Roaming Tariff Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

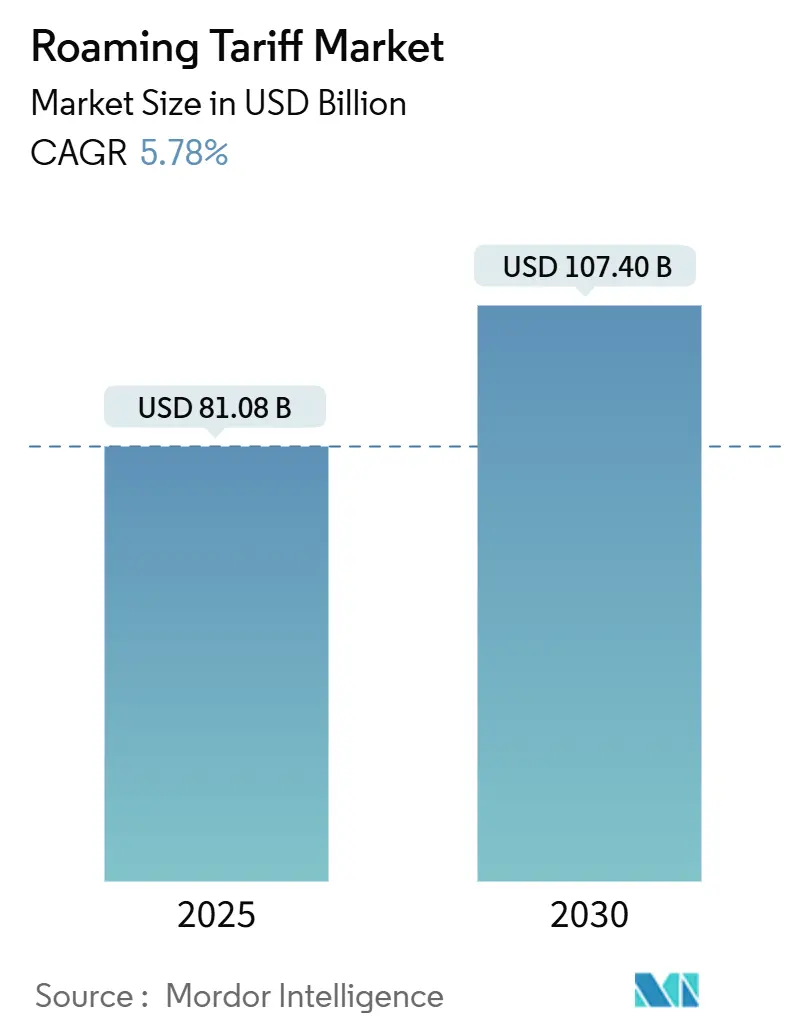

| Market Size (2025) | USD 81.08 Billion |

| Market Size (2030) | USD 107.40 Billion |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

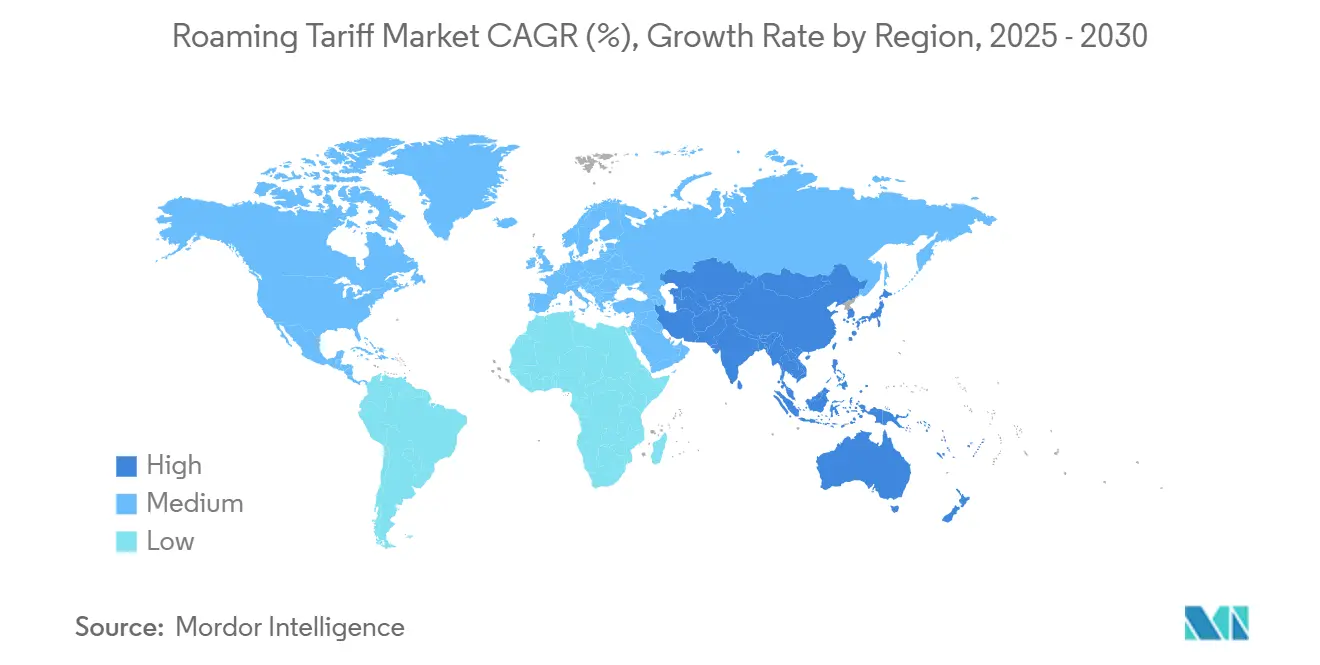

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

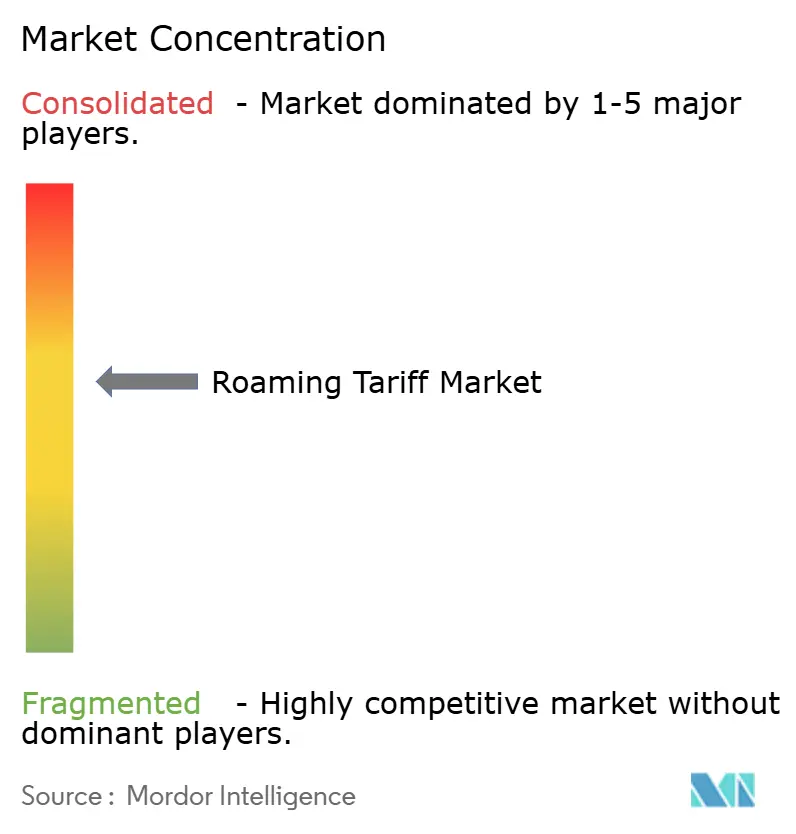

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Roaming Tariff Market Analysis by Mordor Intelligence

The roaming tariff market size was USD 81.08 billion in 2025 and is projected to expand at a 5.78% CAGR, reaching USD 107.40 billion by 2030. Renewed international travel, steady 5G roll-outs, and rising enterprise IoT connections are driving revenue even as traditional voice usage erodes. Operators are capturing higher average revenue per user through premium data-roaming tiers, unlimited regional passes, and network-slicing offers that meet always-connected traveler expectations.[1]GSMA, “Mobile Economy Asia Pacific 2024,” gsma.com At the same time, bilateral wholesale price wars and retail tariff caps, especially in Europe, continue to squeeze margins, compelling carriers to consolidate networks and renegotiate roaming partnerships. New eSIM aggregators and satellite-link alliances are also reshaping competitive dynamics by lowering entry barriers and broadening coverage footprints. The interplay of these forces positions the roaming tariff market for steady but disciplined growth over the forecast horizon.

Key Report Takeaways

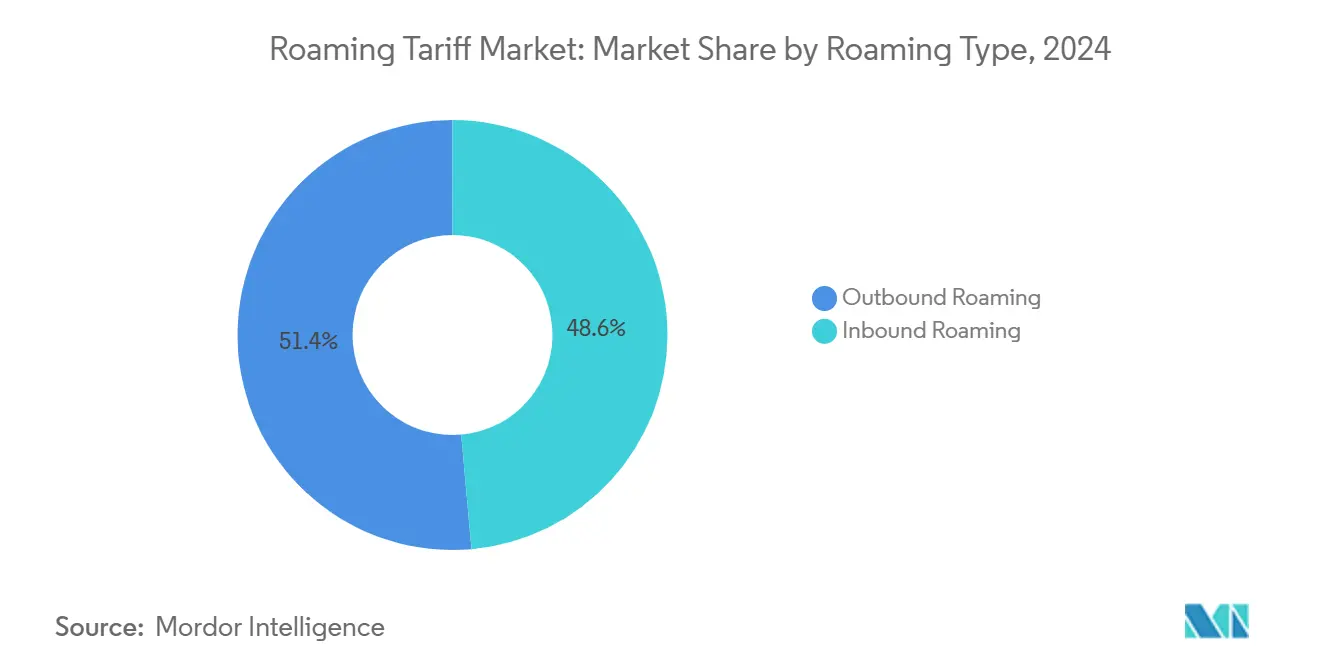

- By roaming type, outbound services led with a 51.4% roaming tariff market share in 2024, while inbound services are forecast to grow at a 7.3% CAGR to 2030.

- By service type, voice accounted for 65.4% of the roaming tariff market size in 2024; data services are advancing at a 6.3% CAGR through 2030.

- By user type, the enterprise segment held 21.9% of the roaming tariff market size in 2024 and is set to expand at a 6.8% CAGR by 2030.

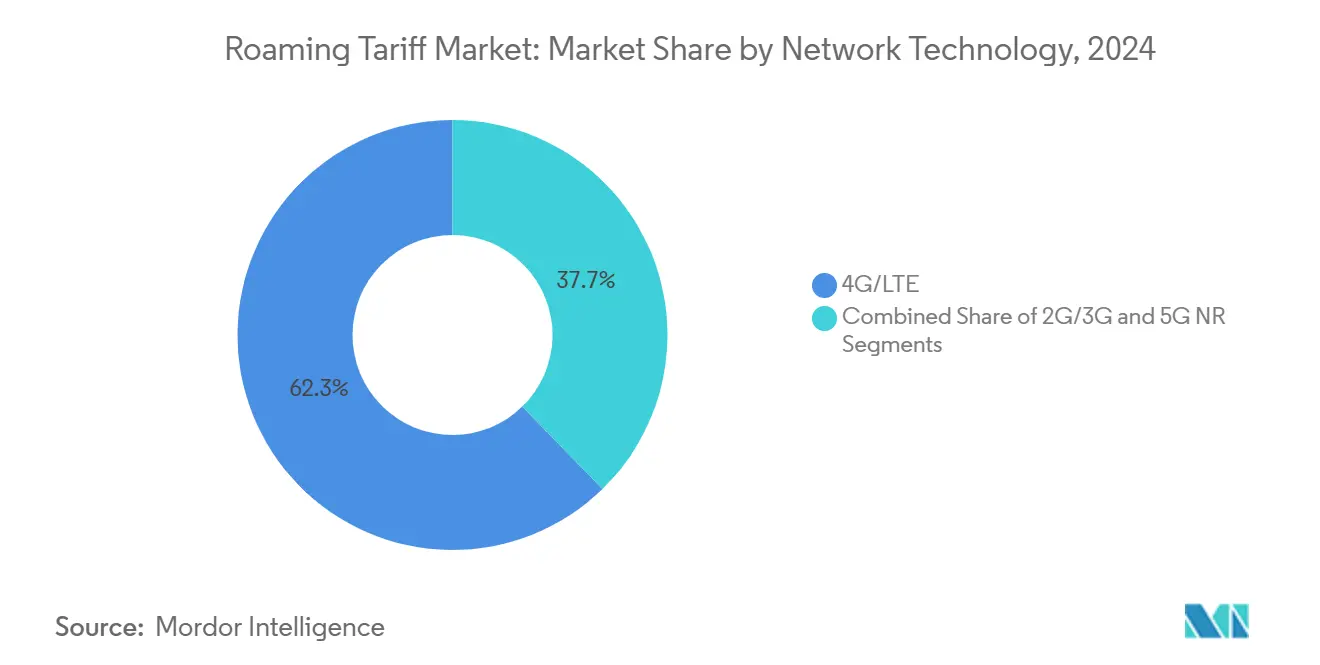

- By network technology, 4G/LTE secured 62.3% of the roaming tariff market share in 2024; 5G NR is poised for a 6.5% CAGR to 2030.

- By geography, North America captured 38.2% of the roaming tariff market size in 2024, whereas Asia-Pacific is recording a 5.8% CAGR in the same period.

Global Roaming Tariff Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in international travel and tourism post-COVID-19 | +1.8% | Global, strongest in Europe and Asia-Pacific | Short term (≤2 years) |

| Expansion of cross-border eSIM adoption | +1.2% | North America and Western Europe | Medium term (2–4 years) |

| 5G roll-outs enabling premium data-roaming ARPU | +0.9% | Developed markets | Long term (≥4 years) |

| Regulatory push toward “Roam-Like-at-Home” in emerging regions | +0.7% | Latin America, GCC, ASEAN | Medium term (2–4 years) |

| Growth of IoT roaming connections in logistics | +0.5% | Global supply corridors | Long term (≥4 years) |

| Aviation-based inflight roaming partnerships | +0.3% | Major aviation routes | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in international travel and tourism post-COVID-19

International arrivals nearly matched 2019 levels in 2024, lifting roaming volumes for both leisure and enterprise travelers. European carriers registered double-digit increases in outbound data usage after the rebound in summer tourist flows. Gulf destinations, led by the UAE and Saudi Arabia, have pledged USD 350 billion in tourism infrastructure outlays by 2030, ensuring sustained inbound roaming demand. Operators responded with unlimited regional passes that align with longer vacation stays, shifting away from pay-per-day bundles. Business travel resumed earlier, delivering higher ARPU and spurring tailored enterprise roaming platforms that bundle voice, data, and device management tools. Overall, the travel upturn adds positive pressure to the roaming tariff market by widening the active user base and encouraging premium usage tiers.

Expansion of cross-border eSIM adoption

Travel eSIM activations are on track to exceed 400 million profiles by 2028 as digital marketplaces simplify purchase and onboarding. Panasonic Avionics introduced seamless inflight Wi-Fi roaming that authenticates a passenger’s existing mobile subscription, a milestone that demonstrates the frictionless potential of eSIM technology. Lufthansa Group’s partnership with eSIM Go shows how airlines are integrating connectivity into the traveler journey. For incumbent carriers, eSIM creates new wholesale channels but also threatens retail margins if travelers opt for third-party profiles. Accordingly, major operators now market own-brand travel eSIMs and explore subscription bundles that integrate terrestrial and non-terrestrial coverage to retain customer stickiness.

5G roll-outs enabling premium data-roaming ARPU

Operators in 25 countries support commercial 5G roaming, with the number of supported destinations rising 60% in 2024 alone. Early adopters charge up to 30% price premiums for 5G daily passes because median speeds often top 350 Mbps for roamers in Gulf hubs. IoT roaming revenue, heavily tied to logistics and industrial automation, is projected to double to USD 2.2 billion by 2029, and 5G devices will account for more than 40% of that revenue despite representing fewer than 10% of connections. China’s four national carriers jointly launched 5G cross-network roaming, demonstrating how shared infrastructure can close coverage gaps while sustaining premium ARPU. Europe’s first 5G standalone international link, by Vodafone and A1, proved that network slicing can follow a subscriber across borders while maintaining service-level attributes. These innovations pave the way for differentiated pricing based on latency, bandwidth, and application priority.

Regulatory push toward “Roam-Like-at-Home” in emerging regions

Regional blocs are drafting frameworks that echo the EU’s zero-surcharge model. ECOWAS’s free roaming initiative now covers Ghana, Togo, and Benin, allowing travelers to use local rates for 30 days. The GCC adopted retail and wholesale caps that mirror European ceilings, aiming to stimulate intra-regional commerce and tourism. Latin American regulators are reviewing similar proposals, though fragmented political alignment slows execution. The ITU’s “Let’s Roam the World” toolkit provides policy templates that underscore transparency, bill shock prevention, and minimum quality-of-service metrics.[2]ITU, “International Mobile Roaming Portal,” itu.int Such frameworks tend to lower per-unit revenue but spur higher usage, forcing operators to strike a balance between volume growth and margin preservation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying bilateral wholesale price wars | -1.4% | North America and Europe | Short term (≤2 years) |

| Regulatory caps on retail roaming tariffs | -0.8% | Europe, GCC | Medium term (2–4 years) |

| Rising adoption of free public Wi-Fi/OTT apps | -0.6% | Urban centers worldwide | Long term (≥4 years) |

| Security concerns over permanent roaming IMSIs | -0.3% | Brazil and China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Intensifying bilateral wholesale price wars

Carriers with cross-border footprints increasingly negotiate near-cost wholesale rates to secure traffic, pressuring smaller operators. T-Mobile’s average North American wholesale data cost fell from USD 181 per GB in 2014 to single-digit figures in 2025, a trajectory mirrored in Europe where data caps will slide to EUR 1.00 per GB by 2027. Canadian rulings banning exclusivity clauses widened access for regional networks but compressed large-carrier margins. Consolidation, such as T-Mobile’s move to buy UScellular, fuels operator concerns that bargaining power is concentrating in a few hands. These pressures reduce unit prices, making scale and efficient traffic management essential for profitability in the roaming tariff market.

Rising adoption of free public Wi-Fi/OTT messaging apps

Wi-Fi OpenRoaming gained traction, with 25% of surveyed enterprises already deploying seamless onboarding architectures that bypass cellular authentication. Messaging applications like WhatsApp and Telegram handle an estimated 80% of cross-border person-to-person traffic for millennials, eroding traditional voice and SMS usage. Indian operators argue that cheap mobile data reduces Wi-Fi relevance, yet in many mature markets municipal networks now deliver gigabit-class speeds that tempt travelers to forego tourist SIMs. Operators counter through hybrid cellular-Wi-Fi packages and value-added identity services, but substitution risk remains a headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Roaming Type: Inbound demand accelerates while outbound remains core

Inbound roaming generated a modest revenue share in 2024 but will outpace outbound at a 7.3% CAGR to 2030, propelled by aggressive tourism campaigns across the GCC, Southeast Asia, and parts of Africa. The growth of the market was mainly due to new bilateral deals that reduced wholesale charges to entice foreign visitors. Operators in destination markets package connectivity with hotel, airline, and entertainment bundles, raising stickiness. Outbound services still dominate current revenue because developed-country subscribers travel frequently; however, margin dilution from retail price caps forces carriers to push higher-tier daily passes and unlimited bundles to defend profitability.

The roaming tariff market benefits from the symbiosis of outbound scale and inbound momentum. As emerging economies’ middle classes travel more, outbound volumes diversify beyond Europe and North America. Destination operators reciprocate by improving network quality, implementing eSIM tourist plans, and offering digital onboarding at airports. Together, these moves elevate overall usage days per traveler, expanding the roaming tariff market.

By Service Type: Data ascends as voice plateaus

Voice remained the single-largest component with 65.4% revenue share in 2024, yet its contribution is shrinking annually. The roaming tariff market size for data services is projected to grow significantly by 2030, closing in on voice even under conservative traffic assumptions. Unlimited social media streaming, cloud gaming, and real-time translation apps all demand low-latency bandwidth that commands price premiums.

Operators are pivoting: they now bundle voice over IP minutes within data passes, effectively monetizing voice through bytes rather than legacy circuits. SMS endures because one-time passwords for digital banking and ticketing remain critical. Meanwhile, network APIs expose quality-on-demand layers that enterprises buy for remote collaboration and AR field support. These shifts consolidate data’s central role in the roaming tariff market.

By User Type: Enterprise accounts unlock premium uptake

The consumer segment contributed 78.1% of the roaming tariff market size in 2024. Enterprise travelers represented a significant share of premium daily-pass revenue due to stringent reliability and security needs. Managed mobility contracts increasingly include real-time spend analytics, eSIM provisioning at scale, and network-slice service-level agreements. Cellular IoT endpoints, ranging from pallet trackers to connected medical devices, will leap from 3.8 billion in 2024 to 6.4 billion by 2029, embedding roaming into the supply chain fabric.

Consumer users continue to dominate in absolute numbers, yet they shop aggressively for price transparency. Loyalty programs now integrate roaming perks; for example, airline status tiers grant discounted unlimited data passes. This bifurcation spurs tiered service design: high-margin enterprise traffic funds infrastructure, while broad consumer bases secure volumes that underpin wholesale negotiating leverage.

By Network Technology: 5G gains ground on established 4G base

4G/LTE supplied 62.3% of traffic revenue in 2024, underpinned by ubiquitous coverage and stable roaming agreements. Still, the roaming tariff market size linked to 5G NR is predicted to grow by a forecast 6.5% annual growth and premium pricing. Early 5G roamers report median speeds four times faster than 4G in leading Gulf corridors, encouraging carriers to monetize high-definition content and enterprise AR use cases.

RedCap launches in the United States illustrate how slimmed-down 5G profiles deliver efficient IoT connectivity at lower cost than full-bandwidth options. Legacy 2G/3G sunsets free up spectrum, yet some developing regions retain fallback networks for voice-centric roamers. The transition phase, therefore, demands multi-mode devices and intelligent steering engines that choose the optimal bearer per session, safeguarding experience while maximizing ARPU.

By Pricing Model: Unlimited plans close in on bundle leadership

Bundles comprising set daily or weekly allowances controlled 55.4% of revenue in 2024, offering predictability that curbs bill shock. Unlimited plans, however, will rise at a 6.0% CAGR through 2030 as heavy data users embrace simplicity, even at higher flat fees. Three UK’s extension of inclusive roaming to 92 countries at GBP 7 per day epitomizes the shift toward easy-to-understand tariffs.

Pay-as-you-go endures among occasional travelers and prepaid subscribers but faces steady decline where regulators mandate spend caps and real-time usage alerts. Price model evolution thus tilts the roaming tariff market toward all-you-can-use structures that better align operator returns with escalating consumption.

Geography Analysis

North America contributed 38.2% of global revenue in 2024 on the back of dense business corridors linking the United States, Canada, and Mexico. The region’s roaming tariff market size benefits from high average revenue per line, often above USD 5 per day for enterprise passes, and from expansive 5G coverage that lets carriers command premiums. Regulatory scrutiny over wholesale practices has intensified; the CRTC now enforces open access to national networks, compelling incumbents to renegotiate rates and adjust margin expectations. Mergers such as T-Mobile’s acquisition of UScellular bolster rural reach but face pushback from small carriers wary of diminished reciprocal arrangements.

Asia-Pacific is the fastest-growing arena, advancing at a 5.8% CAGR through 2030. China, Japan, South Korea, and Australia all support international 5G roaming, and Bridge Alliance’s eSIM platform connects 34 member networks, simplifying regional travel. Unique mobile subscribers in the region topped 1.8 billion in 2024, and governments allocate multi-billion-dollar funds to attract inbound visitors whose connectivity demands can now be met instantly via QR-code eSIM activation in arrival halls. These factors position the roaming tariff market for sustained momentum across the Pacific Rim.

Europe remains structurally important despite the “Roam-Like-at-Home” policy that removes retail surcharges inside the bloc. Wholesale caps will fall further in 2027, yet carriers compensate via greater volumes and by bundling value-added services. Vodafone’s impending integration of Three UK promises GBP 11 billion in network investment to enhance 5G coverage and drive new wholesale revenue streams. Eastern European operators eye GCC travelers and collaborate with Gulf carriers on hub-to-hub premium passes. Meanwhile, the Middle East and Africa achieve some of the highest 5G roaming speeds globally, enabling operators to target affluent pilgrims and business travelers with ultra-premium data tiers that solidify the region as a revenue bright spot.

Mordor Intelligence provides coverage of the roaming tariff market across other key regional markets, including Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The roaming tariff market features moderate fragmentation, with international groups, Vodafone, Orange, Deutsche Telekom, AT&T, and China Mobile, holding commanding but not monopolistic positions. Vodafone recorded 5.1% FY25 service revenue growth after pruning low-return assets and reinforcing core markets in Turkey and Egypt. Deutsche Telekom’s agreement with OQ Technology extends its footprint into satellite NB-IoT, highlighting the race to cover remote assets seamlessly. AT&T, Verizon, and T-Mobile lead North America in 5G roaming readiness, using scale to negotiate favorable bilateral rates and market high-capacity passes.

Consolidation shapes regional plays: Telefónica’s 16-year RAN-sharing deal with Digi Spain secures long-term wholesale revenue while facilitating Digi’s shift from MVNO to MNO status. Vodafone Germany’s roaming partnership with 1&1 guarantees nationwide 5G availability for the newcomer, injecting fresh competition without new macro towers.[3]Vodafone Group, “Vodafone and 1&1 Launch Roaming Partnership in Germany,” vodafone.com Bridge Alliance and Ericsson’s CAMARA API collaboration reveals a pivot toward monetizing network capabilities beyond connectivity, offering low-latency location and quality tiers to app developers.

Operators increasingly bundle roaming with cybersecurity, spend analytics, and device-management features to preserve margins. Wholesale marketplaces leverage blockchain smart contracts for settlement efficiency, cutting invoicing cycles from months to days. The entry of satellite-cellular hybrids further intensifies rivalry, as space-enabled MVNOs promise single-profile global coverage that could siphon traffic from terrestrial incumbents unless agreements align incentives.

Roaming Tariff Industry Leaders

Vodafone Group Plc

Orange S.A.

Telefónica S.A.

Deutsche Telekom AG (T-Mobile)

Verizon Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vodafone completed its merger with Three UK, pledging GBP 11 billion (USD 14.54 billion) in 5G upgrades.

- June 2025: T-Mobile US posted USD 20.8 billion in Q1 2025 wireless service revenue, up 2.7% YoY.

- April 2025: Panasonic Avionics debuted seamless inflight Wi-Fi roaming on Korean Air with SK Telink.

- March 2025: Ericsson and Aduna partnered with Bridge Alliance on CAMARA network APIs.

Global Roaming Tariff Market Report Scope

| Inbound Roaming |

| Outbound Roaming |

| Voice |

| SMS |

| Data |

| Consumer |

| Enterprise |

| 2G / 3G |

| 4G / LTE |

| 5G NR |

| Pay-as-you-Go |

| Bundled Daily/Weekly Pass |

| Unlimited/Flat-Rate Plans |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Roaming Type | Inbound Roaming | ||

| Outbound Roaming | |||

| By Service Type | Voice | ||

| SMS | |||

| Data | |||

| By User Type | Consumer | ||

| Enterprise | |||

| By Network Technology | 2G / 3G | ||

| 4G / LTE | |||

| 5G NR | |||

| By Pricing Model | Pay-as-you-Go | ||

| Bundled Daily/Weekly Pass | |||

| Unlimited/Flat-Rate Plans | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the roaming tariff market size in 2025?

It stood at USD 81.08 billion and is on track to reach USD 107.40 billion by 2030 at a 5.78% CAGR.

Which region currently leads in roaming revenue?

North America accounts for 38.2% of global revenue thanks to dense cross-border business travel and high ARPU levels.

How fast is the enterprise segment growing?

Enterprise roaming revenue is expanding at a 6.8% CAGR, reflecting renewed corporate travel and surging IoT deployments.

Will 5G overtake 4G in roaming traffic?

5G roaming is projected to grow at 6.5% annually and surpass USD 35 billion in revenue by 2030, narrowing the gap with 4G.

How are unlimited plans affecting roaming tariffs?

Unlimited flat-rate plans, growing at 6.0% CAGR, simplify pricing and boost usage, gradually eroding bundle dominance.

What impact do regulatory caps have on operators?

Caps compress per-unit margins but grow volumes, forcing carriers to optimize wholesale terms and diversify premium services.

Page last updated on: