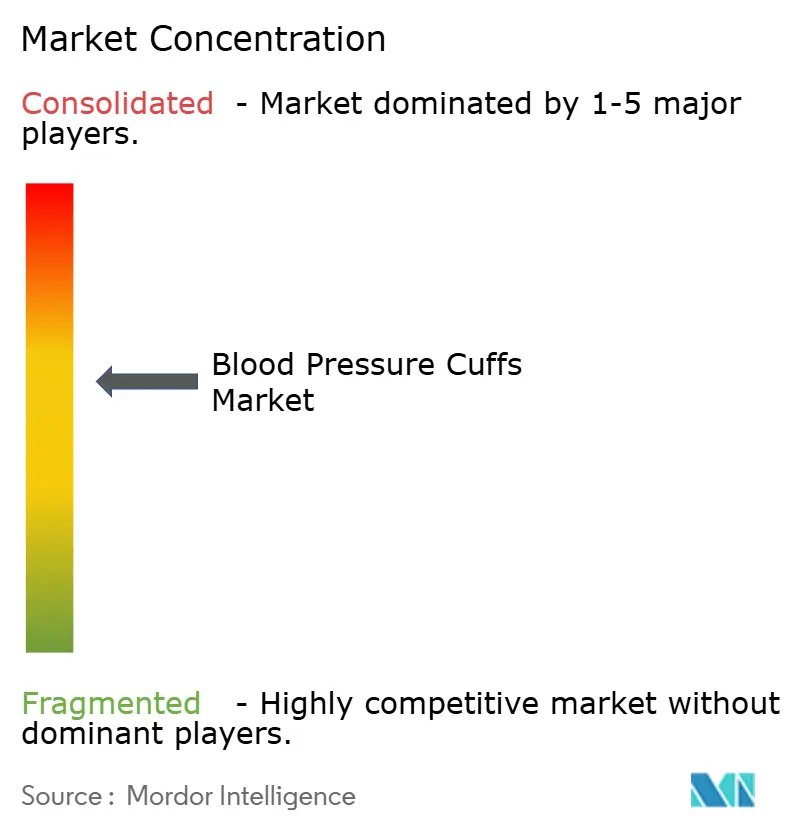

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Pressure Cuffs Market Analysis by Mordor Intelligence

The Blood Pressure Cuffs Market size was valued at USD 586.74 million in 2025 and estimated to grow from USD 620.88 million in 2026 to reach USD 823.71 million by 2031, at a CAGR of 5.82% during the forecast period (2026-2031).

Uptake accelerates as governments embed blood-pressure-focused quality metrics into reimbursement schedules and as health systems migrate from intermittent measurements to connected, longitudinal monitoring. Population aging, the steadily rising incidence of hypertension, and the shift to value-based care are expanding the installed base of automated and Bluetooth-enabled cuffs that feed electronic medical records. Hospitals are simultaneously tightening infection-control protocols, steering procurement toward single-patient disposables. Meanwhile, new CPT and ASCVD codes allow clinicians to bill for remote blood pressure surveillance, making cuff connectivity a core purchasing criterion.

Key Report Takeaways

- By usage type, reusable cuffs held 50.23% of the blood pressure cuffs market share in 2025, while disposable cuffs are forecast to expand at a 6.51% CAGR to 2031.

- By age group, the adult segment captured 69.51% revenue share in 2025; pediatric cuffs are projected to grow at a 7.01% CAGR through 2031.

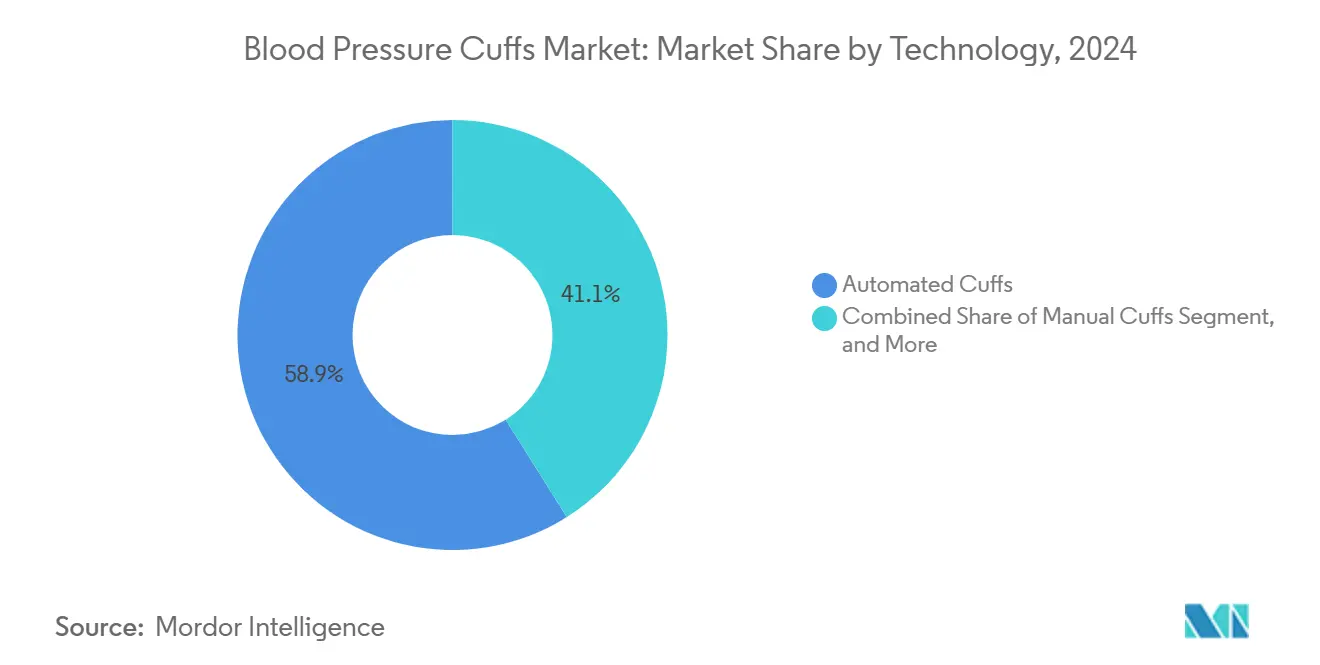

- By technology, automated cuff led the blood pressure cuffs market with a 58.22% share, and Bluetooth-enabled cuffs are expected to advance at a 9.18% CAGR through 2031.

- By end user, hospitals accounted for 36.17% of 2025 revenue, whereas home-care settings recorded the fastest CAGR at 7.79% through 2031.

- By geography, North America dominated the market with a 34.97% market share in 2025; the Asia-Pacific region is expected to have the highest regional CAGR of 7.66% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Pressure Cuffs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hypertension Prevalence & Screening Programmes | +1.2% | North America & Europe lead | Medium term (2-4 years) |

| Ageing Population and Chronic-Care Burden | +0.9% | Developed markets worldwide | Long term (≥ 4 years) |

| Shift Toward Disposable Cuffs to Curb HAIs | +0.8% | Global, hospital settings | Short term (≤ 2 years) |

| Expansion of Home-Health & Telemonitoring | +1.1% | North America & EU lead, APAC following | Medium term (2-4 years) |

| AI-driven EMR Analytics Need Standardized Data | +0.7% | North America & EU | Medium term (2-4 years) |

| Reimbursement Boost for Single-Patient Cuffs | +0.6% | North America, selective EU markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hypertension Prevalence & Screening Programmes

The rising global prevalence of hypertension has prompted large-scale screening initiatives, such as the WHO SEAHEARTS program, which aims to achieve 50% treatment coverage by 2025. U.S. quality measure #317 requires providers to document blood pressure for all adults and outline follow-up plans for elevated readings, incorporating blood pressure cuff checks into routine encounters.[1]Centers for Medicare & Medicaid Services. “Physician Fee Schedule 2025.” cms.govEuropean guidelines updated in 2024 now recommend out-of-office monitoring, expanding demand for clinically validated home devices. Uniform protocols are compressing diagnostic variability, making cuff accuracy pivotal for reimbursement claims. As regulators favor longitudinal data, health systems standardize equipment fleets to ensure comparable readings across care settings.

Ageing Population and Chronic-Care Burden

Older adults already comprise 20% of Hong Kong’s residents and will reach 32% by 2041, pushing health spending to HKD 284.1 billion (USD 36.4 billion) in 2025. Comparable demographic shifts in North America and Europe sustain home-based monitoring programs that cut 30-day readmissions by up to 76%, with blood pressure the most tracked parameter. User-friendly cuffs with large displays and guided inflation sequences reduce training needs for seniors managing multiple chronic conditions. Vendors able to certify devices for extended use cycles and seamless data transfer secure preferred-supplier status within remote-patient-monitoring contracts.

Shift Toward Disposable Cuffs to Curb HAIs

The CDC classifies cuffs as non-critical items, yet many U.S. hospitals now default to single-patient options to limit cross-contamination. GE Healthcare’s CRITIKON line exemplifies disposables optimized for ICU environments. Total cost-of-ownership models show that higher unit prices are offset by savings from reduced cleaning labor and lower infection rates. COVID-19 further entrenched the practice, and infection-control committees continue to champion latex-free, single-use designs that align with Joint Commission accreditation audits.

Expansion of Home-Health & Telemonitoring

UC Davis Health’s partnership with Best Buy Health allows cuff readings to flow directly into patient charts, illustrating how consumer-grade interfaces meet clinical standards. Adoption hinges on Bluetooth or Wi-Fi modules that auto-sync measurements, eliminating manual logging errors. The American Heart Association now endorses remote monitoring in hypertension guidelines, reinforcing procurement of connected cuffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Latex-Free Material Supply Bottlenecks | -0.4% | Global, acute in specialty polymers | Short term (≤ 2 years) |

| Non-Uniform Cuff-Size Standards | -0.3% | Global, affects pediatric & bariatric care | Medium term (2-4 years) |

| Tightening PVC-Waste Rules | -0.2% | EU leads, other developed markets follow | Long term (≥ 4 years) |

| Rise of Cuff-Less Wearable BP Technologies | -0.5% | North America & EU early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Non-Uniform Cuff-Size Standards Causing Mis-Readings

American Heart Association protocols require bladder width equal to 40% of arm circumference and length at 80%, yet manufacturer templates vary, producing errors above 10 mmHg when sizes are mismatched. Pediatric and bariatric populations face the greatest discrepancies, forcing providers to stock wide size inventories. Procurement complexity raises training burdens and can slow workflow if the correct cuff is not immediately available. Harmonized sizing matrices proposed by the International Organization for Standardization are still voluntary, so interoperability gaps persist across brands.

Rise of Cuff-Less Wearable BP Technologies

Aktiia's CE-marked optical sensor and Nanowear's FDA-cleared SimpleSense-BP offer continuous blood pressure insights without inflation bladders. Early validation shows mixed accuracy relative to oscillometric cuffs, but convenience is spurring trials in ambulatory populations. If clinical equivalence is proven, hospitals could redirect capital budgets toward multiparameter patches rather than traditional cuffs, creating competitive pressure on incumbent suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Reusable devices held 50.23% market share in 2025 due to their durability and lower per-patient cost; however, disposable units are growing at a rate of 6.51% annually, which is double the overall blood pressure cuffs market pace. Hospitals that experienced COVID-19 outbreaks quickly adopted single-use cuffs to minimize surface contamination. The blood pressure cuffs market size for disposables is forecast to expand faster than any other product category, supported by Medicare quality metrics that financially reward infection prevention.

Implementation is strongest in critical-care wards, where cross-patient exposure risk is highest, and procurement teams are increasingly evaluating total cost-of-ownership models that factor in sterilization labor and cleaning chemicals. Suppliers now offer biodegradable polymers to address PVC disposal mandates, reducing environmental concerns while retaining soft-touch ergonomics important for patient comfort. Hybrid portfolios that combine bulk reusable lines with premium single-patient SKUs enable vendors to satisfy divergent budget and safety priorities across integrated delivery networks.

Adults dominate with 69.51% revenue, but pediatric demand is rising 7.01% per year as clinicians recognize childhood hypertension’s link to lifelong cardiovascular risk. Neonatal-specific projects, such as the NIH-funded “neoBP,” highlight unmet needs for micro-cuffs calibrated for preterm infants. In 2024, the American Heart Association highlighted the limited pediatric validation of commercially marketed devices, creating a competitive opportunity for manufacturers that conduct rigorous age-stratified trials.

The blood pressure cuffs market share attributable to children remains small in absolute terms; however, higher average selling prices for specialized cuffs disproportionately lift revenue. Telehealth programs now enable parents to transmit home readings that correlate well with clinic results, thereby bolstering demand for easy-to-use pediatric kits. Vendors that bundle gamified mobile apps with colorful cuff designs are differentiating on user engagement, an increasingly important purchasing criterion for pediatric hospitals.

The automated cuffs segment accounts for 58.22% of 2025 shipments, primarily due to their consistent inflation algorithms that minimize operator variability. Bluetooth-enabled models, however, are registering a 9.18% CAGR, mirroring the expansion of home monitoring contracts. Omron’s FDA-authorized AFib detection illustrates how AI features transform a commodity cuff into a clinical decision tool, justifying higher reimbursement tiers.

The blood pressure cuffs market size linked to smart devices is growing as providers invest in dashboards that aggregate data across various vital signs. Manual aneroid and mercury columns persist in niche settings, such as dialysis units, although environmental regulations are accelerating the retirement of mercury. Partnerships between hardware firms and digital-health software vendors are now central to competitive strategy as purchasers seek turnkey solutions that feed predictive analytics engines.

Hospitals still hold 36.17% of sales thanks to central purchasing agreements, but home-care settings exhibit the strongest 7.79% CAGR as RPM codes (CPT 99453/54/57) reimburse device provisioning and data review. Medicare’s policy clarity has prompted insurers to waive copays for qualified self-measured blood pressure devices, accelerating adoption among seniors managing comorbidities.

Connected cuffs integrated with voice prompts and automatic cloud uploads fit seamlessly into tele-nursing workflows. Manufacturers are investing in smartphone-agnostic companion apps to avoid platform lock-in, appealing to health systems that operate mixed device fleets. Clinics and ambulatory centers remain stable customers, prioritizing cost-efficient automated units that streamline high-volume screening days without compromising accuracy.

Geography Analysis

North America represented 35.27% of 2024 revenue, driven by Medicare codes G0537 and G0538, which reimburse ASCVD risk assessments, including blood pressure management. Widespread electronic medical record penetration simplifies device integration, while U.S. FDA guidance provides manufacturers with clear 510(k) pathways for approval. Canada’s harmonized regulations further reduce barriers, and Mexico’s expanding health coverage bolsters volume in lower-priced tiers.

The Asia-Pacific region is the fastest-growing, with a 7.89% CAGR, supported by India’s Production Linked Incentive scheme, which targets a USD 50 billion domestic med-tech sector by 2030.[2]Economic Times Health. “India’s MedTech Sector.” health.economictimes.indiatimes.com Chinese demand rises in tandem with its aging demographic, and regulatory convergence across ASEAN markets now allows multi-country product launches with limited redesign. Japan and South Korea’s advanced telehealth ecosystems create niches for premium Bluetooth cuffs, while Australia’s Medicare item numbers for remote vital signs monitoring fuel procurement of validated devices.

Europe posts steady gains as the Medical Device Regulation (MDR) deadline locks in higher safety standards, favoring suppliers with robust clinical evidence. Nordic countries’ PVC phase-out accelerates adoption of eco-friendly cuff materials, while the EU Green Deal positions reusable systems within circular-economy procurement frameworks. Eastern European hospitals prioritize cost-effective automated units under EU structural-fund financing, whereas Western Europe shifts toward connected cuffs tied to national e-health infrastructures. South America, the Middle East, and Africa continue to develop foundational blood-pressure screening programs, but price sensitivity channels demand toward durable, entry-level devices.

Regulatory Landscape

Blood pressure cuffs are regulated as medical devices, with market access tied to device classification and conformance to recognized performance and validation standards. In the United States, FDA pathways commonly reference recognized consensus standards for non-invasive blood pressure measurement systems (including ISO 81060-series), and FDA has also issued specific guidance covering clinical performance testing for cuffless, non-invasive blood pressure measuring devices, which raises the evidence bar for emerging substitutes.

In Europe, Regulation (EU) 2017/745 (Medical Device Regulation, MDR) is the primary framework for placing cuffs on the market, and the consolidated MDR text was updated as of January 2026. Manufacturers supplying automated systems and their cuffs increasingly align technical documentation and clinical evidence with standards such as ISO 81060-2:2019+A2:2024 for clinical investigation of intermittent automated non-invasive sphygmomanometers, alongside metrological requirements such as OIML R 149-1:2020 for automated non-invasive sphygmomanometers, reinforcing post-market surveillance and verification obligations for global rollouts.

Competitive Landscape

The blood pressure cuffs market features moderate fragmentation. Multinational device firms leverage scale manufacturing, broad regulatory clearances, and field service teams to secure hospital contracts. Emerging digital-health vendors focus on software-centric value propositions, such as AI-driven arrhythmia detection or cloud analytics dashboards, creating fertile ground for partnerships or acquisitions.

Strategic moves increasingly involve vertical integration. Omron embeds AFib algorithms into its cuffs, while BD’s HemoSphere Alta platform unites sensors and predictive software to optimize hemodynamic stability. Withings positions its BPM Vision at retail price points yet embeds clinical-grade measurement sequences that synchronize with telemedicine portals.

Convergence of hardware and software is prompting deal activity. Wipro GE’s USD 960 million Indian investment includes local R&D, aiming to shorten development cycles for region-specific cuff variants. Traditional suppliers also face disruption from cuff-less technologies; however, the clinical validation demands remain high, and early adopters are pursuing hybrid portfolios rather than full substitution.

Blood Pressure Cuffs Industry Leaders

Cardinal Health

Baxter (Hillrom)

GE Healthcare

Omron Healthcare

SunTech Medical (Halma)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most immediate opportunities sit at the intersection of connectivity, reimbursement-driven remote monitoring workflows, and clinically validated performance across diverse populations. As health systems migrate blood pressure readings into electronic medical records through remote patient monitoring programs, procurement criteria increasingly emphasize automated data capture and standardization. At the same time, non-uniform cuff-sizing practices can produce clinically meaningful errors when cuffs are mismatched, particularly in pediatric and bariatric care. This supports demand for suppliers that broaden size matrices (including neonatal micro-cuffs) and back product claims with validation aligned to ISO 81060 expectations, along with documented materials and infection-control compatibility for single-patient disposables used under accreditation and HAI-prevention scrutiny.

Progress in cuffless measurement is also progressing against the same accuracy yardsticks used for cuff-based validation, shaping how cuff vendors defend and expand their installed base. In May 2026, Nature Communications reported clinical validation of a smartwatch approach using electrical bioimpedance (BioZ) and physics-informed neural networks to estimate blood pressure, and in June 2026 the Journal of Clinical Monitoring and Computing described validation of a cuffless finger-clip device against intra-arterial catheters with performance reported against ISO 81060-2 accuracy specifications in an operating room setting. These findings increase incentives for cuff manufacturers to differentiate via integrated algorithms (for example, arrhythmia features embedded into conventional measurement routines), interoperability with RPM platforms, and specialized-use cuffs for NICU and high-acuity environments where cuffs remain the operational standard.

Recent Industry Developments

- April 2026: OMRON Healthcare and the University of California, San Francisco (UCSF) launched the OMRON-AF randomized controlled trial to study home blood pressure monitoring for early atrial fibrillation detection in about 1,900 hypertension patients aged 60 and older. The program links routine cuff measurements with AI-enabled screening objectives, reinforcing the shift from commodity cuffs toward clinically differentiated, software-augmented home monitoring.

- October 2025: GE HealthCare received a CE mark for its Carevance patient monitor, which integrates Cardiac Output Insights for perioperative hypotension management. The clearance strengthens the premium end of the vital-signs ecosystem where proprietary NIBP algorithms and compatible cuffs support higher-acuity use cases and long-term platform procurement.

- November 2024: FDA granted De Novo authorization to OMRON Healthcare for home blood pressure monitors featuring AI-powered IntelliSense AFib detection. The authorization formalized a regulatory route for embedding arrhythmia detection into standard BP measurement workflows, encouraging competitors to add validated diagnostic features to connected cuff-based systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers blood pressure cuffs that inflate to temporarily restrict blood flow and capture a pressure signal for a manual gauge or an automated monitor. Revenue is counted from cuffs sold for clinical and non-clinical use, across common sizes and materials.

Scope exclusions: This scope excludes cuff-less wearable sensors and complete blood pressure monitor devices where the cuff is bundled as part of a full device sale.

Segmentation Overview

- By Usage Type

- Reusable Cuffs

- Disposable Cuffs

- D-ring/Specialty Cuffs

- By Age Group

- Adult

- Pediatric

- Neonatal

- By Technology

- Manual Cuffs

- Automated Cuffs

- Bluetooth/Connected Cuffs

- By End User

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Home-care Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where cuffs are used and what typically drives replacement and purchasing, and then anchoring the model to public healthcare and trade signals. Sources we leaned on include guidance and safety notes from bodies such as the US FDA, standards and test references from groups such as ISO, and health statistics from sources such as the WHO and the US CDC to understand hypertension screening volumes and care pathways.

We also reviewed procurement and utilization context using hospital and public tender notices where available, along with import-export statistics and customs category notes to sanity-check shipment direction by region. Company filings, product catalogs, and investor presentations were used to confirm product scope and price bands, and a paid subscription for company financials and for patent databases supported cross-checks on innovation themes and product refresh cycles. These examples are not exhaustive, and many other public sources were used for collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary inputs were used to pressure-test assumptions from desk work, especially around typical selling prices, replacement frequency, and the share split between reusable and single-use cuffs in different care settings. We spoke with participants across manufacturing, distribution, and clinical procurement, and then checked whether the views stayed consistent across APAC, EMEA, and the Americas before we locked the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 48% |

| Mid tier: 44% | Functional/Unit leaders: 32% | EMEA: 30% |

| Smaller Players: 18% | Managers: 53% | Americas: 22% |

Market-Sizing & Forecasting

The core model starts with a top-down build that reconstructs cuff demand from the installed base of blood pressure measurement points (hospitals, clinics, ambulatory care, and home monitoring) and the expected usage and replacement pattern by setting. Once that demand pool is built, average selling prices are applied by cuff type and usage, and then adjusted for regional mix and procurement channel differences.

To keep the numbers realistic, the totals are corroborated using selective bottom-up checks such as sampling supplier price lists, channel checks on common SKUs, and a limited roll-up of visible revenue cues where cuffs are a clearly stated line item. Inputs that typically move the model include the volume of hypertension screening and follow-up visits, reusable versus disposable adoption, the share of automated monitors that still use standard inflatable cuffs, cleaning and infection-control practices that affect replacement, and regional price differences driven by procurement cycles and currency timing. For forecasting, we used scenario analysis supported by expert consensus on how hospital protocols, outpatient shift, and home monitoring penetration are likely to evolve. Where partial supplier roll-ups were missing, we handled gaps by applying conservative coverage factors and re-checked them later in validation.

Data Validation & Update Cycle

Estimates are validated through stepwise cross-checks so the final number aligns with more than one independent signal. We compare outputs against import-export direction, procurement activity, and known healthcare utilization trends, and then investigate outliers when a country or segment moves outside expected ranges.

Before sign-off, the model is reviewed by another analyst who checks the math flow, key assumptions, and whether the result still matches the stated market definition. The report is refreshed annually, and interim updates are completed when material events shift demand or pricing. Right before delivery, a final pass is done so clients receive the latest updated view available at that time.

Mordor Intelligence's Blood Pressure Cuffs Market Size Compared With Other Published Estimates

Published market sizes for blood pressure cuffs can look far apart even when the same product name is used, and that usually comes down to what is counted and how the pricing and volumes are built. Differences in whether a study includes bundled monitor revenue, cuff-less wearables, or only standalone cuffs, and differences in base year and currency timing, can change the total quite a bit.

The table makes the spread easy to see, and in Mordor Intelligence's model the 2026 value is built around standalone inflatable cuffs only (reusable and disposable) that feed a pressure signal to a manual gauge or an automated monitor, with cuff-less sensors and full monitor devices excluded, which can pull the value below studies that include adjacent device revenue or earlier base-year inflation effects.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 620.88 M (2026) | |

| Global Consultancy A | USD 988.06 M (2024) | Uses an earlier base year and appears to apply a broader revenue lens without clearly separating standalone cuffs from bundled blood pressure monitoring device kits, which can lift the starting value when device revenue and price inflation are not isolated. |

| Research Firm B | USD 565.86 M (2024) | Reports a lower 2024 figure that may reflect a narrower capture of hospital-focused demand and more conservative pricing assumptions for reusable cuffs, and the longer forecast window can mask near-term procurement cycle effects. |

Looking across the three figures, most of the gap is explained by scope boundaries around bundled device revenue and by the choice of base year, which changes how pricing is carried into the model. By keeping inputs tied to clear use points, replacement logic, and reasonable price bands that can be checked in interviews, we end up with a number that is easier to trace and repeat when assumptions are updated.

Key Questions Answered in the Report

What is the current size of the blood pressure cuff market?

The blood pressure cuff market stands at USD 620.88 million in 2026 and is projected to reach USD 823.71 million by 2031.

Which segment is growing fastest within the blood pressure cuff market?

Disposable single-patient cuffs are expanding at a 6.51% CAGR as hospitals prioritize infection control.

How are reimbursement policies influencing adoption of connected cuffs?

New Medicare RPM and ASCVD codes compensate providers for remote blood pressure monitoring, driving demand for Bluetooth-enabled devices that upload data automatically.

Which region shows the highest growth potential?

Asia-Pacific is forecast to register a 7.66% CAGR, supported by India’s med-tech manufacturing incentives and rising chronic disease prevalence.

Page last updated on: