Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 119.26 Billion |

| Market Size (2026) | USD 123.66 Billion |

| Market Size (2031) | USD 148.17 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

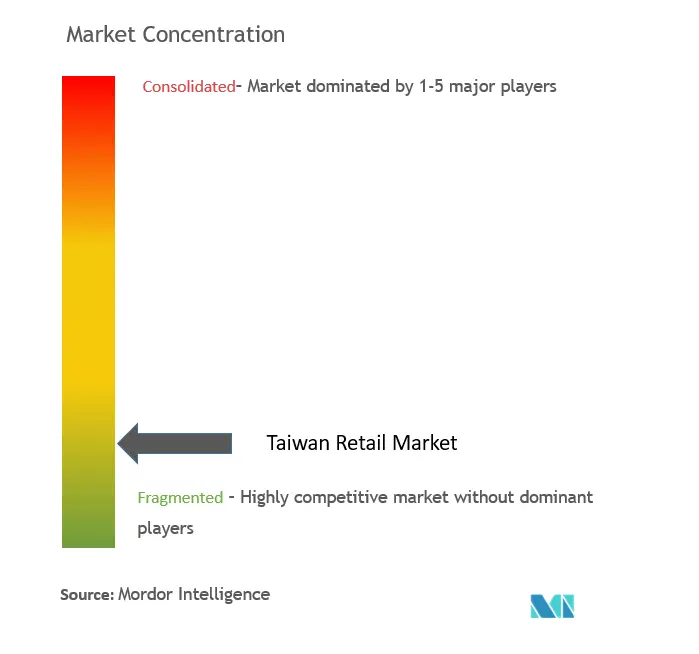

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Retail Market Analysis by Mordor Intelligence

Taiwan retail market size in 2026 is estimated at USD 123.66 billion, growing from 2025 value of USD 119.26 billion with 2031 projections showing USD 148.17 billion, growing at 3.69% CAGR over 2026-2031. Robust purchasing power, high urban density, and rapid digitalization sustain steady value growth even as volume expansion plateaus. Mergers such as PX Mart’s TWD 11.5 billion (USD 358.8 million) takeover of RT-Mart demonstrate how consolidation fortifies bargaining strength with suppliers and streamlines last-mile logistics. Dense convenience-store networks—6.98 outlets per 10,000 residents—act as ready-made fulfillment hubs, creating a formidable omnichannel ecosystem that online-only players struggle to match [1]Taiwan News, “Taiwan Has One Convenience Store per 1,703 People,” taipeitimes.com. . Demographic aging simultaneously restrains labor supply yet expands demand for health-oriented products and services, prompting retailers to invest in AI-driven process automation and elder-friendly merchandising. Meanwhile, regulatory vigilance—exemplified by the Fair Trade Commission’s block of Uber’s USD 950 million Foodpanda acquisition—signals that future market share gains will hinge more on service innovation than on headline-grabbing acquisitions.

Key Report Takeaways

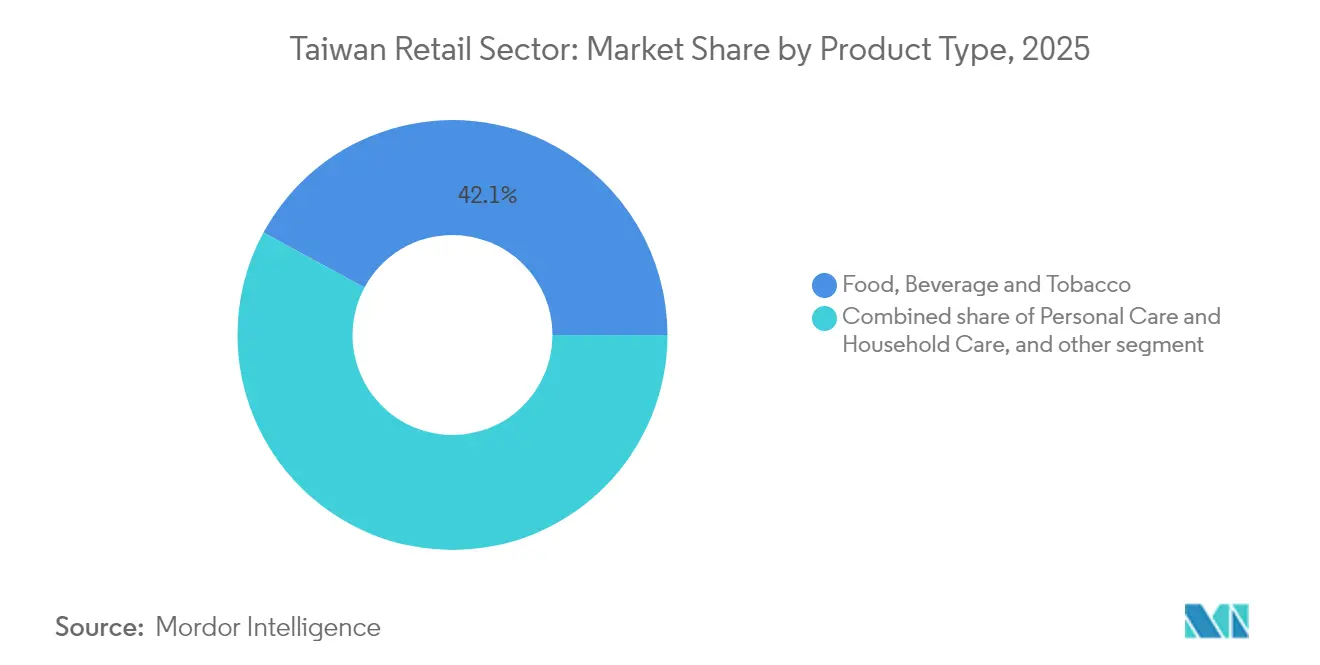

- By product category, food, beverage & tobacco led with 42.10% of the Taiwan retail market share in 2025; electronic & household appliances are forecast to expand at an 8.05% CAGR through 2031.

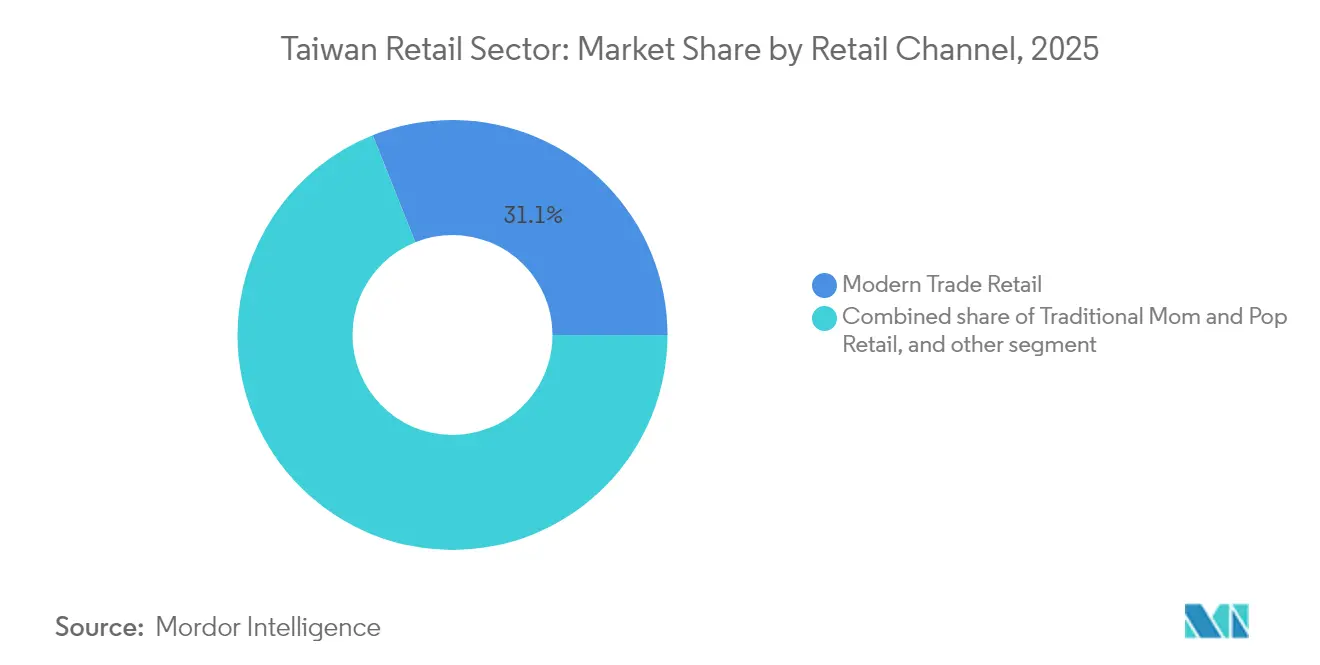

- By retail channel, modern trade held 31.05% of the Taiwan retail market size in 2025, while e-commerce & others are projected to record the highest CAGR at 11.85% through 2031.

- By format, convenience stores accounted for a 29.00% share of the Taiwan retail market size in 2025, and specialty stores are advancing at an 8.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-store density & O2O ecosystems | +1.2% | National, concentrated in urban areas | Medium term (2-4 years) |

| Mobile-first e-commerce & digital payments boom | +0.9% | National, higher penetration in metropolitan areas | Short term (≤ 2 years) |

| Ageing population spurs health-oriented retail demand | +0.7% | National, early gains in Taipei, Taichung, Kaohsiung | Long term (≥ 4 years) |

| Retail consolidation rewrites supplier terms | +0.5% | National | Medium term (2-4 years) |

| Cross-border live-stream commerce inflows | +0.4% | National, youth demographic | Short term (≤ 2 years) |

| Smart-retail subsidies & 5G roll-out | +0.3% | National, pilot programs in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-store Density & O2O Ecosystems

Taiwan’s convenience-store leaders, such as 7-Eleven and FamilyMart, have evolved into digital hubs that handle financial services, parcel collection, and prepared foods while feeding real-time transaction data into AI inventory engines. President Chain Store’s 7-Eleven network operated 6,859 outlets in 2024, averaging TWD 30.1 million (USD 940,000) sales per store and offering same-day delivery to nearly every urban household. Fujitsu-backed pilots employ blockchain payments and computer-vision shelf monitoring to minimize shrinkage and automate replenishment [2]Fujitsu, “Digital Technology Field Trial in FamilyMart Concept Store,” fujitsu.com. . These capabilities reinforce the Taiwan retail market’s omnichannel strength by fusing offline convenience with online reach.

Mobile-First E-Commerce & Digital Payments Boom

Digital wallets and contactless cards processed TWD 8.3 trillion (USD 258.96 billion) in 2024 transactions, a 14.2% jump as smartphone penetration neared 90% and livestream shopping became mainstream [3]Cnyes, “2025 Taiwan Mobile Payment Industry Analysis,” cnyes.com. . The Financial Supervisory Commission's target of TWD 10 trillion (USD 312 billion) by 2026 reflects systematic digitization across retail touchpoints. Mobile-first platforms leverage Taiwan's 90% smartphone penetration to create seamless shopping experiences, with livestream commerce emerging as a critical conversion channel where 73% of online shoppers engage with video content. Shopee dominates with 62% livestream preference share, followed by Facebook at 36%, indicating social commerce integration drives incremental sales rather than channel substitution. This mobile-centric approach enables micro-targeting capabilities that traditional retail formats cannot match, particularly for impulse purchases during peak evening hours between 8-10 PM.

Ageing Population Spurs Health-Oriented Retail Demand

Taiwan's demographic transition accelerates demand for functional foods and health-oriented retail categories, with the elderly care market reaching TWD 3.6 trillion (USD 112.32 billion) in 2025. The 2025 Silver-Friendly Food Awards attracted 135 companies submitting 350 products, demonstrating industry-wide pivot toward age-appropriate nutrition solutions. Major food manufacturers are launching specialized product lines targeting seniors with chewing difficulties, emphasizing high-protein content and easy-to-consume formats. This demographic shift creates sustainable competitive advantages for retailers who establish early distribution relationships with specialized suppliers, as switching costs increase once elderly consumers develop brand loyalty. The Ministry of Agriculture's requirement for 10% Taiwanese agricultural ingredients in silver-friendly products also supports domestic supply chain development.

Retail Consolidation Rewrites Supplier Terms

PX Mart's acquisition of RT-Mart fundamentally alters supplier negotiation dynamics through centralized procurement power, affecting 20% of Taiwan's FMCG market [4]FoodNext, “Silver-Friendly Food Awards Showcase Elderly Nutrition Innovation,” foodnext.net. . The consolidated entity implements consignment systems where suppliers bear inventory risk while paying post-deduction fees based on sales performance, shifting traditional wholesale margins toward retailers. This structural change forces suppliers to develop direct-to-consumer capabilities or accept reduced profitability, accelerating vertical integration trends across food and beverage categories. Smaller suppliers face particular pressure as they lack negotiating leverage against consolidated retail buyers, potentially driving industry consolidation at the manufacturer level. The Fair Trade Commission's monitoring of these practices suggests regulatory intervention may limit the most aggressive terms, but fundamental power rebalancing favors large-format retailers.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Store-saturation cannibalization risk | -0.8% | National, acute in metropolitan areas | Medium term (2-4 years) |

| Labour shortages & rising wage floor | -0.6% | National, service-sector concentration | Short term (≤ 2 years) |

| Supply chain disruptions due to cross-strait tensions | -0.7% | National, especially import-dependent sectors | Short to Medium term (1–3 years) |

| Aging population reducing consumer base | -0.5% | National, more pronounced in rural areas | Medium to Long term (3–5 years) |

| Source: Mordor Intelligence | |||

Store-Saturation Cannibalization Risk

Taiwan's retail density approaches physical limits with convenience store count exceeding 13,706 outlets, creating one store per 1,703 people. This saturation triggers cannibalization effects where new store openings primarily redistribute existing demand rather than generating incremental sales growth. 7-Eleven's expansion beyond 7,000 stores in 2025 demonstrates continued network growth despite diminishing returns on individual locations. Market leaders respond by shifting focus from store count to same-store sales optimization through technology deployment, including smart vending machines and unmanned store formats that reduce labor costs while maintaining market presence. The challenge intensifies in urban cores where rental costs continue rising while foot traffic patterns shift toward suburban shopping centers and online channels.

Labour Shortages & Rising Wage Floor

Taiwan's retail sector confronts acute labor shortages, with 73% of employers reporting recruitment difficulties, particularly for customer-facing roles requiring language skills and cultural sensitivity. The semiconductor industry's expansion compounds this challenge by attracting workers with higher wages, creating upward pressure on retail compensation packages. Service sector wages have remained frozen for over 60% of workers across three years, reducing job satisfaction and increasing turnover rates. Retailers respond through automation investments, with FamilyMart implementing AI-powered inventory systems and 7-Eleven deploying unmanned store technologies to reduce labor dependency. However, customer service quality concerns limit full automation adoption, particularly for complex transactions and elderly customer segments who prefer human interaction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Health Focus Re-Shapes Spending

Food, beverage & tobacco remained the largest category, capturing 42.10% of Taiwan retail market share in 2025 as consumers favored ready-to-eat meals and premium coffee offerings. Electronic & Household Appliances are forecast to post an 8.05% CAGR through 2031, the swiftest pace among product lines. The rise of AI-enabled air purifiers and smart cooking gadgets underpins this trajectory, lifting the Taiwan retail market size for the segment well above historical averages. Personal Care & Household products benefit from the aging demographic, driving growth in adult diapers, low-allergen detergents, and vitamin supplements. Meanwhile, Apparel, Footwear & Accessories confront margin pressure from cross-border fast fashion yet still log mid-single-digit growth by leaning on domestic designers and sustainable fibers. Furniture, Toys & Hobby products gain from urban renovation trends as city dwellers maximize small-space living. Industrial & Automotive categories remain stable, their outlook tied to electric-vehicle accessory demand rather than gasoline-engine maintenance.

Over the next five years, retailers will cluster premium health SKUs adjacent to daily staples to entice impulse purchases and maximize basket value. Product localization accelerates as authorities push a 10% domestic ingredient mandate for silver-friendly foods, aiding local farmers and shortening supply chains. Omnichannel merchandising delivers click-and-collect flexibility, letting shoppers test home-electronics bundles in-store before finalizing digital payments. Private labels broaden into high-protein snacks and eco-detergents, keeping price-sensitive consumers loyal amid cost inflation. This category diversification fortifies resilience in the Taiwan retail market against isolated demand shocks such as tariff hikes or tourism slowdowns.

By Retail Channel: Seamless Journeys Trump Channel Silos

Modern trade accounted for 31.05% of the Taiwan retail market size in 2025, owing to its broad assortments and aggressive loyalty programs. Yet E-Commerce & Others will expand at 11.85% CAGR as frictionless returns, same-day grocery delivery, and livestream promotions woo urban millennials. Domestic giant Momo logged record revenue of TWD 112.56 billion (USD 3.51 billion) in 2024, leveraging proprietary logistics to guard NPS scores and fend off foreign sites. Traditional Mom-and-Pop shops decline in share but persist in rural districts where personal rapport beats speed. Cross-channel hybrid models emerge: PX Mart restricts payments to its own PX Pay, capturing transaction data and slashing interchange costs.

Omnichannel shoppers exhibit 30% higher annual spend, prompting retailers to integrate inventory views and reward points across apps, kiosks, and physical aisles. Cross-border marketplaces inject product novelty and price tension, but domestic players counter with tighter after-sales service and local warranty coverage. As 5G becomes commonplace, augmented-reality product demos and shoppable video further blur lines between browsing and buying. Competitive intensity, therefore, depends less on owning a specific channel and more on orchestrating shopper journeys across the Taiwan retail market.

By Format: Convenience Reigns, Specialty Accelerates

Convenience stores held a 29.00% slice of the Taiwan retail market in 2025, with their 24/7 hours, ready meals, and bill-payment kiosks woven into daily life. Specialty Stores are projected to grow fastest at 8.70% CAGR, fueled by beauty boutiques, pet-care shops, and nutrition clinics that deliver category expertise. Supermarkets maintain stable momentum by curating local produce and meal-kit subscriptions. Hypermarkets battle e-grocery incumbents by rolling out curbside pick-up bays and dynamic pricing screens. Department Stores downsize apparel floors while expanding experiential zones—book cafés, art exhibitions—that extend dwell time.

AI-driven shelf analytics allow convenience chains to cut out-of-stock instances by 20%, lifting same-store sales even in saturated districts. Specialty retailers deploy membership apps offering health diagnostics or personalized cosmetics mixing, deepening loyalty. Unmanned mini-stores and smart lockers appear in office lobbies, tapping micro-commerce demand during commute gaps. Collectively, these shifts reinforce the Taiwan retail market’s pivot toward data-guided microformats over raw square-meter expansion.

Competitive Landscape

The Taiwan retail market is led by a few dominant players, with the top five chains holding a significant share. PX Mart’s expansion through mergers has prompted President Chain Store to enhance its private label offerings and collaborate with Costco’s warehouse club format to maintain pricing competitiveness. Carrefour Taiwan is focusing on refining its gourmet food lines to stand out from deep-discount competitors. Increasingly, technology is replacing price as the key competitive edge. Coretronic’s autonomous robots, for instance, help major retailers cut warehouse picking time significantly.

Retail innovation is rapidly evolving, with 7-Eleven rolling out computer-vision kiosks across Taiwan, reducing checkout times to just 15 seconds and allowing staff to focus on more customer-focused tasks. Cross-border e-commerce platforms rely on algorithmic dynamic pricing, but domestic retailers are responding with integrated loyalty ecosystems. These systems offer added value through transit card top-ups, micro-insurance policies, and utility bill payments. This deepens customer engagement while building data-driven advantages. Meanwhile, regulatory bodies such as the Fair Trade Commission continue to play a strong role in shaping market dynamics.

Proactive regulation has made large-scale mergers more difficult, curbing moves that could lead to monopolistic control. As a result, Taiwan’s retail market remains competitive despite consolidation pressures. Looking ahead, new growth areas are emerging. These include elder-care focused retail, sustainable fashion aligned with circular economy principles, and low-carbon supply chains. These sectors remain relatively untapped by both established players and foreign competitors, offering fresh opportunities for innovation and investment.

Taiwan Retail Industry Leaders

PX Mart (incl. RT-Mart)

President Chain Store (7-Eleven, Carrefour stake)

Costco Taiwan

FamilyMart Taiwan

Momo.com

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: PX Mart finalized the rebrand of all RT-Mart sites under “MEGA PXMART,” integrating over 1,200 locations into a unified supply-chain platform.

- August 2025: President Lai launched “Long-Term Care 3.0,” allocating new subsidies that boost demand for smart health-care products within retail aisles.

- July 2025: Far Eastern Group opened a 5G-enabled logistics hub featuring automated pallet shuttles that serve Swire Coca-Cola and FamilyMart.

- June 2025: Costco Taiwan teamed with Uber Eats to launch nationwide delivery from 14 warehouses, extending Kirkland staples to online baskets.

Taiwan Retail Market Report Scope

Retail implies selling consumer goods or services to customers through various distribution channels to generate profit. This report delves into the Taiwanese retail industry, offering a comprehensive background analysis. It assesses emerging trends across segments, highlights significant shifts in market dynamics, and provides an overarching market overview.

The Taiwanese retail industry is segmented by product type and distribution channel. By product type, the industry is segmented into food, beverage, and tobacco products, personal care and household, apparel, footwear, and accessories, furniture, toys, and hobby, industrial and automotive, electronics and household appliances, and other product types. By distribution channel, the industry is segmented into hypermarkets, supermarkets, convenience stores, specialty stores, department stores, e-commerce, and other distribution channels. The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Product Type

| Food, Beverage, and Tobacco Products |

| Personal Care and Household Care |

| Apparel, Footwear, and Accessories |

| Furniture, Toys, and Hobby |

| Industrial and Automotive |

| Electronic and Household Appliances |

| Other Products |

By Retail Channel

| Traditional Mom and Pop Retail |

| Modern Trade Retail |

| E-Commerce and Others |

By Format

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (Drugstore, Cash and Carry, Wholesaler) |

| By Product Type | Food, Beverage, and Tobacco Products |

| Personal Care and Household Care | |

| Apparel, Footwear, and Accessories | |

| Furniture, Toys, and Hobby | |

| Industrial and Automotive | |

| Electronic and Household Appliances | |

| Other Products | |

| By Retail Channel | Traditional Mom and Pop Retail |

| Modern Trade Retail | |

| E-Commerce and Others | |

| By Format | Hypermarkets |

| Supermarkets | |

| Convenience Stores | |

| Department Stores | |

| Specialty Stores | |

| Others (Drugstore, Cash and Carry, Wholesaler) |

Key Questions Answered in the Report

How large is the Taiwan retail market in 2026 and what growth is expected by 2031?

The Taiwan retail market size reached USD 123.66 billion in 2026 and is projected to expand to USD 148.17 billion by 2031 at a 3.69% CAGR.

Which product category contributes the most revenue?

Food, Beverage & Tobacco represents 42.10% of sales, making it the largest contributor.

Which sales channel is growing fastest?

E-Commerce & Others is forecast to rise at a 11.85% CAGR through 2031 as livestream shopping and cross-border platforms gain traction.

What is driving specialty-store expansion?

Rising demand for curated beauty, pet-care, and health products is fueling an 8.70% CAGR in Specialty Stores.

How does consolidation affect suppliers?

Large chains like PX Mart employ consignment and data-driven fee structures that shift inventory risk and squeeze supplier margins.

What regulatory measures shape competition?

The Fair Trade Commission enforces stringent merger thresholds, illustrated by its 2024 block of Uber’s Foodpanda acquisition, to preserve market competition.

Page last updated on: