Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

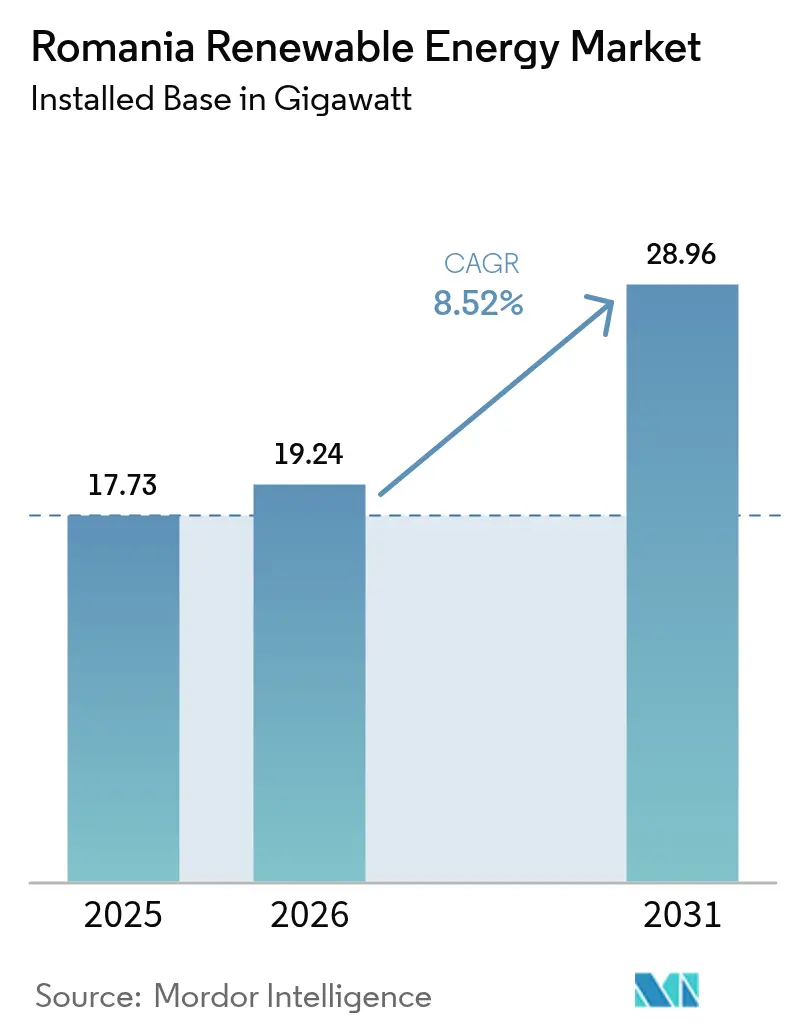

| Base Year Market Size (2025) | 17.73 gigawatt |

| Market Volume (2026) | 19.24 gigawatt |

| Market Volume (2031) | 28.96 gigawatt |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Renewable Energy Market Analysis by Mordor Intelligence

The Romania Renewable Energy Market size is expected to grow from 17.73 gigawatt in 2025 to 19.24 gigawatt in 2026 and is forecast to reach 28.96 gigawatt by 2031 at 8.52% CAGR over 2026-2031.

Robust EU decarbonization mandates, a EUR 3 billion Contracts-for-Difference (CfD) program, and EUR 815 million of grid modernization funds are driving capital inflows as developers pivot from coal toward diversified renewables. Corporate power-purchase agreements (PPAs) have become the primary demand lever, with exporters locking in long-term clean electricity to preserve access to the EU market. A fast-moving prosumer segment, surging from virtually zero in 2018 to more than 77,000 systems by early 2024, adds critical distributed solar capacity and strengthens grid resilience. The technology mix is led by hydropower, yet solar’s double-digit growth rate signals a structural swing toward photovoltaics. While transmission bottlenecks and policy volatility constrain near-term rollouts, targeted grid upgrades and the Black Sea offshore roadmap create multi-gigawatt expansion pathways that sustain the Romanian renewable energy market over the forecast horizon.

Key Report Takeaways

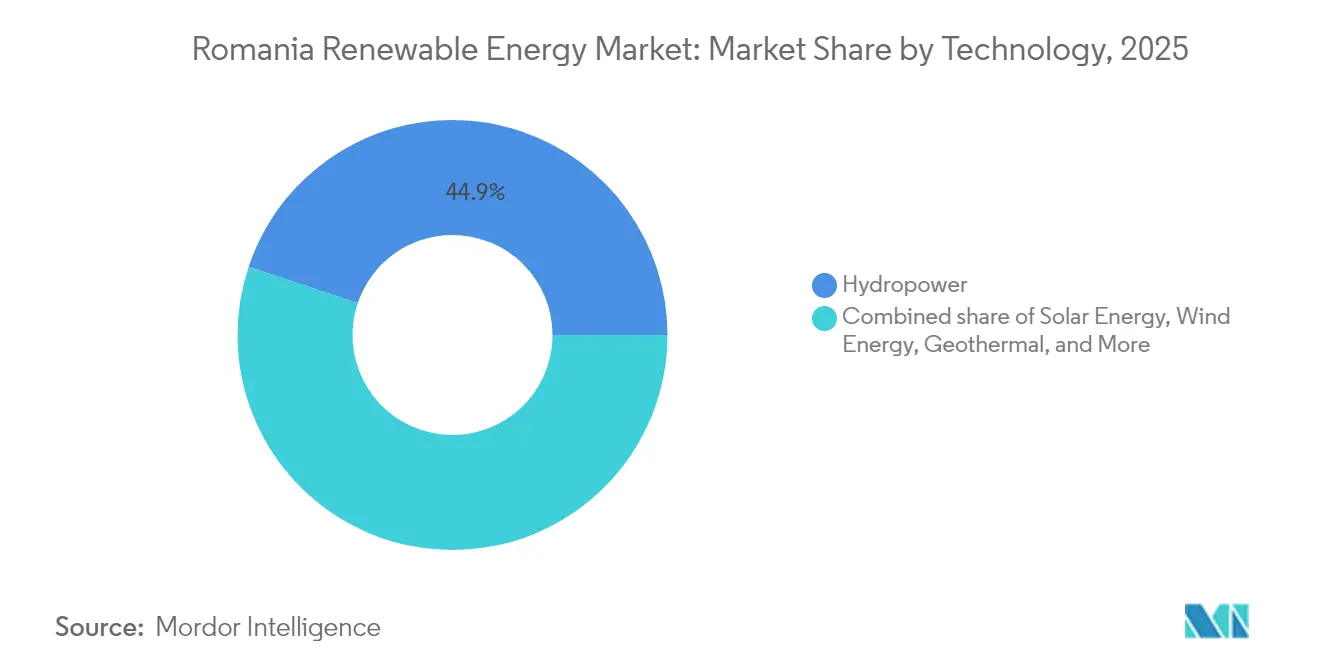

- By technology, hydropower commanded 44.85% of the Romania renewable energy market share in 2025. Solar energy is projected to register a 14.26% CAGR between 2026 and 2031, the fastest pace among all technologies.

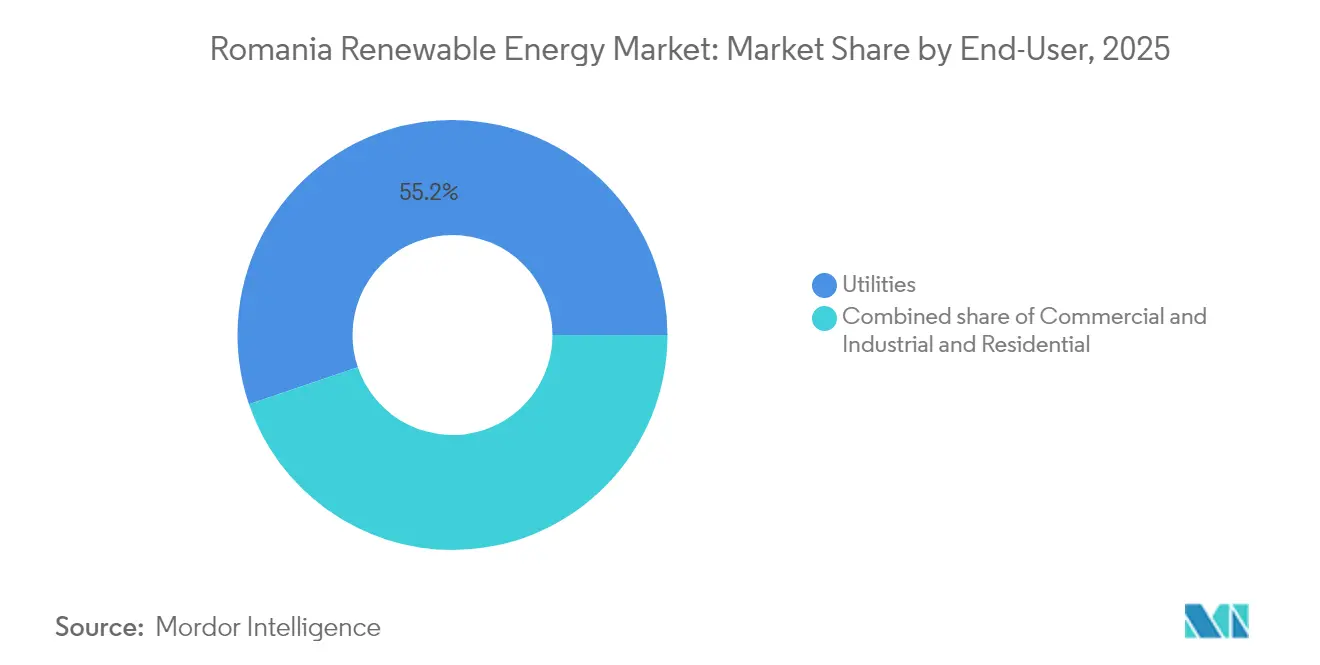

- By end-user, utilities held 55.22% of the Romania renewable energy market share in 2025. The commercial and industrial segment is forecast to expand at a 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EU-funded grid modernisation pipeline | +1.50% | Dobrogea & Muntenia | Medium term (2-4 years) |

| Surge in corporate PPAs from energy-intensive exporters | +1.80% | National | Short term (≤ 2 years) |

| Post-coal land repurposing for mega-solar parks | +1.20% | Gorj, Hunedoara, Mehedinți | Medium term (2-4 years) |

| Black Sea offshore-wind roadmap (3-7 GW by 2035) | +0.90% | Constanța offshore waters | Long term (≥ 4 years) |

| Rapid rise of prosumers (>2 GW by 2024) | +0.60% | Urban & suburban areas | Short term (≤ 2 years) |

| Green-hydrogen pilot demand for RES-backed power | +0.30% | Constanța & Prahova refineries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated EU-funded Grid Modernisation Pipeline

EUR 815 million from the EU Modernisation Fund is earmarked to unlock renewable connections, and Transelectrica broke ground on the EUR 134 million 400 kV Constanța Nord-Medgidia Sud line in 2024, an asset sized to relieve at least 273 MW of constrained wind capacity.(1)Transelectrica, “400 kV Constanța Nord–Medgidia Sud Project Factsheet,” transelectrica.ro The project is the first in a series of high-voltage reinforcements that collectively aim to add more than 2 GW of transferable capacity by 2026. Parallel smart-grid rollouts and 29 transmission-station solar retrofits further digitalize the network, reducing curtailments. These upgrades directly bolster the Romania renewable energy market by compressing interconnection timelines and stabilizing wholesale prices. In concert with national plans for 40 GW of total installed capacity by 2035, of which 80% must be renewable, modernized lines bridge resource hubs with demand centers, enabling future offshore wind injections.

Surge in Corporate PPAs from Energy-Intensive Exporters

Industrial exporters are shifting their procurement models to secure green electricity and avoid looming carbon-border tariffs. The landmark OMV Petrom–DRI solar PPA, signed in 2024, covers approximately 100 GWh annually for 8.5 years.(2)OMV Petrom, “Solar and Wind PPAs Signed in 2024,” omvpetrom.com Saint-Gobain followed with an 800 GWh wind deal effective 2026, while Bekaert inked a 100 GWh virtual PPA with Rezolv Energy, ensuring 10-year price certainty. These contracts diversify revenue streams for developers, derisk project financing, and expedite final investment decisions. PPA momentum enhances demand visibility, increasing the confidence of institutional investors in funding large pipelines, which in turn is expected to expand the Romania renewable energy market.

Post-Coal Land Repurposing for Mega-Solar Parks

Romania’s coal phase-out, legally binding by 2032, releases sizeable tracts of grid-connected land. Gorj County alone has access to EUR 550 million of Just Transition Fund money for redevelopment. CE Oltenia’s delayed replacement program leaves a 2026-28 generation gap that solar developers are eager to fill.(3)CE Oltenia, “Just Transition Projects Overview,” ceoltenia.ro Brownfield mine sites often possess transmission access, water rights, and perimetral fencing, slicing permitting complexity and build costs. Social initiatives such as RenewAcad retrain coal workers, easing local acceptance and assembling a renewable-ready workforce.

Black Sea Offshore-Wind Roadmap (3–7 GW by 2035)

Law 121/2024, enacted in May 2024, created a dedicated offshore regime, setting the stage for up to 7 GW of capacity by 2035 and targeting first power in 2032.(4)Government of Romania, “Law 121/2024 on Offshore Wind,” gov.roThe World Bank finds 76 GW of technical potential in Romanian waters, implying a deep supply-chain opportunity. BSOG's flagship 3 GW Midia perimeter project is now Romania's most advanced offshore proposal. The Black Sea's superior load factors can cut levelized costs by more than 30% compared to inland wind. Although subsea cabling and onshore reinforcement require significant capital investment, offshore wind introduces a new technology vector that could expand Romania's renewable energy market in the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission bottlenecks in Dobrogea wind corridor | -0.80% | Dobrogea | Short term (≤ 2 years) |

| Policy volatility around price caps & CfD rollout | -0.50% | National | Medium term (2-4 years) |

| Lengthy local permitting & land-use disputes | -0.70% | Rural regions | Medium term (2-4 years) |

| Ageing large-hydro assets needing capex overhaul | -0.60% | Carpathian rivers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Transmission Bottlenecks in Dobrogea Wind Corridor

Romania’s highest-yield wind sites in Dobrogea are limited by saturated 220 kV lines that restrain roughly 500 MW of potential additions. Curtailments reach 8% during windy nights, denting project economics. Developers face higher debt-service cover ratios and a slower financial close. Until the Constanța Nord-Medgidia Sud backbone and companion 400 kV loops enter service, grid access queues lengthen, depressing the near-term CAGR in the Romanian renewable energy market.

Policy Volatility Around Price Caps & CfD Rollout

Emergency price caps, which have been shifted quarterly since 2022, compress merchant revenues and create hedging uncertainty. The inaugural 1.5 GW CfD auction cleared at EUR 78 to 82/MWh; however, the parameters for subsequent rounds remain undefined. Variable fiscal terms complicate lender appraisals and extend due diligence cycles. For prosumers, VAT reimbursement delays of up to 12 months sap household cash flow. This governance shift is hampering the otherwise vibrant outlook of the Romanian renewable energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hydropower Anchors While Solar Accelerates

Hydropower retained a 44.85% share of the Romania renewable energy market in 2025, buoyed by 6 GW of installed dams straddling the Carpathian rivers. Solar, however, delivered the steepest trajectory, climbing 59% year-on-year and pushing cumulative photovoltaic capacity to 5.3 GW. Within the Romania renewable energy market size for technologies, hydropower accounted for roughly 7.95 GW in 2025, whereas solar is projected to surpass 13.2 GW by 2031. Generous CfD ceilings of EUR 78/MWh, smarter inverters, and simplified one-stop permitting offices in seven counties underpin a 14.26% CAGR for solar. Wind holds a steady second position, with onshore pipelines of 4.6 GW and the landmark offshore regime offering longer-dated expansion vectors. Bioenergy relies on EU rural development grants to monetize crop waste, and pilot plants in Dolj County are testing the co-digestion of manure and straw. Although ocean energy remains embryonic, the Black Sea's mild tidal range may suit point-absorber wave devices post-2030, thereby extending the diversity of technology.

The Romania renewable energy market benefits structurally from solar's short construction cycle, making it the preferred hedge against policy swings. Nevertheless, the dominance of hydropower ensures a year-round baseload that tempers volatility, boosting investor confidence. Pumped-storage upgrades at Tarnița-Lăpuștești could add 1 GW of storage-enabled flexibility by 2029, magnifying the integration of variable renewables. Hybrid solar-plus-wind plus battery offerings emerge in Constanța County, offering sub-60 EUR/MWh levelized costs and attracting corporate offtakers. Over the forecast window, solar's share of Romania's renewable energy market size is expected to narrow the gap with hydropower as land-repurposed mega-parks in Gorj and Hunedoara come online.

By End-User: Utilities Dominate as C&I Segment Surges

Utilities controlled 55.22% of installed renewable energy capacity in 2025, comprising 9.79 GW of capacity across hydro, wind, and solar assets. Their incumbency grants grid-code familiarity, dispatch rights, and vertically integrated supply portfolios. Yet, commercial and industrial entities are slated to scale their capacity at a 10.05% CAGR, thereby increasing their share of the Romanian renewable energy market size to an expected 6.45 GW by 2031. Multinationals seeking zero-carbon certifications are fueling direct-PPA pipelines, while domestic exporters hedge their exposure to EU carbon border levies. Tier-1 banks now tailor sustainability-linked loans with margin ratchets tied to renewable-sourcing milestones, aligning finance costs with decarbonization paths.

The resurgent prosumer class is accelerating residential participation, forecasted to reach 2.75 GW by 2031. Although residential contributions remain modest versus utility portfolios, their locational diversity reduces line losses and supplies reactive power. Municipalities experiment with community energy cooperatives that bundle rooftop arrays with demand-response platforms, expanding citizen equity in the Romania renewable energy industry. Utilities adapt by offering turnkey rooftop kits and subscription-based flexibility services, defending market share while exploring digital customer channels. The evolving end-user mosaic adds competitive richness and underpins long-run resilience for the Romania renewable energy market.

Geography Analysis

Dobrogea remains the fulcrum of Romanian onshore wind, hosting 29.65% of the national capacity and maintaining average capacity factors above 32% despite curtailments. Transmission reinforcements slated for 2026 will unlock a second wave of developments and lift the Romania renewable energy market size in the region. Southern Oltenia attracts utility-scale solar developers thanks to high irradiation, flat terrain, and grid nodes vacated by coal closures. Gorj and Hunedoara counties alone offer more than 1.5 GW of shovel-ready sites, with Just Transition funds helping to cushion the social impacts.

The Carpathian Mountains remain the heartland of hydropower, supporting multi-decadal plants that anchor base generation. Refurbishment projects, including turbine upgrades at Vidraru, aim to restore lost efficiency and expand peaking ability. The Western Banat and Crișana regions are leveraging agro-biomass resources to pilot combined heat-and-power plants that feed green district-heating loops. Meanwhile, geothermal reservoirs near Oradea supply 150 MWth of thermal capacity, seeding potential electricity projects beyond 2028.

Constanța County is at the center of the emergent offshore-wind supply chain, offering deep-draft Port of Constanța facilities for staging jackets and turbine nacelles. Proximity to Bulgarian and Turkish waters fosters cross-border collaborations, positioning Romania as a Black Sea fabrication hub. Enhanced cross-border interconnectors with Hungary and Bulgaria elevate export opportunities, allowing surplus wind and solar to arbitrage price spreads, thereby amplifying revenue stacking for investors in the Romania renewable energy market.

Competitive Landscape

The Romanian renewable energy market is characterized by a moderate concentration level, with the top five developers accounting for approximately 48% of the installed capacity. Hidroelectrica leverages its hydro core to bankroll solar and onshore wind ventures, including a 300 MW photovoltaic portfolio under construction. Enel Green Power deploys standardized EPC templates and digital-twin asset management to compress opex and extend turbine lifespans. Rezolv Energy aggregates merchant-exposed wind under long-dated PPAs, showcasing innovative finance structures backed by sustainable-bond proceeds.

Strategic moves intensify as OMV Petrom acquires a 50% stake in Electrocentrale Borzești, adding 1 GW of renewables and a green-hydrogen pilot to its downstream decarbonization roadmap. PPC’s USD 768 million purchase of 629 MW in solar and wind assets signals continued Greek investment appetite and introduces balance-sheet heft that sparks competitive tariff bidding. Equipment vendors Vestas, Siemens Gamesa, and GE Vernova are battling for turbine orders, each touting platforms with capacities exceeding 6 MW, tailored for Romania’s mixed wind regimes.

Market dynamics are shifting toward hybrid offerings that combine solar, wind, storage, and software. Transelectrica’s tender for grid-forming inverters opens a service niche for technology suppliers. With offshore wind approaching the procurement stage, international consortia are positioning joint ventures to pool marine expertise, capital, and local content, bringing fresh competition to Romania's renewable energy industry. The interplay between incumbents and challengers drives technological diffusion, capital expenditure efficiency, and accelerates time-to-commission in support of national climate targets.

Romania Renewable Energy Industry Leaders

Energias de Portugal, S.A.

General Electric Company

Enel S.p.A.

Siemens Gamesa Renewable Energy S.A.

CEZ AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: OMV Petrom completed the acquisition of a 50% stake in Electrocentrale Borzesti, adding 1 GW of renewable capacity to its portfolio and strengthening its position in Romania's utility-scale solar market through a strategic partnership with a local developer.

- December 2024: PPC acquired a 629 MW renewable energy portfolio from Evryo Group for USD 768 million, marking Greece's largest renewable energy acquisition in Romania and demonstrating continued foreign investment in the market.

- November 2024: Romania adopted the National Energy Strategy 2025-2035, which mandates a 44% renewable energy penetration by 2035 and a complete coal phase-out by 2032, providing a long-term policy framework for market development.

- October 2024: OX2 sold a 99 MW wind project to Nala Renewables for approximately USD 234 million, with Vestas supplying the turbines, and the project is expected to achieve commercial operation in Q4 2024.

- September 2024: Rompetrol has announced a partnership search for a green hydrogen project at the Petromidia refinery, targeting industrial hydrogen demand and the integration of renewable energy for refining operations.

Romania Renewable Energy Market Report Scope

Renewable energy is the energy collected from renewable resources such as sunlight, wind, the movement of water, and geothermal heat that are naturally replenished.

The Romania renewable energy market is segmented by Type (Solar Energy, Wind, Hydropower, and Other Types). The report offers the market size and forecasts for Romania renewable energy market in megawatts (MW) for all the above segments.

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

What capacity is the Romania renewable energy market expected to reach by 2031?

It is forecast to grow from 17.73 GW in 2025 to 19.24 GW in 2026 and reach 28.96 GW by 2031.

Which technology is expanding fastest in Romania’s renewables mix?

Solar is projected to advance at a 14.26% CAGR between 2026 and 2031.

How large is the corporate PPA pipeline in Romania?

Multiple deals, including OMV Petrom’s 100 GWh solar PPA and Saint-Gobain’s 800 GWh wind contract, signal rapid expansion and rising industrial demand.

What policy supports offshore wind development in Romania?

Law 121/2024 offers a dedicated framework targeting 3–7 GW of Black Sea offshore capacity by 2035.

How is Romania financing grid modernization?

EUR 815 million from the EU Modernisation Fund underwrites high-voltage reinforcements and smart-grid upgrades that facilitate renewable integration.

Page last updated on: