RNAi Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

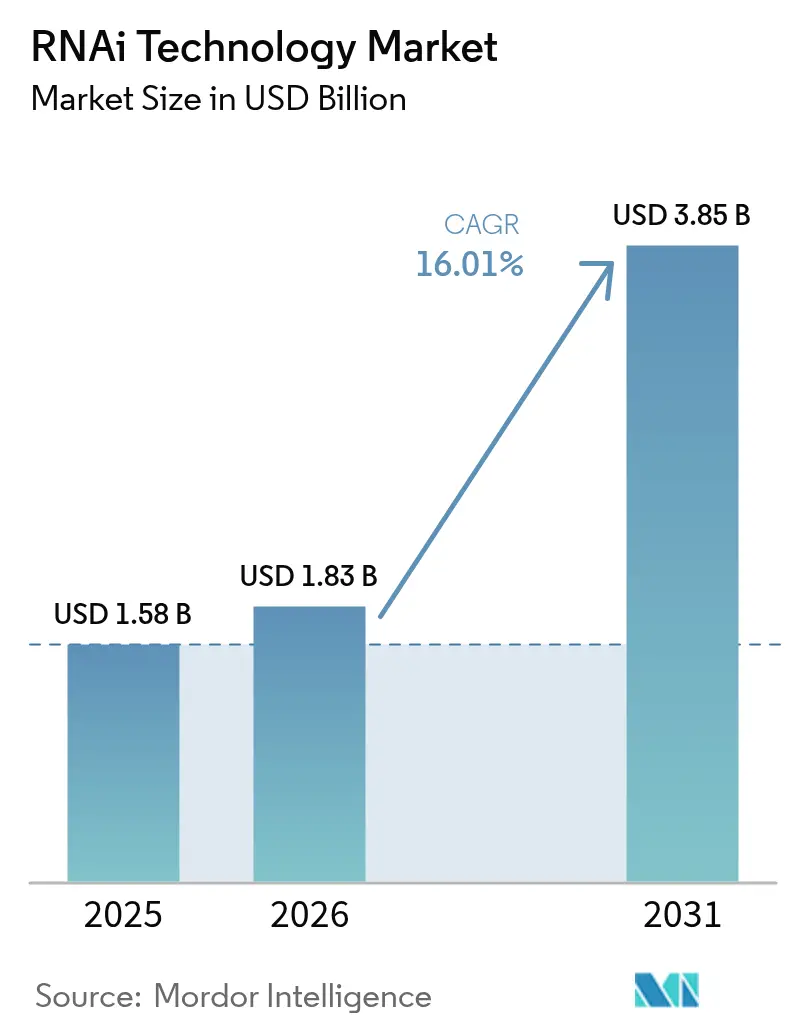

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 3.85 Billion |

| Growth Rate (2026 - 2031) | 16.01% CAGR |

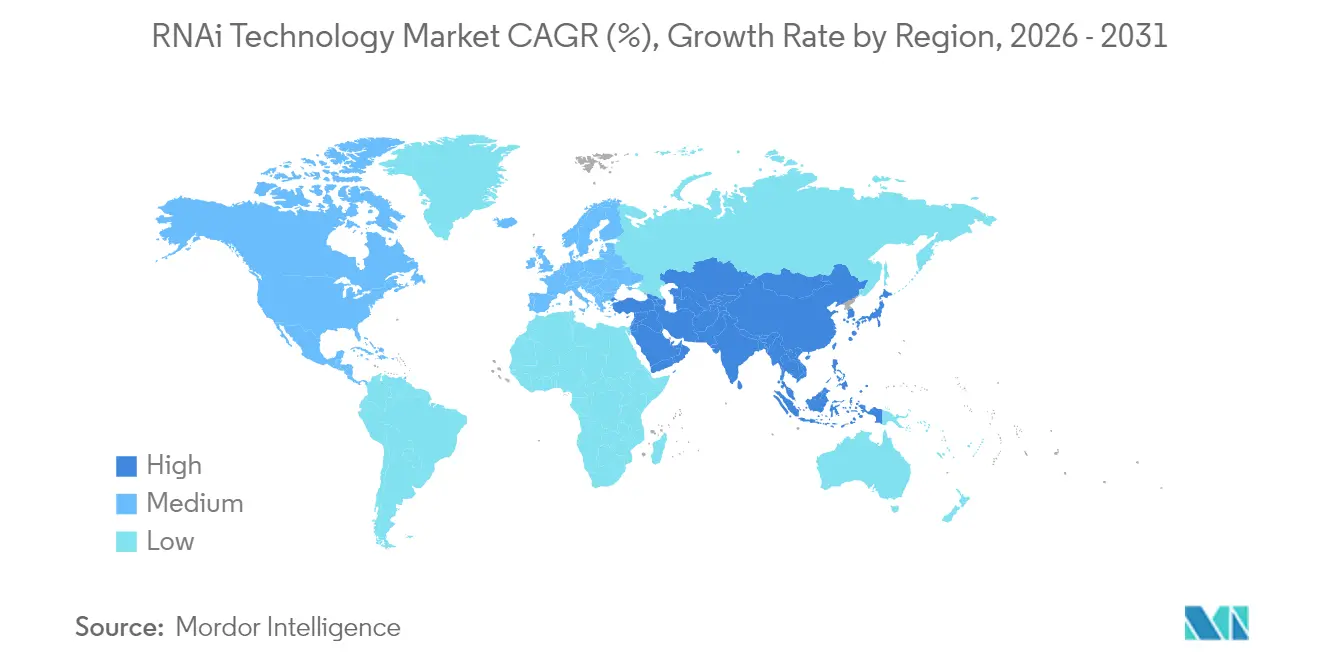

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RNAi Technology Market Analysis by Mordor Intelligence

The RNAi technology market size is expected to grow from USD 1.58 billion in 2025 to USD 1.83 billion in 2026 and is forecast to reach USD 3.85 billion by 2031 at 16.01% CAGR over 2026-2031. This sharp climb mirrors the field’s move from exploratory gene-silencing concepts to proven therapeutic platforms after successive FDA and EMA approvals, large-scale GMP investments, and a wave of delivery breakthroughs that collectively decompress regulatory and manufacturing risk. Wider adoption in oncology, cardiometabolic disorders, and hematology is expanding the RNAi technology market beyond rare genetic diseases, while advanced lipid nanoparticles (LNPs) fine-tune tissue targeting and dampen off-target effects. Investor appetite has deepened; integrated pharmaceutical companies now dominate licensing and acquisition activity, and CDMO outsourcing is soaring as developers forgo in-house oligonucleotide plants to contain capital outlays. Regionally, North America retains leadership, but Asia-Pacific’s cost-effective production and rapid trial initiation position it as the fastest-growing arena, setting up a two-pole dynamic that will influence supply-chain choices through 2030.

Key Report Takeaways

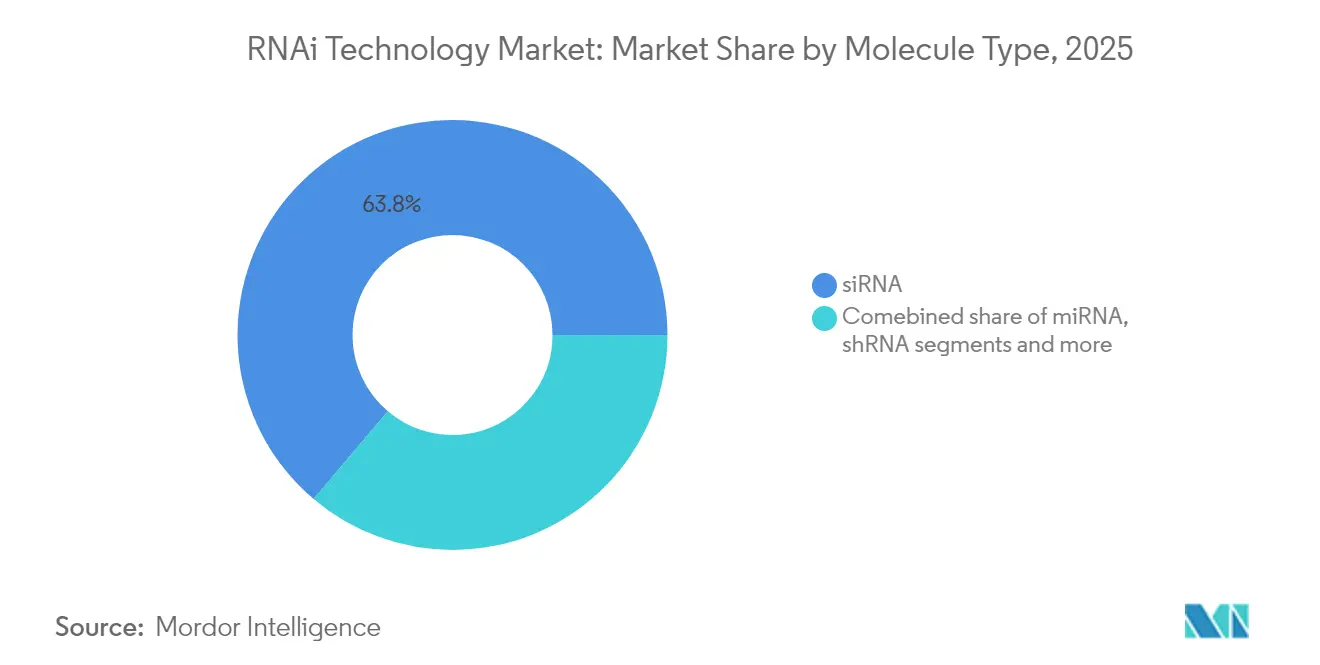

- By molecule type, siRNA captured 63.82% of the RNAi technology market share in 2025.

- By application, oncology accounted for 26.74% of the RNAi technology market size in 2025 and is expanding at a 16.38% CAGR through 2031.

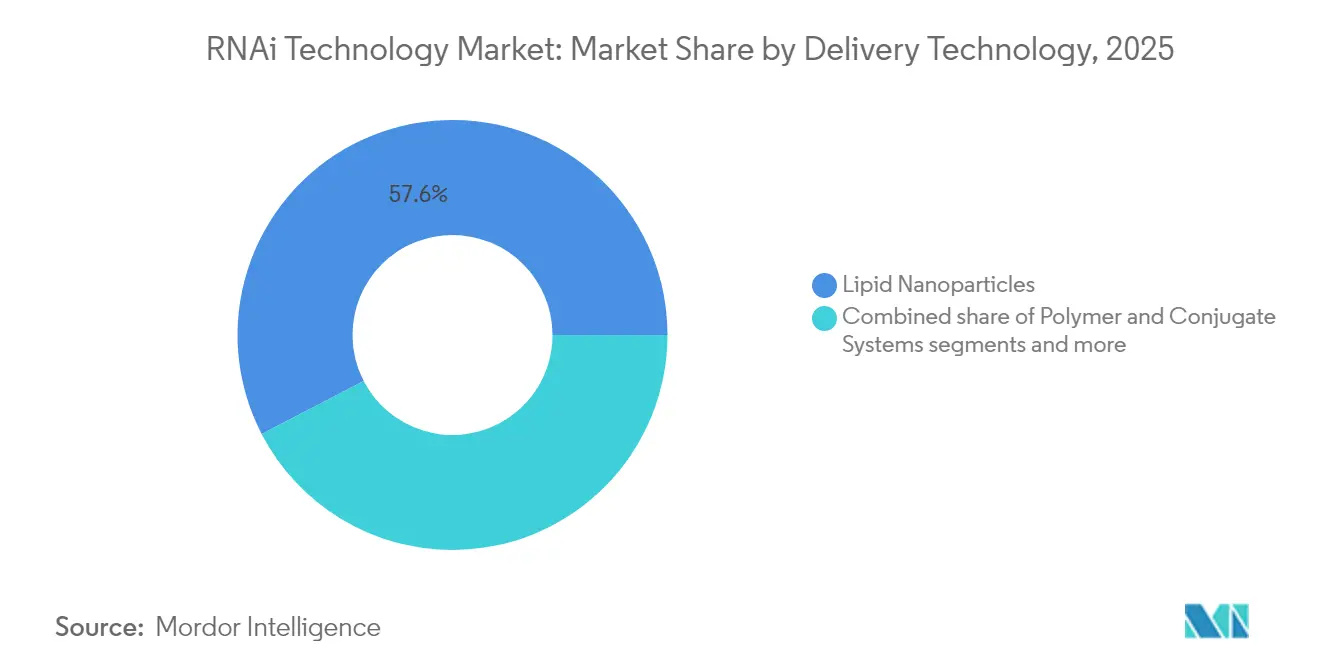

- By delivery technology, lipid nanoparticles held 57.61% revenue share in 2025; polymer-and-conjugate systems are projected to grow at 16.46% CAGR.

- By end user, pharmaceutical and biotechnology companies commanded 67.32% share of the RNAi technology market size in 2025, while CDMOs posted the highest projected CAGR at 16.95% through 2031.

- By geography, North America led with 41.02% of the RNAi technology market share in 2025; Asia-Pacific is forecast to expand at a 17.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global RNAi Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA/EMA approvals of siRNA drugs accelerating investor confidence | +4.2% | Global, with primary impact in North America & Europe | Medium term (2-4 years) |

| Advances in lipid-nanoparticle (LNP) delivery enhancing in-vivo stability | +3.8% | Global, led by North America and Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Government orphan-drug incentives for rare-disease RNAi assets | +2.9% | North America & EU, with emerging programs in Asia-Pacific | Long term (≥ 4 years) |

| Rising prevalence of cardiometabolic & genetic diseases addressable by gene-silencing | +2.1% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Expansion of RNA-focused CDMO capacity enabling smaller biotechs | +1.8% | Global, concentrated in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| AI-driven siRNA design platforms shortening discovery timelines | +1.5% | Global, concentrated in biotech clusters (Boston, San Francisco, Cambridge) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FDA/EMA Approvals of siRNA Drugs Accelerating Investor Confidence

Regulatory momentum has reached an inflection point, with the FDA’s approval of fitusiran for hemophilia A and B in April 2025 marking the latest milestone in a string of siRNA drug endorsements that began gaining pace in 2024. Active interventional trials now top 150, more than triple the 2021 figure, reflecting a strong late-stage pipeline that sustains the RNAi technology market. This validation has catalyzed venture funding; City Therapeutics captured USD 135 million in Series A financing led by former Alnylam executives, underscoring seasoned leadership’s conviction in next-gen RNA therapeutics. EMA’s synchronized review procedures create dual-continent launch potential, trimming commercialization latency and sharpening revenue forecasts for pipeline assets.

Government Orphan-Drug Incentives for Rare-Disease RNAi Assets

Seven-year exclusivity, up to 25% R&D tax credits, and waived FDA fees make rare disorders a capital-efficient proving ground. Silence Therapeutics secured multiple designations, slashing development costs and accelerating market access for hepatological and hematological programs. Parallel EMA incentives double addressable revenue under a single trial design, intensifying investor interest and diversifying the RNAi technology market pipeline toward ultra-rare indications with premium pricing.

Advances in Lipid-Nanoparticle Delivery Enhancing In-Vivo Stability

Second-generation ionizable LNPs combine biodegradable lipids and zwitterionic helpers to fortify serum stability, improve endosomal escape, and cut innate-immune activation. Manufacturing capacity is scaling fast; Wacker Chemie allocated EUR 100 million (USD 108 million) to modular LNP lines that can pivot across payloads, enabling the RNAi technology market to meet rising clinical-batch demand. Ligand conjugation and pH-responsive release broaden indications from liver to CNS and solid tumors, mitigating historical tissue-specific hurdles. These advances reinforce LNPs’ status as the dominant RNA carrier and spur sustained delivery-platform R&D.

AI-Driven siRNA Design Platforms Shortening Discovery Timelines

Machine-learning algorithms now predict potency and off-target effects from sequence and chemistry attributes, reducing wet-lab cycles by roughly 20 months. Integration with in-silico lipid-vehicle modeling yields preclinical candidates with delivery recipes in place, compressing time to IND. Biotech clusters in Boston, San Francisco, and Cambridge aggregate AI talent, feeding a steady stream of optimized assets into the RNAi technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-target toxicity & innate-immune activation concerns | -2.8% | Global, with heightened regulatory scrutiny in North America & EU | Medium term (2-4 years) |

| High cost of GMP-grade lipids/oligonucleotide manufacturing | -3.1% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Patent thickets around proprietary ionizable-lipid chemistries | -2.3% | North America & Europe primarily, affecting global market access | Long term (≥ 4 years) |

| Public opposition to gene-silencing in agriculture | -1.9% | Europe and select Asia-Pacific markets, limited impact on therapeutics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Off-Target Toxicity & Innate-Immune Activation Concerns

Toll-like receptor engagement can trigger cytokine release, imposing dose ceilings and lengthier toxicology studies that extend timelines by 12–18 months. Regulators now demand exhaustive genome-wide screens, adding analytical cost and slowing the RNAi technology market’s systemic-delivery programs.

High Cost of GMP-Grade Lipids/Oligonucleotide Manufacturing

GMP oligonucleotide synthesis costs run 10–15 times higher than small-molecule production, reflecting solvent-intensive steps and scarce high-purity reagents. Agilent invested USD 150 million to double nucleic-acid capacity, yet demand still exceeds output, creating procurement delays that restrict the RNAi technology market’s clinical-batch availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Type: siRNA Dominance Drives Market Leadership

siRNA held 63.82% of the RNAi technology market share in 2025, supported by well-established regulatory precedents from patisiran, givosiran, and fitusiran. The segment’s 16.1% CAGR ensures it remains the prime revenue engine even as newer modalities gain traction. miRNA therapeutics explore bidirectional regulation in cardiovascular and oncology settings, although undefined pathways slow approvals. shRNA vectors enable long-term silencing for chronic diseases, while ribozymes and antisense hybrids occupy niche mechanistic gaps, collectively diversifying the RNAi technology market.

siRNA’s proven delivery compatibility with LNPs and GalNAc conjugates underpins its commercial momentum, attracting Big-Pharma alliances eager to layer platform efficiency across wider disease franchises. Investor capital, however, is incrementally shifting toward miRNA and gene-editing hybrids to hedge technological concentration risk, suggesting a gradual broadening of the RNAi technology market beyond siRNA over the next decade.

By Application: Therapeutics Lead While Diagnostics Emerge

Therapeutics generated the bulk of 2025 revenue, with oncology commanding 26.74% of the RNAi technology market size thanks to its ability to silence undruggable drivers such as KRAS G12D. Cardiometabolic programs aiming at PCSK9 and ANGPTL3 build chronic-dosing annuity streams, enhancing lifetime value per asset. Infectious-disease candidates benefit from rapid sequence redesign to tackle mutating pathogens.

Outside therapeutics, high-content screening libraries and companion diagnostics supply recurring platform revenue. The EPA’s approval of ledprona for Colorado potato beetle control signposted agricultural potential, hinting at a peripheral but strategic extension of the RNAi technology market.

By Delivery Technology: LNPs Dominate as Polymers Accelerate

LNPs contributed 57.61% of 2025 revenue and maintain primacy due to large-scale GMP success during vaccine rollouts. pH-responsive ionizable systems drive sub-mg/kg potency, trimming safety margins and easing regulatory passage. Polymer-and-conjugate carriers, powered by GalNAc ligands, are the fastest risers at 16.46% CAGR, especially for liver-targeted conditions. Viral vectors serve niche durable-silencing use cases, while exosome and metal-oxide nanocarriers sit in preclinical stages, promising later-cycle upside for the RNAi technology market.

By End User: Pharma Dominance Meets CDMO Expansion

Pharmaceutical and biotech firms held 67.32% of 2025 revenue, reflecting integrated R&D and commercialization capabilities. CDMOs registered the fastest expansion at 16.95% CAGR as sponsors outsource oligonucleotide and LNP manufacture to avoid capital-intensive plant builds. Academic institutes and diagnostic labs collectively nurture discovery and biomarker validation, whereas agricultural biotech forms a small but emerging slice as RNA formulations gain regulatory traction.

Geography Analysis

North America retained 41.02% of the RNAi technology market share in 2025 on the back of FDA clarity, venture-capital liquidity, and mature CDMO clusters that compress development timelines. Agilent’s USD 150 million nucleic-acid expansion and MilliporeSigma’s viral-vector facility secure regional supply, further anchoring dominance.

Asia-Pacific is projected to grow at a 17.25% CAGR through 2031 as governments fund biotech parks and streamline approvals. South Korea’s ST Pharm invested USD 126 million to reach 14 mole/year oligo output, positioning the region as a global supply hub. China’s Sanegene Bio drew USD 130 million in funding, illustrating domestic momentum in the RNAi technology market.

Europe sustains steady growth under EMA’s centralized review and robust pharma infrastructure. Wacker Chemie’s EUR 100 million RNA site strengthens continental manufacturing resilience despite Brexit-related dual-filing requirements. Latin America, Middle East, and Africa remain nascent opportunities pending infrastructure upgrades and pricing-model refinements.

Competitive Landscape

Alnylam’s layered patents and first-mover approvals keep it at the forefront, but large pharmaceutical entrants are closing gaps through high-value alliances. Novartis’ USD 4.165 billion cardiovascular RNAi pact with Shanghai Argo illustrates Big-Pharma’s strategic embrace of RNA platforms. Platform differentiation centers on delivery scalability and intellectual-property coverage; City Therapeutics’ USD 135 million funding underscores investor confidence in AI-optimized discovery engines that de-risk off-target profiles. CDMOs compete on turnaround and quality, driving consolidation as capacity becomes a strategic asset in the RNAi technology market.

RNAi Technology Industry Leaders

Alnylam Pharmaceuticals

Silence Therapeutics PLC

Arrowhead Pharmaceuticals, Inc.

Thermo Fisher Scientific Inc

Dicerna Pharmaceuticals (Novo Nordisk A/S)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Novartis announced a USD 4.165 billion collaboration with Shanghai Argo to develop cardiovascular RNAi assets.

- May 2025: Sylentis received GMP clearance for its in-house siRNA facility, enabling commercial-scale output

Global RNAi Technology Market Report Scope

RNA interference is a biological process in which the RNA molecules are observed to inhibit gene expression or translation, by neutralizing the targeted mRNA molecules. Earlier, RNAi was identified by other names, such as co-suppression, post-transcriptional gene silencing (PTGS), and quelling. The extensive study of each of these apparently different processes clarified that the identity of these phenomena was all in fact RNAi. The RNA-interference (RNAi) market is segmented by Application (Drug Discovery and Development, Therapeutics [Oncology, Ocular Disorders, Respiratory Disorders, Hepatitis B and C, Autoimmune Hepatitis, Neurological Disorders, and Other Therapeutics]) and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| siRNA |

| miRNA |

| shRNA |

| Other RNA molecules |

| Therapeutics | Oncology |

| Cardiometabolic Disorders | |

| Infectious Diseases | |

| Neurological Disorders | |

| Rare Genetic Disorders | |

| Drug Discovery & Screening | |

| Diagnostics | |

| Agriculture | |

| Other Applications |

| Lipid Nanoparticles | Ionizable LNPs |

| Liposomes | |

| Polymer & Conjugate Systems | GalNAc Conjugates |

| PEGylated Carriers | |

| Viral Vectors | Adeno-associated Virus |

| Lentiviral Vectors | |

| Physical Delivery Methods | |

| Emerging Nanomaterials (Exosomes, Metal-oxide, etc.) |

| Pharmaceutical & Biotechnology Companies |

| Contract Development & Manufacturing Organizations (CDMOs) |

| Academic & Research Institutes |

| Diagnostic Laboratories |

| Agricultural Biotechnology Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Molecule Type (Value) | siRNA | |

| miRNA | ||

| shRNA | ||

| Other RNA molecules | ||

| By Application (Value) | Therapeutics | Oncology |

| Cardiometabolic Disorders | ||

| Infectious Diseases | ||

| Neurological Disorders | ||

| Rare Genetic Disorders | ||

| Drug Discovery & Screening | ||

| Diagnostics | ||

| Agriculture | ||

| Other Applications | ||

| By Delivery Technology (Value) | Lipid Nanoparticles | Ionizable LNPs |

| Liposomes | ||

| Polymer & Conjugate Systems | GalNAc Conjugates | |

| PEGylated Carriers | ||

| Viral Vectors | Adeno-associated Virus | |

| Lentiviral Vectors | ||

| Physical Delivery Methods | ||

| Emerging Nanomaterials (Exosomes, Metal-oxide, etc.) | ||

| By End User (Value) | Pharmaceutical & Biotechnology Companies | |

| Contract Development & Manufacturing Organizations (CDMOs) | ||

| Academic & Research Institutes | ||

| Diagnostic Laboratories | ||

| Agricultural Biotechnology Firms | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the RNAi technology market in 2026?

The RNAi technology market size stands at USD 1.83 billion in 2026.

What CAGR is forecast for RNAi therapeutics through 2031?

Overall revenue is projected to climb at a 16.01% CAGR over 2026-2031.

Which delivery technology leads current adoption?

Lipid nanoparticles hold 57.61% revenue share and remain the dominant delivery vehicle.

Which region is growing fastest?

Asia-Pacific is advancing at a 17.25% CAGR due to expanding clinical infrastructure and cost-efficient manufacturing.

Why are CDMOs gaining importance?

CDMOs post a 16.95% growth rate as pharma companies outsource GMP-grade oligonucleotide production to avoid high capex.

What recent FDA approval boosted market confidence?

In April 2025, the FDA approved fitusiran for hemophilia A and B, marking a milestone for siRNA therapies.

Page last updated on: