Vein Illuminator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

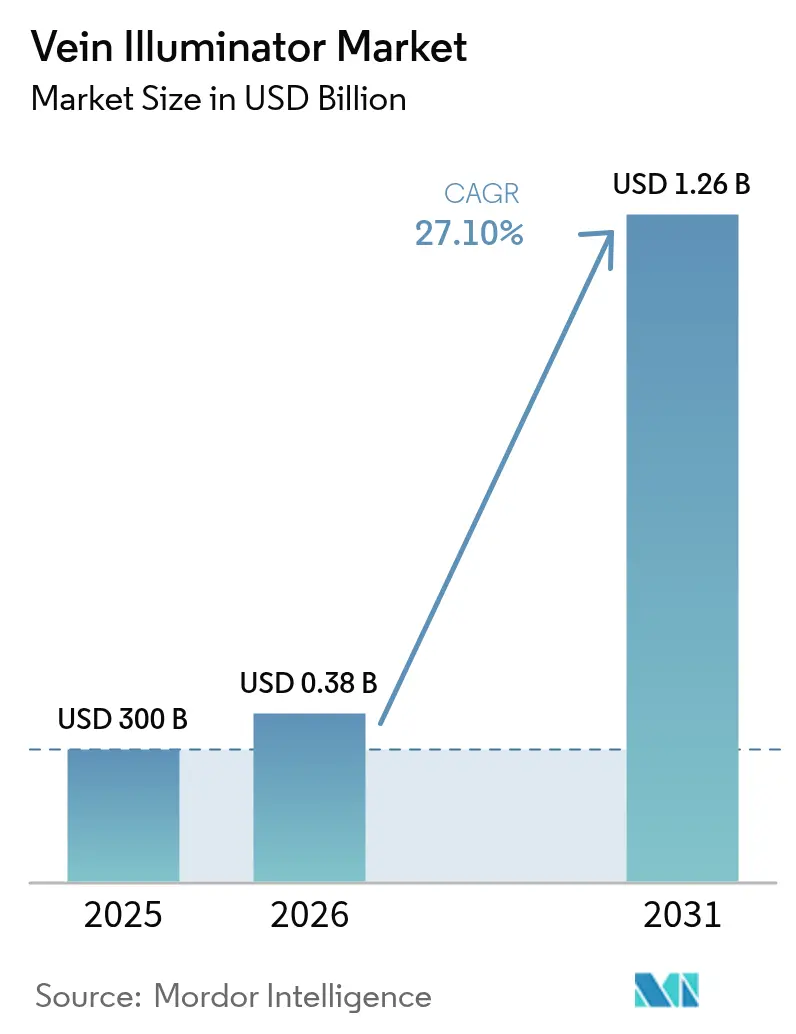

| Market Size (2026) | USD 0.38 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 27.10% CAGR |

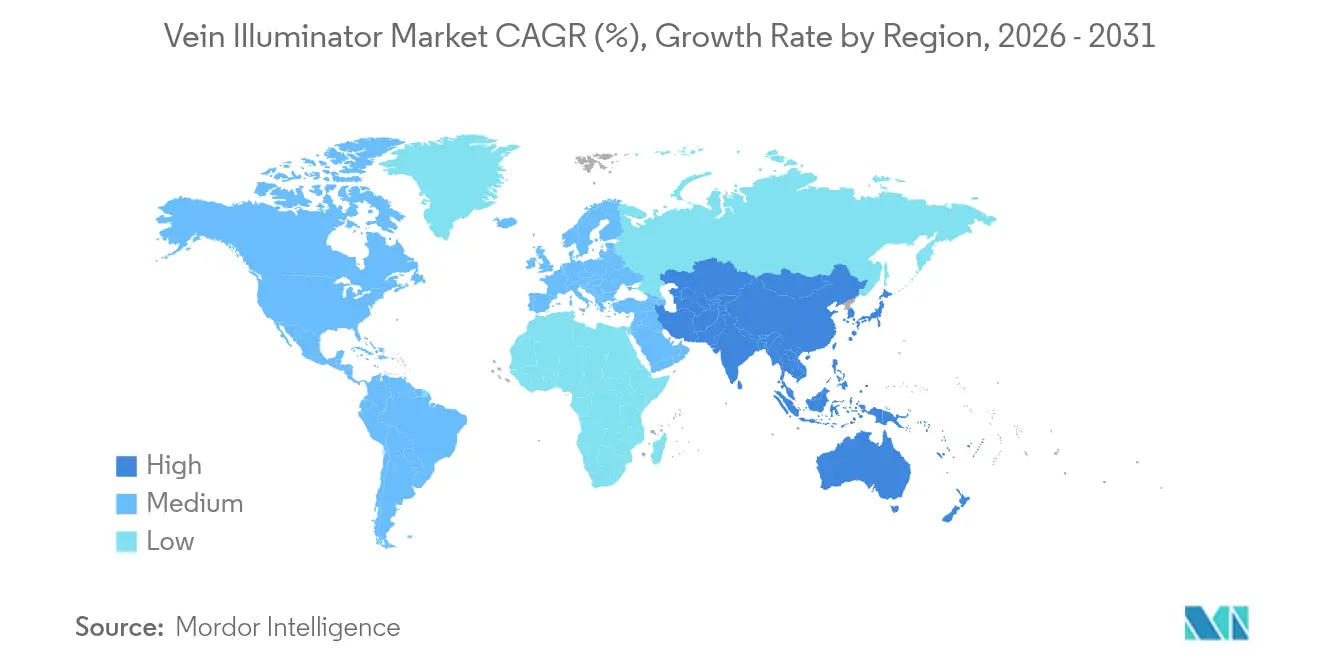

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vein Illuminator Market Analysis by Mordor Intelligence

The Vein Illuminator market size is expected to grow from USD 300 million in 2025 to USD 381.3 million in 2026 and is forecast to reach USD 1.26 billion by 2031 at 27.10% CAGR over 2026-2031. Robust growth reflects health systems’ focus on first-attempt venipuncture success, an outcome now tied to U.S. Medicare’s value-based purchasing scores. [1]AccuVein Inc., “Maury Regional Health Adopts Vein Visualization as Standard of Care to Help Improve Patient Outcomes,” AccuVein, accuvein.com Demand is amplified by aging and obese populations that make traditional vein palpation unreliable, while rising chronic-disease monitoring requires more frequent blood draws. Technology improvements in near-infrared (NIR) imaging, falling component costs, and portable form factors further accelerate adoption. Asia-Pacific’s push to localize medical-device manufacturing and China’s hospital modernization are tilting future revenue toward cost-optimized systems. Competitive pressure is intensifying as local firms introduce low-price NIR devices that undercut established brands while premium models layer on AI guidance and multi-modal imaging.

Key Report Takeaways

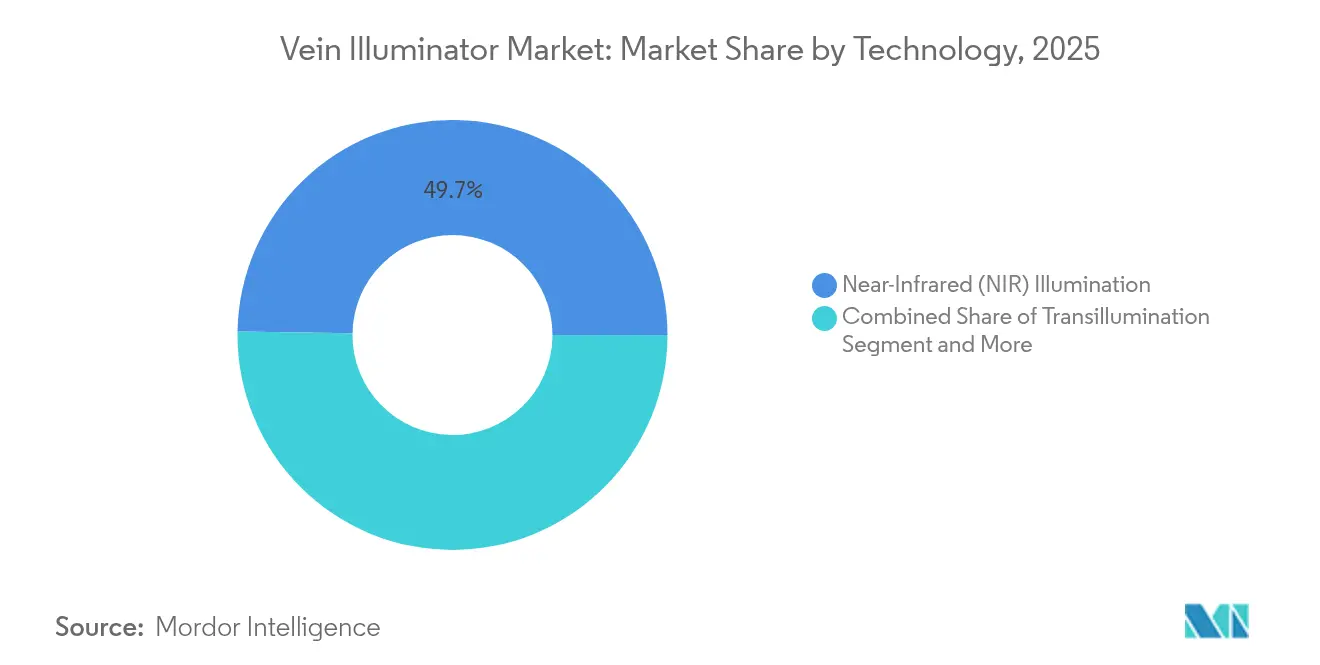

- By technology, Near-Infrared Illumination led with 49.74% revenue share in 2025; Ultrasound-Augmented systems are projected to expand at a 30.9% CAGR through 2031.

- By product type, Hand-held and Portable units held 60.55% of the vein illuminator market share in 2025, while Wearable and Clip-On Modules post the fastest 32.4% CAGR to 2031.

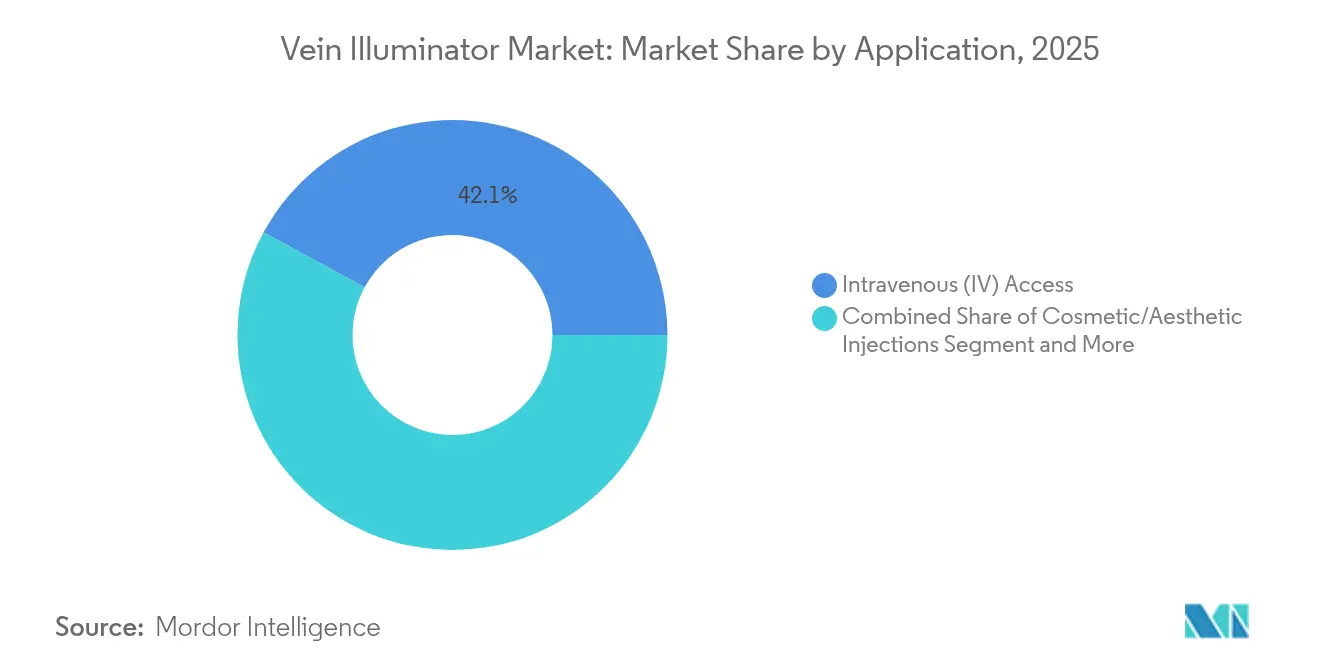

- By application, Intravenous Access accounted for 42.08% of the vein illuminator market size in 2025; Sclerotherapy and Varicose Vein Treatment are forecast to grow at 30.6% CAGR to 2031.

- By end-user, Hospitals and Clinics captured 45.60% revenue in 2025; Ambulatory Surgical Centers recorded the highest 29.55% CAGR through 2031.

- By geography, North America dominated with 36.80% 2025 revenue; Asia-Pacific is the fastest-growing region at 31.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vein Illuminator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising first-attempt success rates for IV and phlebotomy | +8.5% | North America, Europe, global hospitals | Medium term (2-4 years) |

| Growth in chronic-disease blood draws | +7.2% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Ageing and obese populations with difficult venous access | +6.8% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Hospital push for patient-experience KPIs | +4.3% | North America, Europe | Short term (≤ 2 years) |

| AI-integrated mobile vein-finder apps | +3.1% | Early adoption in North America | Medium term (2-4 years) |

| Adoption in cosmetic/aesthetic injections | +2.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising First-Attempt Success Rates Drive Quality Metrics

Clinical trials in pediatric units showed first-stick success climbing to 74.1% with AccuVein AV400 compared with 40.7% using palpation, trimming procedure time from 169 seconds to 44 seconds. [2]Sevil Inal, “Impact of Peripheral Venous Catheter Placement With Vein Visualization Device Support on Success Rate and Pain Levels in Pediatric Patients,” Pediatric Emergency Care, researchgate.net Health-system executives translate these gains directly into higher HCAHPS patient-experience scores, which shape Medicare reimbursements, elevating device purchases to strategic priorities. Patient surveys reveal 93% of respondents rate hospitals higher when staff employ visualization tools.

Growth in Chronic-Disease Blood Draws

More frequent HbA1c, lipid, and renal tests among diabetic and cardiovascular cohorts raise annual venipuncture volumes, stressing phlebotomy capacity. Aging vasculature and drug-induced vein fragility heighten failure risk, prompting facilities to equip labs with portable NIR finders that cut repeat sticks and consumable waste.

Ageing and Obese Populations Challenge Traditional Methods

Obese patients (BMI > 30) experienced a 3.5-fold jump in IV placement success when clinicians used NIR devices, reaching 96% success within two attempts for BMI > 40. Geriatric skin thinning and altered subcutaneous fat distribution compound access difficulty, moving nursing homes and bariatric centers to standardize visualization.

Hospital Push for Patient-Experience KPIs

U.S. value-based payment formulas directly link revenue to patient satisfaction, and vein illuminators measurably raise comfort scores. Maury Regional Health adopted a visualization system-wide to bolster HCAHPS metrics and reduce missed sticks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and per-unit device costs | –4.8% | Emerging markets worldwide | Short term (≤ 2 years) |

| Lack of reimbursement codes | –3.2% | North America, Europe | Medium term (2-4 years) |

| Training gaps in low-resource settings | –2.1% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Regulatory ambiguity for aesthetic-only devices | –1.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Per-Unit Device Costs

Premium NIR systems list between USD 4,000 and USD 27,000, squeezing budgets of small hospitals. Experimental open-source models built from recycled optics have demonstrated comparable vein contrast for USD 25, hinting at future price erosion.

Lack of Reimbursement Codes

Because illumination is bundled into broader IV or phlebotomy codes, providers cannot recoup capital outlays directly. LimFlow’s 2025 CMS approval for a dedicated vascular device category signals that distinct coding pathways could emerge for visualizers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: NIR Dominance Faces Hybrid Disruption

Near-Infrared Illumination controlled 49.74% revenue in 2025, underpinning the vein illuminator market with a mature, cost-efficient platform. Ultrasound-Augmented units, posting 30.9% CAGR to 2031, carve share in difficult-access patients via deeper imaging and synergy with existing ultrasound carts. Transillumination remains a pediatric niche due to softer light, while multispectral hybrids gain research traction. Patent filings such as the dual-mode VeinCAP system illustrate convergence trends toward single devices offering NIR plus diffuse hyperspectral views. As feature sets widen, vendors differentiate on AI algorithms that auto-grade vein quality and log success metrics to electronic health records.

By Product Type: Portability Drives Innovation

Hand-held and Portable devices occupied 60.55% of 2025 revenue because nurses favor pocketable tools that shift easily between wards. Wearable and Clip-On Modules, climbing at 32.4% CAGR, free clinicians’ hands during complex cannulations, and feed video to smart glasses for teaching. Table-top carts persist in blood banks where mounted cameras stay calibrated for long draws. IoT connectivity is redefining design priorities: next-generation wearables integrate Wi-Fi and cloud dashboards that benchmark first-stick rates, transforming basic lights into quality-management nodes.

By Application: Aesthetic Expansion Accelerates Growth

Intravenous Access held a 42.08% share in 2025, the base use case anchoring the vein illuminator market. Yet cosmetic practices fuel the fastest 30.6% CAGR in Sclerotherapy and Varicose Vein Treatment after FDA safety notices highlighted injection-site complication risks. Facial-vein mapping cuts bruising and hematoma rates, making imaging a standard of care in high-volume med-spa chains.

By End-user: Ambulatory Centers Drive Adoption

Hospitals and Clinics captured 45.60% revenue in 2025, but outpatient Ambulatory Surgical Centers are expanding fastest at 29.55% CAGR through 2031. Time-based reimbursement models reward ASC operators who shave minutes off IV setups with visualization, reinforcing spending despite tight capital budgets. Blood Donation Camps value donor comfort to secure repeat visits, while nursing homes purchase compact models that accompany mobile phlebotomy carts.

Geography Analysis

North America retained 36.80% 2025 revenue leadership on the back of sophisticated infrastructure and reimbursement programs that pay for patient-experience outcomes. U.S. hospitals embed first-stick statistics into quality dashboards, ensuring repeat device orders. Canada’s single-payer system favors province-wide contracts that lower per-unit costs, while Mexico’s private medical-tourism clinics install finders as patient-comfort differentiators.

Europe’s multi-payer environment produces steady uptake; Germany’s university hospitals pilot multi-modal units, and the United Kingdom’s NHS negotiates bulk pricing to support vascular-access safety goals. CE Mark harmonization smooths cross-border sales and encourages newer entrants from Scandinavia and Eastern Europe.

The vein illuminator market size in Asia-Pacific is expanding at a 31.7% CAGR, making it the global growth engine. India’s Production-Linked Incentive scheme subsidizes domestic device plants, reducing import reliance. China’s hospital-upgrade program requires equipment that boosts nursing efficiency; local brands undercut imports by bundling visualization with IV kits. Japan’s super-aged population and high device standards favor premium dual-mode systems, while South Korea’s start-ups test AI-enabled smartphone adapters for home infusion services.

Regulatory Landscape

Vein illuminators generally enter the United States market under the US Food and Drug Administration (FDA) medical device framework. Many non-contact vein visualization or projection systems are commonly handled as Class I devices and are often 510(k)-exempt, depending on the specific design and intended use. For electrical safety and electromagnetic compatibility, manufacturers typically align product testing to IEC 60601-1-2 (Edition 4.1, 2020), which is widely referenced for medical electrical equipment and often becomes a de facto gate for hospital acceptance and tender eligibility.

In Europe, access is governed by the EU Medical Device Regulation (MDR) 2017/745, consolidated as of January 1, 2026. Classification is determined via Annex VIII rules, rather than US-style precedent, and Notified Body involvement is required for higher-risk classes. India regulates medical devices under the Medical Devices Rules, 2017, under the Drugs and Cosmetics Act, 1940. Licensing oversight by the Central Licensing Authority shapes import and manufacturing documentation, as well as quality-system expectations for suppliers selling into large public and private hospital networks.

Value Chain Analysis

The vein illuminator value chain begins with specialized optical and electronic inputs, including near-infrared (NIR) emitters/lasers, imaging sensors, projection modules, optics, batteries, and embedded processors. This is followed by device design, integration, verification/validation, and quality management (commonly aligned with ISO 13485), plus product safety and EMC compliance (IEC 60601 series, including IEC 60601-1-2). Manufacturing is carried out by established brands and regional OEMs, with differentiation increasingly tied to software, such as image processing, vein detection algorithms, and workflow aids, and to form factors that improve point-of-care availability in emergency, pediatrics, and high-throughput outpatient settings.

Downstream, distribution is led by direct hospital sales, regional distributors, and tenders, which may be shaped by group purchasing organizations and health system standardization initiatives. Procurement committees typically assess device performance alongside infection-control workflows (covers and cleaning steps), service and calibration support, and interoperability needs when vendors include analytics dashboards or attempt logging that can connect to hospital IT and EHR environments. These integration requirements can add friction and extend sales cycles compared with stand-alone portable devices.

Competitive Landscape

Market concentration is moderate: AccuVein, Christie Medical, and Translite together account for slightly less than half of global sales, while dozens of regional firms compete on price. Leaders defend their share through clinical evidence, 40-plus granted patents, and global distribution networks. Price competition is most acute in basic NIR models, where Asian OEMs ship sub-USD 500 units to community hospitals. Innovation is shifting toward platform propositions that pair imaging with analytics dashboards, cloud logbooks, and AI vein-grading. Strategic moves during 2024-2025 included Christie adding Bluetooth-enabled AVV-X series and AccuVein partnering with cloud-EHR vendors to auto-record cannulation attempts.

Consolidation is expected as firms seek scale for R&D and regulatory compliance. Likely buyers include infusion-therapy giants aiming to bundle visualization with IV set consumables, echoing Philips’ 2024 move to launch LumiGuide surgical navigation that embeds optics expertise within broader vascular portfolios. [3]Koninklijke Philips N.V., “Philips LumiGuide: 3D Human GPS Powered by Light,” philips.com

Vein Illuminator Industry Leaders

AccuVein Inc.

Christie Medical Holdings Inc.

TransLite LLC (Veinlite)

VueTek Scientific LLC

Venoscope LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace exists between clinical need, such as difficult venous access across pediatrics, emergency, and critical care, and the standardized evidence packages that procurement bodies use for broad adult-population deployment. Formal assessments and trial activity offer a pathway to close that gap. NICE has published a Medtech Innovation Briefing covering AccuVein (MIB6), and Malaysia's Health Technology Assessment Section (MaHTAS) issued a 2025 review on vein finder technologies, which provides reference points for hospital value dossiers and tender submissions. At the same time, multiple study protocols and registries are active, including the ICARE trial protocol published in BMJ Open (February 2025) and a Brazilian registry update (REBEC) showing a last recorded approval date in February 2026 for a trial evaluating AccuVein in adults with difficult venous access, supporting more consistent cost-effectiveness narratives.

Technology and commercialization opportunities cluster around connected workflows rather than standalone visualization. This includes software-integrated imaging, machine learning-enabled vein detection, and closer linkage to ultrasound or EHR documentation, where hospitals already track first-stick success and patient-experience KPIs. Miniaturization and point-of-care availability remain practical adoption levers tied to end-user workflow bottlenecks, while group purchasing and system-wide standard-of-care decisions create a path to scaling deployments beyond individual department purchases, particularly when devices can be justified as quality-management tools that reduce repeat sticks, procedure time, and staff burden.

Recent Industry Developments

- March 2026: AccuVein announced the launch of the AccuVein AV600, described as a major upgrade with an enhanced projection engine and higher image resolution. The release expands hospital-wide vein visualization capabilities and strengthens competitive differentiation through improved workflow integration.

- August 2025: Christie Medical Holdings became a contracted supplier for Vizient, expanding procurement access to VeinViewer Vision2 and Flex models across Vizient member facilities. The contract structure supports faster purchasing cycles for hospitals that buy through standardized agreements, strengthening Christie Medical's channel reach in the United States.

- December 2024: Therma Bright signed a US distribution agreement for the Venowave VW5, highlighting continued distributor interest in vascular-access tools sold through channel partners. The move signals that distribution networks remain an important route to broaden availability outside direct-sales footprints, especially for cost-sensitive providers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers dedicated devices that help clinicians see superficial veins by projecting or highlighting vein patterns on the skin to support IV access and blood draws across care settings.

Scope exclusions: We exclude general purpose ultrasound scanners used for broader imaging and any phone accessories that are not sold as regulated vein illumination devices.

Segmentation Overview

- By Technology

- Near-Infrared (NIR) Illumination

- Transillumination

- Ultrasound-Augmented

- Multispectral/Hybrid

- Others

- By Product Type

- Hand-held and Portable

- Table-Top/Cart-Mounted

- Wearable and Clip-On Modules

- By Application

- Intravenous (IV) Access

- Blood Draw/Venipuncture Assistance

- Sclerotherapy and Varicose Vein Treatment

- Emergency and Critical Care

- Cosmetic/Aesthetic Injections

- By End-user

- Hospitals and Clinics

- Blood Donation Camps and Blood Banks

- Ambulatory Surgical Centers

- Rehabilitation and Nursing Homes

- Academic and Research Institutions

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the demand pool and to avoid guessing on basic healthcare activity levels. We referenced public sources such as CDC and NIH publications, FDA device databases and recall notices, OECD and World Bank health spending indicators, and WHO and national health ministry statistics on procedures and workforce.

To translate those signals into a revenue model, we also reviewed company annual reports, investor presentations, product brochures, and reputable press coverage on hospital purchasing and vascular access practices. Where needed, we used paid subscriptions for company financials and patent records to confirm product cycles and technology shifts, without relying on marketing descriptions. These examples are not exhaustive, and we checked many other public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were run with a mix of device-side executives, distributors, and clinical users who regularly influence purchasing decisions, so assumptions could be stress-tested in plain language. Because this is a global market, we checked inputs across APAC, EMEA, and the Americas to reflect differences in IV cannulation practices, budget cycles, and adoption speed in hospitals and outpatient settings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 48% |

| Mid tier: 57% | Functional/Unit leaders: 27% | EMEA: 29% |

| Smaller Players: 17% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure volumes and care-setting activity are used to reconstruct the addressable need for vein visualization support, then adoption and replacement behavior are applied to convert need into unit demand. After that structure was set, we ran selective bottom-up checks, including channel feedback on typical selling prices and a limited roll-up of visible supplier revenues where disclosures were available.

Key model inputs included IV starts and blood draw intensity by care setting, difficult venous access prevalence signals (such as obesity and aging mix), device utilization per site, average selling price bands by form factor, replacement cycles tied to warranty and wear, and regional budget pressure that slows or accelerates purchases. When primary feedback indicated gaps in smaller facility coverage, penetration rates were adjusted using practical guardrails like installed base per bed and realistic training capacity. For forecasting, we used scenario analysis around adoption speed and price drift, and aligned assumptions to the most repeated expectations shared by practitioners and procurement-focused respondents.

Data Validation & Update Cycle

Outputs are checked against independent signals such as healthcare spending direction, device shipment discussions in public filings, and region-level adoption narratives collected in interviews. If a country total looks too high versus procedure intensity or too low versus installed base logic, the inputs are re-checked and follow-up calls are triggered before final sign-off.

A multi-step internal review is completed so the calculations, definitions, and year-to-year changes are consistent and explainable. The report is refreshed annually, and interim updates are made when material events occur, such as regulatory actions or sharp pricing moves. Before delivery, a final pass is completed to ensure the latest public data points are reflected in the market view.

Mordor Intelligence's Vein Illuminator Market Size Compared With Other Published Estimates

Published market values for vein illuminators can differ, even when the product name looks the same, because scope and counting rules are not consistent. The biggest swings usually come from what is treated as a vein illuminator device, what settings are counted, and how prices are carried forward across years.

The main gap comes from whether general purpose ultrasound and adjacent vein access equipment are folded into the total. Mordor Intelligence counts only dedicated vein illumination devices and keeps ultrasound guidance outside the scope. Differences also show up when an estimate relies heavily on a single base-year shipment assumption, uses flat global pricing, or applies a conservative adoption curve that does not match clinician feedback in fast-growing hospital systems.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.30 B (2025) | |

| Global Consultancy A | USD 0.16 B (2025) | Uses a narrower device and channel view, which tends to exclude some hospital purchasing routes and applies tighter adoption assumptions that reduce the addressable installed base. |

| Industry Research Group B | USD 0.09 B (2024) | Anchors sizing to an earlier year with limited validation on procedure-driven demand, and it appears to understate average selling prices by assuming a higher mix of low-cost basic devices. |

The spread in the table is largely explained by scope choices and how fast adoption is assumed to move in hospitals versus outpatient settings. By keeping the model tied to procedure intensity, realistic penetration, and price bands that were checked in interviews, the resulting estimate stays traceable to inputs that can be re-tested as new information becomes available.

Key Questions Answered in the Report

What is the current size of the vein illuminator market and its growth outlook?

The vein illuminator market size is USD 381.3 million in 2026 and is projected to reach USD 1.26 billion by 2031, advancing at a 27.10% CAGR.

Which region is forecast to grow the fastest?

Asia-Pacific is expected to expand at a 31.70% CAGR through 2031, driven by medical-device manufacturing incentives in India and hospital modernization in China.

Which technology holds the largest market share?

Near-Infrared Illumination led with a 49.74% revenue share in 2025, supported by mature clinical validation and cost-efficient components.

Which end-user segment shows the highest growth rate?

Ambulatory Surgical Centers are growing the fastest with a 29.55% CAGR as outpatient care models prioritize shorter procedure times and higher patient satisfaction.

What are the primary factors accelerating adoption?

Higher first-attempt venipuncture success rates, rising chronic-disease blood draws, and hospital patient-experience KPIs are the leading demand drivers.

What key barriers restrain wider deployment?

High capital costs for premium devices and the absence of dedicated reimbursement codes reduce purchasing incentives, especially in cost-sensitive settings.

Page last updated on: