Spring Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

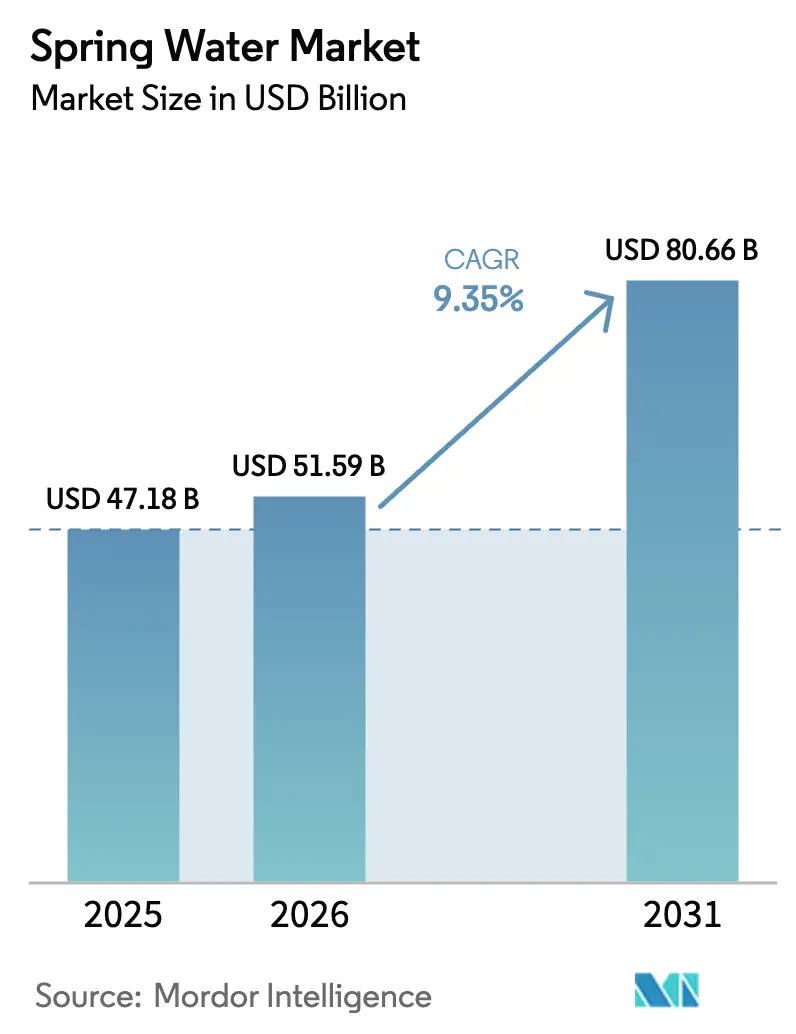

| Market Size (2026) | USD 51.59 Billion |

| Market Size (2031) | USD 80.66 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spring Water Market Analysis by Mordor Intelligence

The spring water market was valued at USD 47.18 billion in 2025 and is projected to grow from USD 51.59 billion in 2026 to USD 80.66 billion by 2031, registering a CAGR of 9.35% during the forecast period (2026-2031). This growth is driven by rising consumer concerns about contaminants in tap water, the trend toward premiumization in everyday beverages, and the growing adoption of sustainable packaging options such as aluminum and glass. In terms of product type, sparkling spring water is gaining popularity and growing faster than still water, despite its relatively smaller market base. In packaging, aluminum cans are seeing significant growth amid increased focus on sustainability. Regarding distribution channels, e-commerce is playing a crucial role in driving the shift toward direct-to-consumer sales, offering consumers convenience and accessibility. The market remains moderately fragmented, with several players competing for market share.

Key Report Takeaways

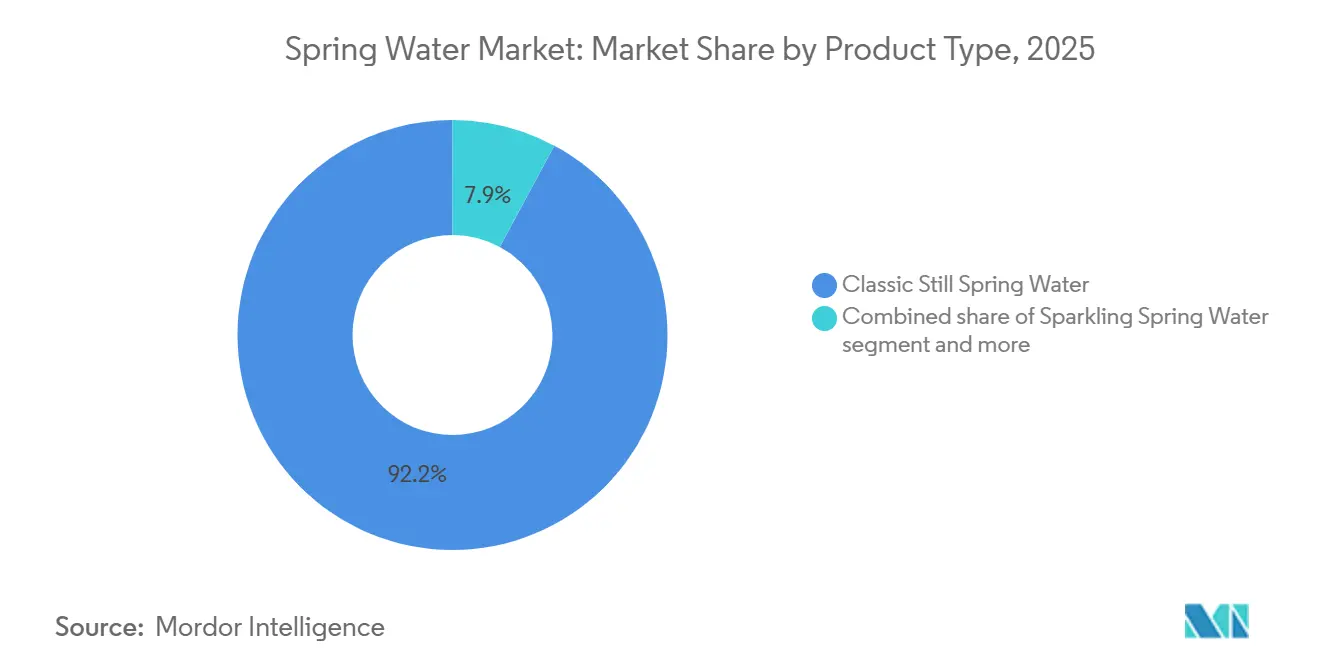

- By product type, still spring water led with 92.15% market share in 2025, while sparkling variants are forecast to expand at a 10.48% CAGR through 2031.

- By packaging, PET bottles held 76.28% share of the spring water market size in 2025, and aluminum cans are projected to grow at a 10.27% CAGR between 2026 and 2031.

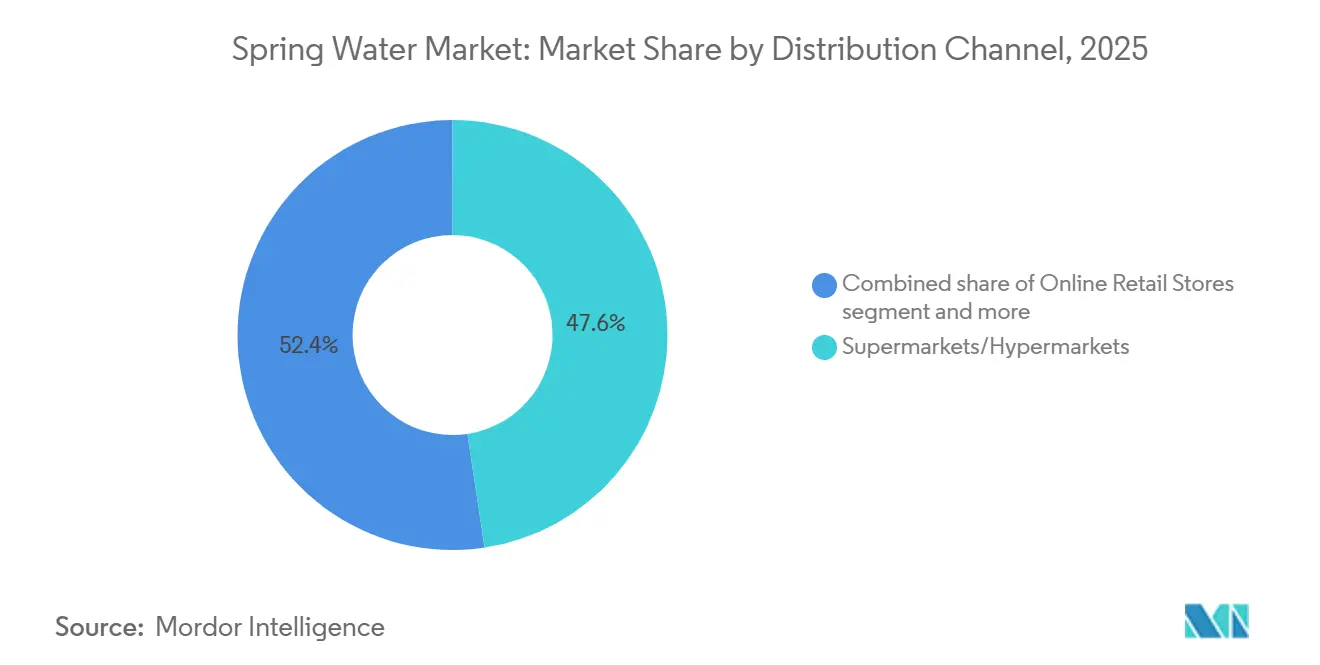

- By distribution, supermarkets and hypermarkets accounted for 47.62% of the spring water market in 2025; online retail is poised to rise at an 11.39% CAGR over the same horizon.

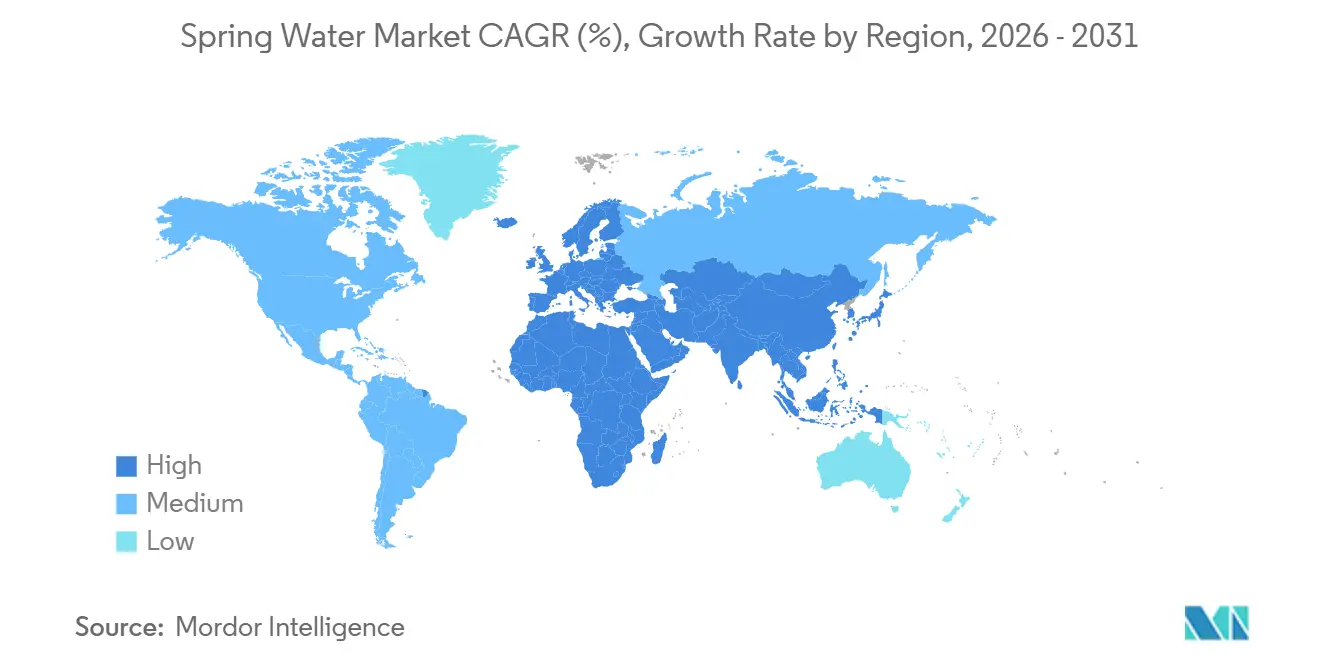

- By geography, Europe commanded 31.76% of the spring water market in 2025, whereas Asia-Pacific is positioned to record a 10.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spring Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization trends positioning spring water as lifestyle product | +1.8% | Global, with strongest uptake in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Tap water quality and safety concerns driving bottled alternatives | +2.1% | North America, Europe, emerging Asia-Pacific markets with infrastructure gaps | Short term (≤ 2 years) |

| Expansion of flavored, functional, and enhanced spring water variants | +1.5% | North America, Europe, urban centers in Asia-Pacific | Medium term (2-4 years) |

| Sustainability focus and eco-friendly packaging adoption | +1.3% | Europe (regulatory mandates), North America (consumer-driven), spillover to Asia-Pacific | Long term (≥ 4 years) |

| Consumer awareness of mineral content and hydration benefits | +1.0% | Global, with premium positioning in developed markets | Medium term (2-4 years) |

| Tourism and hospitality sector growth boosting on-premise consumption | +0.9% | Europe, Asia-Pacific tourist destinations, North America urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing concerns regarding tap water quality and safety

Concerns about tap water safety are leading more people to choose bottled spring water, especially in areas where clean, reliable drinking water is hard to find. The World Health Organization (2025) reports that 1 in 4 people worldwide, or 2.1 billion individuals, still do not have access to safely managed drinking water[1]Source: World Health Organization, "1 in 4 People Globally Still Lack Access To Safe Drinking Water – WHO, UNICEF", who.int. Among them, 106 million people rely on untreated surface water sources, such as rivers and lakes. This lack of access to safe water has made consumers more aware of water quality and the risks of contamination. As a result, many are turning to bottled spring water, which is seen as a safer and more reliable option for drinking water. The growing preference for bottled spring water highlights the need for better water infrastructure and solutions to address global water safety challenges.

Growth in the tourism and hospitality sectors

The tourism and hospitality industries are driving demand for bottled spring water. As global travel continues to grow, the need for safe, convenient, and high-quality drinking water is increasing. According to UNWTO, approximately 1.52 billion international tourists were recorded worldwide in 2025, nearly 60 million more than in 2024[2]Source: United Nations World Tourism Organization, "International Tourist Arrivals up 4% in 2025 Reflecting Strong Travel Demand Around The World", untourism.int. This consistent rise in tourist numbers has led to higher consumption of bottled spring water in hotels, resorts, airlines, cruise lines, and foodservice outlets. Tourists often prefer bottled spring water because of its reputation for purity and consistent quality. In many travel destinations, concerns about the safety of local tap water make bottled spring water the preferred choice for visitors. Additionally, many premium and environmentally conscious hospitality providers are now offering locally sourced or branded spring water to improve guest experiences and align with sustainability initiatives.

Increasing focus on sustainability and eco-friendly packaging

Concerns about sustainability and the growing preference for eco-friendly packaging are driving the global spring water market. Governments and organizations are introducing stricter regulations to reduce environmental impact, prompting companies to adopt innovative packaging solutions. For instance, the European Union introduced the Packaging and Packaging Waste Regulation (PPWR) in December 2024, which will take effect in February 2025[3]Source: European Union, "Packaging Waste", ec.europa.eu. This regulation requires that by 2030, at least 10% of beverages be sold in reusable packaging and that all packaging materials be recyclable. These rules encourage the use of sustainable materials such as aluminum and recycled plastics. Companies are responding to these changes by shifting their packaging strategies. For example, Crown Holdings has reported a noticeable increase in demand for aluminum cans, while brands like Smartwater and Poland Spring have launched recyclable metal packaging options.

Expansion of flavored, functional, and enhanced spring water variants

The growth of the spring water market is being driven by the increasing popularity of flavored, functional, and enhanced water options. Consumers today are looking for hydration products that not only quench thirst but also provide additional health benefits and enjoyable flavors. To meet this demand, beverage companies are introducing innovative products such as spring water enriched with electrolytes, vitamins, and natural flavors. For example, The Coca-Cola Company launched Powerade Power Water in 2026, which contains 50% more electrolytes than similar products and specifically targets athletes who prefer sugar-free hydration options. Similarly, Waterloo Sparkling Water expanded its offerings with unique flavors like Banana Berry Bliss and Melon Medley, catering to consumers who enjoy experimenting with new tastes. This trend of flavor innovation has significantly contributed to the market's growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from low-cost purified water and tap alternatives | -1.5% | Global, with acute pressure in price-sensitive emerging markets | Short term (≤ 2 years) |

| Environmental concerns over plastic waste and carbon footprint | -1.2% | Europe (regulatory-driven), North America (consumer advocacy), spillover to Asia-Pacific | Medium term (2-4 years) |

| Regulatory scrutiny on water extraction permits and labeling claims | -0.9% | North America (state-level), Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of home filtration systems and water purifiers | -0.8% | North America, Europe, urban Asia-Pacific with infrastructure access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental concerns related to plastic waste and carbon footprint from bottled water

Environmental concerns about plastic waste and carbon emissions are becoming significant challenges for the global spring water market. Consumers are increasingly aware of the environmental impact of plastic packaging, and regulatory bodies are imposing stricter rules to address these issues. Studies show that producing PET bottles results in approximately 5.093 kg of CO₂-equivalent emissions per kilogram of resin, highlighting the substantial environmental burden of plastic use. Despite efforts to improve recycling, the PET bottle recycling rate in the U.S. dropped to 30.2% in 2024, highlighting persistent inefficiencies in waste management systems. Additionally, lawsuits filed in 2025 against major beverage companies for contributing to plastic pollution have further increased the pressure on brands. These legal actions push them to adopt more sustainable packaging solutions

High competition from low-cost purified and tap water alternatives

Competition from cheaper purified water and tap water options is a major challenge for the global spring water market. Many consumers, especially in regions with tight budgets, prefer more affordable options over premium spring water. Purified water, which is mass-produced and sold at much lower prices, attracts a large portion of price-sensitive buyers, making it harder for spring water to gain widespread adoption. Additionally, in developed markets, treated tap water is easily accessible and reliable, reducing the need for bottled spring water in daily use. Large companies like C’estbon, which benefit from cost advantages due to large-scale production and extensive distribution networks, further increase price competition. This forces premium spring water brands to work harder to justify their higher prices by emphasizing quality, source authenticity, and health benefits to retain and attract customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sparkling Variants Outpace Still Despite Niche Base

In 2025, still spring water held the largest share of the spring water market, accounting for 92.15%. This dominance stems from its role as a reliable hydration option for households, restaurants, and institutions. Consumers prefer still spring water because it is affordable, widely available, and readily accessible across various retail formats. Its neutral taste and adaptability make it a popular choice across different age groups and regions, ensuring steady demand.

On the other hand, the sparkling spring water segment is expected to grow significantly, with a projected CAGR of 10.48% from 2026 to 2031. This growth is driven by increasing consumer interest in premium and flavored beverages, especially among younger and urban populations. The demand for healthier, low-sugar, and functional drink options is further boosting their popularity. Innovations such as naturally carbonated and infused sparkling water are likely to attract more consumers, thereby contributing to the segment's global expansion.

By Packaging Type: Aluminum Cans Surge as Sustainability Imperative

PET bottles were the most widely used packaging format in the global spring water market in 2025, holding a 76.28% share. Their popularity stems from their affordability, lightweight design, and compatibility with existing production and distribution systems. Consumers prefer PET bottles for their convenience and durability, making them a common choice across retail outlets. Additionally, the strong infrastructure supporting PET bottle production and distribution ensures their continued dominance in the market.

In contrast, aluminum cans are expected to grow at the fastest rate, with a projected CAGR of 10.27% during 2026–2031. This growth is driven by increasing demand for sustainable packaging solutions, as aluminum is highly recyclable and considered more environmentally friendly than plastic. Retailers and regulators are also pushing for eco-friendly alternatives, further boosting the adoption of aluminum cans. Moreover, their premium appeal and suitability for single-serve and on-the-go consumption are contributing to their rising popularity in the market.

By Distribution Channel: E-Commerce Accelerates Direct-to-Consumer Shift

Supermarkets and hypermarkets were the leading distribution channels in the spring water market in 2025, accounting for 47.62% of the total market share. These stores are popular because they offer a wide variety of spring water products, including different brands and sizes, all in one place. Consumers find it convenient to shop for beverages alongside their regular groceries. Supermarkets and hypermarkets often offer competitive pricing, bulk-buy options, and frequent discounts, making them an attractive choice for buyers. Their strong presence in urban and semi-urban areas further solidifies their role as a key channel for spring water sales.

Online retail is expected to grow at the fastest rate, with a projected CAGR of 11.39% through 2031. This growth is driven by the increasing popularity of e-commerce platforms, which offer the convenience of home delivery and subscription services for regular purchases. Consumers are also drawn to the ability to explore a wider range of products, including premium and niche spring water brands, which may not be readily available in physical stores. Online platforms enable companies to gather valuable customer data, which they can use to personalize marketing efforts and improve customer loyalty. These factors are expected to drive the rapid expansion of online retail in the coming years.

Geography Analysis

Europe accounted for 31.76% of spring water market revenue in 2025, driven by strong consumer preference for mineral and spring water, as well as the presence of well-established premium brands. Consumers in the region value high-quality products, heritage branding, and premium packaging, which sustain demand. However, stricter regulations around sustainability, reuse, and labeling are increasing compliance challenges for manufacturers. Despite these hurdles, leading companies continue to rely on their strong brand reputation and unique product offerings to stay competitive in this mature market.

The Asia-Pacific region is expected to grow the fastest, with a projected CAGR of 10.13% from 2026 to 2031. This growth is fueled by rapid urbanization, higher disposable incomes, and growing concerns about tap water safety in emerging economies. The expanding middle class is increasingly choosing packaged spring water as a safe and reliable hydration option. Additionally, rising tourism and the demand for on-the-go consumption are boosting sales of convenient and premium water formats. Investments in production facilities and distribution networks are further supporting the region’s growth potential.

North America remains a key player in influencing global spring water market trends, particularly in areas like regulation and consumer behavior. Concerns about water quality and safety are shaping purchasing decisions, while sustainability efforts are driving a shift toward eco-friendly packaging options. Meanwhile, Latin America and the Middle East & Africa show mixed growth patterns. In these regions, demand for bottled water is supported by inadequate public water infrastructure. However, economic instability and price sensitivity can affect consumer buying habits, leading to uneven growth across these markets.

Competitive Landscape

The spring water market is moderately fragmented and includes several key players, including Nestlé S.A., Danone S.A., BlueTriton Brands, PepsiCo Inc., and Roxane (Cristaline). These companies hold strong positions due to their well-established brands and wide distribution networks. However, no single company dominates the market entirely. Many large players are focusing on mergers and acquisitions to expand their reach and improve efficiency. Meanwhile, smaller regional and niche brands remain competitive by targeting specific local demands and offering premium products.

Competition in the market is growing as companies focus on securing reliable water sources, improving supply chains, and innovating packaging. Many businesses are adopting advanced technologies, such as AI-driven logistics, to streamline operations and reduce costs. Sustainability is also becoming a key focus, with companies investing in eco-friendly packaging to appeal to environmentally conscious consumers. Additionally, some players are integrating their operations vertically, enabling them to control sourcing and production more effectively and helping them stand out in the market.

Entering the spring water market is becoming more challenging due to strict regulations and the high costs of setting up infrastructure for sourcing, testing, and packaging. Companies must also comply with environmental standards, such as water conservation and recyclable packaging requirements, which add to operational complexities. As a result, established players with strong financial and technological resources are better positioned to thrive. These challenges make it harder for new companies to enter the market, further solidifying the dominance of existing players.

Spring Water Industry Leaders

-

Nestlé S.A.

-

Danone S.A.

-

BlueTriton Brands

-

PepsiCo Inc.

-

Roxane (Cristaline)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Billy, an Australia-based beverage company, introduced 100% natural spring water packaged in recyclable aluminium cans, emphasizing its sustainability-focused approach. The water was sourced from natural springs in Victoria and offered in both still and sparkling variants to meet diverse consumer preferences.

- October 2025: Eternal Water, a naturally alkaline spring water brand sourced from springs across the United States, was reported to have introduced its new 800mL (27 fl.oz) bottle during this year's NACS Show. The launch highlighted the brand's commitment to providing convenient, sustainable packaging options to meet evolving consumer demands.

- April 2025: RAIN Pure Mountain Spring Water launched a 24-pack of aluminum-bottled spring water, targeting eco-conscious consumers and expanding availability across major U.S. retailers, including Kroger, Smart & Final, and West Marine.

- October 2024: Flow Beverage Corp. introduced Flow Sparkling Mineral Spring Water in 300ml aluminum bottles in Canada, with flavors like OG, Blackberry + Hibiscus, Lemon + Ginger, and Cucumber + Mint, using sustainable packaging featuring 70% recycled aluminum.

Global Spring Water Market Report Scope

Spring water is naturally sourced groundwater that flows to the surface from an underground aquifer and is collected at or near the spring. The global spring water market consists of product type, packaging type, distribution channel, and geography. Based on product type, the market is segmented into classic still spring water, sparkling spring water, flavored spring water, and other spring water. Based on packaging type, the market is classified into PET bottles, glass bottles, aluminum cans, and Tetra Pak. Based on distribution channel, the market is classified into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market forecasts are provided in terms of value (USD) and volume (Liters.)

| Classic Still Spring Water |

| Sparkling Spring Water |

| Flavored Spring Water |

| Other Spring Water |

| PET Bottles |

| Glass Bottles |

| Aluminum Cans |

| Tetra Pak |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Classic Still Spring Water | |

| Sparkling Spring Water | ||

| Flavored Spring Water | ||

| Other Spring Water | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Aluminum Cans | ||

| Tetra Pak | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the spring water market be by 2031?

It is projected to reach USD 80.66 billion by 2031, expanding at a 9.35% CAGR from 2026-2031.

Which product format is growing fastest?

Sparkling spring water is forecast to post a 10.48% CAGR, outpacing still, flavored, and functional lines.

What packaging format is gaining share most rapidly?

Aluminum cans are projected to grow at a 10.27% CAGR thanks to recyclability and supportive regulation.

How are leading brands responding to sustainability pressures?

Strategies include launching aluminum and glass formats, investing in refillable systems, and securing eco-friendly supply chains to meet emerging reuse mandates.

Page last updated on: