SCARA Robot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

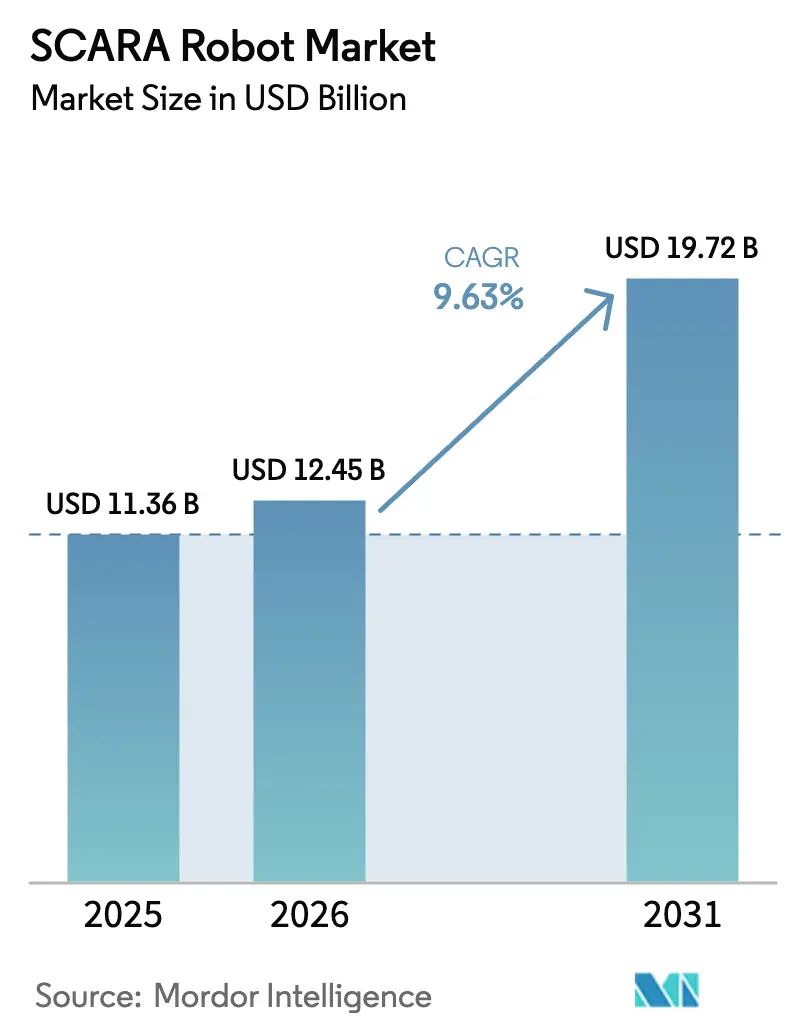

| Market Size (2026) | USD 12.45 Billion |

| Market Size (2031) | USD 19.72 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SCARA Robot Market Analysis by Mordor Intelligence

SCARA robot market size in 2026 is estimated at USD 12.45 billion, growing from 2025 value of USD 11.36 billion with 2031 projections showing USD 19.72 billion, growing at 9.63% CAGR over 2026-2031. Accelerated deployment in precision-critical assembly, rising electrification of mobility, and widening labor shortages have kept demand robust even as manufacturers confront tighter capex budgets. Intensifying reshoring initiatives in North America and Europe paired with ongoing factory expansions across Asia-Pacific further reinforce unit shipments. At the same time, software-centric value creation—most notably AI-driven path optimization and digital twin-based commissioning—has begun to influence purchasing criteria and push average selling prices upward. Together, these factors clarify why multi-industry end users increasingly view SCARA robots as the baseline automation platform rather than a niche technology within broader motion-control portfolios.

Key Report Takeaways

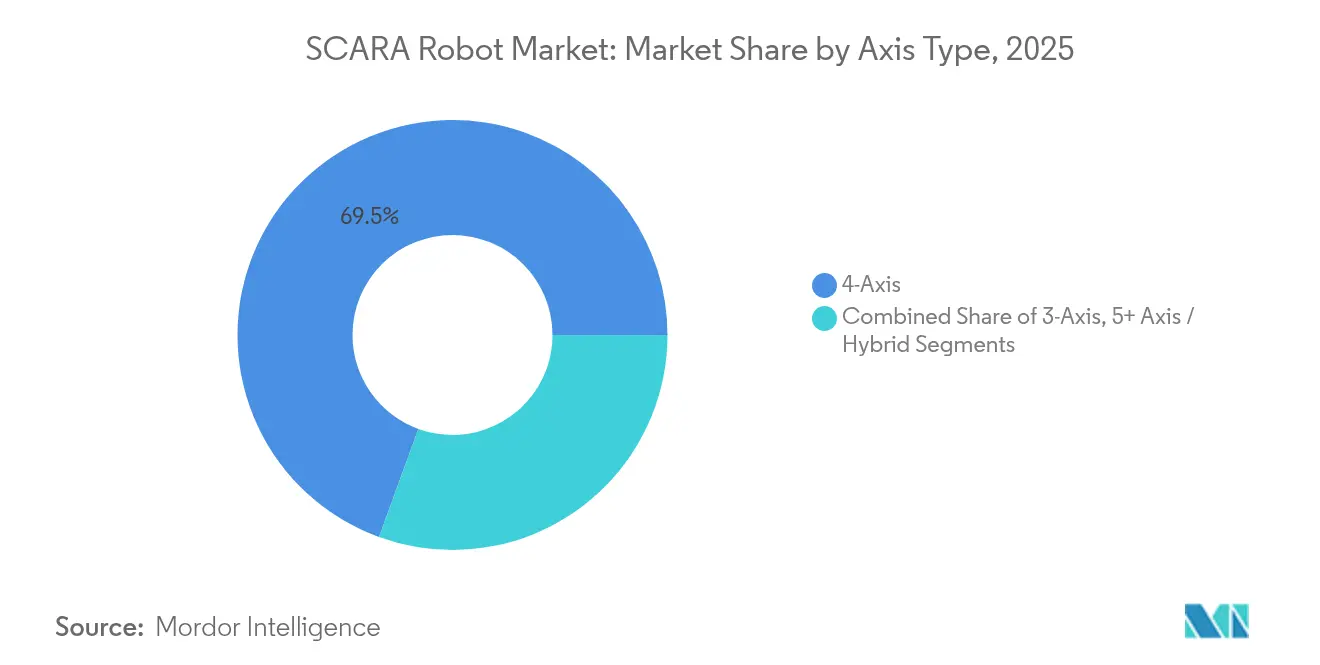

- By axis type, 4-Axis systems led with 69.45% of SCARA robot market share in 2025, while 5 + Axis/Hybrid units posted the fastest 13.78% CAGR to 2031.

- By payload capacity, the 5.01–10 kg bracket commanded 39.62% share of the SCARA robot market size in 2025; payloads above 20 kg are projected to expand at an 11.18% CAGR through 2031.

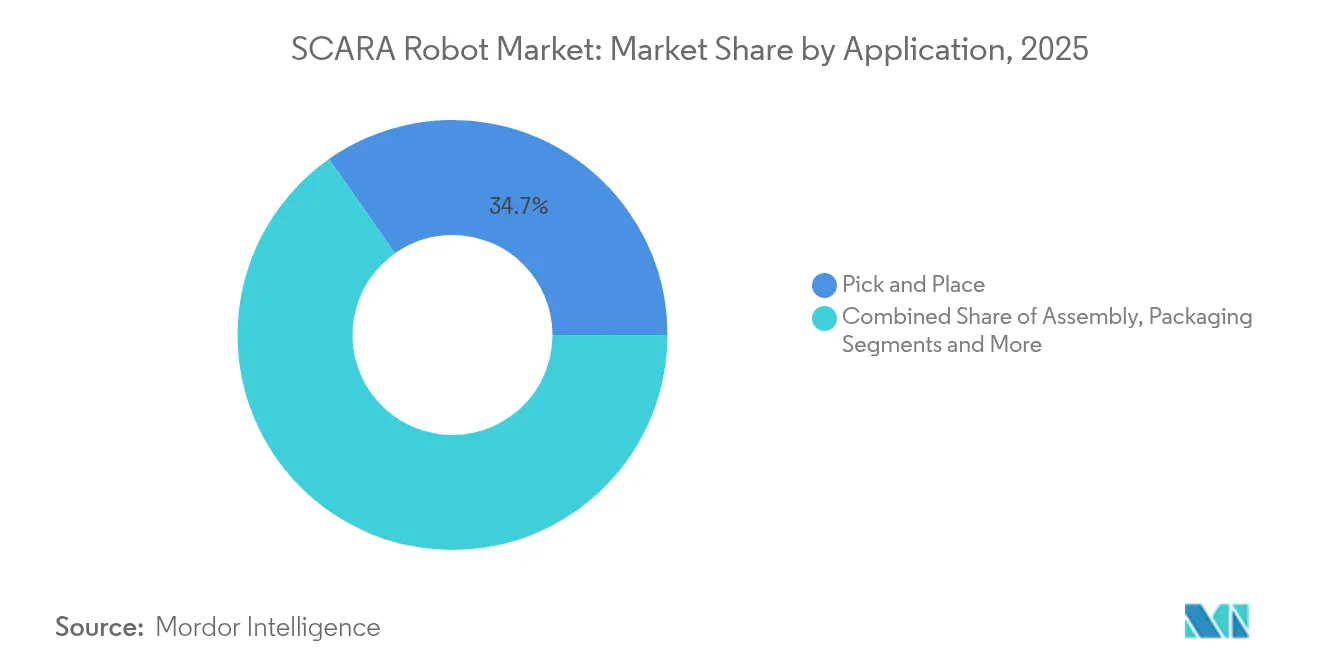

- By application, pick-and-place accounted for 34.74% of the SCARA robot market size in 2025, yet dispensing and soldering is advancing at 11.96% CAGR between 2026-2031.

- By industry vertical, electronics and semiconductor held 41.35% revenue share in 2025, whereas automotive EV power-train is set to grow at 14.62% CAGR.

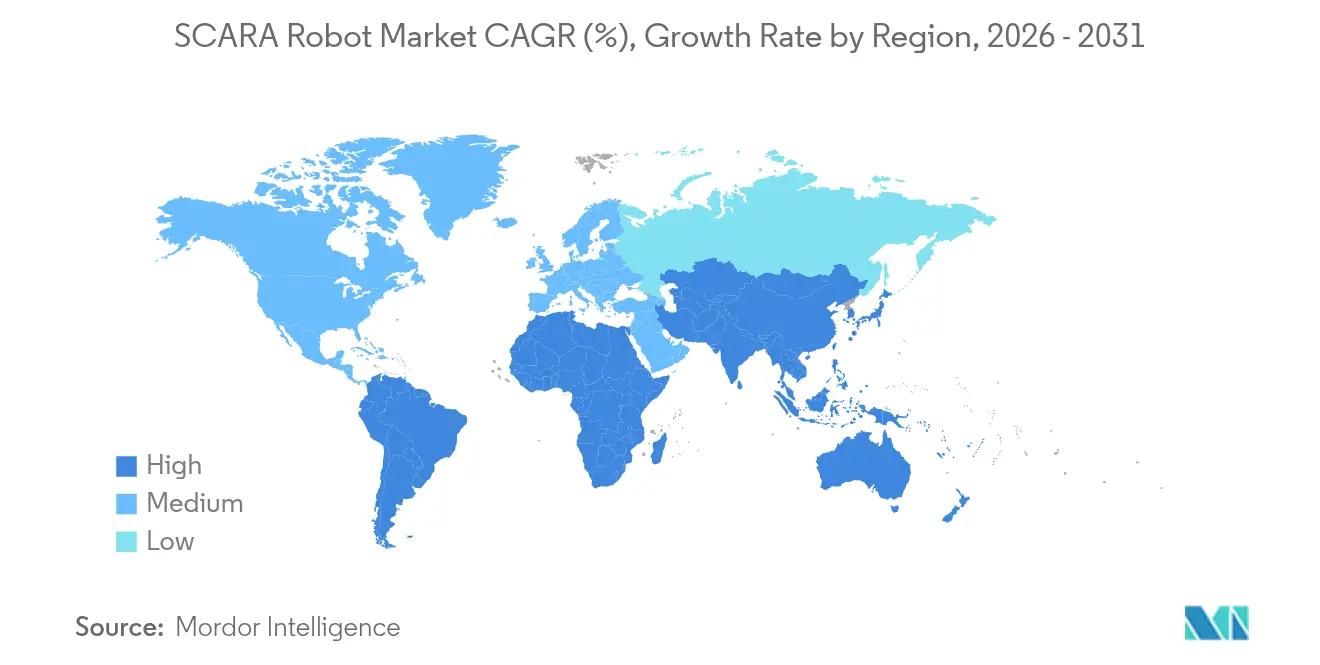

- By geography, Asia-Pacific captured 62.75% SCARA robot market share in 2025; South America records the fastest 9.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global SCARA Robot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of automation in manufacturing | +2.1% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Shrinking product life-cycles in electronics demanding flexible assembly lines | +1.8% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Escalating labor costs and skilled-worker scarcity in high-wage economies | +2.3% | North America and Europe, emerging in APAC urban centers | Long term (≥ 4 years) |

| Integration of SCARA arms with collaborative-robot safety standards | +1.4% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Demand from EV battery and module assembly operations | +1.6% | Global, with concentration in China, Europe, and North America | Short term (≤ 2 years) |

| SME-focused government subsidy programs for factory automation | +0.9% | National programs in Japan, North America, and select European countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Automation in Manufacturing

Manufacturers across automotive, medical device, and consumer-electronics domains scaled automation programs in 2024-2025, leveraging SCARA robots to bridge manual and fully autonomous processes. Seiko Epson quintupled domestic SCARA capacity from 15,000 to more than 30,000 units per year after investing JPY 4 billion (USD 27 million) in its Nagano plant, positioning Japan for export-led gains. [1]日刊工業新聞社, “Epson to Boost Domestic Robot Output Fivefold,” newswitch.jp Comparable expansion programs in China and Vietnam widened the installed base, which in turn catalyzed local supplier ecosystems for servo motors and drives. As vertical integration of hardware and software deepens, early adopters report shorter commissioning cycles and higher first-pass yields, reinforcing the automation flywheel that sustains the SCARA robot market.

Shrinking Product Life-Cycles in Electronics

Consumer electronics makers reduced average model refresh intervals to under 12 months in 2025. Delta Systems demonstrated the operational upside by programming more than 20 Epson SCARA robots to solder 2.25 million joints across 750,000 hour-meters annually, halving total production cost versus legacy fixtures. Similar quick-change philosophies are now diffusing into telecom gear and medical wearables, spurring demand for re-programmable robots with compact footprints that ease factory line re-configuration.

Escalating Labor Costs and Skilled-Worker Scarcity in High-Wage Economies

In 2024, Closure Systems International improved overall equipment effectiveness from 2.5% to 97.5% after deploying FANUC SCARA units, raising monthly output by 25% or roughly 30 million closures. Comparable gains across packaging, plastics and food processing highlight how rising wages and absenteeism swing ROI calculations decisively toward automation. With unemployment at multi-decade lows in North America and Western Europe, management teams prioritize reliable throughput over incremental labor savings, cementing long-term growth for the SCARA robot market.

Integration of SCARA Arms with Collaborative-Robot Safety Standards

ISO/TS 15066 compliance has enabled SCARA robots to function cage-free in mixed human-robot work cells. Precise Automation’s PF400 combines an integrated controller and force-limited design to minimize setup and floor-space needs, unlocking new use cases in life-science labs and boutique electronics assembly. End users cite 30-40% lower safety-infrastructure cost versus conventional guarding, converting previously marginal automation projects into financially viable deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX and total cost of ownership | -1.2% | Global, particularly affecting SMEs in emerging markets | Medium term (2-4 years) |

| Technical limitations in high-payload (>20 kg) SCARA designs | -0.8% | Global, with higher impact in automotive and heavy manufacturing | Long term (≥ 4 years) |

| Supply-chain risk for precision harmonic drives and servo motors | -1.1% | Global, with concentration in regions dependent on Asian suppliers | Short term (≤ 2 years) |

| Rising cybersecurity-compliance cost for connected shop-floor robots | -0.7% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX and Total Cost of Ownership

Government incentives have narrowed but not eliminated funding gaps for small-to-mid manufacturers. North Dakota’s Automate ND program approved USD 5 million across 18 projects in 2024, yet 24 proposals requesting USD 6.8 million remained unfunded, underscoring latent demand. Even where grants cover 30-40% of purchase price, firms still absorb integration, training, and maintenance outlays that stretch payback beyond board-mandated horizons, tempering full penetration of the SCARA robot industry.

Technical Limitations in High-Payload Designs

Horizontal-arm geometry becomes less rigid at payloads above 20 kg, forcing OEMs to thicken castings or slow cycle times. FANUC’s SR-20iA addresses part of the challenge by achieving 20 kg payload at 1,100 mm reach but still cannot match six-axis counterparts in off-axis torque. [2]FANUC America, “SR-20iA Product Sheet,” fanucamerica.com As heavier battery modules and drivetrain housings enter production, some automakers migrate to articulated or gantry platforms, capping the attainable ceiling for the SCARA robot market in heavy industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Axis Type: Advanced Configurations Drive Innovation

4-Axis platforms retained 69.45% share of the SCARA robot market in 2025 because they strike the optimal balance between cost and throughput. Demand for the traditional architecture continued through 2025 as electronics, plastics, and FMCG producers favored well-understood programming environments. Conversely, 5 + Axis/Hybrid units are projected to register a 13.78% CAGR, absorbing workloads that previously defaulted to six-axis arms yet requiring shorter takt times. Early adopters noted 15-20% faster cycle performance after adding the fifth rotary joint while preserving SCARA-level repeatability. Within this context the SCARA robot market size for advanced configurations should climb steadily as OEMs integrate AI-enabled vision packages that compensate for tighter tolerances in consumer device enclosures. 3-Axis variants, though modest sellers, remain entrenched in cost-sensitive pick-and-place stations.

As line complexity rises, integrators deploy mixed fleets in which four-axis units handle gross positioning and hybrid units conduct fine insertion. This orchestration, enabled by software synchronization, has cut changeover intervals by up to 60% in small-lot contract manufacturing. Simultaneously, demand for modular arm kits permits field retrofits that extend installed-base lifetime and keep 4-Axis market share resilient even while the technology mix shifts.

By Payload Capacity: Heavy-Duty Applications Reshape Demand

Segments between 5.01–10 kg captured the largest slice of SCARA robot market size in 2025 at 39.62% due to alignment with typical printed-circuit boards, smartphone sub-assemblies, and cosmetics packaging. The above-20 kg tier, however, is forecast to log 11.18% CAGR as automotive cell-to-pack assembly lines ramp globally. FANUC’s SR-20iA validated the economic case by consolidating what previously needed dual six-axis robots, thereby lowering cell-level investment outlays. The 10.01–20 kg bracket functions as a bridge, with adoption accelerating in tier-one auto components such as inverter casings requiring both heft and precision.

Payloads up to 5 kg stay relevant in die-bonding and micro-fluidics, where gentle handling offsets weight limitations. Collectively, these stratifications underscore a widening divergence between commodity units and high-specialization models, a pattern that should keep pricing rational as value migrates from raw payload toward software and sensing add-ons.

By Application: Dispensing Technologies Lead Growth

Pick-and-place retained 34.74% of 2025 volume, yet growth decelerated as maturity set in. In contrast, dispensing and soldering use cases are rising at 11.96% CAGR thanks to gigafactory build-outs that need micron-level adhesive and flux deposition. End users report first-pass yield improvements exceeding 10 percentage points after switching from manual fixtures to SCARA-based precision tracks, a saving critical in battery assembly where rework is cost-prohibitive. Assembly operations remained the backbone for white goods and power-tool manufacturing, while packaging gained renewed momentum from direct-to-consumer shipping formats.

Material-handling roles now often partner SCARA units with AMRs, enabling continuous flow between kitting and final assembly. Inspection and testing, still embryonic, benefits from sub-30 µm repeatability; semiconductor back-end lines in Taiwan deployed twin-camera SCARA cells that inspect 28-nm logic dies at 600 UPH, reducing off-line sampling.

By Industry Vertical: Automotive EV Transformation Accelerates

Electronics and semiconductor dominated revenue in 2025 with 41.35% share, anchored by smartphone, data-center, and memory fabs across China and South Korea. Yet automotive EV power-train is forecast to grow 14.62% annually, reshaping equipment supplier roadmaps. Volkswagen’s Foshan site validated scale by using 100 robots to assemble 300,000 battery packs annually. That performance triggered parallel investments by BYD, GM, and Stellantis, funneling new capital toward high-rigidity SCARA platforms.

Pharmaceuticals and medical devices preserve consistent demand as cGMP mandates favor closed-loop production. Food and beverage applications widened modestly under pressure to reduce allergen cross-contamination, leading dairy and bakery processors to swap manual conveyors for wash-down SCARA cells. Logistics and warehousing still largely rely on articulated or delta robots, yet proof points in e-grocery micro-fulfillment suggest future penetration for compact SCARA sorters. Renewable-energy components, particularly photovoltaic junction-box soldering, provide a nascent but strategic tailwind.

Geography Analysis

Asia-Pacific accounted for 62.75% of global shipments in 2025, anchored by China, Japan, and South Korea’s intertwined supply chains. Government smart-factory subsidies trimmed payback periods to under 18 months for mid-tier electronics subcontractors, cementing regional leadership in the SCARA robot market. Capital investment momentum continued into 2025 as Vietnam and India expanded export-oriented clusters, though talent shortages in servo integration remain a potential bottleneck.

Europe maintained a steady 16.85% revenue contribution, propelled by premium automotive and pharmaceutical projects. The continent’s stringent safety directives accelerated migration to collaborative-grade SCARA variants, allowing brownfield facilities to retrofit existing lines without perimeter fencing. Germany and Italy together accounted for two-thirds of regional demand, with battery megafactories in Sweden and Spain poised to lift volumes further.

North America experienced renewed interest linked to reshoring and the Inflation Reduction Act’s domestic-content rules. Tier-one suppliers shifted from CBUs imported from Asia toward on-shore sourcing, elevating the SCARA robot market size for U.S. integrators that offer turnkey MES connectivity. Nevertheless, small-batch contract manufacturers still cite integration costs as a barrier, suggesting upside if forthcoming tax credits become permanent.

South America delivered the fastest 9.94% CAGR outlook due chiefly to Brazil’s return to 25th place in global manufacturing rankings in 2024. Currency volatility and credit spreads, however, capped many projects at pilot scale. Meanwhile, Middle East and Africa remained under 2.90% of global volume; yet Saudi Arabia’s local-content mandates for consumer-electronics assembly and South Africa’s auto-export program provide green-shoots for gradual adoption.

Competitive Landscape

Market concentration remains moderate. FANUC, ABB, Epson, Yaskawa, and Stäubli collectively held an estimated 55-60% share in 2024, while domestic Chinese brands such as Estun and Efort expanded footprints in price-sensitive niches. FANUC reported a 16% decline in industrial robot sales in fiscal 2024, attributing weakness to cyclical electronics demand. [4]The Robot Report, “FANUC Industrial Robot Sales Drop 16%,” therobotreport.com Yaskawa’s robotics revenue dipped 9.5% to JPY 261.6 billion (USD 1.75 billion) in FY 2024 because of deferred spending in mainland China. ABB responded by announcing the spin-off of its USD 2.3 billion robotics division to sharpen strategic focus—an action confirmed in its April 2025 investor note.

Competition increasingly emphasizes software ecosystems. FANUC broadened its European presence by quadrupling Iberia facility space, adding training bays to shorten customer ramp-up time. Epson bundled Gyroplus vibration dampening with edge-AI controllers that self-tune acceleration curves, delivering cycle-time gains without larger motors. Smaller firms differentiate through vertical specialization: Precise Automation targets lab automation, while Mecademic positions nano-precision arms for optics assembly.

Supply-chain resilience became a strategic lever after harmonic-drive shortages in 2024 forced some OEMs to redesign gearboxes. Companies with in-house gear production or multiple qualified suppliers protected delivery schedules and captured share. Patent filings on obstacle-recognition algorithms and force-adaptive gripping suggest that the next frontier will combine perception and compliance rather than purely mechanical upgrades.

SCARA Robot Industry Leaders

Fanuc Corporation

ABB Ltd.

Yaskawa Electric Corporation

Mitsubishi Electric Corporation

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Japan’s Small and Medium Enterprise Agency opened the third round of its automation-investment subsidy program for SMEs.

- April 2025: ABB confirmed plans to spin off its robotics division as a separately listed company by Q2 2026.

- March 2025: Charge Robotics secured USD 22 million for its portable solar-farm assembly platform following a pilot with SOLV Energy.

- February 2025: FANUC Corporation completed the relocation and fourfold expansion of its FANUC IBERIA office in Sant Cugat del Vallès, Spain.

Global SCARA Robot Market Report Scope

The SCARA robots market encompasses the development, production, and sale of Selective Compliance Assembly Robot Arm (SCARA) robots, which are designed for high-speed, precise, and repetitive tasks. These robots are primarily used in industrial automation applications such as assembly, pick-and-place, packaging, and material handling. The market also includes related software, integration services, and advancements in robotics technology.

The SCARA Robot Market is segmented by axis type (3-axis, 4-axis, other axis type), payload capacity (up to 5 kg, 5.01 to 10 kg, above 10 kg), application (assembly, pick and place, packaging, material handling, inspection, other applications), industry vertical (electronics and semiconductor, automotive, pharmaceuticals, food and beverage, logistics and transportation, and other industry verticals) and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| 3-Axis |

| 4-Axis |

| 5+ Axis / Hybrid |

| Up to 5 kg |

| 5.01 - 10 kg |

| 10.01 - 20 kg |

| Above 20 kg |

| Assembly |

| Pick and Place |

| Packaging |

| Material Handling |

| Inspection and Testing |

| Dispensing and Soldering |

| Electronics and Semiconductor |

| Automotive |

| Pharmaceuticals and Medical Devices |

| Food and Beverage |

| Logistics and Warehousing |

| Renewable Energy Components |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN-5 | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Axis Type | 3-Axis | ||

| 4-Axis | |||

| 5+ Axis / Hybrid | |||

| By Payload Capacity | Up to 5 kg | ||

| 5.01 - 10 kg | |||

| 10.01 - 20 kg | |||

| Above 20 kg | |||

| By Application | Assembly | ||

| Pick and Place | |||

| Packaging | |||

| Material Handling | |||

| Inspection and Testing | |||

| Dispensing and Soldering | |||

| By Industry Vertical | Electronics and Semiconductor | ||

| Automotive | |||

| Pharmaceuticals and Medical Devices | |||

| Food and Beverage | |||

| Logistics and Warehousing | |||

| Renewable Energy Components | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN-5 | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the SCARA robot market by 2031?

The SCARA robot market is expected to reach USD 19.72 billion by 2031 on a 9.63% CAGR.

Which region currently leads the SCARA robot market?

Asia-Pacific led with 62.75% market share in 2025 owing to dense electronics and automotive supply chains.

Which application segment is growing the fastest?

Dispensing and soldering is forecast to expand at 11.96% CAGR as EV battery and semiconductor packaging lines demand high-precision adhesive and solder deposition.

Why are 5 + Axis/Hybrid SCARA robots gaining traction?

They deliver added dexterity close to six-axis performance while retaining SCARA-level speed, leading to a 13.78% CAGR outlook.

What is the main barrier for small manufacturers?

High upfront CAPEX and total cost of ownership remain the primary obstacles despite subsidy programs and leasing options.

How concentrated is the competitive landscape?

Top five vendors control slightly above 60% of global revenue, indicating moderate concentration with room for regional challengers.

Page last updated on: