MicroRNA Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 6.96 Billion |

| Growth Rate (2026 - 2031) | 15.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

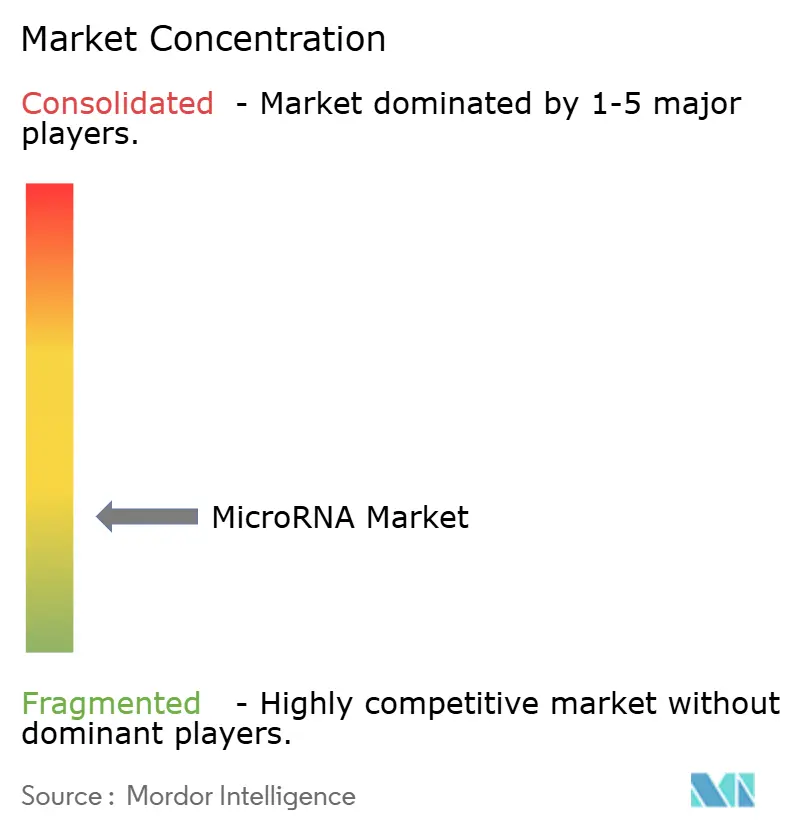

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MicroRNA Market Analysis by Mordor Intelligence

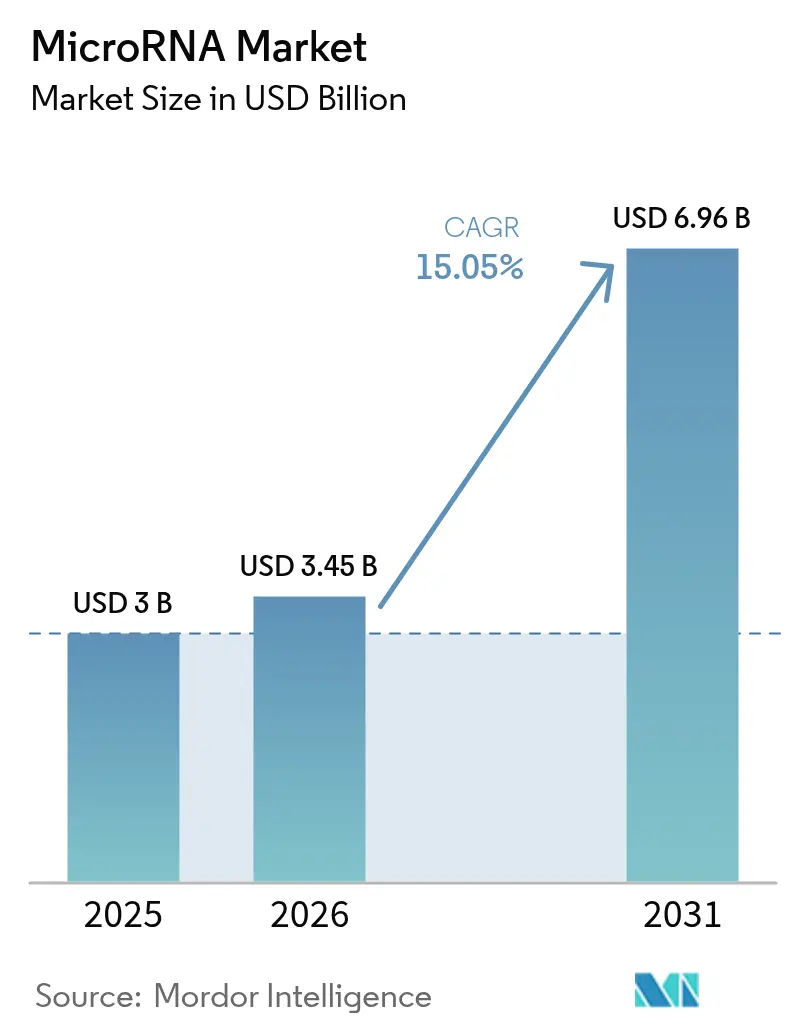

The micro RNA market size was valued at USD 3.00 billion in 2025 and estimated to grow from USD 3.45 billion in 2026 to reach USD 6.96 billion by 2031, at a CAGR of 15.05% during the forecast period (2026-2031). Momentum comes from growing adoption in precision diagnostics, expanding therapeutic pipelines, and the steady rollout of biomarker-based test menus in core laboratory settings. Regulatory fast-track incentives for oligonucleotide drugs, deeper venture funding, and continuous upgrades in next-generation sequencing (NGS) and real-time PCR (RT-qPCR) platforms are catalyzing demand across both high-income and emerging economies. Platform convergence, where a single instrument can interrogate DNA, RNA, and proteins, is pushing customers toward integrated multi-omic workflows. Meanwhile, the democratization of liquid biopsy and exosome-derived microRNA assays is enabling earlier disease detection and broadening the end-user base beyond research settings. Delivery challenges for therapeutics and lingering off-target toxicity concerns remain the primary technical hurdles, yet these restraints are opening whitespace opportunities for companies specializing in novel nanoparticle vehicles and AI-guided sequence design.

Key Report Takeaways

- By product & service, the Services segment led with 47.78% of micro RNA market share in 2025, while Kits & Reagents are projected to expand at a 15.92% CAGR through 2031.

- By technology, Real-Time PCR dominated with 38.25% revenue share in 2025; Microarray platforms show the highest forecast CAGR at 15.54% to 2031.

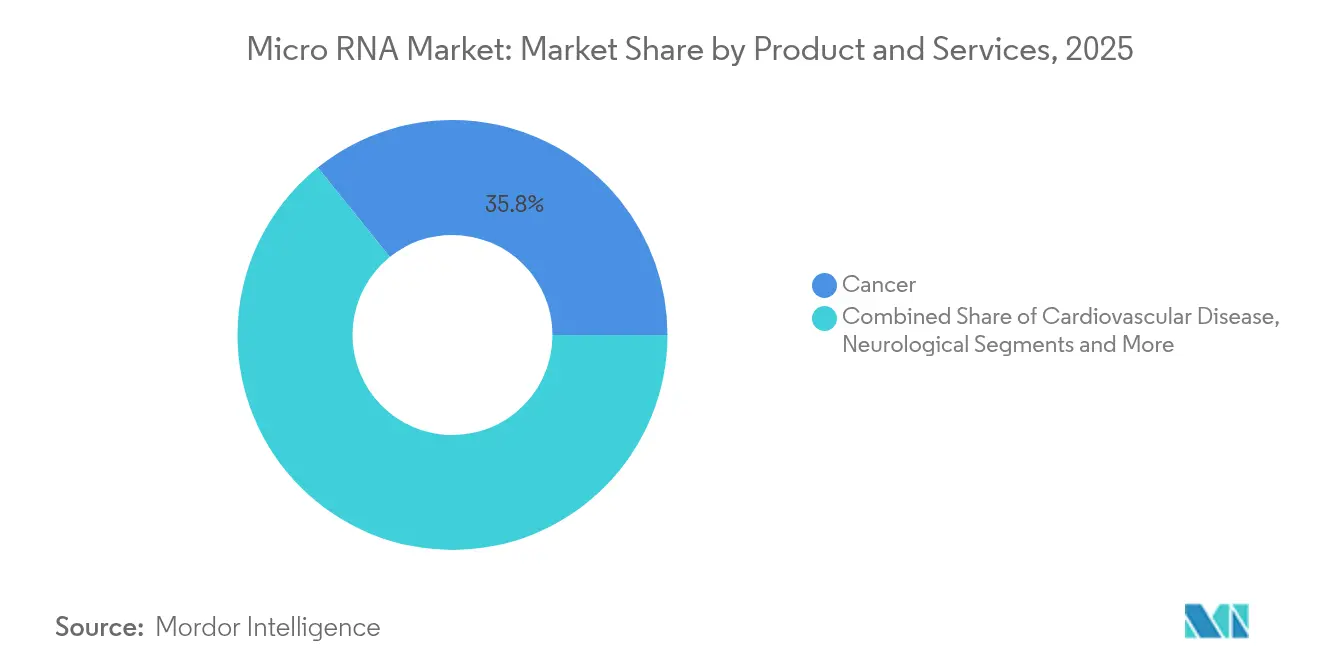

- By application, cancer captured 35.78% share of the micro RNA market size in 2025, whereas infectious diseases applications are poised for the fastest 16.02% CAGR.

- By end-user, biopharmaceutical companies held 39.86% of micro RNA market size in 2025; diagnostic centers are the quickest-growing user group at a 16.28% CAGR.

- By geography, North America commanded 41.72% micro RNA market share in 2025; Asia–Pacific is projected to advance at 16.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global MicroRNA Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & oncological diseases | +3.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of precision molecular diagnostics & liquid biopsy | +2.8% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Intensifying R&D funding and strategic partnerships in miRNA therapeutics | +2.1% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Advancements in NGS & RT-qPCR platforms for small-RNA analysis | +1.9% | Global, with technology hubs in North America, Europe, Asia | Short term (≤ 2 years) |

| Regulatory fast-track / orphan-drug incentives for oligonucleotide drugs | +1.7% | North America & EU primarily | Medium term (2-4 years) |

| AI-enabled multi-omics pipelines and exosome-based miRNA assays | +1.4% | Technology-advanced regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of chronic & oncological diseases

Chronic illnesses continue to rise, with cancer alone causing 10 million deaths in 2024, amplifying demand for microRNA-based diagnostics and therapeutics [1]World Health Organization, “Cancer Fact Sheet,” who.int. Emerging evidence shows microRNAs such as miR-4454 yielding an AUC of 0.889 for type 2 diabetes detection, spotlighting metabolic disease potential. Cardiovascular research indicates microRNAs regulating myocardial injury post-coronary microembolization, pointing to treatments beyond existing care. This widening disease spectrum reduces dependence on oncology and supports preventive medicine initiatives across aging populations in high-income countries and lifestyle-driven morbidity in emerging markets.

Rapid adoption of precision molecular diagnostics & liquid biopsy

Liquid biopsy assays using microRNA signatures now reach 90% sensitivity across nine cancers while maintaining 99% specificity. Non-invasive tests fill screening gaps for low-incidence yet deadly tumors such as pancreatic cancer; urinary miR-210-3p achieves 82.8% sensitivity and 74.3% specificity for early detection [2]Marta Gómez-Martínez et al., “Diagnostic Utility of miR-4454 in Type 2 Diabetes,” BMC Endocrine Disorders, biomedcentral.com. Diagnostic centers integrate these assays alongside protein markers and imaging, accelerating routine adoption. AI-enhanced signature discovery shortens analysis time and boosts accuracy, granting first-mover advantage to laboratories embedding machine learning into data interpretation.

Intensifying R&D funding and strategic partnerships in miRNA therapeutics

Venture and strategic investments reached new highs in 2024-2025. ARTHEx Biotech secured EUR 42 million to progress ATX-01, an antimiR targeting microRNA-23b for myotonic dystrophy; the asset carries orphan-drug designations on both sides of the Atlantic [3]ARTHEx Biotech, “ARTHEx Raises EUR 42 Million Series B,” arthxbiotech.com. Korro Bio and Novo Nordisk structured an RNA-editing alliance valued at up to USD 530 million, blending platform specialization with global clinical infrastructure. Such deals de-risk development, compress timelines, and signal large-cap pharma confidence in next-generation oligonucleotides.

Advancements in NGS & RT-qPCR platforms for small-RNA analysis

Illumina’s push into clinical multi-omics promises 18% annual growth for its sequencing installed base over the decade. LNA-enhanced RT-qPCR kits quantify microRNAs from 1 pg inputs, broadening sample compatibility. Cost-efficient microarrays gain renewed traction, with circular RNA panels delivering higher sensitivity than RNA-seq for specific targets. CRISPR-Cas12a coupled with hybridization chain reaction achieves 1 pM detection within 15 minutes, suiting point-of-care settings.

Regulatory fast-track / orphan-drug incentives for oligonucleotide drugs

US FDA and EMA continue to grant priority pathways that shorten review cycles for rare-disease oligonucleotide therapeutics, cutting both time and cost to market. In tandem with advanced manufacturing guidance, these incentives underpin robust clinical pipelines across oncology, neurology, and metabolic disorders, reinforcing revenue visibility for platform companies that satisfy quality-by-design expectations.

AI-enabled multi-omics pipelines and exosome-based miRNA assays

AI accelerates biomarker discovery by integrating genomic, transcriptomic, and proteomic datasets, producing interpretable microRNA panels tailored to disease biology. Parallel interest in exosome-derived cargo improves signal stability, allowing room-temperature transport and broadening access in low-resource settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delivery & stability challenges for miRNA therapeutics | -2.1% | Global, particularly affecting therapeutic applications | Long term (≥ 4 years) |

| Safety and off-target toxicity concerns | -1.8% | Global, with stricter regulatory scrutiny in developed markets | Medium term (2-4 years) |

| Patent expiry of first-generation miRNA assay technologies | -1.3% | North America & Europe primarily, affecting established players | Short term (≤ 2 years) |

| Batch-to-batch variability in synthetic miRNA reagents | -0.9% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Delivery & stability challenges for miRNA therapeutics

Achieving tissue-specific delivery beyond the liver remains elusive. Lipid nanoparticles degrade rapidly in circulation, driving up dosage and toxicity. Single microRNAs modulate multiple pathways, demanding precision engineering to avoid unintended physiology. Research now pivots to ionizable polymer carriers and bioreducible linkers seeking enhanced pharmacokinetics. The technical gap delays broad systemic indications but spurs innovation among startups offering next-generation vehicles.

Safety and off-target toxicity concerns

Historical setbacks, such as MRX34’s discontinuation for immune-related adverse events, underscore safety vigilance. Modern AI-driven target prediction and chemical modifications—locked nucleic acids, 2’-O-methyl substitutions—are mitigating risk, yet regulatory agencies still require extensive toxicology packages. Twenty-two nucleic acid therapeutics have won FDA approval since 1998, demonstrating that well-designed chemistry can clear clinical hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Services Lead Through Complexity

Services held 47.78% micro RNA market share in 2025, equal to USD 1.43 billion of spending, as laboratories outsourced extraction, quantification, and bioinformatics workflows to contract research organizations (CROs). High capital barriers, talent shortages, and the rising complexity of multi-omic data interpretation encourage research institutes and biotech firms to tap external expertise rather than build internal capacity. CROs expand bundled offerings that marry wet-lab testing with AI-assisted analytics, reinforcing stickiness.

Kits & Reagents form the fastest-growing category at a 15.92% CAGR through 2031. Standardized, ready-to-use consumables shrink protocol variability and reduce turnaround time, enabling wider adoption by mid-tier clinical labs. Innovative silicon-carbide spin columns and magnetic bead chemistries improve yield and purity, supporting downstream NGS or RT-qPCR. Instruments remain essential for centralized core facilities, yet high unit costs and long replacement cycles temper growth. Major vendors refresh portfolios with modular upgrades—automated liquid handling, cloud-native software—that extend asset life while boosting throughput.

By Technology: Real-Time PCR Dominance Faces Platform Convergence

Real-Time PCR accounted for 38.25% of total revenue in 2025 due to regulatory familiarity, scalable throughput, and ease of use in clinical labs. Sensitivity continues to climb through LNA-enhanced primers and microfluidic chips capable of multiplexing dozens of targets per run.

Microarray platforms, although matured, log the highest 15.54% CAGR by offering economical whole-panel profiling for exploratory studies and circular RNA analyses where sequencing depth proves costly. Innovations in probe design and dye chemistry revive interest among academic researchers and CROs requiring large cohort screens. NGS gains ground through falling per-base costs on instruments such as NovaSeq X, which marry high throughput with flexible lane configurations suitable for both discovery and clinical validation use cases.

By Application: Cancer Leadership Chased by Infectious Disease Growth

Cancer retained 35.78% share of the micro RNA market size in 2025, driven by extensive literature linking dysregulated microRNAs to tumor initiation, progression, and therapy resistance. Companion diagnostics for targeted therapies leverage tumor-specific microRNA panels to stratify patients and monitor minimal residual disease.

Infectious disease testing is projected to outpace all other segments at a 16.02% CAGR. Pandemic-induced investments demonstrated that microRNA signatures from serum, saliva, or urine can distinguish viral from bacterial infections within hours, guiding antimicrobial stewardship. Research programs now profile host microRNA responses to influenza, HIV, and tuberculosis, aiming to embed rapid panels into emergency departments. Cardiovascular and neurological indications also expand as longitudinal cohort data affirm prognostic value, diversifying revenue away from oncology.

By End-User: Biopharmaceutical Shift Toward Diagnostic Democratization

Biopharmaceutical companies represented 39.86% micro RNA market size in 2025, reflecting heavy spending on target validation, lead optimization, and companion diagnostic co-development. Their dominance persists, yet diagnostic centers are projected for the fastest 16.28% CAGR, propelled by accreditation of microRNA panels under in-vitro diagnostic regulations and the cost advantage of non-invasive specimen types.

Hospitals and clinics integrate point-of-care cartridges that deliver microRNA-based answers in under 30 minutes, encouraging test adoption for acute settings such as stroke triage. Academic institutions retain critical influence as discovery hubs but increasingly partner with commercial labs to monetize intellectual property, shortening technology translation timelines.

Geography Analysis

North America contributed 41.72% of global revenue in 2025 underpinned by a mature biotechnology ecosystem, sizable NIH and venture funding, and FDA programs that prioritize innovative oligonucleotide therapeutics. Reimbursement frameworks covering liquid biopsy and companion diagnostics facilitate rapid hospital uptake.

Asia–Pacific is forecast as the fastest-growing region at 16.95% CAGR to 2031. Governments in China, Japan, and South Korea offer matching grants and tax incentives for RNA research infrastructure, while contract development and manufacturing organizations leverage cost-efficient supply chains to attract global sponsors. Rising chronic disease prevalence, together with aging demographics, lifts demand for early detection tests. Domestic firms tailor assays for hepatitis- and gastric cancer-heavy disease profiles, building regulatory pathways through National Medical Products Administration and Pharmaceuticals and Medical Devices Agency reforms.

Europe maintains strong market positioning through Horizon-funded consortia, sophisticated clinical trial networks, and cohesive data-protection rules that facilitate multi-center biomarker validation. ARTHEx Biotech’s latest EUR 42 million round illustrates venture appetite for microRNA-targeting therapeutics headquartered in the region. Middle East & Africa and South America remain nascent but promising; increased expenditure on tertiary care hospitals and laboratory automation sets the foundation for gradually expanding microRNA diagnostics.

Competitive Landscape

Industry structure is moderately fragmented yet trending toward consolidation. Novartis set a precedent by spending USD 1.7 billion for Regulus Therapeutics in 2025, underscoring big pharma’s intention to secure proprietary microRNA pipelines before clinical proof-of-concept milestones. Large instrumentation vendors defend share through full-stack solutions that combine chemistry, hardware, and cloud analytics, whereas mid-sized biotechs carve niches in delivery technologies or rare-disease programs.

Strategic alliances dominate deal flow. Platform providers license proprietary detection chemistries to diagnostic firms entering decentralized testing, while therapeutic developers co-develop companion assays with CROs to streamline regulatory submissions. Venture investors reward differentiated capability—tissue-specific nanoparticle delivery,

AI-based off-target prediction—over scale alone. Competitive intensity rises in point-of-care testing, where start-ups promise 15-minute cartridge results, challenging central-lab incumbents. Barriers to entry include intellectual property around LNA chemistry, robust quality management systems, and clinical validation datasets linking microRNA panels to hard outcomes.

MicroRNA Industry Leaders

Qiagen N.V.

Thermo Fisher Scientific, Inc.

PerkinElmer, Inc.

Illumina, Inc.

Takara Bio, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Enzene Biosciences launched a new drug discovery division to complement its biologics manufacturing facility employing EnzeneX technology, expanding integrated CDMO offerings.

- May 2024: Emory University School of Medicine opened the Center for New Medicines, creating an ecosystem where scientists and clinicians co-develop novel therapeutics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the microRNA market as all revenue generated from research-grade and clinical-grade kits, reagents, dedicated instruments, and fee-based profiling or synthesis services that quantify, modify, or deliver endogenous or exogenous microRNA molecules. According to Mordor Intelligence, therapeutic pipeline licensing fees are excluded because they sit inside the broader RNA therapeutics value chain.

Scope exclusion: Mordor analysts intentionally omit bulk oligonucleotide contract manufacturing that is not microRNA-specific.

Segmentation Overview

- By Product & Service

- Kits & Reagents

- Instruments

- Services

- By Technology

- Real-Time PCR

- Microarray

- Next-Generation Sequencing (NGS)

- Immunoassay

- Northern Blotting

- In-situ Hybridization (ISH)

- By Application

- Cancer

- Cardiovascular Disease

- Neurological Disease

- Infectious Diseases

- Immunological Disorders

- Other Applications

- By End-User

- Biopharmaceutical Companies

- Diagnostic Centers

- Hospitals & Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team held structured calls with principal investigators at cancer genomics labs, procurement heads at North American CROs, and product managers from sequencing platform OEMs across Europe and Asia. These conversations validated service pricing spreads, clarified kit reorder frequencies, and flagged regional funding shifts that desktop data could not reveal.

Desk Research

We began with authoritative public datasets, such as NIH RePORTER grant records, FDA 510(k) listings, European CE-mark databases, and UN Comtrade HS-level exports of miRNA prep reagents, which anchor production and trade flows. Annual reports and 10-Ks from at-scale tool vendors, patent families accessed through Questel, and peer-reviewed prevalence studies in journals like Nature Genetics provided context around demand triggers. A second sweep tapped industry associations, for example, the American Association for Clinical Chemistry, plus news coverage pulled through Dow Jones Factiva. This mix lets us triangulate baseline volumes, typical ASP ranges, and adoption curves. The sources cited above are illustrative; many additional publications fed our desk work.

Market-Sizing & Forecasting

We built a top-down model that reconstructs the global demand pool from reported research funding, test throughput, and patient cohort counts, which are then cross-checked with a bottom-up roll-up of major supplier revenues and sampled ASP × unit volumes. Key variables include NGS run volumes, RT-qPCR kit conversion rates, miRNA panel sizes, and average service contract lengths. An ARIMA time series with scenario overlays for funding cycles produces the 2025-2030 outlook, while missing distributor data are gap-filled through region-specific penetration rates agreed upon in expert interviews.

Data Validation & Update Cycle

Each interim output passes variance checks versus NIH funding growth, quarterly vendor filings, and import trends; anomalies trigger a re-query of our respondents before sign-off. Reports refresh yearly, and an analyst re-runs core queries just before client delivery so users receive the latest view.

Why our Microrna baseline withstands scrutiny

Published estimates differ because firms vary their scope choices, currency conversions, and refresh cadence. Our disciplined mix of funding-based demand reconstruction and supplier cross-checks keeps totals transparent and repeatable for decision makers.

Key gap drivers include narrower product baskets, limited country coverage, and absent primary validation in several alternative studies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.00 billion (2025) | Mordor Intelligence | |

| USD 1.76 billion (2024) | Global Consultancy A | Excludes service revenue and applies list prices without ASP adjustments |

| USD 2.16 billion (2025) | Regional Consultancy B | Covers only 25 countries and relies mainly on public grant totals |

| USD 1.64 billion (2024) | Trade Journal C | Uses shipment data only, omitting sequencing-based assays and lab contracts |

These comparisons show that when services, full geography, and real-world pricing are integrated, as we have done, microRNA market value rises to a balanced, defensible baseline that clients can trust.

Key Questions Answered in the Report

How big is the MicroRNA Market?

The MicroRNA Market size is expected to reach USD 3.45 billion in 2026 and grow at a CAGR of 15.05% to reach USD 6.96 billion by 2031.

What factors are driving rapid growth in the micro RNA market?

Growth stems from rising chronic disease prevalence, regulatory incentives for oligonucleotide drugs, and continuous improvements in NGS and RT-qPCR platforms that make microRNA diagnostics and therapeutics more accessible.

Who are the key players in MicroRNA Market?

Qiagen N.V., Thermo Fisher Scientific, Inc., PerkinElmer, Inc., Illumina, Inc. and Takara Bio, Inc are the major companies operating in the MicroRNA Market.

Which is the fastest growing region in MicroRNA Market?

Asia–Pacific is forecast to expand at a 16.95% CAGR through 2031, propelled by government R&D incentives, expanding clinical trial activity, and increasing chronic disease burdens.

Page last updated on: