Robot Vacuum Cleaners Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

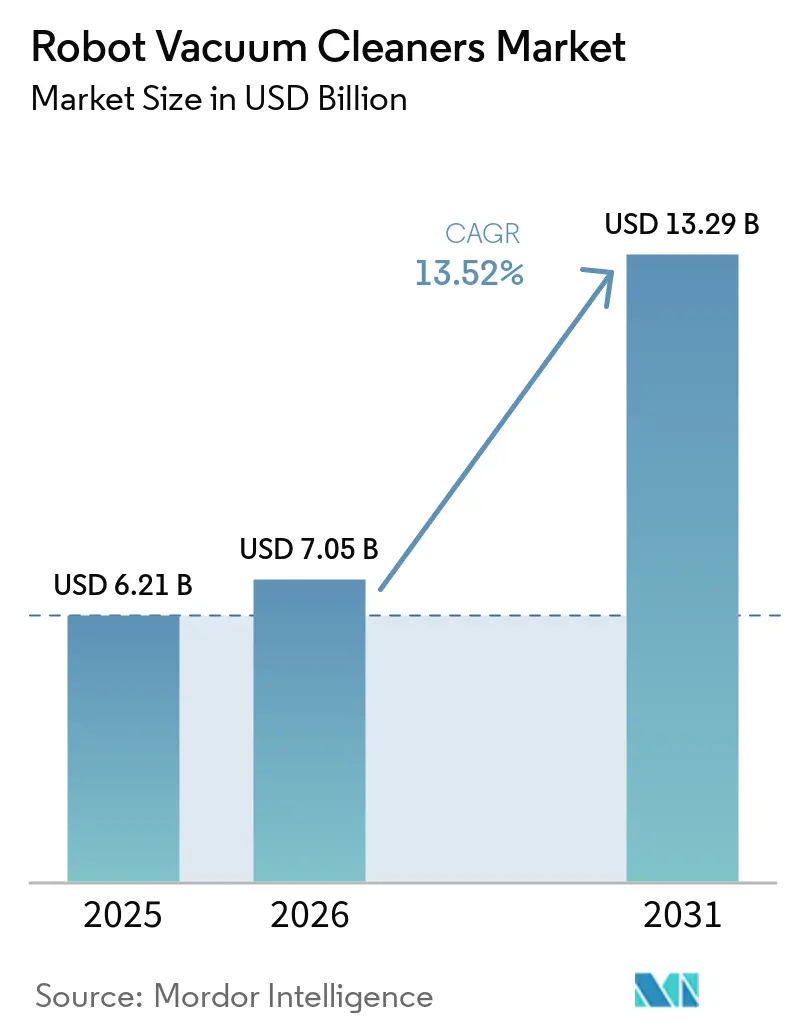

| Market Size (2026) | USD 7.05 Billion |

| Market Size (2031) | USD 13.29 Billion |

| Growth Rate (2026 - 2031) | 13.52% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robot Vacuum Cleaners Market Analysis by Mordor Intelligence

Robotic vacuum cleaners market size in 2026 is estimated at USD 7.05 billion, growing from 2025 value of USD 6.21 billion with 2031 projections showing USD 13.29 billion, growing at 13.52% CAGR over 2026-2031. Rising smart-home penetration, falling sensor and battery costs, and demographic shifts toward automated domestic care are the key forces behind this trajectory. Asia Pacific remains the pivotal growth engine as digitization programs spur infrastructure that supports always-connected appliances, while policy incentives in Japan and South Korea strengthen uptake in elderly-care settings. Component price deflation lets manufacturers embed LiDAR, AI navigation, and self-emptying docks in mid-range models, widening the consumer base. Competitive intensity is reshaped by Chinese vendors that leverage scale and rapid iteration to bring premium functionality to mainstream price tiers. Hospitality operators facing higher labor costs add an institutional demand layer that accelerates adoption across commercial real estate.

Key Report Takeaways

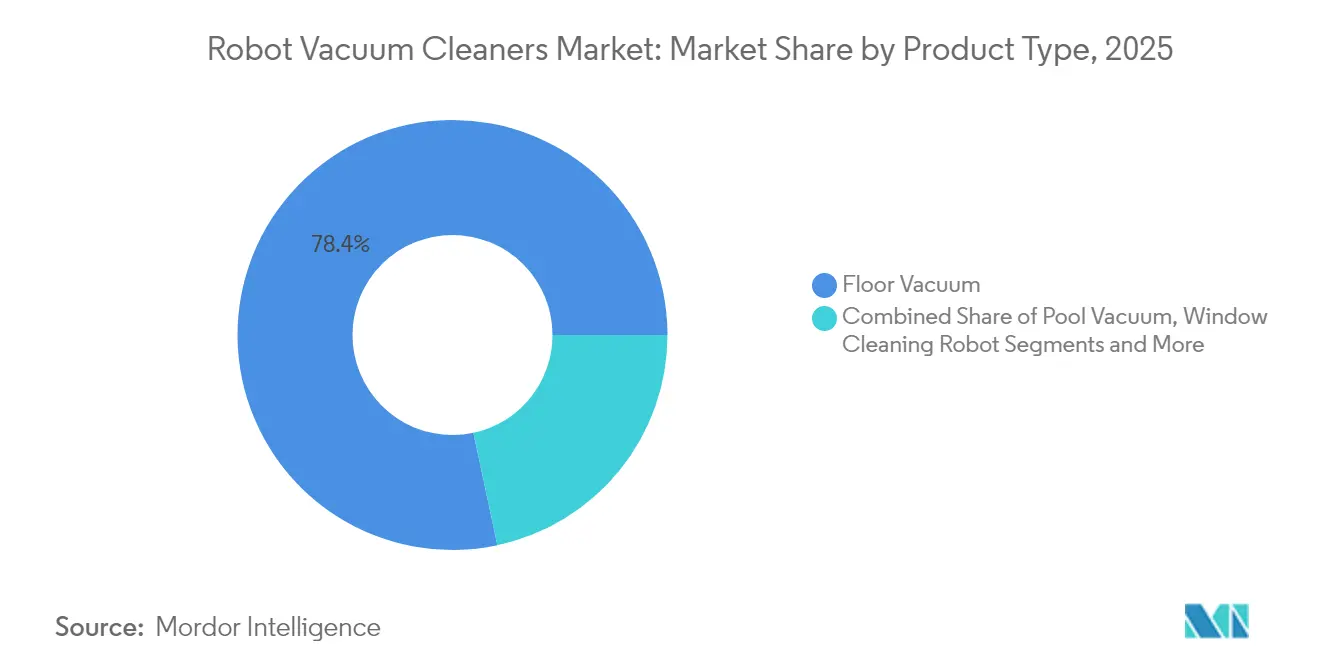

- By product type, floor vacuum models led with 78.35% revenue share in 2025; hybrid 2-in-1 systems are projected to expand at a 16.6% CAGR through 2031.

- By end-user, the residential segment accounted for 90.25% of the robotic vacuum cleaners market share in 2025, while the commercial hospitality segment is advancing at a 14.95% CAGR to 2031.

- By battery type, lithium-ion packs commanded 93.70% share in 2025; high-density variants are growing at 13.55% CAGR.

- By connectivity, smart-connected units captured a 67.60% share in 2025 and are rising at a 16.05% CAGR.

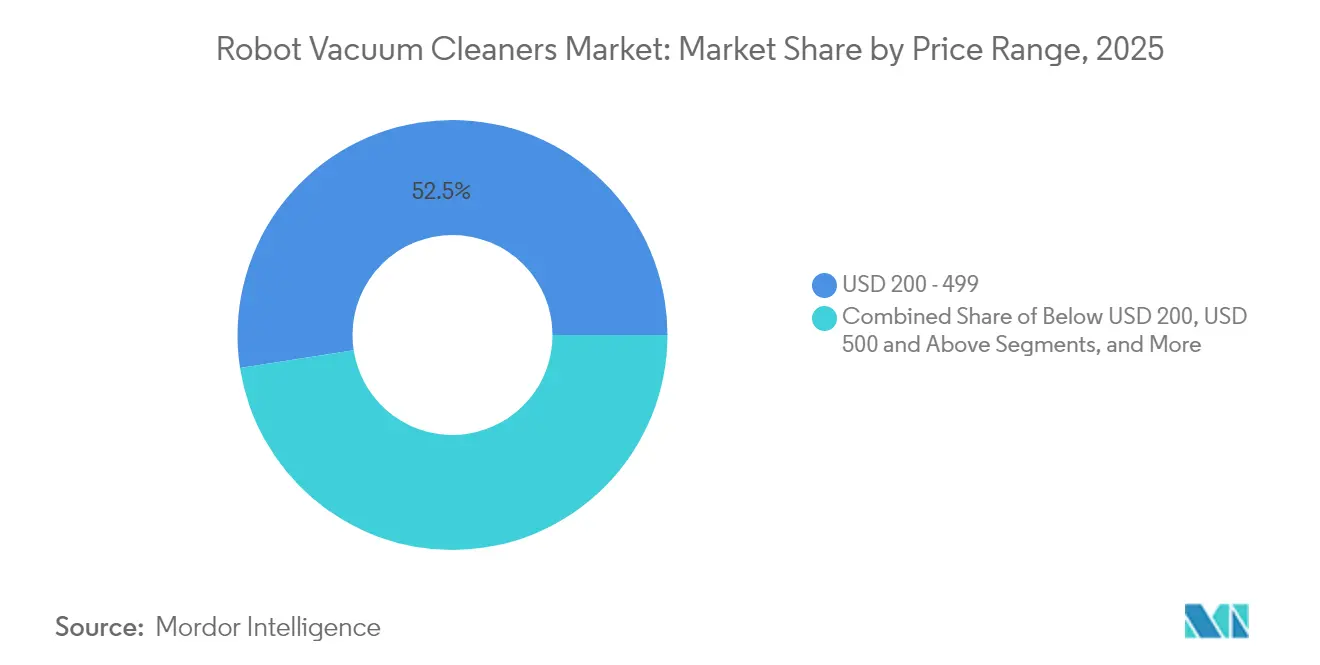

- By price range, the USD 200-499 bracket held 52.45% of the robotic vacuum cleaners market size in 2025, whereas premium USD 500+ models are climbing at a 14.35% CAGR.

- By distribution channel, online marketplaces retained a 64.10% share in 2025; brand e-commerce sites are expanding at an 17.65% CAGR.

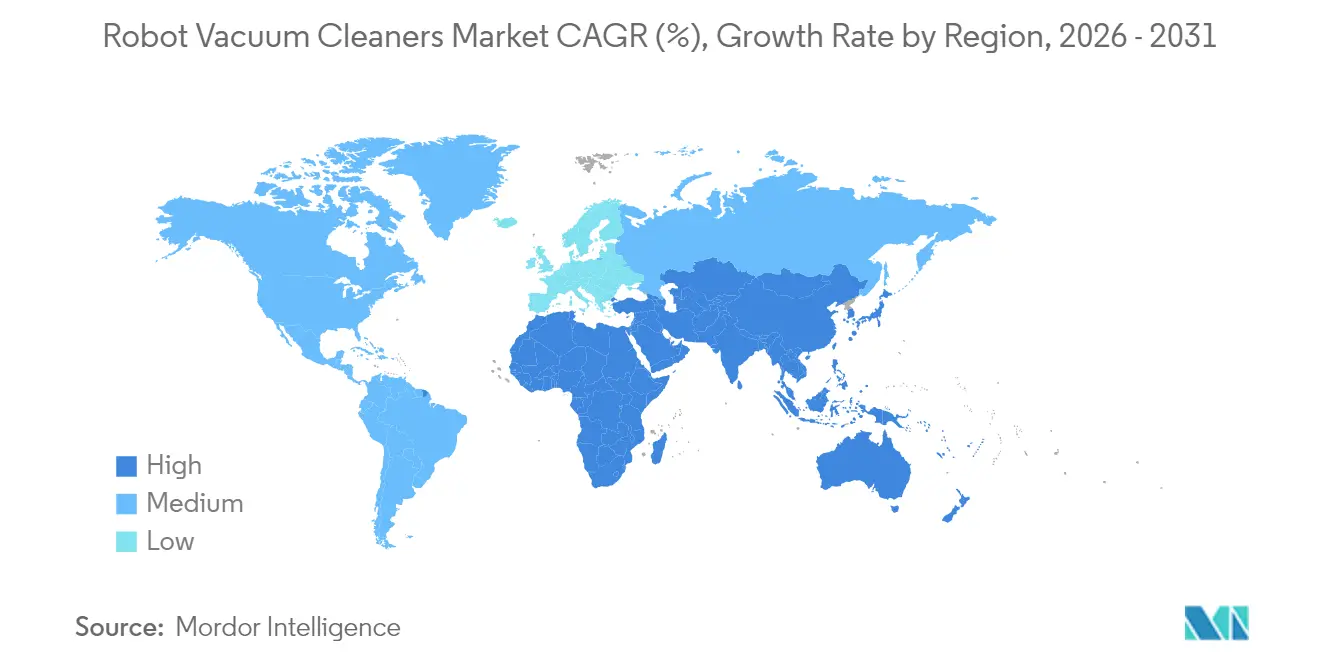

- By region, Asia Pacific led with 40.70% share in 2025; the Middle East is the fastest-growing geography at 18.3% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robot Vacuum Cleaners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of smart-home ecosystems in Asia | +3.20% | Asia Pacific, spillover to North America | Medium term (3-4 years) |

| Rapid price declines in Li-ion and sensor components | +2.80% | Global | Short term (≤2 years) |

| Growing demand for hybrid vacuum-mop models in Europe | +1.90% | Europe, spillover to North America | Medium term (3-4 years) |

| Hospitality sector’s pivot in Middle-East luxury hotels | +1.50% | Middle East, spillover to Asia Pacific | Medium term (3-4 years) |

| Government incentives for elderly-care tech in Japan and South Korea | +1.20% | Japan and South Korea | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Smart-Home Ecosystems in Asia

Voice-assistant compatibility is now a baseline requirement, and regional adoption rates exceed 10% in advanced economies. Brands localize features such as remote security monitoring and AI-driven room mapping to meet hygiene and safety preferences. Samsung and LG models tuned for domestic use illustrate how local incumbents defend share against Chinese challengers while aligning with national elderly-care programs.

Rapid Price Declines in Li-ion and Sensor Components

Volume manufacturing of LiDAR modules, cameras, and control ICs lowers production costs, pushing retail prices from USD 2,000-5,000 in 2024 toward USD 500-1,500 by 2030. [1]Dong Haiwei, “Bringing Robots Home: The Rise of AI Robots in Consumer Electronics,” arXiv, arxiv.orgChinese vendors translate vertical integration into aggressive pricing, while incumbents respond by bundling premium navigation and self-cleaning docks in mid-tier lines. Lower barriers enhance penetration among first-time buyers and fuel upgrade cycles among existing owners.

Growing Demand for Hybrid Vacuum-Mop Models in Europe

Mixed-floor housing stock and strict hygiene norms make multifunctional robots attractive. Heated-water mopping, automated cloth washing, and sanitization deliver end-to-end hard-floor maintenance. EU sustainability rules that prioritize product longevity and battery recyclability favor these all-in-one formats. [2]European Parliament & Council, “Regulation (EU) 2023/1542 on Batteries,” eur-lex.europa.eu

Hospitality Sector’s Pivot to Autonomous Cleaning in Middle-East Luxury Hotels

Luxury operators report 50% lower hard-floor upkeep costs after deploying commercial-grade robots with 3-liter dust bins and corridor-optimized navigation. Continuous operation during off-peak hours elevates cleanliness standards and staff productivity, encouraging broader adoption across regional hotels and adjacent commercial venues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low penetration in deep-pile carpet regions (US Midwest) | -1.40% | North America | Short term (≤2 years) |

| Battery-safety recalls impacting brand trust in EU | -2.10% | Europe | Short term (≤2 years) |

| High import tariffs on smart appliances in South America | -0.80% | South America | Medium term (3-4 years) |

| Inter-brand software interoperability gaps | -1.30% | Global | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Low Penetration of High-Suction Models in Deep-Pile Carpet Regions

Deep-pile carpets demand higher airflow and specialized brushes that raise cost and power consumption. Premium units rated at 20,000 Pa address the performance gap but remain unaffordable for price-sensitive households. Traditional uprights persist in these markets, limiting robotic uptake until high-performance features scale down in cost.

Battery-Safety Recalls Impacting Brand Trust in EU

Fire incidents triggered multiple recalls of cordless vacuums and aftermarket battery packs, prompting regulatory scrutiny and heightened consumer caution. [3]U.S. Consumer Product Safety Commission, “CPSC Warns Consumers to Immediately Stop Using INSE Cordless Stick Vacuums,” cpsc.gov EU mandates on battery traceability, thermal safeguards, and recyclability increase compliance costs but also provide a quality signal for brands that meet the standard.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Models Drive Innovation

Floor vacuum units held a 78.35% share in 2025, anchoring the robotic vacuum cleaners market through proven efficacy across common floor types. Hybrid 2-in-1 systems, however, are advancing at a 16.6% CAGR as consumers seek single devices that vacuum and mop. ECOVACS’ DEEBOT T30, with tangle-free rollers and heated mop pads, exemplifies the design philosophy that merges convenience with deeper cleaning.

Hybrid penetration improves especially in Europe where mixed wood-tile layouts prevail. Innovative models with edge-to-edge brush reach and auto-wash stations position the robotic vacuum cleaners market as a gateway to wider smart-home automation. Such versatility attracts upgrade buyers eager for devices that handle multiple chores without manual intervention.

By End-User: Commercial Hospitality Accelerates

Residential buyers still represent 90.25% of the robotic vacuum cleaners market size in 2025 due to mass-market pricing and app-based controls that cater to busy households. Commercial hospitality is the fastest-rising customer set, growing 14.95% annually as hotels mitigate labor shortages with 24/7 autonomous floor care. Units purpose-built for corridor geometry and larger debris hoppers underscore this shift.

Office and retail facilities gradually follow, deploying fleets managed from cloud dashboards that optimize routing and maintenance. The resulting data insights on traffic patterns and cleaning intensity evolve robots from single-function tools into integrated facility-management assets, deepening their value proposition.

By Battery Type: High-Density Li-ion Dominates

Lithium-ion technology accounts for 93.70% of 2025 shipments, reflecting superior energy density, recharge speed, and weight-to-capacity ratio. High-density cells that enable 150-minute run times are growing at 13.55% CAGR, positioning manufacturers to extend coverage area without enlarging form factors. Safety recalls, however, place renewed emphasis on cell chemistry, thermal management, and smart charging safeguards.

Nickel-metal hydride alternatives linger only in low-cost imports and remain in steady decline. Forthcoming EU rules mandating traceable sourcing and recyclability are likely to accelerate a shift toward next-generation solid-state chemistries, although commercial availability remains beyond the current forecast period.

By Connectivity: Smart Integration Accelerates

Smart-connected models held 67.60% share in 2025 and are climbing 16.05% annually as Wi-Fi modules and voice-assistant APIs become inexpensive to embed. Cloud-hosted maps, scheduling, and firmware updates enhance device longevity, strengthening the robotic vacuum cleaners market. Matter protocol adoption assures interoperability across major ecosystems, easing buyer concerns about platform lock-in.

Non-connected variants persist mainly in entry-level tiers or in regions with spotty broadband. As IoT costs continue to fall, manufacturers will likely standardize connectivity even in budget segments, making remote diagnostics and predictive maintenance table stakes.

By Price Range: Premium Segment Surges

The USD 200-499 bracket commanded 52.45% of the robotic vacuum cleaners market size in 2025, balancing affordability with useful feature sets. Premium USD 500+ devices advance at 14.35% CAGR, buoyed by AI vision, self-empty stations, and wet-mess detection that justify higher outlays. Hardware cost deflation feeds trickle-down of flagship capabilities to mid-range SKUs, expanding the addressable audience without cannibalizing top-tier demand.

Budget models under USD 200 face reliability and performance trade-offs that limit appeal in developed economies. Nonetheless, they create a low-risk entry point in emerging markets, from which users can progress to higher-spec units as incomes rise.

By Distribution Channel: Brand E-Commerce Accelerates

Online marketplaces held 64.10% share in 2025, supported by extensive SKU variety and user reviews. Direct-to-consumer webstores are the fastest-growing outlet at 17.65% CAGR as brands pursue margin expansion and direct ownership of customer data. Bundled consumables, extended warranties, and app-based accessory subscriptions fortify recurring revenue streams.

Specialty retailers retain relevance among buyers seeking physical demos or same-day pickup, though limited shelf space constrains model breadth. Hybrid click-and-collect models may help brick-and-mortar channels defend traffic as online sales proliferate.

Geography Analysis

Asia Pacific anchored 40.70% of global demand in 2025, leveraging domestic manufacturing ecosystems that compress lead times and costs. Chinese producers refine designs at home before exporting, while South Korean incumbents differentiate on AI features tailored to safety-conscious users. Government grants for elder-care robots translate into sustained volume, embedding robots into daily routines.

The Middle East is the fastest-growing region at 18.3% CAGR through 2031 as luxury hotels operationalize 24/7 cleaning to offset staffing gaps. Dust-laden climates elevate demand for high-capacity filtration, and premium property owners adopt robotic fleets both for performance and brand differentiation.

North America and Europe exhibit high household awareness yet confront distinct regulatory dynamics. EU battery and AI legislation heightens compliance costs but reinforces consumer trust in brands that meet stringent safety thresholds. In Latin America, tariffs of 20-60% on imported appliances incentivize regional assembly strategies that could shift value-chain investment over the forecast window.

Competitive Landscape

Eight of the ten largest brands are now Chinese, underscoring a power shift from legacy Western incumbents. Scale advantages in component procurement let these firms release annual model refreshes that fold in edge-AI processors, self-washing docks, and climbing mechanisms faster than rivals. Legacy leaders concentrate on reliability and data security to preserve share among risk-averse buyers.

Commercial partnerships illustrate diversification paths. Nilfisk teamed with LionsBot to launch autonomous scrubbers, bridging industrial cleaning expertise with consumer-grade robotics know-how. Component vendors also influence competitive dynamics; battery suppliers that achieve higher energy density without safety compromises become critical allies in premium-segment battles.

European compliance regimes around algorithmic transparency favor manufacturers equipped to certify data governance, potentially reshuffling competitive hierarchies. As premium functionality seeps into mid-range price bands, differentiation will rely less on suction specs and more on lifetime service models, accessory ecosystems, and software-delivered upgrades that extend product relevance.

Robot Vacuum Cleaners Industry Leaders

iRobot Corporation

Haeir Group Corporation

Neato Robotics Inc.

Ecovacs Robotics Co. Ltd

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Anker Innovations enters robotic lawn-care with Eufy mowers featuring computer-vision obstacle avoidance.

- May 2025: Kanagawa Prefecture opens applications for subsidies up to 1 million yen per robot under its elderly-care technology program.

- April 2025: US CPSC warns consumers to stop using INSE cordless vacuums due to fire hazards from battery overheating.

- January 2025: Dreame Technology showcases X50 Ultra able to climb 6 cm thresholds and deliver 20,000 Pa suction.

Global Robot Vacuum Cleaners Market Report Scope

Robotic vacuum cleaners are designed to clean autonomously without human control. North America occupies the largest market share, while Asia-Pacific is expected to be the fastest-growing market. The growing adoption of Contract Cleaning Service solutions across commercial facilities, hospitality spaces, and office environments is further supporting demand for robotic vacuum cleaners. Robots used for professional cleaning-related activities - including floor cleaning, window and wall cleaning, sewers, tank, tube, and pipe cleaning, and hull cleaning (aircraft, vehicles, ships, etc.), among others, are considered in the segment scope.

The Robot Vacuum Cleaners Market is segmented by By Type (Floor Cleaner, Pool Cleaner, Window Cleaner), End-user (Commercial, Residential), and Geography (North America (United States, and Canada), Europe (Germany, United Kingdom, France, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, and Rest of Asia Pacific), and Rest of the World). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Floor Vacuum |

| Pool Vacuum |

| Window Cleaning Robot |

| Hybrid 2-in-1 Vacuum-Mop |

| Residential |

| Commercial |

| Lithium-ion |

| Nickel-Metal Hydride |

| Smart-Connected (Wi-Fi / Voice-Assist) |

| Non-Connected |

| Below USD 200 |

| USD 200 - 499 |

| USD 500 and Above |

| Online Marketplaces |

| Brand E-commerce |

| Specialty Stores |

| Mass Retailers and Hypermarkets |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Nordics | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific |

| By Product Type | Floor Vacuum | |

| Pool Vacuum | ||

| Window Cleaning Robot | ||

| Hybrid 2-in-1 Vacuum-Mop | ||

| By End-User | Residential | |

| Commercial | ||

| By Battery Type | Lithium-ion | |

| Nickel-Metal Hydride | ||

| By Connectivity | Smart-Connected (Wi-Fi / Voice-Assist) | |

| Non-Connected | ||

| By Price Range | Below USD 200 | |

| USD 200 - 499 | ||

| USD 500 and Above | ||

| By Distribution Channel | Online Marketplaces | |

| Brand E-commerce | ||

| Specialty Stores | ||

| Mass Retailers and Hypermarkets | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the robotic vacuum cleaners market?

The market is valued at USD 7.05 billion in 2026 and is projected to reach USD 13.29 billion by 2031 at a 13.52% CAGR.

Which region leads global demand?

Asia Pacific holds 40.70% of global sales, supported by rapid smart-home adoption and government incentives for domestic robotics.

What product segment is growing fastest?

Hybrid vacuum-mop models are expanding at a 16.6% CAGR as consumers favor multifunctional cleaning.

How are battery safety issues being addressed?

Regulators now mandate stricter thermal safeguards and recyclability, and brands are integrating smarter battery-management systems to improve safety.

Why are hotels adopting robotic vacuums?

Luxury properties report up to 50% reductions in hard-floor maintenance costs and improved staff productivity after deploying autonomous cleaners.

Which price band sells the most units?

Models priced between USD 200 and USD 499 represent 52.45% of 2025 unit sales, balancing affordability with popular smart-home features.

Page last updated on: